|

BUSINESS

& POLITICS IN THE WORLD GLOBAL

OPINION REPORT NO. 775 Week: December 26, 2022 – January

01, 2023 Presentation: January 06, 2023 1

In 5 Pakistanis Say That The Availability Of Drinking Water At Their Child’s

School Is Bad China’s

FMCG Spend Rises By A Further 3.1% Pharmacy

Users In England Are Currently Satisfied With Pharmacy Services The

Average Check Of Russians Before The New Year Was Lower Than Last Year War

In Ukraine Cited By Canadians As Top International News Story Of 2022 (71%) Opportunities

For Science, Technology And Innovation Open Up In Bogotá Only

10% Of The European Population States That They Have Never Taken Supplements INTRODUCTORY NOTE

775-43-15/Commentary:

One

In Ten Women Say They Have Had Their Drink Spiked (To Spike A Drink Means To

Put Alcohol Or Drugs Into Someone's Drink Without Their Knowledge Or

Permission)

Four in 10 Britons say

they do not think the police would believe them if they reported a drink

spiking As Britons get set to hit the bars, pubs and clubs

to see in the new year, YouGov figures have revealed the extent to which

people say they have ever had their drink spiked. Drink spiking is the adding of alcohol or drugs to

another person’s drink without their knowledge or permission. The aim may be

to incapacitate someone enough to rob or sexually assault them. A new YouGov survey shows that 10% of women say they

have personally had a drink spiked. Meanwhile, 8% say someone in their family

has had a drink spiked, while 10% say a friend has had a drink spiked. One in

seven women (14%) say someone else they know has been a victim of spiking. In

total, 35% of women say they have either had a drink spiked themselves or

know someone who has, or both. Among men, 5% say they have had a drink spiked,

while 7% say members of their family have had their drink spiked. One in

eight men (12%) say a friend of theirs has had their drink spiked and a

further 11% say someone else they know has had a drink spiked. More than a

quarter of men overall (28%) say they know someone who has had a drink spiked

or have experienced it themselves.

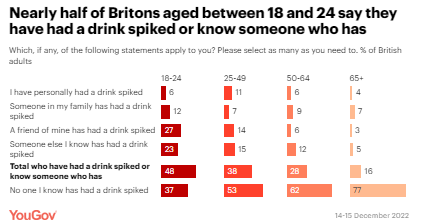

Nearly half of those aged between 18 and 24 (48%)

say they have had a drink spiked or know someone who has. However, it is

those aged between 25 and 49 who are the most likely to say they have

personally had a drink spiked (11%).

How confident do people

feel that reports of drink spiking would be taken seriously? When it comes to how confident Britons are that

police would believe them if they reported having their drink spiked, they

are split over the issue. Four in ten Britons (40%) are very or fairly

confident the police would believe them, but this includes only 8% who say

they are “very confident” they would be taken seriously. Equally, 40% are not

very or at all confident the police would believe them, including 15% who are

“not confident at all”. Britons also have little faith that a venue would

believe them if they told them they had a drink spiked there. Only 29% are

confident that a venue would take them seriously if they had a drink spiked

there compared to 42% who are not very or at all confident a venue would

believe a report of drink spiking under its roof. There is, however, more faith among the British

public that friends and family would take an incidence of drink spiking

seriously. Eight in ten Britons (80%) are confident that both their friends

and their family would believe them if they told them their drink had been

spiked. Half (51%) are “very confident” their family would believe them and

44% say the same about their friends.

(YouGov UK) December 28, 2022 ASIA (Pakistan) 1 In 5 Pakistanis Say That The

Availability Of Drinking Water At Their Child’s School Is Bad A nationally

representative sample of adult men and women from across the country who have

schoolgoing children in their household was asked the following question

regarding, “On a scale of 1 to 5, where 1 is “very bad” and 5 is “very good”,

how would you rank each of the following services provided to your child by

their school?- Availability of drinking water for kids in school” 10% said it

is very bad, 9% said it is bad, 15% said the availability of drinking water

for kids in school is normal, 44% said that this service is good while only

18% said that it is very good. (Gallup Pakistan) December 29, 2022 (China) China’s FMCG Spend Rises By A Further 3.1% Spend on groceries in

urban China was up by 3.1% during the 12 weeks to 7 October 2022, compared

with the same period last year. This growth was mainly driven by shoppers in

the east of the country, where value sales rose 5.2% year-on-year. Consumers

maintained their stockpiling behaviour as COVID outbreaks continued, with

those in the east spending the most per trip. Value sales in hypermarkets and

large supermarkets fell by 4.1% and 4.5% respectively compared to a year ago,

while in small supermarkets and convenience stores value rose by 12.5% and 9%

respectively, driven by growing baskets and an expanding consumer base. (Kantar) 27 December 2022 WEST EUROPE (UK) One In Ten Women Say They Have Had Their Drink

Spiked (To Spike A Drink Means To Put Alcohol Or Drugs Into Someone's Drink

Without Their Knowledge Or Permission) As Britons get set to hit

the bars, pubs and clubs to see in the new year, YouGov figures have revealed

the extent to which people say they have ever had their drink spiked. A new

YouGov survey shows that 10% of women say they have personally had a drink

spiked. Meanwhile, 8% say someone in their family has had a drink spiked,

while 10% say a friend has had a drink spiked. One in seven women (14%) say

someone else they know has been a victim of spiking. In total, 35% of women

say they have either had a drink spiked themselves or know someone who has,

or both. (YouGov UK) December 28, 2022 A New YouGov Survey Has Revealed That One In

Five Britons (21%) Say They Will Make A New Year’s Resolution For 2023 As we bid farewell to

2022, many Britons will be taking the opportunity to make some New Year’s

resolutions. A new YouGov survey has revealed that one in five Britons (21%)

say they will make a New Year’s resolution for 2023, compared to just one in

seven (14%) who say they made a resolution for 2022. The younger generation

are the most likely to vow to make some changes for the new year, with four

in ten 18-24 year olds (41%) saying they’ll make a resolution for 2023

compared to just one in nine of those aged 55 and over (11%). (YouGov UK) December 28, 2022 Pharmacy Users In England Are Currently

Satisfied With Pharmacy Services In England, small chain or

independent pharmacies are the most commonly contacted or visited by the

public (41%), followed by large or medium sized pharmacy chains (35%).

However, their usage is not a frequent occurrence with only around

one-quarter (26%) saying they contact or visit a pharmacy at least monthly,

either for themselves or someone they care for. Meanwhile, one in five (20%)

say they do not normally contact or visit a community pharmacy. In general,

pharmacy users are habitual when it comes to contacting or visiting a

pharmacy: around three-quarters (73%) say they tend to use the same community

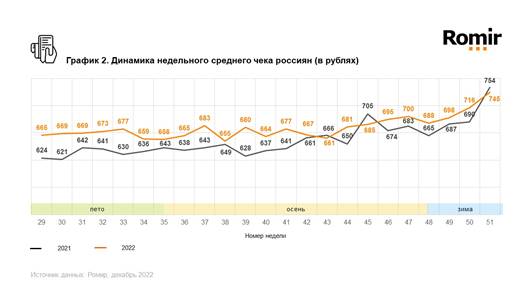

pharmacy. (Ipsos MORI) 29 December 2022 (Russia) The Average Check Of Russians Before The New

Year Was Lower Than Last Year Research holding Romir

presents data on the weekly spending index (WPI) and the weekly average bill

index (WIN). In the period from December 19 to 25, the average weekly

expenses of Russians increased by 2.0% compared to the previous week. Weekly spending index amounted

to 6,346 rubles. In annual dynamics, the index rose by 0.1%. The average check index increased

by 4.0% compared to the previous week and amounted to 745 rubles in monetary

terms. Compared to the same period last year, the average check is 1.2%

lower. (Romir) 29 December 2022 NORTH AMERICA (USA) In Recent Decades, The U S Drinking Rate Has

Consistently Registered Near The Long-Term Average Of 63% The percentage of U.S.

adults aged 18 and older who say they drink alcohol averaged 63% over the

past two years, whereas 36% described themselves as “total abstainers.” The

drinking rate ticks up to 65% when narrowed to adults of legal drinking age,

which is 21 and older nationwide. Relatedly, drinking also differs by

education, with college graduates (76%) and postgraduates (75%) the most

likely to report they drink. This is followed by nearly two-thirds of those

with some college education (65%) and about half of those who haven’t

attended college (51%). (Gallup) DECEMBER 29, 2022 (Canada) War In Ukraine Cited By Canadians As Top

International News Story Of 2022 (71%) A new Ipsos poll conducted

on behalf of Global News finds that Canadians cite some of the major

conflicts occurring this year as the most memorable news stories which shaped

2022. Overwhelmingly, Canadians point to the war in Ukraine as the top

international news story of 2022 (71%). Following this, rising interest rates

and inflation around the world this year (40%) have been deemed most

noteworthy, perhaps only exacerbated by current concerns about the potential

for a recession in 2023. (Ipsos Canada) 28 December 2022 Almost Two Thirds Of Canadians (64%) Rate 2022

As Good For Themselves And Their Family, But Only A Third (34%) Would Say The

Same For The World As

2022 comes to an end, Canadians are reflecting on the events of the past

year. Although a sense of post-pandemic and work-life normalcy have warranted

cautious optimism - high inflation, rising interest rates and uncertain

geopolitics have weighed down Canadians’ year-end outlook. Indeed, a recent

poll conducted by Ipsos on behalf of Global News has shown that Canadians

look back unevenly on this last year for themselves, the country and the

world. Around two thirds (64%) say 2022 was ‘good’ for themselves and their

family, half (51%) say the same for Canada, and only a third (34%) think this

was a good year for the world. (Ipsos Canada) 30 December 2022 (Bogota) Opportunities For Science, Technology And

Innovation Open Up In Bogotá With the contribution to

collective construction and in which actors from academia, civil society

organizations, the public and business sectors participated, Probogotá

prepared a long-term document, in which it is highlighted that one of the

objectives is the construction of an integral link between CteI –Science,

Technology and Innovation– and urban-regional development. The region of

Bogotá and Cundinamarca forms the economic and business center of the

country. Here are 32% of all companies in Colombia. In 2021, the total number

of registered and renewed companies in Bogotá and the 59 municipalities of

the jurisdiction of the Bogotá Chamber of Commerce in the department of

Cundinamarca reached 470,579 companies. (CNC) 28 December 2022 AUSTRALIA One Of Australia’s All-Time Favourite TV

Campaigns Will Be Back On Our Screens From New Year’s Day, Bigger And Better

Than Ever A

group of Norm’s closest friends have recreated the iconic original TV ads,

originally envisioned by Phillip Adams and created by legendary artist, Alex

Stitt in 1975. The original campaign is still fondly

remembered by almost all Aussies who remember the seventies which was largely

funded by the Victorian Government. Considered possibly the most

effective health initiative ever in Australia, the ads promoted the simplest

messages (like get up off the couch

and get active) without preaching or being accusatory in the

least. (Roy Morgan) December 29, 2022 MULTICOUNTRY STUDIES War In Ukraine Destroys Russia's Reputation And

Leaves It At Record Lows; Study Carried Around 33 Nations Shows Before the invasion of Ukraine , almost half

(45%) of people worldwide thought that Russia would have a positive influence

internationally, currently that percentage has fallen 16 points, to

29%. It is clear that Russia's public image has suffered a significant

decline in the immediate aftermath of its invasion of Ukraine nearly nine

months ago, and as the invasion drags on, expectations that Russia will have

a positive influence on world affairs have been diminishing. In

fact, it is the only country or

international institution that has shown a dropped series . (Ipsos Spain) December 28, 2022 Only 10% Of The European Population States That

They Have Never Taken Supplements The Covid-19 pandemic has

brought with it an increase in concern for health and self-care, as

confirmed by the Ipsos study "European attitudes towards food

supplements" . In the last three years, food supplements and

vitamins have become an essential part of the lifestyle of consumers in

Europe., partly as a reinforcement to achieve some immunity against

covid. Almost nine out of ten (88%) people in Europe have consumed a

food supplement at some point in their lives, and the vast majority of them

(93%) have consumed it in the last 12 months, this figure being higher in the

last 12 months. Eastern European countries, such as the Czech Republic (97%),

Romania (97%), Slovenia (96%) and Poland (98%), and also in Finland (94%). (Ipsos Spain) December 29, 2022 Covid-19 Restrictions Feed Economic Contraction

To Drive Down Living Standards In Africa, A Study In 34 African Countries Across 34 countries

surveyed in 2019/2021, six in 10 respondents (61%) reported facing shortages

of medicine or medical services at least once in the previous 12 months, and

nearly as many experienced shortages of clean water (55%) and food (52%).

Nearly four in 10 experienced shortages of cooking fuel (46%) (Figure 1). 1

The weighted Mozambique Round 8 sample is nationally representative except

that it excludes rural Cabo Delgado, comprising 6.3% of the adult population

of Mozambique. (Afrobarometer) 30 December 2022 ASIA

775-43-01/Polls 1 In 5

Pakistanis Say That The Availability Of Drinking Water At Their Child’s

School Is Bad

According to a survey

conducted by Gallup & Gilani Pakistan, 1 in 5 Pakistani say that the

availability of drinking water at their child’s school is bad. A nationally

representative sample of adult men and women from across the country who have

schoolgoing children in their household was asked the following question

regarding, “On a scale of 1 to 5, where 1 is “very bad” and 5 is “very good”,

how would you rank each of the following services provided to your child by

their school?- Availability of drinking water for kids in school” 10% said it

is very bad, 9% said it is bad, 15% said the availability of drinking water

for kids in school is normal, 44% said that this service is good while only

18% said that it is very good. Question: “On a scale of 1 to 5, where 1 is

“very bad” and 5 is “very good”, how would you rank each of the following

services provided to your child by their school? – Availability of drinking

water for kids in school”

(Gallup Pakistan) December 29, 2022 Source:

https://gallup.com.pk/wp/wp-content/uploads/2022/12/29-Dec.pdf 775-43-02/Polls China’s FMCG

Spend Rises By A Further 3.1%

Spend on groceries in

urban China was up by 3.1% during the 12 weeks to 7 October 2022, compared

with the same period last year. This growth was mainly driven by shoppers in

the east of the country, where value sales rose 5.2% year-on-year. Consumers

maintained their stockpiling behaviour as COVID outbreaks continued, with

those in the east spending the most per trip. Modern trade growth

stagnates – and diverges Value sales in

hypermarkets and large supermarkets fell by 4.1% and 4.5% respectively

compared to a year ago, while in small supermarkets and convenience stores

value rose by 12.5% and 9% respectively, driven by growing baskets and an

expanding consumer base. Sun Art Group held an 8.1%

market share in last 12 weeks and maintained its leading position, yet lost

0.5pts in their value share compared to last year. In the latest trading

report, the group reported a 2.2% drop in revenue and 0.2% drop in Same Store

Sales Growth (SSSG). Meanwhile, the offline revenue of its new 2.0 store

transformation achieved a double-digit growth. Yonghui Group followed in the

second place, with 5.6% market share. Thanks to the expansion of Sam’s Club,

Wal-Mart Group gained 0.2pts share year on year and became the third largest

retailer, holding 5.3% share of the national market in last 12 weeks. Lockdowns drive further

ecommerce growth Spend on FMCG via the

ecommerce channel grew by 7.5% in urban China compared with the same period

last year, driven by consumers in upper-tier cities accelerating their demand

for online shopping as lockdown created the need to keep their pantries

stocked. Almost three quarters (71.6%) of urban Chinese households purchased

FMCG through ecommerce platforms in the 12-week period.

Alibaba Group leads the

core players, despite losing 2.8% market share compared to the same time last

year, dropping to 37.1%. JD Group gained 0.3%, growing its share to 15.9%,

while also increasing its consumer base. The expansion of social commerce

platform Pinduoduo appeared to retrench: its market share fell to 9.7%,

representing a loss of 1.3%. Meanwhile, the short video

platforms are developing rapidly by attracting new users, and Douyin’s

penetration is catching up with that of JD: 18.1% of urban Chinese households

placed orders for FMCG on Douyin in the past 12 weeks, more than double the

figure from last year. Both Douyin and Kuaishou are expanding their market

share rapidly, year on year. For China’s influential

Double 11 online shopping festival this year, platforms focused more on

strengthening connections with consumers rather than only on making sales.

This proved effective: Alibaba reported that more than 300 million users

watched its Taobao livestreaming in the lead up to the big day, for example.

In addition, O2O platforms played an active part in Singles’ Day promotions,

fuelling growth for the bricks-and-mortar stores. If you would like to learn

more about the evolution of China’s FMCG market, please get in touch with our

experts or access our data visualisation tool to explore current and

historical grocery market data. (Kantar) 27 December 2022 Source:

https://www.kantar.com/inspiration/fmcg/china-fmcg-spend-rises-by-a-further-3-1 WEST

EUROPE

775-43-03/Polls One In Ten Women Say They Have Had Their Drink

Spiked (To Spike A Drink Means To Put Alcohol Or Drugs Into Someone's Drink

Without Their Knowledge Or Permission)

Four in 10 Britons say

they do not think the police would believe them if they reported a drink

spiking As Britons get set to hit the bars, pubs and clubs

to see in the new year, YouGov figures have revealed the extent to which

people say they have ever had their drink spiked. Drink spiking is the adding of alcohol or drugs to

another person’s drink without their knowledge or permission. The aim may be

to incapacitate someone enough to rob or sexually assault them. A new YouGov survey shows that 10% of women say they

have personally had a drink spiked. Meanwhile, 8% say someone in their family

has had a drink spiked, while 10% say a friend has had a drink spiked. One in

seven women (14%) say someone else they know has been a victim of spiking. In

total, 35% of women say they have either had a drink spiked themselves or

know someone who has, or both. Among men, 5% say they have had a drink spiked,

while 7% say members of their family have had their drink spiked. One in

eight men (12%) say a friend of theirs has had their drink spiked and a

further 11% say someone else they know has had a drink spiked. More than a

quarter of men overall (28%) say they know someone who has had a drink spiked

or have experienced it themselves.

Nearly half of those aged between 18 and 24 (48%)

say they have had a drink spiked or know someone who has. However, it is

those aged between 25 and 49 who are the most likely to say they have

personally had a drink spiked (11%).

How confident do people

feel that reports of drink spiking would be taken seriously? When it comes to how confident Britons are that

police would believe them if they reported having their drink spiked, they

are split over the issue. Four in ten Britons (40%) are very or fairly

confident the police would believe them, but this includes only 8% who say

they are “very confident” they would be taken seriously. Equally, 40% are not

very or at all confident the police would believe them, including 15% who are

“not confident at all”. Britons also have little faith that a venue would

believe them if they told them they had a drink spiked there. Only 29% are

confident that a venue would take them seriously if they had a drink spiked

there compared to 42% who are not very or at all confident a venue would

believe a report of drink spiking under its roof. There is, however, more faith among the British

public that friends and family would take an incidence of drink spiking

seriously. Eight in ten Britons (80%) are confident that both their friends

and their family would believe them if they told them their drink had been

spiked. Half (51%) are “very confident” their family would believe them and

44% say the same about their friends.

(YouGov UK) December 28, 2022 775-43-04/Polls A New YouGov Survey Has Revealed That One In Five

Britons (21%) Say They Will Make A New Year’s Resolution For 2023

As we bid farewell to 2022, many Britons will be

taking the opportunity to make some New Year’s resolutions. A new YouGov

survey has revealed that one in five Britons (21%) say they will make a New

Year’s resolution for 2023, compared to just one in seven (14%) who say they

made a resolution for 2022. The younger generation are the most likely to vow to

make some changes for the new year, with four in ten 18-24 year olds (41%)

saying they’ll make a resolution for 2023 compared to just one in nine of

those aged 55 and over (11%).

For the

fourth consecutive year, doing more exercise or improving their fitness

tops the list for more than half of Britons (53%) who intend to make a

resolution for 2023. Health dominates the top three plans that Britons have

for the new year with 43% saying they plan to lose weight and the same

proportion resolving to improve their diet. Health-based resolutions are more popular among

women with 57% of those intending to make resolutions planning to do more

exercise or improve their fitness compared to 47% of men. Losing weight is

also a more popular resolution for women (46% compared to 40% of men) as well

as improving their diet (45% of women compared to 39% of men).

In the biggest change year-on-year in terms of resolutions,

four in ten Britons who are making resolutions (41%) say they want to save

more money, up from 30% who resolved to put more money into their savings in

2022. This resolution is also more important to women with 46% saying they

hope to save money as part of their plans for 2023 compared to 34% of men. In another increase from last year, 18% of those

making resolutions for the new year plan to decorate or renovate part of

their home, up eight percentage points from last year. One in five women (20%)

plan to spruce up their home in 2023, an increase of 11 percentage points

from the previous year How many Britons kept

their 2022 New Year’s resolutions? A New Year’s resolution isn’t just for January,

however, of those who made resolutions at the end of 2021, only 28% of them

say they kept all of them. Just over half (53%) say they managed to keep some

but one in six (17%) admit they didn’t keep any of their resolutions. While a similar percentage of men (11%) and women

(17%) made resolutions for 2022, among people who made resolutions, men are

nearly twice as likely to claim they kept all of their resolutions than women

are (40% vs 21%).

(YouGov UK) December 28, 2022 775-43-05/Polls Pharmacy Users In England Are Currently Satisfied

With Pharmacy Services

Pharmacy users in England are currently satisfied

with pharmacy services, and would be comfortable with them providing certain

new services, according to the Public

Perceptions of Community Pharmacy Survey conducted by Ipsos

for NHS England. Use of community

pharmacies In England, small chain or independent pharmacies

are the most commonly contacted or visited by the public (41%), followed by

large or medium sized pharmacy chains (35%). However, their usage is not a

frequent occurrence with only around one-quarter (26%) saying they contact or

visit a pharmacy at least monthly, either for themselves or someone they care

for. Meanwhile, one in five (20%) say they do not normally contact or visit a

community pharmacy. In general, pharmacy users are habitual when it comes to

contacting or visiting a pharmacy: around three-quarters (73%) say they tend

to use the same community pharmacy. Awareness and use of

pharmacy services Pharmacies are known to offer a multitude of services;

primarily, providing medicines prescribed by a doctor (78%), selling

medicines like paracetamol or eye drops to treat minor illness (72%), and

providing advice, about both medicines (64%) and about minor health problems

(61%). Indeed, of the various health services or sources of information

available , the public identify pharmacies as the organisations they would be

most likely to go to if they needed information and advice on medicines (68%)

or information and advice on a minor condition such as a sore throat or

earache (54%). Base: All respondents living in England who have

contacted or visited a pharmacy in the last year (n= 1,680). Survey conducted

via Ipsos KnowledgePanel Fieldwork 20th -27th July 2022.

In line with this, when asked what services

community pharmacies should offer (outside of the obvious services, like

dispensing prescribed medicines), the key services identified are providing

advice about both minor health problems (71%) and medicines (67%). However,

these are closely followed by a number of routine services that are currently

primarily viewed as services provided by GP practices, such as offering flu

vaccines (64%) and checking blood pressure (64%). This suggests that there is

public appetite for using community pharmacies for some functions they would

currently be seen as the domain of GP practices, representing a clear

opportunity for expanding the services pharmacies offer. Confidence and

satisfaction with community pharmacies Pharmacy users in England report positive experiences

of community pharmacies. For example, on their last visit to a community

pharmacy, most feel they were treated with respect (87%), were able to get

what they needed (87%) and thought that the facility was clean and well

maintained (87%). Similarly, those who have used a pharmacy in the

last year for advice about medicines, a health problem or injury, or what

health service they should use, are overwhelmingly positive about the quality

of the advice that they received. Nearly all (91%) say that they received

good advice and just 3% say that it was poor. There are high levels of confidence in a pharmacist

prescribing medication independently of a doctor or nurse when prescribing

medicines a person has had before (77%) and for medication they are currently

prescribed (70%). However, this confidence falls to 56% if the medication

being prescribed is something they have not taken before. Level of comfort with new

pharmacy services In general, the public would feel comfortable with

community pharmacies offering the new services that were asked about, though

there is some variation.

Infographic

(Ipsos MORI) 29 December 2022 Source: https://www.ipsos.com/en-uk/public-perceptions-community-pharmacy 775-43-06/Polls The Average Check Of Russians Before The New Year

Was Lower Than Last Year

Research holding Romir presents data on the weekly

spending index (WPI) and the weekly average bill index (WIN). In the period from December 19 to 25, the average

weekly expenses of Russians increased by 2.0% compared to the previous

week. Weekly spending index amounted

to 6,346 rubles. In annual dynamics, the index rose by 0.1%.

The average check index increased

by 4.0% compared to the previous week and amounted to 745 rubles in monetary

terms. Compared to the same period last year, the average check is 1.2%

lower.

WPI (weekly spending

index) of the research holding Romir

shows the dynamics of the volume of consumption of consumer goods by Russians

and is calculated for each calendar week based on the Romir Unified Data

Panel. INSCh (index of weekly

average check) of the research holding

Romir shows the dynamics of the cost of household purchases and is calculated

for each calendar week based on data from the Romir Unified Data Panel. (Romir) 29 December 2022 Source: https://romir.ru/studies/romir-sredniy-chek-rossiyan-pered-novym-godom-okazalsya-nije-proshlogodnego NORTH

AMERICA

775-43-07/Polls In Recent

Decades, The U S Drinking Rate Has Consistently Registered Near The Long-Term

Average Of 63% The percentage of U.S. adults aged 18 and older who

say they drink alcohol averaged 63% over the past two years, whereas 36%

described themselves as “total abstainers.” The drinking rate ticks up to 65%

when narrowed to adults of legal drinking age, which is 21 and older

nationwide. Since 1939, Gallup has asked Americans whether they

“have occasion to use alcoholic beverages such as liquor, wine or beer” or if

they are “a total abstainer.” Across the trend, the percentage saying they

drink has dipped as low as 55% (in 1958) and risen as high as 71% (in the

1970s). However, in recent decades, the U.S. drinking rate has consistently

registered near the long-term average of 63%.

Drinking Varies Most by

Financial Means The drinking rate among U.S. adults

differs more by household income than by any other standard demographic

characteristic. According to the 2021-2022 data, 80% of adults aged 18 and older living in

households earning $100,000 or more say they drink, far exceeding the 49% of

those earning less than $40,000. The rate among middle-income earners falls

about halfway between, at 63%. Relatedly, drinking also differs by education, with

college graduates (76%) and postgraduates (75%) the most likely to report

they drink. This is followed by nearly two-thirds of those with some college

education (65%) and about half of those who haven’t attended college (51%).

Religiosity Also a Factor

in Likelihood That People Drink Whether people drink also varies

significantly by their religiosity. Adults who attend their church or other

place of worship weekly (50%) are less likely than less-frequent attenders (63%) and nonadherents

(69%) to say they drink. By contrast, religious denomination is not a strong

factor in use of alcohol. Protestants are the least-likely major religious

category in the U.S. to say they ever drink alcohol. However, the 60% of Protestants

who in 2021-2022 reported they drink is only modestly lower than the 68%

among U.S. Catholics and 67% among those with no religious affiliation.

Men, Younger and White

Adults More Likely to Drink Than Their Counterparts In contrast to the wide variations seen by income

and religiosity, alcohol consumption varies only slightly by gender, with 66%

of men versus 61% of women saying they ever have occasion to drink. Drinking is more common among younger than older

adults, but this is evident only when the analysis is limited to those of

legal drinking age. Whereas 60% of adults aged 18 to 29 say they drink, the

rate is 71% among those aged 21 to 29. That matches the percentage of 30- to

49-year-olds who drink (70%), while it exceeds the rate among those 50 to 64

(64%) and 65 and older (54%). Among the nation’s largest racial and ethnic groups,

White adults aged 18 and older (68%) are more likely than Hispanic adults

(59%) or Black adults (50%) to report they drink. A review of Gallup’s

longer-term data confirm that White adults have been consistently more likely

than Hispanic and Black adults to drink, while the rate among the last two

groups has been statistically similar.

How Much Do Drinkers

Consume? On the whole, U.S. drinkers

reported consuming a modest

amount of alcohol in 2022, averaging four drinks per week for all drinkers.

The figure rises to six drinks per week on average for those who appear to be

regular drinkers, defined as those who had at least one drink in the past

week. More specifically, when asked how many alcoholic

drinks of any kind they had in the past seven days, a third of drinkers (34%)

in 2022 said they had had none. About half (53%) said they had between one

and seven drinks, while 12% reported consuming eight or more drinks, thus

averaging more than one per day. What Is Americans’ Drink

of Choice? For many years, beer was the strong

favorite of U.S. drinkers, mentioned by close to half as the alcoholic

beverage they most often drink. It still leads, but by a thinner, four-percentage-point margin over

wine, 35% to 31%, according to the 2022 survey. Meanwhile, 30% favor liquor

-- a new high -- and 3% have no preference.

(Gallup) DECEMBER 29, 2022 Source: https://news.gallup.com/poll/467507/percentage-americans-drink-alcohol.aspx 775-43-08/Polls War In Ukraine Cited By Canadians As Top

International News Story Of 2022 (71%)

As

2022 draws to a close, many Canadians have been reflecting on the major

national and international events that have shaped this historic year. A new

Ipsos poll conducted on behalf of Global News finds that Canadians cite some

of the major conflicts occurring this year as the most memorable news stories

which shaped 2022. Overwhelmingly, Canadians point to

the war in Ukraine as the top international news story of 2022 (71%).

Following this, rising interest rates and inflation around the world this year (40%) have been

deemed most noteworthy, perhaps only exacerbated by current concerns about

the potential for a recession in 2023.[i] Two international stories are tied for third place:

the death of Queen Elizabeth II, the longest-reigning monarch in British

history, in September (34%), and COVID-19 (34%), the latter of which may

still be on Canadians’ radars in light of the lifting of restrictions and the

availability of the bivalent vaccine this fall. One in five Canadians (19%)

say the overturn of Roe v. Wade and abortion rights in the United States was

among the top news stories of the year, with no significant differences

across age or gender. Although significant cultural events, in light of

such major international conflicts and threats to daily life for many around

the world, Canadians are less likely to cite the first James Webb space

telescope images as a top international news story (3%), nor were the Winter

Olympics particularly memorable (3%).

Canadians of different demographic groups have

varying perspectives on what was most noteworthy in 2022. Older Canadians age

55+ are significantly more likely to say the war in Ukraine was a top news

story of 2022 (83% vs. 64% 35-54 and 65% 18-34), while Canadians in their

prime working and family-formation years are more likely to cite rising

interest rates and inflation (50% 35-54 vs. 41% 55+ and 26% 18-34). Younger

Canadians are more likely to say billionaire Elon Musk’s acquisition of

Twitter was a top news story this year (19% 18-34 vs. 8% 35-54 and 5% 55+).

By gender, women are significantly more likely than men to cite the death of

Queen Elizabeth II (38% vs. 30%), and the children’s medication shortage

currently worrying parents in many parts of the world (14% vs. 9% men).

By contrast, men are more likely to cite ongoing protests in Iran (10%

vs. 3% women). Freedom Convoy Top News

Story of 2022 in Canada Closer to home, six in ten (62%) Canadians say the

disruptive Freedom Convoy protests of January and February constitutes the

top news story shaping the country this year. Closely aligned in second and

third place are the Rogers Communications major service outage of July, which

impacted millions of Canadians, including businesses and government offices

(37%), and Charles III becoming King of Canada at Rideau Hall in September

(35%). Storm chips at the ready,[ii] one-quarter

(23%) of Canadians say post-tropical storm Fiona hitting the east coast in

September was a top news story in the country. Mention of Fiona, a storm

which left thousands of Atlantic Canadians without power in its wake, is

highest in Atlantic Canada in particular (58%) and outranks the Freedom

Convoy (56%) as top Canadian news story of 2022 in this region. Nationally, not far behind ranks Pierre Poilievre’s

win of the 2022 Conservative Party of Canada leadership election in September

(22%). Erin O’Toole’s removal as Conservative Party leader, however, is

comparatively not as memorable (7%).

In terms of demographic differences, older Canadians

are more likely to have found the Freedom Convoy protest notable (73% 55+ vs.

56% 35-54 and 55% 18-34), as well as post-tropical storm Fiona (31% 55+ vs.

19% 35-54 and 16% 18-34) and Pierre Poilievre’s leadership win (29% 55+ vs.

20% 35-54 and 16% 18-34). Younger Canadians are more likely to have found

conversion therapy becoming illegal in the country in January 2022

significant (14% 18-34 vs. 6% 35-54 and 3% 55+). Women (43%) are more likely

than men (30%) to cite the Rogers Communications outage, while men are more

likely than women to cite Poilievre’s win (27% men vs. 18% women) and

O’Toole’s removal as party leader (9% men vs. 4% women). Regionally, Ontarians are most likely to say

Canada’s qualification for the FIFA World Cup this year is a top news story

(28% ON vs. 23% BC, 20% AB, 15% QC, 13% SKMB, 10% ATL). Given her roots in

Nova Scotia, it is unsurprising that Atlantic Canadians are more likely than

those in other regions to cite Mattea Roach’s winning streak in Jeopardy! this past spring as

notable (14% ATL vs. 10% BC, 5% AB, 5% ON, 4% QC, 3% SK/MB). Significant national and international events have

marked 2022 as one for the history books. As the year enters its final days,

Canadians will be looking ahead to see what 2023 might have in store, and

whether it will bring just as many newsworthy developments and surprises as

previous years. (Ipsos Canada) 28 December 2022 Source: https://www.ipsos.com/en-ca/news-polls/war-in-ukraine-cited-as-top-international-news-story-2022 775-43-09/Polls Almost Two Thirds Of Canadians (64%) Rate 2022 As

Good For Themselves And Their Family, But Only A Third (34%) Would Say The

Same For The World

As

2022 comes to an end, Canadians are reflecting on the events of the past

year. Although a sense of post-pandemic and work-life normalcy have warranted

cautious optimism - high inflation, rising interest rates and uncertain

geopolitics have weighed down Canadians’ year-end outlook. Indeed, a recent

poll conducted by Ipsos on behalf of Global News has shown that Canadians

look back unevenly on this last year for themselves, the country and the

world. Around two thirds (64%) say 2022 was ‘good’ for themselves and their

family, half (51%) say the same for Canada, and only a third (34%) think this

was a good year for the world. Improved but uneven

outlook on the country and the world

Age appears to be a key driver of

optimism, specifically at the personal level. Those aged 55+ are more likely

to rate these past

three years as good for themselves and their family: 69% (vs. 51%: 18-34;

58%: 35-54) for 2020, 68% (vs. 54%: 18-34; 56%: 35-54) for 2021 and 75% (vs.

63%: 18-34; 54%: 35-54) for 2022. Similarly, Quebecers appear significantly

more optimistic compared to other regions on a personal scale: 79% for 2020

(+19 pts compared to the national average), 77% for 2021 (+17 pts compared to

the national average), 77% for 2022 (+13 pts compared to national average). Even if 2022 was better than the last two years,

Canadians are split on their assessment on how this year turned out. Indeed,

half (50%) of Canadians agree 2022 was better than they thought it would be

(6% strongly, 44% somewhat) while the other half (50%) disagree (33%

somewhat, 17% strongly). Regionally, residents of Alberta and Saskatchewan

and Manitoba are more likely to fall on the pessimistic side of the coin (AB:

66%; SK/MB: 69% vs. 43%: BC; 50%: ON; 45%: QC; 39%: ATL). Furthermore, Canadians appear to be tempering their

optimism by signaling their apprehension for the uncertain economic

situation. Three quarters (75%) agree that 2022 has made them more fearful

for an upcoming recession (21% strongly, 54% somewhat), which is higher among

households with kids (83% vs. 73% for households without kids). Moreover,

only 44% agree that they were able to save enough money this year while a

majority disagrees (56%) – this proportion is higher among women (61% vs. 51%

for men) as well as those aged 35-54 (69% vs. 51%: 18-34; 48%: 55+). Finally,

three in ten (30%) agree this year has made them fearful for their job

security, which is higher among those aged 18-34 (52% vs. 35%: 35-54; 9%:

55+). Finally, among working Canadians, more than a third (36%) agree this

year has made them fearful for their job security, which is higher among

those aged 18-34 (49% vs. 35%: 35-54; 18%: 55+). Personal stability and

cautious optimism Taking stock of the past three years, most Canadians

haven’t experienced significant shifts in their outlook of their personal

lives and remain generally optimistic. In 2022, over three quarters (77%,

unchanged) rate their personal happiness as good, while a similar proportion

say the same for their health (75%, -1). Two thirds rate their social life

(66%, -3) and financial situation (64%, -2) as good, while six in ten (59%,

+1) say the same for their sex or romantic life. Thinking about these

various aspects of your life, would you rate them to be good or bad? % Rating Very/Somewhat

Good

Again, age appears to be a significant driver of

optimism on an individual scale. Those aged 55 and over are more likely to

positively rate their financial situation (80% vs. 53%: 18-34; 55%: 35-54),

their personal happiness (86% vs. 74%: 18-34; 72%: 35-54) and their social

life (72% vs. 62% for both 18-34 and 35-54). Stability at the individual level is also echoed in

Canadians’ yearly personal reviews, registering only slight variations.

Continuing its downward trend since the lockdowns of 2020, a quarter (24%,

-3) say they have struggled with their mental health. Similarly, the number

of Canadians who’ve worked from home for an extended period of time has also

continued to steadily decrease (10%, -5) since 2020, which is also the case

for those who say they’ve consumed more alcohol over the last year (12%, -2).

Tellingly, those who’ve selected ‘none of the above’ (18%) has increased by 4

points since last year, suggesting some return to normalcy. Thinking about the past 12

months, which of the following apply to you personally?

Unfortunately, stability isn’t synonymous with

improvement, especially among certain socio-demographic groups. 47% (-1)

still say they cut spending this year. Women (29% vs. 18% for men) and

younger age groups (18-34: 35%; 35-54: 29% vs. 10%: 55+) are more likely to

have struggled with their mental health over the last year, which is also the

case for residents of Saskatchewan and Manitoba (45%, +21 points compared to

the nation-wide average). Further, those aged 18-34 are the likeliest to say

they lost their job in 2022 (13% vs. 5%: 35-54; 2%: 55+), which is also the

case for households with kids (12% vs. 5% for households without kids). In

sum, compared to the past two years, Canadians tend to view 2022 positively -

especially when thinking of their personal lives; however, this optimism

remains cautious while reflecting on broader economic trends, and is uneven

among different generations and regions. (Ipsos Canada) 30 December 2022 Source: https://www.ipsos.com/en-ca/news-polls/personal-optimism-meets-global-pessimism-2022 775-43-10/Polls Opportunities For Science, Technology And Innovation

Open Up In Bogotá

With the contribution to collective construction and

in which actors from academia, civil society organizations, the public and business

sectors participated, Probogotá prepared a long-term document, in which it is

highlighted that one of the objectives is the construction of an integral

link between CteI –Science, Technology and Innovation– and urban-regional

development. In the document called "Visión Bogotá Región Inteligente

2051", a long-term planning and prospective exercise is developed that

seeks to connect capacities and take advantage of knowledge and collective

effort to promote and develop city initiatives, leveraged on innovation,

information and technology that improve the quality of life of the

inhabitants of Bogotá and the region, with criteria of environmental and

economic sustainability. María Carolina Castillo, president of Probogotá,

assured that "Probogotá Region, structured the Bogotá Intelligent Region

Vision by 2051 as a platform that seeks to identify synergies between actors

to promote the regional agenda in terms of smart cities and territories and

specify strategic projects that materialize it. ”.

Challenges

The greatest challenges in terms of

territorial intelligence do not reside in the application of physical and

digital infrastructure to support technological development; The biggest

challenges are found in digital appropriation, information governance and the generation of

soft skills to make responsible, ethical and effective use of these tools. In

the Vision, a series of recommendations are proposed that are oriented not

only to improve the connectivity and coverage of digital services in the region,

but also to establish institutional structures and public-private governance

arrangements to produce the necessary knowledge to manage them and make them

useful. in solving regional challenges such as mobility, waste management,

bioeconomy, climate resilience, among others. Territorializing science,

technology and innovation is essential to build an intelligent territory and

oriented towards meeting goals in terms of sustainability, progress and

well-being. The objective from the presentation of this Vision is to identify

and create networks of actors with common initiatives and agendas useful when

formulating strategies and collaborative projects that fulfill a central

objective: to turn the region into an intelligent territory. We are at an

opportune moment to influence the use of CTeI in the country, with the new

government and the next territorial elections and change of local leaders in

2023. The "Vision Bogotá Intelligent Region 2051" generates inputs

and recommendations that guide decision-making at the local level (municipal

development plans for the region) and regional (master plan for the

metropolitan region). The Vision also hopes to influence the concretion of

joint institutional agendas for the development of strategic projects that

stimulate and potentiate the use of CTeI to solve city-region problems, with

a strategic perspective on the regional challenges that local governments

must face. , private organizations of the ecosystem of smart cities and

territories and the instance defined for the coordination of matters of

regional interest.

The business On the other hand, this week the

Bogotá Chamber of Commerce released the Great Entrepreneurship Survey, which

makes a 360° x-ray of the business fabric, of those businesses that are

consolidated and

those that are in the growth stage. This survey, conducted in conjunction

with the Centro Nacional de Consultoría and applied to 2,272

businessmen and businesswomen, it is the only measurement in Bogotá and the

Region that makes an x-ray of the companies, their owners and those who make

decisions, which provides tools that allow guiding the construction of public

policy and strategies for strengthening business. The region of Bogotá and

Cundinamarca forms the economic and business center of the country. Here are

32% of all companies in Colombia. In 2021, the total number of registered and

renewed companies in Bogotá and the 59 municipalities of the jurisdiction of

the Bogotá Chamber of Commerce in the department of Cundinamarca reached

470,579 companies. This section presents the analysis of the behavior of

active, created, renewed and canceled companies and compares them with the

three previous years. In each section there are the figures according to the

location of the companies, their size, economic sector, location in Bogotá

and legal nature.

Economic units

According to the count carried out by DANE, in 2021,

2,548,896 economic units were identified in Colombia. Bogota represents 17.7%

of the total counted units. The economic units of the 59 municipalities

represent 60.1% of the total of Cundinamarca. Soacha, Fusagasugá, Zipaquirá

and Chía are the municipalities in the jurisdiction with the largest number

of economic units (50,081 units). In Bogotá there are, on average, 10.4

economic units per block.

11.5% of the economic units in Bogotá were

unoccupied during the survey of the economic count carried out by DANE in the

first half of 2021.

In Cundinamarca, unoccupied establishments

represented 7.7% of the total number of economic units listed. The sectoral

distribution of occupied dwellings indicates that for Bogotá there are

399,041 and, for the 59 municipalities, 75,230. Regional vision The management of the development

of Bogotá and Cundinamarca commits a regional vision and agreements between

the city and neighboring municipalities on policies and mechanisms for common

issues such as environmental sustainability, mobility and territorial planning, road

infrastructure, transport and services, that have a decisive impact on travel

times and costs and, consequently, on the sustainability and competitiveness

of the territory. 57.5% of occupied economic units carry out commercial activities

in Bogotá. In the jurisdiction of the Bogotá Chamber of Commerce (CCB),

43,145 units of the commerce sector were identified, which represent 57.4% of

the total number of occupied units in the 59 municipalities. In Bogotá, the

service sector participates with 36.4% of the total and in Cundinamarca with

38.4%. For its part, industry in Bogotá represents 5.8% of the total economic

units occupied, while in Cundinamarca it is 3.5%. Bogotá has a higher

proportion of mobile posts with 5.7%, while the 59 municipalities have 2.8%.

The 59 municipalities have the highest proportion of housing with economic

activity with 5.2%, while Bogotá has 2.8%. (CNC) 28 December 2022 AUSTRALIA

775-43-11/Polls One Of Australia’s All-Time Favourite TV Campaigns

Will Be Back On Our Screens From New Year’s Day, Bigger And Better Than Ever

A group of Norm’s closest

friends have recreated the iconic original TV ads, originally envisioned by

Phillip Adams and created by legendary artist, Alex Stitt in 1975. The new versions are all in widescreen HD and carry

the same gentle reminders to get up of the couch and exercise. All

major networks have the new TV ads on hand. They are also all accessible on

YouTube from THIS

LINK. The original campaign is still fondly remembered by

almost all Aussies who remember the seventies which was largely funded by the

Victorian Government. Considered possibly the most effective health

initiative ever in Australia, the ads promoted the simplest messages

(like get up off the couch and get

active) without preaching or being accusatory in the least. Michele Levine, CEO of Australia’s longest

established and most trusted research organisation, Roy Morgan, has

agreed to Co-Chair Life Be In It™ with

the existing Chairman, Dr Colin Benjamin OAM. Roy Morgan, the Foundation Partner in the

rejuvenation of this important community health initiative has announced a

new Index to track Australians’ health. ‘The

Life Be In It Wellness

Index’™. Roy Morgan data scientists have analysed over a quarter

of a million in-depth interviews with Australians since 2007. This exceptionally robust study shows that the

lockdowns have had a negative impact on Australians' choices in terms of food

and exercise resulting in a decline in overall health and wellbeing. Clearly, the time is right for a few friendly

reminders and to support programs aimed at helping us become healthier and

happier. It’s time to live more

of your life. Michele Levine says: “I have spent my 40 year

career in research, essentially an independent ‘observer’ – systematically

asking people questions, listening to what they say and seeking to understand

and report people’s views faithfully to ensure decision makers are making the

best possible evidence-based decisions. “I’m now delighted to be

part of what I believe will be a powerful movement – to help us all live more

of our lives and, in doing so, stave off so many of the ills of our modern

lives – and have fun doing it.” Life Be In It™, a registered Australian charity,

has an overall aim of engendering health, hope and happiness for all

Australians, with a strong focus on family, children, parents, and community. The organisation intends to have a

positive influence in five key spheres – Health, Sport and Recreation, Work,

Education & Community. Life Be In It aims

provide or support programs to:

‘Norm’ and many endearing characters of Life Be In It hit our screens from

New Year’s Day, thanks to the generosity of all major Australian television

networks who have enthusiastically embraced the relaunch campaign. (Roy Morgan) December

29, 2022 Source: https://www.roymorgan.com/findings/9137-life-be-in-it MULTICOUNTRY

STUDIES

775-43-12/Polls War In Ukraine Destroys Russia's Reputation And

Leaves It At Record Lows; Study Carried Around 33 Nations Shows

We live in a context of global instability, both

economically and geopolitically, which directly influences the reputation and

influence of the different players globally. Ipsos, once again this

year, in the study carried out in 33 countries for the Halifax International

Security Forum , wanted to analyze the state of the reputation of

these actors and how this impacts their positive influence worldwide. Russia's reputation

sinks Before the invasion

of Ukraine , almost half (45%) of people worldwide thought

that Russia would have a positive influence internationally, currently that

percentage has fallen 16 points, to 29%. It is clear that Russia's

public image has suffered a significant decline in the immediate aftermath of

its invasion of Ukraine nearly nine months ago, and as the invasion drags on,

expectations that Russia will have a positive influence on world affairs have

been diminishing. In fact, it is

the only country or international institution that has shown a dropped series . Canada, Germany and France

will be the most influential countries in the next decade At the other extreme, the study shows that Canada

and Germany remain the two countries most expected to have a positive

influence for the sixth consecutive year, after tying for first place in

2016. Other historically

influential international actors China ,

another of the most relevant global players, has not managed to recover its reputation since 2020 ,

when the COVID-19 pandemic began. The global average of people who say

that China will have a positive influence on world affairs fell from 53% in

2019 to 42% in 2020, increased slightly to 43% in 2021 and is now back at

42% (Ipsos Spain) December 28, 2022 775-43-13/Polls Only 10% Of The European Population States That They

Have Never Taken Supplements

The Covid-19 pandemic has brought with it an

increase in concern for health and self-care, as confirmed by the Ipsos study "European attitudes towards

food supplements" . In the wake of the pandemic,

consumers are increasingly turning to self-care and digital and personalized

medicine to monitor their own health data and gain greater control over their

health and immunity. This boom directly affects the consumption and

sales of the pharmaceutical and food supplements sectors. Only 10% of the European population states that they

have never taken supplements. Of this group, nearly half (45%) said they

had never done it because they simply never felt the need to, and 31% said

they believed they were getting all the nutrients they needed from their

diet. Approximately one in ten respondents have never taken supplements

because they don't like to swallow pills (14%), find supplements too expensive

(12%), or don't know which supplements are right for them (10%). Medical and pharmacy

professionals, trusted prescribers The main sources of

information that consumers consult to take supplements are the recommendation

of medical professionals (40%) and pharmacists (31%) . Even

among the few European consumers who had never taken supplements or vitamins

in the past (1 in 10), almost half of them (46%) mentioned that a doctor's or

healthcare professional's recommendation to take supplements would make them

reconsider. to do so in the future. The pharmacy, the

preferred point of sale to buy food supplements Nearly two-thirds of respondents who had ever taken

food supplements had purchased them at a pharmacy (63%), while a quarter had

purchased them at a supermarket, grocery store, convenience store, or

department store. The next most common places of purchase were health

food stores or herbalists (15%), websites specializing in food supplements

and/or vitamins (15%), and brand websites (10%). According to Ester Bueno,

Ipsos Mystery Shopping Expert in Spain :“As the figures show, the pharmacy and the

pharmacist's recommendation are key when it comes to selling this type of

product without a prescription. Pharmaceutical companies know this and

invest heavily in building strong business relationships with pharmacists to

promote their OTC brands, products and innovations. Understanding how

the pharmacist interacts with customers and what they advise or recommend is

important for the success of a brand in the market, hence the relevance of

the mystery shopper at the point of sale. The best tool to monitor the

real recommendation in the pharmacy is Mystery Shopping, since through an

objective measurement all the relevant information is recorded to know if the

commercial arguments are being well conveyed, what reasons for

non-recommendation are arising in the speech, (Ipsos Spain) December 29, 2022 775-43-14/Polls Covid-19 Restrictions Feed Economic Contraction To

Drive Down Living Standards In Africa, A Study In 34 African Countries

Key findings §

Lived poverty varies widely across the continent. In Mauritius, people rarely

endured shortages of a basket of basic necessities (food, clean water, health

care, cooking fuel, and a cash income) during the previous year. At the other

extreme, the average Guinean and Gabonese reported that they frequently went

without several of these basic necessities. §

Lived poverty is clearly moving upward, reversing a decade-long trend of

steadily improving living conditions that we saw coming to an end in

Afrobarometer Round 7 surveys in 2016-2018. For countries that have conducted

the longest time series of surveys, deprivation of basic necessities captured

by our Lived Poverty Index has returned to the same levels as measured in

2005-2006. The trend is similar for “high lived poverty,” the proportion of

people who experience frequent shortages of basic necessities. §

Increases in national levels of lived poverty over the past decade tend to be

largest in countries where the economy has stagnated or contracted, as

measured by changes in GDP per capita. §

Comparing levels of lived poverty recorded in Round 7 and Round 8 surveys,

there was no statistically significant difference in the extent of change

based on whether the Round 8 survey was conducted before or after COVID-19

lockdowns. § However, among countries whose Round 8 survey

followed the first wave of COVID-19, more stringent government responses were

associated with larger increases in lived poverty. And increases in poverty

were also larger where higher percentages of respondents told interviewers

that it had been difficult to comply with these restrictions. The extent of lived poverty today To measure lived

poverty, Afrobarometer asks respondents: Over the past year, how often, if

ever, have you or anyone in your family gone without: Enough food to eat?

Enough clean water for home use? Medicines or medical treatment? Enough fuel

to cook your food? A cash income? A range of response options are offered:

“never” for those who experienced no shortages, “just once or twice,”

“several times,” “many times,” and “always.” Because these questions are

asked in all surveyed countries, we are able not only to monitor shifts in

the levels and nature of poverty over time, but also to compare experiences

across countries and regions. Large numbers of Africans fail to meet their

most basic needs. Across 34 countries surveyed in 2019/2021, six in 10

respondents (61%) reported facing shortages of medicine or medical services

at least once in the previous 12 months, and nearly as many experienced

shortages of clean water (55%) and food (52%). Nearly four in 10 experienced

shortages of cooking fuel (46%) (Figure 1). 1 The weighted Mozambique Round 8

sample is nationally representative except that it excludes rural Cabo

Delgado, comprising 6.3% of the adult population of Mozambique. Insecurity

and resulting difficulties in obtaining necessary fieldwork clearances

prevented Afrobarometer from collecting sufficient data in this area.

Measuring poverty Poverty can be measured in a number of different ways. At

the national level, all countries produce national accounts data to calculate

their gross national income (GNI), which is used to summarize national wealth

and the total state of the economy. However, some analysts have questioned

the capacity of many African countries’ national statistics systems to

generate these numbers reliably (Jerven, 2013). At the personal or household

level, national statistics offices conduct large household surveys to measure

incomes, expenditures, assets, and access to services, which are then used to

calculate national poverty lines and place individuals above or below these

lines. The United Nations’ Sustainable Development Goal 1 focusing on

reducing the number of people living on less than $1.90 a day is a good

example. However, such surveys are expensive and are conducted infrequently

in many African countries. Other development organizations’ collect data on

the consequences of poverty in a given country, such as the proportion of

people who don’t use improved drinking water sources or the proportion of

children under age 5 who are underweight. As a contribution to the tracking

of poverty in Africa, Afrobarometer offers the Lived Poverty Index (LPI), an

experiential measure that is based on a series of survey questions about how

frequently people actually go without basic necessities during the course of

a year. The LPI measures a portion of the concept of poverty that is not

captured well by other measures, and thus offers an important complement to

official statistics on poverty and development (Mattes, 2008). Because people

are the best judges of their own interests, survey respondents are best

placed to tell us about their quality of life, though they might not be able

to do it with a great deal of precision. If Amartya Sen (1999) is right and

the value of one’s standard of living lies in the living itself, an

experiential measure of shortages of the basic necessities of life takes us

directly to the central core of the concept of poverty. Reflecting the continent’s ongoing employment

crisis, the most commonly cited form of deprivation remains access to cash

income, with four-fifths (80%) reporting that they went without cash income

at least once in the previous year. While cash income is not in itself a

basic need, access to it can enable citizens to meet their basic and

non-basic needs. Income shortages therefore have many spillover effects on

people’s lives. The fact that fourfifths of Africans report having gone

without cash income at least once – and that 42% did so frequently – poses a

major development challenge, as many adults on the continent cannot afford to

buy resources for immediate use or to invest in assets. These average

figures, however, mask a great deal of variation across the continent, as

well as within societies. In terms of food, for instance, one in 10 Mauritians

(10%) experienced a shortage in the previous year, compared to three-quarters

of Liberians (73%), Zambians (75%), Nigeriens (76%), and Malawians (79%) (not

shown). Similarly, one in five Mauritians (17%) and about one in three

Ghanaians (31%) and Cabo Verdeans (34%) went without needed medicine or

clinic visits, compared to four in five citizens in Benin (78%), Zambia

(79%), Gabon (81%), Sierra Leone (82%), Liberia (83%), and Guinea (84%) (not

shown).

The Lived Poverty Index (LPI) Treating the responses

to Afrobarometer’s five “gone without” questions as a continuous scale, we

can combine them to calculate an average score for each respondent, and for

each country, that captures the overall level of a phenomenon we call “lived

poverty.” The Lived Poverty Index (LPI) score ranges along a five-point scale

from 0, for someone who never goes without any necessity, to a high of 4,

which implies an individual is experiencing a constant absence of all basic

necessities. 2 Afrobarometer describes those who score “0” ashaving “no lived

poverty,” those with scores of 0.2 to 1.0 as having “low lived poverty,”

those with scores of 1.2 to 2.0 as experiencing “moderate lived poverty,” and

those with scores above 2.0 as experiencing “high lived poverty.” The score

for the mean level of lived poverty across all 34 countries surveyed in

2019/2021 is 1.34, and the median African respondent went without each of

these basic necessities once or twice over the previous year. However, as

suggested above by the responses to specific questions, there are significant

cross-national variations around that mean. The highest index scores can be

found in Guinea (2.00), Gabon (1.93), and Benin (1.81) – the median person in

these countries experienced shortages across everything in our basket of

basic necessities several times a year. In sharp contrast, the typical person

in Mauritius (0.34) never or rarely went without (Figure 2).

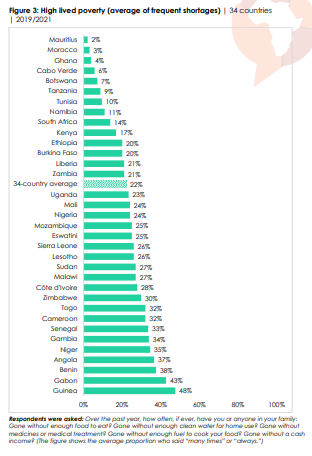

High lived poverty Even more troubling is the

intensity of deprivation. Across Africa, between one in seven and four in 10

people encountered frequent shortages (“many times” or “always”) in the

previous year with respect to cash income (42%), water (24%), medicine or

medical treatment (22%), food (16%), and cooking fuel (15%). One of the

potential statistical limitations of the LPI is that it treats each

additional increment in the response scale the same (e.g. the difference

between “never” and “just once or twice” is treated the same as that between

“sometimes” and “many times”), which may not be strictly appropriate. One way

to check this is by calculating the most intense or extreme reports of

shortages – those who said they went without “many times” or “always” – and

see whether these responses follow the same general pattern across countries

as the overall index. Thus, we calculate the proportion of people who, on

average, experienced frequent shortages across each dimension. 3 Across all

34 countries, an average of nearly one in four people (22%) experienced high

lived poverty, going without food, water, medical care, cooking fuel, and

cash income on a frequent basis. High lived poverty is almost non-existent in

Mauritius (2%) and Morocco (3%), and is relatively rare in Tanzania (9%),

Botswana (7%), Cabo Verde (6%), and Ghana (4%). At the other extreme, half of

all citizens live in severe poverty in Guinea (48%), and four in 10 do so in

Gabon (43%) and Benin (38%) (Figure 3). Despite a few differences between the

country rankings for the LPI and those for high lived poverty, overall the

scores for the two scales are strongly correlated. 4 Across the 32 countries

surveyed in both Round 7 and Round 8, the mean individual level of lived

poverty increased by 0.13 points, led by the Gambia (+0.63), Nigeria (+0.46),

and Sierra Leone (+0.39) (Figure 4). Twenty countries recorded an increase of

0.08 points or more (that is, greater than the largest country-level standard

error, or .035 points), and only three countries recorded significant

reductions in lived poverty: Niger (-0.08), Togo (-0.19), and Tanzania (-0.21).

Across the same period, the proportion experiencing high lived poverty

increased by a mean of 3 percentage points across 32 countries (Figure 5).

Fourteen countries recorded an increase of 4 points or more in the proportion

of people experiencing high lived poverty. The largest increases were in the

Gambia (+22 percentage points), Nigeria (+14 points), and Sierra Leone (+11

points), showing a strong correlation with changes in the overall index

scores (see Figure 4). Three countries reported decreases of more than 4

points: Togo (-9 points), Tanzania (-5 points), and Niger (-5 points) – the

same countries that saw significant improvements in overall index scores.

Twelve countries did not record a significant change on this indicator (i.e.

they recorded only changes between +2 and -2 percentage points).

Resurgent lived poverty Examining longer-term trends

is complicated by the fact that Afrobarometer has expanded over time. Thus

different sets of countries have to be examined over different time spans.

The longest trend can be observed across the 16 countries that have been

included in each round of Afrobarometer since Round 2 (2002/2003). 5 For this

group, average LPI scores peaked at 1.27 (on a scale running from 0 to 4) in

2005/2006 and then fell consistently to a low of 1.06 in 2014/2015 (Mattes,

Dulani, & Gyimah-Boadi, 2016). However, since then, these economies have

given back almost all of their hard-earned gains. As of Round 8, their mean

LPI score again stands at 1.27, precisely where it stood in 2005/2006 (Figure

6). We can also examine larger sets of countries over shorter time frames,

and observe the same trends. Across the largest group of 30 countries that

have been included since 2011/2013, 6 the average LPI score initially fell from

1.25 to 1.14 in 2014/2015 before climbing to 1.29 in 2019/2021.

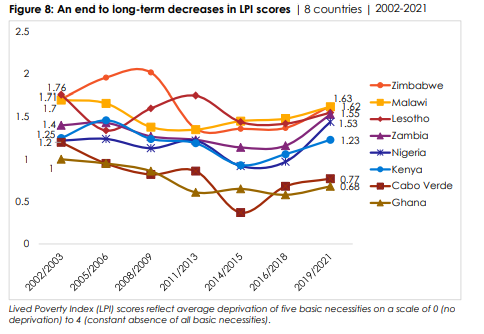

Dashed hopes: Lived poverty reduction in specific

countries? In our last report (Mattes, 2020), we identified a set of nine

countries that had exhibited real, consistent decreases in lived poverty over

at least the four previous surveys. However, once we include the 2019/2021

results, we find that compared to 2016/2018, with the exception of Burkina

Faso, poverty has now risen in each case (Figure 8)

In only three countries – Tanzania, Burkina Faso,

and Morocco – do we find sustained livedpoverty reduction compared to our

first measurements (Figure 9). The more positive patterns in these countries

may reflect government and donor investment in food security. For example, in

Tanzania, improved service delivery and social safety net programmes such as

the Tanzania Social Action Fund (TASAF) and Productive Social Safety Nets

(PSSN) may have contributed to these trends (Rosas et al., 2019). In 2019,

the World Bank reclassified Tanzania from “low income” to “lower-middle

income” country status (Battaile, 2020). In Burkina Faso, one of the poorest

countries in the world, innovations in agriculture that aim to “regreen” the

Sahel may be showing results, reportedly helping 500,000 Burkinabè to become

food secure (Eckas, 2020). At the same time, significant proportions of the

population have increasingly come under attack by non-state armed groups.

This has fuelled a humanitarian crisis and created the Sahel’s largest

displaced population – challenges that could undermine the country’s gains (ReliefWeb,

2022). Morocco, meanwhile, benefited from large increases in development

assistance over the course of the decade, with inflows more than doubling

from $940 million in aid in 2010 to a peak of $2.55 billion in 2017

(TheGlobalEconomy.com, 2022), which may help to explain the modest observed

decrease in poverty (European Court of Auditors, 2019).

Finally, in four countries – Guinea, Benin, Senegal,

and South Africa – lived poverty has, on average, increased over the last

10-20 years, and in all cases is now higher than when it was first measured

by Afrobarometer (Figure 10).

Poverty escalation: Driving trends? We know that

there are several important country-, local-, and individual-level factors

that consistently correlate with individual levels of poverty at any given

point in time. In Round 7, for instance, we found that the most important

predictors of individual levels of lived poverty were the length of time the

country had sustained democratic rule and the quality of local

service-delivery infrastructure (such as the presence and quality of water

and electricity grids and good roads), as well as individual characteristics

such as gender, age, education, occupation, and employment (Mattes, 2020).

Most of these factors, however, are relatively fixed and thus cannot account

for significant and relatively rapid national shifts in individual

well-being. Extent of democracy One factor that has shifted around the world

recently is the extent of democracy. Various projects that track the level

and quality of democracy across countries agree that we are now in a “reverse

wave of democracy” (Repucci & Slipowitz, 2022) or a period of

“autocratization” (Lührmann & Lindberg, 2019) in which the extent of

democratic regression outstrips the extent of democratic progress around the

world. Africa has not been immune to these trends, with significant

retrograde movements of democracy in places such as Benin, Senegal, Tanzania,

Mozambique, and, up until its recent election, Zambia. In order to test

whether negative trends in democracy have anything to do with recent