|

BUSINESS

& POLITICS IN THE WORLD GLOBAL

OPINION REPORT NO. 822-825 Week: November 20 – December

17, 2023 Presentation: December 22,

2023 16%

Prefer Koizumi As Prime Minister; 36% Choose ‘No One’ Overall,

8 In 10 People In Pakistan Are Concerned About Impacts Of Climate Change South

Africans Want To See Greater Government Initiative To Promote Gender Equality Young

Ethiopians Prioritise Management Of The Economy For Government Action As

Climate Change Worsens Life In Gambia, Citizens Want Collective Action To

Fight It Why

Do Britons Think Inheritance Tax Is Unfair Britons

Support Rejoining The Single Market, Even If It Means Free Movement Just

11% Of Britons Think COP28 Will Result In Significant Action On Climate

Change More

Than Two In Five Britons Worry About How Much Christmas Is Going To Cost Do

The Public Praise Or Blame Rishi Sunak And Jeremy Hunt When It Comes To

Inflation 58%

Of French People Admit That They Could Make More Effort To Reduce Their

Energy Consumption First

Anniversary Of Chat GPT, 77% Of French People See This Tool As A Revolution Americans

More Upbeat About Future Social Security Benefits Americans’

Views Of The Israel-Hamas War About

Half Of Republicans Now Say The U.S. Is Providing Too Much Aid To Ukraine Older

Workers Are Growing In Number And Earning Higher Wages Falling

Inflation Provides Scant Relief As Canadians Cool Holiday Spending For A

Second Year There

Were Nearly Two Million Extra Vehicle Insurance Policies In 2023 Global

Attitudes On An Interconnected World, A Survey Across 24 Nations How

The Israel-Hamas War In Gaza Is Changing Arab Views INTRODUCTORY

NOTE 822-825-43-30/Commentary: More Than Two In

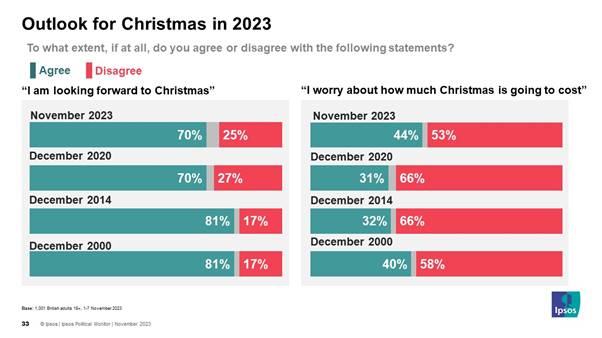

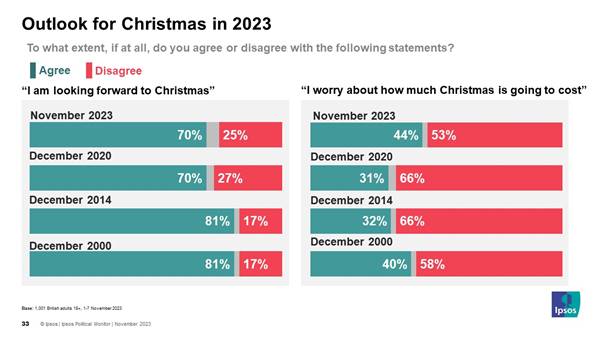

Five Britons Worry About How Much Christmas Is Going To Cost

The latest Ipsos Political Monitor, taken 1st – 8th

November 2023, explores public attitudes towards the cost of Christmas and

whether the economy (and other facets of life in Britain) will improve or get

worse in the next 12 months. The cost of Christmas Whilst most Britons are looking forward to Christmas

(70%), many are concerned by how much it will cost. This year 44% say they

are concerned, compared to around three in ten in December 2020 and

2014.

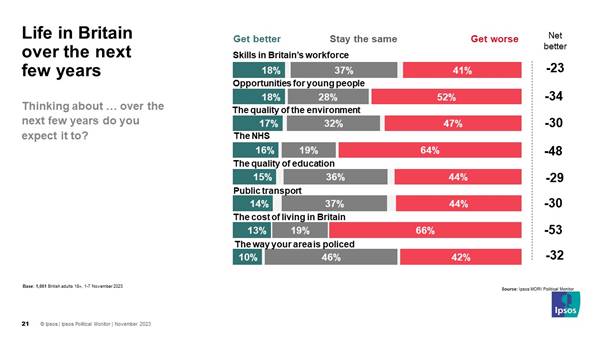

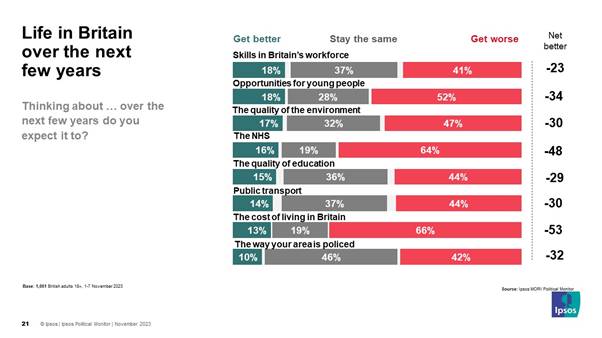

The economy and cost of

living 55% of Britons expect the economy to worsen over the

next 12 months, 19% think it will improve. This gives a net score of -36

which is very similar to last month (-34) and the start of the year (-33 in

January). When asked about difference facets of life in

Britain there is a lot of pessimism around – especially on the NHS and cost

of living. 66% expect the cost of living in Britain to get worse in the next

few years and 64% say the same about the NHS.

Gideon Skinner, Head of

Political Research at Ipsos, said: The rate of inflation may

be falling, but Britons are still feeling its impact. Most people are

still pessimistic about the cost of living over the next few years, and even

Christmas does not escape. Even though most people are still looking forward

to the festivities, over 4 in 10 are worried about its cost – with young

people, renters and women in particular feeling the pressure. Ahead of the

Autumn Statement the Prime Minister and Chancellor have hit their pledge to

halve inflation, but will know they will also need to deliver on their other

targets to grow the economy and reduce people’s financial insecurities over

the cost of living to change the public mood. (Ipsos MORI) 21 November 2023 Source: https://www.ipsos.com/en-uk/more-two-in-five-britons-worry-about-how-much-christmas-is-going-to-cost SUMMARY OF POLLS ASIA (Japan) 16% Prefer Koizumi As

Prime Minister; 36% Choose ‘No One’ Former Environment Minister Shinjiro Koizumi is

considered the “most suitable” for prime minister by voters from among seven

ruling party lawmakers, including incumbent Fumio Kishida, according to an

Asahi Shimbun survey. Koizumi was picked by 16 percent of survey respondents

in the “suitability” question, followed closely by Shigeru Ishiba, former

Liberal Democratic Party secretary-general, at 15 percent, and Taro Kono,

minister for digital transformation, at 13 percent. (Ashi Shimbun) 20 November 2023

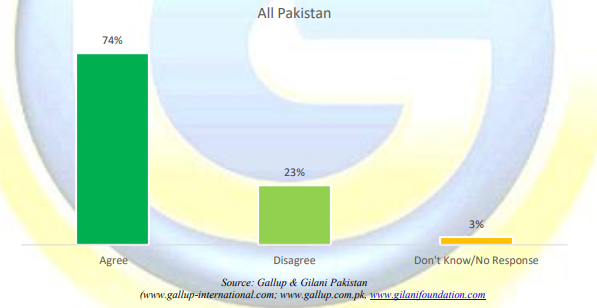

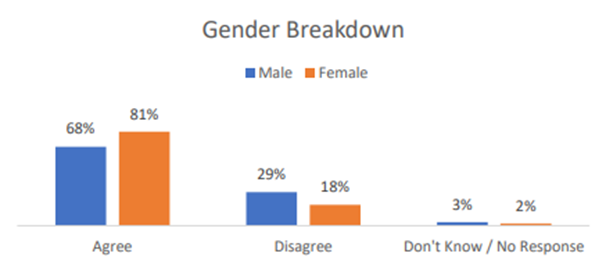

Nearly Three

Quarters (74%) Of Pakistanis Think That The Environment For Working Women Is

Less Supportive As Compared To Working Men According to a survey conducted by Gallup &

Gilani Pakistan, a significant majority (81%) of women in Pakistan think that

the environment for working women is less supportive as compared to working

men, while 29% of men in Pakistan think that it is not less supportive. A

nationally representative sample of adult men and women from across the

country was asked the question, “Do you think the environment for working

women, compared to working men, is less supportive?” In response, 74% said

‘yes’, 23% said ‘no’, and 3% said that they did not know or gave no response. (Gallup Pakistan) 13 December 2023 Overall, 8 In 10

People In Pakistan Are Concerned About Impacts Of Climate Change According to a recent report published by the World

Bank Group (for the full report click here) using data collected by Gallup

Pakistan it was found that 8 in 10 people in Pakistan are concerned about

impacts of climate change, with females and educated people being more

concerned. People are more likely to take energy-saving actions like turning

off lights (83.4%) that lead to financial savings, instead of other

actions such as reduction beef or paper, consumption etc. (Gallup Pakistan) 14 December 2023 AFRICA (South Africa) South Africans Want

To See Greater Government Initiative To Promote Gender Equality In South Africa, the gender gap is steadily

narrowing, especially in education, where female students outperform their

male counterparts (Ramaphosa, 2023). But despite marked improvement, women’s

labour force participation rates lag behind men’s. The Quarterly Labour Force

Survey shows that in the second quarter of 2023, women’s participation rate

stood at 54.3% compared to 64.9% for men, representing a

10.6-percentage-point gap (Statistics South Africa, 2023). (Afrobarometer) 29 November 2023

Young Ethiopians

Prioritise Management Of The Economy For Government Action More than two-thirds of Ethiopians are under age 30

(Ethiopian Statistical Service, 2013), a powerful asset and resource for

growth that has gone largely untapped. Historically, the relationship between

successive Ethiopian governments and the youth has been “a combination of

repression and co-optation” linking state resources and employment

opportunities to youth associations affiliated with the ruling party (Kefale,

Dejen, & Aalen, 2021). (Afrobarometer) 30 November 2023 As Climate Change

Worsens Life In Gambia, Citizens Want Collective Action To Fight It More than six in 10 Gambians (62%) say floods have

become more severe in their region over the past decade. Half as many (31%)

say the same about droughts. o Rural residents and poor citizens are

significantly more likely to report worsening floods and droughts than their

urban and better-off counterparts. A slim majority (56%) of Gambians say they

have heard of climate change, a 12- percentage-point decrease compared to

2021. (Afrobarometer) 01 December 2023 WEST EUROPE (UK) Why Do Britons Think

Inheritance Tax Is Unfair There has been speculation at

various points this year that the government would make cuts to inheritance

tax. YouGov tracker polling has

consistently shown that Britons consider inheritance tax

to be unfair, and a July survey found that a majority (56%) would support

scrapping it. Few estates actually pay inheritance tax (less

than 4% in 2020-21), although YouGov

research for The Times in July found that

approximately 15% of Britons expect to receive an inheritance in future that

they will have to pay the tax on, and 31% expect that the tax will be levied

on assets they themselves leave behind when they die. (YouGov UK) 23 November 2023 Britons Support

Rejoining The Single Market, Even If It Means Free Movement New YouGov data indicates that more Britons are in

fact supportive of joining the single market, even under this condition, than

in opposition. Just short of six in ten Britons (57%) would support the UK

joining the single market, even if this meant a return to free movement, with

only around one in five (22%) opposed. More than eight in ten Remain voters

(83%) would support doing so, compared to around a third (35%) of Leave

voters, who tend to be opposed (45%). (YouGov UK) 29 November 2023 Just 11% Of Britons

Think COP28 Will Result In Significant Action On Climate Change (YouGov UK) 30 November 2023 Despite Pressures

Facing Young Families Today, Most Parents Take Precious Moments To Play With

Their Babies Four in five primary caregivers of nine-month-old

babies reported cuddling, talking and playing with their little one several

times a day, in the first national long-term study of babies in over two

decades, led by UCL in partnership with Ipsos. More than half engaged in

physical or turn-taking play, singing, pretend games and noisy play with

their babies several times a day – activities which were linked to improved

early language development. Around three quarters showed their babies picture

books or took them outside at least once a day. (Ipsos MORI) 20 November 2023 More Than Two In

Five Britons Worry About How Much Christmas Is Going To Cost The latest Ipsos Political Monitor, taken 1st – 8th

November 2023, explores public attitudes towards the cost of Christmas and

whether the economy (and other facets of life in Britain) will improve or get

worse in the next 12 months. Whilst most Britons are looking forward to

Christmas (70%), many are concerned by how much it will cost. This year 44%

say they are concerned, compared to around three in ten in December 2020 and

2014. (Ipsos MORI) 21 November 2023 Do The Public Praise

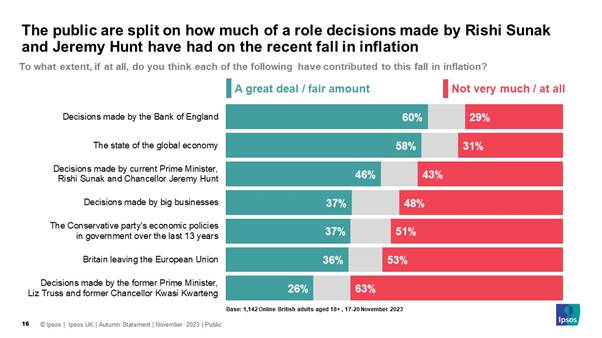

Or Blame Rishi Sunak And Jeremy Hunt When It Comes To Inflation New polling from Ipsos in the UK, taken before the

recent Autumn Statement (Friday 17th to Monday 20th November), explored

public attitudes to the economy, inflation and Rishi Sunak’s performance in

delivering against his 5 key policy pledges announced earlier this year. When

asked how far various factors have contributed to falling inflation, we find

the public are split on the role of Rishi Sunak and Jeremy Hunt. 46% think

they have contributed a great deal or fair amount to falling inflation and

43% say they have had not very much impact or have made no contribution at

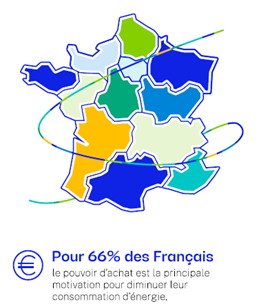

all. (Ipsos MORI) 24 November 2023 (France) 58% Of French People

Admit That They Could Make More Effort To Reduce Their Energy Consumption Nationwide,

in a context still marked by inflation, against the backdrop of the climate

crisis, the two main concerns of the French are purchasing power (60% rank it among their three main

concerns) and the environment (35%). Located at the

intersection of these two dimensions, the issue of energy sobriety appears more than ever to be a priority issue

for the country. Thus, purchasing power is the most important

factor encouraging the French to reduce their energy consumption (66%),

followed by the environment (21%). (Ipsos France) 28 November 2023 First Anniversary Of

Chat GPT, 77% Of French People See This Tool As A Revolution On November 30, 2022, the French version of Chat GPT

was made available to the general public. One year after this launch, the

awareness of Chat GPT has reached a very high level: more than one in two French people (55%) now say

they know what Chat GPT is and 83% of French people have

heard of it. Chat GPT is best known by younger people (72% of those under 35

have a good idea of what it is), executives (83%) and people with a diploma

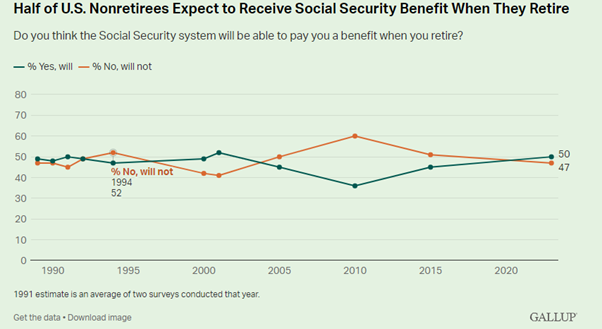

above the baccalaureate (67%). (Ipsos France) 01 December 2023 NORTH AMERICA (USA) Americans More

Upbeat About Future Social Security Benefits Americans are more optimistic about the future of

Social Security than they have been in recent years, even though only about

half currently express optimism. Among U.S. nonretirees, 50% expect the

Social Security system to pay them a benefit when they retire, while 47% do

not. In three readings taken between 2005 and 2015, nonretirees were more

inclined to predict they would not receive Social Security retirement

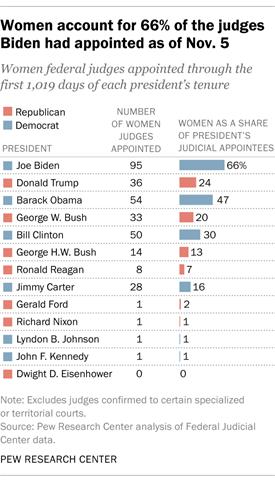

benefits. (Gallup) 08 December 2023 Most Of Biden’s

Appointed Judges To Date Are Women, Racial Or Ethnic Minorities – A First For

Any President Nearly two-thirds of the federal judges President

Joe Biden has appointed so far are women, and the same share are members of

racial or ethnic minority groups, according to a Pew Research Center analysis

of statistics

from the Federal Judicial Center. Biden still has more

than a year left in his term, so these patterns could change. But no

president has ever appointed a slate of judges consisting mostly of women or

racial and ethnic minorities. (PEW) 4 December 2023 Americans’ Views Of

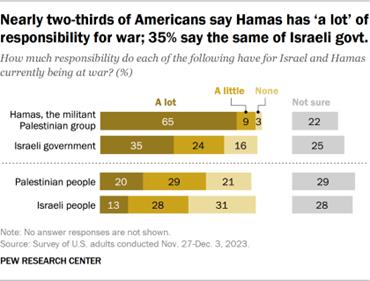

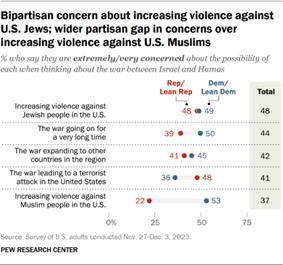

The Israel-Hamas War As the war between Hamas and Israel continues with

no end in sight, far more Americans (65%) say Hamas bears a lot of

responsibility for the current conflict than say that about the Israeli

government (35%). Much smaller shares of Americans say the Palestinian people

(20%) and the Israeli people (13%) have a lot of responsibility for the war. Nearly

half of Americans (48%) say that when thinking about the war, they are

extremely or very concerned about the possibility of increasing violence

against Jewish people in the United States. (PEW) 8 December 2023 About Half Of Republicans

Now Say The U.S. Is Providing Too Much Aid To Ukraine As the war in Ukraine nears the two-year mark, about

three-in-ten Americans (31%) say the United States is providing too much

assistance to Ukraine in its fight against Russia, while about half say that

the U.S. is providing the right amount of support (29%) or not providing

enough (18%). The share of Americans who say the U.S. is giving too much support to Ukraine has

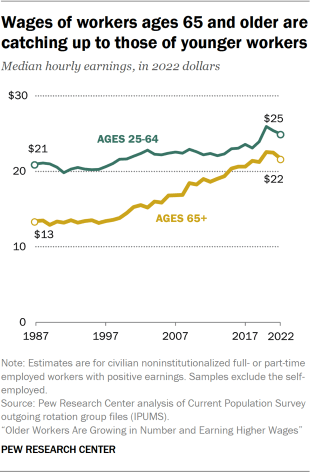

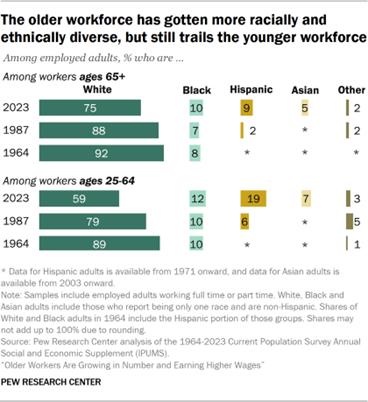

grown steadily over the course of the war, especially among Republicans. (PEW) 8 December 2023 Older Workers Are

Growing In Number And Earning Higher Wages Roughly one-in-five Americans ages 65 and older

(19%) were employed in 2023 – nearly double the share of those who were

working 35 years ago. Not only are older workers increasing in number, but

their earning power has grown in recent decades. In 2022, the typical worker

age 65 or older earned $22 per hour, up from $13 in 1987. Earnings for

younger workers haven’t grown as much. As a result, the wage gap between

older workers and those ages 25 to 64 has narrowed significantly. (PEW) 14 December 2023

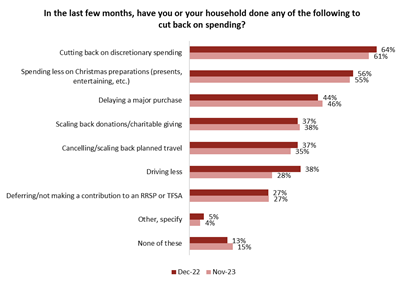

Falling Inflation

Provides Scant Relief As Canadians Cool Holiday Spending For A Second Year New data from the non-profit Angus Reid Institute

finds Canadians finding little reprieve from a stabilizing inflation

situation. Underscoring how economic conditions continue to drag, the sting

of a second year of high consumer prices affecting everything from the cost

of vitamins to bread and rent has majorities saying they will spend less on

holiday preparations this year (55%) and have cut back on discretionary

spending overall in recent months (61%). This continues a trend that emerged

last year, when similar numbers said they had cut back. (Angus Reid Institute) 30 November 2023 AUSTRALIA Readership Of Magazines Is Up 3.5% From A Year Ago With

Increases In Readership For All Magazine Categories Now 11.6 million Australians aged 14+ (53.0%) read

print magazines, up 3.5 per cent on a year ago, according to the results

released today from the Roy Morgan Australian Readership report for the 12

months to September 2023. This market broadens to 15.1 million Australians

aged 14+ (69.2%) who read magazines in print or online either via the web or

an app, which is virtually unchanged from a year ago. These are the latest

findings from the Roy Morgan Single Source survey of 65,331 Australians aged

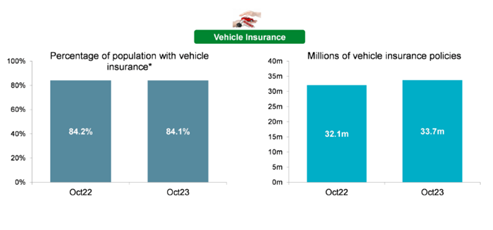

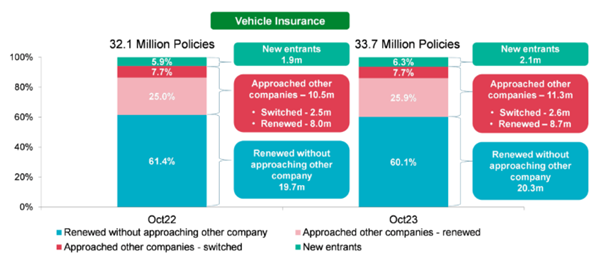

14+ in the 12 months to September 2023. (Roy Morgan) 28 November 2023 There Were Nearly Two Million Extra Vehicle Insurance

Policies In 2023 New data from Roy Morgan shows that there were

nearly two million more vehicle insurance policies in 2023 compared to 2022. The

substantial increase in Australia’s population after the winding down of

COVID restrictions has contributed to an increasing number of registered

motor vehicles on Australian roads. More motor vehicles have boosted the

number of vehicle insurance policies, with the number increasing by 1.6

million between October 2022 (32.1 million) and October 2023 (33.7 million). (Roy Morgan) 04 December 2023 Australian Employment Increased To Over 14 Million For The

First Time In November, But Still Over 3 Million Unemployed Or Under-Employed In November 2023

Australian employment hit a record high of over 14 million for the first time

with over 9 million now employed full-time and over 5 million employed

part-time. However, despite surging employment – up

by 430,000 compared to a year ago – a massive 3.04 million Australians (19.6%

of the workforce) were unemployed or under-employed in November. ‘Real’

unemployment was down 0.2% to 9.7% - an estimated 1,505,000 Australians (down

37,000) in November. (Roy Morgan) 12 December 2023 ANZ-Roy Morgan Consumer Confidence Jumps 4.4pts To 80.8

After The RBA Leaves Interest Rates Unchanged – The Highest For Over Ten

Months Since Early February 2023 ANZ-Roy Morgan Consumer Confidence jumped 4.4pts to

80.8 this week after the RBA left interest rates unchanged at last week’s

final meeting for the year. However, despite the increase, Consumer

Confidence has now spent a record 45 straight weeks below the mark of 85.

Consumer Confidence is now 2.1pts below the same week a year ago, December

5-11, 2022 (82.9) and nearly 3 points above the 2023 weekly average of 77.8. (Roy Morgan) 12 December 2023 MULTICOUNTRY STUDIES Seven In Ten People Anticipate Climate Change Will Have A

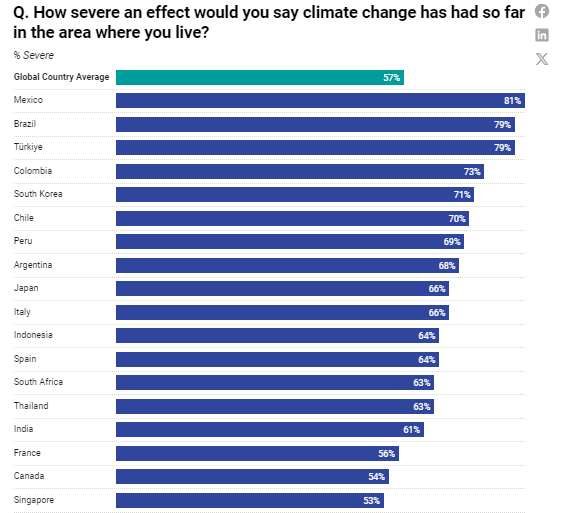

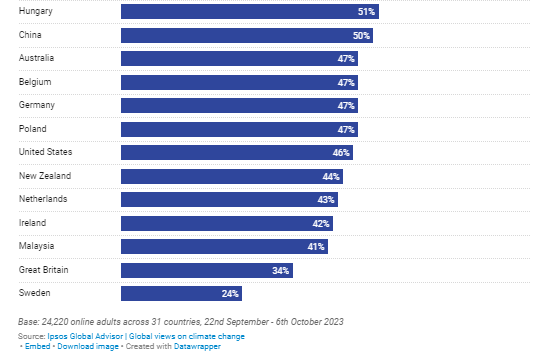

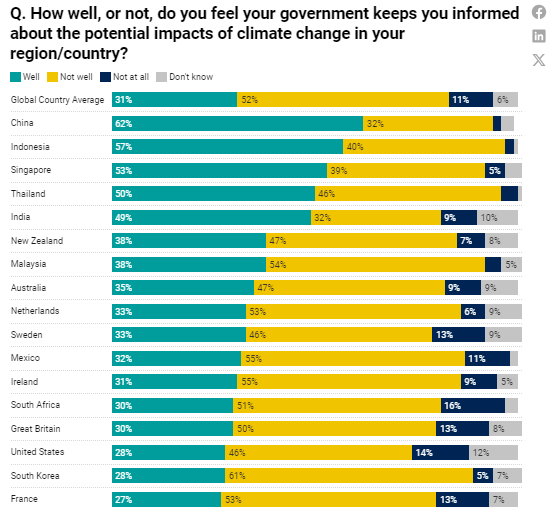

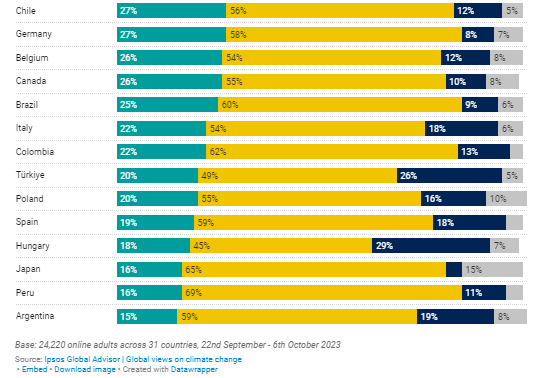

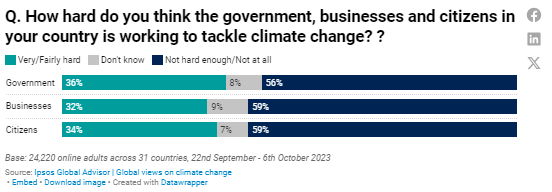

“Severe Effect” In Their Area Within The Next Ten Years, A Survey Across 31

Nations This Ipsos study, released ahead of the COP28 UN

Climate Change Conference, provides a new assessment on how people feel about

climate change right now – focusing on what they see around them and what

they think about actions being taken to address the challenges it brings. A

majority (57%) across 31 countries have already witnessed a severe impact of

climate change where they live. For countries like Mexico, Brazil and

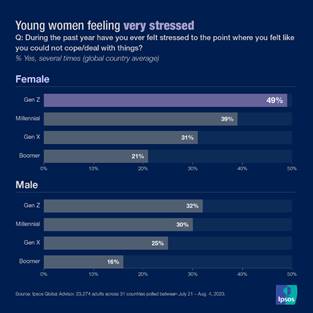

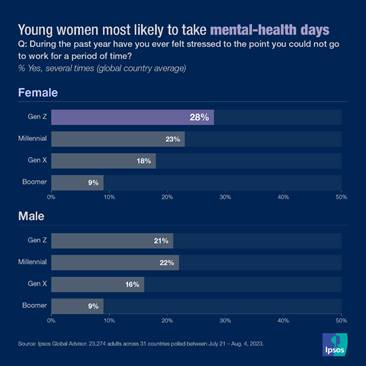

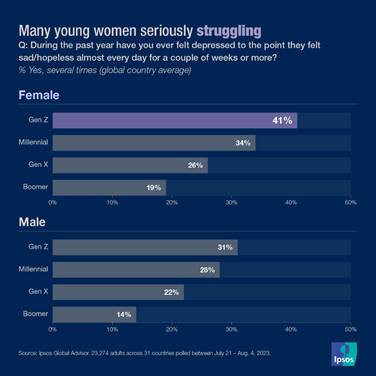

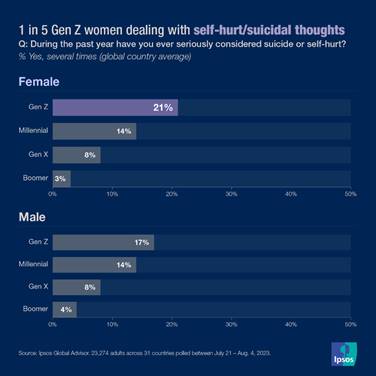

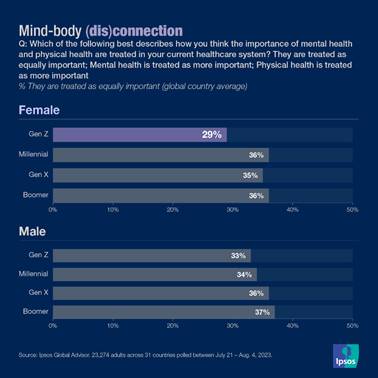

Türkiye, this figure is as high as eight in ten. (Ipsos Global) 27 November 2023 Data Dive: Gen Z Women Are Struggling The Most With Stress,

Mental Health Issues, A Survey Across 31 Countries And our recent global

polling finds Generation Z women* are finding

it quite difficult to cope these days. Just over two in three (68% on average

globally) Gen Zers say mental health and physical health are equally

important, followed by 73% of Millennials, 82% of Gen Xers and 87% of

Boomers. Yet, only 35% think healthcare providers are placing equal emphasis

on mental and physical health – with Gen Z women the least likely to think

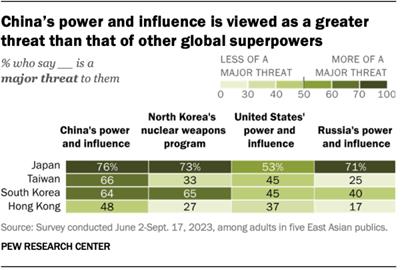

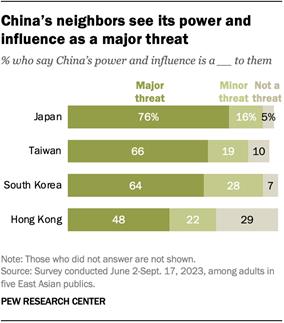

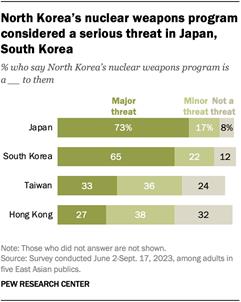

both are being treated equally. (Ipsos Global) 05 December 2023 Source: https://www.ipsos.com/en/data-dive-gen-z-women-are-struggling-most-stress-mental-health-issues In East Asia, Many People See China’s Power And Influence

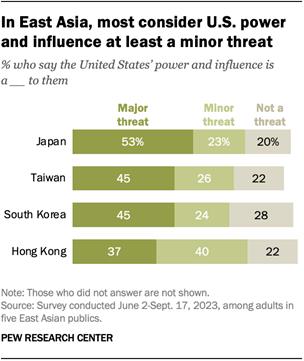

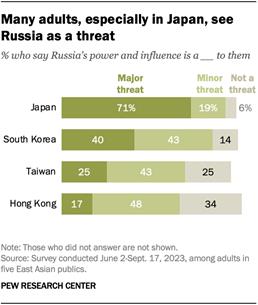

As A Major Threat, A Survey In Five Asian Nations Majorities of adults in Japan, Taiwan and South

Korea see China’s power and influence as a major threat to them. Roughly half

of adults in Hong Kong (48%) agree. And large majorities in all places

surveyed call China at least a minor threat.

In Japan, 76% of adults consider China a major threat. This is comparable to

the share (74%) who said the same in 2013, amid

flare-ups in the East China Sea, and higher than the

share (69%) who said this toward the end of the last decade. (PEW) 05 December 2023 Global Attitudes On An Interconnected World, A Survey

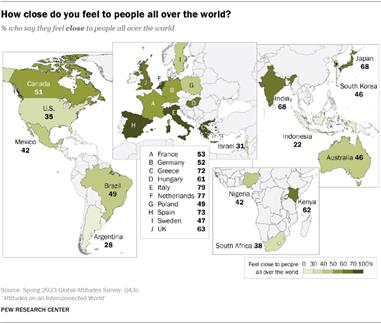

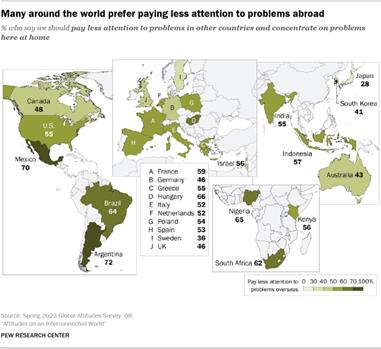

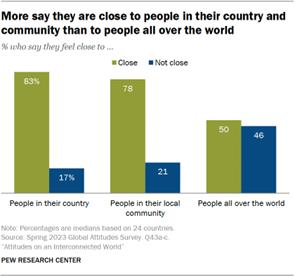

Across 24 Nations A median of 50% say they feel very or somewhat close

to people all over the world, while 46% feel not too or not at all close.

Feeling close to others around the world is more common in Europe than in

other regions. Only 35% express this view in the United States, and it is

even less common in Argentina, Indonesia and Israel. When it comes to

engagement and cooperation with other nations, views differ significantly

among the nations we polled, but a median of 55% want to pay less attention

to problems in other countries and concentrate on problems at home; 43% think

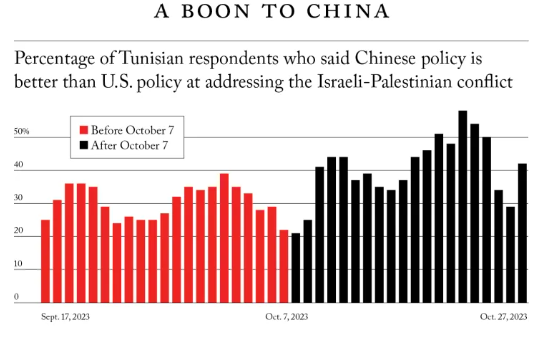

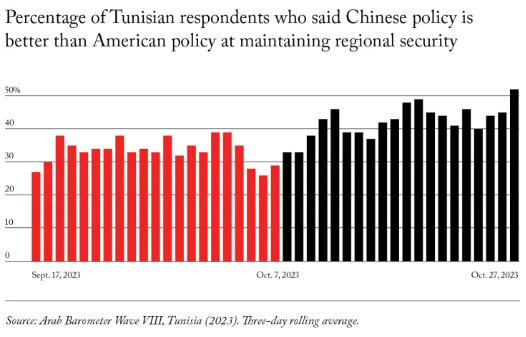

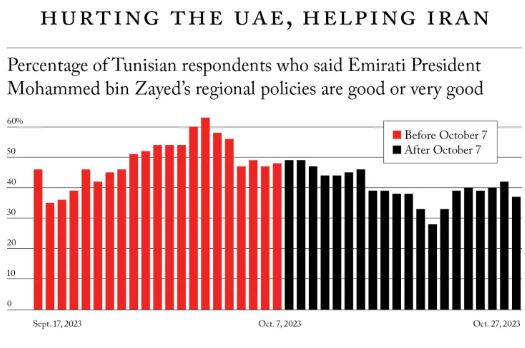

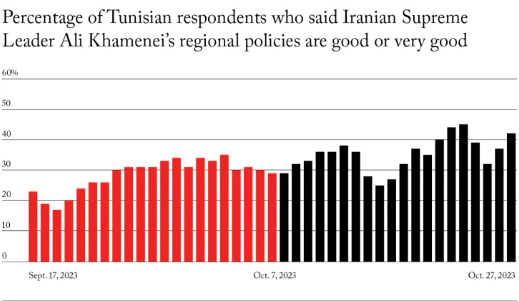

it’s best for the future of their country to be active in world affairs. (PEW) 06 December 2023 Source: https://www.pewresearch.org/global/2023/12/06/attitudes-on-an-interconnected-world/ How The Israel-Hamas War In Gaza Is Changing Arab Views Since October 7, the latest war between Hamas and

Israel has claimed the lives of more than 15,000 Palestinians and over 1,200

Israelis. Scores more have been injured. The war has displaced more than 1.8

million Palestinians and left the fates of many of Israel’s people unknown;

over 100 of those abducted in Israel remain hostages. Fighting has resulted

in damage to 15 percent of the buildings in Gaza, including over 100 cultural

landmarks and more than 45 percent of all housing units. (Foreign Affairs) 14 December 2023 ASIA

822-825-43-01/Polls 16% Prefer

Koizumi As Prime Minister; 36% Choose ‘No One’

The other four were each chosen by less than 10

percent. Sanae Takaichi, minister of economic security,

gained 8 percent of the picks, Kishida received 7 percent, and former Foreign

Minister Yoshimasa Hayashi and LDP Secretary-General Toshimitsu Motegi each

got 1 percent. However, 36 percent of respondents said none of the

seven is suitable for prime minister, highlighting the lack of a clear public

favorite to lead the country. The Asahi Shimbun conducted the nationwide telephone

survey on Nov. 18 and 19. Since Shinzo Abe became prime minister for the

second time in 2012, Koizumi, Ishiba and Kono have ranked high in surveys on

voters’ preferences for prime minister. Although they were the top three in the latest

survey, the percentages suggest they have lost a considerable amount of

public support. Takaichi, an outspoken conservative who was close to

Abe and has shown her interest in succeeding Kishida, was chosen by 11

percent of male respondents but only 5 percent of women, the survey showed. Motegi, who heads the third-largest LDP faction, and

Hayashi, who is the No. 2 individual in the Kishida faction, the fourth

largest, are considered influential in the political arena, but they are not

particularly well known among the public. Among LDP supporters, Koizumi was picked by 19

percent, followed by Kono at 17 percent, Kishida and Ishiba at 15 percent

each, and Takaichi at 9 percent. 20 November 2023 Source: https://www.asahi.com/ajw/articles/15062017 822-825-43-02/Polls Nearly Three

Quarters (74%) Of Pakistanis Think That The Environment For Working Women Is

Less Supportive As Compared To Working Men

GENDER BREAKDOWN: 81% of the women agreed with the statement while

only 18% disagreed. There is a 13% difference in the number of women who

agreed with the statement as compared to men.

13 December 2023 Source: https://gallup.com.pk/wp/wp-content/uploads/2023/12/13.12.23.Daily-Poll-English.pdf 822-825-43-03/Polls Overall, 8 In

10 People In Pakistan Are Concerned About Impacts Of Climate Change

According to a recent

report published by the World Bank Group (for the full report click here) using data collected

by Gallup Pakistan it was found that 8 in 10 people in Pakistan are concerned about

impacts of climate change, with females and educated people being more concerned. 13 key learnings from the report are: 1. In a global comparison involving 19 countries

conducted to gain a deeper understanding of attitudes towards climate change

Pakistan’s values lie somewhere in the middle. Ranking #15 in terms of considering

climate change a major threat. 2. Overall, 8 in 10 people in Pakistan are concerned

about impacts of climate change, with females and educated people being more

concerned. 3. People’s perception of climate change can be

affected by their experiences of income shocks. With 16.2% more personally caring about

climate change, and 6.2% more concerned with the impact of climate change on

children when having previously experienced income loss as an impact of climate

change. 4. Although around 80% of people express concern

about climate change and its impacts, when asked specifically about it, it does

not necessarily rank high on their list of priorities to address, with less than 25%

considering it as one of their “Top 3 problems”. 5. Less than half the people believe that climate

change is caused by human activity. People with higher levels of education tend to be

more knowledgeable about climate change issues. 6. 37.7% of illiterate people do not trust any of

the sources of climate related information. This number decreases to 26.1% for

people with higher education or above. 7. Trust in sources of information also varies

depending on the location of people, with rural areas being more skeptical. 34.2% people in

rural areas and 29.6% in urban areas do not trust any sources of climate change

information, making it difficult to convey the necessary information to them

through traditional channels. 8. Despite widespread support, with 94% of parents

demanding climate education in schools, less than half of them discuss climate

change with their children at home. 9. Despite high levels of concern about climate

change, support for personal and government action is relatively low across all forms

of intervention. 10. More than two-thirds of people were prepared to

pay for environmentally friendly goods. There are, however, differences in demand

based on education level. 11. 92% of individuals consider conserving energy

somewhat or very important, however, less than 13% people across all educational groups

mentioned they support energy conservation for environmental reasons. 12. When compared to overall concern for the

environment shared by over 80%, the percentage of people willing to contribute income or

pay taxes for environment is less than 60%. 13. People are more likely

to take energy-saving actions like turning off lights (83.4%) that lead to financial

savings, instead of other actions such as reduction beef or paper, consumption etc. These findings highlight

the complexities presented in understanding and

addressing climate change issues in Pakistan, as well as how the

approach to combat climate change issues varies across different socio-economic groups. 14 December 2023 Source: https://gallup.com.pk/wp/wp-content/uploads/2023/12/World-Bank-Report-PR-4.pdf AFRICA

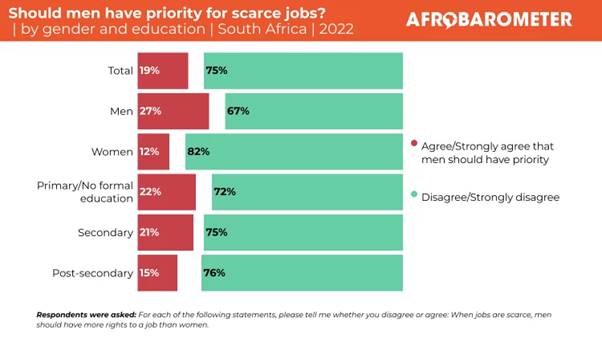

822-825-43-04/Polls South Africans Want To See

Greater Government Initiative To Promote Gender Equality

In August, South Africa

celebrated its annual Women’s Day and Women’s Month under the theme “Women’s

socio-economic rights and empowerment: Building back better for women’s

improved resilience” (South African Government, 2023). Meeting this goal will

require a holistic approach anchored in the economic, social, and political

empowerment of women (Statistics South Africa, 2022). In South Africa, the gender gap is steadily

narrowing, especially in education, where female students outperform their

male counterparts (Ramaphosa, 2023). But despite marked improvement, women’s

labour force participation rates lag behind men’s. The Quarterly Labour Force

Survey shows that in the second quarter of 2023, women’s participation rate

stood at 54.3% compared to 64.9% for men, representing a

10.6-percentage-point gap (Statistics South Africa, 2023). When

employed, women are overwhelmingly engaged in precarious forms of work

characterised by low pay and difficult work conditions (Teuteberg &

Benjamin, 2023). Significant progress has

been made in political representation, with 42% of seats in Parliament now

held by women (Brothers, 2023). But girls and women

continue to bear the brunt of violence, abuse, harassment, and

discrimination. The Department of Justice and Constitutional Development

reports that it handles more than 50,000 cases of domestic violence and

femicide annually (Maine, 2023), while many other cases of gender-based

violence go unreported. In an attempt to deal with the scourge of violence

against women, the government last year passed the Criminal Law (Sexual

Offences and Related Matters) Amendment Act Amendment Bill, the Criminal and

Related Matters Amendment Bill, and the Domestic Violence Amendment Bill

(South African Government, 2022; Vallabh, 2022). This dispatch reports on a

special survey module included in the Afrobarometer Round 9 questionnaire to

explore Africans’ experiences and perceptions of gender equality in

control over assets, hiring, land ownership, and political leadership.

(For findings on gender-based violence, see Mpako & Ndoma,

2023). In South Africa, findings

show close to gender-equal educational attainment, but women trail men

slightly in control over certain assets and household financial decisions.

Large majorities express support for gender equality in hiring, land ownership,

and political leadership, but many also consider it likely that a woman will

suffer criticism and harassment from the community if she runs for

elective office. Overall, South Africans

say the government should do more to promote equal rights and

opportunities for women, ranking gender-based violence and women’s

under-representation in positions of power as the most important

women’s-rights issues that their government and society must address. Key findings

29 November 2023

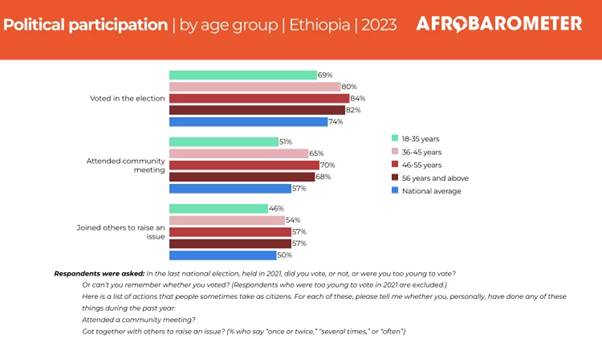

822-825-43-05/Polls Young Ethiopians

Prioritise Management Of The Economy For Government Action

In 2004, Ethiopia

introduced its first National Youth Policy, which defines youth as 15- to 29-

year-olds and seeks to ensure that they have professional competencies,

skills, and ethics to contribute to and benefit from the country’s

development. Components of the policy emphasise youth participation in

education and training, economic progress, and democracy and governance

(Ministry of Youth, Sports and Culture, 2004). Measures designed to empower

the youth include the Youth Revolving Fund, a multibillion-birr fund intended

to help unemployed youth in urban and rural areas get jobs (Federal

Democratic Republic of Ethiopia, 2017). Despite such initiatives,

the official rate of youth unemployment as of February 2021 stood at 12% in

rural areas and 23% in cities, and migrants leaving the country in search of

opportunities are predominantly the young aged 15-29 (Ethiopian Statistical

Service, 2021). Ethiopia remains a country where youth development is

low, ranking 158th out of 181 countries on the Global Youth Development

Index (Commonwealth, 2020). The Afrobarometer Round 9

survey (2023) offers some insights into the situation Ethiopian youth

(defined here as ages 18-35). Findings show that young people are more

educated than their elders but are also more likely to be unemployed. The

economy is topmost on the minds of young Ethiopians, who think their

government is doing a poor job on economic management and job creation. A

majority of youth think their country is headed in “the wrong direction,”

though they are somewhat more optimistic than older citizens that things will

improve in the near future. Despite their

dissatisfaction, young citizens are less likely than their elders to engage

in political processes. Key findings

30 November 2023

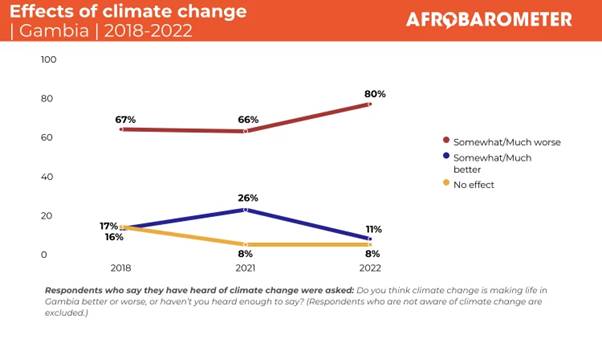

822-825-43-06/Polls As Climate Change Worsens

Life In Gambia, Citizens Want Collective Action To Fight It

Agriculture and tourism

combine for almost half of the Gambia’s gross domestic product (GDP) (Gambia

Bureau of Statistics, 2022), and both are highly vulnerable to increasingly

frequent and severe climate-related disasters that have plagued the country, including

droughts, floods, windstorms, bushfires, soil intrusion, and coastal erosion.

Climate change poses substantial risks to property, productive assets,

livelihoods, and health, impeding the country’s progress toward its

development objectives (Ministry of Environment, Climate Change and Natural

Resources, 2022; Republic of the Gambia, 2022). The Gambia ranks 148th out

of 182 countries on the Notre-Dame Global Adaptation Initiative’s (2021)

Country Index, which rates both vulnerability to climate change and

resilience. This dispatch reports on a

special survey module included in the Afrobarometer Round 9 questionnaire to

explore Gambians’ experiences and perceptions of climate change. Findings show that a

majority of Gambians say flooding has become more severe in their region over

the past decade – perceptions that are especially common among rural and poor

citizens. Among the slim majority of

Gambians who have heard of climate change, most say it is making life in the

country more difficult. And almost unanimously, they demand greater efforts

by the government and other stakeholders to address the threat. Key findings

01 December 2023 WEST

EUROPE

822-825-43-07/Polls Why Do Britons Think

Inheritance Tax Is Unfair

Topping

the list is the idea that it represents ‘double taxation’ There has been speculation at

various points this year that the government would make cuts to inheritance

tax. YouGov tracker polling has

consistently shown that Britons consider inheritance

tax to be unfair, and a July survey found that a majority (56%) would support

scrapping it. Few estates actually pay inheritance tax (less

than 4% in 2020-21), although YouGov

research for The Times in July found that

approximately 15% of Britons expect to receive an inheritance in future that

they will have to pay the tax on, and 31% expect that the tax will be levied

on assets they themselves leave behind when they die. Nevertheless, these

figures are still significantly smaller than the 61% of Britons who said that

inheritance tax is unfair in a survey in late September. So why do people

consider the tax to be unfair? We asked these respondents to describe their

reasoning for us – respondents answered in their own words, which we have

grouped into the categories below. By far the most common

reason is the perception that inheritance tax represents ‘double taxation’ –

that the deceased had already paid various taxes when they earned their money

and purchased their property, and were now effectively being forced to do so

again in order to pass it on. More than four in ten of those who consider

inheritance tax unfair gave this as a reason (42%). "Why

should anyone have to pay tax on money that has already been taxed god knows

how many times over? Inheritance tax is grossly unfair to anyone who has to

pay it." "People

work all their lives to save and leave something for their children having

already paid tax on it, its a double hit." "People

are taxed on earnings, savings, pensions - so all dues have been paid." Why

is inheritance tax unfair? In a distant second place

(at 17%) was a general rejection of the principle, with respondents simply

saying that the government shouldn’t tax inheritance. That the inheritance tax

threshold kicks in at too low a level was one of the more common responses,

at 10%. Many of these respondents feel that it is unfair that rising house

prices are drawing people who are otherwise not ‘wealthy’ into the

inheritance tax bracket. "House

prices have risen to such a degree that the £325,000 limit affects too many

people and while ordinary folk lose 40%, rich and financially sophisticated

people will find ways around it." "Considering

average house prices currently, the sale after a death of a somewhat ordinary

property attracts this tax." "The

limit is too low for people living in the South where house prices are much

higher than in the North of the country." Why

is inheritance tax unfair? That the 40% inheritance

tax rate is too high is also a source of unfairness for 9% of respondents. "If

an average family works hard and saves it seems wrong that the benefits are

confiscated by such an onerous 40% tax." "Astronomical

rate of tax for £325,000, it should be tiered so the more you inherit the

more tax you pay." "40%

is too high to take from a grieving family and their hard earned

earnings." Why

is inheritance tax unfair? One in nine (11%) are

critical of what they see as a penalising aspect of inheritance tax – that it

punishes those who choose to save in order to pass on a nest egg when they

die, rather than simply spending all the money while they live. "It

is a tax on those who budgeted for their future and that of their families,

often going without." "It's

double taxation, a punishment for being financially responsible and totally

immoral." "People

work hard, save and go without to leave as much as possible to loved ones

only to have a part of it deducted. Others who have not made the effort and

taken from the tax payer have nothing taken away." Why

is inheritance tax unfair? Separately, as can be seen

in some of the examples above, there is a noticeable emotional seam cutting

across categories: that the money involved has been ‘hard earned’, either by

the respondent themselves or by their family members. Around one in seven (15%)

brought this up when explaining why they think inheritance tax is unfair. 23 November 2023 Source:

https://yougov.co.uk/politics/articles/47940-why-do-britons-think-inheritance-tax-is-unfair

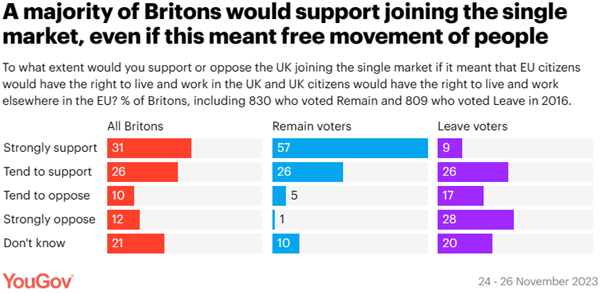

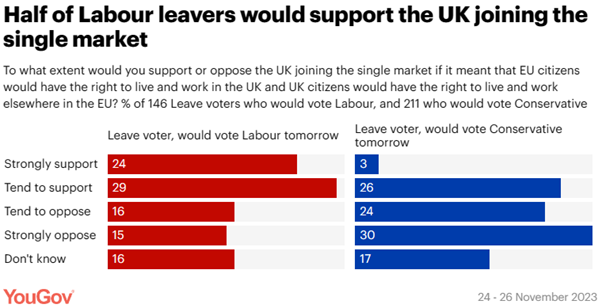

822-825-43-08/Polls Britons Support Rejoining

The Single Market, Even If It Means Free Movement

Seven

in ten Britons support a closer relationship with the EU than we have now As we approach the fourth

anniversary of Brexit, 52% of Britons now believe that the UK leaving the EU

was the wrong decision. The Labour party – likely to form the next government

– have so far resisted calls to move towards rejoining the single market,

despite pressure from some businesses who say this could improve the

situation. Joining the single market

would allow for the free movement of goods and services between the UK, the

EU and other non-EU countries who are member of the single market, like

Norway and Lichtenstein. However, this would also likely mean agreeing to the

free movement of people between the UK and the EU – a frightening prospect

for Keir Starmer’s Labour given the role of immigration in driving the Leave

vote. But is this fear justified?

Leave

voters backing Labour are keener on joining the single market As could be expected,

Remain voters are more likely to be supportive of joining the single market

than Leave voters. More than eight in ten Remain

voters (83%) would support doing so, compared to around a third (35%) of

Leave voters, who tend to be opposed (45%). YouGov’s latest Westminster voting intention poll has about 18% of Leave voters backing

Labour if there were an election tomorrow, with 29% supporting the

Conservatives and 13% Reform UK. Our data shows that Labour

committing to a return to the single market might not prove as alienating as

Starmer may fear. Of Leavers who would back Labour in an election tomorrow,

53% would support the UK joining the single market, even if this meant allowing

the free movement of people, with three in ten opposed (31%). By contrast, Leave voters

intending to back the Conservatives generally oppose a return to the single

market (54%), although a minority of 29% support doing so.

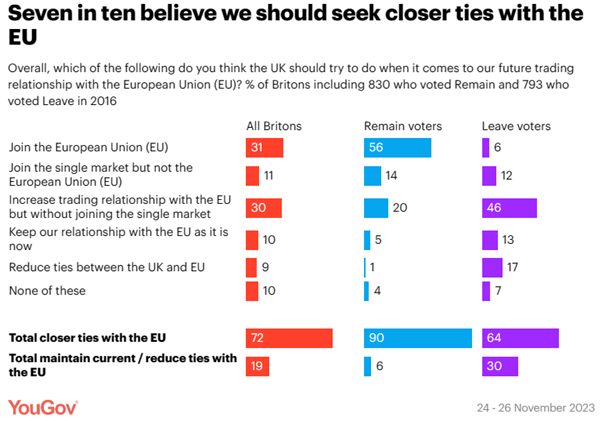

Britons

want closer ties with the EU Whilst Labour has so

far ruled out rejoining the single market, Starmer has asserted his intention to

build closer ties with the EU, pledging to try and establish closer trading

ties with if Labour win at the next election. In general, Britons favour

building closer ties with the EU. Seven in ten Britons (72%) want to see the

UK have closer ties with the EU in some form or another, including a majority

of both Remain (90%) and Leave (64%) voters. By contrast, one in five (19%)

favour the UK maintaining the status quo or further reducing ties with the

EU. The most popular proposals

for the UK’s future relationship with the EU are rejoining the European Union

(31%) and increasing the trading relationship with the EU without joining the

single market (30%). A further one in nine (11%) want to join the single

market, but not the EU. Of the options offered,

most Remain voters favour joining the EU (56%), while those who voted Leave

are instead generally in favour of increasing the amount of trade we do with

the EU without joining the single market (46%).

29 November 2023

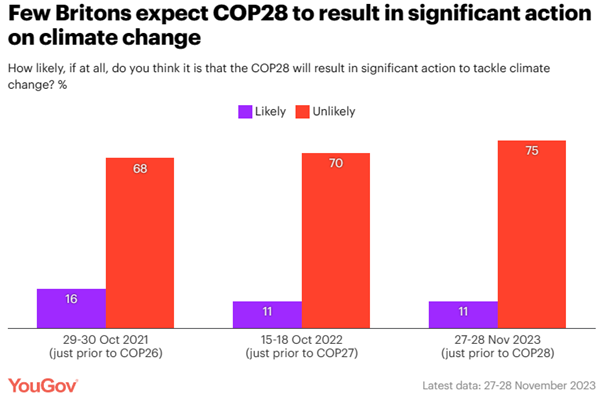

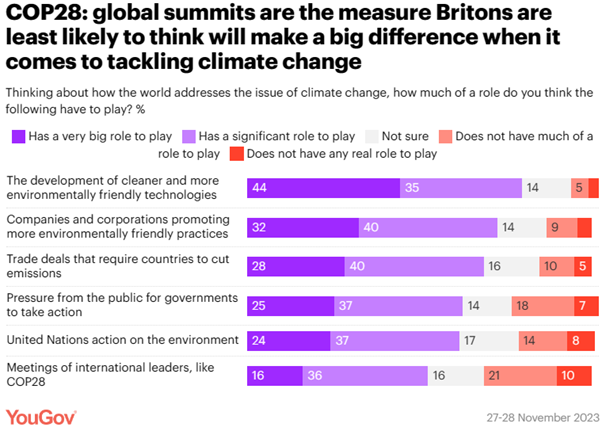

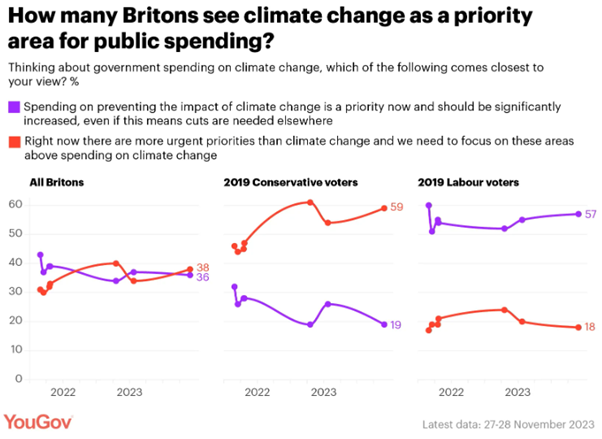

822-825-43-09/Polls Just 11% Of Britons Think

COP28 Will Result In Significant Action On Climate Change

Britons

are split on whether climate change spending should be a priority at the

current time The 28th United Nations

Climate Change conference from 30 November - 12 December in Dubai – dubbed

COP28 – will see world leaders gather to discuss how the world is tackling

rising temperatures as we come to the close of the hottest year on record.

Very few are paying

attention to the conference, with 81% saying they have heard little or

nothing about it just two days prior to the start of the conference. When asked about what role

different developments can have when it comes to addressing climate change,

meetings of international leaders like COP28 are seen as being the least

influential of all the measures tested. While 79% say the development of

cleaner and more environmentally friendly technologies can play a “very big”

or “significant” role in tackling climate change – the most important

according to the public – just half (52%) say the same of conferences like

COP28. Measures such as companies

promoting more environmentally friendly practices (72%), trade deals that

require countries to cut emissions (68%), pressure from the public for

governments to take action (62%) and United Nations action (61%) are all

likewise seen to have a bigger role than conferences such as COP28.

Despite a distinct lack of

enthusiasm for COP28, Britons remain worried about climate change (63% are

currently very or fairly worried), but are cautiously optimistic that there

is still time to tackle the issue, with 60% saying that we can still avoid the

worst effects if we make drastic changes. However, this does not

translate into public support for government spending on climate change. In

fact, the British public are split when it comes to whether climate change

spending should be prioritised – 36% say spending on climate change should be

a priority now, and should be increased, even if this means cuts elsewhere,

while 38% say that there are other priorities for government spending that

are more urgent than climate change. While Rishi Sunak may have

hoped to see his diluting of some net zero policies in September would shift

the dial on whether people see climate change spending as a priority, the

figures do not appear to bear this out. The results are largely similar to our

previous survey in January, when 37% saw climate change as the priority but

34% wanted to priorities other spending areas.

Results for this measure

vary drastically according to political persuasion – 2019 Conservative voters

are far more likely to say that there are other priorities right now (59%),

while almost the same proportion (57%) of Labour voters feel that climate change

spending should be seen as a priority at the current time and should be

increased. 30 November 2023

822-825-43-10/Polls Despite Pressures Facing

Young Families Today, Most Parents Take Precious Moments To Play With Their

Babies

For just over one in 14

(7.4%) of these babies, most of those daily interactions will be with their

father, who is their primary caregiver. Just 20 years ago, only one in 1,000

(0.11%) of nine-month-olds were cared for primarily by their dad at this age. The first report from the

Children of the 2020s study,

published today by the UK Department for Education (DfE) and led by UCL in

partnership with Ipsos and the universities of Cambridge and Oxford, and

Birkbeck, University of London, revealed that these home activities are

having positive effects on babies’ understanding of common words, like

‘ball’, ‘bye-bye’ and ‘mummy’, as babies that played more with caregivers

understood more words at this age. Overall, nine-month-olds

understood an average of 14 out of 51 common words. This was similar to

pre-pandemic norms, despite added pressure on today’s families. The findings also showed

that parents are navigating significant challenges in their babies’ first

months, with a quarter facing at least some financial strain and around a

fifth reporting seeking help from a doctor for feelings of depression since

the birth of their child. Commissioned by the DfE,

Children of the 2020s is following more than 8,500 families and their babies,

born in England between September and November 2021. It is the first

long-term, nationally representative study of babies since the UK Millennium

Cohort Study was launched more than 20 years ago. Children of the 2020s will

follow families for at least the first five years of their children’s lives,

shedding new light on the factors that can influence early years development.

The first survey took place when the babies were, on average, nine and a half

months old. The first findings from

the study paint a picture of a new generation of infants and their families. Today’s

parents

Family

finances

Childcare

Screen

use

Play

and language development

Access

to healthcare services

COVID-19

A Department for Education (DfE) spokesperson said: The

department commissioned this research to better understand early childhood

development factors which will help shape policy decisions. We are encouraged

by many parents engaging in activities like reading and play, recognising its

importance in early development. 20 November 2023

822-825-43-11/Polls More Than Two In Five

Britons Worry About How Much Christmas Is Going To Cost

The

cost of Christmas

The

economy and cost of living 55% of Britons expect the

economy to worsen over the next 12 months, 19% think it will improve. This

gives a net score of -36 which is very similar to last month (-34) and the

start of the year (-33 in January). When asked about

difference facets of life in Britain there is a lot of pessimism around –

especially on the NHS and cost of living. 66% expect the cost of living in

Britain to get worse in the next few years and 64% say the same about the

NHS.

Gideon

Skinner, Head of Political Research at Ipsos, said: The

rate of inflation may be falling, but Britons are still feeling its impact.

Most people are still pessimistic about the cost of living over the

next few years, and even Christmas does not escape. Even though most

people are still looking forward to the festivities, over 4 in 10 are worried

about its cost – with young people, renters and women in particular feeling

the pressure. Ahead of the Autumn Statement the Prime Minister and Chancellor

have hit their pledge to halve inflation, but will know they will also need

to deliver on their other targets to grow the economy and reduce people’s

financial insecurities over the cost of living to change the public mood. 21 November 2023 Source:

https://www.ipsos.com/en-uk/more-two-in-five-britons-worry-about-how-much-christmas-is-going-to-cost

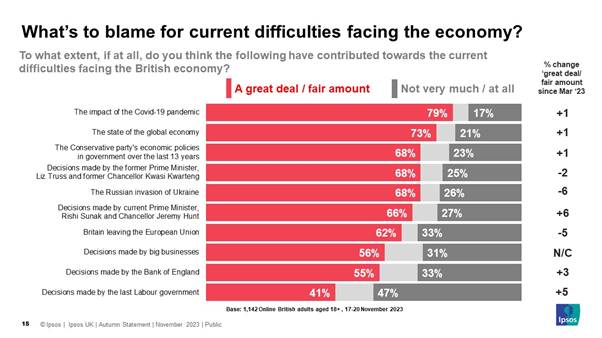

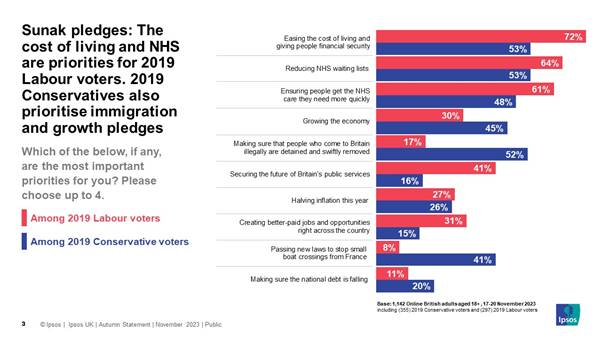

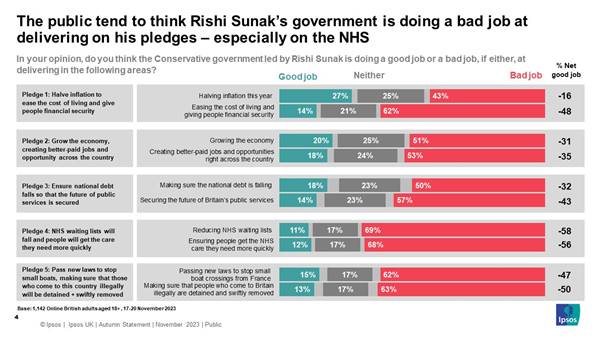

822-825-43-12/Polls Do The Public Praise Or

Blame Rishi Sunak And Jeremy Hunt When It Comes To Inflation

Who

do the public credit for falling inflation? When asked how far various factors have contributed

to falling inflation, we find the public are split on the role of Rishi Sunak

and Jeremy Hunt. 46% think they have contributed a great deal or fair amount

to falling inflation and 43% say they have had not very much impact or have

made no contribution at all. Decisions made by the

Bank of England (60%) and the state of the global economy generally (58%) are

seen to have contributed more.

The

Conservatives and the economy

Prime

Minister Rishi Sunak's pledges Overall, the public

continue to think Sunak’s pledges around easing the cost of living and giving

people financial security (61%), reducing NHS waiting times (55%) and

ensuring people get the NHS care they need more quicky (52%) are most

important to them. Although 2019 Conservative voters also rank pledges around

illegal immigration and economic growth as important.

The public also still

think Sunak’s government are performing badly against the pledges that are

most important to them. 62% think his government are doing a bad job easing

the cost of living, 69% think it is doing a bad job reducing NHS waiting

lists, 68% say the same about ensuring people get the NHS care they need more

quickly.

On the other hand, given

recent inflation figures, 27% now think Sunak’s government has done a good

job halving inflation this year (+13 points from September) but 43% still

think they have done a bad job (down 14 points in the same time period). Ipsos

Director of Politics Keiran Pedley said of the

findings: These

findings show that there is some improving public goodwill towards Rishi

Sunak and Jeremy Hunt in light of falling inflation but this has not yet led

to a fundamental reassessment of the government’s record on the economy.

Almost half think Sunak and Hunt have contributed a great deal or fair amount

towards falling inflation. However, 6 in 10 still think this government is

doing a bad job easing the cost of living and two-thirds think Sunak and

Hunt’s actions have contributed towards difficulties facing the economy in

the first place. 24 November 2023

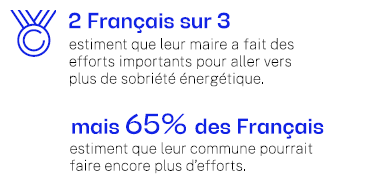

822-825-43-13 /Polls 58% Of French People Admit

That They Could Make More Effort To Reduce Their Energy Consumption

Energy

sobriety, a key issue at both the national and local levels

At

the local level, mayors themselves are directly affected by the energy

crisis. A significant proportion of them have

had to postpone or abandon projects due to rising energy costs (31%, 57% in

large cities). In fact, it is the 2nd

highest concern of mayors for their municipality (41% cite it

as one of their 3 main concerns) behind

security (43%). In municipalities with more than 2000

inhabitants, energy sobriety even comes in 1st place (62% cite it as one of

their 3 main concerns, 78% in municipalities with 30,000 inhabitants or

more). For their part, the French

recognise the investment of their mayors and municipal teams (66%) in their

municipality, but believe that it is possible to do more (65%), especially in large

cities (73%).

On

the side of mayors and citizens alike, new habits to move towards more

sobriety Most

French people say they have made efforts to reduce their energy consumption. On

average, they adopted 2.5 new actions in 2023 to reduce their consumption

(out of a list of 11 actions to reduce their consumption identified by Enedis

and Ipsos). For example, 30% say they have started to turn down the heating

to 19° at home when they did not do so before, and 28% have started to turn

off all their appliances on standby when they are not in use. At the same

time, more than three-quarters of them

monitored their electricity consumption more closely (78%).

However, despite their recognized effectiveness, actions such as insulating

the home and using public transport remain the least adopted because of the

constraints they impose. In addition, the

majority of French people recognise that they could make more of an effort to

reduce their energy consumption (58%).

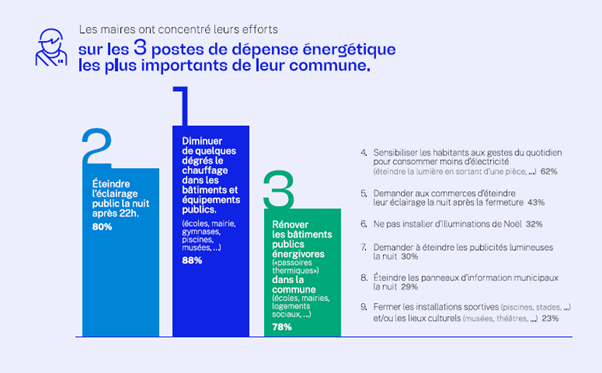

For

their part, mayors have implemented an average of 4.7 measures

to reduce their municipality's energy consumption (out of 9 proposed

measures). However, many French people are not well informed about the

actions put in place by their mayor. The

most common municipal actions were to reduce heating in public buildings

(88%), to turn off public lighting after 22 p.m. (80%) and to renovate

municipal buildings (78%). On the other hand, few have

switched off municipal billboards at night (just under half of the

municipalities concerned), or asked to turn off illuminated advertisements at

night (just under half of the municipalities concerned as well). For their

part, the French are in favour of most

energy sobriety measures, with the exception of those that

involve giving up Christmas lights or closing sports and cultural spaces

(measures put in place by 32% and 23% of municipalities respectively).

Turning off the lights after 22 p.m. is also much less popular in large

cities than in rural areas.

Difficulties

in moving towards more effective sobriety at the municipal level, partly

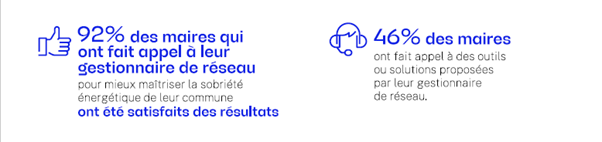

linked to a low use of the services made available Of the mayors who have

made energy sobriety an important objective for their municipality (83%),

most have encountered difficulties in achieving it (91%). They most often say they have faced financial (77%)

and regulatory (49%) constraints, but also a lack of technical expertise and

knowledge (44%). In addition, while a very large majority of

mayors believe that the measures taken have had an impact in terms of energy

savings for the municipality, only 1

in 5 consider that this impact has been "strong" (19%). In this context,

electricity distribution stakeholders are seen as essential partners in

helping mayors control energy consumption. Thus, 92% of mayors who called on their network operator to better

control the energy sobriety of their municipality were satisfied with the

results. So far, however, only a minority of mayors have used their services

(46%).

28 November 2023

822-825-43-14/Polls First Anniversary Of Chat

GPT, 77% Of French People See This Tool As A Revolution

A significant increase in awareness and use of Chat GPT One year after the launch of Chat GPT, a strong increase in

its notoriety

A

rapid craze for Chat GPT, and a use that has become regular for a significant

part of respondents

Significant

attractiveness potential The

French are interested in a wide variety of services offered by Chat GPT or

similar tools

The

shared feeling of an ongoing revolution, with multiple consequences The

French are unanimous on the impact of Chat GPT and AI tools in general

The

perception of the consequences of this revolution varies from one field to

another

A

particularly important impact for the world of work Important

changes coming in the world of work

French

people divided on the impact of AI tools in the workplace

The

mastery of AI is becoming an important issue for the coming years

As

a result, a majority of opinion in favor of teaching on the use of AI

01 December 2023 NORTH

AMERICA

822-825-43-15/Polls Americans More Upbeat

About Future Social Security Benefits

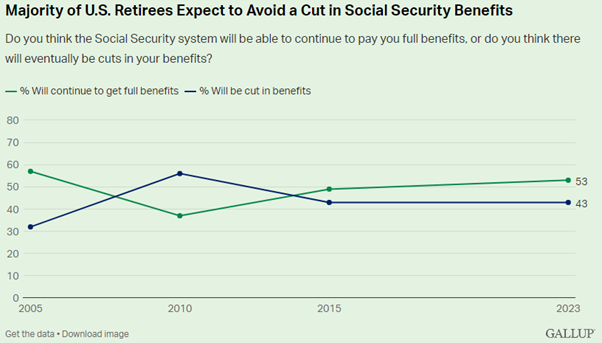

Further, 53% of current

U.S. retirees believe they will continue to receive their full Social

Security benefits, up from 37% in 2010 and 49% in 2015. Forty-three percent

of retirees currently believe their benefits will eventually be cut.

Despite the improved

outlook among both retirees and nonretirees, neither group is any more upbeat

about the future of their Social Security benefits now than they were in the

1980s, 1990s and early 2000s. These results are based on

Gallup polling conducted in June and July, including a sample of more than

1,300 nonretirees and over 600 retirees. Social Security’s future

has been a topic of debate for decades. The system is expected to be able to

continue to pay full benefits to recipients through 2033 if no changes are

made to the system. In 2034, the system is projected to be able to pay 80% of

benefits to recipients. President Joe Biden

brought up the future of the system in his 2023 State of the Union speech and

appeared to receive support from both parties to protect Social Security from

near-term cuts in federal budget negotiations. It is unclear to what extent

this recent display of bipartisan consensus on the issue has influenced

Americans’ opinions about their future Social Security benefits. Greater optimism about the

future of Social Security in recent years comes at a time when Americans’ satisfaction with the Social

Security system has

also been higher. Nonretirees

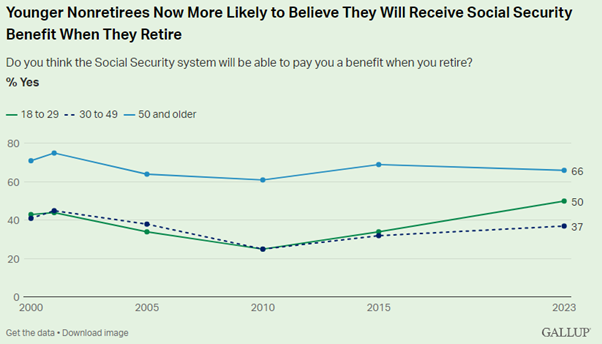

Aged 30 to 49 Not Counting on Getting Benefits Expectations for receiving

Social Security benefits vary by age among nonretirees. As might be expected,

older nonretirees are fairly confident, with 66% of those aged 50 and older

expecting to get benefits. But it is the next oldest

age group, rather than the youngest that is furthest away from retirement,

that is least confident. Thirty-seven percent of nonretirees between the ages

of 30 and 49 believe they will get Social Security benefits, while 61% do not. The youngest adults, those

aged 18 to 29, are divided -- 50% think they will get benefits, and 48% do

not. Compared with 2015, older

and middle-aged nonretirees’ expectations about receiving benefits are not

meaningfully different now. Meanwhile, the youngest age group is

significantly more likely today (50%) than in 2015 (34%) to predict they will

receive benefits.

The youngest nonretirees

today are more optimistic about getting Social Security benefits than that

age group has been at any point since 2000. Today, the cohort of 18-

to 29-year-olds consists of the youngest millennials and oldest members of

Generation Z. In 2015, the 18-to-29 age group included only members of the

millennial generation. Many of those people have now aged into the 30-to-49

age bracket and retain more pessimistic views about Social Security. Politics

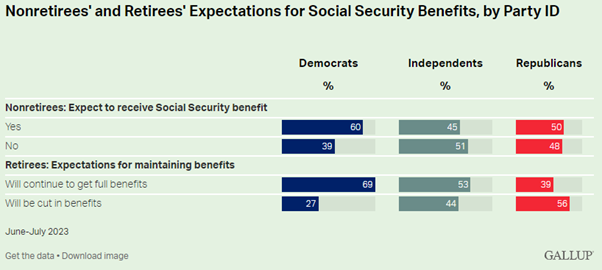

Modestly Related to Social Security Expectations Democratic nonretirees

(60%) are more likely than Republican (50%) and independent (45%) nonretirees

to expect to receive Social Security benefits when they retire. There are larger party

differences in current retirees' faith that their Social Security benefits

will be maintained. Democratic retirees (69%) are substantially more

confident than Republican retirees (39%) about avoiding cuts to their Social

Security benefits. A slim majority of retired independents, 53%, expect to

continue receiving their current benefits.

Party differences on these

items have been inconsistent over time. For example, the party gap in

nonretirees’ belief that they will get Social Security payments is smaller

this year than in 2015 (when the difference was 22 percentage points, 59% for

Democrats and 37% for Republicans), larger than it was in 2001 and 2010 when

there were essentially no party differences, and about the same as it was in

2000 and 2005. When gaps have existed, those who identify with the party of

the incumbent president have typically been more positive about the future of

Social Security. Americans

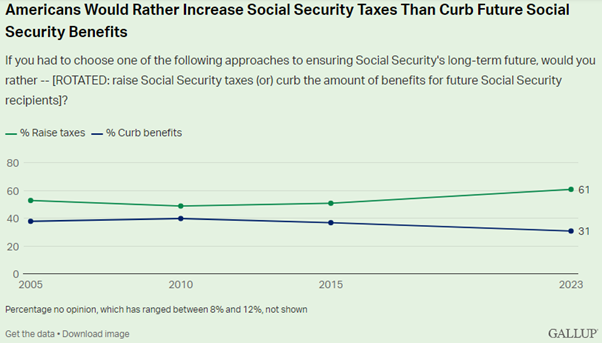

Prefer Higher Taxes to Benefit Cuts Discussions about

preserving Social Security in the future largely center on raising payroll

taxes of current workers that fund the system, curbing benefits for current

and/or future recipients, and possibly raising the age at which retirees can

receive full Social Security benefits (currently 67 years old). U.S. adults

have typically favored raising Social Security taxes as opposed to curbing

benefits as a means of ensuring the long-term future of the system, but they

are more likely to favor tax increases now than in the past. Sixty-one percent of

Americans say they would prefer the government raise Social Security taxes,

while 31% would rather the government curb Social Security benefits. In three

previous surveys in 2005, 2010 and 2015, the margin in favor of increased

taxes has been smaller than the 30-point gap seen this year, ranging from

nine to 15 points.

Majorities of Democrats

(69%) and independents (53%) prefer raising taxes to beef up Social Security,

while 39% of Republicans agree. Fifty-six percent of Republicans prefer the

government curb Social Security benefits for recipients, a view shared by 44%

of independents and 27% of Democrats. Democrats are more likely

today than in the past to favor increased taxes (averaging 59% between 2005

and 2015), while Republicans are now more likely to favor curbing benefits

(averaging 45% in those years). Bottom

Line While policymakers may not

share Americans’ increasingly positive outlook, U.S. adults are more

optimistic about the future of Social Security, at least as it pertains to

them, than they were in Gallup’s most recent surveys in 2010 and 2015. Much

of this increased optimism comes from the youngest Americans, who are roughly

four decades away from retirement. Nonretirees are more

likely to believe that a 401(k) plan will be a major source of income in their retirement than to say this about Social

Security. However, among current retirees, Social Security is the clear

leader over other retirement funding sources, underscoring the importance of

the system to U.S. seniors. The subject of Social

Security has been an issue in the 2024 presidential campaign. Most candidates

have pledged to keep the system largely intact, while some have offered

modest proposals to help ensure the system’s longer-term viability. 08 December 2023 Source:

https://news.gallup.com/poll/546890/americans-upbeat-future-social-security-benefits.aspx

822-825-43-16/Polls Most Of Biden’s Appointed

Judges To Date Are Women, Racial Or Ethnic Minorities – A First For Any

President

Nearly two-thirds of the federal judges President

Joe Biden has appointed so far are women, and the same share are members of

racial or ethnic minority groups, according to a Pew Research Center analysis

of statistics

from the Federal Judicial Center.

To put Biden’s judicial

appointments into historical context, we examined how his appointed judges to

date compare with those of other presidents at the same point in their

tenures, going back to Dwight D. Eisenhower in the 1950s. This analysis

begins with Eisenhower because he was the first president to be sworn in to a

first term on the modern inauguration date of Jan. 20. As of Nov. 5 – exactly a

year before the 2024 presidential election – Biden had appointed 145 judges

to the three main tiers of the federal judicial system: the district courts,

the appeals courts and the U.S. Supreme Court. Women accounted for just over

66% of those judges (95 of 145). The 95 women judges Biden

had appointed as of Nov. 5 far exceed both the number and share any other

president had appointed at the same point in their term. For example,

then-President Donald Trump had appointed 36 women judges by the same point

four years ago (24% of his total at the time), while then-President Barack

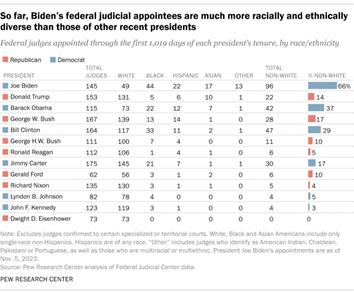

Obama had appointed 54 women judges (47% of his total at the time). The pattern is similar

when it comes to judges who are racial or ethnic minorities. Nearly

two-thirds of the judges Biden had appointed as of Nov. 5 (96 of 145, or just

over 66%) are Black, Hispanic, Asian American or members of another racial or

ethnic minority group. That is far more than any other president had

appointed at the same point in their tenure. Trump, for instance, had

appointed 22 minority judges by the same stage (14% of his total at the

time), while Obama had appointed 42 (37% of his total at the time). Combining gender with race

and ethnicity, women who are Black, Hispanic, Asian or part of another racial

or ethnic minority group account for 42% of the judges Biden had appointed as

of Nov. 5 (61 of 145). They include Biden’s sole appointee to the U.S. Supreme

Court, Justice Ketanji Brown Jackson, the first Black woman to serve on the

nation’s highest court.

How

does Biden compare with other presidents in total judges appointed?

Biden does not especially

stand out in terms of the overall number of federal judges he has appointed

so far. He appointed 145 judges through Nov. 5 – fewer than Trump had

appointed at the same point in his presidency (153), but more than Obama had

(115). Overall, Biden’s appointed

judges include one Supreme Court justice (Jackson), 36 appeals court judges

and 111 district court judges. Trump, by comparison, had appointed two

Supreme Court justices by the same point in his tenure (Neil Gorsuch and

Brett Kavanaugh), in addition to 43 appellate judges and 110 district judges. Both Biden and Trump

appointed some people to multiple judgeships. Biden, for example, appointed

Jackson to an appeals court position before elevating her to the Supreme

Court. In this analysis, these judges are counted separately for each

position, but only once in each president’s total. How

many active federal judges were appointed by Biden? Another way of looking at

the effect that each president has had on the federal judiciary is to

evaluate the share of currently active judges who were appointed by

that chief executive.

As of Nov. 5, there were

798 active federal judges serving in the 91 district courts and 13 appeals

courts governed by Article III of the U.S. Constitution, as well as on the

Supreme Court. Biden had appointed 18% of those judges. Of the federal judges who

were active as of Nov. 5, larger shares were appointed by other recent

presidents. Trump appointed 28% of active judges, while Obama appointed 31%

and George W. Bush appointed 16%. Not surprisingly, relatively few judges who

are still active today were appointed by presidents who served more than two

decades ago – including Bill Clinton (4%), George H.W. Bush (1%) and Ronald

Reagan (1%). How

many active federal judges were appointed by Democratic versus Republican

presidents? The current federal

judiciary is closely divided between appointees of Democratic presidents, who

comprise 54% of all active judges, and those chosen by Republican presidents,

who account for 46%. However, the breakdown

varies by type of court. More than half of active judges in district courts

were appointed by Democratic presidents (56%), while a smaller share (44%)

were appointed by GOP presidents. The reverse is true in the appeals courts,

where 53% of active judges were appointed by Republican presidents and 47%

were appointed by Democrats. The Supreme Court consists of six justices

appointed by Republican presidents and three justices appointed by Democrats,

a 67%-33% split. 4 December 2023

822-825-43-17/Polls Americans’ Views Of The

Israel-Hamas War

A new Pew Research Center

survey, conducted Nov. 27-Dec. 3 among 5,203 adults, finds sizable partisan

and age differences on these questions, as well as about many other aspects

of the two-month-old war:

Related: About

half of Republicans now say the U.S. is providing too much aid to Ukraine The war between Israel and

Hamas has spurred a number of concerns among Americans, including the

possibility of a wider regional conflict and terror attacks in this country: Bipartisan

concern over violence against Jews in the U.S.

Another 31% say they are

somewhat concerned about this; just 19% have little or no concern about

increasing violence against American Jews. Nearly identical shares of

Democrats (49%) and Republicans (48%) say they are extremely or very

concerned about the possibility of increasing violence against Jews in this

country. Democrats

more likely than Republicans to express concern about increased violence

against U.S. Muslims About half of Democrats

(53%) say they are extremely or very concerned about the possibility that

violence against Muslims in the U.S. will increase, compared with 22% of

Republicans. While about half of

Republicans (53%) say they are at least somewhat concerned

about the prospect of rising violence against Muslims in the U.S., 46% say

they are not too concerned or not at all concerned about this. That compares

with 15% of Democrats. (Explore this further in chapter 2.) Biden

administration’s response to Israel-Hamas war viewed more negatively than

positively

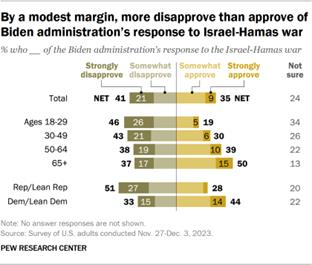

Roughly a third of adults

(35%) approve of the Biden administration’s response to the Israel-Hamas war,

while 41% disapprove and 24% are not sure.

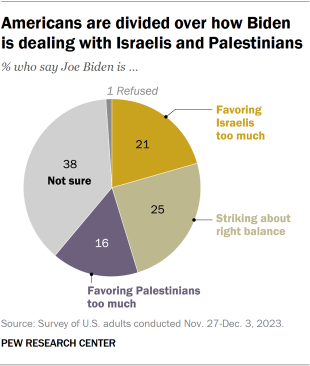

Americans generally differ

over whether President Joe Biden is striking the right balance in dealing

with the Israelis and Palestinians (25%), favoring the Israelis too much

(21%), or favoring the Palestinians too much (16%). Nearly four-in-ten adults

say they are not sure how Biden is handling this. (Explore this further in chapter 3.) Public

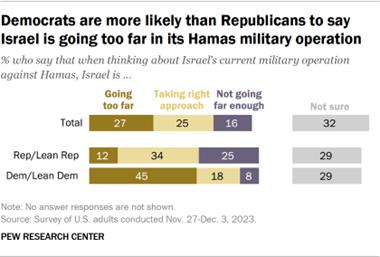

is divided in views of Israel’s military operation against Hamas Americans also differ over

Israel’s ongoing military operation against Hamas, with nearly a third (32%)

not sure.

About a quarter (27%) say

Israel is going too far in its current military operation, while about as

many (25%) say it is taking the right approach; 16% of Americans say Israel

is not going far enough militarily. More than four-in-ten

Democrats (45%) say Israel is going too far in its military operation against

Hamas, compared with 12% of Republicans. There also are age

differences in these opinions, with younger Americans more likely than older

age groups to say Israel is going too far. Other

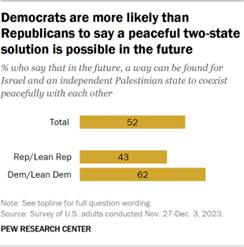

important findings

About

half of Americans say a two-state solution is still possible in the future. Currently,

52% say that, in the future, a way can be found for Israel and an independent

Palestinian state to coexist peacefully; 45% say this is not possible.

Democrats (62%) are more likely than Republicans (43%) to say that a

peaceful, two-state arrangement is possible. About

a quarter of Americans (26%) are following the Israel-Hamas war extremely or

very closely. Another 37% say they are

following news about the war somewhat closely, while 36% are following not

too or not at all closely. As with most international

news events, younger adults are following developments in the conflict less

closely than are older people. About a third of adults ages 50 and older

(35%) say they are following the war extremely or very closely, roughly

double the share of those under 50 (18%). Americans

who have been paying greater attention to news about the war are more likely

than others to have an opinion about the administration’s response and to

approve of it. Both Democrats and Republicans

who have been following the war extremely or very closely give the

administration much higher ratings than do those who have been following the

conflict less closely. 8 December 2023 Source:

https://www.pewresearch.org/politics/2023/12/08/americans-views-of-the-israel-hamas-war/

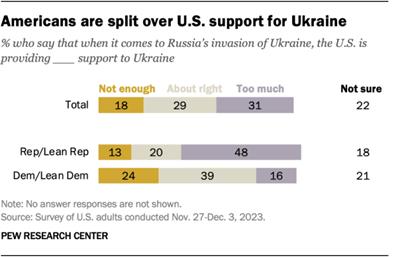

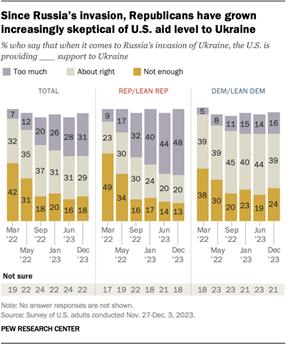

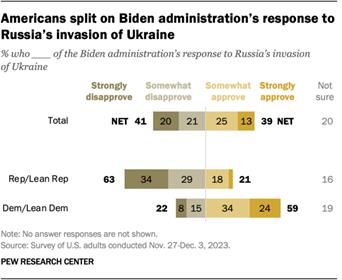

822-825-43-18/Polls About Half Of Republicans

Now Say The U.S. Is Providing Too Much Aid To Ukraine

A new Pew Research Center

survey, conducted Nov. 27 to Dec. 3, 2023, among 5,203 members of the

Center’s nationally representative American Trends Panel, finds that:

Public attention to the

Russia-Ukraine conflict is little changed in recent months. Six-in-ten

Americans, including similar shares of Republicans (62%) and Democrats (61%),

say they follow news about the invasion at least somewhat closely. How

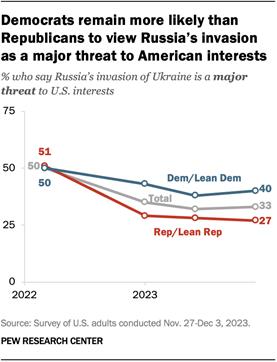

much of a threat to the U.S. is Russia’s invasion of Ukraine?

A third of Americans say

Russia’s invasion of Ukraine is a major threat to U.S. interests. A similar

share (34%) say it is a minor threat, while 10% say it is not a threat. These views have changed

only modestly since June. But in March 2022, half of Americans said Russia’s invasion

posed a major threat to U.S. interests. As has been the case for

the last year, Democrats are more likely than Republicans to say Russia’s

invasion is a major threat (40% vs. 27%). But people in both parties are less

likely to say this now than in the early days of the war in March 2022. Views

of the Biden administration’s response to Russia’s invasion of Ukraine

Around four-in-ten U.S.

adults (39%) say they approve of the Biden administration’s response to

Russia’s invasion of Ukraine, while a similar share (41%) disapprove.

Two-in-ten say they are not sure. Disapproval of the

administration’s response has increased slightly (from 35% to 41%) since

June. A majority of Democrats

(59%) approve of the administration’s response, while 22% disapprove. In

contrast, a slightly larger majority of Republicans (63%) disapprove of the administration’s

response, while 21% approve. In both parties, somewhat

larger shares now disapprove of the Biden administration’s response to the

invasion than did so in June, when 57% of Republicans and 16% of Democrats

said they disapproved. 8 December 2023

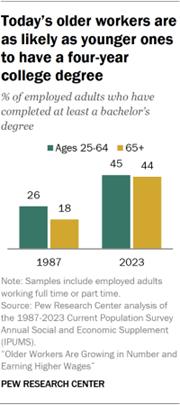

822-825-43-19/Polls Older Workers Are Growing

In Number And Earning Higher Wages

Linked to their higher

wages, today’s older workers are different from older workers of the past in

other important ways:

Continuing a longstanding

trend, older workers are more than twice as likely as younger workers to be

self-employed (23% are, compared with 10% of workers ages 25 to 64). Taking all these factors

into account – more older adults in the workforce, working longer hours with

higher levels of education and greater pay per hour – older workers’ overall

contribution to the labor force has grown quite a bit. In 2023, they accounted

for 7% of all wages and salaries paid by U.S. employers. That is more than

triple the share in 1987 (2%). A recent Pew Research Center survey found that workers ages 65 and older

are more satisfied with their jobs overall than younger workers. They’re also

more likely to say they find their job enjoyable and fulfilling all or most

of the time, and less likely to say they find it stressful. In addition to the key

findings covered in this overview, the two sections that follow provide more

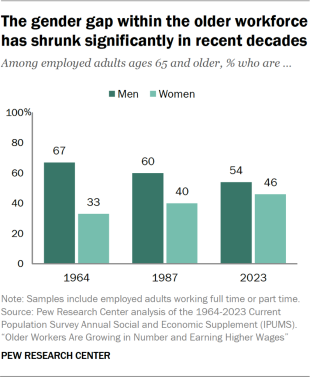

detail on: Gender,

race and the older workforce The demographic makeup of

the U.S. workforce overall has changed substantially in recent decades. Some

of those changes reflect broader societal shifts – like more women entering

the labor force and going to college. Others are tied to the changing racial

and ethnic makeup of the country. These trends can be seen across the older