|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 783 Week: February

20 – February 26, 2023 Presentation:

March 03, 2023 Inside

Afghanistan: Record Numbers Struggle to Afford Basics 11 UAE

Parents Have High Concerns over Their Child’s Exposure To Inappropriate

Online Content 13 Health

Insurance Coverage for Nigerians Still Abysmal; An Urgent Call For New

Strategy. 15 Labour

Voters More Wary about Politics of Child’s Spouse 17 Most

Brits Expect Recession, As Consumer Confidence Dips To Six-Year Low 19 Half

of Leave Voters Doubt Johnson Can Secure New Brexit Deal 21 Few

Believe the Government's Explanation of Why Parliament Is To Be Suspended 23 Brits

Oppose Parliament Suspension By 47% to 27% 24 5

Facts about the Abortion Debate In America 25 U.S.

Concern about Climate Change Is Rising, But Mainly Among Democrats 28 Most

Americans Say Science Has Brought Benefits to Society and Expect More to

Come 31 Parents'

Concern about School Safety Remains Elevated 34 As

Labor Day Turns 125, Union Approval Near 50-Year High 36 Americans'

Satisfaction with U.S. Education at 15-Year High 38 Most

Cannabis Consumers Use on a Weekly Basis or More 41 Ride-Sharing

App Uber Overtakes Taxis as Preferred Private Transport Service 43 Rising

Numbers of Australians Looking At Electric and Hybrid Vehicles for Their

Next Set of Wheels 45 Toyota

And Mazda Drivers Most Brand Loyal; Have The Luxury Brands Lost Their

Lustre? 48 Britons

Make Worst Tourists, Say Britons (And Spaniards And Germans) 50 Brazilians

Least Satisfied in Amazon With Environment 55 India

Ranks 9th on Happiness among 28 Global Markets: Ipsos Global Happiness

Survey 58 The

Biggest Beauty Influencer Isn’t Who You Think It Is 59 INTRODUCTORY NOTE This weekly

report consists of eighteen surveys. The

report includes four multi-country studies from different states across the

globe.

783-43-19/Commentary: Arab

Public Opinion Prefers China Over USA 11 Out Of 12 Surveyed Nations Hold That

View

This piece is

part of a four-part series published by the Middle East Institute

in cooperation with Arab Barometer analyzing the results of the seventh wave of the Arab Barometer surveys. Apart from Europe and the South

China Sea region, the Middle East and North Africa is one of the epicenters

for what the U.S. has termed “great power competition” especially between the

U.S. and China, although Russia also figures into the assessment. There is

particular sensitivity to China’s perceived economic inroads into the region

as it has surged to become its largest economic partner. Apart from China’s

dependence on imports of Gulf oil to meet its energy needs, China’s Belt and

Road Initiative (BRI) has expanded Beijing’s footprint from Oman in the east

to Morocco in the west. Based on Arab

Barometer’s Wave 7 raw favorability numbers, China’s

increased presence in the region appears to have paid dividends in terms of

its popular standing, especially in North Africa. Except for Morocco, where

favorability for the U.S. at 69% is marginally higher than China’s rating at

64%, the U.S. consistently lags behind China in the view of respondents to

the 12-country survey. The favorability gap is particularly notable in

Algeria, where China enjoys a 20-point edge over the U.S. at 67% vs. 47%. One

possible explanation for the broad disparity in favorability ratings for the

U.S. between Morocco and Algeria, of course, is widespread anger in Algeria,

and the converse in Morocco, over the Trump

administration’s December 2020 decision to recognize Moroccan

sovereignty in the Western Sahara. The Arab Barometer seventh wave polling

was undertaken after that decision, between October 2021 and July 2022. But even in Tunisia and Libya,

where the U.S. has focused a great deal of effort in promoting positive

outcomes in their political transitions since the Arab Spring, China is

viewed far more favorably than the U.S. (in Tunisia by 50% vs. 33% and in

Libya by 49% vs. 37%). Skepticism over the U.S. intent in providing foreign

assistance appears to underlie unfavorable views of the U.S. Only 18% of

rural and 15% of urban Tunisians agreed that U.S. assistance is motivated by

a desire to improve people’s lives whereas a plurality of Tunisians (40%

rural and 44% urban) and a majority of Libyans (50% rural and 53% urban)

believe the U.S. uses its foreign assistance to gain influence. By contrast,

pluralities of Libyans (35%) and Tunisians (40%) saw Chinese objectives in

providing foreign assistance as aiding either economic development or

internal stability. One contributing factor in low U.S.

favorability ratings is likely the overhang of negative regional sentiments

toward U.S. policy in the Trump administration. Broad regional attitudes

toward Biden administration policies are notably higher than his

predecessor’s poll results. In Sudan, for example, a majority of Sudanese

(52%) consider Biden administration policies to be good or very good compared

to only 20% who viewed Trump policies in a positive light. In Morocco,

Biden’s approval stands at 46% vs. the 14% who viewed Trump favorably despite

the Western Sahara decision. Even among populations that continue to hold the

U.S. in low esteem, there has been improvement since the Biden administration

came into office. In Tunisia, 23% of those polled think that Biden’s policies

are good or very good as compared to Trump’s 10% while the similar comparison

in Palestine is 11% vs. 6%. In that regard, despite overall improvement in

attitudes toward Biden’s regional policies, the vast majority of Palestinians

clearly see little reason for optimism in U.S. policy toward their issues

since Biden came into office. Biden’s improved numbers also

reflect an uptick in popular perceptions of Biden’s foreign policy as

compared to Chinese President Xi Jinping’s policies. A majority of Sudanese

(52%) see Biden’s policies as good or very good compared to Xi’s 43%. In

Morocco, as well, the public holds generally more favorable attitudes toward

Biden (46%) as opposed to Xi (39%). Elsewhere in the region, including,

surprisingly, in Jordan and Lebanon, U.S. and Chinese policies are seen in

roughly equivalent terms (Jordan: Biden 28%/Xi 26%; Lebanon: Biden 31%/Xi

35%). And Xi is notably more popular with the publics in several countries,

including Algeria (Xi 53%/Biden 35%), Iraq (Xi 48%/Biden 35%), and Tunisia

(Xi 35%/Biden 23%). On economic relations, there is

clearly a region-wide desire to strengthen relations with global partners.

For both the U.S. and China, young people (18-29) generally favor the

economic relationships more than their older fellow citizens (30+). Even in

Tunisia, nearly 60% of young respondents favor closer economic ties to the

U.S, nearly equal to the 65% who would like to see closer economic ties to

China. Overall in the region, even in those countries that are generally

skeptical of ties to the U.S., there is a desire to seek stronger economic

links. In Iraq and Libya, for example, equal numbers of young people want to

strengthen economic ties to the U.S. and China. In several other countries,

including Morocco, Mauritania, and Sudan, young people clearly favored the

U.S. as an economic partner over China. Despite these seemingly solid

favorability numbers overall for the Chinese, however, a public diplomacy

professional in Beijing would clearly see warning signs in some of the Arab

Barometer measures of popular perceptions. In particular, there appears to be

a fairly high degree of ambivalence about their country’s economic relations

with China among the publics as compared to the U.S. Notably, there are

significant minorities in several of the countries, particularly among rural

and less-educated respondents, that would like to see economic links to China

reduced. In Lebanon, for example, 23% of respondents with a maximum secondary

education and a full third of rural respondents preferred to see economic

ties to China loosened. In Iraq, 23% of secondary educated and 21% of rural

respondents advocated for reduced economic relations with China, as well. There are a number of factors that

appear to contribute to the ambivalence about China as an economic partner.

In all of the countries surveyed, often by wide margins, the Chinese are seen

as the country that provides the lowest quality products. In Iraq, for

example, 69% of respondents thought that Chinese products were low quality as

compared to only 8% who thought of U.S. products that way. Similarly, in

Jordan, 64% of survey participants saw China as a producer of low quality

products compared to 7% who viewed U.S. products in that light. In the other

seven countries surveyed, a plurality of respondents all agreed that Chinese

goods were of low quality. Conversely, the U.S. and Germany were seen through

all of the nine countries surveyed as producers of the highest quality

products. Respondents who viewed Chinese products positively ranged from a

low of 8% in Algeria to a high of 18% in Libya. Similarly, Chinese companies were

held in generally low esteem as business partners and employers. For the most

part, respondents in the surveyed countries preferred businesses in either

the U.S. (Lebanon, Mauritania, Sudan) or Germany (Algeria, Libya, Morocco,

Tunisia) as contracting partners. Only in Iraq did the plurality (27%) of

respondents prefer Chinese companies as business partners. Integrity appears

to be a factor in that perception as respondents generally saw U.S. (Iraq,

Jordan, Lebanon, Morocco, Sudan) and German (Algeria, Mauritania, Tunisia)

businesses as least likely to pay bribes while Chinese companies lagged

behind. Likewise, U.S. (Iraq, Jordan, Libya, Mauritania, Morocco, Sudan) and

German (Algeria, Lebanon, Tunisia) businesses were deemed most likely to pay

their local employees top salaries with Chinese companies generally scoring

poorly in that regard. Arab Barometer’s Wave 7 surveys

straddled the outbreak of conflict between Russia and Ukraine, so we will

have to await Wave 8 to determine if Russia’s war of aggression will affect

regional attitudes toward Russia and Vladimir Putin. For the most part, views

of Russia and Putin in Wave 7 were not substantially different from views of

the U.S. and Biden or China and Xi. In fact, in a number of instances, views

of Russia and Putin closely approximated respondent attitudes toward China

and Xi. In Lebanon, Algeria, and Libya respondents rated Russian and Chinese

favorability in nearly identical terms (Lebanon: China-51%/Russia-52%;

Algeria: China-67%/Russia-66%; Libya: China-49%/Russia-49%) while in Iraq and

Tunisia, respondents rated Putin and Xi equally (Iraq: Putin-46%/Xi-48%;

Tunisia: Putin-34%/Xi-35%). Only in Morocco did U.S. favorability

significantly exceed Russia and China (U.S.-69%/China-64%/Russia-38%) while in

Jordan, the U.S. and China were rated equally ahead of Russia

(U.S.-51%/China-51%/Russia-39%). The same holds true as to the personal

favorability estimations for Biden, Putin, and Xi. Only Sudanese and Moroccan

respondents held a significantly more favorable view of Biden (Sudan:

Biden-52%/Xi-43%/Putin-34%; Morocco: Biden-46%/Xi-39%/Putin-26%). The same picture also holds among

the three competitors in economic favorability ratings. Only in Algeria did a

significantly higher number of respondents favor stronger economic ties to

Moscow as compared to the U.S. or China (Russia-55%/China-38%/U.S.-31%). In

Morocco and Sudan, respondents favored stronger ties to the U.S. (Morocco:

U.S.-42%/China-36%/Russia-28%; Sudan: U.S.-58%/China-48%/Russia-45%). Among

the other countries participating, there are few distinctions among the U.S.,

China, and Russia, although China is the preferred partner in Tunisia, Libya,

and Iraq. Trend lines may be somewhat more revealing. After enjoying a

significant rise in economic favorability during the Obama years (Wave 3 and

Wave 4), positive views of U.S. economic ties dropped significantly during

the Trump administration (Wave 5) but have now recovered somewhat in the

latest (Wave 7) survey. By contrast, both China and Russia saw drops in their

economic favorability ratings between Wave 5 and Wave 7, with China

experiencing a precipitate decline in its favorability rating in Jordan,

albeit from an extremely high 70% favorable to a still respectable 50%. Aside

from Tunisia, where its favorability rating essentially flat-lined from Wave

4 to Wave 7, Russia’s favorability has also declined between Wave 5 and Wave

7. A recurring theme in discussions

with interlocutors in the region is that the MENA countries will resist

becoming a battleground in a “great power competition” between the U.S.,

Russia, and China. Although there are clearly differences in how the three

competitors are viewed in the region, it’s also clear that public opinion in

the Arab Barometer Wave 7 survey echoes the views of political leaders that

they seek to maintain positive political and economic relations with all

three. As noted, the potential impact of Russia’s aggression in Ukraine on

MENA popular attitudes remains to be measured. But that variable aside,

unlike the post-World War II Cold War era, these populations will favor

strongly remaining non-combatants in any new cold war. (Arabbarometer) February 21, 2023 SUMMARY OF

POLLS

SUMMARY

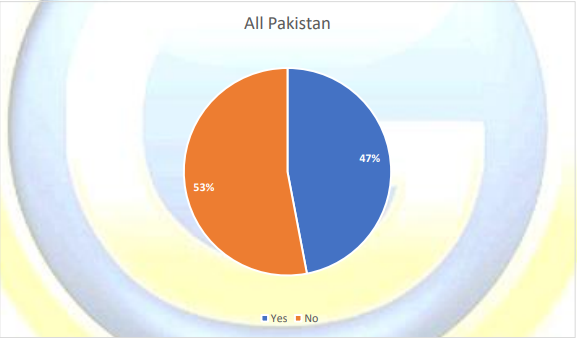

OF POLLS ASIA (Pakistan) 47% Pakistanis Say That They

Have Experienced The Lack Of Medicine While Visiting The Hospital In The Past

Year According to a survey conducted by

Gallup & Gilani Pakistan, 47% Pakistanis say that they have experienced

the lack of medicine while visiting the hospital in the past year. A

nationally representative sample of adult men and women from across the

country, was asked the following as a follow up question, “In the last twelve

months, have you experienced any of the following problems in a government

hospital/clinic? - Lack of medication?” 47% responded yes while 53% said no. (Gallup Pakistan) February 24, 2023 AFRICA (Nigeria) Political Party Logo

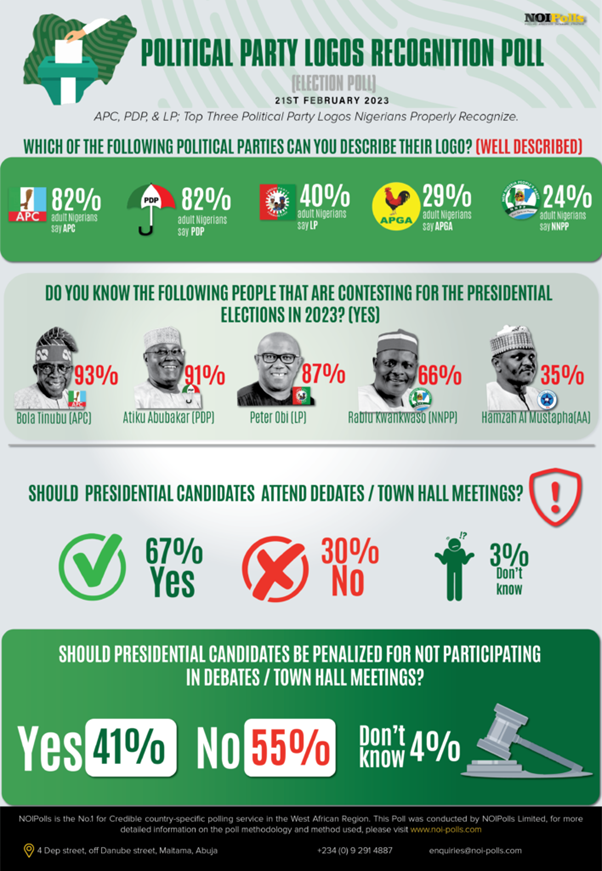

Recognition Poll (Election Poll) A new public opinion poll conducted

by NOIPolls has revealed that the top three political party logos properly

described in Nigeria are those of the All-Progressive Congress (APC),

People’s Democratic Party (PDP) and the Labour Party (LP). The APC and PDP

logos had larger proportion of adult Nigerians (82 percent each) who could

easily describe the party’s logos, while 40 percent had good description of

the Labour party logo amongst other party logos. (NOI Polls) 21 February

2023 WEST EUROPE (UK) Rishi Sunak Registers Lowest

Favourability Scores As Prime Minister The latest update to the Ipsos

Political Pulse shows Rishi Sunak registering his weakest favourability

ratings since becoming Prime Minister amidst significant public pessimism

about the impact of Brexit and the direction of the country. Looking at

opinions of leading politicians, Keir Starmer is seen most favourably, with

32% favourable and 39% unfavourable he achieves a Net score of -7. In

comparison, the current Prime Minister, Rishi Sunak, is seen favourably by

27% of Britons while 46% disagree, giving a score of -19. Starmer’s

numbers are unchanged from January but Rishi Sunak has seen falling scores

(January: 30% favourable and 39% unfavourable). (Ipsos MORI) 22 February 2023 Only A Third Of The Public

Think The NHS Is Providing A Good Service Nationally, Yet Support For The

Founding Principles Remains Strong The Health Foundation has

partnered with Ipsos to deliver a 2-year programme of research into public

expectations and perceptions of health and social care. Every 6 months, we

poll a representative sample of the UK public using the UK

KnowledgePanel – Ipsos’ random probability online panel. There

is deepening public concern about NHS services. Nearly two thirds (63%) think

the general standard of care has got worse in the past 12 months. Across the

UK, only a third (33%) of the public think the NHS is providing a good

service nationally, a significant fall from the previous survey (43%) in May

2022. Additionally, just 10% think their national government has the right

policies for the NHS. (Ipsos MORI) 23 February 2023 The Majority Of Britons Have

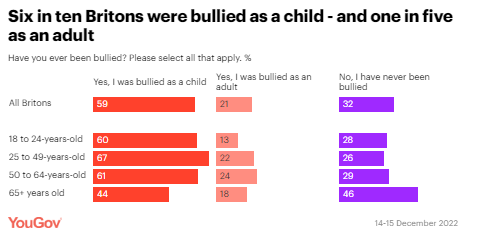

Been Bullied – And It Had A Significant Impact On Most Two thirds of Britons (66%) say

they have been bullied at some point in their lives, according to a new

YouGov poll. One in five people (21%) say they experienced bullying as an

adult, while six in ten Britons (59%) were bullied as a child (some

respondents will have been bullied in both childhood and adulthood). Older

Britons aged 65 and over are least likely to say (or remember) that they’ve

been bullied, with 52% saying they have been, compared to between 63% and 72%

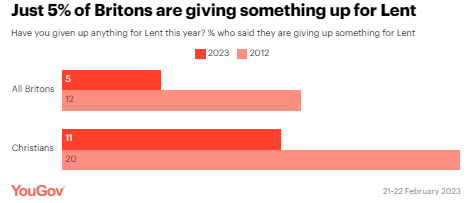

of other age groups. (YouGov UK) February 23, 2023 Only 5% Of Britons

Are Giving Anything Up For Lent 2023 The centuries-old Christian

tradition of Lent will see millions across the world give up something they

love for the 40 days leading up to Easter. But just 5% of Britons are

partaking in the ancient festival this year, including just 11% of British

Christians. That represents a notable fall since 2012, when 12% of Britons

and 20% of British Christians marked the occasion. One in ten (10%) have

turned their back on fatty foods, while 8% are abstaining from sex and the

same proportion are giving up eating out and takeaways (8%). (YouGov UK) February 24, 2023 (France) Energy Renovation: More Than

Half Of Owners Are Considering Taking Steps, But There Are Still Many

Obstacles Inflation, the increase in the

share of housing in the household budget and the context of tensions on the

energy market that we have been experiencing for months have undoubtedly

contributed to placing this problem at the heart of French life.

Indeed, half of French people (49%) feel that over the past two

years, the share of housing in their overall budget has increased, and

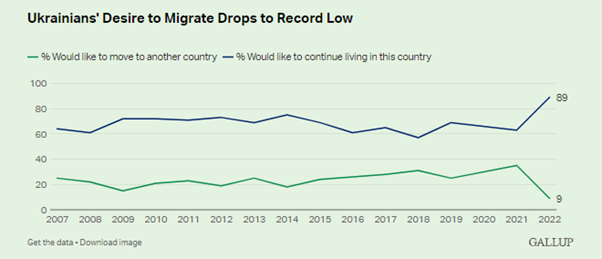

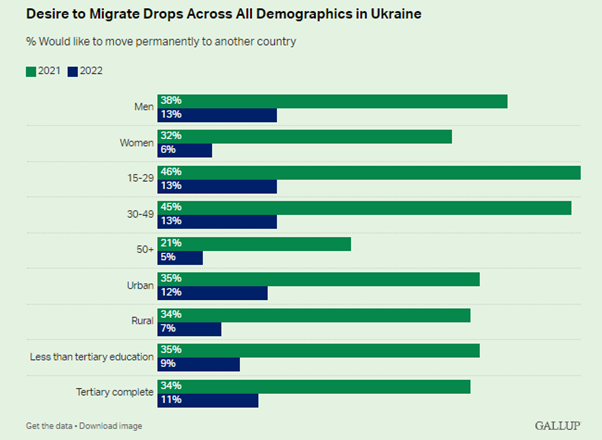

even "increased a lot" for more than 1 in 5 French people (22 %). (Ipsos France) February 23, 2023 (Ukraine) Desire To Migrate In Ukraine

Hits Record Low Before Russia invaded Ukraine a

year ago, more Ukrainians than ever said they would like to leave Ukraine

permanently. But that desire quickly faded after the war began, and now, most

Ukrainians do not want to leave even if they could. A record-low 9% of

Ukrainians surveyed in September of last year -- almost seven months into

Russia’s war with their country -- said they would like to leave Ukraine

permanently, which is down sharply from a record-high 35% just the year

before. (Gallup) FEBRUARY 24, 2023 NORTH AMERICA (USA) 60% Of Americans Would Be

Uncomfortable With Provider Relying On AI In Their Own Health Care A new Pew Research Center survey explores public views on artificial

intelligence (AI) in health

and medicine – an

area where Americans may increasingly

encounter technologies

that do things like screen for skin cancer and even monitor a patient’s vital

signs. The Pew Research Center survey, conducted Dec. 12-18, 2022, of 11,004

U.S. adults finds only 38% say AI being used to do things like diagnose

disease and recommend treatments would lead to better health outcomes for

patients generally, while 33% say it would lead to worse outcomes and 27% say

it wouldn’t make much difference. (PEW) FEBRUARY 22, 2023 Americans Largely Satisfied

With Their Personal Life The 83% of Americans who are at

least somewhat satisfied with their personal life matches the historical

average since 1979, and broad majorities of U.S. adults likewise report they

are satisfied with nine specific life aspects. Between 81% and 90% of U.S.

adults are either “very” or “somewhat” satisfied with their family life,

current housing, education, job, community and personal health, while 71% to

77% express the same degree of satisfaction with the amount of leisure time

they have, their standard of living and their household income. (Gallup) FEBRUARY 23, 2023 48% Of Americans

Played A Sport In 2022 The latest poll from Ipsos unpacks

what sports Americans play and watch, how they tune into their favorite

games, and attitudes towards the biggest controversies in the world of

sports. Ipsos explores American attitudes and behavior toward

sports betting, showing few Americans bet on sports as the country remains

split on legalizing sports betting. Still, 8% of Americans report betting on

sports online or on an app in the past year, while 4% of have done so

in-person. The NFL is the most popular league to bet on. (Ipsos USA) 22 February 2023 American Health In

Polarizing Times This week we released our

first Axios-Ipsos

American Health Index, which builds off of our Axios-Ipsos

Coronavirus Index and expands into some of the biggest

worries Americans have around healthcare, behaviors surrounding health and

wellness, and what policies the public supports. Most Americans have received

at least one dose of the COVID vaccine. Given the hesitancy surrounding and

political jousting over the COVID vaccine, this is a remarkable feat to

reach. But booster shots are lagging way behind. (Ipsos USA) 24 February 2023 (Canada) Inflation Taking

Disproportionate Toll On Canadians Aged 18-34, Impacting Confidence In Their

Financial Future Given today’s economic environment,

just 18% of Canadians aged 18-34 are feeling more confident about their

financial future than before, a significant drop from the 31% who, last year,

said they were feeling more confident about their future emerging from the

pandemic. Nearly eight in ten of those aged 18-34 (77%) are concerned (31%

very/47% somewhat) about their cashflow right now, significantly higher than

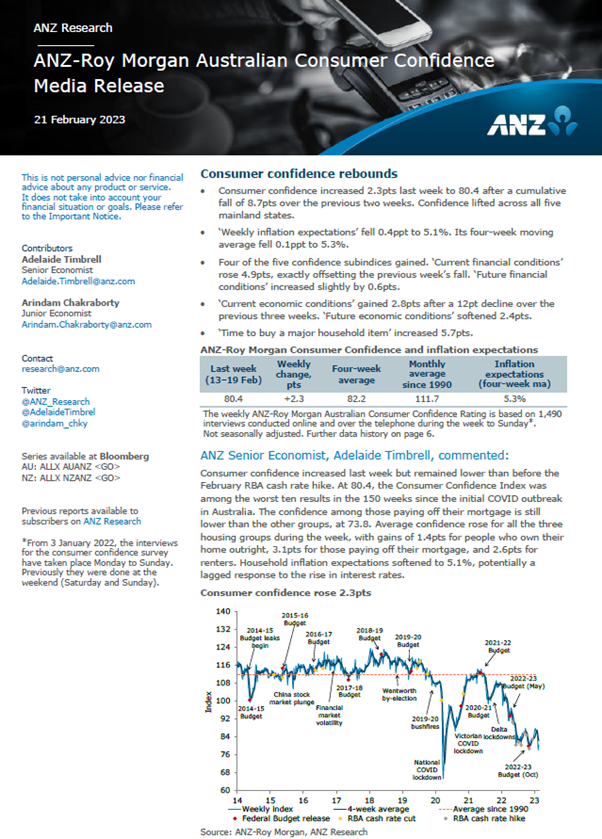

the proportions of those aged 35-54 (69%) and 55+ (57%) who say the same. (Ipsos Canada) 23 February 2023 AUSTRALIA ANZ-Roy Morgan Consumer

Confidence Recovers Slightly, Up 2.3pts To 80.4 Driving this week’s recovery in

Consumer Confidence was sentiment related to personal finances compared to a

year ago and whether now is a ‘good/bad time to buy’ major household items. Consumer

Confidence was up in all five mainland States this week and above 80 in

Victoria, Western Australia and South Australia but under 80 in New South

Wales and Queensland. Now 22% of Australians (up 3ppts) say their families

are ‘better off’ financially than this time last year compared to 47% (down

2ppts) that say their families are ‘worse off’ financially. (Roy Morgan) February 21,

2023 MULTICOUNTRY STUDIES Arab Public Opinion Prefers

China Over USA 11 Out Of 12 Surveyed Nations Hold That View Based on Arab

Barometer’s Wave 7 raw favorability numbers, China’s

increased presence in the region appears to have paid dividends in terms of

its popular standing, especially in North Africa. Except for Morocco, where

favorability for the U.S. at 69% is marginally higher than China’s rating at

64%, the U.S. consistently lags behind China in the view of respondents to

the 12-country survey. The favorability gap is particularly notable in

Algeria, where China enjoys a 20-point edge over the U.S. at 67% vs. 47%. (Arabbarometer) February 21, 2023 Between Economic And

Environmental Concerns, Europeans Are Reinventing Their Mobility Habits, A

Survey In 6 European Nations Since the Covid and the multiple

periods of confinement, Europeans have adapted their way of life,

including their mobility habits. Some "soft" modes of transport are

used more frequently than before: walking (31% of Europeans say they

walk more often than before Covid), cycling (30% of electric bike users use

it more frequently, 25 % for classic bikes), but also scooters (28% of personal

scooter users do it more often). On the contrary, certain modes of

transport involving proximity to strangers have seen their use

decrease: carpooling (27% of users do so less often), public transport

(25% use them less often), taxis or car sharing follow the same trend. (Ipsos France) February 21, 2023 North American

Tracker: Artificial Intelligence (Ai) Tools And Politics Canadians and Americans are most

likely to trust AI tools (a great deal or somewhat) to complete tasks at

home or answer questions about products/services via a website

chat. They are least likely to trust them to teach their

children or help them find a life partner online. Canadians are

most concerned that AI tools lack the emotion/empathy required to

make good decisions (75% agree) and/or are susceptible

to fraud/hacking (72% agree). Americans are most concerned that

they are susceptible to fraud/hacking (73% agree)

and/or threaten human jobs (72% agree). (Leger Opinion) February 23rd, 2023 Source: https://blog.legeropinion.com/en/surveys/north-american-tracker-february-15-2023/ Remote Employees Most Wary

Of Job Security, A Survey Across 10 Nations Global workers are watching as many

corporations struggle in the current economic climate, resulting in layoffs

for many. The global workforce has been under considerable strain since 2020

- first acclimating to the expansion of pandemic-fueled remote work, then

adjusting back to hybrid or reintroduction of return-to-office plans. 69% of

Gen-Z are worried about the security of their roles, compared to 51% of

Boomers. Additionally, the vast majority - 86% - of workers at a Manager

level or below are concerned about layoffs, compared to only 14% of those are

Director level or higher. (Kantar) 23 February 2023 Source: https://www.kantar.com/inspiration/research-services/remote-employees-most-wary-of-job-security-pf ASIA

783-43-01/Polls 47%

Pakistanis Say That They Have Experienced The Lack Of Medicine While Visiting

The Hospital In The Past Year

According to a survey conducted by

Gallup & Gilani Pakistan, 47% Pakistanis say that they have experienced

the lack of medicine while visiting the hospital in the past year. A

nationally representative sample of adult men and women from across the

country, was asked the following as a follow up question, “In the last twelve

months, have you experienced any of the following problems in a government

hospital/clinic? - Lack of medication?” 47% responded yes while 53% said no. Question:

“In the last twelve months, have you experienced any of the following

problems in a government hospital/clinic? - Lack of medication?”

February

24, 2023 Source: https://gallup.com.pk/wp/wp-content/uploads/2023/02/24th-Feb_24-Feb_merged.pdf AFRICA

783-43-02/Polls Political

Party Logo Recognition Poll (Election Poll)

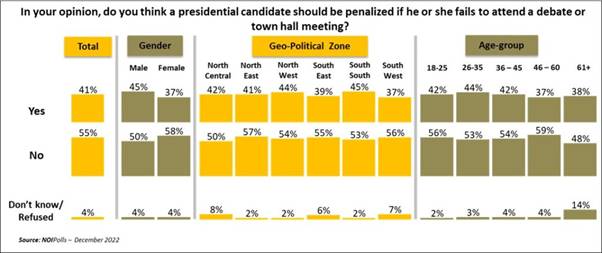

In terms of popularity across

Nigeria, the poll assessed the popularity of the 18 candidates vying for the

presidential position. The findings revealed that the top five (5) popular

candidates in the upcoming February 25th Presidential

election in Nigeria are Bola Ahmed Tinubu of the APC (93 percent), Atiku

Abubakar of the PDP (91 percent), Peter Obi of LP (87 percent), Rabiu

Kwankwaso of the NNPP (66 percent) and Hamza Al Mustapha of AA (35 percent)

amongst other Presidential candidates. Further findings revealed that most

adult Nigerians nationwide (67 percent) advocated that it should be

compulsory for a presidential candidate to attend a debate or town hall

meeting. Of this proportion, 41 percent of adult Nigerians nationwide

recommend that candidates should be penalized if they fail to participate in

a debate. Although there is no law which makes it compulsory for candidates

seeking political offices to participate in any debate, it will be

interesting for this aspect to be included in the election process as stated

by 67 percent of adult Nigerians. This will give the voters the opportunity

to make side-by-side comparisons and afford candidates the opportunity to say

why they are best suited for the elected office they are vying for. Nigerians will be going to the

election booths in three (3) days’ time (25th February 2023).

This is the 7th consecutive election that will be conducted

in the country without interruption. With over 9 million new registrants in

the election being mostly youths, it makes the election an interesting one[1].

However, the country still faces election challenges which include

insecurity, INEC preparedness, money politics, and election rigging amongst

other issues. It remains to be seen if these issues will be addressed before

the election or if they will form a stumbling block to the success of the election. These are some of the key findings

from the Election series poll following the countdown to the 2023 general

election, conducted on the week commencing 12th December

2022. This is the fifth (5) in the series of monthly election polls conducted

by NOIPolls as Nigerians countdown to February 25th, 2023,

elections. Survey Background It is time again, precisely on 25th February,

2023, for Nigerians to go to the ballots and elect their next President. It

is also a time that democracy affords Nigerians another opportunity to choose

a leader that will steer the affairs of the country for another 4 years. The

election period is indeed a critical one for Nigerians as they stand to

either continue with the ruling APC and its candidate or entirely take a

departure completely to another party like they did in 2015. It remains to be

seen what the outcome of the election will be[2]. However, the popularity of

candidates and the party’s amongst the populace is an important and crucial

factor as it tends to be a deciding coefficient on which the election

trajectory may tilt. It is pertinent to note that the more popular a

candidate is amongst the electorate, the higher the chances the candidate has

in winning the election and vice-versa. Therefore, all the candidates have

embarked on rigorous campaigning to increase their visibility and popularity

and to canvass for votes amongst the electorates. The importance of this election

cannot be over-emphasized as it affords all Nigerians the opportunity to

choose their leaders at all levels. However, All Nigerians are earnestly

hoping that the elections will provide them with the opportunity of having

new sets of leaders that will curb the myriad of challenges the country is

facing such as inflation, joblessness, banditry, kidnapping, terrorism, and

the rest. It remains to be seen if the country will achieve this feat

or will continue in the trajectory of the current trend of affairs[3]. Against this background, NOIPolls

conducted its Election Series Poll to seek the views of Nigerians on

political party logo and candidate’s popularity ahead of the February 25th,

2023, general elections. This is the fifth in the series of monthly election

polls conducted by NOIPolls (the first one was conducted in July 2022) as

Nigerians countdown to the February 25th, 2023. General

elections. Survey Findings The first question revealed that 93

percent of adult Nigerians disclosed they have been thinking of the February

25th general election in the country. In addition, while 92

percent of the respondents indicated that they have registered to vote for

the general election, 91 percent claimed to have their PVCs. Furthermore, respondents were asked

to describe the logos of the 18 political parties that are contesting for the

Presidential election. The findings revealed that All Progressive Congress

(APC) and People’s Democratic Party (PDP) logos were easily described by most

adult Nigerians (82 percent each) across the country. This is followed by 40

percent of the respondents who properly described the Labour Party’s logo and

29 percent for All Progressives Grand Alliance (APGA) while 24 percent

described the party logo of the New Nigeria People’s Party (NNPP) amongst all

other party logos.

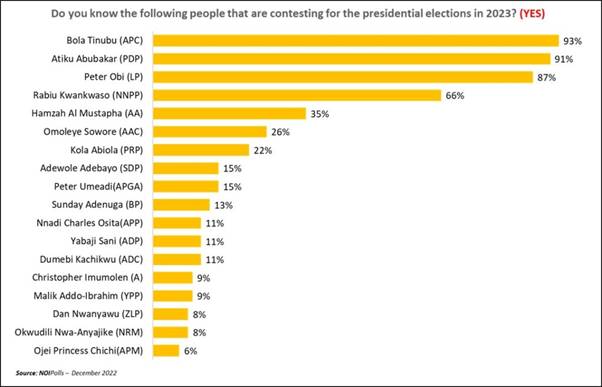

Subsequently, the poll assessed

awareness of adult Nigerians on the 18 candidates vying for the Presidential

position. Findings revealed that the top five (5) popular candidates in the

February 25th presidential election in Nigeria are Bola Ahmed

Tinubu of the APC (93 percent), Atiku Abubakar of the PDP (91 percent), Peter

Obi of LP (87 percent), Rabiu Kwankwaso of the NNPP (66 percent) and Hamza Al

Mustapha of AA (35 percent) amongst other Presidential candidates.

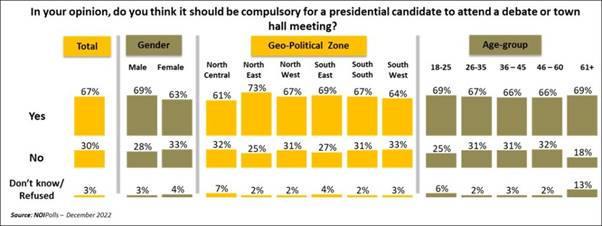

The poll result also revealed most

adult Nigerians nationwide (67 percent) suggest it should be compulsory for a

presidential candidate to attend a debate or town hall meeting. This

assertion cuts across gender, geographical location, and age-group with a

minimum representation of 61 percent. On the other hand, 30 percent think

otherwise while 3 percent did not respond to the question.

When respondents were asked of

their opinion on penalty should a candidate fail to attend a debate or town

hall meeting, the poll revealed 41 percent of adult Nigerians nationwide

recommended that the candidate should be penalized while 55 percent responded

negatively.

Conclusion The poll findings have shown that

not all electorates are aware of the political party logo that they support

in the February 25th, 2023, general election. On the other hand,

the poll revealed that the name of the candidates resonates more with the

electorates than the party logo of the candidate. For instance, the top 3

candidates mentioned by Nigerians in terms of popularity for the Presidential

position are Bola Tinubu, (93 percent), Atiku Abubakar (91 percent) and Peter

Obi (87 percent) respectively. Therefore, given that it is only party logo

that are printed in the ballot paper, it would be advised that political parties

in future carry out enough awareness on their party logo during meetings,

rallies, and campaigns. Finally, it is advised that debates

be considered as an aspect of the electioneering process as advocated by 67

percent of adult Nigerians who think it should be compulsory for a

Presidential candidate to attend a debate or town hall meeting. This will

give Voters the opportunity to make side-by-side comparisons and give

candidates a chance to say why they are best suited for the elected office

they intend to vie for. 21 February 2023 Source:

https://noi-polls.com/apc-pdp-and-lp-top-three-political-party-logo-nigerians-properly-recognize/ WEST EUROPE

783-43-03/Polls Rishi

Sunak Registers Lowest Favourability Scores As Prime Minister

Favourability of

politicians A similar number of the public are

favourable towards Boris Johnson as Rishi Sunak (28% vs 27%). However, with

52% unfavourable to the former PM, his overall net favourability rating is

lower at -24.

Looking at specifically at their

own voters, Boris Johnson is seen slightly more favourably than Rishi Sunak.

More than half of 2019 Conservative voters are favourable to Johnson (55%)

while 49% say the same for Sunak. Overall, among 2019 Conservative voters,

Johnson scores +29 while Sunak scores +23. However, Johnson’s lead owes

more to falling ratings for Mr Sunak rather than improving ratings for the

former PM. Liz Truss sees the worst

favourability rating of the politicians on our list with the public overall.

Only 1 in 10 (9%) are favourable and 71% unfavourable meaning she has a net

score of -62, significantly lower than other politicians such as Jeremy

Corbyn (-36), Suella Braverman (-33), Jeremy Hunt (-28) and Theresa May

(-27%). Favourability

towards parties With a net score of+2, the Labour

Party appears the most popular political party currently, 38% have a

favourable opinion of the Opposition party (+3 pts from Jan) while 36% are

unfavourable (no change). With 28% positive towards the Green Party (+5 pts)

and 30% negative (-2), they see a net score of -2. The Conservatives see the

lowest score with -29, 25% are favourable towards them (unchanged) while 54%

are unfavourable (+3). The Liberal Democrats see a score of -17 while Reform

UK (new to our list) score -24. However, many are neutral or do not

have an opinion of each.

Brexit and

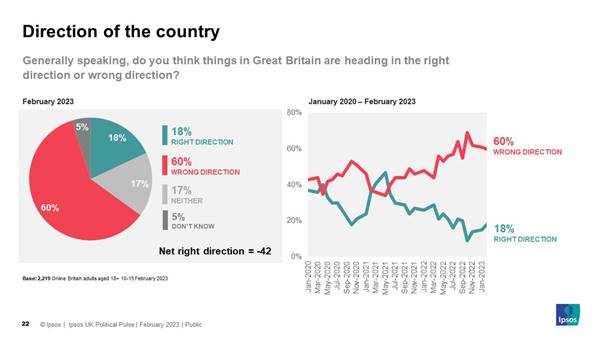

direction of country The public are increasingly

negative about the impact of Brexit over time. Now, 55% of Britons say the

UK’s decision to leave the European has had a negative impact on the country,

the fourth straight month we have recorded numbers over half. Only 1 in 5

(21%) believe Brexit has had a positive impact while a similar proportion say

it has made no difference (18%). If we subtract the proportion

saying Brexit has had a negative impact from the proportion saying positive

the result is a net positivity score of -34. This continues to be the lowest

we have recorded on Brexit, since we started asking this question in January

2020.

In line with this, we see 6 in 10

now believe the country is heading in the wrong direction (60%), remaining

stable since January (61%).

Keiran Pedley, at

Ipsos, said: When Rishi Sunak

became Prime Minister it was notable that his personal poll ratings were

significantly better than those of his party. This increasingly no longer

appears to be the case amidst public pessimism about the direction of the

country. Our polling shows strong public concern about the cost of living and

public services, whilst Brexit is being viewed more negatively over time as

well. The Prime Minister will hope he is able to seize the political agenda

in the coming weeks and months if he is to have any chance of turning his

fortunes around. 22

February 2023 Source: https://www.ipsos.com/en-uk/rishi-sunak-registers-lowest-favourability-scores-prime-minister

783-43-04/Polls Only

A Third Of The Public Think The NHS Is Providing A Good Service Nationally,

Yet Support For The Founding Principles Remains Strong

The Health Foundation has partnered with Ipsos to deliver

a 2-year programme of research into public expectations and perceptions of

health and social care. Every 6 months, we poll a representative sample of

the UK public using the UK KnowledgePanel – Ipsos’ random probability online

panel. The findings from the third survey show:

23

February 2023

783-43-05/Polls The

Majority Of Britons Have Been Bullied – And It Had A Significant Impact On

Most

Schools and

workplaces are at the centre of most of Britain’s bullying

Those who experienced bullying as a

child are most likely to say it happened repeatedly: 42% say it happened many

times while a further 38% say it happened on several occasions. Only 17% say

it only happened once or twice. Bullying as an adult seems to have

been less sustained: a lower figure of 23% of victims say it happened many

times. Around half say they were subjected to bullying several times (47%),

while 28% say it happened only once or twice. Majority of

bullied Britons say being targeted by bullies had a significant impact on

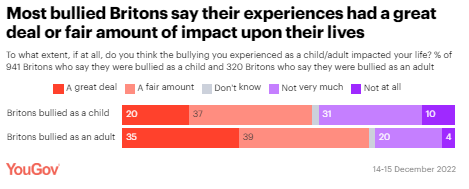

their life Three-quarters of people who were

bullied as an adult say the experience impacted their life a great deal (35%)

or a fair amount (39%). In comparison, one in five of those

bullied as children (20%) say it had a great deal of impact while 37% say it

had a fair amount of impact on their life. Just 4% of Britons targeted by

bullies in adulthood say it had no impact on their life, while one in ten

(10%) of those bullied as children say the same.

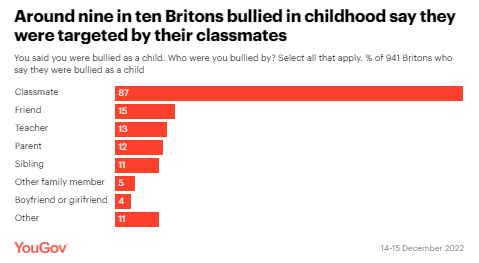

Classmates blamed

by most of those bullied as children Nearly nine in ten (87%) of those

who were bullied in childhood say they were bullied by a classmate, with

friends (15%) and teachers (13%) also among the culprits cited. And a significant proportion of

those Britons say they were targeted by members of their own family,

including 12% who were bullied by a parent, 11% by a sibling and 5% by

another family member.

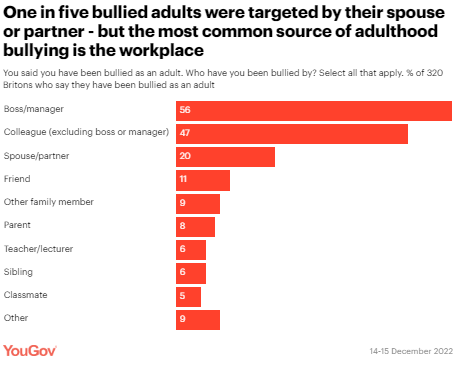

One in five

bullied adults say they were targeted by their partner A significant proportion of Britons

bullied as an adult say they have suffered at the hands of those who arguably

should love them the most – their spouse or partner. One in five (20%) report being

bullied by a partner, while 16% have been bullied by other family members,

including 8% who say they were bullied by a parent and 6% who were bullied by

a sibling. However, the most likely source of

bullying in adulthood is the workplace – more than half of those bullied as

adults (56%) say they have been bullied by a boss or manager and 47% by a

colleague.

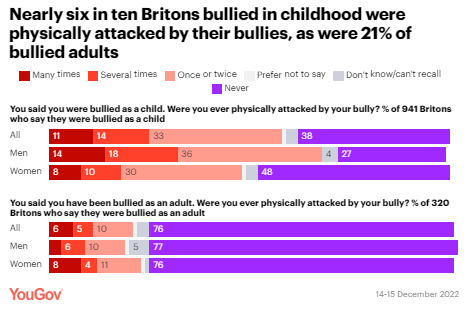

Most Britons

bullied as children were physically attacked Around six in ten Britons (58%)

bullied in childhood say their bully physically attacked them, including 11%

who say they were attacked “many times”. Men are more likely than women to

have been physically set upon by their childhood bully, at 68% to 48%. But when it comes to bullying in

adulthood, the gender gap narrows – 21% of those who say they were bullied as

an adult report being attacked at least once or twice, including 19% of men

and 23% of women.

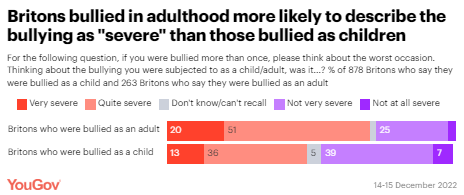

Those who were bullied in adulthood

are more likely to describe the worst bullying they were subjected to as

severe, with 71% of bullied adults saying it was compared to 49% of Britons

bullied in childhood.

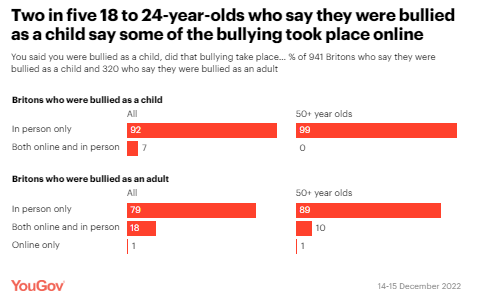

Internet brings

shift in the nature of bullying for young people The nature of bullying has shifted

since the advent of the internet, with 42% of 18 to 24-year-olds who were

bullied as a child saying at least some of the bullying they experienced took

place online – although almost all say they were also bullied in person. One in six Britons (18%) who have

experienced bullying as an adult say at least part of it happened online.

February

23, 2023

783-43-06/Polls Only

5% Of Britons Are Giving Anything Up For Lent 2023

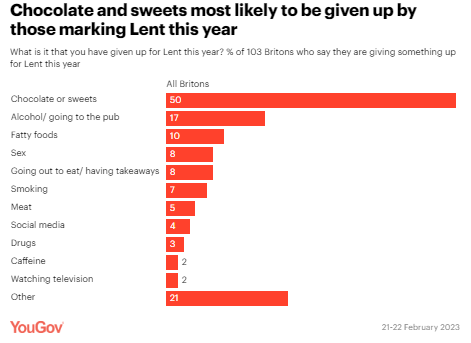

Chocolate and

sweets most commonly given up by those marking the tradition

Chocolate and

sweets most likely to be given up for Lent Half of those marking the occasion

(50%) say they have temporarily given up eating chocolate and sweets, while

17% have put pub-going and booze drinking on a temporary hiatus.

February

24, 2023

783-43-07/Polls Energy

Renovation: More Than Half Of Owners Are Considering Taking Steps, But There

Are Still Many Obstacles

A context marked

by the growing weight of housing in household budgets… Inflation, the increase in the

share of housing in the household budget and the context of tensions on the

energy market that we have been experiencing for months have undoubtedly

contributed to placing this problem at the heart of French life. ,

even more than was the case before: now, every expense counts, and everything

that can be done to relieve an overly constrained budget is considered.

Energy renovation,

a subject that concerns the French Four out of five

French people have heard of the renovation of old dwellings, a

very substantial proportion for a subject that at first glance might be

considered quite "technical" (for comparison: slightly more than

half of French people have heard of the Climate Resilience Law) And 55% of them feel personally concerned by the energy renovation of

housing. This high figure can be explained in particular

because nearly a third of French

people feel that they live in a thermal colander (29%), a

figure roughly equivalent to the proportion of landlords (33%) who think of

renting colanders thermal. More than half of

landlords and landlords are considering formalities The proportion of French people who

are considering eco-renovation approaches is substantial:

For the French who are considering

the eco-renovation of the housing they own, it is:

Their general knowledge of the

subject and its issues is relatively good:

Two types of

obstacles to energy renovation Financial

obstacles, due to amounts to be committed deemed too high There is a difficulty in finding

the financing necessary for energy renovation: half of French people who do not plan to

eco-renovate their home invoke the fact that the budget to be mobilized is

too large for their finances (46% first, 52% overall). A sign of the importance of the

problem of financing in the transition to the act of renovation, their own bank is the second interlocutor to whom

the French turn most spontaneously to undertake the

procedures and manage the works (19% first, 45% in total), behind the France

Rénov site (44% first, 58% in total). The practical

obstacles, the French experiencing difficulties on how to undertake these

renovations 26% of French people thus cite this

type of obstacle as a priority as a hindrance to renovation: 13% say they do not know by whom and how to get

support (33% of responses in total), 6% do not know how to identify serious companies and

are afraid of scams (31% in total) and finally 7% consider the help too complicated, too numerous

and not clear enough (40% of quotes in total). In addition, State aid is considered by the vast majority to be

illegible: if there are many people who feel concerned and ready

to act, the passage to action is hampered by a lack of legibility of State

aid: 69% of French people think that

it is not easy to find their way around (including 40% not at

all easy). A figure that sums up the extent of the simplification

efforts still to be made by the public authorities. Similar obstacles

within condominiums Quite logically, and because of

these major difficulties raised - informational, financial and logistical

-, the proportion of French people

judging that in their co-ownership, the co-owners are in favor of a complete

eco-renovation of the co-ownership only amounts to 38%. . All of the difficulties encountered

in the context of eco-renovation constitute an opportunity for a trusted

third party such as the trustee, who

is currently only identified by one owner in four as a door to entered to

undertake an eco-renovation approach (23%). The inability of co-owners to

achieve a clear majority in favor of overall eco-renovation work on

co-ownerships is responsible for a large part of the wait-and-see attitude in

this area. At Nexity, we observe that on average 8% of renovation

projects are blocked for lack of a majority vote according to the current

rules. One of the possible solutions would be to change the voting rules

in this area, moving from an absolute majority to a majority of those present

(simple majority).

A real risk of

resignation Owners who plan to

sell because they cannot renovate Financial concerns, the difficulty

of finding one's way in state aid, and the difficulties of obtaining

majorities within condominiums no doubt explain why a large proportion of

owners say they are ready to put their thermal sieve up for sale (rather than

renovating it at great expense):

And tenants who

mostly accept a de facto situation Asked about their intentions:

February

23, 2023

783-43-08/Polls Desire

To Migrate In Ukraine Hits Record Low

Gallup collected these data Sept.

2-11 among Ukrainians who currently reside in Ukraine, including those who

had been internally displaced to other areas within their country by the war. The survey represents views across

Ukraine, including the four occupied regions in the country's south and east,

where Russia launched referendums on Sept. 23 to annex them and later

declared martial law. Notably, before either of these developments, desire to

migrate was only marginally higher in the country’s east (12%) and west

(12%). Desire to Leave at

Record Lows Among Ukrainians From All Walks of Life Desire dropped precipitously across

most demographics of Ukrainians in 2022. The largest declines were evident

among younger Ukrainians -- who in past surveys have usually been the most

likely to want to leave. Before the war, nearly half of Ukrainians (45%)

younger than age 50 expressed a desire to leave their country for good, but

by last fall, these figures had dropped to just 13%.

Shortly after the war began,

Ukraine banned men of fighting age -- those between the ages of 18 and 60 --

from leaving the country. This ban may have factored into the drop in men’s

desire to leave, which declined from 38% in 2021 to 13% in 2022. However,

women’s desire to migrate dropped just as much, falling from 32% to 6% within

the same period. Canada, U.S. and

Poland Top Desired Destinations for Those Who Want to Move Shortly after Russia invaded,

millions of Ukrainians -- mostly women and children -- began fleeing Ukraine

for other countries, including

bordering countries to the west. Although several million returned

home within months, in October 2022, the United Nations estimated 7.6 million

Ukrainian refugees were still spread across Europe, including nearly 3

million in Russia. Although relatively few Ukrainians

desire to move, if they do, they are most likely to name Canada (19%), the

U.S. (16%) and Poland (16%) -- which has taken in more Ukrainian refugees

than any other country -- as their most desired place to move. In a departure

from years past, no potential migrants in Ukraine named Russia or Belarus as

a desired destination. Bottom Line Despite the stream of refugees who

left Ukraine in the months after the war broke out, few Ukrainians

interviewed in Ukraine late last year were interested in making a permanent

move to another country. Even if everyone who left and did not return to

Ukraine were people who wanted to migrate previously, it would still not

account for the 26-percentage-point drop in Ukrainians’ desire to migrate in

2022. Instead, this lack of interest may reflect a heightened sense of

patriotism among Ukrainians with their country at war and a reluctance to

move. Still, even as Ukrainians

have rallied

around their institutions and remained committed

to victory, surveys in Ukraine later this year will show how much

the protracted conflict has tested their resolve. FEBRUARY

24, 2023 Source: https://news.gallup.com/poll/471119/desire-migrate-ukraine-hits-record-low.aspx NORTH

AMERICA

783-43-09/Polls 60%

Of Americans Would Be Uncomfortable With Provider Relying On AI In Their Own

Health Care

A new Pew Research Center

survey explores public views on artificial intelligence (AI) in health and medicine –

an area where Americans may increasingly encounter technologies

that do things like screen for skin cancer and even monitor a patient’s vital

signs.

The survey finds that on a personal level, there’s significant

discomfort among Americans with the idea of AI being used in their own health

care. Six-in-ten U.S. adults say they would feel uncomfortable if their own health

care provider relied on artificial intelligence to do things like diagnose

disease and recommend treatments; a significantly smaller share (39%) say

they would feel comfortable with this. One factor in these views: A majority of the public is unconvinced that

the use of AI in health and medicine would improve health outcomes. The Pew Research Center survey, conducted Dec. 12-18,

2022, of 11,004 U.S. adults finds only 38% say AI being used to do things

like diagnose disease and recommend treatments would lead to better health

outcomes for patients generally, while 33% say it would lead to worse

outcomes and 27% say it wouldn’t make much difference. These findings come as public attitudes toward AI continue to take

shape, amid the ongoing adoption of AI technologies across industries and the

accompanying national conversation about the benefits and risks that AI

applications present for society. Read recent Center analyses for more on

public awareness of AI

in daily life and

perceptions of how much advancement emerging

AI applications represent for their fields. Asked in more detail about how the use of artificial intelligence would

impact health and medicine, Americans identify a mix of both positives and

negatives. On the positive side, a larger share of Americans think the use of AI

in health and medicine would reduce rather than increase the number of

mistakes made by health care providers (40% vs. 27%). And among the majority of Americans who see a problem with racial and

ethnic bias in health care, a much larger share say the problem of bias and

unfair treatment would get better (51%) than worse (15%) if AI was used more

to do things like diagnose disease and recommend treatments for patients. But there is wide concern about AI’s potential impact on the personal

connection between a patient and health care provider: 57% say the use of

artificial intelligence to do things like diagnose disease and recommend

treatments would make the patient-provider relationship worse. Only 13% say

it would be better. The security of health records is also a source of some concern for

Americans: 37% think using AI in health and medicine would make the security

of patients’ records worse, compared with 22% who think it would improve

security.

Though Americans can identify a mix of pros and cons regarding the use

of AI in health and medicine, caution remains a dominant theme in public

views. When it comes to the pace of technological adoption, three-quarters of

Americans say their greater concern is that health care providers will move

too fast implementing AI in health and medicine before fully understanding

the risks for patients; far fewer (23%) say they are more concerned that

providers will move too slowly, missing opportunities to improve patients’

health. Concern over the pace of AI adoption in health care is widely shared

across groups in the public, including those who are the most familiar with

artificial intelligence technologies. Younger adults, men, those with higher levels of education are more

open to the use of AI in their own health care

There is more openness to the use of AI in a person’s own health care

among some demographic groups, but discomfort remains the predominant

sentiment. Among men, 46% say they would be comfortable with the use of AI in

their own health care to do things like diagnose disease and recommend

treatments, while 54% say they would be uncomfortable with this. Women

express even more negative views: 66% say they would be uncomfortable with

their provider relying on AI in their own care. Those with higher levels of education and income, as well as younger

adults, are more open to AI in their own health care than other groups.

Still, in all cases, about half or more express discomfort with their own

health care provider relying on AI. Among those who say they have heard a lot about artificial

intelligence, 50% are comfortable with the use of AI in their own health

care; an equal share say they are uncomfortable with this. By comparison,

majorities of those who have heard a little (63%) or nothing at all (70%)

about AI say they would be uncomfortable with their own health care provider

using AI. At this stage of development, a modest share of Americans see AI

delivering improvements for patient outcomes. Overall, 38% think that AI in

health and medicine would lead to better overall outcomes for patients.

Slightly fewer (33%) think it would lead to worse outcomes and 27% think it

would not have much effect.

Men, younger adults, and those with higher levels of education are more

positive about the impact of AI on patient outcomes than other groups,

consistent with the patterns seen in personal comfort with AI in health care.

For instance, 50% of those with a postgraduate degree think the use of AI to

do things like diagnose disease and recommend treatments would lead to better

health outcomes for patients; significantly fewer (26%) think it would lead

to worse outcomes. Americans who have heard a lot about AI are also more optimistic about

the impact of AI in health and medicine for patient outcomes than those who

are less familiar with artificial intelligence technology. Four-in-ten Americans think AI in health and medicine would reduce the

number of mistakes, though a majority say patient-provider relationships

would suffer Americans anticipate a range of positive and negative effects from the

use of AI in health and medicine.

The public is generally optimistic about the potential impact of AI on

medical errors. Four-in-ten Americans say AI would reduce the number of

mistakes made by health care providers, while 27% think the use of AI would lead

to more mistakes and 31% say there would not be much difference. Many also see potential downsides from the use of AI in health and

medicine. A greater share of Americans say that the use of AI would make the

security of patients’ health records worse (37%) than better (22%). And 57%

of Americans expect a patient’s personal relationship with their health care

provider to deteriorate with the use of AI in health care settings. The public is divided on the question of how it would impact the

quality of care: 31% think using AI in health and medicine would make care

for people like themselves better, while about as many (30%) say it would

make care worse and 38% say it wouldn’t make much difference. Americans who are concerned about bias based on race and ethnicity in

health and medicine are more optimistic than pessimistic about AI’s potential

impact on the issue

When it comes to bias and unfair treatment in health and medicine based

on a patient’s race or ethnicity, a majority of Americans say this is a major

(35%) or minor (35%) problem; 28% say racial and ethnic bias is not a problem

in health and medicine. There are longstanding efforts by the federal

government and across

the health

and medical care sectors to

address racial and ethnic inequities in access to care and in health

outcomes. Black adults are especially likely to say that bias based on a

patient’s race or ethnicity is a major problem

in health and medicine (64%). About four-in-ten Hispanic (42%) and

English-speaking Asian adults (39%) also say this. A smaller share of White

adults (27%) describe bias and unfair treatment related to a patient’s race

or ethnicity as a major problem in health and medicine.

On balance, those who see bias based on race or ethnicity as a problem

in health and medicine think AI has potential to improve the situation. About

half (51%) of those who see a problem think the increased use of AI in health

care would help reduce bias and unfair treatment, compared with 15% who say

the use of AI would make bias and unfair treatment worse. A third say the

problem would stay about the same. Among those who see a problem with bias in health and medicine, larger

shares think the use of AI would make this issue better than worse among

White (54% vs. 12%, respectively), Hispanic (50% vs. 19%) and

English-speaking Asian (58% vs. 15%) adults. Views among Black adults also

lean in a more positive than negative direction, but by a smaller margin (40%

vs. 25%). Note that for Asian adults, the Center estimates are representative of

English speakers only. Asian adults with higher levels of English language

proficiency tend to have higher levels of education

and family income than

Asian adults in the U.S. with lower levels of English language proficiency.

Asked for more details on their views about the impact of AI on bias in

health and medicine, those who think it would improve the situation often

explain their view by describing AI as more objective or dispassionate than

humans. For instance, 36% say AI would improve racial and ethnic bias in

medicine because it is more neutral and consistent than people and human

prejudice is not involved. Another 28% explain their view by expressing the

sense that AI is not biased toward a patient’s characteristics. Examples of

this sentiment include respondents who say AI would be blind to a patient’s

race or ethnicity and would not be biased toward their overall appearance. Among those who think that the problem of bias in health and medicine

would stay about the same with the use of AI, 28% say the main reason for

this is because the people who design and train AI, or the data AI uses, are

still biased. About one-in-ten (8%) in this group say that AI would not

change the issue of bias because a human care provider would be primarily

treating people even if AI was adopted, so no change would be expected. Among those who believe AI will make bias and unfair treatment based on

a patient’s race or ethnicity worse, 28% explain their viewpoint by saying

things like AI reflects human bias or that the data AI is trained on can

reflect bias. Another reason given by 10% of this group is that AI would make

the problem worse because human judgment is needed in medicine. These

responses emphasized the importance of personalized care offered by providers

and expressed the view that AI would not be able to replace this aspect of

health care. Americans’ views on AI applications used in cancer screening, surgery

and mental health support The Center survey explores views on four specific applications of AI in

health and medical care that are in use today or being developed for

widespread use: AI-based tools for skin cancer screening; AI-driven robots

that can perform parts of surgery; AI-based recommendations for pain

management following surgery; and AI chatbots designed to support a person’s

mental health. Public awareness of AI in health and medicine is still in the process

of developing, yet even at this early stage, Americans make distinctions

between the types of applications they are more and less open to. For

instance, majorities say they would want AI-based skin cancer detection used

in their own care and think this technology would improve the accuracy of

diagnoses. By contrast, large shares of Americans say they would not want any

of the three other AI-driven applications used in their own care. For more on how Americans view the impact of these four developments

read, “How

Americans view emerging uses of artificial intelligence, including programs

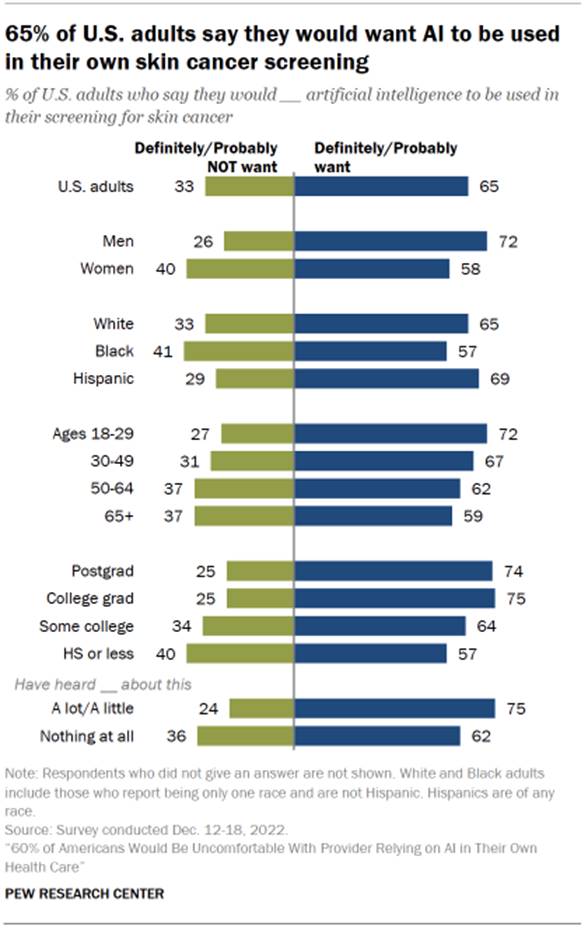

to generate text or art.” AI-based skin cancer screening AI used for skin cancer detection can scan images of people’s skin and

flag areas that may be skin cancer for testing.

Nearly two-thirds of U.S. adults (65%) say that they would definitely

or probably want AI to be used for their own skin cancer screening.

Consistent with this view, about half (55%) believe that AI would make skin

cancer diagnoses more accurate. Only 13% believe it would lead to less

accurate diagnoses, while 30% think it wouldn’t make much difference. On the whole, Americans who are aware of this AI application view it as

an advance for medical care: 52% describe it as a major advance while 27%

call it a minor advance. Very few (7%) say it is not an advance for medical

care.

Majorities of most major demographic groups say they would want AI to

be used in their own screening for skin cancer, with men, younger adults, and

those with higher education levels particularly enthused. A larger majority of men (72%) than women (58%) say they would want AI

to be used in their screening for skin cancer. Black adults (57%) are somewhat less likely than White (65%) and

Hispanic (69%) adults to say they would want AI used for skin cancer

screening. Experts have raised questions

about the accuracy of

AI-based skin cancer systems for darker skin tones. Younger adults are more open to using this form of AI than older

adults, and those with a college degree are more likely to say they would

want this than those without a college degree. In addition, those who have heard at least a little about the use of AI

in skin cancer screening are more likely than those who have heard nothing at

all to say they would want this tool used in their own care (75% vs. 62%). AI for pain management recommendations AI is being used to help physicians prescribe

pain medication. AI-based

pain management systems are designed to minimize the chances of patients

becoming addicted to or abusing medications; they use machine learning models

to predict things like which patients are at high risk for severe pain and

which patients could benefit from pain management techniques that do not

involve opioids.

Asked to consider their own preferences for treatment of pain following

surgery, 31% of Americans say they would want this kind of AI guiding their

pain management treatment while two-thirds (67%) say they would not. This reluctance is in line with people’s beliefs about the effect of

AI-based pain management recommendations. About a quarter (26%) of U.S.

adults say that pain treatment would get better with AI, while a majority say

either that this would make little difference (40%) or lead to worse pain care

(32%). Among those who say they’ve heard at least a little about this use of

AI, fewer than half (30%) see it as a major advance for medical care, while

another 37% call it a minor advance. By comparison, larger shares of those

aware of AI-based skin cancer detection and AI-driven robots in surgery view

these applications as major advances for medical care.

Those with some familiarity with AI-based pain management systems are

more open to using AI in their own care plan. Of those who say they have

heard at least a little about this, 47% say they would want AI-based

recommendations used in their post-op pain treatment, compared with 51% who

say they would not want this. By comparison, a large majority (72%) of those

not familiar with this technology prior to the survey say they would not want

this. Demographic differences on this question are generally modest, with

majorities of most groups saying they would not want AI to help decide their pain treatment

program following a surgery. Performing surgery with AI-driven robots AI-driven robots are in development that could complete surgical

procedures on their own, with full autonomy from human surgeons. These

AI-based surgical robots are being tested to perform parts

of complex surgical procedures and are expected to increase the precision and consistency of the

surgical operation. Americans are cautious toward the idea of surgical robots used in their

own care: Four-in-ten say they would want AI-based robotics for their own

surgery, compared with 59% who say they would not want this.

Still, Americans with at least some awareness of these AI-based

surgical robots are, by and large, convinced they represent an advance for

medical science: 56% of this group says it is a major advance and another 22%

calls it a minor advance. (For more on how Americans view advances in

artificial intelligence, read “How

Americans view emerging uses of artificial intelligence, including programs

to generate text or art.”)

Public familiarity with the idea of AI-based surgical robots is higher than

for the three other health and medical applications included on the survey;

59% say they have heard at least a little about this development.

As with other AI applications included in the survey, those unfamiliar

with AI-driven robots in surgery are especially likely to say they would not

want them used in their own care (74% say this). Those who have heard of this

use of AI before are evenly divided: 50% say they would want AI-driven robots

to be used in their surgery, while 49% say they wouldn’t want this. Across demographic groups, men are more inclined than women to say they

would want an AI-based robot for their own surgery (47% vs. 33%). And those

with higher levels of education are more open to this technology than those

with lower levels of education. There is little difference between the views of older and younger

adults on this: Majorities across age groups say they would not want an AI-based robot for their

own surgery. This contrasts with preferences about other uses of AI in

medical care in which younger adults are more likely than older adults to say

they would want AI applications for skin cancer screening or pain management. AI chatbots designed to support mental health Chatbots aimed at supporting

mental health use AI

to offer mindfulness check-ins and “automated conversations” that may

supplement or potentially provide an alternative to counseling or therapy

offered by licensed health care professionals. Several chatbot platforms are

available today. Some are touted as ways to support mental health wellness

that are available on-demand and may appeal to those reluctant to seek

in-person support or to those looking for more affordable options.

Public reactions to the idea of using an AI chatbot for mental health

support are decidedly negative. About eight-in-ten U.S. adults (79%) say they

would not want to use an AI chatbot if they were seeking mental health

support; far fewer (20%) say they would want this. In a further sign of caution toward AI chatbots for mental health

support, 46% of U.S. adults say these AI chatbots should only be used by

people who are also seeing a therapist; another 28% say they should not be

available to people at all. Just 23% of Americans say that such chatbots

should be available to people regardless of whether they are also seeing a

therapist. Large majorities of U.S. adults across demographic and educational

groups lean away from using an AI chatbot for their own mental health

support. Read the Appendix for details.

Even among Americans who say they have heard about these chatbots prior

to the survey, 71% say they would not want to use one for their own mental

health support. And among those who have heard about these AI chatbots, relatively few

(19%) consider these to be a major advance for mental health support; 36%

call them a minor advance, while 25% say they are not an advance at all.

Public opinion on this use of AI, as with many others, is still developing:

19% of those familiar with mental health chatbots say they’re not sure if

this application of AI represents an advance for mental health support. FEBRUARY 22, 2023

783-43-10/Polls Americans

Largely Satisfied With Their Personal Life

Personal

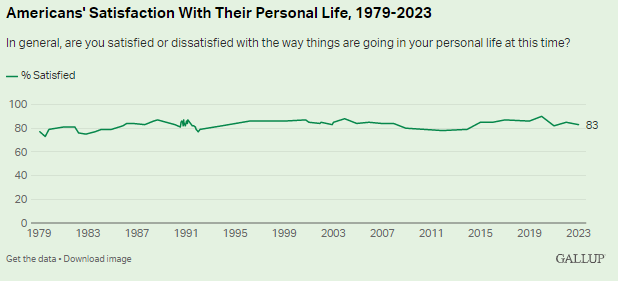

Satisfaction Matches Average Since 1979 Americans’ satisfaction with their

overall personal life has ranged from 73% to 90% in Gallup’s periodic

measures since 1979. The record

high was measured in 2020, two months before the COVID-19

pandemic swept across the U.S. It was short-lived, however, as the

reading fell

to 82% in 2021. Last year, it edged

up to 85%. The low point in personal satisfaction

came in the summer of 1979 during the energy crisis. Personal satisfaction

was also below 80% during challenging economic times in the early 1980s,

early 1990s and the years after the Great Recession.

Gallup has asked a follow-up

question in most years since 2001 about the degree to which Americans are

satisfied with their personal life. In a Jan. 2-22 Gallup survey, 50% of U.S.

adults say they are very satisfied,

in line with the previous two years’ 51% readings but well below the 65% high

from 2020. The only times Gallup found a smaller share of Americans very

satisfied with their life were in December 2008, during the global economic

crisis, and in 2011, as the country was still recovering from the 2007-2009

recession.

Satisfaction

Highest for Family Life, Housing; Lowest for Household Income Gallup also measures U.S. adults’

degrees of satisfaction and dissatisfaction with the nine specific life

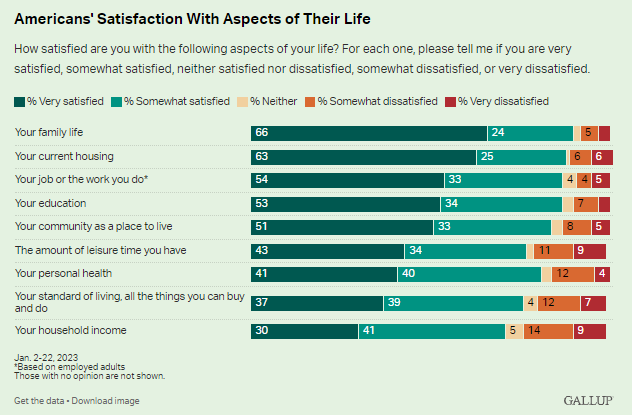

aspects. Majorities of Americans are very satisfied with four of the

elements, including their family life (66%), current housing (63%), education

(53%) and community as a place to live (51%). In addition, a majority of

employed Americans are very satisfied with their work (54%). Fewer express such high

satisfaction with the remaining four life elements -- the amount of leisure

time they have (43%), their personal health (41%), their standard of living

(37%) and their household income (30%). However, taking the percentages who

are “somewhat satisfied” into account, no fewer than 71% of Americans are satisfied

with any of these aspects.

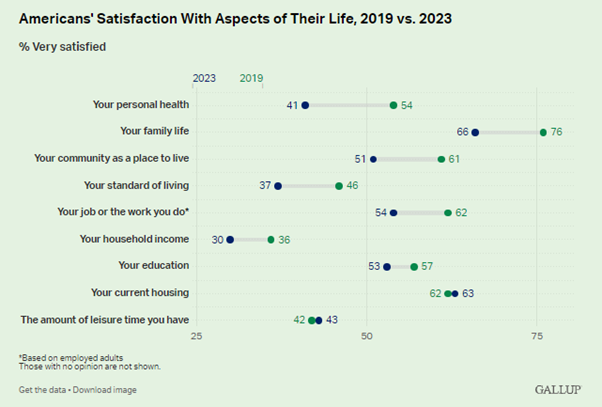

Americans’ levels of high

satisfaction are lower than they were in the

2019 poll on all but two of the life aspects -- housing and

amount of leisure time, for which the readings differ by just one percentage

point. The aspects with the greatest declines in the percentage of U.S.

adults saying they are very satisfied are personal health (-13 points),

family life (-10), community as a place to live (-10), standard of living

(-9) and household income (-6). Among U.S. employees, high satisfaction with

their job has declined by eight points.

Satisfaction with many of the life

aspects was also measured in a 1995 survey, but the results are not

comparable because of differences in the content of the two surveys. Income, Age,

Marital Status, Education Affect Life Satisfaction Income has more of an effect than

any other major demographic factor on Americans’ satisfaction with their

personal life and with most specific life aspects. Those with a higher

household income are more likely than lower-income adults to say they are

very satisfied with all measures except for the amount of leisure time they

have. The biggest differences between these two groups’ satisfaction levels

are seen in household income, standard of living and housing.

Americans’ satisfaction with their

personal life overall and with the specific aspects also differs by other demographic

factors, including age, marital status and college education. By age:

By marital status:

By education level:

Bottom Line Even as the American public

is largely

dissatisfied with the way things are going in the U.S., they

are broadly satisfied with the direction their personal life is taking.

Still, they are now slightly less satisfied with their overall personal life

than they were in the few years before the COVID-19 pandemic. While

satisfaction in the immediate pre-pandemic years was high for the trend,

current attitudes match the historical average. Americans’ latest depressed

satisfaction with their household income and standard of living likely

reflects the toll

inflation has taken over the past year. The pandemic also may

have affected people’s physical

or mental health, their job and

their family life. FEBRUARY

23, 2023 Source: https://news.gallup.com/poll/470888/americans-largely-satisfied-personal-life.aspx

783-43-11/Polls 48%

Of Americans Played A Sport In 2022

Latest Polling on

Sports Fandom

A slim majority of Americans,

particularly Black Americans, support allowing college athletes to profit off

their name, image, and likeness (NIL).

More data here. Latest Polling on

Sports Betting Ipsos explores American attitudes and behavior toward sports betting, showing few