|

BUSINESS & POLITICS IN THE WORLD

GLOBAL OPINION REPORT NO. 778

Week: January 16

– January 22, 2023

Presentation:

January 27, 2023

China’s Pessimistic Gen Z Poses Challenge For Xi Post-COVID

Britons’ Views Of Qatar Remain Very Negative Following 2022

World Cup

Consumer Confidence Sees A Small New Year Bounce As Outlook

For Household Finances Improves

Support For Nurses’ Strikes Lower Than Last Month’s But Blame

Placed Mainly With The Government

Half Of Generation Z Would Prefer To Have Grown Up When Their

Parents Were Children

The Average Check Of Russians In December Increased By 7.5%

The Economic Confidence Of Russians Is In The Positive Zone

Pension Reform: The Majority Of French People Reject The

Project And Support The Strikes

The Propensity Of Italians Towards A Plant-Based Lifestyle Is

Growing

Americans Sour On U.S. Healthcare Quality

For Black History Month, A Look At What Black Americans Say Is

Needed To Overcome Racial Inequality

Canadians Becoming Increasingly Concerned And Regretful About

Their Debt

Canadians Unconvinced If Fining Airlines For Failed Service

Will Help Improve Future Outcomes

64% In Ecuador Do Not Feel Safe Walking Alone At Night

What Do Aussie Consumers Consider When Looking To Purchase

Consumer Electronics

Costs Of Living Increase Around The World, A Survey Across 36

Nations

Will Companies Adopt A Four-Day Working Day In 2023, A Survey

Across 36 Nations

Global Consumer Confidence On The Upswing As New Year Begins,

Among 23 Countries

INTRODUCTORY NOTE

This weekly report

consists of twenty-two surveys.

The report includes four multi-country studies from different

states across the globe.

778-43-23/Commentary: Half Of

Generation Z Would Prefer To Have Grown Up When Their Parents

Were Children

The report

provides a comprehensive outline of what we know currently about

Generation Z based on long-term and high-quality data sources

that allow us to track changing attitudes and values over time.

Key headlines include:

Technical note

(Ipsos MORI)

19 January 2023

SUMMARY OF POLLS

ASIA

(China)

China’s Pessimistic Gen Z

Poses Challenge For Xi Post-COVID

The first

weekend after COVID-19 restrictions ended last month, dozens of

young Chinese jostled in the dark at a heavy-metal concert in a

tiny Shanghai music venue that reeked of sweat and hard liquor.

After three years of lockdowns, testing, economic hardship and

isolation, many of China’s Generation Z--the 280 million born

between 1995 and 2010--had found a new political voice,

repudiating their stereotypes as either nationalist keyboard

warriors or apolitical loafers. Some 62% of China’s Gen Z

worried about job security and 56% worried about prospects for a

better lifestyle, far more than older generations, according to

the Wyman survey conducted in October and released in December.

(Asahi Shimbun)

January 18, 2023

(Singapore)

Chinese New Year Celebrations

Have Traditionally Been About Large Family Gatherings And Lots

Of Feasting

Chinese New Year

celebrations have traditionally been about large family

gatherings and lots of feasting – with delectable meats from

land and sea. But as mainstream awareness of the environmental and human health impact of eating

meat grows, how are attitudes towards meat consumption and

plant-based/vegetarian diets changing in Singapore? Singaporeans

who are trying to eat less meat are more likely to shop local

and in small quantities than the average consumer. Close to

three in five of this segment express a preference for buying

from local businesses (58%) and shopping “little and often” as

opposed to “big and less often” (59%).

(YouGov

Singapore)

WEST EUROPE

(UK)

Britons’ Views Of Qatar

Remain Very Negative Following 2022 World Cup

Now, a YouGov

Political Research survey has revealed that the World

Cup has done little to improve Britons’ opinions of the host

nation. A month before the opening fixture, two-thirds of

Britons (67%) had a negative view of Qatar, a figure which rose

to 72% after the tournament had finished. Only 12% of Britons

have a positive view of Qatar, about the same as before the

World Cup (9%). Among football fans, however, attitudes towards

Qatar have improved somewhat. While fans were more likely to

have an unfavourable opinion of Qatar than the wider population

before the start of the World Cup (78%), this figure has since

fallen slightly to 72%. Nevertheless, few football fans have a

positive view of the gulf state (18%, up from 8%).

(YouGov UK)

January 16, 2023

Consumer Confidence Sees A

Small New Year Bounce As Outlook For Household Finances Improves

Consumer

confidence saw a slight uptick in December 2022, according to

new analysis from YouGov and the Centre for Economics and

Business Research (Cebr). YouGov collects consumer confidence

data every day, conducting over 6,000 interviews a month.

Respondents answer questions about household finances, property

prices, job security, and business activity, both over the past

30 days and looking ahead to the next 12 months.

(YouGov UK)

January 17, 2023

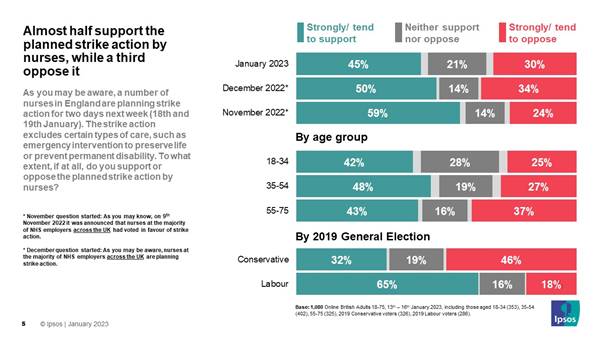

Support For Nurses’ Strikes

Lower Than Last Month’s But Blame Placed Mainly With The

Government

Ipsos’ latest

poll shows 45% support the upcoming strike action by

nurses in England, which is lower than the 50% who supported

similar nurse strikes across the UK in December and 59% in

November. However, still only 3 in 10 (30%) oppose the strikes.

. Support is significantly higher among 2019 Labour voters, 65%

are in favour of the strikes while 2019 Conservative voters are

half as likely to say the same (32%).Support for ambulance

drivers is similar, with 45% in favour and 30% opposed. While

support for these strikes has fallen by 2ppt since December,

opposition has fallen by 7ppt.

18 January 2023

Half Of Generation Z Would

Prefer To Have Grown Up When Their Parents Were Children

Public awareness

of generations in the UK is high, with over nine in ten familiar

with at least one cohort. However, Generation Z have much lower

brand awareness than the Millennial or Baby Boomer generations

at present. Despite this, the sense of belonging to their cohort

is far stronger among Gen Z and the Millennials than it is for

older generations. Generation Z appear to be more financially

optimistic than Millennials when they were the same age.

(Ipsos MORI)

19 January 2023

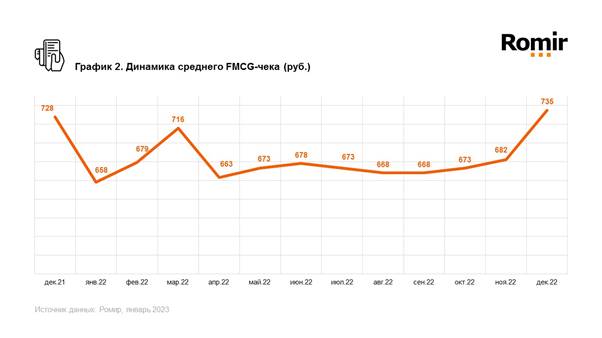

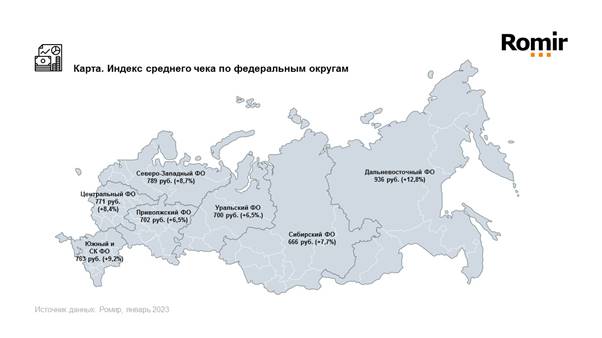

(Russia)

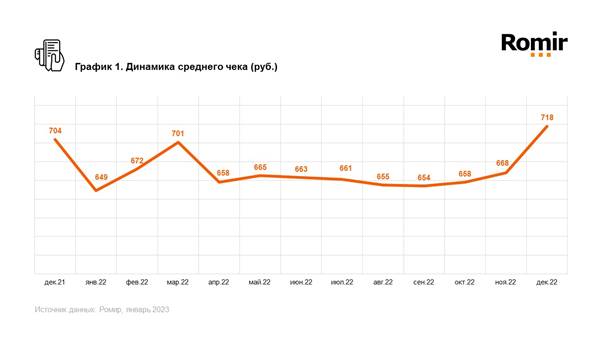

The Average Check Of Russians

In December Increased By 7.5%

As part of a study of consumer behavior,

Romir calculated the index of the average check of a Russian

citizen (an index of the average value of total purchases and an

index of purchases of FMCG goods) for December 2022. The index

of the average check of a Russian in December increased by 7.5%

(50 rubles) compared to the previous month and amounted to 718

rubles. In annual dynamics, the index grew by 1.9% (14 rubles).

(Romir)

January 18, 2023

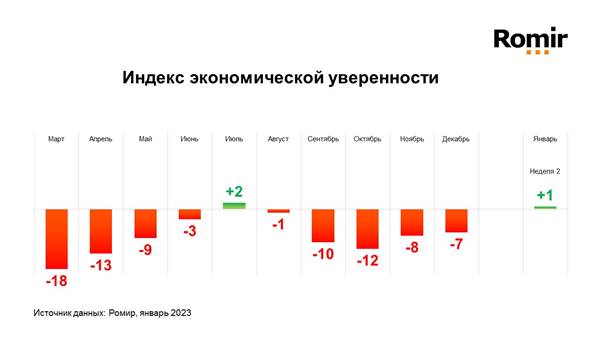

The Economic Confidence Of

Russians Is In The Positive Zone

As part of

regular monitoring of the impact of the socio-economic situation

on human behavior and moods, the Romir research holding assessed

the level of economic confidence of Russians. By mid-January

(between January 9 and 15) *the index of economic confidence of

Russians went into the positive zone and amounted to +1. More

positive moods were noted among TV viewers. The index was

+6. Among those who have YouTube as a source of information, the

index was -19.

(Romir)

January 19, 2023

(France)

Pension Reform: The Majority

Of French People Reject The Project And Support The Strikes

95% of French people have heard of the reform project, including

70% who even say they know exactly what it contains. This

notoriety concerns all categories of French people. If the

youngest are the least well informed, 89% of 18-24 year olds

have heard of it and almost one in two (48%) can clearly see

what the project contains. The French are therefore well

informed about the reform planned by the government.

(Ipsos France)

January 18, 2023

(Spain)

84% Of The Spanish Population Declares That The Increase In Energy

Prices Has A Significant Impact On Their Purchasing Power

Since the second

half of 2021 there has been a sharp increase in energy prices in

the EU and worldwide. The price of fuels has risen further as a

result of the war in Ukraine. After almost a year since the

start of the Ukrainian war and its direct impact on rising

energy prices, more than 80% of people in Europe now agree that

this rise has a significant impact on your purchasing power.

(Ipsos Spain)

19 January 2023

(Italy)

The Propensity Of Italians

Towards A Plant-Based Lifestyle Is Growing

In a research

conducted by BVA Doxa for Just

Eat, where it was highlighted that over

60% of those who tried to change their food style retraced their

steps after an average period of 6 months. The survey

provides us with a clear overview of the food habits of

Italians: most are omnivores (85%), however in the

younger age groups (18-30 years) a high share of

people emerge who have decided to undertake different food

styles including the vegetarian/vegan

regime or the flexitarian regime.

(BVA Doxa)

20 January 2023

NORTH AMERICA

(USA)

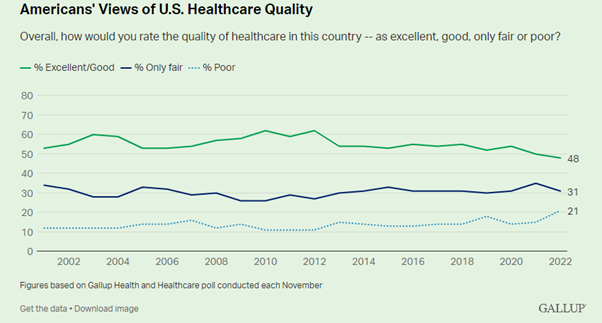

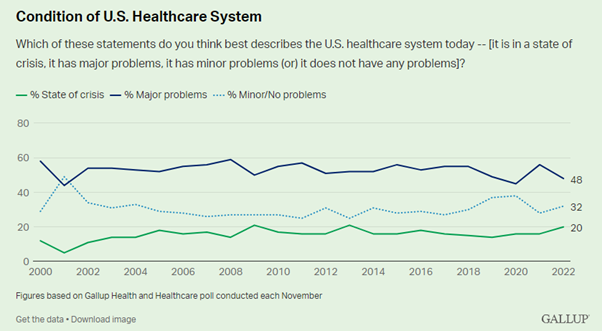

Americans Sour On U.S.

Healthcare Quality

For the first

time in Gallup’s two-decade trend, less than half of Americans

are complimentary about the quality of U.S. healthcare, with 48%

rating it “excellent” or “good.” The slight majority now rate

healthcare quality as subpar, including 31% saying it is “only

fair” and 21% -- a new high -- calling it “poor.” The latest

excellent/good rating for U.S. healthcare quality is just two

percentage points lower than in 2021; however, it is well below

the 62% high point twice recorded in the early 2010s. It also

trails the average 55% reading since 2001.

(Gallup)

JANUARY 19, 2023

For Black History Month, A

Look At What Black Americans Say Is Needed To Overcome Racial

Inequality

More than

six-in-ten Black adults (63%) say voting is an extremely or very

effective strategy for Black progress. However, only around

four-in-ten (42%) say the same about protesting.

There are

notable differences in these views across political and

demographic subgroups of the Black population.Black Democrats

and Democratic-leaning independents are more likely than Black

Republicans and Republican leaners to say voting is an extremely

or very effective tactic for Black progress (68% vs. 46%). Black

Democrats are also more likely to say the same about supporting

Black businesses (63% vs. 41%) and protesting (46% vs. 32%).

(PEW)

JANUARY 20, 2023

(Canada)

Canadians Becoming

Increasingly Concerned And Regretful About Their Debt

Consistent with

last quarter, nearly half (45%, -1) of Canadians report that

they are $200 away or less from not being able to meet all of

their financial obligations, including three in ten (30%,

unchanged) who say they already don’t make enough to cover their

bills and debt payments. While a those at risk of insolvency

remains steady, the average amount of money that Canadians have

left over at the end of the month has notably increased to $851,

up $197 from the previous quarter, as Canadians are likely to be

more cautious about their spending and reconsidering what they

think are necessities.

(Ipsos Canada)

16 January 2023

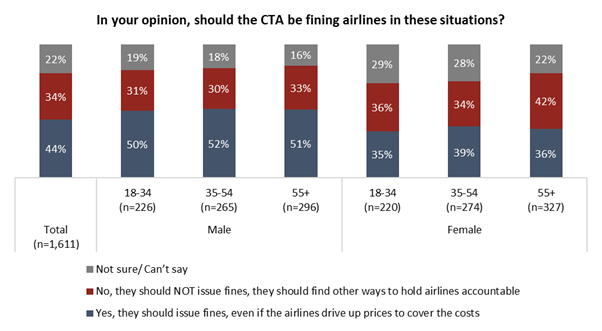

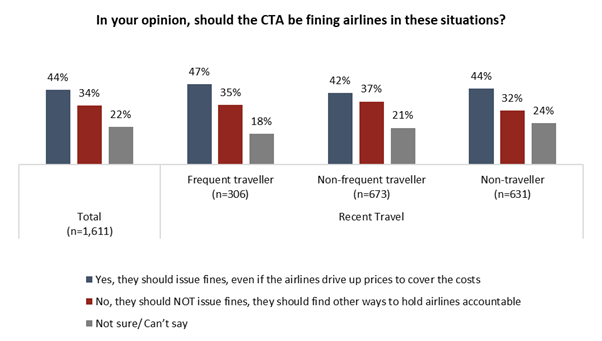

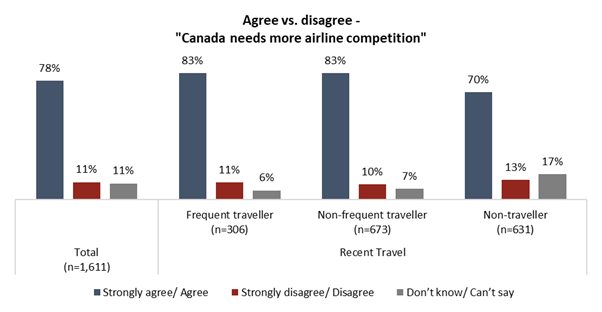

Canadians Unconvinced If

Fining Airlines For Failed Service Will Help Improve Future

Outcomes

New data from

the non-profit Angus Reid Institute finds Canadians as likely to

blame the weather (70%) as the airlines and rail companies (68%)

for the holiday travel chaos. One-in-three (33%) point the

finger at the federal government. A similar number (30%) blame

the travellers for putting themselves in the situation. Those

affected are most likely to blame the weather (54%) for dumping

snow on their holiday plans, but they do so at a lower rate than

those who avoided the travel snarls completely (71%).

(Angus Reid

Institute)

January 18, 2023

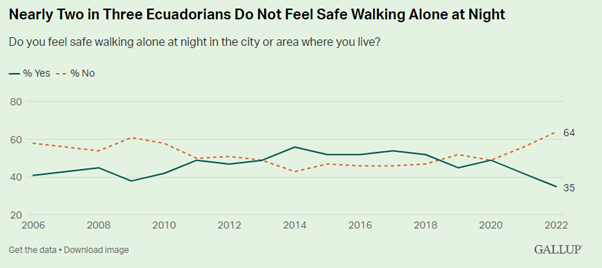

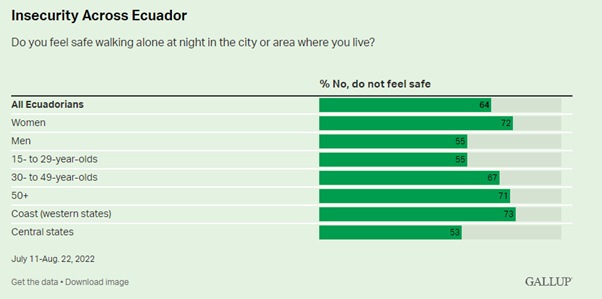

(Ecuador)

64% In Ecuador Do Not Feel

Safe Walking Alone At Night

Ecuador now

ranks as the least safe country in Latin America, thanks to

escalating gang violence, drug trafficking and civil unrest in

2022. Nearly two in three (64%) Ecuadorians interviewed last

year said they do not feel safe walking alone at night where

they live, while just 35% said they do. This situation

represents a rapid and dramatic change in fortunes for the

Andean country. Just five years ago, Ecuador ranked among the

safest countries in the region, with a majority of its

population feeling safe (52%) walking alone at night.

(Gallup)

JANUARY 20, 2023

AUSTRALIA

Australian Unemployment

Increased To 9.3% In December In Line With The Usual Seasonal

Trends For This Time Of The Year

Unemployment in

December increased 46,000 to 1.38 million Australians (9.3% of

the workforce) although under-employment was down slightly, by

16,000 to 1.36 million (9.1% of the workforce). Overall

unemployment and under-employment was up 30,000 to 2.74 million

(18.4% of the workforce). Australian employment decreased by

12,000 to 13,568,000 in December. The decrease was driven by a

drop in full-time employment, down 97,000 to 8,771,000, although

part-time employment increased in line with the usual seasonal

trends, up by 85,000 to 4,797,000.

(Roy Morgan)

January 19, 2023

What Do Aussie Consumers

Consider When Looking To Purchase Consumer Electronics

Sustainability

and data safety have emerged as hot topics in the electronics

goods sector in recent years. Data from YouGov’s latest report, Consumer electronics: Safety and sustainability in 2023, indicates

that consumers in Australia are indeed placing an increasing

focus on them, with sustainability and data privacy moving up in

the purchase decision hierarchy. Three-quarters of Australian

consumers state price as the most important factor in future

electronics purchases (77%), however price is less of a priority

for younger age groups (under 34s).

(YouGov

Australia)

January 19, 2023

MULTICOUNTRY STUDIES

Costs Of Living Increase

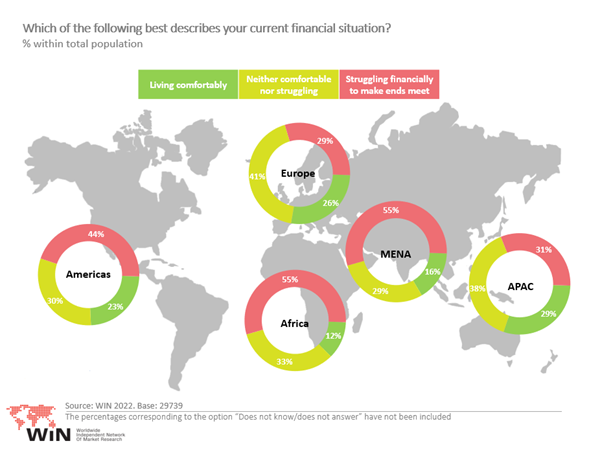

Around The World, A Survey Across 36 Nations

The cost of

living has increased due to various factors, including COVID-19

and political and economic crises affecting many countries. Many

people struggle financially, so much so that only 25% of

citizens worldwide are living comfortably. People

between the ages of 35 and 44 are among the most affected ones, probably

because of the costs related to supporting a family.

On a country level, Argentina

(76%), Lebanon (69%) and Chile (65%) are among the countries

with the highest percentage of population expressing financial

difficulties.

(WIN)

16 Jan 2023

Source:

https://winmr.com/the-costs-of-living-increase-around-the-world/

Will Companies Adopt A

Four-Day Working Day In 2023, A Survey Across 36 Nations

Brazil's number

is in line with the global average, which is 37%. Residents of

the United Arab Emirates, with 68%, are the ones who believe

most in a reduction in working hours. India, with 63%, and

Indonesia, with 54%, complete the top of the list. At the other

end of the ranking are Japan (15%), Sweden (22%) and Argentina

(22%). Global data indicate that the debate on reducing working

hours is far from a consensus.

(Ipsos Brazil)

January 17, 2023

Global Consumer Confidence On The Upswing As New Year Begins,

Among 23 Countries

The Global

Consumer Confidence Index is the average of all surveyed

countries’ National Indices. This month’s installment is based

on a monthly survey of more than 17,000 adults under the age of

75 from 23 countries conducted on Ipsos’ Global Advisor online

platform. This survey was fielded between December 23, 2022 and

January 6, 2023. This month, Mexico (+2.0), Italy (+1.9), and

China (+1.5) are the only countries to show a significant

month-over-month gain in their National Index (i.e., 1.5 points

or more). However, for the second consecutive month, no country

shows a significant decline.

(Ipsos Canada)

19 January 2023

Source:

https://www.ipsos.com/en-ca/global-consumer-confidence-upswing-new-year-begins

One Year In, Global Public

Opinion About The War In Ukraine Has Remained Remarkably Stable,

Survey Across 28 Countries

As the war in

Ukraine nears the one-year mark, nearly two-thirds (64%) of

adults across 28 countries still report closely following news

about it. A new Ipsos survey finds that global public opinion

about the conflict has not changed much since the weeks

following the country’s invasion and that citizens of most

western nations remain steadfast in their support of Ukraine.

However, the survey points to some risks of fatigue. At the

global level, fewer now agree that their country should take in

Ukrainian refugees (66%, down 7 points since March-April 2022)

and that “doing nothing in Ukraine will encourage Russia to take

further military action elsewhere in Europe and Asia” (63%, down

5 points). Also, slightly more now agree that “the problems of

Ukraine are none of our business and we should not interfere”

(42%, up 3 points).

(Ipsos Global)

20 January 2023

Source:

https://www.ipsos.com/en/war-in-ukraine-january-2023

ASIA

778-43-01/Polls

China’s

Pessimistic Gen Z Poses Challenge For Xi Post-COVID

It was the kind

of freedom young Chinese had demanded in late November in

protests against the zero-COVID policy that became the biggest

outpouring of public anger in mainland China since President Xi

Jinping took power a decade ago.

Pacifying a

generation faced with near-record youth unemployment and some of

the slowest economic growth in nearly half a century presents a

policymaking challenge for Xi, who is just beginning a

precedent-breaking third term. Improving young people’s

livelihoods without abandoning the country’s export-led growth

model poses inherent conflicts for a government that prioritizes

social stability.

This generation

is the most pessimistic of all age groups in China, surveys

show. While the protests succeeded in hastening the end of COVID

curbs, the hurdles Chinese youth face in achieving better living

standards will be harder to overcome, some analysts say.

“As the road

ahead for the youth gets narrower and tougher, their hopes for

the future evaporate,” said Wu Qiang, a former politics lecturer

at Tsinghua University who is now an independent commentator in

Beijing. Young people no longer had “blind confidence and

adulation” towards China’s leaders, he added.

Some Chinese

youth who spoke to Reuters reflected the sense of frustration.

“If they didn’t

change the policy, then more people would protest, so they had

to change,” said 26-year-old Alex, who declined to give her last

name for fear of retribution from the authorities, in an

interview before the Shanghai concert.

“But I don’t

think young people will go back to thinking that nothing bad

ever happens in China.”

‘EDUCATED PESSIMISM’

Young people,

especially in cities, are often at the forefront of protests

globally; students led China’s biggest pro-democracy uprising in

1989, which Beijing crushed in a military crackdown.

But China’s Gen

Z has its own characteristics that present a dilemma for Xi,

some analysts said.

In recent years,

some young Chinese social media users have drawn international

attention for their ferocity in attacking critical views about

China online, including of Beijing’s COVID policies. They became

known as “little pinks,” a term associated with the color of a

nationalist website, and drew comparisons with China’s

aggressive “wolf warrior” diplomats and the Red Guards of Mao

Zedong’s Cultural Revolution.

With the economy

slowing under the weight of pandemic restrictions, a

countertrend emerged, but not quite of the liberal type that

pushes against growing nationalism in the West. Many young

Chinese have been choosing to “lie flat,” a term used to

describe people who have rejected the corporate rat race by

adopting a minimalist lifestyle and doing just enough to get by.

There is no data

on how many Chinese are inclined towards those perspectives.

Brewing under the surface before the protests, however, was one

unifying factor: growing discontent with their perceived

economic prospects.

A survey of

4,000 Chinese by consultancy Oliver Wyman found Gen Z to be the

most negative about China’s economic outlook of all the age

groups. Their peers in the United States, by contrast, are more

optimistic than most preceding generations, according to a study

by McKinsey.

In the United

States, the study released in October showed 45% of

18-to-24-year-olds worried about job stability but scored better

on McKinsey’s gauge of perceptions of future economic

opportunities than all groups except those aged 25-34.

Earlier in the

Xi era, things were looking brighter.

In 2015, a Pew

Research Center study found seven in 10 of Chinese people born

in the late 1980s felt positively about their economic

situation. A whopping 96% felt their living standard was better

than their parents’ at the same age.

“It’s educated

pessimism. It’s based on the facts and the reality that they’re

witnessing,” said Zak Dychtwald, founder of research firm Young

China Group, which examines trends among Chinese youth, of the

mood among young adults.

“I don’t think

these protests would have happened ten years ago, but this young

generation believes they ought to be heard in a way that older

generations didn’t.”

He said further

unrest appeared unlikely in the near term, but the ruling

Communist Party was under pressure to offer “some hope and

direction” to the country’s youth at an annual legislative

meeting in March.

Failure to

deliver such solutions could reignite protests in the long term,

he said.

FIXING THE YOUTH

In a New Year

speech, Xi acknowledged the need to improve the prospects of

China’s youth, without mentioning the protests against his

zero-COVID approach.

“A nation will

prosper only when its young people thrive,” Xi said, without

elaborating on potential policies.

For China’s

stability-obsessed Communist Party, giving Gen Z more political

agency is unthinkable.

Instead,

analysts say Chinese policymakers need to create well-paid jobs

for young people and ensure they thrive economically, like their

parents’ generation, who accepted limited freedoms in exchange

for promised prosperity.

But achieving

that is harder in a slower economy, and some of the policies

that could improve living standards for younger Chinese are in

conflict with other priorities for the world’s second-largest

economy: ensuring the engines behind its 15-fold expansion over

the past two decades keep running, some political analysts and

economists say.

Meeting Gen Z’s

expectations for higher wages would make Chinese exports less

competitive. Making housing more affordable could mean allowing

a sector responsible for a quarter of China’s economic activity

in recent years to collapse.

Xi’s second-term

crackdown on tech and other private sector industries has also

led to job losses and fewer opportunities for young people.

For all the

government’s talk about “common prosperity,” levelling the

playing field for this new generation seems impossible, said

Fang Xu, an urban sociologist at the University of California,

Berkeley.

“Their parents

were able to accumulate such a massive amount of wealth from the

housing market, from private entrepreneurship, and that leap is

not likely to be repeated,” Fang said.

“Levelling the

playing field means devaluing the property market enough that

it’s not impossible for young people to buy a house, but that

would be a huge blow to older generations.”

URGE TO LEAVE

Given the risk

of arrest, most of those who took part in the protests against

COVID restrictions are laying low. It is unclear what their

hopes and plans are or how they vary. But some young people feel

driven to pursue their ambitions elsewhere.

University

student Deng, 19, who spoke to Reuters on the condition of

partial anonymity because of the sensitivity of the situation,

has little hope that she will be able to thrive in China.

“If I want to

stay in China, I have these two choices: stay in Shanghai to

work and take an average office job or listen to my parents,

return to my hometown, take the public servant exam, lie flat,”

said Deng, adding she planned to emigrate instead.

Data from

internet giant Baidu shows online searches for studying abroad

were five times the 2021 average during the two-month lockdown

of Shanghai’s 25 million residents last year. Another spike

occurred during the November protests.

Neither Deng nor

Alex see much room for further dissent in the near future.

“You can either

accept the system or leave China. You can’t change the system

here, the authorities are too powerful,” Alex said.

A few days

later, at the Shanghai venue, Alex found a vantage point among

fellow metal fans for the first time since COVID rules eased.

She took in the sounds of the band, Rat King, her concerns for

the future put aside for one night.

January

18, 2023

Source:

https://www.asahi.com/ajw/articles/14817270

778-43-02/Polls

Chinese

New Year Celebrations Have Traditionally Been About Large Family

Gatherings And Lots Of Feasting

Chinese New Year

celebrations have traditionally been about large family

gatherings and lots of feasting – with delectable meats from

land and sea.

But as

mainstream awareness of the environmental and human health impact of eating

meat grows, how are attitudes towards meat consumption and

plant-based/vegetarian diets changing in Singapore?

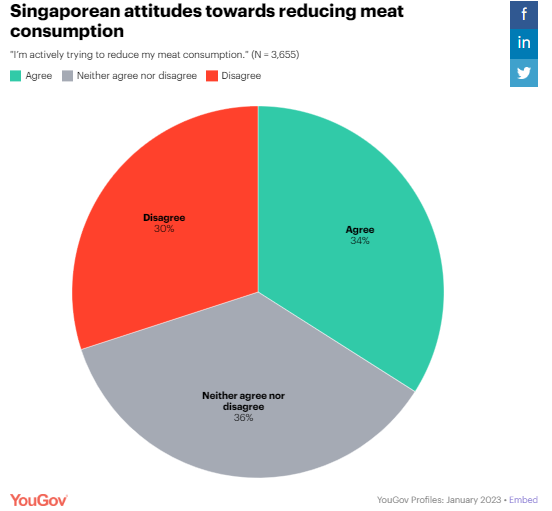

What proportion of Singaporeans are looking to actively reduce

their meat consumption?

Latest data

from YouGov Profiles reveals

that as of January 2023, more than a third of Singaporean

consumers say they are actively trying to reduce their meat

consumption (34%). In contrast, just three in ten are not (30%),

while over a third are undecided about altering their level of

meat consumption (36%) – indicating that they may at least be

considering it.

Notably, about a

third of Singaporeans in each generation remain on the fence

when it comes to changing their amount of meat-eating.

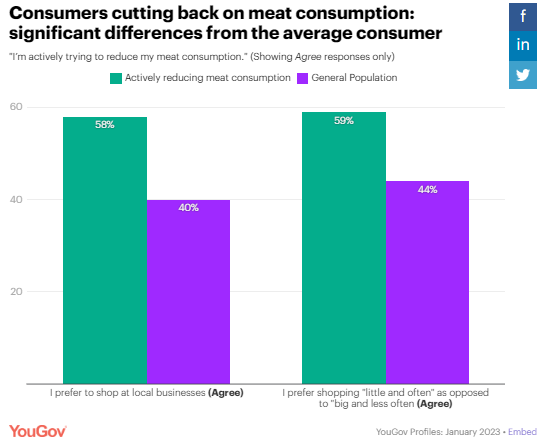

Singaporeans who

are trying to eat less meat are more likely to shop local and in

small quantities than the average consumer. Close to three in

five of this segment express a preference for buying from local

businesses (58%) and shopping “little and often” as opposed to

“big and less often” (59%), compared to less than half of

Singaporean consumers in general (40% and 44% respectively).

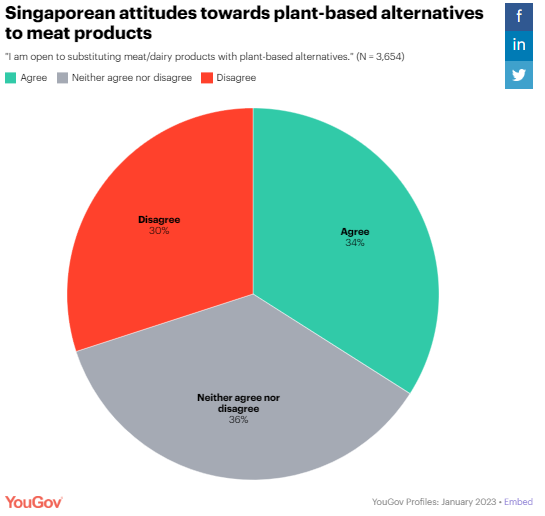

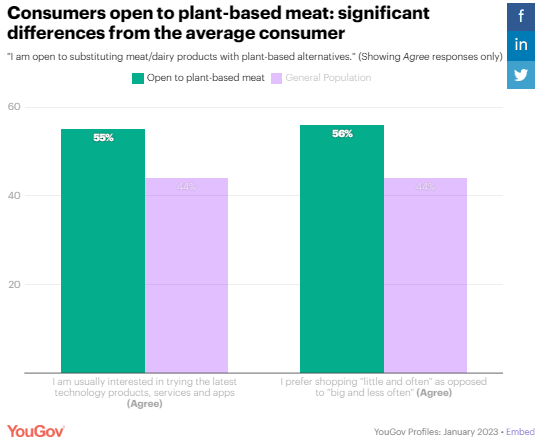

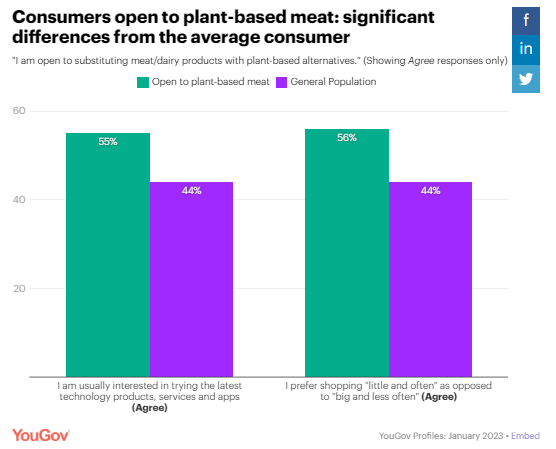

How open are Singaporeans to substituting their meat products

for plant-based alternatives?

Data from YouGov

Profiles also shows that about a third of Singaporeans are open

to substituting meat products they consume with plant-based

alternatives (34%). On the other hand, about the same proportion

are currently undecided (34%), while three in ten say they would

not do so (30%).

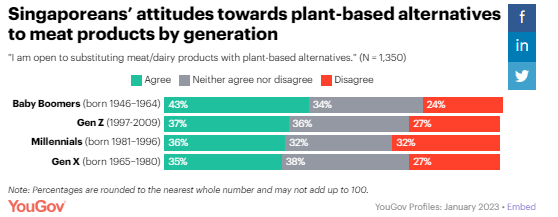

Baby Boomers are

relatively more open to plant-based meat substitutes, with more

than two in five agreeing (43%) compared to 35-37% of younger

Gen Z, Millennial and Gen X consumers. On the flip side,

Millennials are least likely to be open to plant-based meat

substitutes, with nearly a third closed to the idea, compared to

around a quarter for other generations (24-27%).

Singaporeans who

are open to replacing traditional meat products with plant-based

alternatives are more likely to be early tech adopters and

prefer buying small quantities when shopping than the average

consumers. Over half of this segment say they are “usually

interested in trying the latest technology products, services

and apps” (55%) and prefer shopping “little and often” as

opposed to “big and less often” (56%), compared to less than

half of Singaporean consumers in general (both 44%

respectively).

(YouGov

Singapore)

Source:

https://sg.yougov.com/en-sg/news/2023/01/18/singapore-meat-eating-consumption-plant-based/

WEST EUROPE

778-43-03/Polls

Britons’ Views Of Qatar Remain Very Negative Following 2022

World Cup

Opinion of FIFA is now even more negative following their

handling of the tournament

The 2022 World

Cup in Qatar was mired in controversy before a ball had even

been kicked. The country’s human rights record, treatment of

migrant workers and position towards the LGBT community

dominated headlines. But on the field the tournament provided

football fans with arguably the

greatest final of all time as Argentina’s Lionel

Messi finally got his hands on the trophy.

Now, a YouGov Political Research survey has

revealed that the World Cup has done little to improve Britons’

opinions of the host nation. A month before the opening fixture,

two-thirds of Britons (67%) had a negative view of Qatar, a

figure which rose to 72% after the tournament had finished. Only

12% of Britons have a positive view of Qatar, about the same as

before the World Cup (9%).

Before the

tournament, 18% of the general public said it was acceptable for

Qatar to host international sporting events, that figure rising

marginally to 22% following the country’s handling of the World

Cup. Among football fans, the number who think it’s acceptable

for Qatar to host such events increased from 17% pre-World Cup

to 29% after the competition finished.

For both

football fans and the wider population, there is still a

majority (60% in both cases) who think it is unacceptable for

Qatar to host sporting events such as the World Cup.

FIFA’s reputation among Britons is worse now than it was before

the World Cup

Tournament

organisers FIFA threatened to book

any players who planned to wear the OneLove armband to

promote diversity and inclusion.

Two-thirds of

Britons (65%) have an unfavourable view of FIFA since the

tournament ended, down slightly from 69% following the OneLove

armband row on 21-22 November, but higher than the

pre-tournament figure of 54%.

Three-quarters

of football fans (73%) now have a negative opinion of football’s

governing body. While this is lower than the 79% who said they

had an unfavourable opinion of FIFA following the

early-tournament threat of sporting sanctions for those teams

wearing the rainbow armband, it is still significantly higher

than the 62% it was pre-tournament.

OneLove hit proves to be a blip for the FA

Closer to home,

while the FA’s reputation among English people took

a knock over the OneLove armband incident, their

reputation has since bounced back. Prior to the competition, 30%

said they had a favourable view of the FA and 35% an

unfavourable one. After the FA announced that England players

would not be wearing the rainbow armband, those with a positive

view of the organisation fell to 27% and the number with a

negative view increased to 43%. However, numbers have now

returned to pre-Qatar 2022 levels with the FA seen favourably by

33% and unfavourably by 38%.

Football fans in

England have a higher opinion of the FA with 60% holding a

favourable view of the organisation both before and after the

World Cup, although this number did fall to 50% in the fallout

from the OneLove armband row. The number with an unfavourable

opinion has fallen since the same incident from 39% to 33%.

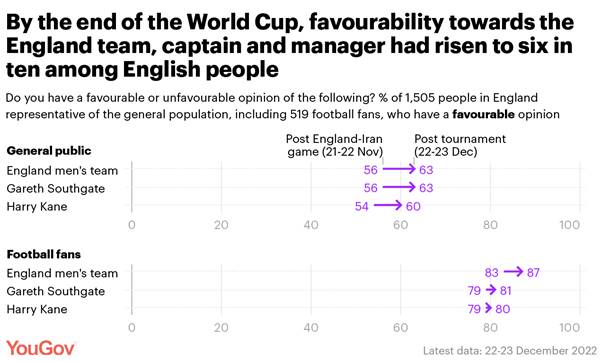

Opinion towards the England team, Gareth Southgate and Harry

Kane is now even more positive

English people’s

opinion towards the England team is even higher post-tournament

than it was at the time of our mid-tournament survey (on 21-22

November, shortly after the England-Iran game). The proportion

of those with a favourable view of the Three Lions has increased

from 56% to 63%.

Similarly, both

Gareth Southgate and Harry Kane have also seen opinions towards

them improve during the World Cup. Those with a favourable view

towards the England manager have risen from 56% to 63% while his

captain has seen positive opinion towards him increase from 54%

to 60%. (There are no

pre-tournament comparison figures for the England team, Gareth

Southgate or Harry Kane).

English football

fans, too, are even more behind their team following their

efforts in Qatar. In our group-stage poll, 83% of fans said they

had a favourable opinion of the men’s national side, this figure

rising to 87% in our post-tournament survey.

Fans’ opinions

of both the team’s manager and captain also remain high with

eight in ten having a favourable opinion of Southgate (81%) and

Kane (80%) since the World Cup finished.

January 16, 2023

778-43-04/Polls

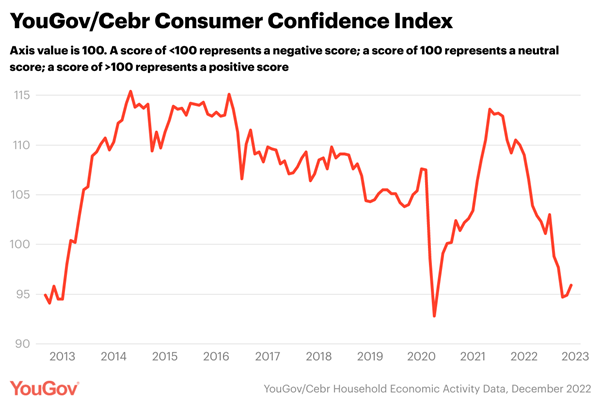

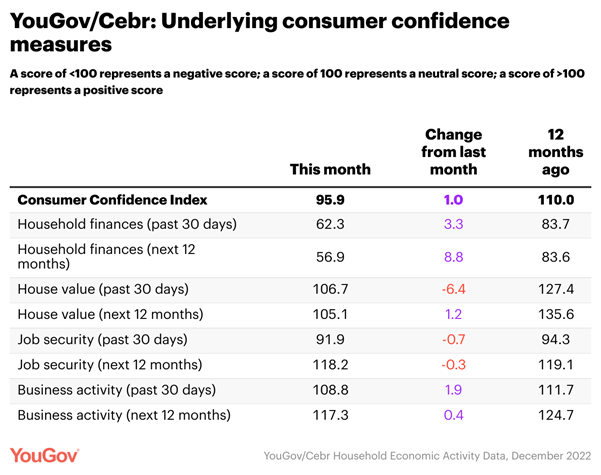

Consumer Confidence Sees A Small New Year Bounce As Outlook For

Household Finances Improves

The improvement

in overall consumer confidence can largely be attributed to a

rise in household finance measures. Retrospective scores saw an

increase of 3.3 points, increasing from 59.0 to 62.3, while

outlook jumped 8.8 points from 48.1 to 56.9. In December 2022,

Bank of England Governor Andrew Bailey suggested that inflation was lower than expected,

and had started to come down from its 41-year high. While the

mood around household finances is still sour – for perspective,

if these scores were recorded a year ago, they would have been

the worst in the history of the index – it nevertheless appears

to be moving in a more positive direction.

Other areas are

more of a mixed bag. Homeowners are a little more optimistic

about the value of their properties over the next 12 months,

with forward-looking measures increasing by 1.2 points from

103.9 to 105.1. But with six consecutive months of

deterioration, short-term measures are in freefall: December saw

a decline of 6.4 points, falling from 113.1 to 106.7.

Meanwhile,

perceptions of job security among employees saw little movement,

with short-term metrics falling by 0.7 points (from 92.6 to

91.9) and outlook by 0.3 points (from 118.5 to 118.2).

Perceptions of business activity over the past 30 days moved up

1.9 points from 106.9 to 108.8, while measures for the next 12

months inched up 0.4 points from 116.8 to 117.2.

January 17, 2023

778-43-05/Polls

Support

For Nurses’ Strikes Lower Than Last Month’s But Blame Placed

Mainly With The Government

From what they

know about the strikes, large majorities continue to feel

sympathy towards nurses (82%) and ambulance workers (80%),

however they are most likely to feel sympathy towards NHS

patients (90%). Around 3 in 5 (61%) are sympathetic towards

unions representing nurses and ambulance workers while just

under half say the same for NHS management (46%). Just a quarter

(26%) feel sympathy for the UK Government, compared to 7 in 10

(70%) who don’t.

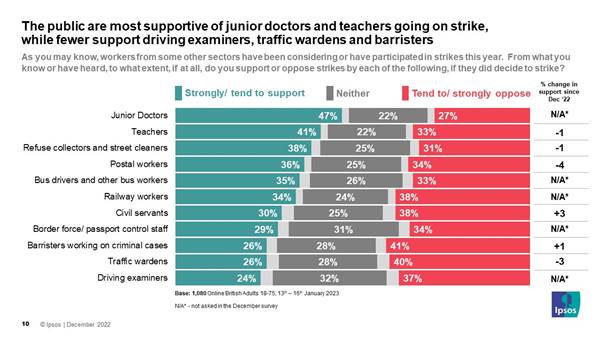

As various

professions vote to start or continue striking, junior

doctors (47%) and teachers (41%) are most likely to be

supported, along with refuse collectors and street cleaners

(38%) and postal workers (36%). Those most likely to be opposed

are barristers working on criminal cases (41%), traffic wardens

(40%), railway workers (38%) and civil servants (38%).

Trade Union Power

Around a third

believe trade unions have too much power in Britain today (34%),

seeing little change on our tracker since June 2022. We have

seen more fluctuation in the proportion who say they have about

the right amount, now 33% believe this is the case, up from 25%

in June of last year. Meanwhile, after a significant drop last

month (30% in September to 19% in December), the proportion who

believe trade unions do not have enough power remains consistent

(19%).

In comparison,

32% say employers have too much power, 44% say they have the

right amount and 10% say they have too much. Only 1 in 10 (11%)

believe workers have too much power, 38% say they have the right

amount while the same proportion (38%) believe they have too

little.

A large majority

say it is important to have trade unions to protect workers’

interests (79%), falling slightly from 83% last September and

85% last June. Only 13% say they are not important.

18 January 2023

Source:

https://www.ipsos.com/en-uk/support-nurses-strikes-lower-last-months-blame-placed-mainly-government

778-43-06/Polls

Half Of

Generation Z Would Prefer To Have Grown Up When Their Parents

Were Children

The report

provides a comprehensive outline of what we know currently about

Generation Z based on long-term and high-quality data sources

that allow us to track changing attitudes and values over time.

Key headlines include:

Technical note

19 January 2023

778-43-07/Polls

The

Average Check Of Russians In December Increased By 7.5%

The average check for FMCG purchases in

December amounted to 735 rubles, which is 7.8% higher (53

rubles) than in November. During the year, the indicator

increased by 1.0% (7 rubles).

In terms of federal districts, the Far

Eastern Federal District (+12.6%) showed the largest increase in

the average check compared to November. The indicator grew least

of all in the Volga and Ural Federal Districts (+6.5% each).

January 18, 2023

Source:

https://romir.ru/studies/romir-sredniy-chek-rossiyan-v-dekabre-vyros-na-75

778-43-08/Polls

The

Economic Confidence Of Russians Is In The Positive Zone

In 2022, the

highest average monthly economic confidence index was recorded

in July (+2). The lowest is in March (-18).

*The index of economic confidence is a

combination of Russians' assessment of the current economic

situation in the country and their expectations regarding the

prospects for its development. The scores are calculated as the

difference between positive and negative responses.

January 19, 2023

Source:

https://romir.ru/studies/romir-ekonomicheskaya-uverennost-rossiyan-nahoditsya-v-polojitelnoy-zone

778-43-09/Polls

Pension

Reform: The Majority Of French People Reject The Project And

Support The Strikes

Announced as the

major project of Emmanuel Macron 's second

five-year term , the pension reform project has sparked many

debates, since its presentation by Elisabeth Borne on January

10. In view of the importance of this project, the media

coverage was significant and consequently the vast majority of

French people have heard of it.

A general rejection on the part of the French of this pension

reform, but support from sympathizers of the presidential party

and the right

This pension

reform project is being rejected by the majority of French

people. 61% say they are

opposed to it, including more than a third (36%) who are even

completely opposed to the reform. While 39% say they

are on the contrary in favour, only 13% say they are completely

in favor of the reform project carried out by Elisabeth Borne.

Support for

reform varies greatly depending on the political orientation of

respondents. Left-wing

sympathizers are mostly opposed (70%). Nevertheless,

this opposition is not uniform in its proportion. Thus, 76% of

supporters of France Insoumise declare themselves opposed to the

reform, against 66% of those of the PS and 63% of those of EELV.

On the side of the National Rally, we also see a frank

opposition to the reform, 75% of the

sympathizers of the party of Marine Le Pen declaring themselves

opposed to the government project.

On the other

hand, Renaissance sympathizers

are overwhelmingly in favor (82%), as are Republican

sympathizers (73%). Emmanuel Macron and Elisabeth

Borne therefore seem to be able to benefit

from the support of their electoral base, extended to the right, in

what promises to be a difficult moment.

Beyond the

political categories , working people

directly affected by the reform are more opposed to it than the

average of the French respondents (67%). This is

particularly the case for manual workers (82%), who are the most

opposed to this project, ahead of employees and intermediate

professions (70% in both cases), while executives are very

divided, 51% between them being in favor of this reform and 49%

being opposed to it. Finally, retirees are mostly in favor of

the reform (57%).

Support for the principle of reforming the pension system, but

which would require reform and a different timetable

The French generally approve of the principle of a pension

reform, 81% considering that the pension

system must be reformed. However, only

23% believe that the pension reform proposed by the government

should be implemented as soon as possible. 15%

consider that this reform should be implemented, but disagree on

the timetable, preferring to wait until the economic and social

situation is better. More than 4 out of 10 French people (43%)

consider that the reform should be done according to

different methods from those proposed by the government, and

19% believe that it is not necessary to reform the pension

system.

Opposition to measures to extend working hours, but support for

certain aspects of the reform

In detail, we

observe that it is above all the measures to extend working

hours that arouse the rejection of the French. 62%

are thus opposed to the gradual postponement of the legal

retirement age from 62 to 64, a particularly strong

rejection among working people (66%). Same

observation for the extension of the contribution period to 43

years, which is opposed by 58% of French people and

62% of active people. Supporters of the left-wing parties and

the National Rally are, unsurprisingly, overwhelmingly opposed

to these two proposals.

Conversely, the

abolition of special pension schemes for new recruits is

approved by 65% of French people. If supporters of

the Republic in March (87%) and Republicans (83%) are largely in

favor, a majority of supporters of the RN also approve of this

measure (61%). Left-wing sympathizers, on the other hand, are

divided on this point. If those of the PS and EELV approve of

this measure (respectively 64% and 72%), those of France

Insoumise reject it (only 38% agree).

Finally, the

establishment of a minimum pension of approximately 1200 euros

gross per month creates consensus, the vast majority

of French people being in favor of it (86%), as are supporters

of all the major political forces.

Opposed to the reform, the French support at this stage the

mobilizations and the strike

While a first

day of mobilization was announced by the unions on Thursday

January 19, 2023, a clear

majority of French people approve of the upcoming mobilizations

against the pension reform (65%, including 40% who

totally approve of them). This support is stronger among

supporters of parties opposed to the pension reform, in

particular France Insoumise (90% support the mobilizations). The

same goes for the strike movement, supported by 59% of French

people (including 37% who fully support it) and which receives

particularly strong support from supporters of France Insoumise

(83%).

In this

context, one in five French

people (20%) declare that they have the certain intention of

demonstrating against the pension reform, while 22%

of working people and students also declare that they have the

certain intention of going on strike against this

reform. Supporters of left-wing parties and the Rassemblement

National are the most likely to want to demonstrate or strike

against government reform.

January 18, 2023

778-43-10/Polls

84% Of

The Spanish Population Declares That The Increase In Energy

Prices Has A Significant Impact On Their Purchasing Power

Since the second

half of 2021 there has been a sharp increase in energy prices in

the EU and worldwide. The price of fuels has risen further as a

result of the war in Ukraine. This has also

raised concerns regarding the security of energy supply in the

EU, and Russia's decision to suspend gas deliveries to several

member states has further affected the situation. The

European Commission has proposed the "REPowerEU" action plan,

which aims to make Europe independent of Russian fossil fuels

well before 2030.

Majority support for European measures to address energy

challenges

In this context

more and more people, eight out of ten, agree that the EU should

continue to take steps to reduce its dependence on Russian oil

and gas as soon as possible. Spain (86%) is among the countries

most in agreement with this idea.

While this

independence arrives, the EU has taken a series of measures to

guarantee the energy supply and mitigate the increase in energy

prices, measures that receive very high support from the

Europeans. More than eight in ten agree that the EU must protect

critical infrastructure such as oil pipelines and internet

cables, that the price of electricity should not depend on the

price of gas, that the war in Ukraine makes it more urgent than

the Member States invest in renewable energy, and that everyone

should make an effort to reduce energy consumption during peak

hours.

Where there is

not such a large majority (56%), is the idea that the recent

price rises are mainly due to aggressive behavior by Russia. For

its part, Spain shows greater agreement with this statement, 65%

of the population considers it so, ranking among the five

countries that most agree.

Home changes to reduce energy use and bills

The proportion

of people who are willing to take personal measures to mitigate

the effect of rising prices on their pocket is a vast majority

(95%). People are already or would be willing to turn off the

lights when they leave a room for a while, at home or at work,

unplug electronics when not in use, or lower the room

temperature at home or at work, which they already do. half of

the Spanish population (52%)

Approximately

four in ten already use or are willing to use alternatives to

getting around the car or motorbike, such as walking, cycling,

using public transport or carpooling, buying energy-efficient

equipment with a good energy rating, a much less welcome in the

case of Spain, where only 1 in 4 is or would be willing to do

so.

The most

expensive actions or those with the greatest impact on personal

life, although more efficient, are the ones that show the least

adoption, such as adding better insulation in the home, opting

for renewable forms of energy, installing equipment to control

and reduce their consumption of energy and take the train

instead of the plane to get around.

19 January 2023

778-43-11/Polls

The

Propensity Of Italians Towards A Plant-Based Lifestyle Is

Growing

The propensity of Italians towards a plant-based lifestyle is

growing, but for 60% implementing a new diet is difficult. Food

delivery is confirmed as an ally and a stratagem adopted above

all by young people to overcome the initial adaptation phase. On

the occasion of Veganuary, the largest vegan movement in the

world, the data from the BVA Doxa research for Just Eat presents

were presented to analyze how Italians approach new food regimes

such as the vegan diet, the motivations that drive them, the

difficulties they face and the tricks they use to stay on track.

CHANGE YOUR

LIFESTYLE - The beginning of a new year always brings with it a

long list of good resolutions and it is in January that new

goals are set, such as the strong desire to change one's

lifestyle. The need to get back in shape, thanks to the holidays

that have just ended, is the mantra that guides Italians in

choosing a healthier diet. In 2014, Veganuary, the largest vegan

movement, was born in this directionaround the world,

with the aim of inspiring people to try a plant-based diet not

only for their own personal well-being, but also for that of the

planet. A real challenge: if on the one hand the interest in a

plant-based diet is growing, on the other hand implementing new

habits in one's daily life represents a great challenge. The

confirmation comes from a research

conducted by BVA Doxa for Just

Eat, where it was highlighted that over

60% of those who tried to change their food style retraced their

steps after an average period of 6 months .

PLANT-BASED –

The survey provides us with a clear

overview of the food habits of Italians: most are omnivores

(85%), however in the younger

age groups (18-30 years) a high share of people

emerge who have decided to undertake different food styles

including the vegetarian/vegan

regime or the flexitarian regime

, i.e. an omnivorous diet, with a preference for veggie

solutions and the occasional consumption of animal-derived

products. The reasons are to be found above all in the growing

interest in the theme of sustainability , which leads

them to try to integrate low environmental impact solutions into

their diet as much as possible.

BENEFITS AND

DIFFICULTIES - If we look at the past year, 4

out of 10 Italians changed their diet in 2022 ,

mainly guided by the desire to improve their physical

well-being, and they are carrying it out with the intention of

making it a definitive choice. However, 61%

retraced their steps after a period of about 6 months ,

due to the difficulties encountered in the excessive

rigidity in terms of times and quantities of meals (40%) ,

as well as in the preparation

of the latter (34%) . Not only that, those who

reflect themselves within a modern profile and therefore

consider themselves worldly and busy people, believe that thedifficulty

reconciling one's eating style with the desire to order food at

home , may represent an important barrier in the

adoption of a new regimen.

The research

also reveals how for 6 out of

10 Italians these difficulties emerge both in the initial phase

of the path and in its maintenance . Only those who

identify with the portrait of the sportsman and who are therefore used to leading nutritional

lifestyles suitable for supporting performance and achieving

certain results, declare that they do not experience particular

difficulties when approaching new diets . Starting

a new food journey, on the other hand, is particularly tiring

for the 25-30 age group , but once the adaptation

phase has been overcome, maintaining the new nutritional plan is

carried out with extreme ease. This is also thanks to the

positive effectswhich manifest themselves over time,

as confirmed by as many as 88% of

the interviewees.

THE NEW FOOD

REGIME – Among the other difficulties encountered by those who

choose to start a new food journey, there is also the discipline

in respecting the very rules of the new regime, which

is particularly difficult for the 45-64

age group (53 %) , while the younger target (18-24

years), claims to experience some difficulties

in relating to their families and being able to combine food

style/dietary regimen with the family's daily habits (23%) .

The approach

towards a more balanced diet therefore involves a great spirit

of adaptation, which often leads to a twofold attitude: the

new rules are adopted immediately (57%) , especially

in the 45-64 age group and by those who decides to implement a

new lifestyle for health reasons, or

gradually (43%) , as happens in the 18-24 age group,

who gradually change some aspects of their daily menu.

STRATAGEMS AND

FOOD DELIVERY - To deal with the change, various stratagems are

also put in place , including the organization

of meals with care and attention to

eating only at certain times of the day, necessary to compensate

or avoid the mistakes that the 90% say they do when

implementing a new regimen. In particular, the youngest group

(18-24 years) declares that they do so often because they find

it difficult to control the

lack of certain foods , but the 45-64 age group is

the most "transgressive": 76% in fact declare that they eat

unexpected food.

Among the

stratagems adopted, a very interesting fact stands out: 6

out of 10 Italians in fact declare that they order food at home

to respect their diet . The 25-30 age group and those

who start a new path gradually declare that they often rely on

their trusted food delivery service, driven above all by the practicality of receiving the ready meal (50%) and by the possibility

of ordering food when I'm away from home/city (34%) . This

is especially true when you approach lifestyles that are often

very distant from your usual diet, as happens with veganism or

vegetarianism.

20 January 2023

Source:

https://www.bva-doxa.com/il-food-delivery-nel-mese-del-veganuary/

NORTH AMERICA

778-43-12/Polls

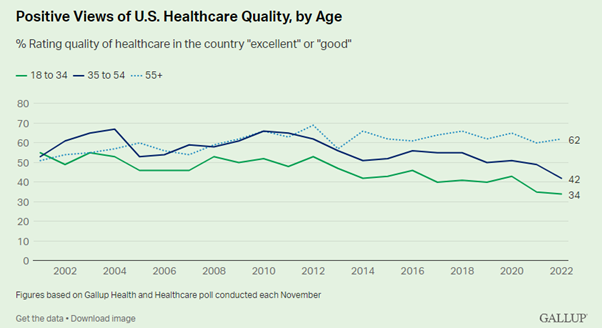

Americans Sour On U.S. Healthcare Quality

These findings

are from Gallup’s annual Health and Healthcare survey. The

latest update was conducted Nov. 9-Dec. 2, 2022.

A key reason

views of U.S. healthcare quality have been trending downward in

recent years is that Republicans’ positive ratings have been

subdued since President Donald Trump left office. Currently, 56%

of Republicans rate healthcare quality as excellent or good,

whereas 69% felt this way in 2020 and 75% in 2019. Republicans’

views of healthcare quality also dropped in 2014 after

implementation of the Affordable Care Act before rebounding

under Trump. Meanwhile, Democrats’ positive ratings have been

steady at a lower level (currently 44%).

Additionally,

since 2012, public satisfaction with healthcare has trended

downward among middle-aged and younger adults, while remaining

high among those 55 and older. Whether this change (seen across

party lines) stems from rising healthcare costs for those not on

Medicaid, perceived changes brought about by the ACA, or

something else isn’t clear. The more recent declines among young

adults may reflect changes to healthcare that have taken place

amid the COVID-19 pandemic or curtailed access to abortion since

the Supreme Court’s Dobbs decision.

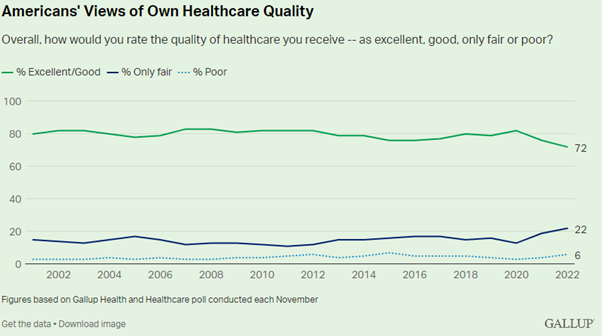

Positive Views of Own Healthcare Quality Also Shrink

Americans’

evaluations of the quality of healthcare they personally receive

are also at a low ebb -- albeit higher than their U.S. rating --

with 72% giving it excellent or good marks. This low reading has

been two years in the making, with the metric falling six points

to 76% in 2021 and another four points in the past year.

The initial

decline was seen about evenly across all age groups, while the

drop in 2022 is exclusively among adults 18 to 34. Barely half

of this younger age group (53%) is now upbeat about the quality

of care they receive, versus 72% of those 35 to 54 and 85% of

those 55 and older.

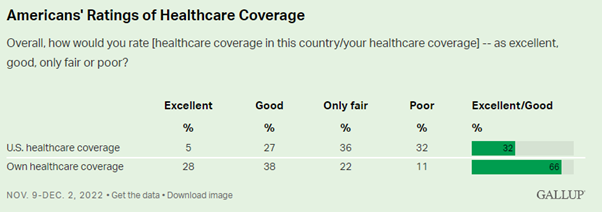

No Change in Views of Healthcare Coverage

The same poll

asks Americans to rate healthcare coverage -- both in the nation

and their own. The ratings gap between these is even wider than

that seen for healthcare quality, with 32% of Americans

considering healthcare coverage nationally to be excellent or

good versus 66% rating their own coverage this highly.

Unlike

healthcare quality, however, these are not the worst ratings for

healthcare coverage, historically. The national rating of 32% is

similar to 2021’s 29% and equal to the average from 2001 to

2021. And while Americans’ positive rating of their personal

coverage is down five points from 2021, the figure has been as

low as 63% previously (in 2005).

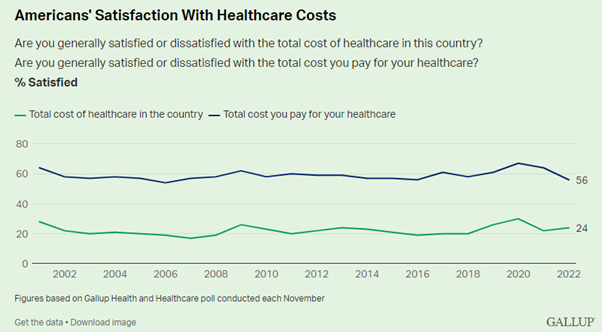

Cost Remains a Pain Point

Public

satisfaction with the total cost of healthcare in the U.S. is

fairly typical of what it has been over the past two decades,

with just 24% satisfied and 76% dissatisfied. The percentage

satisfied has averaged 22% since 2001, only once straying more

than a few points from that -- in 2020 during the pandemic, when

30% were satisfied.

Meanwhile, amid

high inflation in 2022, 56% of Americans report being satisfied

with the total cost they have to pay for healthcare -- the

lowest Gallup has measured since 2016. The lowest in the trend

was 54%, recorded in 2006.

Two-Thirds Still Diagnose System With Major Problems or Worse

Perhaps

reflecting their increasing concerns about healthcare quality,

Americans’ perception that the U.S. healthcare system is in a

state of crisis has grown to 20%, the highest since 2013.

However, the 68% overall saying it is in crisis or has major

problems is similar to the figure in most years from 2002 to

2021.

Bottom Line

For most of

Gallup’s tracking of Americans’ views on healthcare since 2001,

there was a clear distinction between the high regard people had

for the quality of care in the country versus the problems they

saw in healthcare administration, including coverage and cost.

That is no longer the case, with public praise for U.S.

healthcare quality dipping below 50% and the slight majority now

viewing quality as only fair or poor.

Some of this

shift reflects partisan positioning, because since

implementation of the ACA in 2013 under former President Barack

Obama, Republicans have been less likely to offer a positive

assessment of healthcare quality under Democratic presidents (as

they are now under President Joe Biden) than they were under

Trump or, before that, under George W. Bush. But the shifts by

age suggest additional factors are at work.

Even as they

lament the cost, a majority of Americans continue to have high

regard for the quality of their own healthcare and healthcare

coverage. Yet even their own healthcare quality ratings are not

what they once were. Should these continue to worsen, Americans

may be less resistant to rocking the U.S. healthcare boat. That

could, in turn, influence the types of policy changes they may

be willing to accept in the furtherance of improved public

health outcomes.

JANUARY 19, 2023

Source:

https://news.gallup.com/poll/468176/americans-sour-healthcare-quality.aspx

778-43-13/Polls

For

Black History Month, A Look At What Black Americans Say Is

Needed To Overcome Racial Inequality

Black History

Month originated

in 1926 as Negro History Week. Created by Carter G.

Woodson, a Black historian and journalist, the week celebrated

the achievements of Black Americans following their emancipation

from slavery.

Since 1928, the

organization that Woodson founded, the Association for the Study

of African American Life and History, has selected an annual

theme for the celebration. The theme for 2023, “Black

Resistance,” is intended to highlight how Black

Americans have fought against racial inequality.

Black Americans’

resistance to racial inequality has deep roots in U.S. history

and has taken many forms – from slave

rebellions during the colonial era and through the

Civil War to protest

movements in the 1950s, ’60s and today. But Black

Americans have also built

institutions to support their communities such as

churches, colleges and universities, printing presses, and

fraternal organizations. These movements and institutions have

stressed the importance of freedom, self-determination and equal

protection under the law.

Black Americans

have long articulated a clear vision for the kind of social

change that would improve their lives. Here are key findings

from Pew Research Center surveys that explore Black Americans’

views about how to overcome racial inequality.

How we did this

Most Black

adults see voting as

an extremely or very effective strategy for helping Black people

move toward equality, but fewer than half say the same about

protesting. More than

six-in-ten Black adults (63%) say voting is an extremely or very

effective strategy for Black progress. However, only around

four-in-ten (42%) say the same about protesting.

There are

notable differences in these views across political and

demographic subgroups of the Black population.

Black Democrats

and Democratic-leaning independents are more likely than Black

Republicans and Republican leaners to say voting is an extremely

or very effective tactic for Black progress (68% vs. 46%). Black

Democrats are also more likely to say the same about supporting

Black businesses (63% vs. 41%) and protesting (46% vs. 32%).

Views also

differ by age. For example, around half of Black adults ages 65

and older (48%) say protests are an extremely or very effective

tactic, compared with 42% of those ages 50 to 64 and 38% of

those 30 to 49.

Black Americans say Black Lives Matter has done

the most to help

Black people in recent years. Around four-in-ten

Black adults (39%) say this, exceeding the share who point to

the NAACP (17%), Black churches or other religious organizations

(13%), the Congressional Black Caucus (6%) and the National

Urban League (3%).

Black Democrats

are more likely than Black Republicans (44% vs. 26%) to say

Black Lives Matter has done the most to help Black people in

recent years. And Black adults with at least a college degree

are more likely than those with less education (44% vs. 37%) to

say Black Lives Matter has done the most.

Some Black adults see Black-owned

businesses and

Black-led communities as effective remedies for inequality. When

it comes to moving Black people toward equality, about

four-in-ten Black adults (39%) say having all businesses in

Black neighborhoods be owned by Black people would be an

extremely or very effective strategy. Smaller shares say the

same about establishing a national Black political party (31%)

and having all the elected officials governing Black

neighborhoods be Black (27%).

While none of

these strategies have majority support among Black adults,

certain groups are more likely than others to say they would be

effective. Those who say being Black is at least very important

to their identity are especially likely to say each of the three

strategies are effective, for example.

Those with a

high school education or less are more likely than college

graduates to say establishing a national Black political party

would be effective at achieving equality for Black people.

Meanwhile, younger Black adults (ages 18 to 49) are more likely

than older ones (50 and older) to say Black officials governing

Black neighborhoods would help make progress toward equality.

The vast majority of Black adults say the prison

system needs significant changes for

Black people to be treated fairly. That includes a

majority of Black adults (54%) who say the prison system needs

to be “completely rebuilt” in order to ensure fair treatment.

Groups especially likely to say this include Black Democrats and

those who say being Black is extremely or very important to how

they see themselves.

Far smaller

shares of Black adults say the prison system requires only minor

or no changes, though this view is more common among Black

Republicans and those who say being Black is somewhat, a little

or not at all important to their identity.

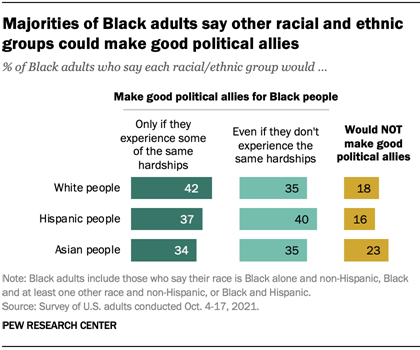

Clear majorities of Black adults say people of other races or

ethnicities could make

good political allies for

Black people. About four-in-ten Black adults (42%)

say White people would make good political allies only if they

experience the same hardships as Black people; another 35% say

White people would make good political allies even if they don’t

experience these same hardships. Around one-in-five Black adults

(18%) say White people would not make good political allies.

About

four-in-ten Black adults (37%) say Latinos would make good

allies only if they experience the same hardships as Black

people, while a similar share (40%) say Latino people would make

for good allies even if they don’t experience the same

hardships. Some 16% of Black adults say Latinos would not make

good political allies.

The views of

Black adults on this question are similar when it comes to Asian

people, though a somewhat higher share (23%) say Asian Americans

would not make good political allies.

JANUARY 20, 2023

778-43-14/Polls

Canadians Becoming Increasingly Concerned And Regretful About

Their Debt

The quarterly

MNP Debt Index has taken a drastic plunge to 77 points, down 15

points from the last quarter and marking an all time low since

the Debt Index was created over 5 years ago. The massive decline

in attitudes about personal debt reflects rising concerns about

interest rates, persistent inflation, and heightened

affordability concerns. The debt index traditionally

deteriorates in December, but this quarter’s decline is

unprecedented, underscoring the anxieties that Canadians have

about their debt situation.

Average Canadians Saving Money During Economic Crisis

All provinces

have experienced an increase in average finances at month-end,

most notably Alberta, with an increase of $404 and placing them

at the top for most leftover funds after essentials are taken

care of. However, Quebec is not far behind with an increase of

$297 to average at $919, followed by Atlantic Canada ($662,

+$262), and Ontario ($845, +$148). Saskatchewan/Manitoba ($753,

+$40) and British Columbia ($787, +$34) has seen a minor

increase, nevertheless any increase while inflation is rampant

is noteworthy.

A third of

Canadians say they plan on reducing their consumer expenses to

make ends meet (36%, +4). Canadians are clearly trying to create

a cushion for themselves by cutting back on their discretionary

spending, which is leaving more in the pockets of the average

Canadian, overall. However, this masks the fact that many are

still struggling as they’re unable to create a cushion, and

those struggles are intensifying as interest rates continue to

rise.

Canadians Personal Debt Rating Takes a Significant Dive

Canadians’ net

personal debt rating has decreased notably to 10 points, a

nineteen-point decrease from last quarter. The significant shift

is a result of fewer Canadians rating their personal debt

situation as ‘excellent’ (31%, -12) and more are rating it as

terrible (21%, +7). The impact of rising interest rates is

beginning to show in consumers’ current debt situation as

Canadians’ are feeling less confident about their current debt.

When Canadians

were asked about their current debt situation compared to one

year ago, a fifth perceive their current debt situation to be

better (21%, -2). However, more Canadians have rated their

current debt situation as much worse compared to a year ago, an

increase of 6 points from the previous quarter (20%). When asked

to forecast their expected debt situation year from now,

slightly fewer Canadians expect their debt situation to improve

(28%, -2) but more believe it will worsen (17%, +6). As

Canadians were asked to consider looking five years into the

future, four in ten (39%, -1) believe their debt situation will

be much better, while more believe that their debt situation

will worsen (14%, +4).

Further Interest Rate Hikes May Reach Breaking Point for Many

Canadians

With interest

rates rapidly rising, Canadians are feeling significantly worse

about their ability to absorb interest rates increases. When

asked their ability to absorb an interest rate increase of 1

percentage point, a fifth (20%, -5) say they are better equipped

to deal with this increase, while more (26%, +9) say their

ability to deal with this increase has worsened. A similar

outcome was observed when the question was rephrased to ask

their ability to absorb an interest rate increase of an extra

$130, one in six (16%, -5) say their ability to absorb this

increase is much better, while over a third (36%, +9) say it is

much worse.

Three in five

Canadians agree they are concerned about the impact of rising

interest rates on their financial situation (62%, +3), while

only half are confident with their ability to cover all

living/family expenses in the next year without going further

into debt (51%, -5). Furthermore, half of Canadians say they

regret the amount of debt they’ve taken on in life (49%, +7) and

that they are concerned about their current level of debt (47%,

+7).

As interest

rates continue to rise, more Canadians say that they’re already

beginning to feel the effects of interest rate increase (68%,

+11), which has triggered the majority of Canadians agree they

will be more careful with how they spend their money (87%, +3).

As Canadians are becoming more conscious with their money, more

Canadians say that as interest rates rise, they are more

concerned about their ability to pay their debts (64%, +9) and

if interest rates go up much more, they will be in financial

trouble (59%, +9)

Women and

Canadians ages 35-54 and 55+ are most likely to agree they will

be more careful with how they spend their money due to rising

interest rates. Canadians with less than $40K household income

and those ages 18-34 and 35-54 are most likely to feel the

effects of interest rate increases, concerned with their ability

to repay their debts, will be in financial trouble, and fear

that rising interest rates moving them close towards bankruptcy.

Canadians Struggling With Affordability Resort to Financial ‘Bad

Habits’ to Make Ends Meet

Canadians are

feeling the pressures of the rising costs of living which is

evident in net affordability for housing and savings continuing

to fall even lower. A growing proportion say it is becoming less

affordable for them to put money aside for savings, and one’s

ability to afford debt payments is also deteriorating. Among a

list of everyday essentials, over half Canadians has noted that

feeding themselves and their family (57%, +5) of and putting

money aside for savings (56%, +7) is less affordable, while

about half say that transportation (50%, +5), clothing or other

household necessities (51%, +6), and housing (45%, +8) is

becoming less affordable.

Canadians are

likely being forced to build more debt to make ends meet.

Compared to December 2021, more say they have paid only the

minimum balance on their credit card (26%, +5), borrowed money

they can’t afford to pay back quickly (18%, +7), paid minimum

balance on their line of credit (17%, +6). One in five say they

will use their savings to pay their bills (21%, +3), while 1 in

10 say they will use their credit card to pay their bills (14%,

+1) or borrow from friends or family (13%, +5).

16 January 2023

778-43-15/Polls

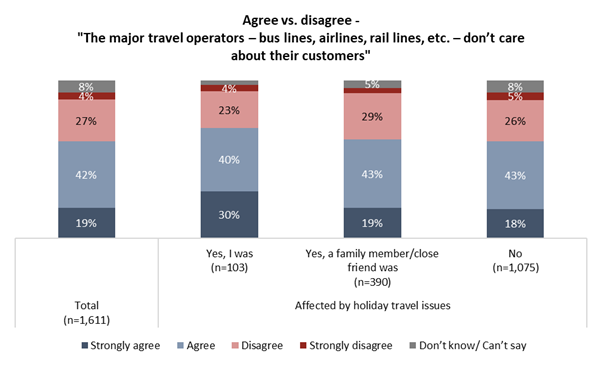

Canadians Unconvinced If Fining Airlines For Failed Service Will

Help Improve Future Outcomes

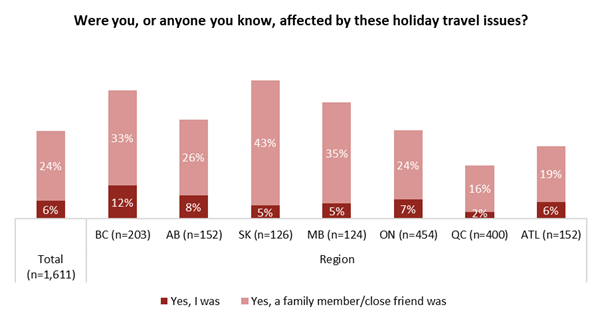

The snowstorms

that iced many Canadians out of their holiday travel plans,

continue to leave airline and railway executives and politicians

on the hot seat.

A similar number

(30%) blame the travellers for putting themselves in the

situation. Those affected are most likely to blame the weather

(54%) for dumping snow on their holiday plans, but they do so at

a lower rate than those who avoided the travel snarls completely

(71%).

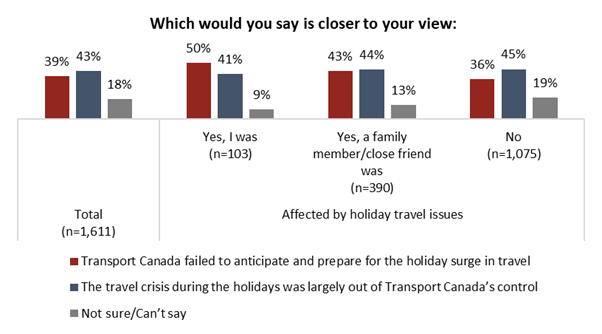

The data also

indicate strong desire from Canadians for more government

regulation to protect consumers from cancellations (78% say

this), but a mixed belief that the regulation already in place

will have much effect. Two-in-five (44%) want the Canadian

Transportation Agency to levy fines against the airlines who

failed to uphold customer rights even if it means the companies

raise airfares to cover them. One-third (34%) want the CTA to

find other ways to hold airlines accountable for cancellations

and delays.

Travel troubles

have become an all-too-familiar phenomenon for Canadians. Last

summer saw persistent delays and long lines at Canadian

airports. To “learn lessons” from the summer, and prepare for

the holiday travel season, Transport Minister Omar Alghabra held

a summit with airlines and airports in

November. Still, two-in-five (39%) believe Transport

Canada failed to prepare for the holiday surge in travel.

Two-in-five (43%) are more likely to absolve the government

ministry and say the December travel mess was out of its

control.

More Key Findings:

About ARI

The Angus Reid Institute (ARI) was

founded in October 2014 by pollster and sociologist, Dr. Angus

Reid. ARI is a national, not-for-profit, non-partisan public