|

BUSINESS

& POLITICS IN THE WORLD GLOBAL

OPINION REPORT NO. 848-857 Week: May 20 – July 28,

2024 Presentation: August 02,

2024 Surveys Show Chinese Economy Growing But

At Modest Pace Japan Atomic Power Should Decommission

Tsuruga Reactor Kuwait’s Suspended Parliament: Where Does

The Public Stand? Iranians’ Attitudes Toward The 2024 Snap

Presidential Election Amid War In Gaza, 58% Of Israelis Say

Their Country Is Not Respected Internationally Israelis Are More Pessimistic Than

Optimistic About The Future Of Their Political System Amid Adaptations To Changes In Weather,

Ugandans Call For Collective Climate Action Seychellois Want More Government Action To

Curb The Country’s Drug Epidemic Emaswati Support Media’s Watchdog Role,

Insist On Media Freedom Emaswati Applaud Government’s Provision Of

Electricity, Though Reliability Issues Remain When Did Britons Make Up Their Minds How

They Would Vote At The 2024 General Election? Are Britons Looking Forward To The Paris

Olympics? Voters Split On Future Leader Of The

Conservative Party And Reasons For Election Defeat 7 In 10 Britons Believe Immigrants Place

Extra Pressure On The NHS Most Spaniards Think That AI Will Not

Replace Them At Work Slim Majority Of U.S. Adults Still Say

Changing Gender Is Morally Wrong In The UK, Dissatisfaction With Economy,

Democracy Is Widespread Ahead Of Election About 3 In 10 Americans Would Seriously

Consider Buying An Electric Vehicle Amid Doubts About Biden’s Mental

Sharpness, Trump Leads Presidential Race Joe Biden, Public Opinion And His

Withdrawal From The 2024 Race How Americans Get Local Political News Mortgage Stress Increased In June, But Set

To Ease In The Months Ahead After The Stage 3 Tax Cuts Varied Beliefs And Actions On Climate

Change In 39 Countries Global Attitudes To Refugees: A 52-Country

Survey From Ipsos And UNHCR Global Attitudes To Crime And Law

Enforcement, A Survey Across 31 Countries More People View The U.S. Positively Than

China Across 35 Surveyed Countries INTRODUCTORY NOTE 848-857-43-32/Commentary: Israelis Are

More Pessimistic Than Optimistic About The Future Of Their Political System

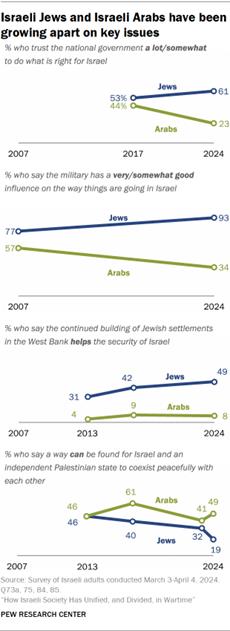

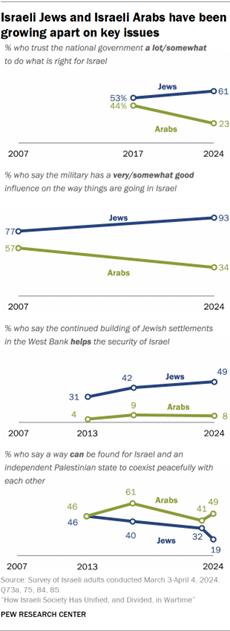

As the Israel-Hamas war

rages on, the shares of Israelis who see deep conflicts within their society have lessened

over the past year:

Research

in the West Bank and Gaza Pew Research Center has

polled the Palestinian territories in previous years, but in our 2024 survey,

we were unable to survey in Gaza or the West Bank due to security concerns.

We are actively investigating possible ways to conduct both qualitative and

quantitative research on public opinion in the region and will provide more

data as soon as we are able.

At the same time, Israeli public opinion has become more polarized in

other ways. For example, Arab Israelis and Jewish Israelis

have increasingly diverging views on key institutions – such as the military

– and on policy issues:

Views among those on the

ideological left and right have also diverged on some of these key issues

since we last asked about them. For example, 19% of those who place

themselves on the left trust the national government, compared with 75% of

those on the right – a difference of 56 percentage points. In 2017, the

difference was 43 points (26% on the left trusted the government, compared

with 69% of those on the right).

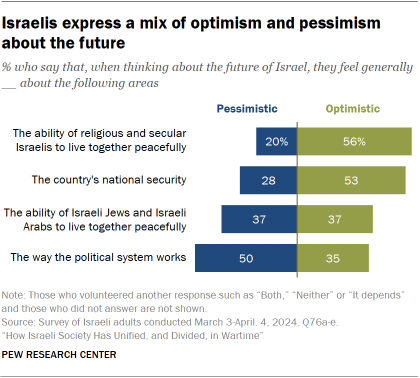

Against this

backdrop, Israelis are more

pessimistic (50%) than optimistic (35%) about the way their political system

works. And, whereas Arabs and Jews were about equally

pessimistic about the political system in 2019, Arabs have become more pessimistic (69%, up from 57%)

while Jews have become less so

(44%, down from 55%). Israelis

are also divided on the prospect of Arab and Jewish Israelis living together

peacefully, with equal shares saying they are

optimistic (37%) and pessimistic (37%) about this. About a quarter (23%) said

they are both, neither or that it depends. Still, Israelis are more

optimistic than pessimistic about the country’s national security and the

ability of religious and secular Israelis to live together peacefully. Related: Israeli

Views of the Israel-Hamas War These are among the key

findings of a survey of 1,001 Israelis, conducted via face-to-face interviews

from March 3 to April 4, 2024. Views

of political leaders

In March and early April,

attitudes toward Israel’s political leadership were largely negative. (The

survey took place before war cabinet member Benny Gantz resigned from the government and before Prime Minister Benjamin

Netanyahu disbanded the emergency war cabinet.) At

the time of the survey, just one of the seven officials we asked about –

Defense Minister Yoav Gallant –

received favorable ratings from a clear majority of Israelis. Jewish and Arab Israelis

had very different views of the six other Israeli politicians we asked about.

The largest gaps were in evaluations of Gallant (Jews were 65 percentage

points more favorable than Arabs); Mansour Abbas, the leader of the United

Arab List, which is better known in Israel as Ra’am (-56); and Netanyahu

(+44). Only Israeli opposition leader Yair Lapid was seen about equally favorably by

Jews and Arabs (37% vs. 41%). Ideological divides

between the right and left were also large – particularly when it came to

Netanyahu (those on the right were 61 points more favorable than those on the

left), Ben-Gvir (+54) and Smotrich (+54). (Read

more about views of Israeli leaders in Chapter

1, and

explore views of Palestinian leaders in our previous

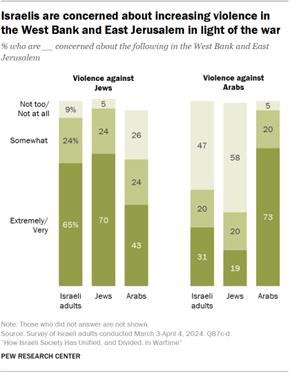

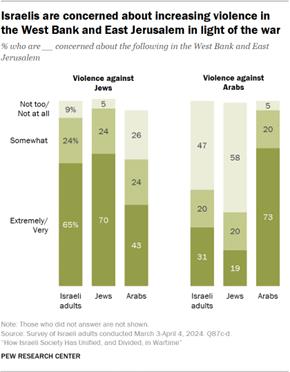

report.) Violence

in the West Bank and East Jerusalem

Around two-thirds of

Israelis say they are extremely or very concerned about violence against Jews

in the West Bank and East Jerusalem. Around a third are similarly concerned

about violence against Arabs. But concerns differ dramatically by ethnicity:

Israeli

Jews are almost evenly split on whether they are optimistic (40%) or

pessimistic (44%) about the political system – though they are significantly

more optimistic than Israeli Arabs (15%). About seven-in-ten Arabs (69%) say

they are pessimistic about the future of the political system in Israel. People

on the right are also more optimistic (47%) than those in the center (25%) or

on the left (21%). Relatedly, Israelis with positive views of Netanyahu and

his governing coalition also express more optimism about the political system

in general than do those with unfavorable views. There are also ideological

differences, with left-leaning Israelis expressing much more concern than

right-leaning Israelis about violence against Arabs and much less concern

about violence against Jews. (PEW) 20 July, 2024 SUMMARY OF POLLS ASIA (China) Surveys Show Chinese Economy

Growing But At Modest Pace The China Federation of

Logistics and Purchasing’s official purchasing managers index, or PMI,

remained at 49.5, the same as in May, on a scale up to 100 where 50

marks the cut off for expansion. A private-sector survey released Monday by

the financial media group Caixin was ?more optimistic, edging up to 51.8 from

51.7 in the previous month. That was the fastest expansion of factory output

in two years, it said. Analysts had forecast that it would fall. (Asahi Shimbun) 02 July, 2024 (Japan) Japan Atomic Power Should

Decommission Tsuruga Reactor The Nuclear Regulation

Authority has determined that the No. 2 reactor of the Tsuruga Nuclear

Power Plant in Fukui Prefecture does not meet its safety standards. The

decision will block efforts to restart the idled reactor. At a July 26 review

meeting, the nuclear safety watchdog concluded that the possibility of

an active fault running directly beneath the containment building that houses

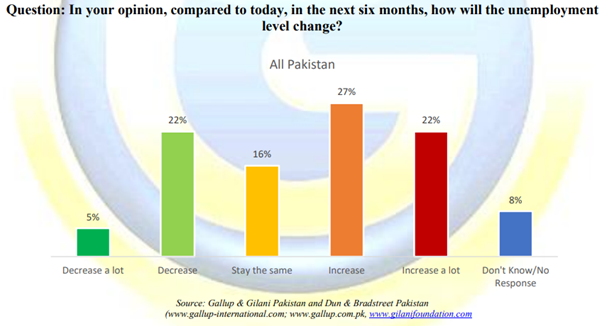

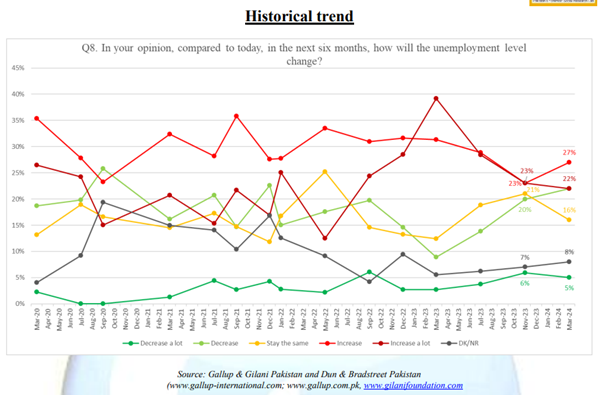

the Tsuruga No. 2 reactor cannot be ruled out. (Asahi Shimbun) 27 July, 2024 (Pakistan) Over A Quarter (27%) Of

Pakistanis Are Hopeful That Unemployment Will Decrease In The Next Six

Months, While Nearly Half (49%) Remain Pessimistic According to a survey

conducted by Gallup & Gilani Pakistan and Dun & Bradstreet Pakistan,

over a quarter (27%) of Pakistanis are hopeful that unemployment will

decrease in the next six months, while nearly half (49%) remain pessimistic.

To view the full Consumer Confidence Index for Q3 2023-24, click here. A

nationally representative sample of adult men and women from across the

country was asked the question, “In your opinion, compared to today, in the

next six months, how will the unemployment level change?” (Gallup Pakistan) 18 July, 2024 An Overwhelming Number Of

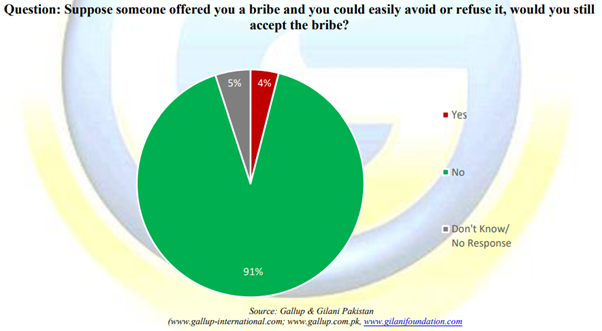

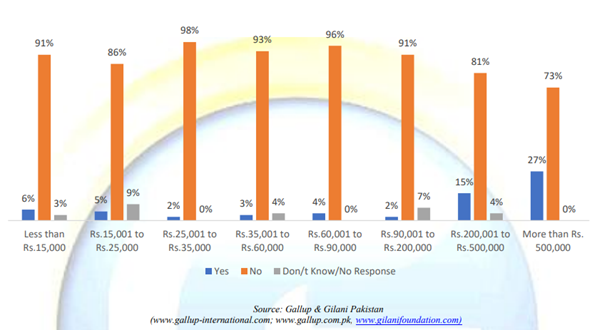

Pakistanis Would Not Accept A Bribe That They Could Easily Avoid Or Refuse

(91%) Compared To Those That Would Accept It (4%) According to a survey

conducted by Gallup & Gilani Pakistan, an overwhelming number of

Pakistanis would not accept a bribe that they could easily avoid or refuse

(91%) compared to those that would accept it (4%). There is a higher

prevalence to accept a bribe among relatively higher income groups, with 15%

of the ‘Rs. 200,001 to Rs. 500,000’ income group and 27% of the ‘More than Rs

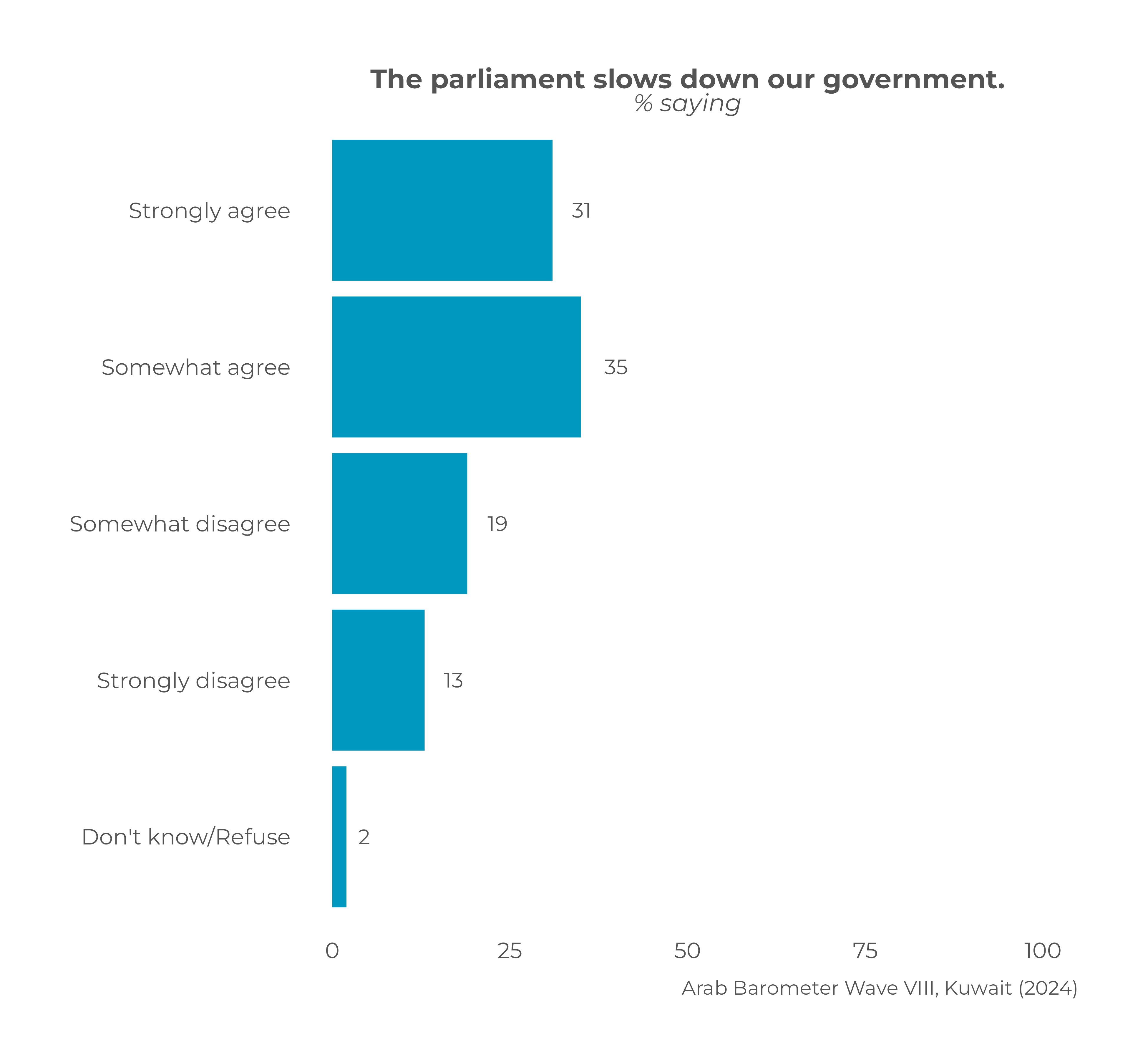

500,000’ income group claiming they would accept a bribe. (Gallup Pakistan) 23 July, 2024 MENA (Kuwait) Kuwait’s Suspended Parliament:

Where Does The Public Stand? In a televised address on May 10, Kuwait’s Emir, Sheikh

Mishal Al-Ahmad Al-Jaber Al-Sabah, firmly stated, “I will not let democracy

be exploited to destroy the state.” This address came as he dissolved the

National Assembly for the second time in three months and enacted temporary

suspensions of specific constitutional provisions for up to four years. We

asked a series of questions to probe Kuwaitis’ perspectives on the National

Assembly. Most notably, a striking 66 percent of Kuwaitis “strongly” or

“somewhat” agreed with the statement that the National Assembly slowed down the government. (Arabbarometer) 23 May, 2024 (Iran) Iranians’ Attitudes Toward The

2024 Snap Presidential Election Comparing the electoral

behavior of respondents in the previous elections (March 2024) with their

decision for the upcoming election shows that 85% of those who did not vote

in last year’s elections do not intend to participate in this year’s election

either. In contrast, 6% of those who did not vote in the previous elections

stated that they will vote in the presidential election. Also, 48% of

first-time voters (those who can vote for the first time in the presidential

election) do not intend to participate in the election, while about 34% of

them want to vote. 22 June, 2024 (Israel) Amid War In Gaza, 58% Of

Israelis Say Their Country Is Not Respected Internationally Even before a prosecutor

at the International Criminal Court called for the arrest of Israel’s prime

minister, Israelis were concerned about their

country’s global image. Nearly six-in-ten (58%) said in a poll this spring

that Israel is not respected around the world. A 58% majority of Israelis say

their country is not respected around the world, including 15% who say

it’s not at all respected.

A smaller share of Israelis (40%) say Israel is respected internationally,

including 9% who say it’s very respected. (PEW) 11 June, 2024 Israelis

Are More Pessimistic Than Optimistic About The Future Of Their Political

System Jewish Israelis trust the

national government to do what is right for Israel more than they did in 2017 (61%, up

from 53%). Arab Israelis trust it less (23%, down from 44%).93% of Jewish

Israelis think the military has a positive influence on the way things are

going in Israel, while just 34% of Arab Israelis agree. This gap has grown

significantly since we last asked the question in 2007, when 77% of Israeli

Jews and 57% of Israeli Arabs said the military’s influence was

positive. (Read more about confidence

in the government and institutions in Chapter

2.) (PEW) 20 July, 2024 AFRICA (Uganda) Amid Adaptations To Changes In

Weather, Ugandans Call For Collective Climate Action Africa is the continent

most vulnerable to climate change and its impacts, yet many African

countries remain unprepared to confront this threat (World Meteorological

Organization, 2023). Seven in 10 Ugandans (70%) say that crop failure has

become more severe in their area over the past 10 years, and 53% say the same

about droughts. o Increasingly severe droughts are reported most commonly in

the Northern region (71%), while large majorities in all regions except

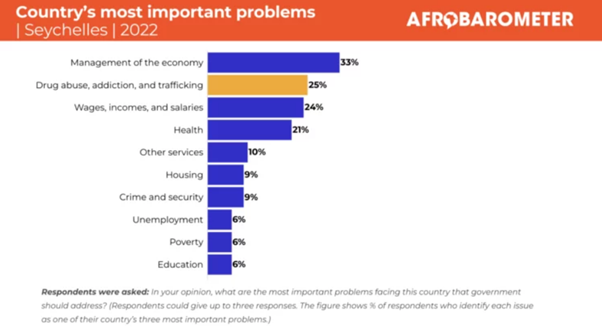

Kampala say crop failure has become more severe. (Afrobarometer) 27 June, 2024 (Seychellois) Seychellois Want More

Government Action To Curb The Country’s Drug Epidemic The World Drug Report 2022

from the United Nations Office of Drugs and Crime (2022) estimates that

about 284 million people worldwide used illicit drugs in 2020, a 26%

increase over the past decade. A majority (55%) of Seychellois say the

government is performing “fairly well” or “very well” in tackling drug abuse.

Nearly half (46%) of citizens oppose decriminalising the sale and consumption

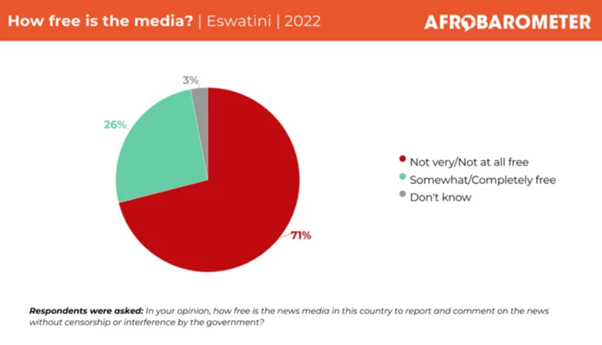

of marijuana or cannabis. (Afrobarometer) 05 July, 2024 (Emaswati) Emaswati Support Media’s

Watchdog Role, Insist On Media Freedom In February 2024,

Eswatini’s newly appointed prime minister, Russell Dlamini, sparked

concern about the future of press freedom in the country by announcing

plans to establish a state controlled media regulator as part of the Media

Commission Bill. Two-thirds (67%) of Emaswati say the media should

“constantly investigate and report on government mistakes and

corruption.”More than seven in 10 citizens (72%) say the media should be free

from government interference, while 26% think the government should have the

right to prevent the publication of things it disapproves of. (Afrobarometer) 22 July, 2024 Emaswati

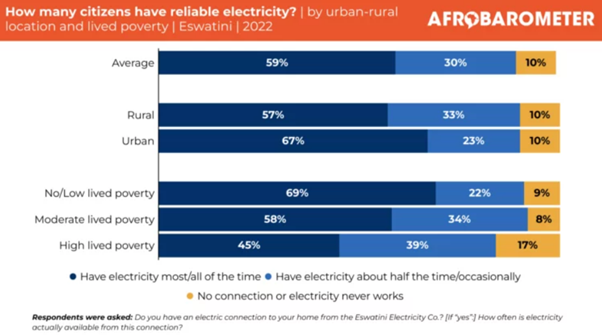

Applaud Government’s Provision Of Electricity, Though Reliability Issues

Remain With an overall

electrification rate of 85% (UNDP Eswatini, 2024), Eswatini boasts one of

the highest rates of electricity access in sub-Saharan Africa. More

than nine in 10 citizens (92%) live in households that are connected to the

national power grid. Of those who are connected to the grid, about two-thirds

(65%) say their electricity works “most” or “all” of the time. o Combining

connection and reliability rates shows that about six in 10 (59%) of all

Emaswati enjoy a reliable supply of electricity, though these figures are

lower among rural residents (57%) and citizens experiencing high levels of

lived poverty (45%). (Afrobarometer) 26 July, 2024 WEST EUROPE (UK) When Did Britons Make Up Their

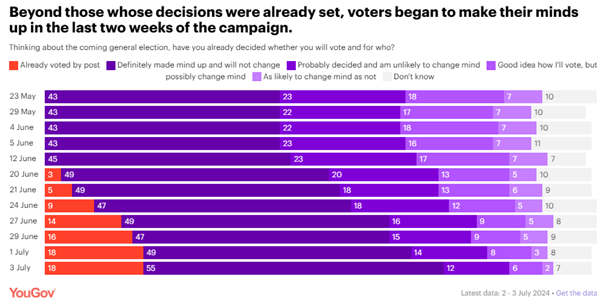

Minds How They Would Vote At The 2024 General Election? Back in May, when this

year’s election was called, there was room for this again. YouGov tracker

data compiled over the course of the election campaign shows that only 43% of

Britons had, at that point, definitely made up their mind and weren’t going

to change how (or whether) they voted. A further 23% said they were unlikely

to change their mind over the next six weeks, leaving a crucial 35% of

Britons unsure of their polling day behaviour or open to changing their

minds. (YouGov UK) 19 July, 2024 Are Britons Looking Forward To

The Paris Olympics? This Friday, billions of

eyes around the world will settle upon Paris and the opening ceremony of the

2024 Olympic games, sparking a fortnight of sport that will generate drama,

create new household names and maybe bring home a few gold medals. This time,

just over four in ten (42%) Britons say they are interested in the Paris

games, with one in eight (13%) being very interested. So while we can expect

Brits to be more absorbed in the Paris games than their immediate

predecessors, it does seem that the Olympics no longer resonate as widely as

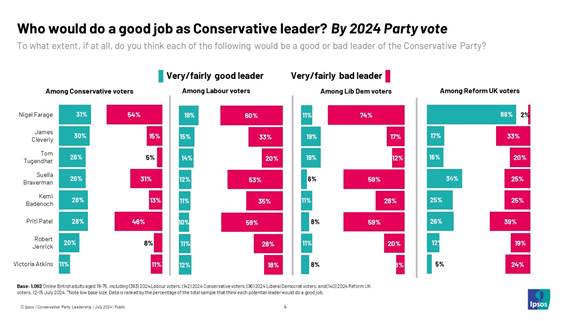

they did a decade ago. (YouGov UK) 23 July, 2024 Voters Split On Future Leader

Of The Conservative Party And Reasons For Election Defeat New Ipsos polling, taken

July 12-15 2024, asked the British public who they think would do a good or

bad job as Conservative Party leader and what the key reasons were for their

recent General Election defeat. When asked if different hypothetical candidates

would make good or bad leaders of the Conservative Party, Nigel Farage is the

most likely to be seen as someone that would do a good job (28%). However,

almost half of the public think he would do a bad job (48%). For the public

as a whole, many of the hypothetical candidates are not well known. In fact,

only three candidates have half or more Britons offering an opinion one way

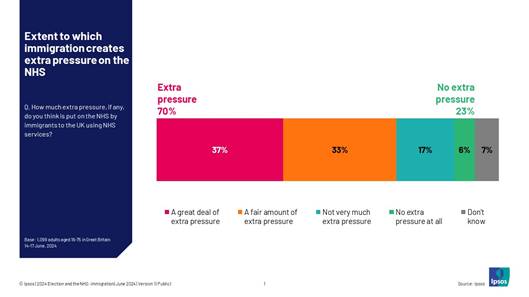

or another. (Ipsos MORI) 24 July, 2024 7 In 10 Britons Believe

Immigrants Place Extra Pressure On The NHS New polling from Ipsos has

found that 7 in 10 (70%) of the British public believe immigrants to the UK

put additional pressure on the NHS. This includes almost two in five (37%)

who say they place a great deal of extra pressure on the NHS, and a third (33%)

who say they place a fair amount of extra pressure. Over three in ten (32%)

say migrants use NHS services more than the UK population. A similar

proportion (30%) say migrants use NHS services the same amount, and one in

five (20%) think migrants use NHS services less than people born in the UK.

Fairly high proportions (18%) don’t know. (Ipsos MORI) 01 July, 2024 (Spain) Most Spaniards Think That AI

Will Not Replace Them At Work Ipsos, one of the world's

leading market research firms, has just published its annual study "AI

Monitor", which analyses the public's knowledge of AI, as well as the

trust and expectations it generates. 65% of people say they know what AI is, but

only 46% say they know which products and services use it, compared to 34%

who say they do not know, a figure that has not changed since 2023. However,

half (50%) agree that these services and products have more advantages than

disadvantages. (Ipsos Spain) 06 June, 2024 NORTH AMERICA (USA) Slim Majority Of U.S. Adults

Still Say Changing Gender Is Morally Wrong Majorities of political

liberals (81%), Democrats (72%), those who do not identify with a religion

(67%), those who do not attend religious services regularly (59%), young

adults aged 18 to 29 (56%) and college graduates (53%) believe changing

genders is morally acceptable. Less than half of their counterparts say the

same.While slightly less than half of women believe in the moral

acceptability of changing genders, they are significantly more likely than

men to think as much (48% vs. 39%, respectively). (Gallup) 07 June, 2024 Is

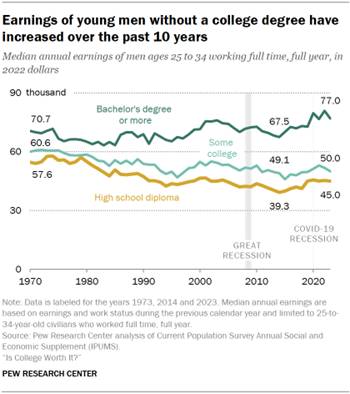

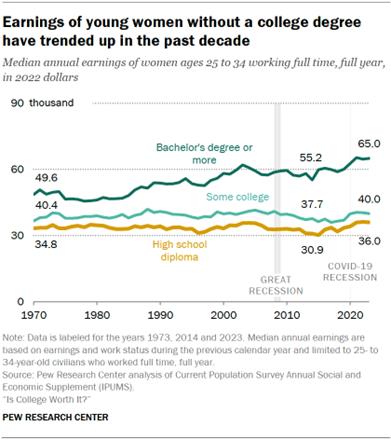

College Worth It? After decades of falling

wages, young U.S. workers (ages 25 to 34) without a bachelor’s degree have

seen their earnings increase over the past 10 years. Their overall wealth has

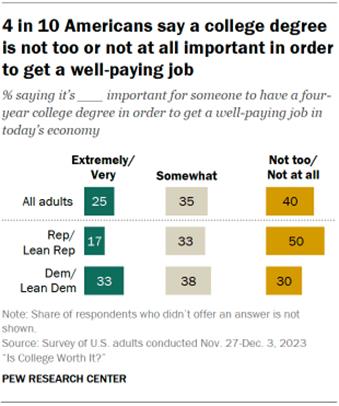

gone up too, and fewer are living in poverty today. Only one-in-four U.S. adults say it’s extremely or very important to

have a four-year college degree in order to get a well-paying job in today’s

economy. About a third (35%) say a college degree is somewhat

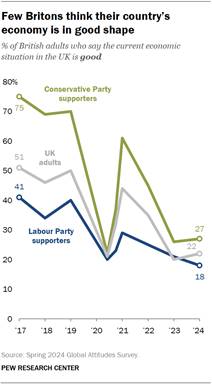

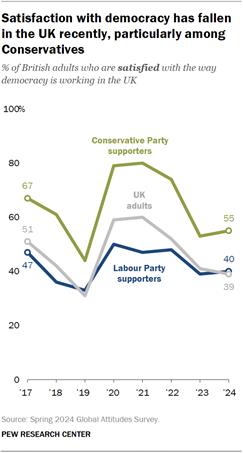

important, while 40% say it’s not too or not at all important. (PEW) 23 May, 2024 In The UK, Dissatisfaction With

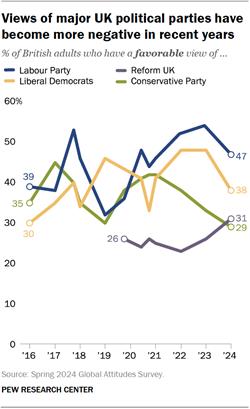

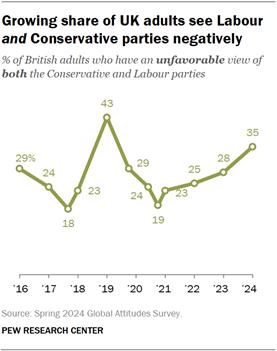

Economy, Democracy Is Widespread Ahead Of Election None of the four major

British political parties we asked about in our survey – the Labour Party,

the Liberal Democrats, the Conservative Party and Reform UK – receive net

positive ratings from the British public. The Labour Party is seen most

favorably at 47%, though this is down somewhat from 54% favorable last year.

The Liberal Democrats get positive ratings from around four-in-ten Britons

(38%). Again, this is down from 48% last year. (PEW) 20 June, 2024 About 3 In 10 Americans Would

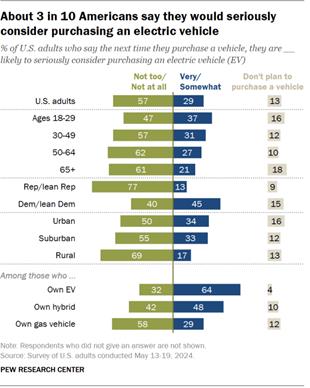

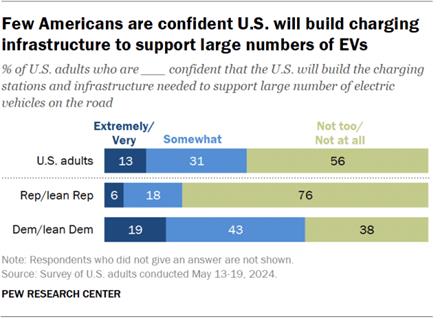

Seriously Consider Buying An Electric Vehicle One area where Americans

rate EVs more favorably than gas vehicles is their environmental benefits.

Nearly half (47%) say EVs are better for the environment than gas vehicles.

Smaller shares say they are about the same (31%) or are worse for the

environment (20%). However, the share of Americans who say electric vehicles

are better for the environment than gas vehicles has decreased 20 points

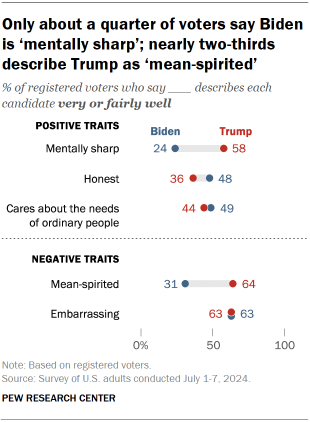

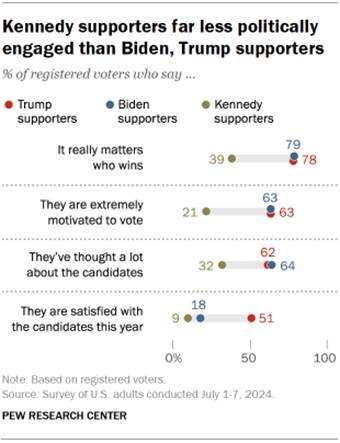

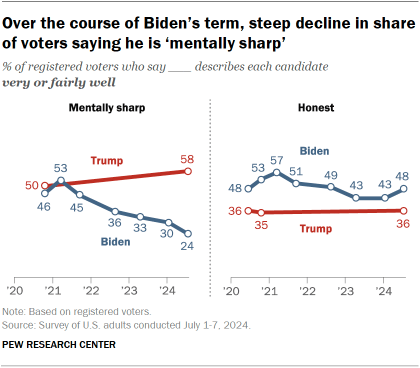

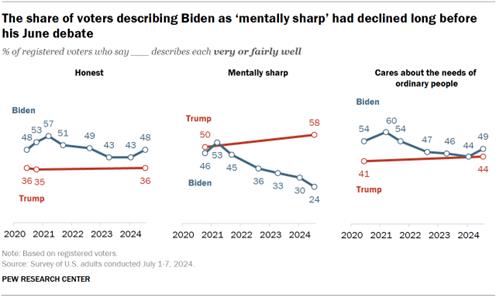

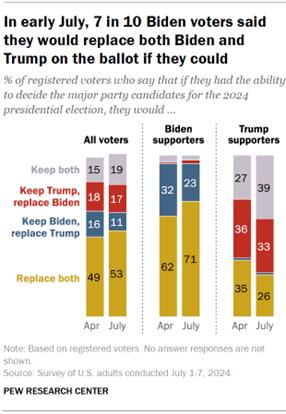

since 2021, from 67%. (PEW) 27 June, 2024 Amid Doubts About Biden’s

Mental Sharpness, Trump Leads Presidential Race The share of voters

describing Biden as mentally sharp has declined 6 points since January and is

considerably lower than it was in 2020. The new survey by Pew Research

Center, conducted July 1-7 among 9,424 adults, including 7,729 registered

voters, finds that both Biden and Trump are widely viewed as flawed, though

in different ways. And nearly seven-in-ten voters (68%) say they are not

satisfied with their choices for president.

Most voters describe Trump as “mean-spirited.” Trump trails

Biden on honesty and, by a narrower margin, on empathy. And about twice as

many voters describe Trump as mean-spirited (64%) as say that about Biden

(31%). (PEW) 11 July, 2024 Joe

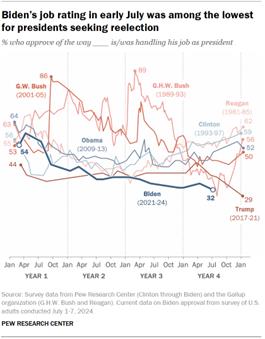

Biden, Public Opinion And His Withdrawal From The 2024 Race Only about a quarter of Americans (26%) – including fewer than half of

Democrats and Democratic-leaning independents – said the administration had

done an excellent or good job of handling the situation. Biden’s overall job approval declined 11 points,

from 55% to 44%, between July and September 2021. It has never been in

positive territory since then. It fell another 9 points, to 24%,

following his performance in the June 27 debate. (PEW) 23 July, 2024 How

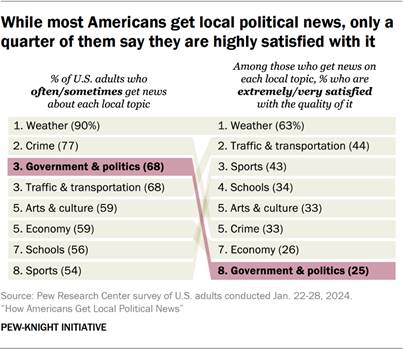

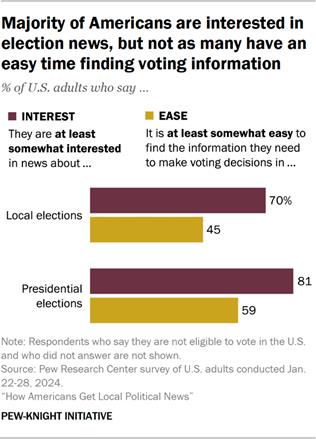

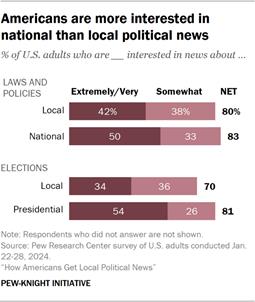

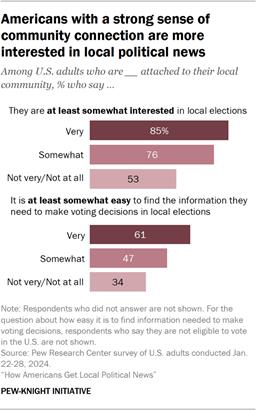

Americans Get Local Political News U.S. adults get news about

local government and politics from a variety of different sources. The most

common are friends, family and neighbors (70%) and local news outlets (66%).

Just over half (54%) also say they often or sometimes get news about local

politics from social media. Smaller shares say they at least sometimes get

local political news from local government websites (32%), local nonprofits

or advocacy groups (31%), or local politicians (30%). (PEW) 24 July, 2024 AUSTRALIA Mortgage Stress Increased In June, But Set To

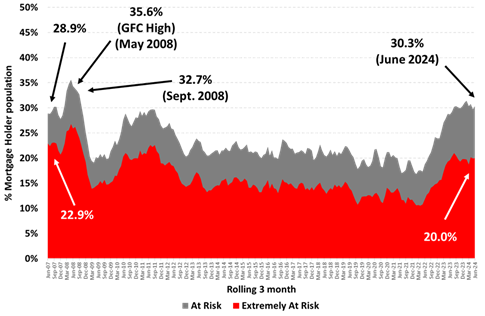

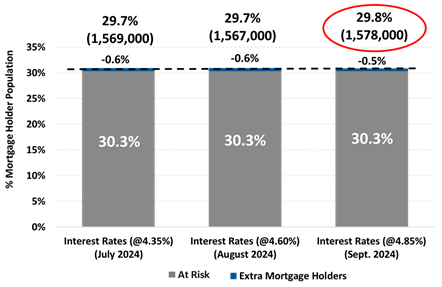

Ease In The Months Ahead After The Stage 3 Tax Cuts The level of mortgage

holders ‘At Risk’ of ‘mortgage stress’ in June (30.3% of mortgage holders) is

set to fall further over the next few months after the Stage 3 tax cuts were

introduced for Australian income earners from the first week of July. In percentage

terms the record high of 35.6% of mortgage holders in mortgage stress was

reached in mid-2008. However, with population growth and increased numbers of

mortgages in the 14 years since the Global Financial Crisis (GFC), there are

now more Australian ‘At Risk’ of mortgage stress. (Roy Morgan) 22 July, 2024 Net Trust In Australian Charities Is On The Rise

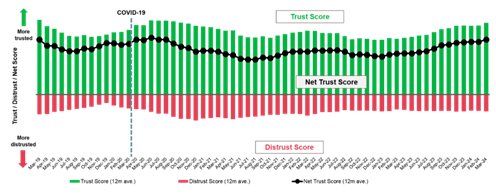

Over The Last Few Years After Hitting A Low In Mid-2021 The Net Trust Score of the

Charities sector reached a record high just after the onset of the pandemic,

then declined steadily to mid-2021, before recovering from early 2022. The

net trust score as of March 2024 has increased by over 50% is nearly back to

its peak reached in June 2020 in the early days of the pandemic. The

Salvation Army and RSPCA have both dropped one ranking to come in at second

and third place respectively. Perhaps unremarkably, there are no Charities on

our list with more distrust than trust. (Roy Morgan) 23 July, 2024 ANZ-Roy Morgan Consumer Confidence Jumps 5.9pts

To 84.4 After Stage 3 Tax Cuts Hit The Bulk Of Consumer’s Pockets; Highest

Consumer Confidence Since January 2024 Now over a fifth of

Australians, 22% (up 2ppts), say their families are ‘better off’ financially

than this time last year compared to 49% (down 4ppts) that say their families

are ‘worse off’. Views on personal finances over the next year returned to

positive territory this week, with a third of Australians, 33% (up 3ppts)

expecting their family to be ‘better off’ financially this time next year

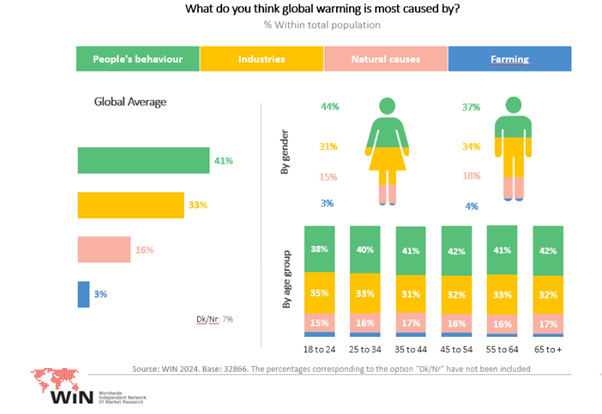

while only 32% (down 3ppts) are expecting to be ‘worse off’. (Roy Morgan) 23 July, 2024 MULTICOUNTRY STUDIES Varied Beliefs And Actions On Climate Change In

39 Countries 41% of the global survey

respondents believed that human behaviour was responsible for global warming,

with women (44%) more likely than men (37%) to hold this belief. Beliefs

surrounding global warming are consistent across all age groups however

globally those in MENA countries are far more likely to believe industries

are behind climate change at 45%, whereas only 26% of people in APAC blame

industries, identifying people’s behaviours as the main cause (49%). (WIN) 07 June, 2024 Source:

https://winmr.com/varied-beliefs-and-actions-on-climate-change/ Global Attitudes To Refugees: A 52-Country

Survey From Ipsos And UNHCR There

is significant support or ‘openness’ among the public to finding solutions

that enable refugees to access their rights. While

attitudes varied, half of those surveyed believe in refugees being able to

integrate and, for example, access their full right to education, and nearly

as many support their full access to healthcare and jobs (44% and 42%,

respectively). Around three-quarters (77%) expressed support, to a varying

degree, for policies that allow refugee families to be reunited in the

country of asylum. (Ipsos Global) 18 June, 2024 Global Attitudes To Crime And Law Enforcement, A

Survey Across 31 Countries Crime

is a key concern, but the economy is front and centre. Creating

jobs and boosting the economy remains the top priority for people (50% on

average across the 31 countries), surpassing protecting local citizens’

health and environment (27%) and stopping or reducing crime (24%). Poverty

and unemployment (53%) is seen as the most significant cause of crime and

violence, followed by drug and alcohol abuse (43%). Ineffective law

enforcement is cited as a cause by 37% of global respondents, on

average. (Ipsos Global) 25 June, 2024 Source:

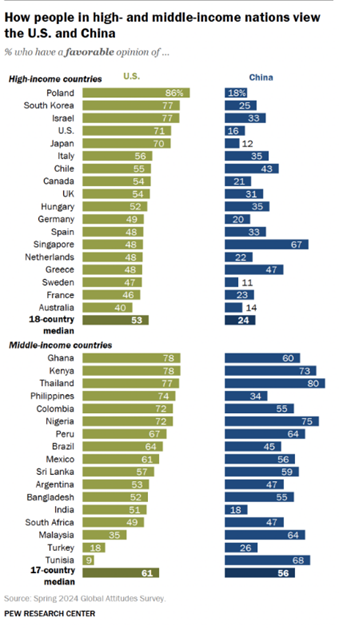

https://www.ipsos.com/en/global-attitudes-crime-and-law-enforcement More People View The U.S. Positively Than China

Across 35 Surveyed Countries A median of 53% in 18

high-income countries have a favorable view of the U.S. A median of 61% in 17

middle-income countries also see the U.S. favorably. Favorability ratings of

the U.S. range from a high of 86% in Poland to a low of 9% in Tunisia. And 71%

of Americans themselves have a positive view of their country. In the

high-income countries surveyed, a median of just 24% have a favorable view of

China. Far more in middle-income nations (a median of 56%) see China

positively. (PEW) 09 July, 2024 ASIA

848-857-43-01/Polls Surveys Show Chinese Economy Growing But At Modest Pace

Surveys

of Chinese factory managers showed a mixed outlook for the world’s

second-largest economy in June, with growth steady but not picking up much

steam. The China Federation of

Logistics and Purchasing’s official purchasing managers index, or PMI,

remained at 49.5, the same as in May, on a scale up to 100 where 50

marks the cut off for expansion. “From the perspective of

output, China’s economy is maintaining expansion, but the momentum of

recovery still needs to be consolidated,” the official Xinhua News Agency

cited Zhao Qinghe, senior statistician for the National Bureau of Statistics,

as saying. The PMI for new export

orders slipped to 49.4 from 49.6, perhaps reflecting announcements by

the European Union and United States of plans to increase

their tariffs on imports of electric vehicles from China. A private-sector survey

released Monday by the financial media group Caixin was more optimistic,

edging up to 51.8 from 51.7 in the previous month. That was the fastest

expansion of factory output in two years, it said. Analysts had forecast that

it would fall. But while sentiment was

positive, the level of confidence among purchasing managers fell to the

lowest in over four-and-a-half years due to worries over intense competition

and uncertain market conditions, Caixin said. The surveys offered scant

insight into whether various measures to boost the property sector, such as

cutting mortgage interest rates and down payments, have had much impact on an

industrywide slump that followed a crackdown on excessive borrowing by developers. “The PMIs for June were

mixed but on balance suggest that the recovery lost some momentum last

month,” Capital Economics said in a report. The official PMI reading

for high-tech manufacturing rose to 52.3 in June from 50.7 in May, reflecting

the government’s drive to boost investment in upgrading factories and

equipment in new industries such as computer chip and electric vehicles. “This shows that the

transformation and upgrading of China’s manufacturing industry has continued

to advance,” Zhao was quoted as saying. Chinese leader Xi Jinping

has made growth of such advanced industries a top priority, a theme likely to

dominate an upcoming meeting of top officials of the ruling Communist Party

when they meet later in the month. Xinhua said in a separate

report that during the meeting the party would disclose a new round of “deep

and comprehensive reforms.” Such measures will “chart

the course forward for the world’s second largest economy,” it said. (Asahi Shimbun) 02 July, 2024 Source:

https://www.asahi.com/ajw/articles/15328747

848-857-43-02/Polls Japan Atomic Power Should Decommission Tsuruga Reactor

The Nuclear Regulation

Authority has determined that the No. 2 reactor of the Tsuruga Nuclear

Power Plant in Fukui Prefecture does not meet its safety standards. The

decision will block efforts to restart the idled reactor. Operator Japan Atomic

Power Co. should make a decision to decommission the reactor given the grim

fact it has been unable to meet the safety requirements to bring the unit

back online in spite of the huge amount of time it has spent on the effort, while

many other reactors have met the regulatory requirements. At a July 26 review

meeting, the nuclear safety watchdog concluded that the possibility of

an active fault running directly beneath the containment building that houses

the Tsuruga No. 2 reactor cannot be ruled out. The stricter nuclear

safety standards established after the catastrophic accident at the Fukushima

No. 1 nuclear plant in 2011 categorically state that critical facilities such

as nuclear reactors must not be located directly above an active fault, which

is a fracture or a zone of fractures in the Earth’s crust where the movement

of rocks can cause earthquakes. If ground surface displacement occurs around

such vital facilities, it can cause significant damage, leading to a severe

accident. The NRA is expected to

reject Japan Atomic Power’s application to restart the reactor, following the

compilation of the review document. Since the NRA’s

establishment, 27 reactors have applied for permission to restart, and 17

have been recognized as meeting the new safety standards. If the application

to reactivate the Tsuruga No. 2 unit is rejected, it will mark the first such

action by the regulatory body. A major nuclear accident

would cause irreversible damage. Based on this lesson, regulatory decisions

on the safety of reactors should err on the side of greater safety when in

doubt. The risk from an active

fault directly below a critical nuclear facility is extremely high, and if

its presence under the reactor cannot be denied, there is a compelling case

for not allowing the operation of the reactor. However, the NRA cannot

force the decommissioning of nuclear reactors that do not meet the new safety

standards. Japan Atomic Power plans to seek further reviews from the NRA

after additional plant surveys to secure permission to restart the reactor. Yet, nine years have

already passed since the application to restart the Tsuruga No. 2 unit was

submitted. The prolonged review process is due to the operator’s mishandling

of the procedure. There were more than 1,000

errors in the application documents. Tampering with geological data was

also discovered. These were serious issues

that shook the foundation of the safety assessment, leading to the NRA’s

decision to suspend the process. Given the backlog of other

nuclear plant reviews and the time the NRA has already devoted to this

application, Japan Atomic Power must surely realize it is being unreasonable

in pursuing the undertaking. In the first place, the

location of the Tsuruga nuclear plant is not suitable for a nuclear facility.

Japan Atomic Power acknowledges that an active fault, known as “Urasoko

Danso,” runs through the site. Located on a peninsula,

evacuation routes would be limited in the event of an earthquake causing a

serious accident. We just witnessed how the Jan. 1 Noto Peninsula earthquake

flattened many buildings and cut off roads at many locations, reaffirming the

difficulty of sheltering indoors or evacuating when a major earthquake hits a

peninsula. Japan Atomic Power is a

company that sells electricity generated from nuclear power to major electric

utilities that are its shareholders. But since the earthquake

and tsunami disaster in 2011, it has been decided that two of the company’s

four reactors need to be decommissioned. As the other two are not in

operation, the company is forced to operate only on the “basic fees” paid by

the electric power companies. This cost is passed on to

the public through higher electric bills. The major electric power companies

have a responsibility to consider the future of Japan Atomic Power, including

whether to continue or discontinue its operations. (Asahi Shimbun) 27 July, 2024 Source:

https://www.asahi.com/ajw/articles/15364629

848-857-43-03/Polls Over A Quarter (27%) Of Pakistanis Are Hopeful That

Unemployment Will Decrease In The Next Six Months, While Nearly Half (49%)

Remain Pessimistic

According to a survey

conducted by Gallup & Gilani Pakistan and Dun & Bradstreet Pakistan,

over a quarter (27%) of Pakistanis are hopeful that unemployment will

decrease in the next six months, while nearly half (49%) remain pessimistic.

To view the full Consumer Confidence Index for Q3 2023-24, click here. A

nationally representative sample of adult men and women from across the

country was asked the question, “In your opinion, compared to today, in the

next six months, how will the unemployment level change?” In response, 5%

said ‘decrease a lot’, 22% said ‘decrease’, 16% said ‘stay the same’, 27%

said ‘increase’, 22% said ‘increase a lot’, and 8% said that they did not

know or gave no response.

(Gallup Pakistan) 18 July, 2024 Source:

https://gallup.com.pk/wp/wp-content/uploads/2024/07/18.07.24.Daily-poll-English.pdf

848-857-43-04/Polls An Overwhelming Number Of Pakistanis Would Not Accept A

Bribe That They Could

Easily Avoid Or Refuse (91%) Compared To Those That Would Accept It (4%)

According to a survey

conducted by Gallup & Gilani Pakistan, an overwhelming number of

Pakistanis would not accept a bribe that they could easily avoid or refuse

(91%) compared to those that would accept it (4%). A nationally

representative sample of adult men and women from across the country was

asked the question, “Suppose someone offered you a bribe and you could easily

avoid or refuse it, would you still accept the bribe?” In response, 91% said

‘No’, 4% said ‘Yes’, and 5% said that they did not know or gave no response.

Across income: There is a

higher prevalence to accept a bribe among relatively higher income groups,

with 15% of the ‘Rs. 200,001 to Rs. 500,000’ income group and 27% of the

‘More than Rs 500,000’ income group claiming they would accept a bribe.

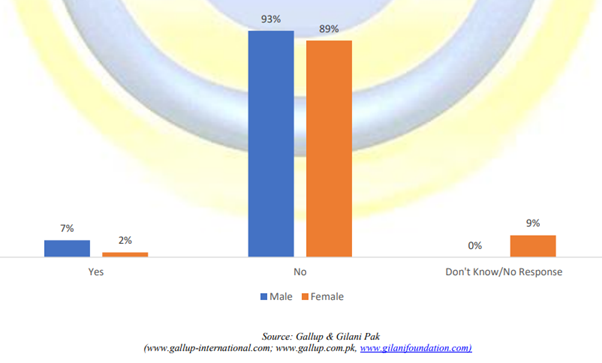

Across gender: Pakistani

men were more likely to accept a bribe (7%), compared to Pakistani women

(2%), but more Pakistani women did not have a response (9%).

(Gallup Pakistan) 23 July, 2024 Source: https://gallup.com.pk/wp/wp-content/uploads/2024/07/23.07.24.Daily-poll-English.pdf MENA

848-857-43-05/Polls Kuwait’s Suspended Parliament: Where Does The Public Stand?

In a televised address on May 10, Kuwait’s Emir, Sheikh

Mishal Al-Ahmad Al-Jaber Al-Sabah, firmly stated, “I will not let democracy

be exploited to destroy the state.” This address came as he dissolved the

National Assembly for the second time in three months and enacted temporary

suspensions of specific constitutional provisions for up to four years.

Subsequently, the Emir sanctioned the formation of a new cabinet and articulated his determination

to pursue reforms. This stance not only underscores his

willingness to push through controversial policies but also signals a

strategic pivot aimed at reducing the nation’s dependence on oil revenues. The suspension of the

parliament has elicited surprise among some Kuwaitis and Kuwait observers.

After all, Kuwait has long been hailed as a bastion of democracy within a region characterized by a

trend toward authoritarianism following the Arab uprisings. In stark contrast to its Gulf Cooperation

Council (GCC) counterparts, Kuwait boasts a parliament endowed with legislative

powers, capable of engaging in the formulation,

deliberation, and enactment of laws. It can also interpellate cabinet

ministers and cast votes of no confidence, which often led to ministerial

resignations. Just a month prior, on April 4, the nation had held snap elections to elect a new parliament. Kuwaitis

take great pride in their democratic traditions, including political openness

and freedom of expression. Nowhere else in the GCC do citizens enjoy

comparable rights. Some observers, however,

might have seen the decision to suspend parliament as a culmination of

longstanding tensions and disagreements within Kuwait’s political system.

Persistent gridlocks between the elected members of the parliament and the

government have gripped the nation for years, including over economic

reforms. Notably, since 2006, the National Assembly has been dissolved ten times and nullified three

times by the Constitutional Court,

emblematic of the ongoing challenges besetting the nation. In “Will Kuwait’s Next Parliament Be Its

Last?”, a Journal of Democracy Online Exclusive

from March 2024, Sean Yom rightly predicted the suspension of the parliament.

Scrutinizing the historical context of Kuwait’s democratic journey, marked by

recurrent legislative crises and political upheavals, he raised valid

concerns about the sustainability of its parliamentary democracy. Yom also

predicted that if the Emir were to suspend parliament, Kuwait might face

considerable opposition. Nevertheless, street protests have not materialized

thus far, and Kuwaitis have largely exhibited a subdued response on social

media platforms regarding the parliamentary suspension. Where might the public

stand? Our latest survey, conducted in collaboration with Tarek Masoud of

Harvard University and the Arab Barometer, offers valuable insights.

Administered prior to Ramadan this year, the survey unveils a nuanced

picture: while respondents convey disillusionment with the parliament, they

simultaneously underscore the significance of electoral processes. Our data includes 1210

face-to-face interviews conducted between February 14 and March 18. The

survey employed probability sampling techniques to ensure representation of

Kuwaiti nationals aged 18 and above. It included a wide range of questions

aimed at gauging the attitudes of ordinary Kuwaitis on political, economic,

and social matters. It is worth noting that Kuwait stands as the sole GCC

country where such comprehensive, nationally representative public opinion

surveys are readily accessible, underscoring the importance of this research

endeavor. Kuwaiti

sentiments toward the parliament’s performance are characterized by

discontent. We asked a series of

questions to probe Kuwaitis’ perspectives on the National Assembly. Most

notably, a striking 66 percent of Kuwaitis “strongly” or “somewhat” agreed

with the statement that the National Assembly slowed down the government. This prevailing sentiment

of disapproval remains consistent across demographic segments, regardless of

age, income level, or educational attainment, suggesting widespread

disillusionment with the parliament’s performance.

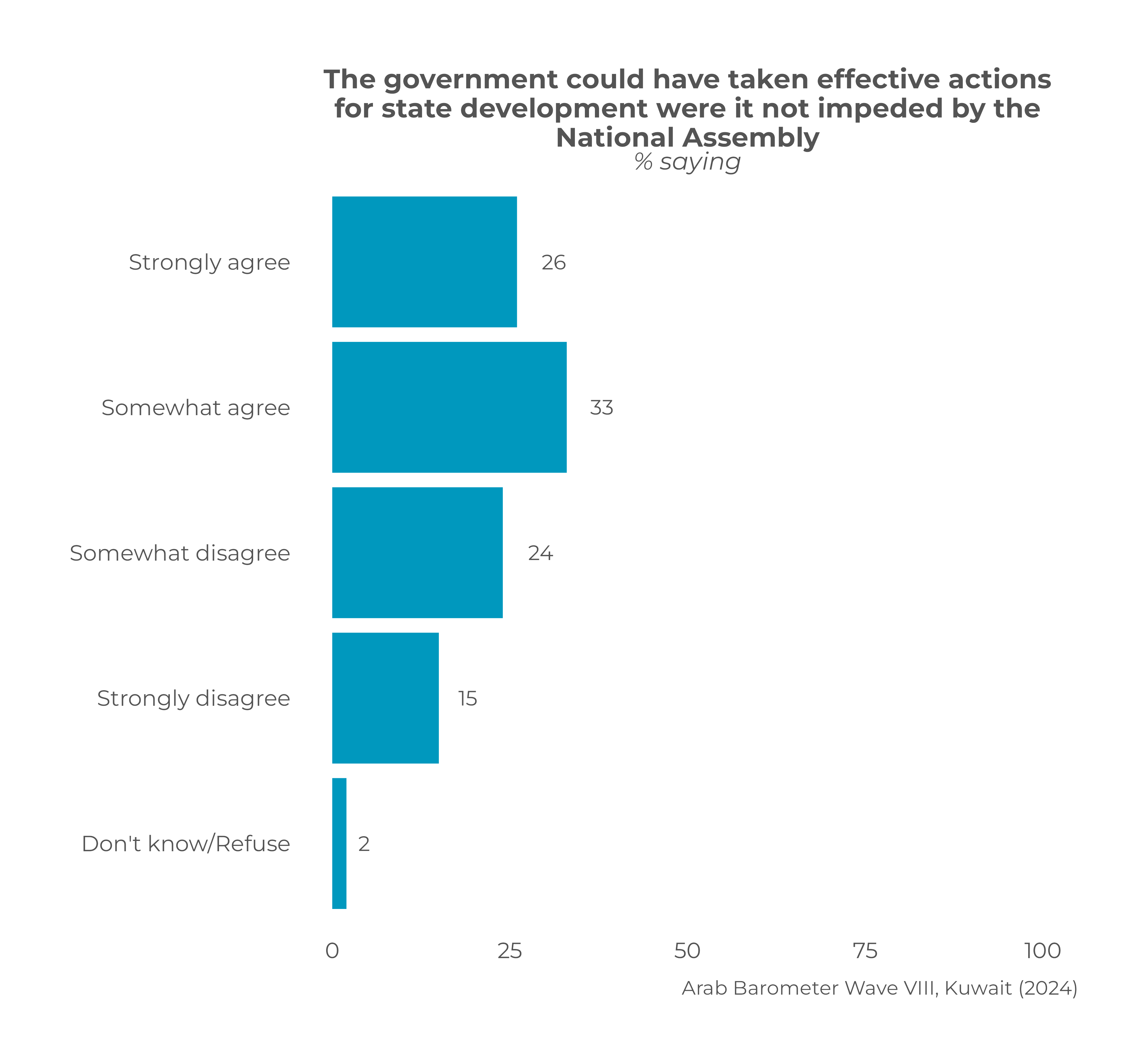

Similarly, 60 percent

agreed that “the government could carry out effective actions to advance the

state if it were not held back by

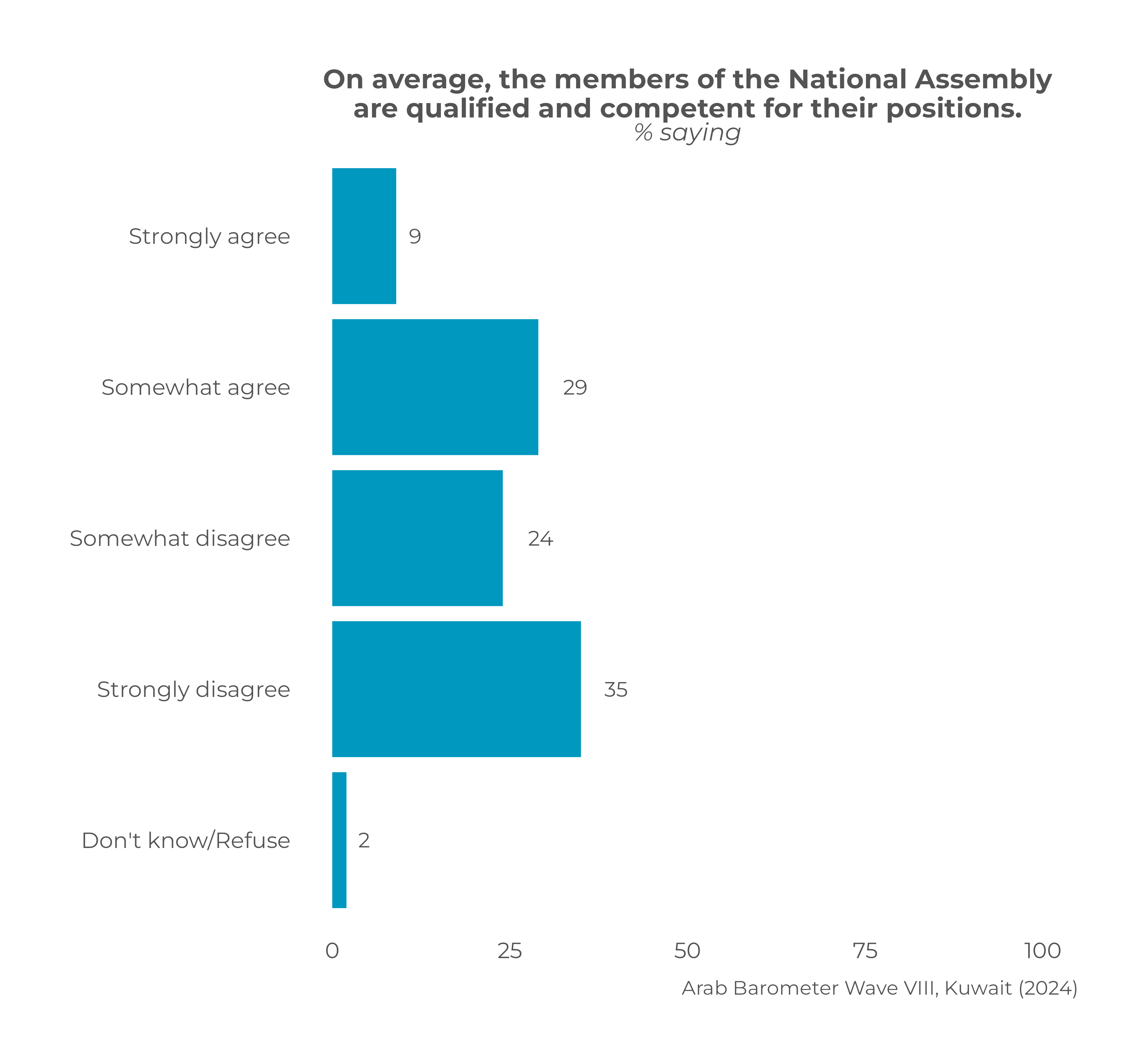

the parliament.” Furthermore, a mere 39 percent agreed that members of the

parliament were qualified and competent for their positions, in contrast to

the 50 percent who held a similar view regarding government ministers. These

were our original questions, not included in previous waves of the Arab

Barometer. A distinctive advantage of

collaborating with the Arab Barometer lies in our ability to conduct

longitudinal analyses, enabling comparisons of responses over time. For

instance, when respondents were prompted to either agree or disagree with the

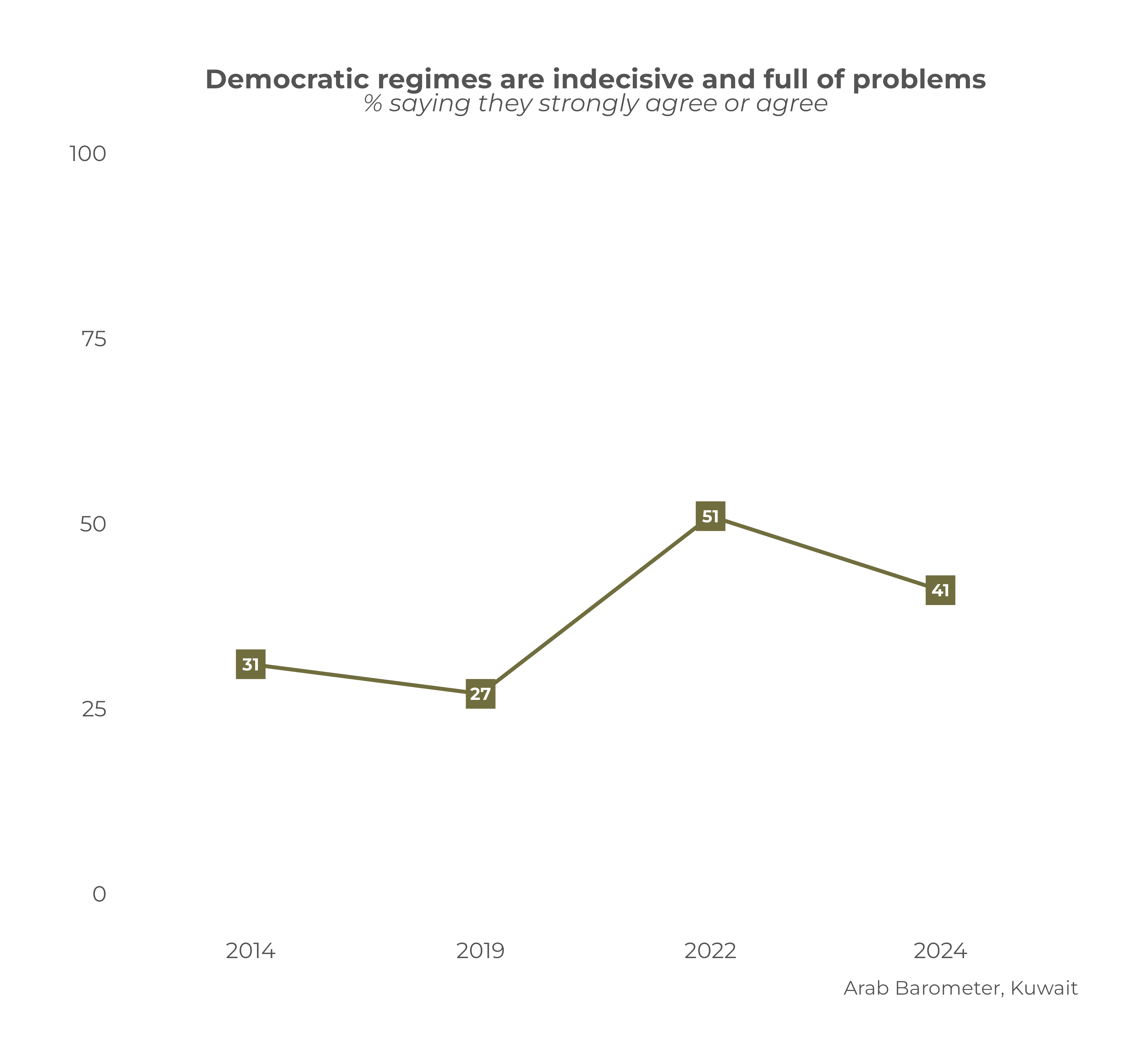

statement, “democratic regimes are indecisive and full of problems,” 41

percent agreed or strongly agreed. This marks a notable increase from the 27

percent who had agreed with the statement when the same question was asked in

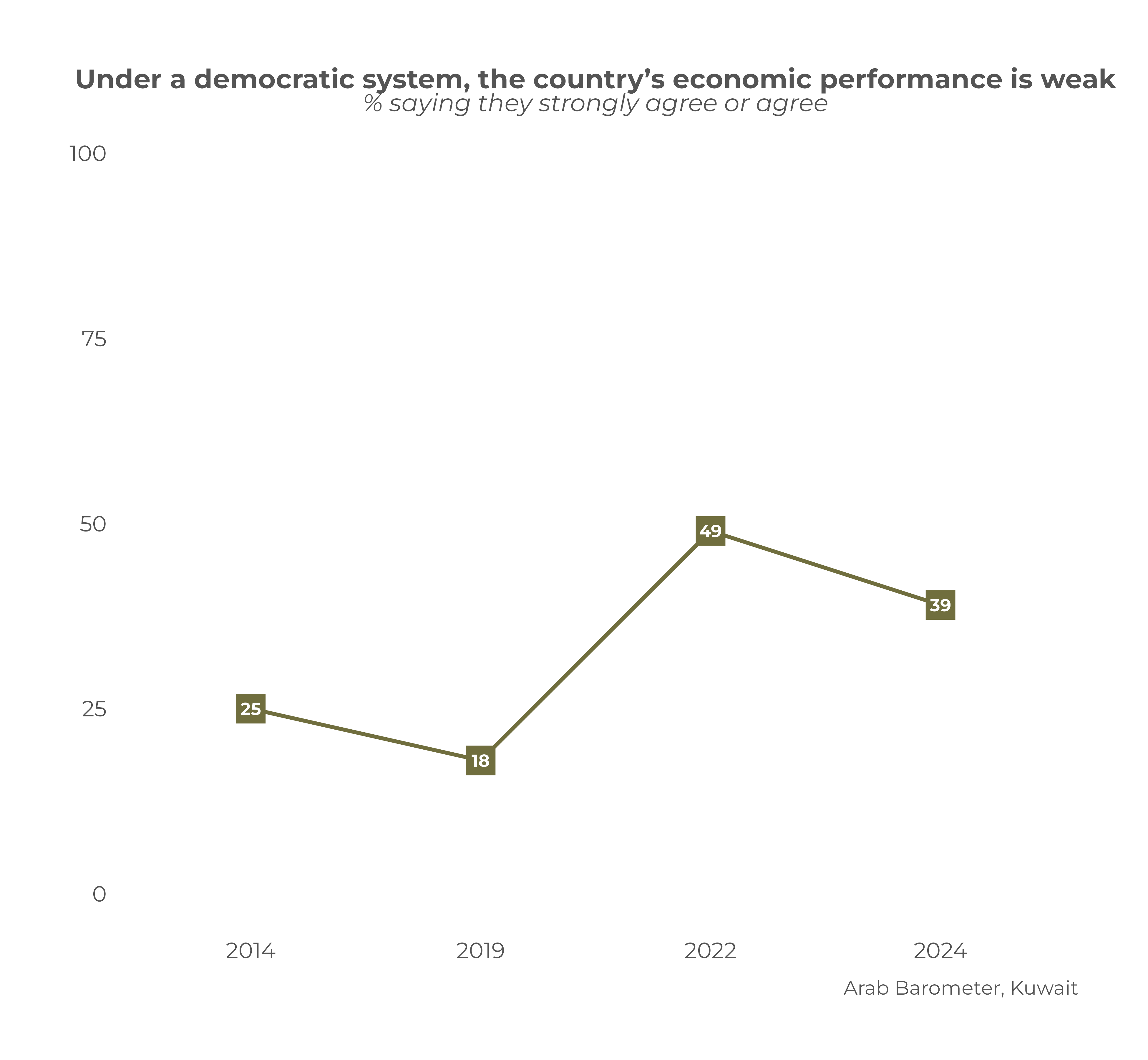

the Arab Barometer’s 2018 survey. Similarly, in response to the statement

that “under a democratic system, the country’s economic performance is weak,”

39 percent agreed in the recent survey. Interestingly, a significantly lower

proportion, only 18 percent, expressed agreement with the statement in 2018.[1]

The

results do not mean that Kuwaitis are ready to part with their democratic

principles. Our findings thus far

indicate that Kuwaitis acknowledge the imperfections within the country’s

democratic framework. What implications might these results carry for the

future of democracy in Kuwait? Will Kuwaiti society acquiesce to

authoritarian alternatives? While Kuwaitis undeniably harbor frustration over

recent parliamentary impasses, they also express a resolute endorsement of

Kuwait’s democratic heritage. In particular, 66 percent of Kuwaitis agreed

that “the parliament provides important oversight of the government.”

Moreover, an overwhelming majority perceive the “ability to freely choose

political leaders in elections” to be a very essential

pillar of democracy or human dignity.[2] Similarly, a remarkable 85 percent

agreed with the statement that “democratic systems may have problems, yet

they are better than other systems.”[3] Historically, during periods of

National Assembly suspension by Kuwaiti rulers (1976-1981; 1986-1991), the

populace consistently managed to reinstate it, a testament, perhaps, to their

enduring tradition of consensus-building that predates the constitution. Furthermore, when asked

about the culpability for Kuwait’s recent “political instability, resulting

in the formation of five governments in one year and three parliamentary

elections in three years,” 69 percent attributed responsibility to both the government and the

parliament. Subsequently, when evaluating potential measures to rectify the

situation in Kuwait, 64 percent identified that “Emiri intervention to stop

the implementation of government decisions” would help to a great extent,

while 57 percent also answered that “new parliamentary elections based on a

new election law” would help greatly. Kuwaitis understand that the complex

interplay between the elected assembly and the cabinet of ministers likely

shaped the country’s recent political tumult. They recognize that both

entities bear a shared responsibility for the myriad challenges and

disruptions that have characterized Kuwait’s recent political landscape. In the absence of

parliamentary scrutiny, the government could potentially implement

long-awaited economic reforms and other initiatives. However, the

accountability for governmental performance now rests squarely on the

shoulders of the executive branch. This elevated responsibility increases the

pressure on the government to demonstrate effective leadership, address

societal concerns, and tackle pressing challenges. Consequently, the

government must navigate this period of political transition with diligence

and transparency, aiming to rebuild public trust and steer the nation toward

progress. Yuree

Noh is Assistant Professor of Political Science at Rhode Island College and

Research Fellow at the Middle East Initiative at Harvard. Beginning in Fall

2024, she will be Assistant Professor of Political Science at the University

of Utah. Her research focuses on electoral institutions, gender &

politics, and public opinion in the Middle East and North Africa. (Arabbarometer) 23 May, 2024 Source:

https://arabbarometer.org/2024/05/kuwaits-suspended-parliament-where-does-the-public-stand/

848-857-43-06/Polls Iranians’ Attitudes Toward The 2024 Snap Presidential

Election

Survey

Summary According to the survey,

with about 10 days remaining until the presidential elections, approximately

22% of the target population stated that they will definitely vote in the

election, while about 65% stated that they will not vote; about 12% are still

undecided. (Gamaan) 22 June, 2024 Source:

https://gamaan.org/2024/06/22/election1403-english/

848-857-43-07/Polls Amid War In Gaza, 58% Of Israelis Say Their Country Is Not

Respected Internationally

Even before a prosecutor

at the International Criminal Court called for the arrest of Israel’s prime

minister, Israelis were concerned about their

country’s global image. Nearly six-in-ten (58%) said in a poll this spring

that Israel is not respected around the world. Most Israelis also feel

that antisemitism and Islamophobia are common and that both kinds of

prejudice are on the rise globally, according to the survey of 1,001 Israeli

adults conducted from March 3 to April 4, 2024. Here’s a closer look at the

survey’s findings: A

majority of Israelis do not think their country is respected internationally

A 58% majority of Israelis

say their country is not respected around the world, including 15% who say

it’s not at all respected. A smaller share of

Israelis (40%) say Israel is respected internationally, including 9% who say

it’s very respected. Israelis who place

themselves on the ideological left are especially likely to say that their

country is not respected internationally. Two-thirds of Israelis on the left

hold this view, including around a quarter (27%) who say Israel is not at all respected abroad. Views on this question

also differ depending on how Israelis perceive their country’s war against

Hamas. Israelis who believe the country’s military response against Hamas has

gone too far are especially likely to believe that Israel is not respected

around the world. By comparison, Israelis who think their country’s military

response has been about right are more likely to say that Israel is respected

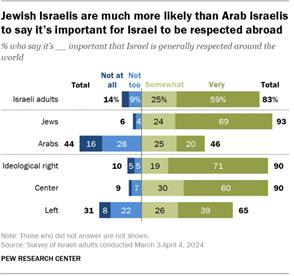

abroad. Most

Israelis want their

country to be respected abroad

Although only 40% of

Israelis think their country is respected internationally, the vast majority

(83%) think it’s very or somewhat important for the country to have this kind

of global respect. That includes 59% who say it is very important. Jewish Israelis are much

more likely than Arab Israelis to place importance on international respect

for Israel (93% vs. 46%). Indeed, among Jews, nearly seven-in-ten say this

is very important. Israelis on the

ideological right (90%) and in the center (90%) are more likely than those on

the left (65%) to feel it’s important for Israel to be respected abroad. Israelis

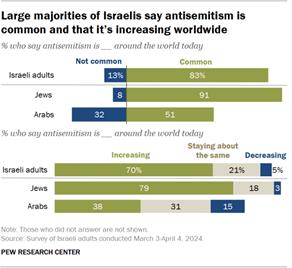

see rising antisemitism around the world

Most Israelis (83%) think

antisemitism is common around the world, with nearly half (49%) saying

it’s very common

today. Jewish Israelis are more

likely than Arab Israelis (91% vs. 51%) to say antisemitism is common

globally. So are Israeli adults on the ideological right (91%) and in the

center (83%) when compared with those on the left (72%). A majority of Israelis

(70%) also think antisemitism is increasing around the world today. An

additional 21% say it’s staying about the same, while just 5% think it’s

decreasing. Israeli Jews are more

likely than Israeli Arabs to perceive an increase in antisemitism (79% vs.

38%). But among Arabs, younger people – those under 50 – are more likely than

older ones to think antisemitism is on the rise globally (42% vs. 28%). Israelis

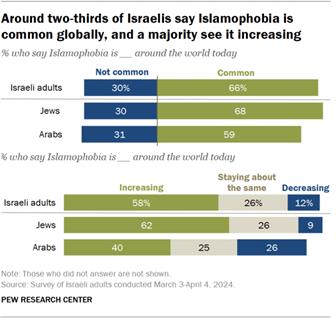

also see growing Islamophobia around the world

Two-thirds of Israelis

think Islamophobia is common around the world today, with around a third

(34%) saying it’s very common. Israeli Jews are less

likely to say Islamophobia is common than to say the same about antisemitism

(68% vs. 91%). But they are still more likely than Israeli Arabs (59%) to see

Islamophobia as common (and more likely to offer an opinion on the question). A majority of Israelis

(58%) also think Islamophobia is increasing around the world. Another 26% say

it’s staying about the same, while 12% say it is decreasing. Israeli Jews are more

likely than Israeli Arabs to say Islamophobia increasing around the world

(62% vs. 40%), while Arabs are more likely than Jews to say it’s decreasing

(26% vs. 9%). The two groups are about equally likely to say it’s staying the

same. (PEW) 11 June, 2024

848-857-43-08/Polls Israelis Are More Pessimistic Than Optimistic About The

Future Of Their Political System

As the Israel-Hamas war

rages on, the shares of Israelis who see deep conflicts within their society have lessened

over the past year:

Research

in the West Bank and Gaza Pew Research Center has

polled the Palestinian territories in previous years, but in our 2024 survey,

we were unable to survey in Gaza or the West Bank due to security concerns.

We are actively investigating possible ways to conduct both qualitative and quantitative

research on public opinion in the region and will provide more data as soon

as we are able.

At the same time, Israeli public opinion has become more polarized in

other ways. For example, Arab Israelis and Jewish Israelis

have increasingly diverging views on key institutions – such as the military

– and on policy issues:

Views among those on the

ideological left and right have also diverged on some of these key issues

since we last asked about them. For example, 19% of those who place

themselves on the left trust the national government, compared with 75% of

those on the right – a difference of 56 percentage points. In 2017, the

difference was 43 points (26% on the left trusted the government, compared

with 69% of those on the right).

Against this

backdrop, Israelis are more

pessimistic (50%) than optimistic (35%) about the way their political system

works. And, whereas Arabs and Jews were about equally

pessimistic about the political system in 2019, Arabs have become more pessimistic (69%, up from 57%)

while Jews have become less so

(44%, down from 55%). Israelis

are also divided on the prospect of Arab and Jewish Israelis living together

peacefully, with equal shares saying they are

optimistic (37%) and pessimistic (37%) about this. About a quarter (23%) said

they are both, neither or that it depends. Still, Israelis are more

optimistic than pessimistic about the country’s national security and the

ability of religious and secular Israelis to live together peacefully. Related: Israeli

Views of the Israel-Hamas War These are among the key

findings of a survey of 1,001 Israelis, conducted via face-to-face interviews

from March 3 to April 4, 2024. Views

of political leaders

In March and early April,

attitudes toward Israel’s political leadership were largely negative. (The

survey took place before war cabinet member Benny Gantz resigned from the government and before Prime Minister Benjamin

Netanyahu disbanded the emergency war cabinet.) At

the time of the survey, just one of the seven officials we asked about –

Defense Minister Yoav Gallant –

received favorable ratings from a clear majority of Israelis. Jewish and Arab Israelis

had very different views of the six other Israeli politicians we asked about.

The largest gaps were in evaluations of Gallant (Jews were 65 percentage

points more favorable than Arabs); Mansour Abbas, the leader of the United

Arab List, which is better known in Israel as Ra’am (-56); and Netanyahu

(+44). Only Israeli opposition leader Yair Lapid was seen about equally favorably by

Jews and Arabs (37% vs. 41%). Ideological divides

between the right and left were also large – particularly when it came to

Netanyahu (those on the right were 61 points more favorable than those on the

left), Ben-Gvir (+54) and Smotrich (+54). (Read

more about views of Israeli leaders in Chapter

1, and

explore views of Palestinian leaders in our previous

report.) Violence

in the West Bank and East Jerusalem

Around two-thirds of

Israelis say they are extremely or very concerned about violence against Jews

in the West Bank and East Jerusalem. Around a third are similarly concerned

about violence against Arabs. But concerns differ dramatically by ethnicity:

Israeli

Jews are almost evenly split on whether they are optimistic (40%) or

pessimistic (44%) about the political system – though they are significantly

more optimistic than Israeli Arabs (15%). About seven-in-ten Arabs (69%) say

they are pessimistic about the future of the political system in Israel. People

on the right are also more optimistic (47%) than those in the center (25%) or

on the left (21%). Relatedly, Israelis with positive views of Netanyahu and

his governing coalition also express more optimism about the political system

in general than do those with unfavorable views. There are also ideological

differences, with left-leaning Israelis expressing much more concern than

right-leaning Israelis about violence against Arabs and much less concern

about violence against Jews. (PEW) 20 July, 2024 AFRICA

848-857-43-09/Polls Amid Adaptations To Changes In Weather, Ugandans Call For

Collective Climate Action

Africa is the continent

most vulnerable to climate change and its impacts, yet many African

countries remain unprepared to confront this threat (World Meteorological

Organization, 2023). According to the Notre Dame Global Adaptation Initiative

(2023) country index, Uganda ranks high (14th) in vulnerability and low

(163rd) in readiness to act against climate change. Given that agriculture

accounts for about one-fourth of Uganda’s gross domestic product and

employs more than 70% of its labour force, rising temperatures and changing

rainfall patterns pose threats to livelihoods and food security (World

Bank Group, 2021; Ministry of Foreign Affairs of the Netherlands,

2018). Citizens are also grappling with the consequences of global

warming and more frequent extreme weather events, including both droughts

and destructive floods (World Bank Group, 2021; Andrew, 2021). The glaciers of the

Rwenzori Mountains, a major source of fresh water for Ugandans, are

melting at an accelerated rate, triggering floods and landslides (Baluku,

2023). Flooding is eroding copper waste pools from old mining

operations, washing toxic waste into Uganda’s water supply and

soil (Mukpo, 2024). The government and

stakeholders have worked to mainstream climate action in the country’s

National Climate Change Policy (Republic of Uganda, 2015) and Green Growth

Development Strategy (National Planning Authority, 2017), prioritising

strategies to protect the economy and the livelihoods of the

population. In June 2023, the government launched a $2.9 million

initiative to develop a National Adaptation Plan to address the growing

impacts of climate change (United Nations Environment Programme, 2023). A special question module

in Afrobarometer’s Round 10 survey (2024) explores Ugandans’

experiences, awareness, and attitudes related to climate change. Findings

show that a majority of citizens report worsening drought and crop

failure in their region. Among the two thirds of Ugandans who are familiar

with climate change, large majorities blame it on human activity, say

it is making life worse, and call for urgent action by their government

and developed countries. In significant numbers,

Ugandans report taking steps to adapt to changing weather patterns,

including changes related to crops and foods, livestock, and water use. And

majorities express support for government investment in

weather-resilient infrastructure, funding for wind and solar energy, a

ban on tree cutting for fuel, and other policies in response to changes

in climate. Key findings

(Afrobarometer) 27 June, 2024

848-857-43-10/Polls Seychellois Want More Government Action To Curb The

Country’s Drug Epidemic

The World Drug Report 2022

from the United Nations Office of Drugs and Crime (2022) estimates that

about 284 million people worldwide used illicit drugs in 2020, a 26%

increase over the past decade. In addition to endangering the physical

and mental health of the user, the adverse effects of drug abuse ripple

across societies and generations, including its links to violence and

other forms of crime. In Seychelles, a surge in

heroin use has more than quadrupled the estimated number of users, from

1,200 in 2011 to 5,000-6,000 in 2019 – meaning that nearly 10% of the

country’s working-age population is dependent on the drug (Saigal, 2019).

This would give Seychelles the highest national per-capita heroin-use

rate in the world. Cannabis is also widely consumed, while the use of

other drugs, such as crack cocaine and methamphetamines, is steadily rising

(Bird, Stanyard, Moonien, & Randrianarisoa, 2021). Seychelles’ Division for

Substance Abuse Prevention, Treatment and Rehabilitation (DSAPTR)

endeavours to curb drug abuse through a variety of programmes. Its methadone

treatment programme, based on an approach to drug policy that views drug

addiction as a chronic disease, has received local criticism for its

distribution of needles, which seeks to avert the spread of HIV and

hepatitis C through the sharing of needles (Rodrigo, 2022). Meanwhile, reports of

police harassment of drug users has raised concern within civil society

that Seychelles will move toward a “zero tolerance” approach under which drug

users are penalised rather than assisted (Bird et al., 2021). In its first-ever survey

in Seychelles, Afrobarometer included a special module of questions to

explore citizens’ views related to drugs. Seychellois say that drug abuse,

addiction, and trafficking should be the government’s second-highest priority,

trailing only management of the economy. A majority of citizens think

the government is doing a decent job of tackling drug abuse, but views

are divided on whether ordinary Seychellois can play a role in fighting

drug abuse. Only about one-third of

respondents favour legalising the sale and consumption of marijuana.

Asked what they consider the most effective strategy to curb drug

abuse, Seychellois most often cite intensifying efforts to reduce

trafficking and enforcing severe penalties for users. Key findings

(Afrobarometer) 05 July, 2024

848-857-43-11/Polls Emaswati Support Media’s Watchdog Role, Insist On Media

Freedom

In February 2024, Eswatini’s

newly appointed prime minister, Russell Dlamini, sparked concern about

the future of press freedom in the country by announcing plans to establish a

state controlled media regulator as part of the Media Commission Bill, which

has long been on the books but inactive (Harber, 2024). Although Section 24 of

Eswatini’s Constitution guarantees freedom of expression, including

freedom of the media, the country’s media environment is heavily restricted

by laws such as the Suppression of Terrorism Act (2008), which critics argue

is used to protect the monarchy from criticism (Collaboration on

International ICT Policy for East and Southern Africa, 2022). A range of colonial-era

statutes also severely limit media freedom in Eswatini, and critics say

they are weaponised to punish the media for investigative reporting (African

Media Barometer, 2018; Konrad-Adenauer-Stiftung, 2021). These include

the Cinematography Act (1920), the Obscene Publications Act (1927), the

Sedition and Subversive Activities Act (1938), the Magistrates Courts

Act (1939), the Books and Newspapers Act (1963), the Protected Places

and Areas Act (1966), and the Proscribed Publications Act (1968). In 2022, the Eswatini

government declared the online publication Swaziland News and its

editor, Zweli Martin Dlamini, “terrorist entities” under the Suppression of

Terrorism Act (Media Institute of Southern Africa, 2022). Dlamini has

been in exile in South Africa since 2020 after police raided his home

and held him for six hours (Committee to Protect Journalists, 2020;

Reporters Without Borders, 2021). A court application to have Dlamini

extradited to Eswatini to face charges of terrorism is expected to be

heard by South Africa’s High Court next month (Maromo, 2024; Dlamini,

2024). Since the 2023 enactment

of the long-dormant Eswatini Broadcasting Act, which looks to break the

state broadcaster’s stronghold on media affairs and encourage media

pluralism (Hlatshwayo, 2020; Kingdom of Eswatini, 2023), Eswatini has

risen sharply in the World Press Freedom Index rankings, from

131st in 2022 to 85th out of 180 countries (Reporters Without

Borders, 2024). But some media observers say that journalists continue to be

prevented from working freely and independently (Media Institute of Southern

Africa Regional, 2023), and Freedom House (2024) rates the country as

“not free” in terms of political rights and civil liberties. In early

2023, gunmen killed prominent human rights lawyer, columnist, and

opposition activist Thulani Maseko (Al Jazeera, 2023). How do Emaswati assess

their media scene? According to the most

recent Afrobarometer survey, in late 2022, Emaswati broadly agree that

the media should act as a watchdog over the government, exposing

government missteps and wrongdoing. Citizens value media freedom and

reject the notion that public information should be the exclusive

preserve of government officials. However, most believe that media

freedom does not exist in practice in their country. Television and radio are

the most popular news sources in Eswatini, but the Internet and social

media are favoured, too, especially by youth, urban residents, and more

educated citizens. Key findings

(Afrobarometer) 22 July, 2024

848-857-43-12/Polls Emaswati Applaud Government’s Provision Of Electricity,

Though Reliability Issues Remain

With an overall

electrification rate of 85% (UNDP Eswatini, 2024), Eswatini boasts one of

the highest rates of electricity access in sub-Saharan Africa, second

in Southern Africa behind South Africa (Nzima, 2021). Imports make up a large

share of electricity consumed in the country (Government of Eswatini,

2018a; ISS African Futures, 2023). Conservative estimates suggest that

Eswatini imports about 60%-80% of its energy supply from South Africa’s

Eskom and Mozambique’s Electricidade de Moçambique (African

Development Bank, 2021; Club of Mozambique, 2022; Government of

Eswatini, 2023), while other approximations place imports from

South Africa alone at up to 90% (World Bank, 2024).

This makes energy security a significant concern for the country,

especially as the current iteration of the import agreement with South

Africa’s embattled power utility is set to expire next year (Pachymuthu,

2022). In 2022, electricity was the third-most imported product in

Eswatini (OEC World, 2024). To address its

over-reliance on imports and ensure a more sustainable energy future,

the government of Eswatini has committed to accelerate renewable energy

generation (United Nations, 2019). According to the country’s Energy

Masterplan 2034, Eswatini aims to have a 50% share of renewable energy

in the national energy mix by 2030, to be met primarily through the

adoption of biomass, hydro, solar, and wind energy technologies

(Government of Eswatini, 2018b; UNDP Eswatini, 2021). Embracing the

transition toward cleaner sources of energy also promises to contribute

to limiting climate change, which is an important item on the

government’s to-do list (UNDP Eswatini, 2023). Eswatini’s Independent

Power Producer Policy, adopted in 2016, aims for greater private sector

participation in the electricity sector (USAID Southern Africa Trade Hub,

2016). Speaking at the 2024 Standard Bank Eswatini Energy Indaba, Eswatini

Electricity Co. Managing Director Ernest Mkhonta indicated that the

national power utility is eager to collaborate with independent power

producers to increase domestic power generation, including by bringing

them online to the national electricity grid (Sikhondze, 2024). A recent Afrobarometer

survey provides an on-the-ground look at electricity access in

Eswatini. Findings show that while the country enjoys almost total grid

coverage, only about six in 10 citizens enjoy a reliable supply of

electricity, including fewer than half of the poor. Even so, electricity ranks

far down the list of problems that Emaswati want their government to

address, and most citizens applaud the government’s performance in providing

a reliable electricity supply. Key findings

(Afrobarometer) 26 July, 2024 WEST EUROPE

848-857-43-13/Polls When Did Britons Make Up Their Minds How They Would Vote At

The 2024 General Election?

Most only became certain of how they would vote in the last

fortnight of the campaign Regardless of what the

opinion polls say going into an election or how long they’ve said it,

politicians will always be quick to respond that nothing is set in stone, it

can all change during the campaign. This is not without reason – most voters

don’t definitively make up their minds until polling day is in sight, and as

recent elections have shown, this can lead to them creating surprise shifts

during the campaign. Back in May, when this

year’s election was called, there was room for this again. YouGov tracker

data compiled over the course of the election campaign shows that only 43% of

Britons had, at that point, definitely made up their mind and weren’t going

to change how (or whether) they voted. A further 23% said they were unlikely

to change their mind over the next six weeks, leaving a crucial 35% of

Britons unsure of their polling day behaviour or open to changing their

minds.

The first four weeks of

the campaign did not create much movement on this front – the proportions of

voters still harbouring some uncertainty of which way to go remaining steady

until mid-June. It was only during the final fortnight of the campaign, once

some had already started voting by post, that people’s voting intentions

seemingly began to solidify. By the eve of polling day, with one in six (18%)

Britons saying they had already voted, the number unsure or likely to change

their minds had fallen to 15%. Of course, not all voters

made their minds up at the same time – different party campaigns will have

triggered different reactions and some will have been convinced for tactical

reasons that may only have become evident weeks into the election.

Nigel Farage’s entrance

into the campaign at the start of June, for instance, clearly triggered

something of a shoring up of Reform UK’s support. Despite no increase among

all Britons definitely making their mind, the proportion of those intending

to vote Reform who were certain in their choice increased from 45% to 54%

after Farage announced his return as leader, putting Reform voters more on a

par with supporters of the two larger parties. By the end of the campaign,

they were marginally the most definite in their vote. Those leaning towards the

Lib Dems and Greens took longer to become firm in their choice, with Lib Dem

supporters only beginning to attain a similar level of certainty to those

supporting the Conservatives and Labour in the final week of the campaign. Even

on the eve of polling day, four in ten (40%) Green supporters were not

concrete in their vote. This fits with the evidence that Lib Dem and Green voters were the most

likely to feel pressure to vote tactically. (YouGov UK) 19 July, 2024

848-857-43-14/Polls Are Britons Looking Forward To The Paris Olympics?

42%

of Britons are interested in the Olympics, fewer than ahead of the London and

Rio games This Friday, billions of

eyes around the world will settle upon Paris and the opening ceremony of the

2024 Olympic games, sparking a fortnight of sport that will generate drama,

create new household names and maybe bring home a few gold medals. Olympic organisers will

have hoped that this year’s games can trigger a bit more love than the Tokyo

Olympics three years ago, enthusiasm for which was dampened heavily by Covid

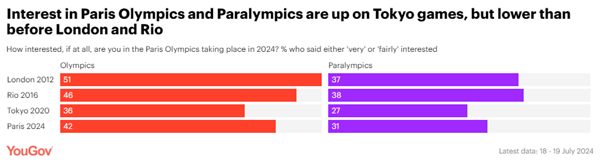

and the absence of spectators in the stadiums. Prior to the Tokyo games, 36% of Britons said they were interested in

the forthcoming Olympics, significantly down from 46% ahead of the

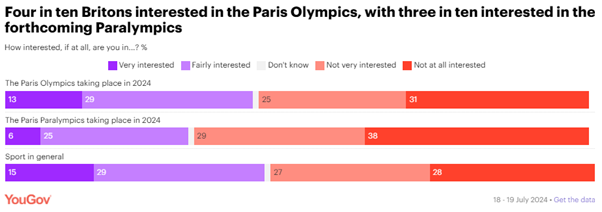

2016 Olympics in Rio and the 51% interested in London 2012. This time, just over four

in ten (42%) Britons say they are interested in the Paris games, with one in

eight (13%) being very interested. So while we can expect Brits to be more

absorbed in the Paris games than their immediate predecessors, it does seem that

the Olympics no longer resonate as widely as they did a decade ago.

A partial, but not full,

recovery in interest can also be seen with the Paralympics, which will begin

on 28th August. Three in ten (31%) Britons say they are interested in this

summer’s event in Paris, up from the mere 27% interested ahead of Tokyo 2020,

but down from the 37-38% interested ahead of the London and Rio games. There is obviously a

strong level of overlap between the 42% interested in the Olympics and the

44% figure for those interested in sport in general, but it is not universal.

Only three-quarters (74%) of Olympics fans have a general interest in sport,

while only seven in ten (71%) sports fans pay particular attention to the

Olympics.

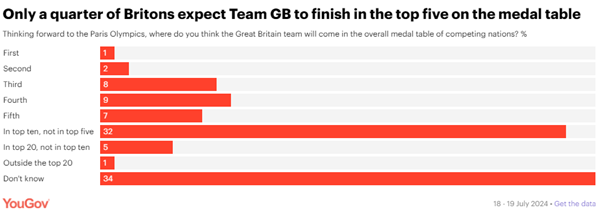

But although the Olympics

will still excite a good degree of interest, the British public are rather

sceptical of Team GB’s chances. Only a quarter of the public (27%) expect

Great Britain to finish in the top five places on the overall medal table,

slightly up on the 24% who expected such a placing ahead of Tokyo 2020, but

pessimistic considering Team GB have finished in the top five in the last

four games (including fourth in Tokyo).

(YouGov UK) 23 July, 2024 Source:

https://yougov.co.uk/sport/articles/50148-are-britons-looking-forward-to-the-paris-olympics

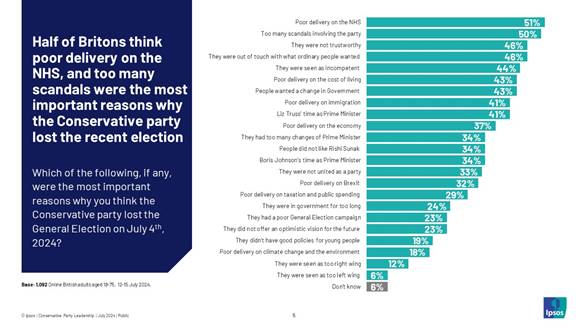

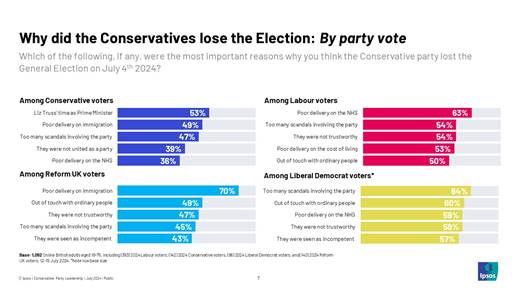

848-857-43-15/Polls Voters Split On Future Leader Of The Conservative Party And

Reasons For Election Defeat

New Ipsos polling, taken

July 12-15 2024, asked the British public who they think would do a good or

bad job as Conservative Party leader and what the key reasons were for their

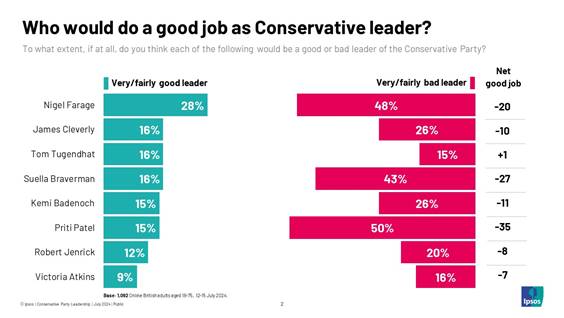

recent General Election defeat. No

consensus on who would do a good job as Conservative leader

Elsewhere in the poll, the

public were asked what they thought were the most important factors behind

the Conservative party’s election defeat. Half named poor performance on the

NHS (51%) and too many scandals (50%). This was followed by a lack of trustworthiness

and being out of touch with ordinary people on 46% each.

Ipsos

Director of Politics Keiran Pedley said of the

findings: Whoever

the new Conservative Party leader is, they will need to diagnose why the

party lost the recent General Election and come up with a plan for how to

respond. However, these findings show there is no clear public consensus on

why they lost. Reform UK / Leave supporters tend to point to immigration,

whereas others point to public services, various scandals that took place

when the Conservatives were in office and a general sense of a party out of

touch. In this context, it is perhaps no surprise that there is no public

consensus about who the next leader should be. Those popular on the right

tend to divide opinion with the public as a whole and many of the other

candidates are relative unknowns. For lots of reasons, this feels like a

leadership contest that is hard to call. (Ipsos MORI) 24 July, 2024

848-857-43-16/Polls 7 In 10 Britons Believe Immigrants Place Extra Pressure On

The NHS

New polling from Ipsos has

found that 7 in 10 (70%) of the British public believe immigrants to the UK

put additional pressure on the NHS. This includes almost two in five (37%)

who say they place a great deal of extra pressure on the NHS, and a third (33%)

who say they place a fair amount of extra pressure.

On the question of whether

migrants use NHS services more, less or about the same as the UK population,

the public are split. Over three in ten (32%) say migrants use NHS services

more than the UK population. A similar proportion (30%) say migrants use NHS

services the same amount, and one in five (20%) think migrants use NHS

services less than people born in the UK. Fairly high proportions (18%) don’t

know. However, there is also

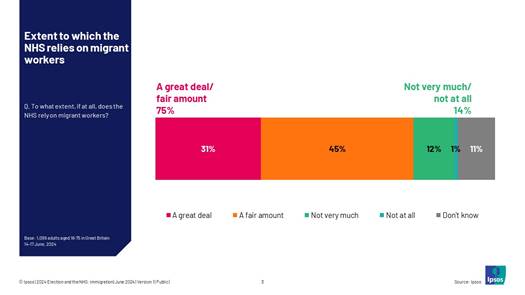

high awareness of the reliance the NHS has on migrant workers. Three quarters

(75%) say the NHS relies on migrant workers a great deal, or a fair

amount.

Commenting on the

findings, Anna Quigley, Research

Director at Ipsos, said: We

have heard some politicians put the blame for long NHS waiting lists on

non-essential immigration. These results show us that amongst the public

there are divergent views on the complex relationship between immigration and

the NHS. The public may over-inflate the pressure immigration puts on the

NHS, while recognising the important role they play in service delivery. A

more nuanced debate on these issues should help the public become better

informed about the real pressures the NHS is under, and the challenges ahead. (Ipsos MORI) 01 July, 2024 Source:

https://www.ipsos.com/en-uk/7-in-10-britons-believe-immigrants-place-extra-pressure-on-nhs

848-857-43-17/Polls Most Spaniards Think That AI Will Not Replace Them At Work

Over the past year, we

have witnessed the rise of Generative AI. In fact, the magnitude of its

impact and the speed of its deployment are placing this technology at the

centre of social conversation, as well as on the innovation agendas of

companies, due to its multiple applications in daily and work life. In this

context, Ipsos, one of the world's leading market research firms, has just

published its annual study "AI Monitor", which analyses the