|

BUSINESS & POLITICS IN THE WORLD

GLOBAL OPINION REPORT NO.773

Week:

December 12 – December 18, 2022

Presentation: December 23, 2022

Inside Afghanistan: Record Numbers Struggle to Afford Basics

UAE Parents Have High Concerns over Their Child’s Exposure To

Inappropriate Online Content

Health Insurance Coverage for Nigerians Still Abysmal; An Urgent

Call For New Strategy.

Labour Voters More Wary about Politics of Child’s Spouse

Most Brits Expect Recession, As Consumer Confidence Dips To

Six-Year Low

Half of Leave Voters Doubt Johnson Can Secure New Brexit Deal

Few Believe the Government's Explanation of Why Parliament Is To

Be Suspended

Brits Oppose Parliament Suspension By 47% to 27%

5 Facts about the Abortion Debate In America

U.S. Concern about Climate Change Is Rising, But Mainly Among

Democrats

Most Americans Say Science Has Brought Benefits to Society and

Expect More to Come

Parents' Concern about School Safety Remains Elevated

As Labor Day Turns 125, Union Approval Near 50-Year High

Americans' Satisfaction with U.S. Education at 15-Year High

Most Cannabis Consumers Use on a Weekly Basis or More

Ride-Sharing App Uber Overtakes Taxis as Preferred Private

Transport Service

Rising Numbers of Australians Looking At Electric and Hybrid

Vehicles for Their Next Set of Wheels

Toyota And Mazda Drivers Most Brand Loyal; Have The Luxury

Brands Lost Their Lustre?

Britons Make Worst Tourists, Say Britons (And Spaniards And

Germans)

Brazilians Least Satisfied in Amazon With Environment

India Ranks 9th on Happiness among 28 Global Markets: Ipsos

Global Happiness Survey

The Biggest Beauty Influencer Isn’t Who You Think It Is

INTRODUCTORY NOTE

773-43-22/Commentary:

SUMMARY OF POLLS

ASIA

773-43-01/Polls

12 Percent Of

Japanese People Say They Cook To Relax

In

countries other than Japan, many people said they enjoy the act

of cooking, such as baking and boiling. (Photo by Atsuko

Shimamura)

This

was the finding of a private survey among 800 men and women aged

at least 18 each in Japan, the United States, Italy, China,

Thailand and Indonesia carried out in January by Sigmaxyz Inc.,

a Tokyo-based consulting firm. It has

been conducting surveys on diet and well-being in six countries

since 2019.

“Nothing is enjoyable in cooking” and “deciding what to cook”

were cited by the second-largest portion of Japanese respondents

at 17 percent each.

The

results showed that two negative answers--“they don't cook” and

“nothing is enjoyable in cooking”--were included in the top five

answers in Japan.

The

ratios for these two answers were up from the previous survey

conducted in 2020.

But

positive answers came high on the list in the other countries.

“Cooking itself” and “serving meals” were cited by the largest

portion of respondents in the United States at 44 percent, while

“cooking itself” was cited by 55 percent of those in China and

47 percent of those in Thailand.

And

when the respondents were asked to give multiple answers on why

they cook, “to cut down on food expenses” was outstandingly high

among those in Japan at 44 percent.

“By

necessity” came next at 18 percent, followed by “they don’t

cook” (17 percent), “out of a sense of obligation to the family”

(16 percent), “to have communication time with family members”

and “to control their own health and condition” (14 percent).

Only 12

percent of the respondents in Japan said they “are interested in

cooking itself and can obtain knowledge.”

But

more than twice as many said so in the other Asian countries,

with Thailand at 35 percent, China at 34 percent and Indonesia

at 33 percent.

Even

those in Italy, which ranked second from bottom only above

Japan, agreed at 25 percent.

And

while 12 percent of the respondents in Japan said they cook to

“relax,” at least 30 percent of those in each of the other five

countries said so, with Italy ranked first at 43 percent.

“There

are two factors in cooking, with one being a form of household

chore and the other involving creativity,” said Tomomichi Sumi of

Sigmaxyz. “There is a good balance between the two in the

overseas countries, while (cooking) is more strongly accepted as

domestic labor in Japan.”

December 13, 2022

Source:

https://www.asahi.com/ajw/articles/14778595

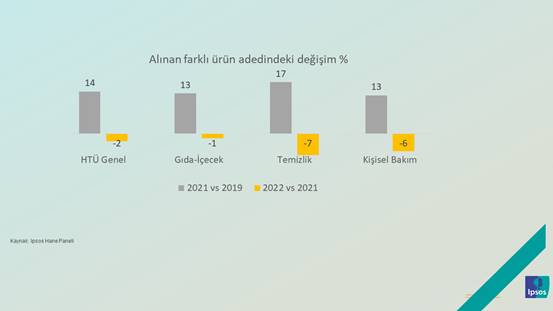

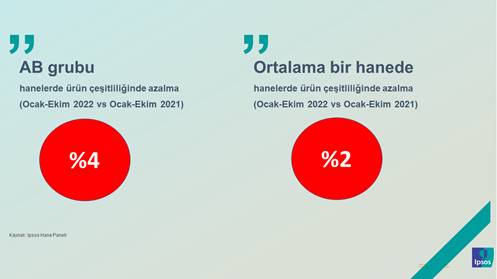

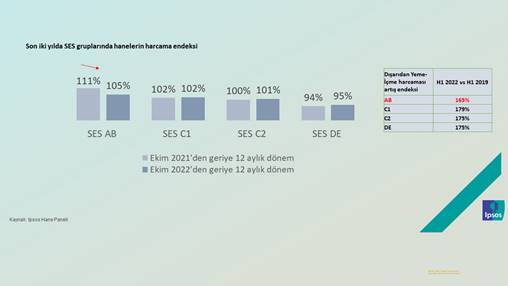

773-43-02/Polls

High Inflation

Is Moving Households Away From Buying More Diverse, Different

Products

The

decline in product diversity was sharper in EU SES group

households.

The

Ministry of Labor announced that the proportion of minimum wage

earners among all employees is 37%. And the minimum wage has

increased by more than 90% in January and July in 2022. For the

low-paid people, we can say that it is much more difficult, even

impossible, to save, so this wage increase means that disposable

income is somewhat protected against inflation. Of course, it

would not be right to see this as an increase in welfare, but we

can only say that it is a reduction in the loss of welfare. On

the other hand, salaries increased relatively less in higher

income groups, especially those who worked for wages. The rate

of loss in the disposable income of this group is greater. We

started to see the reflections of this situation in consumption

statistics. As I mentioned, the variety of products purchased in

an average household decreased by 2% in the period

January-October 2022 compared to the same period last year,

while this decrease was 4% in households in the EU socioeconomic

segment. EU households are (declining) approaching the average,

spending 11% more than the average in the 12 months before

October 2021, spending 5% above average in the last 12 months in

October 2022. C2 households were on average during the same

periods, rising 1% above average, while DE households also took

a step towards the average, approaching 1% (rising).

The

loss faced by citizens belonging to the EU socio-economic group

is also reflected in their general satisfaction and

expectations. At the end of 2021, dissatisfaction with the

personal standard of living in this group was behind the general

average, but by September 2022, we started to see an

above-average dissatisfaction. The same applies to expectations

for the next few months. About a year ago, the proportion of

people who thought their personal economies would deteriorate

was lower in the EU segment than the national average. 10 months

later, the situation reversed. The EU is more desperate than the

general population.

This

economic erosion that the upper socioeconomic groups face as

consumers is a change that needs a lot of thought. Of course, a

more balanced picture in income distribution is the goal of

every country, but we should aim to be equalized by getting

richer, not by getting poorer.

16 December 2022

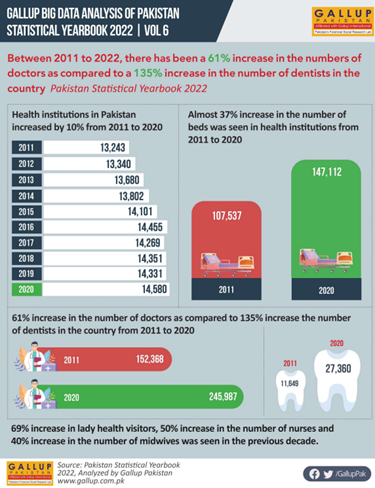

773-43-03/Polls

Between 2011 To

2022, There Has Been A 61% Increase In The Numbers Of Doctors As

Compared To A 135% Increase In The Number Of Dentists In The

Country

Abstract As a developing country, Pakistan has been struggling

with developments in the health sector. Even though there has

been constant development happening, the country still has a

long way to go. Undertaking an analysis of facts and figures

available in The Pakistan Statistical Yearbook 2022 published by

the Pakistan Bureau of Statistics, this press release provides

an overview of the growth in the health sector over the last

decade. The complete Pakistan Statistical Yearbook is available

HERE. What is the Big Data Analysis Series by Gallup: Gallup

Pakistan’s Big Data series was started by Bilal I Gilani,

Executive Director of Gallup Pakistan. Bilal explains the

rationale of the series, “The usual complaint from academics and

policy makers is that Pakistan does not have data availability.

Our experience negates that. Pakistan has lots of data, but it

is not available in a usable form and it’s not widely

accessible. At Gallup we plan to bridge this gap in terms of

accessibility and use of data. The Gallup Big Data series has

earlier worked with data sets such as PSLM, Labour Force Survey,

and Economic Survey reports as well as National Census Reports

and Election Commission Data sets.” The current series is using

the Pakistan Statistical Yearbook, an annual compilation which

seldom has data points not covered in many other reports. We

hope that these series are useful, and we welcome both feedback

as well as possible collaborations as we create a public good in

the form of useful data sets in Pakistan’ What data points this

current edition covers: This series aims to present the

important learnings from the Pakistan Statistical Yearbook 2020

for policy makers, the public, as well as for marketers in an

easy and understandable way. In particular, this edition looks

at the developments in the health sector over the last decade.

The health sector has been flourishing when it comes to the

number of medical personnel as it has increased. However, there

hasn’t been much progress in the development of new health

institutions and the facilities available at them. The series’

main aim is to provide data. Implications of these data points

for the health sector as well as wider socio-political

ramifications is something we would like to trigger in relevant

circles.

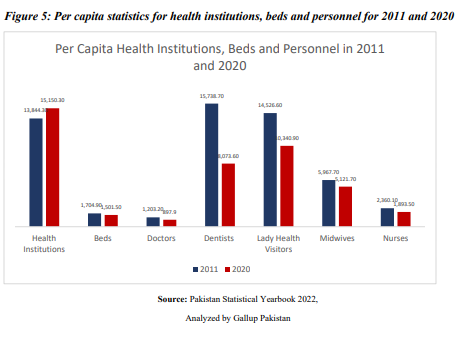

Today’s

Topic is “Health” Key Findings 1) The

number of health institutions in Pakistan increased by 10% from

2011 to 2020 2) Almost 37% increase in the number of beds was

seen in health institutions from 2011 to 2020 3) 61% increase in

the number of doctors as compared to 135% increase the number of

dentists in the country from 2011 to 2020 4) 69% increase in

lady health visitors, 50% increase in the number of nurses and

40% increase in the number of midwives was seen in the previous

decade Table 1: Increase in health institutions, bed and

personnel from 2011 to 2020 Health Institutions 10% Beds 37%

Doctors 61% Dentists 135% Lady Health Visitors 69% Midwives 50%

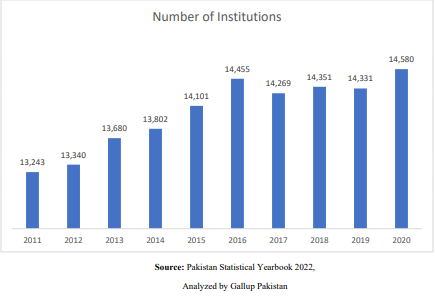

Nurses 40% 1) The number of health institutions in Pakistan

increased by 10% from 2011 to 2020 Healthcare in Pakistan has

been a focal point after the country signed the U.N. Millennium

Development Goals (MDGs). Pakistan began to initiate healthcare

programs, establishing both Basic Health Units as well as Rural

Health Units. Basic Health Units are assigned to NGOs, who

manage the day-to-day operations, administer medicine and

overlook the facilities. The number of health institutions

increased from 13243 in 2011 to 14455 in 2016, however, the

number of health institutions fell from 2016 to 2017, after

which it increased gradually till 2020. The decline in 2017

could be due to the privatization of government hospitals due to

mismanagement. Instead of increasing and improving facilities at

government hospitals, the government was focused on transferring

public hospitals to private organizations to operate under

public-private partnership. However, the sudden increase in the

number of health facilities that can be seen in 2020 could be

owed to the Covid-19 pandemic. As the number of covid cases

started to increase in the country, the government had to build

new health facilities to treat the patients. Figure 1: Number of

health institutions in Pakistan from 2011-2020

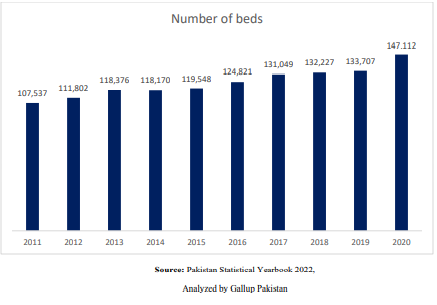

2)

Almost 37% increase in the number of beds was seen in health

institutions from 2011 to 2020 The number of beds in health

institutions has increased over the decade, however, it has not

been sufficient to cater the populations needs, as we saw how

the hospitals quickly ran out of bed spaces during the pandemic.

The population of the country is growing annually at a rate of

over 2% and the rate at which the beds are increasing are not

enough to sustain the growing population. The sudden increase

from 2019 to 2020 could be due to the Covid pandemic. When the

pandemic broke out, the government converted some of the public

centers like the expo center into covid wards with a large

number of beds – to cater to the increasing number of patients.

This led to an increase in the hospital beds Figure 2: Number of

beds in health facilities in Pakistan from 2011-2020

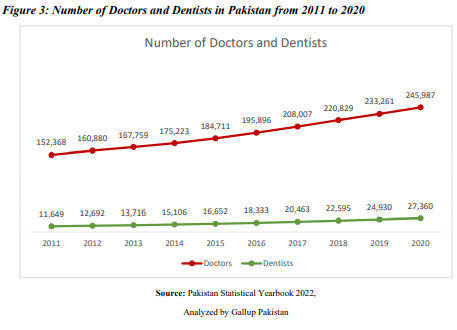

3) 61%

increase in the number of doctors as compared to 135% increase

the number of dentists in the country from 2011 to 2020 In a

press release published by Gallup Pakistan previously, (which

can be found here) it was seen that there has been a trend of

pursuing science amongst matriculation students, and the number

of students passing their matriculation exams has increased

significantly in the last decade. The increase in the number of

doctors and dentists could be owed to that. As per the

statistics, the number of doctors has increased significantly,

however, the on-ground situation tells us that there is still a

lack of doctors. This can be attributed to the incompetence of

the government, an appropriate number of doctors have not been

posted in hospitals, owing to which the patients face lot of

problems daily in getting medical treatment at private and

government hospitals in the entire country. Moreover, as per the

recommendations of the World Health Organization, a dental

surgeon versus population ratio should be one to 20,000 people.

However, even with the huge increase in the number of dentists,

the ratio of dentists to population is one dentist for more than

75000 people. Thus, the number of dentists is still too low.

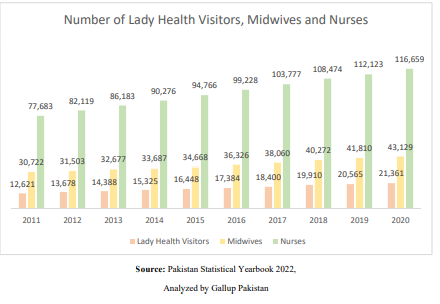

4) 69%

increase in lady health visitors, 50% increase in the number of

nurses and 40% increase in the number of midwives was seen in

the previous decade Even though the number of nurses has

increased by 50%, it is still not enough to keep up with the

increasing population as the country still faces a shortage of

more than 1.4 million nurses. As per the global standards, it is

an obligation that around two doctors, a dentist and eight

nurses should be taking care of 1,000 people however the story

in the country is different where this standard is not met in

number of doctors and nurses. Lady health Visitors have a broad

understanding of basic health care and are responsible for a

wide range of activities at the community level, which is why

they are essential health professionals. The increase in lady

health workers and midwives can be said to have decreased the

maternal mortality rate as these professionals attend to females

giving birth. Lady health visitors have also been essential in

informing and educating the rural females of various health

issues. The increase in the number of Lady Health Visitors could

be owed to the Lady Health Worker Program (LHWP), introduced in

1994. In 2000, the program was renamed the National Program for

Family Planning and Primary Health Care, but it is still

commonly known as the Lady Health

Worker

Program. Following the 18th Amendment, the management of the

LHWP has been devolved to the Provincial Governments. Figure 4 –

Number of Lady Health Visitors, Midwives and Nurses from 2011 to

20202

5) 69%

increase in lady health visitors, 50% increase in the number of

nurses and 40% increase in the number of midwives was seen in

the previous decade A quick glance at the statistics makes it

seem like the situation of the health sector in Pakistan has

been improving over the past decade, however, if we look at the

per capita statistics, we can see that even though the situation

has improved, it is still not enough to cater to the needs of

the population. According to World Bank’s data on the Pakistani

population, the population in 2011 was 183340168 while in 2020,

the population was 220892331. Based on these figures, the

situation of beds, and health personnel has gotten slightly

better. The recommended number of doctors by WHO is one doctor

per 1000 people, in 2020, Pakistan had one doctor per 8073.6

people. This is almost eight times greater than the recommended

number, which can put into perspective how poorly the country is

doing. Moreover, the number of health institutions per capita

has increased, which means that the increase in the number of

health institutions has not been enough.

December 16, 2022

Source:

https://gallup.com.pk/wp/wp-content/uploads/2022/12/Health-pr.pdf

AFRICA

773-43-04/Polls

Government Officials And The Police Remain The Most Violators Of

Human Rights In Nigeria

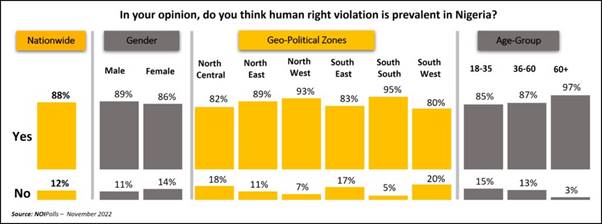

More findings from the poll also revealed that issues

of human rights violation are prevalent in Nigeria as disclosed

by 88 percent of respondents interviewed. Regarding violation,

31 percent of adult Nigerians nationwide claimed their human

rights have been violated in the past.

Analysis by gender showed that there are more male (36 percent)

than female (26 percent) respondents whose rights have been

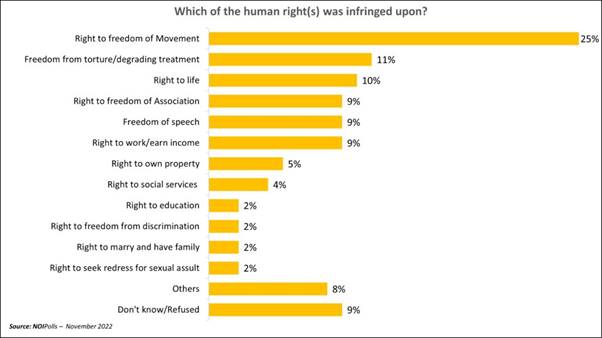

violated before. Consequently, when asked about the component of

human rights that have been violated, 25 percent claimed that

their ‘right to freedom of movement had been trampled upon in

one way or another. While 11 percent mentioned that their ‘right

to freedom from torture/degrading treatment’ has been infringed

on, another 10 percent disclosed the ‘right to life’ amongst

other human rights violations.

Finally, the poll result showed that most victims (75 percent)

of human rights violations in Nigeria do not report violations

committed against them. Therefore, it is important to create

frequent awareness campaigns for the citizenry on their basic

human rights as recommended by 36 percent of the adult Nigerians

interviewed. Also, as advocated by 19 percent of Nigerians, the

government should enforce laws against human rights (s)

violators in the country as this will serve as a warning to

other violators of human rights in Nigeria. These are some of

the key findings from the Human Rights Poll conducted in the week commencing November

7th, 2022.

Background

NOIPolls joins the world in commemorating the 75th Anniversary

of the Universal Declaration of Human Rights, which is observed

annually across the world on 10th December. This

campaign aims to draw people’s attention to the issues

surrounding their human rights irrespective of who or where they

are in the world. This year’s Human Rights Day theme is “Dignity, Freedom, and Justice for All” and

the call to action is hashtagged #StandUp4HumanRights. In commemoration of

World Human Rights Day, NOIPolls conducted a public opinion poll

to gauge the awareness and perception of Nigerians regarding

their basic human rights.

Survey Findings

The

first question sought to measure human rights awareness in

Nigeria and the result showed that a larger proportion of adult

Nigerians nationwide (88 percent) claimed to be mindful of their

basic human rights.

Furthermore, findings from the poll also revealed the concern

for human rights violations is prevalent in Nigeria as disclosed

by 88 percent of respondents interviewed.

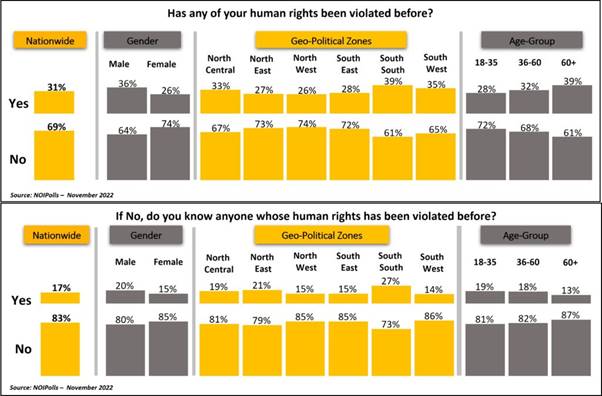

Regarding violation, 31 percent of adult Nigerians nationwide

claimed that their human rights were violated. Analysis by

gender showed that there are more male (36 percent) than female

(26 percent) respondents whose rights have been violated before.

Also, an analysis of the geographical location indicated that

the South-South zone accounts for the highest number of

Nigerians in this category.

Similarly, of the 69 percent who claimed that their rights have

not been violated before, 17 percent admitted that they know

someone whose rights have been violated before. The South-South

zone also had the highest number of Nigerians who mentioned

this.

Consequently, when asked which human rights have been violated,

25 percent claimed that their ‘right to freedom of movement had

been trampled upon in one way or another. While 11 percent

mentioned that their ‘right to freedom from torture/degrading

treatment’ has been infringed on, 10 percent disclosed the

‘right to life’ amongst other human rights violations.

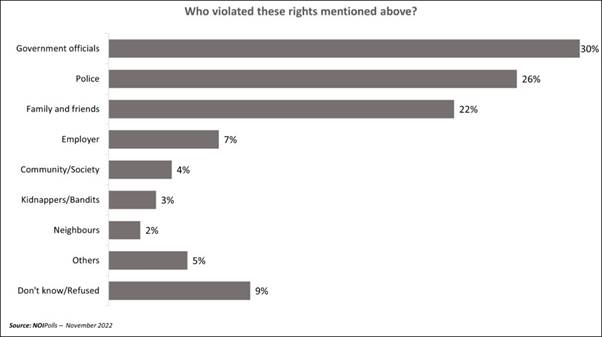

In

addition, Nigerians who claimed that their rights were violated

were further probed, and sadly, the poll findings revealed that

30 percent of Nigerians nationwide claimed that government

officials are primarily responsible for violating their rights.

Similarly, 26 percent lamented that their rights have been

violated by the police, while 22 percent blamed family and

friends for violating their human rights.

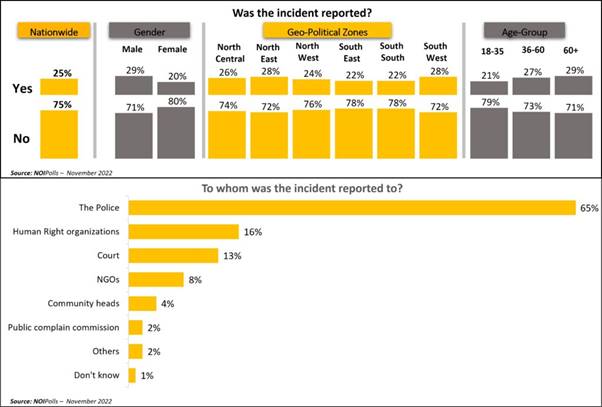

When

asked if the incident was reported, 25 percent indicated that

the incident was reported while 75 revealed that it was not

reported.

Of the

proportion (25 percent) who claimed that the incident was

reported, 65 percent stated that they reported it to the police.

While 16 percent mentioned that they reported to Human Rights

Organizations, 13 percent reported to the court among other

organizations

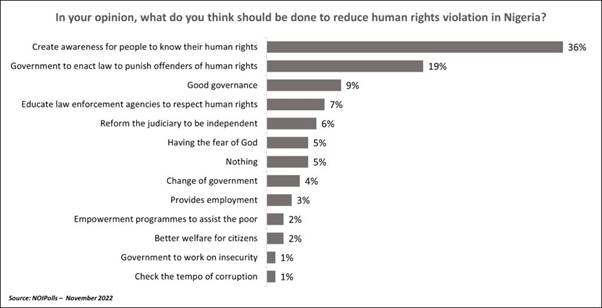

With

regards to recommendations on reducing human rights violations

in Nigeria, 36 percent of Nigerians suggested that the

government should create awareness for people to know their

basic human rights. Similarly, while 19 percent advocated for

the government to enforce laws against human rights violators in

the country, 9 percent encouraged good governance as a way of

reducing human rights violations in Nigeria. Another 7 percent

advised that law enforcement agencies in Nigeria should be

taught and made to respect basic human rights while 6 percent

hinted that the judicial system in the country should be allowed

to be independent amongst other mentions.

In

conclusion, the poll results have shown that most Nigerians

believe that human right violation is prevalent in the country.

For instance, 31 percent of adult Nigerians nationwide disclosed

that their rights have been trampled upon before while few

claimed that they know people whose rights have been infringed

on in the past.

Sadly,

respondents who claimed that their right to freedom of movement,

‘right to freedom from torture/degrading treatment, and ‘right

to life had been violated in the past reported they were

primarily violated by government officials and the police. Given

that government officials and the police are ranked highest

violators of human rights, it is, therefore, imperative that

routine training is conducted, reorientation of law enforcement

officers across all cadres, and government officials are

sensitized on what constitutes human rights as part of efforts

to protect the citizenry.

Finally, the poll result showed that most victims of human

rights violations in Nigeria do not report violations committed

against them. Therefore, it is important to create frequent

awareness campaigns for the citizenry on their basic human

rights as recommended by 36 percent of the adult Nigerians

interviewed. Also, as advocated by 19 percent of Nigerians, the

government should enforce laws against human rights violators in

the country as this will serve as a warning to other violators

of human rights in Nigeria.

December 15, 2022

Source:

https://noi-polls.com/human-rights-poll-2/

WEST EUROPE

773-43-05/Polls

Six In Ten Are Reducing Their Heating Usage, Despite

Recent Cold Weather

Half of

the population are wearing more layers or using blankets to

avoid high energy costs while 13% are still not using heating at

all

Similarly to when we

asked in October,

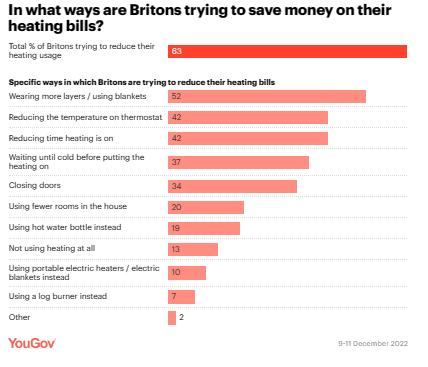

three quarters (73%) of the public are cutting back on the

amount of gas and electric they use at home, with six in ten

(63%) reducing their heating usage specifically.

The most common ways the public are trying to

reduce heating usage include wearing more layers or using

blankets (52%), reducing the temperature on the thermostat (42%)

or reducing the time they have the heating on (42%). People are

also being cautious about heating individual rooms, with

a third (34%) making sure they are closing doors to keep heat in

a certain room and one in five (20%) using fewer rooms in their

home. The number of people taking these steps have all increased

since October.

Despite temperatures dropping below zero in many

areas of the country, 13% of Britons say they are not using

their heating at all. This is down from 25% back in October when

temperatures were a lot milder. Amongst those struggling

financially, a quarter (26%) are currently still not using

heating at all, down from 44% two months ago.

December 14, 2022

773-43-06/Polls

Support For Nurse Strikes Falls – Though Still

Outweighs Opposition – As Half Say The Pay Rise They’re Asking

For Is Too High

Most Britons appear to be aware of the reasons for

the strikes, with around three-quarters (77%) believing they are

striking for an increase in pay, while around a third (32%) say

it is for better standards of care for patients. Other common

reasons for the strikes mentioned are to increase staff numbers

in the NHS (41%) or to increase the amount of money spent on the

NHS (33%).

When considering how acceptable it is for healthcare

workers to strike for different reasons, the majority of Britons

find both an increase of pay (61%) and better standard of care

for patients (68%) acceptable reasons.

Looking specifically at the request of the Royal

College of Nursing for a 5% pay rise on top of inflation – a

total pay rise of 17%, around half of Britons (49%) think this

pay rise is too high. Meanwhile, 37% say it is about right and

only 7% deem it too low.

The public are concerned about the ability of the NHS

to provide safe care for patients during the strike actions -

80% are concerned about this for the nurse strikes, and 82% for

the strikes by ambulance workers.

Kate

Duxbury, Research Director at Ipsos, said:

There

are signs that support for the nurses’ strikes has fallen since

November, perhaps as the strikes have become a reality and

concerns about the ability of the NHS to provide safe care for

patients during the strikes set in. On balance though, the

public are supportive rather than in opposition to both the

nurses’ and ambulance workers’ strikes – it remains to be seen

how this will change as the strikes progress, given the public’s

often positive views of, and concern for, NHS staff.

15

December 2022

773-43-07/Polls

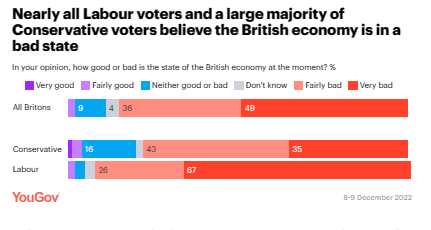

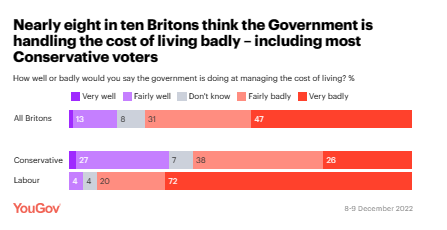

Most Britons Have A Negative Economic Outlook For The

Country Amid The Rising Cost Of Living

The

majority of Britons say the government is managing the cost of

living badly

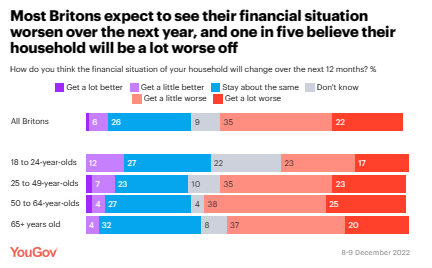

There has been a small shift in people’s expectations

of their own finances, although this should also be of concern

to the Government. When first asked in September, 65% said that

they expected their household’s financial situation to get worse

over the next year; this figure has now dropped to 57%.

However, while fewer people are now saying they have

negative expectations, they have only moved as far as saying

they expect their situation to be about the same, rather than

anticipating better times ahead. Given that nearly two thirds

(64%) say their finances have got worse over the last 12 months,

it appears that government support is having a limited impact.

The British public are also concerned about exactly

what measures will be taken to try and boost the economy. Three

quarters (73%) are worried that in the next two to three years

people like them will suffer directly from cuts in public

services spending as the government looks to tighten the purse

strings, while 4 in 10 (43%) are concerned about losing their

job or struggling to find work.

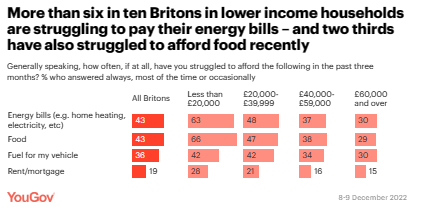

Low-income households are struggling with essential costs

Low-income households are particularly feeling the

pinch, with 70% of Britons with a household income of Ł20,000 or

less saying that they have already had to make cuts to their

usual spending in response to the rising cost of living

including more than half (56%) who say they expect to make

further cuts. Amongst Britons in low-income households, 4 in 10

(37%) say they are struggling to pay their energy bills most or

all of the time, and a third (32%) say they struggle to afford

food most or all of the time.

Most worryingly, half of Britons (49%) in low-income

households are either struggling to make ends meet (35%) or

cannot afford their essential costs and are going without food

and heating (14%) as we enter the coldest months of the year.

773-43-08/Polls

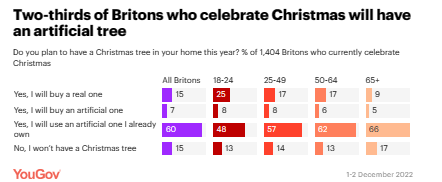

Two-Thirds Of Britons Who Celebrate Christmas Will

Have An Artificial Tree This Year

More

than half of Britons believe a fake tree is the greener option

This is likely because the older generation has long

since invested in an artificial tree, before environmental

considerations became a factor, with two-thirds of those aged 65

and over using a fake tree they already own compared to 48% of

18-24 year olds.

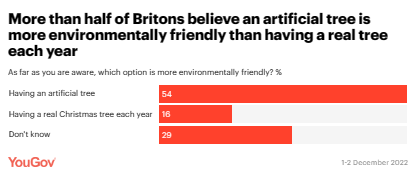

More

than half of Britons believe an artificial tree is more

environmentally friendly

When considering manufacturing, materials, packaging

and transport, a six-and-a-half-foot artificial tree has a

carbon footprint equivalent to about 40kg of greenhouse gas

emissions.

This is more than twice that of a real tree of the same size

that ends up in landfill and more than 10 times that of a real

tree which is burnt.

More than half of Britons (54%) think that having an

artificial tree is more environmentally friendly than having a

real tree each year, with only 16% believing a real tree is the

greener option. It is estimated that you would need to keep

a fake Christmas tree for at least 7 years before it has

less of a carbon impact than buying a real tree each year.

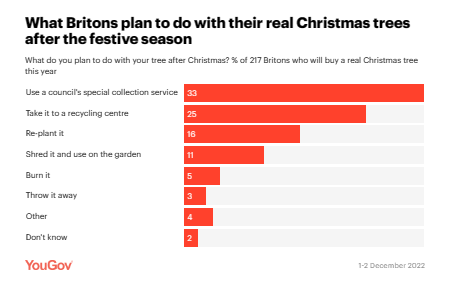

How do

Britons with real Christmas trees dispose of them?

In terms of disposing of a real Christmas tree

following the festive season, a third of Britons (33%) will take

advantage of their local authority’s special collection service,

with the trees then shredded and used on gardens and parks. A

quarter of Britons (25%) will take their tree to a recycling

centre, while 16% will re-plant it, and one in nine (11%) will

shred it and use it on their own garden.

December 16, 2022

773-43-09/Polls

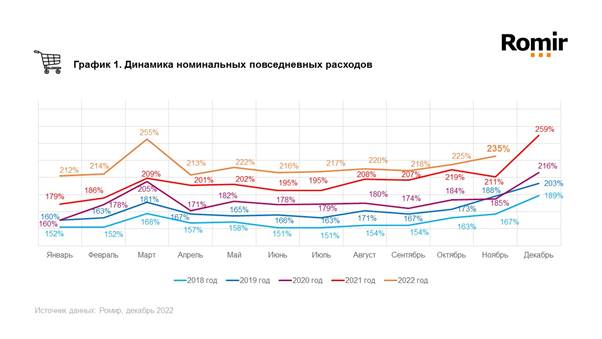

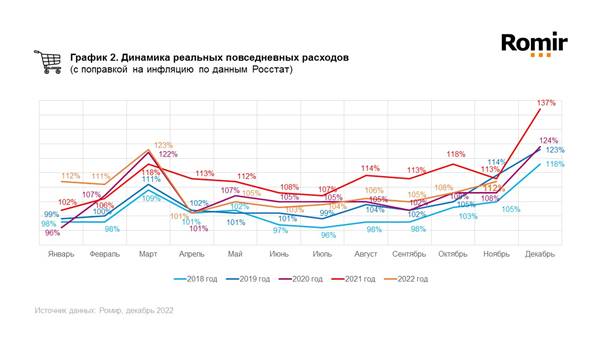

Spending Of Russians In November Increased

Romir presents a monthly index of consumer activity*

of Russians, demonstrating a change in household consumption of

consumer goods. The index is calculated for both nominal and

real expenses (adjusted for inflation according to Rosstat).

The index of real expenditures (adjusted for

inflation) in October was 112%. Real

expenditures increased by 4 percentage points (3.7%) compared to

the previous month, but lower by 11 percentage points (0.9%)

than in November last year.

16

December 2022

Source:

https://romir.ru/studies/romir-rashody-rossiyan-v-noyabre-uvelichilis

773-43-10/Polls

1 in 3 Dutch people cut back on groceries

The rising prices of groceries and other fixed costs

areputting the Dutch in their pockets. The reaction to this is

visible: the Dutch consumer keeps his hand on the cut.

For example,the five Dutch people pay

attention to the expenditure, whereby this is really necessary

for one third to be able to make ends meet. The Dutch are

cutting back in different ways. This way, athird saves on

groceries. This is evident from representative online

research by Motivaction among 1,020 Dutch people, conducted in

October 2022.

Consumers go for cheaper and replace A-brands for private labels

How does Dutch consumers tackle austerity? Consumers

are opting for cheaper products in large numbers. For example,

eand a quarter of consumers buy fewer products from

A-brands. Eand larger group – a third of consumers – mainly buys

more private label products. The second way to cut back is to

cook more yourself. Eand a quarter of consumers dive into the

kitchen more often and are less likely to use convenience

products and ready-made products. Thirdly, we see a slight

decrease in the purchase of organic products, sustainable

products and local products. Finally, there is one way of

cutting back that everyone knows and that 34% also actively

use: offers.

Consumers cut back on unhealthy food and pull the cutting

board out of the closet more often

Although in the winter

months the supermarkets are full of goodies, from wreaths for

the tree to chocolate milk with whipped cream, a fifth of

consumers are cutting back on unhealthy food this

year. We mainly cut back on sweets and cakes. But ohok the ready

meals, frozen pizzas and other frozen meals latand we stand more

often. At the same time, there is an increase in the often

cheaper, healthy options such as fresh, uncutn vegetables, dry pasta

and frozenvegetablesn.

Saving

money and feeling good

Dutch and saving is a well-known combination. We go

to the drugstore for promotions such as 2 for the price of 1, we

drive to the neighboring countries for cheaper

beer and gasoline and on the groceries weet 71% of the Dutch how

they can best save. Besparen provides financialbenefit, but that

is not the only thing. For example, 64% of consumers get a good

feeling from this. To save money, just under half of consumers

visit several supermarkets every week. In addition, a third of

consumers go to a supermarket with lower prices in order to

score the best deals.

(Motivaction

Insights and Strategy)

12

December 2022

773-43-11/Polls

More Than 4 Out Of 10 French People Have Been Victims

Of Cyberviolence

Moreover, among

the respondents to the victims' survey,

the majority are women (84%

of respondents) as well as people discriminated

against because of their gender identity and sexual orientation

(43%). In more than 1 in 2 cases (51%) the victim was under 30

years of age at the time of the crime. As for the gendered

dimension of online attacks, it also appears via the data

collected on those identified as responsible for cyberviolence: men

are involved in the perpetration of this violence in at least

74% of cases.

While threats and insults are the most frequent

situations encountered by victims (93%), the non-consensual

dissemination of intimate or degrading content concerns more

than half of them (52%). Revictimization

is frequent and 93% of victims say they have experienced several

situations of cyberviolence, 40% of them even report having

experienced between 7 and 10. Insults, threats,

sending photos of genitals and exposure to violent content are

situations that the majority of victims have suffered several

times.

Far from being a

virtual evil, cyberviolence

has an extremely heavy impact on the health of victims,

but also on their relational, family, school and professional

development. The consequences

can be extreme and 14% of victims say they have attempted

suicide as a result of the violence suffered. It is

impossible today to draw a clear line between offline and

online: cyberviolence is intertwined with violence experienced

in the tangible space and is part of a continuum of

violence that most often targets women, girls and the most

discriminated against.

However, the fight against this violence still relies

mainly on the victims, who, in the absence of satisfactory

remedies, feel isolated and develop costly and exhausting coping

strategies. Less than one

victim in 10 say they knew how to react at the time of violence

and more than a third of them (36%) report having been made

guilty when they confided in their entourage or professionals, this

figure even rises to 69% for victims of non-consensual

dissemination of intimate or degrading content.

Violence that is part of a continuum and continues offline

The digital space is not separated from the tangible

world: threats made online do not remain at the stage of threats

and are carried out, thus, 72%

of victims say that cyberviolence has continued in person. They

are even nearly 1 in 5 (16 and 18%) to report a experience of

physical or sexual violence accompanying online violence.

Victims of cyberviolence are therefore at great risk: it is not

enough to turn off your computer or deactivate your social media

accounts to stop this violence.

Moreover, for one

in two victims (49%) the situation has been long-term and the

violence has continued for at least a month – or even more than

a year for a quarter of the victims. This violence

leads victims to submit to costly coping and avoidance

strategies that cause physical and psychological exhaustion and

are harmful to their agency and freedom of expression. 32%

of them have deactivated their social accounts following the

violence.

Serious

consequences for the health and lives of victims

The psychological and social consequences of

cyberviolence are numerous and significant for victims, even

more so when it comes to women and people discriminated

against. In 1 in 2 cases, a

medium to very high impact is reported by victims on their

education or professional life. Online violence is

also the cause of major health problems: it has a psychological

impact in 80% of cases, and even a physical impact for 1 in 2

victims (46%).

Among

the consequences reported by the victims, there are many

symptoms of post-traumatic stress: hypervigilance

(91%), anxiety and depressive disorders (88%) and insomnia (78%)

and suicidal thoughts (49%). 45% of victims develop eating

disorders and nearly 1 in 5 victims say they have already

self-harmed as a result of violence. Finally, 31% of victims say

they have increased their consumption of alcohol and substances

because of the violence suffered.

An

over-representation of women and discriminated against among

respondents.

The digital world is a reflection of our society:

there are all the oppressions and inequalities observed offline

and the violence perpetrated there often targets the most

discriminated against. Thus, the victims of cyberviolence who

took the time to answer the questionnaire to testify about their

experiences are mostly women

(84%) and people who say they belong to a minority group and/or

have a disability (80%). 72% of LGBTQI+ people report

having experienced 7 to 10 situations of cyberviolence compared

to 40% of respondents overall. In addition, people

from disadvantaged groups or with disabilities report

significantly greater consequences on their lives and health. Thus,

LGBTQI+ people are more likely to feel hopeless and anxious than

those who are not part of a minority group, they are also 3

times more likely to self-harm.

People with

disabilities report 2 times more often a physical impact of violence than non-disabled people and are 3 times more

likely than them to fail their studies — moreover, the violence

they suffer has 6 times more often very serious consequences on

their schooling or studies. As for racialized people, they

report becoming hypervigilant 2 times more frequently than

people who do not belong to a minority group. Victims

discriminated against because of their religion are 3 times more

likely to say they can no longer go to school or work as a

result of online violence.

Poor

access to the law

The

judicial process of victims is fraught with pitfalls: 61% of

respondents think that filing a complaint is useless and they

cannot really be proven wrong. Although

one in 4 victims went to the police station or gendarmerie, they

complain in 70% of cases that their complaint has not resulted

in any prosecution, while a third of victims have

been refused to file a complaint – although this refusal is

illegal. As for people from a religious minority, they are 4

times more likely to be unwelcome by the police and gendarmerie

and not to be able to file a complaint than people who are not

part of a minority group. Overall, online violence experienced by respondents resulted in a

complaint followed by legal proceedings in only 3% of cases. Access

to victims' rights is clearly insufficient and 17%

of them say they did not file a complaint because they did not

know they could do so.

A cruel

lack of information and recourse

69% of

victims admit that they did not know how to react when

confronted with a situation of cyberviolence. While

74% were able to talk to at least one person about the violence,

more than a third of those who remained silent did so because

they did not know who to talk to or because they were afraid of

the consequences/that the situation would worsen, and more than

a quarter remained silent because they felt guilty. When they

confided, the victims did so primarily in the friendly sphere —

much less in the family or medical context. In

addition, the level of information regarding support systems

remains very low: 81% of victims say they are poorly informed on

platforms available to help them, this figure even

rises to 92% for those who were under 25 years old at the time

of the violence. Only 27% of

victims say they have heard of a device such as 30 18 and only

3% have used it. These figures point to serious and

regrettable shortcomings in terms of government initiatives to

ensure public information and care for victims of cyberviolence.

December 15, 2022

Source:

https://www.ipsos.com/fr-fr/cyberviolences-et-cyberharcelement-le-vecu-des-victimes

773-43-12/Polls

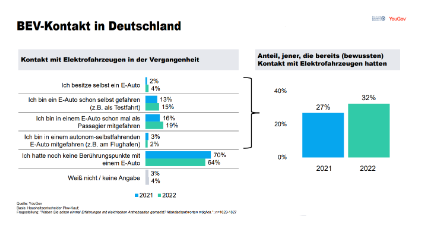

German E-Car Market Is Growing

In the joint project "Electric Car Market &

Innovation Report 2022", YouGov and the Center of Automotive

Management (CAM) are examining, among other things, the

demographic composition of potential BEV customers and the

purchase intentions of German consumers, as well as the

developments in the electric mobility market in Germany.

Who buys electric cars?

The group of potential BEV buyers more often consists

of men (62 percent) between the ages of 31 and 50 (43 percent).

34 percent of this target group currently owns more than one car

and one in three BEV buyers (29 percent) believes that

environmental policy should be completely preventive.

Environmental protection is a high priority for potential BEV

buyers and they see themselves as environmentalists. The

majority of this target group (82 percent) sees climate change

as the greatest threat to humanity (vs. 71 percent of the total

population). 80 percent are of the opinion that fewer cars

should be driven to protect the environment and that electric

cars are clearly the means of transport of the future (76 vs. 47

percent of the total population). Potential BEV buyers are open

to new technologies and products and generally have a keen

interest in science and computers. The vast majority (88

percent) of the target group believe that technology makes life

easier and many like to test products before they hit the market

(69 vs. 62 percent car decision makers). Almost half of

potential BEV buyers (49 percent) are interested in science and

finance (47 percent)

Existing problems

Although the German EV market continues to grow

dynamically, there are still large gaps in consumer knowledge

that need to be closed for a possible purchase. The number of

household decision-makers who previously had direct contact with

electric vehicles (e.g. through their own ownership, test or

taxi rides) increased by 5 percentage points compared to the

previous year, but only 32 percent still had direct contact due

to a lack of concrete contact points. Consumers most frequently

come into contact with electric cars as passengers (19 percent).

Despite few points of contact, consumers see the

advantages of e-cars: 29 percent of potential BEV buyers believe

that current energy costs have made e-cars more attractive.

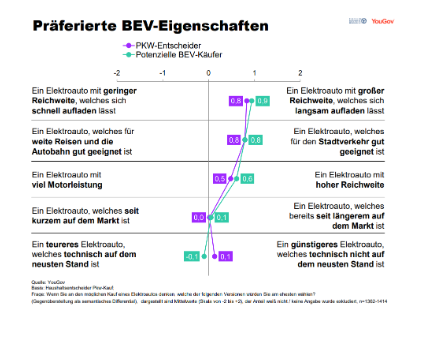

However, the target group of potential BEV buyers have concrete

ideas about the basic technical needs that an electric car

should meet. Both potential BEV buyers and the group of car

decision-makers in the household prefer an electric car with a

long range and would also accept a longer charging time (0.9 and

0.8 percent respectively). In the eyes of consumers, an electric

car should also be more suitable for city traffic and have a

long range. A high engine power and a good suitability for the

highway are currently rather less interesting.

With regard to improving the range and the public

charging infrastructure, expectations of manufacturers and

politicians are high, but consumers expect government support

programs for electric mobility (37 percent) and electricity

costs (74 percent) to deteriorate over the next 12 months. Many

are already of the opinion that politics does not relieve

motorists enough (51 percent potential BEV buyers, 64 percent

car decision-makers).

December 13, 2022

Source:

https://yougov.de/topics/consumer/articles-reports/2022/12/13/deutscher-e-auto-markt-wachst

773-43-13/Polls

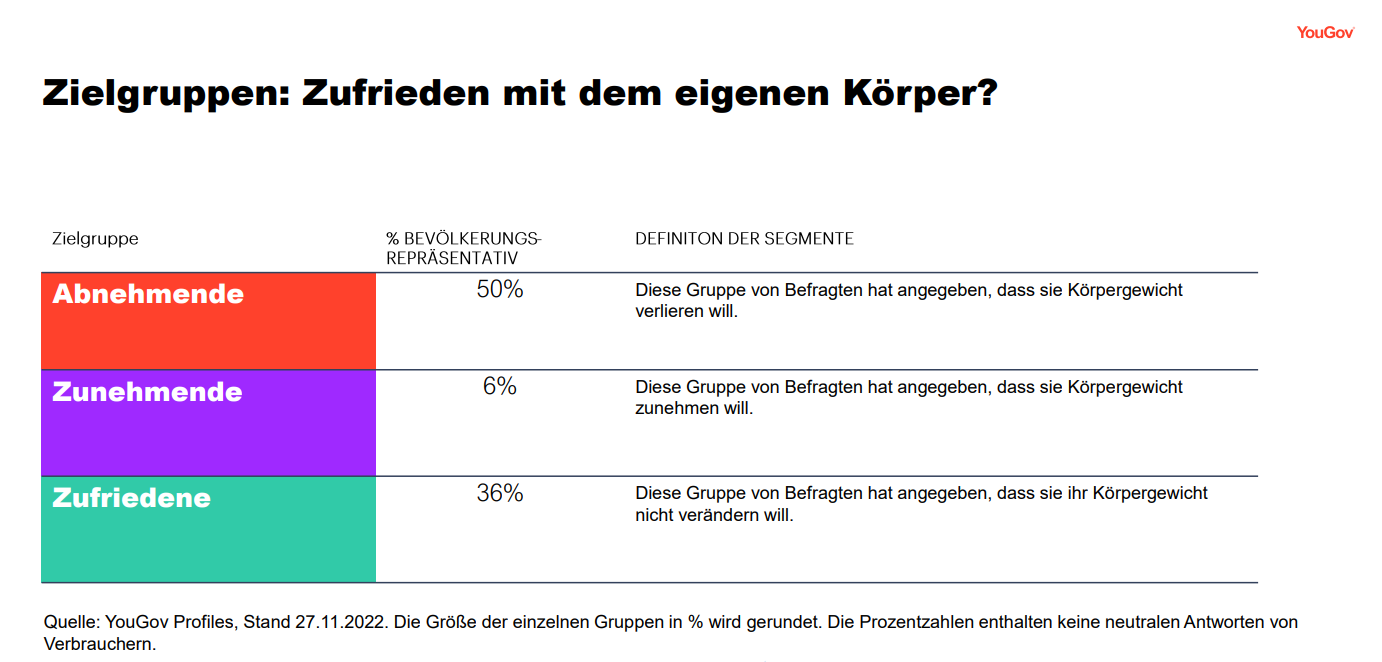

Good Intentions: More Than Half Of Germans Want To

Change Body Weight

Regardless of summer or winter, a slight majority of

people in Germany want to change their own weight. As reasons,

they name not feeling comfortable in their own body, but often

health reasons are also mentioned. In the current target group

analysis "Bodytransformation",

we use the target group segmentation tool YouGov Profiles and

data from the YouGov

RealTime Omnibus to examine the target groups of those

consumers who plan to gain or lose weight, but also those who

are satisfied with their weight. The analysis takes a look at

the demographic characteristics as well as the motivations and

approach of the three consumer groups.

Women

most often want to lose weight

Half of Germans are losing weight (50 percent), so

they want to lose body weight. Decreasing are predominantly

women (57 percent) and people who live in relationships (57

percent vs. 52 percent of the total population). More than half

of this group (51 percent) eat frequently out of boredom (vs. 42

percent). Losing weight people spend a lot of time on social

media, most often on Facebook (62 percent) and Instagram and

YouTube (42 percent each). 57 percent of people losing weight

want to lose weight because they don't feel comfortable in their

bodies. But health reasons are also

often cited as motivation to lose weight (42 percent). To lose

body weight, the majority of people losing weight plan to eat

less (64 percent), change their diet (55 percent) or exercise

(52 percent).

Increasing are more likely to be men

Only 6 percent of Germans say they want to gain

weight. This target group is more often male (71 percent) and

significantly more likely to have a migrant background (40

percent vs. 17 percent of the total population). The vast

majority of this consumer group (76 percent) enjoy discovering

new dishes and foreign cuisines. This group is less active on

Facebook than those consumers who want to lose weight (54 vs. 62

percent). Instagram (46 percent) and YouTube (44 percent), on

the other hand, use them more often. The reasons for the desired

weight gain are similar to those of those who lose weight: not

feeling comfortable in their own body (38 percent) and health

reasons (36 percent). In contrast to the group of people losing

weight, the increasing also cite great social pressure as

motivation (20 percent vs. 6 percent of those losing weight). To

gain weight, this target group plans to eat more (45 percent),

exercise (37 percent) and change their diet (32 percent).

December 15, 2022

NORTH AMERICA

773-43-14/Polls

Americans Don’t Have A Clear Idea Of Which Of Their

Actions Have The Strongest Impact On Climate Change

Majorities of Americans think recycling, using energy

efficient appliances, and carpooling have a large or moderate

effect on reducing greenhouse gas emissions caused by a single

person, despite research showing

that these don’t make as much of a difference. The public is

split on the impact of avoiding long flights, lowering the room

temperature, buying fewer things, and installing a heat pump.

Far fewer believe that changing their diet through eating

vegetarian, vegan, or organic food has a large or moderate

impact on a single person’s emissions, even as outside research

indicates that these actions can have a sizeable impact on

reducing greenhouse gas emissions. Through it all, across nearly

all of these actions, partisan divisions exist.

To learn more about this, visit the interactive quiz

the New York Times put together here.

Detailed findings:

About

the Study

This NYTimes/Ipsos poll was conducted December 9 –

12, 2022, by Ipsos using the probability-based KnowledgePanel®.

This poll is based on a nationally representative probability

sample of 1,023 general population adults age 18 or older.

The margin of sampling error for this study is plus

or minus 3.3 percentage points at the 95% confidence level, for

results based on the entire sample of adults. The margin of

sampling error takes into account the design effect, which was

1.17. The margin of sampling error is higher and varies for

results based on other sub-samples. In our reporting of the

findings, percentage points are rounded off to the nearest whole

number. As a result, percentages in a given table column may

total slightly higher or lower than 100%. In questions that

permit multiple responses, columns may total substantially more

than 100%, depending on the number of different responses

offered by each respondent.

The survey was conducted using KnowledgePanel, the

largest and most well-established online probability-based panel

that is representative of the adult US population. Our

recruitment process employs a scientifically developed

addressed-based sampling methodology using the latest Delivery

Sequence File of the USPS – a database with full coverage of all

delivery points in the US. Households invited to join the panel

are randomly selected from all available households in the U.S.

Persons in the sampled households are invited to join and

participate in the panel. Those selected who do not already have

internet access are provided a tablet and internet connection at

no cost to the panel member. Those who join the panel and who

are selected to participate in a survey are sent a unique

password-protected log-in used to complete surveys online. As a

result of our recruitment and sampling methodologies, samples

from KnowledgePanel cover all households regardless of their

phone or internet status and findings can be reported with a

margin of sampling error and projected to the general

population.

The data for the total sample were weighted to adjust

for gender by age, race/ethnicity, education, Census region,

metropolitan status, household income, and party identification.

The demographic benchmarks came from the 2021 March Supplement

of the Current Population Survey (CPS). The party identification

benchmark comes from ABC News.

15

December 2022

Source:

https://www.ipsos.com/en-us/news-polls/new-york-times-climate-action

773-43-15/Polls

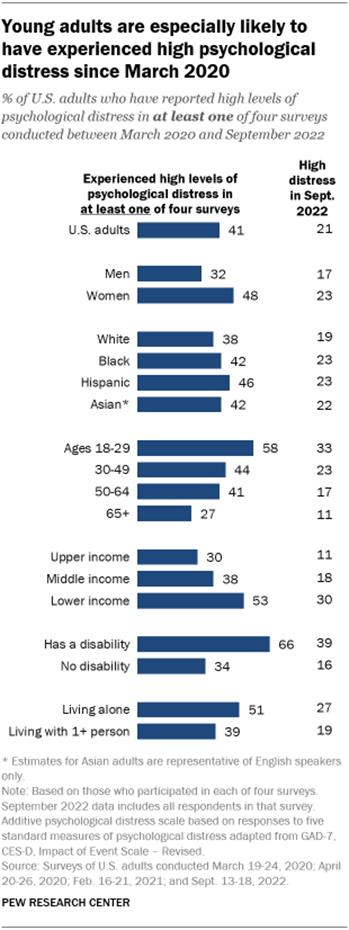

At Least Four-In-Ten US Adults Have Faced High Levels

Of Psychological Distress During Covid-19 Pandemic

At least four-in-ten U.S. adults (41%) have

experienced high levels of psychological distress at least once

since the early stages of the coronavirus

outbreak,

according to a new Pew Research Center analysis that examines

survey responses from the same Americans over time.

How we

did this

The analysis highlights the fluid nature of

psychological distress among Americans, as measured by a

five-item index that asks about experiences such as loneliness,

anxiety and trouble sleeping.

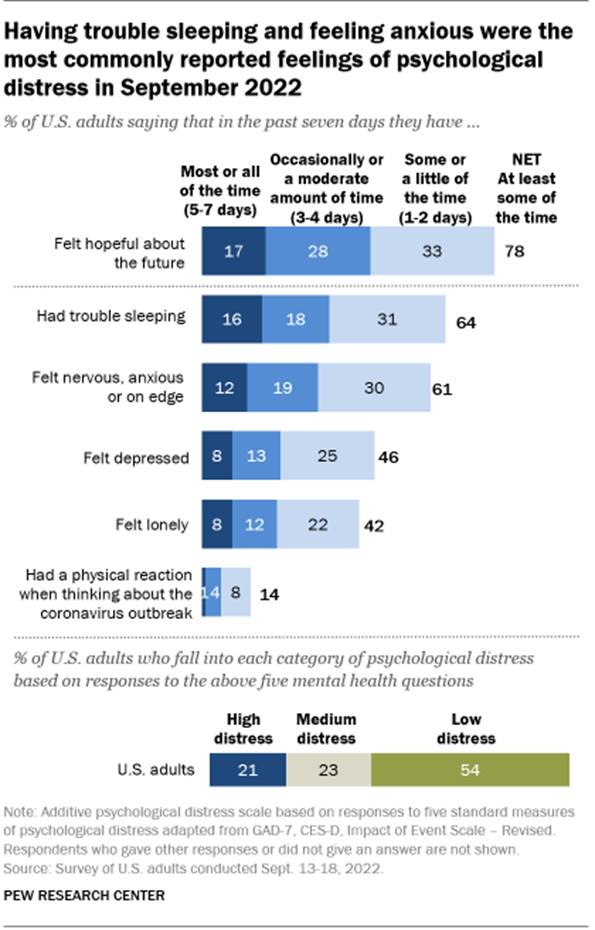

In the September 2022 survey, 21% of U.S. adults fell

into the high psychological distress category; in each of four

surveys, no more than 24% of adults have fallen into this

category. But because individuals experience varying levels of

distress at different points in time, a significantly larger

share of Americans (41%) have experienced high psychological

distress at least once across

the four surveys conducted over the past two and a half years.

In addition to age, experiences of high psychological

distress are strongly tied to disability status and income.

About two-thirds (66%) of adults who have a disability or health

condition that keeps them from participating fully in work,

school, housework or other activities reported a high level of

distress at least once across the four surveys. And those with

lower family incomes (53%) are more likely than those from

middle- (38%) and high-income households (30%) to have

experienced high psychological distress at least once since

March 2020.

While many Americans faced challenges with mental

health before the coronavirus pandemic, public health officials warned

in early 2020 that the pandemic could exacerbate

psychological distress. The negative effects of the outbreak

have hit some people harder than others, with women, lower-income

adults, and Black and Hispanic adults among the groups who

have faced disparate health or financial impacts.

Americans’ personal levels of concern about getting

or spreading the coronavirus have continued

to decline over the course of 2022. The coronavirus is one

of many potential sources

of stress, including the economy and worries about the

future of the nation.

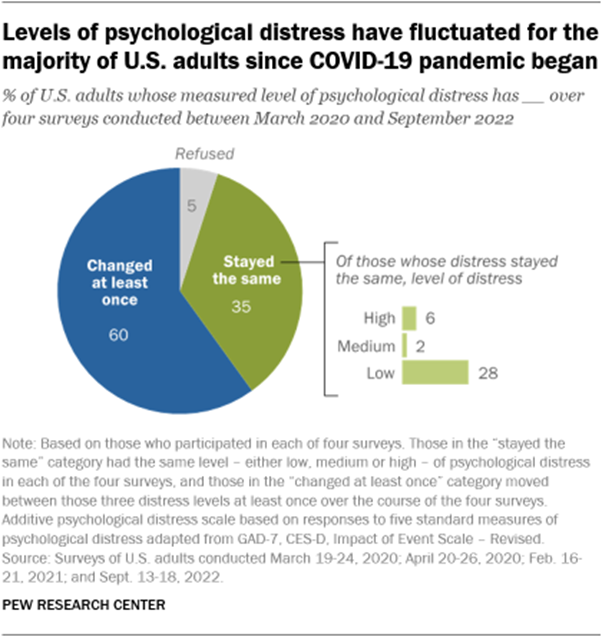

Psychological distress levels have shifted for most Americans

during the pandemic

Amid the shifting

landscape of COVID-19 in the United States, just 35% of

Americans have registered the same level of psychological

distress – whether high, medium or low – across all four surveys

conducted by the Center since March 2020.

Instead, a majority of respondents (60%) moved in and

out of levels of psychological distress. Psychological distress

increased for some but decreased for others. One illustration of

the fluid nature of these experiences is that while 41% of U.S.

adults faced high psychological distress at

least once across four surveys, just 6% experienced

high distress in all four surveys. Nearly five times as many

(28%) experienced low distress in all of the surveys.

The index of psychological distress is based on

measures of five types of possible distress experienced in the

past week, such as anxiety or sleeplessness, that are adapted

from standard psychological measures. As used in the current

survey, the questions are not a clinical measure nor a

diagnostic tool; they describe people’s emotional experiences

during the week prior to the interview.

Only one question refers specifically to the

coronavirus outbreak. It asks how often in the past week

Americans have “had physical reactions, such as sweating,

trouble breathing, nausea, or a pounding heart” when thinking

about their experience with the coronavirus outbreak. In the

most recent September survey, 14% of Americans answered this

question affirmatively. In March 2020, in the early stages of

the outbreak, 18% said they had experienced this.

Trouble sleeping is one of the most common forms of

distress measured in the surveys. In the latest survey, about

two-thirds of adults (64%) reported trouble sleeping at least

some or a little of the time during the past week. A similar

share (61%) said they had felt nervous, anxious or on edge.

Experiences with depression and loneliness also

register with sizable shares of Americans. In the most recent

survey, 46% of adults said they had felt depressed at least one

or two days during the past week, and 42% said they had felt

lonely.

All four surveys have included a question about

positive feelings, though it is not part of the psychological

distress index. Overall, 78% of U.S. adults said they had felt

hopeful about the future at least one or two days in the past

week, according to the latest survey from September. However,

22% of adults said they had felt hopeful about the future rarely

or none of the time during the past week.

DECEMBER 12, 2022

773-43-16/Polls

Striking Findings From 2022

Pew Research Center’s surveys have shed light on

public opinion around some of the biggest news events of 2022 –

from Russia’s military invasion of Ukraine to the

overturning of Roe v. Wade to Americans’

experiences with extreme weather events.

Here’s a look back at the past year through 15 of our

most striking research findings, which cover these topics and

more. These findings represent just a sample of the Center’s research

publications this year.

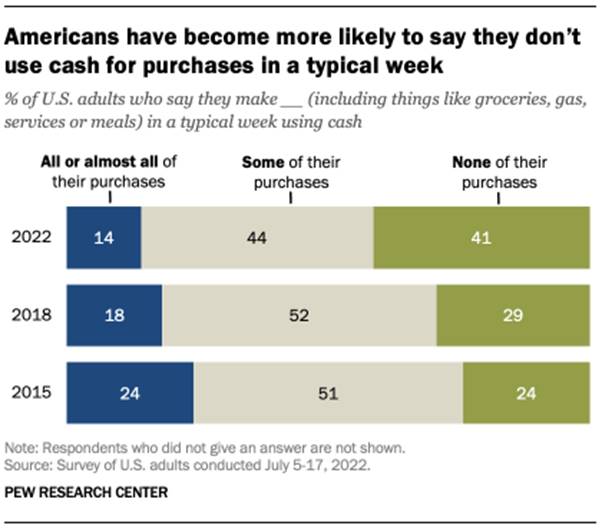

Today, roughly four-in-ten Americans (41%) say none

of their purchases in a typical week are paid for using cash, a

July survey found. This is up from 29% in 2018 and 24% in 2015.

While growing shares of Americans across income

groups are relying less on cash than in the past, this is

especially the case among the highest earners. Roughly

six-in-ten adults whose annual household income is $100,000 or

more (59%) say they make none of their typical weekly purchases

using cash, up sharply from 43% in 2018 and 36% in 2015.

If

recent trends continue, Christians could make up a minority of

Americans by 2070. That’s according to

a September report that models several hypothetical scenarios

of how

the U.S. religious landscape might change over the next 50

years, based on religious switching patterns.

Since the 1990s,

large numbers of Americans have left Christianity to join the

growing ranks of U.S. adults who describe their religious

identity as atheist, agnostic or “nothing in particular.”

Depending on whether religious switching continues at

recent rates, speeds up or stops entirely – the

last of which is not plausible because it assumes all

switching has already ended – the projections show Christians of

all ages shrinking from 64% to somewhere between 54% and 35% of

all Americans by 2070. Over that same period, “nones” would rise

from their current 30% of the population to somewhere between

34% and 52%.

Views

of reparations for slavery vary

widely by race and ethnicity,

especially between Black and White Americans, a

November analysis found. Overall, 30% of U.S. adults say

descendants of people enslaved in the United States should be

repaid in some way, such as given land or money. About

seven-in-ten (68%) say these descendants should not be repaid.

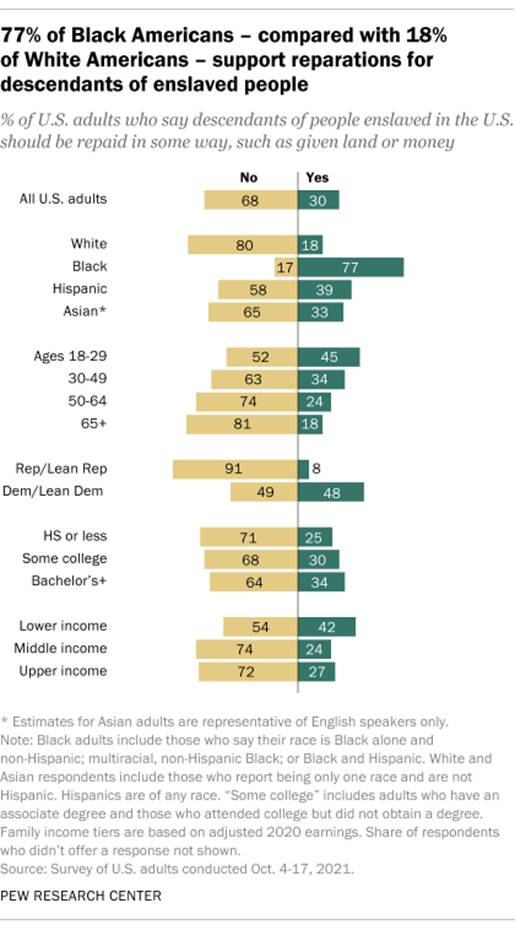

Around three-quarters of Black adults (77%) say the

descendants of people enslaved in the U.S. should be repaid in some way. Just 18% of White adults hold

this view.

There are also notable differences by party

affiliation and age. Among Democrats and Democratic-leaning

independents, views are split: 48% say descendants of enslaved

people should be repaid in some way, while 49% say they should

not. Only 8% of Republicans and GOP leaners say these

descendants should be repaid in some way, and 91% say they

should not.

And 45% of adults under 30 say these descendants

should be repaid, compared with 18% of those 65 and older.

Notably, three-quarters of adults who say descendants

of those enslaved in the U.S. should be

repaid (including 82% of Black adults who say this) say it’s a

little or not at all likely this will happen in their lifetime.

A

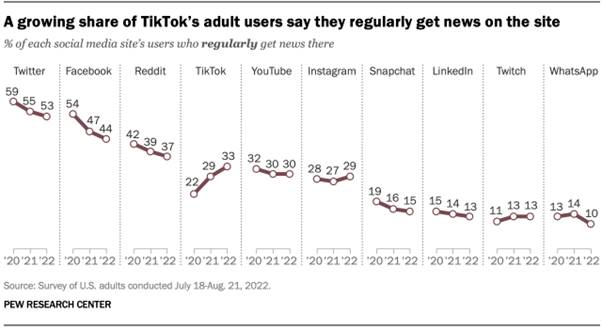

growing share of adult TikTok users in the U.S. are getting

news on the platform,

bucking the trend on other social media sites, according

to a survey fielded in July and August. A third of adults who

use TikTok say they regularly get news there, up from 22% two

years ago. The increase comes even as news consumption on many

other social media sites has either decreased or stayed about

the same in recent years. For example, the share of adult

Facebook users who regularly get news there has declined from

54% in 2020 to 44% this year.

Most

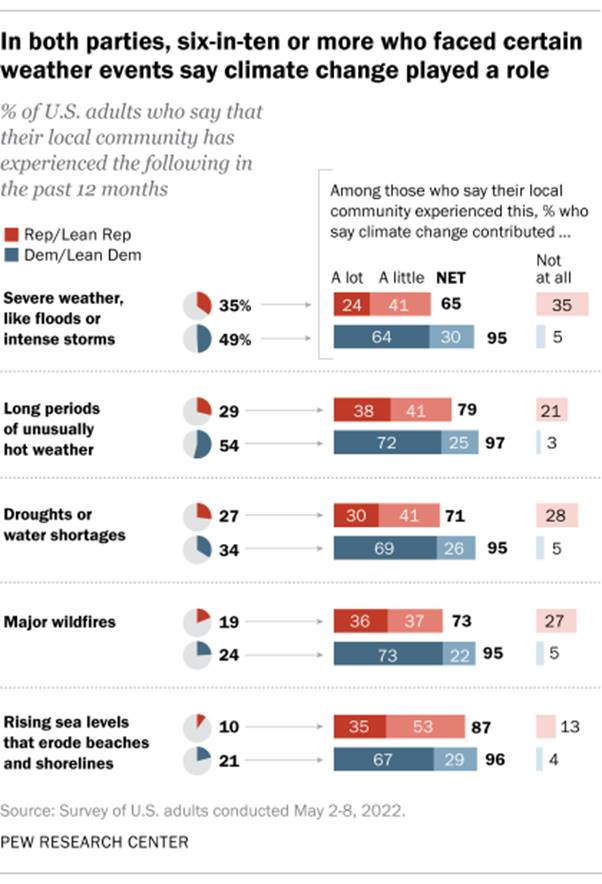

Americans who have experienced extreme weather in the past year

– including majorities in both political parties – see climate

change as a factor, according

to a May survey.

Overall, 71% of Americans said that, in the past 12

months, their community had experienced at least one of the five

forms of extreme weather the Center’s survey asked about. Among

those who had recently encountered extreme weather, more than

eight-in-ten said climate change contributed at least a little

to each type of event.

Among Democrats as well as Republicans, majorities of

those who had experienced one of these forms of extreme weather

said climate change contributed to the event. But Democrats were

more likely than Republicans to say climate change contributed a lot.

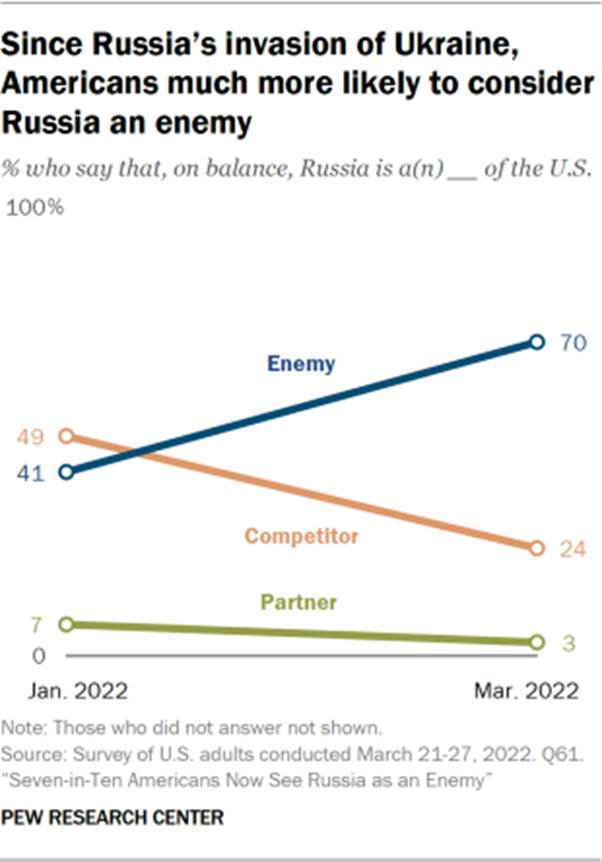

Following Russia’s military invasion of Ukraine, Americans

became much more likely to

see Russia as an enemy of the United States. In March, just after the invasion, 70% of Americans said

that, on balance, Russia is an enemy of the U.S., up sharply

from 41% who held this view in January. In the January survey,

Americans were more likely to describe Russia as a competitor of

the U.S. than as an enemy. In both surveys, very few Americans

described Russia as a U.S. partner.

Democrats and

Republicans largely agreed in the March survey that Russia is an

enemy of the U.S., but partisan and ideological differences

still existed. Liberal Democrats,

for example, were the most likely to see Russia as an enemy

(78%), while moderate and liberal Republicans were the least

likely to do so (63%).

Relatively few Americans take an absolutist view on the legality

of abortion –

either supporting or opposing it at all times, according

to a survey conducted in March, before the Supreme Court

overturned Roe v. Wade. The vast majority of the public is somewhere

in the middle when it comes to abortion: Most think it

should be legal in at least some circumstances, but most are

also open to limitations on its availability in others.

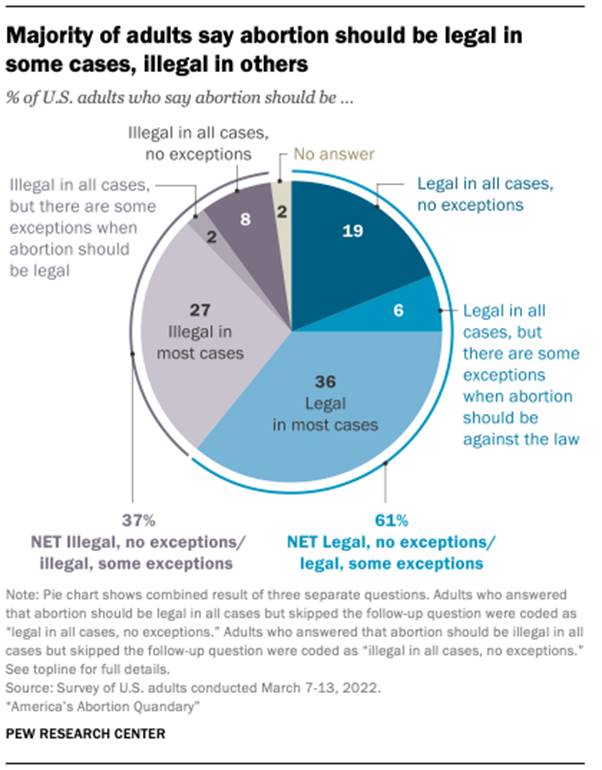

Overall, 19% of Americans say that abortion should be

legal in all cases, with no exceptions. Fewer (8%) say abortion

should be illegal in every case, without exception. But 71%

either say it should be mostly legal or mostly illegal, or say

there are exceptions to their blanket support for or opposition

to legal abortion.

A separate survey conducted in

June and July – after the Supreme Court struck down Roe –

found that 57% of adults disapproved of the decision, including

43% who strongly disapproved. About four-in-ten (41%) approved,

including 25% who strongly approved.

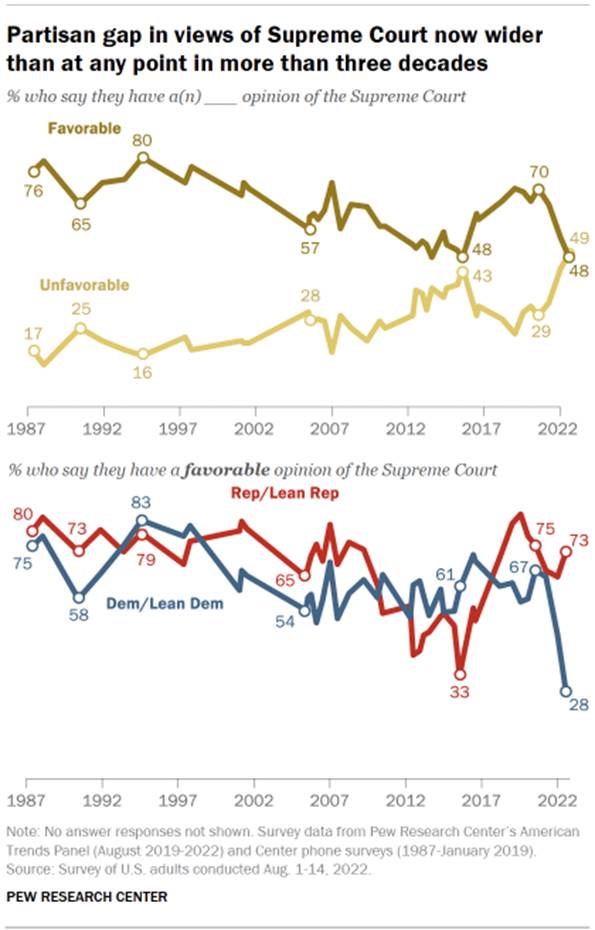

Following the Supreme Court’s decision to overturn Roe v. Wade, the

partisan gap in views of the court grew

wider than at any point in more than three decades. While

73% of Republicans expressed a favorable view of the court in an

August survey, only 28% of Democrats shared that view. That

45-point gap was wider than at any point in 35 years of polling

on the court.

The current

polarization follows a

term that included the

ruling on abortion and several

other high-profile cases that often split the justices along

ideological lines.

Growing shares of Democrats also say the Supreme

Court has a conservative tilt: 67% said this in August, up from

57% in January. And about half of Democrats (51%) said in August

that the justices on the court are doing a poor job of keeping

their own political views out of their judgments on major cases,

nearly double the share who said this in January (26%).

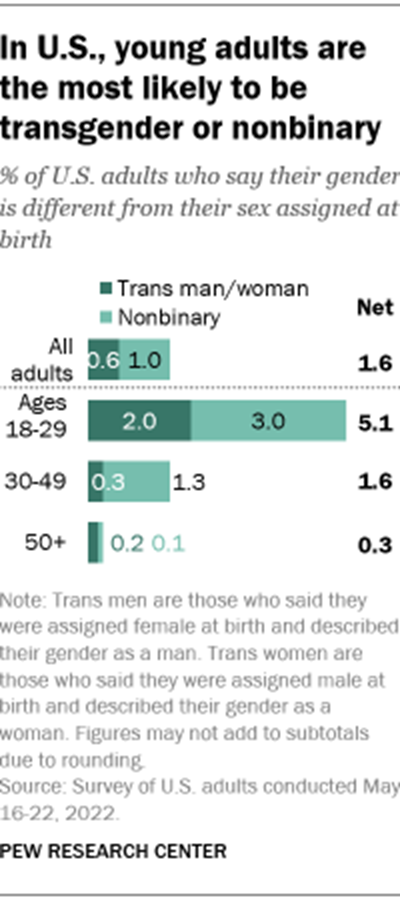

About

5% of Americans younger than 30 are transgender

or nonbinary – that is,

their gender is different from their sex assigned at birth, according

to a survey conducted in May. By comparison, 1.6% of those ages

30 to 49 and 0.3% of those 50 and older say that their gender is

different from their sex assigned at birth. Overall, 1.6% of

U.S. adults are transgender or nonbinary – that is, someone who

is neither a man nor a woman or isn’t strictly one or the other.

While a

relatively small share of U.S. adults

are transgender or nonbinary, many say they know someone who is.

More than four-in-ten (44%) say they personally know someone who

is trans and 20% know someone who is nonbinary. The share of

adults who know someone who is transgender has

increased from 42% in 2021 and from 37% in 2017.

In focus

groups with trans and nonbinary adults, most participants

said they knew from an early age – many as young as preschool or

elementary school – that there was something different about

them, even if they didn’t have the words to describe what it

was.

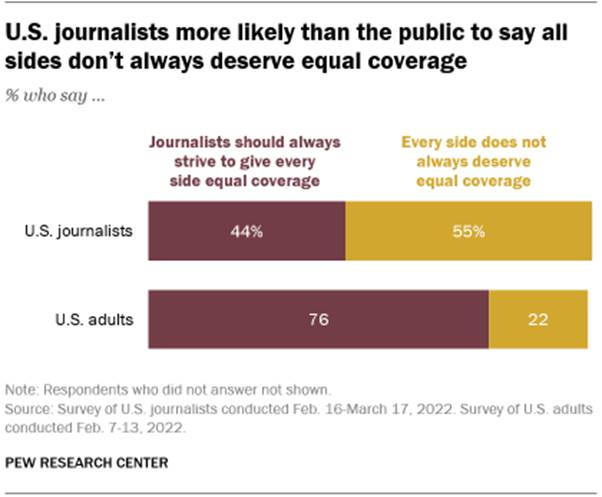

Most

Americans say journalists should always

strive to give every side equal coverage,

but journalists themselves are more likely to say every side

does not always deserve equal coverage, according to

two separate surveys conducted in late winter amid debate over “bothsidesism”

in the media.

Among Americans overall, 76% say journalists should

always strive to give all sides equal coverage, while 22% say

every side does not always deserve equal coverage. The balance

of opinion is reversed among journalists themselves: A little

more than half (55%) say every side does not always deserve

equal coverage, while 44% say journalists should always strive

to give every side equal coverage.

This issue gained new

intensity during Donald Trump’s presidency and the widespread

disinformation and competing views surrounding the 2020

election and the COVID-19 pandemic. Those who favor equal

coverage argue that it’s always necessary to allow the public to

be equally informed about multiple sides of an argument, while

those who disagree contend that people making false statements

or unsupported conjectures do not warrant as much attention as

those making factual statements with solid supporting evidence.

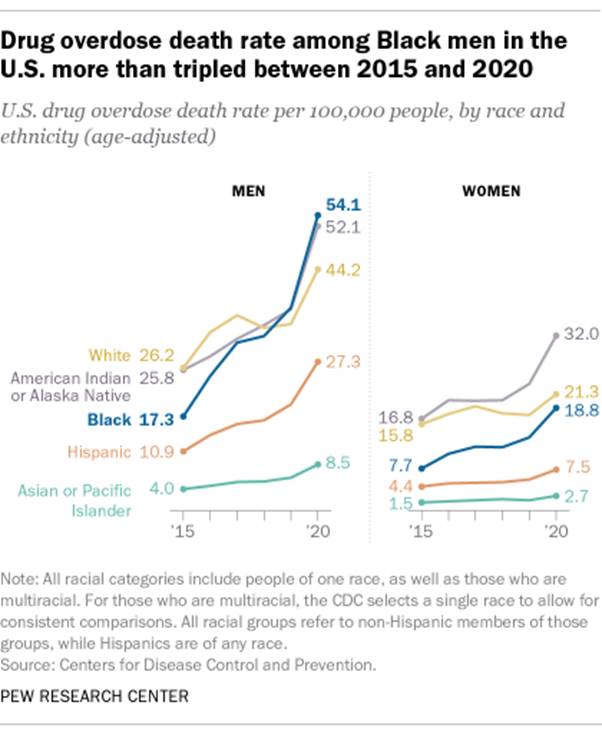

A

recent surge in U.S. drug overdose deaths has hit Black men the

hardest, a January analysis found.

While overdose

death rates have increased in every major demographic group

in recent years, no group has seen a bigger increase than Black

men. As a result, Black men have overtaken White men and are now

on par with American Indian or Alaska Native men as the

demographic groups most likely to die from overdoses.

Nearly 92,000 Americans died of drug overdoses in

2020, up from around 70,000 in 2017. During the same period,

the rate of fatal

overdoses rose from 21.7 to 28.3 per 100,000 people.

Despite these increases, the share of Americans who

say drug addiction is a major problem in their local community declined

by 7 percentage points in subsequent surveys – from 42% in

2018 to 35% in 2021. And in a separate

survey in early 2022, dealing with drug addiction ranked

lowest out of 18 priorities for the president and Congress to

address this year.

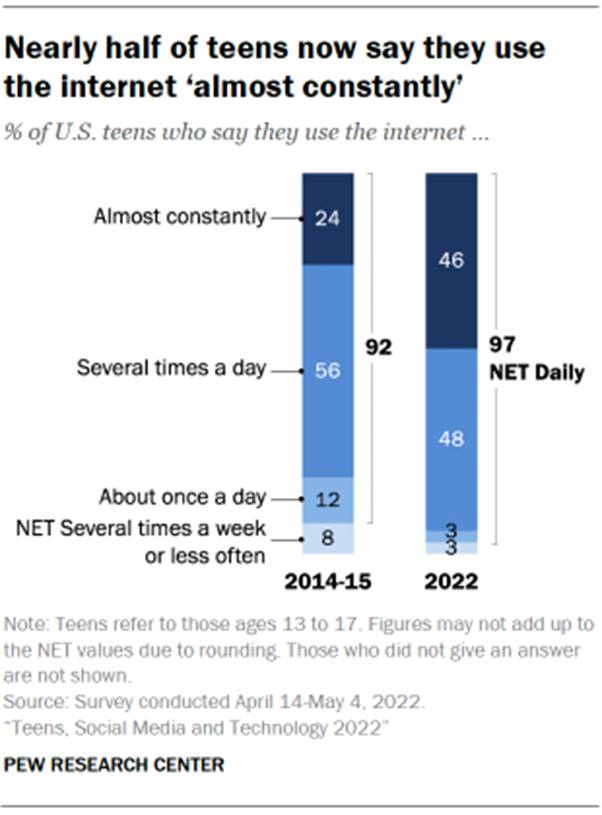

Nearly

half of U.S. teens now say they

use the internet “almost constantly,” according to a survey

conducted in April and May. This percentage has roughly doubled

since 2014-15, when 24% said they were almost constantly online.

Black and Hispanic teens stand out for being on the

internet more frequently than White teens. Some 56% of Black

teens and 55% of Hispanic teens say they are online almost

constantly, compared with 37% of White teens. (There were not

enough Asian American teens in the sample to analyze

separately.)

Older teens are also more likely to be online almost

constantly. About half of 15- to 17-year-olds (52%) say they use

the internet almost constantly, while 36% of 13- to 14-year-olds

say the same. And 53% of urban teens report doing this, compared

with somewhat smaller shares of suburban and rural teens (44%

and 43%, respectively).

Since 2014-15, there has been a 22-point rise in the

share of teens who report having access to a smartphone (from

73% then to 95% now). While teens’ access to smartphones has

increased, their access to other digital technologies, such as

desktop or laptop computers or gaming consoles, has remained

statistically unchanged.

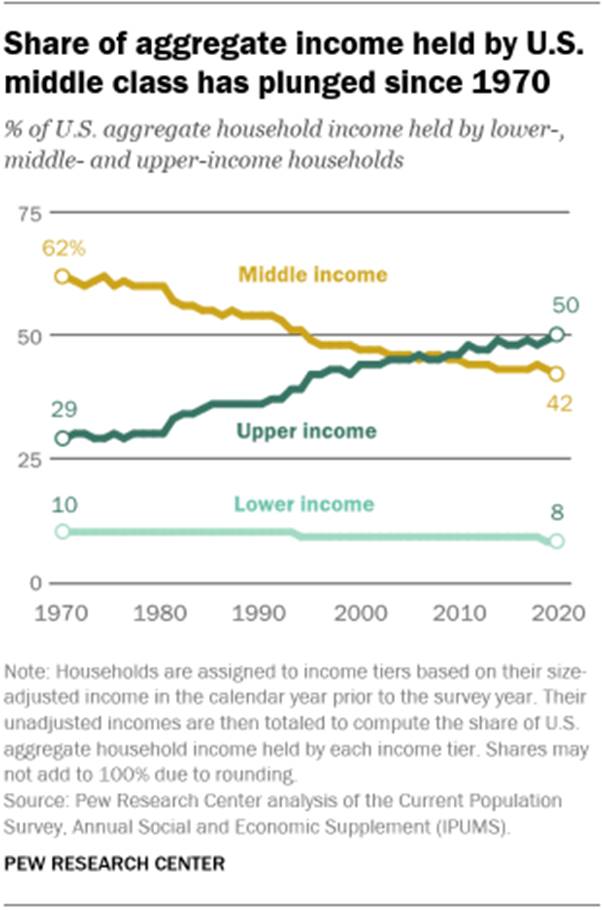

The

share of aggregate

U.S. household income held by the middle class has fallen steadily since 1970, according to an analysis

published in April.

In 1970, adults in middle-income households accounted

for 62% of aggregate income, a share that fell to 42% by 2020.

Meanwhile, the share of aggregate income held by upper-income

households has increased steadily, from 29% in 1970 to 50% in

2020. Part of this increase reflects the rising share of adults

who are in the upper-income tier; another part reflects more

rapid growth in earnings for these adults.

The share of U.S. aggregate income held by

lower-income households edged down from 10% to 8% over these

five decades, even though the proportion of adults living in

lower-income households increased over this period.

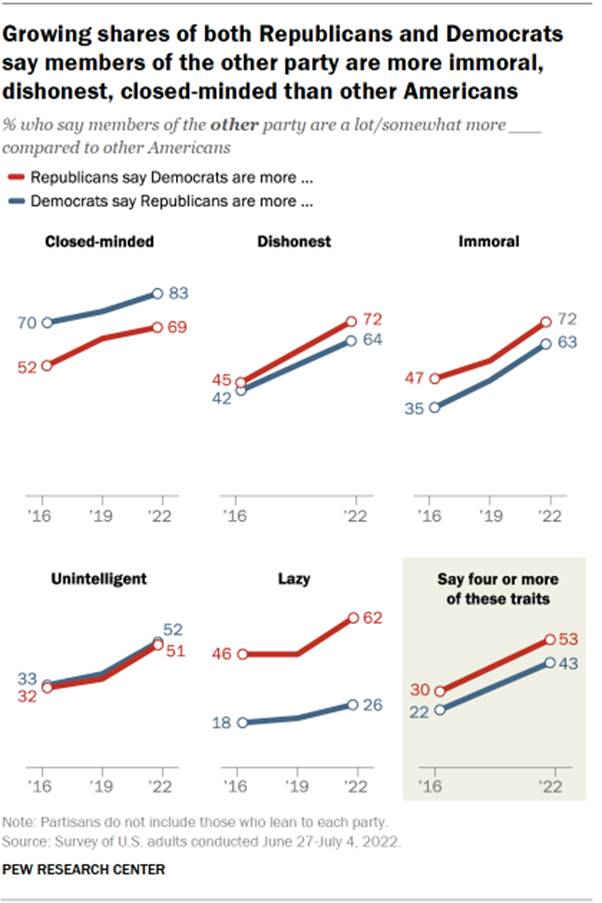

Growing

shares of both Republicans and Democrats say that members of the

other party are more immoral, dishonest and closed-minded than

other Americans, according to a survey

conducted in June and July.

The percentage of Americans

who view the people in the opposing political party in a

negative light has increased in recent years. In 2016, 47%

of Republicans and 35% of Democrats said those in the other

party were a lot or somewhat more immoral than other Americans.

Today, 72% of Republicans regard Democrats as more immoral than

other Americans, and 63% of Democrats say the same about

Republicans. Similar patterns exist when it comes to seeing

members of the other party as more dishonest, closed-minded and

unintelligent than other Americans.

There is one negative trait that Republicans are far

more likely than Democrats to link to their political opponents.

A 62% majority of Republicans say Democrats are “more lazy” than

other Americans, up from 46% in both 2019 and 2016.

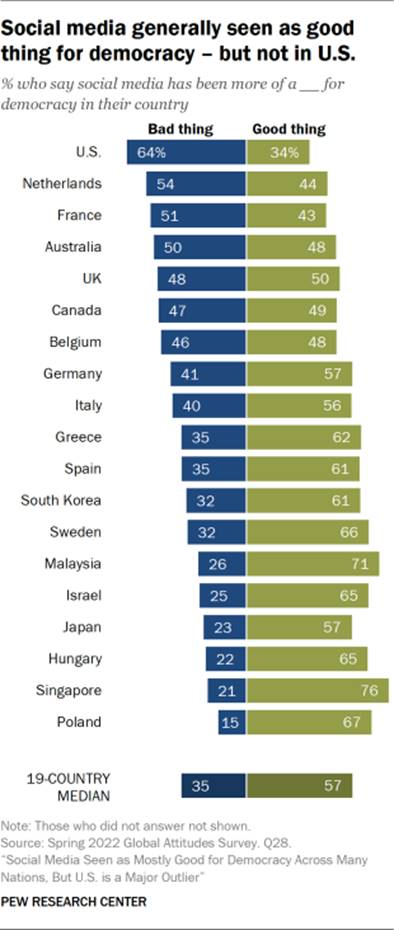

Majorities in nations around the world generally see

social media as a good thing for democracy – but not in the United States, a survey of people in 19

advanced economies found.

Americans are

the most negative about the impact of social media on democracy:

64% say it has been bad. Republicans are much more likely than

Democrats (74% vs. 57%) to see the ill effects of social

media on the political system.

In addition to being the most negative about social

media’s influence on democracy, Americans are consistently among

the most negative in their assessments of specific ways that

social media has affected politics and society. For example, 79%

in the U.S. believe access to the internet and social media has

made people more divided in their political opinions, the

highest percentage among the countries polled.

DECEMBER 13, 2022

Source:

https://www.pewresearch.org/fact-tank/2022/12/13/striking-findings-from-2022/

773-43-17/Polls

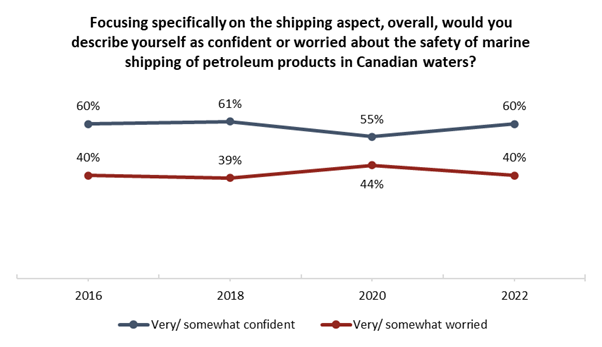

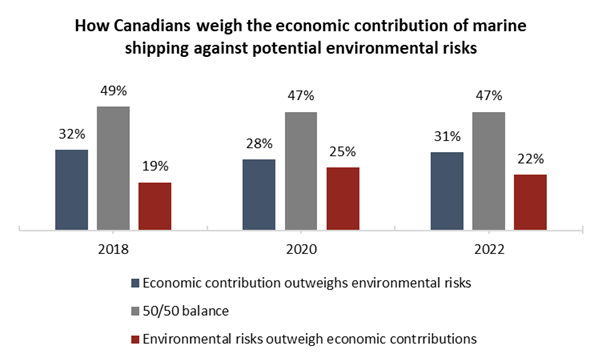

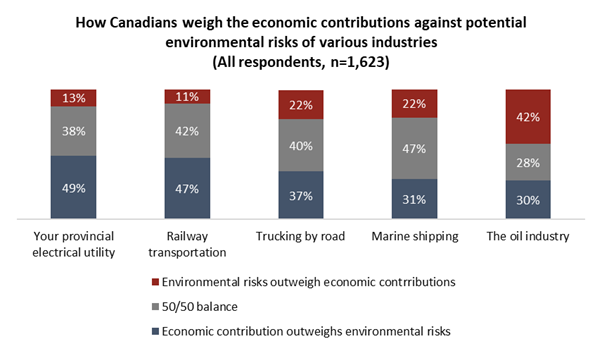

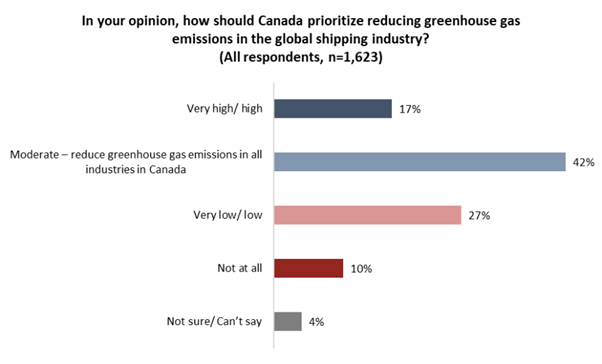

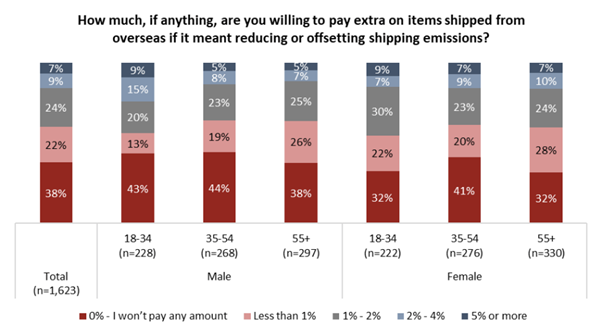

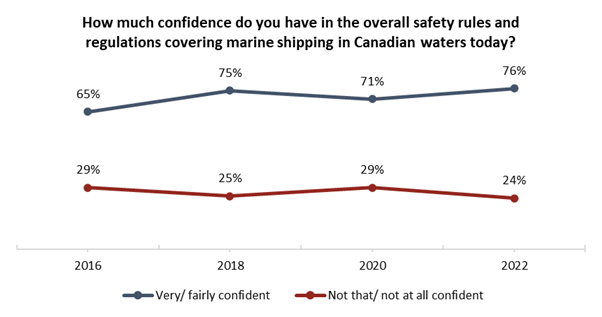

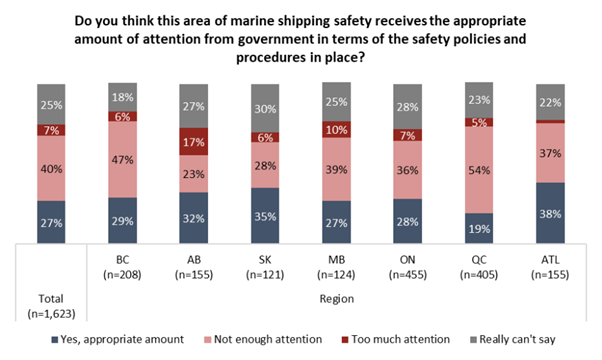

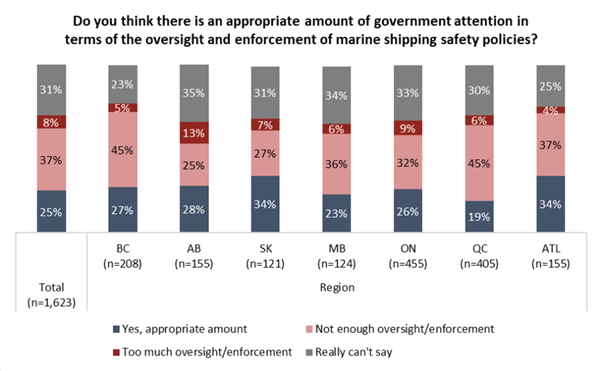

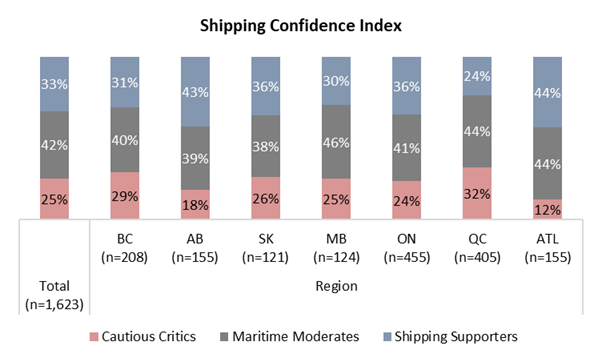

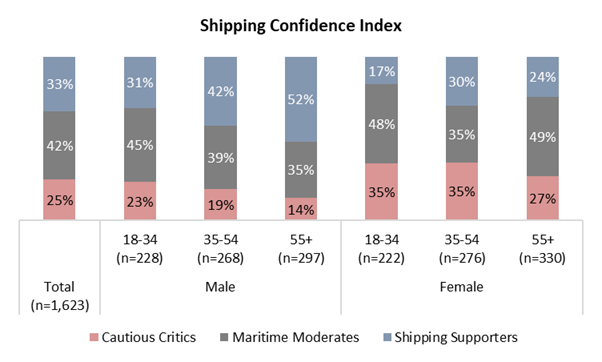

Supply Chain Crunch Provides New Perspective For

Canadians On Marine Shipping

A stubborn feature of the pandemic era has been a

relentless supply chain crunch that has affected everything from

new cars to children’s

medicine.

New data from the non-profit Angus Reid Institute, in

partnership with Clear

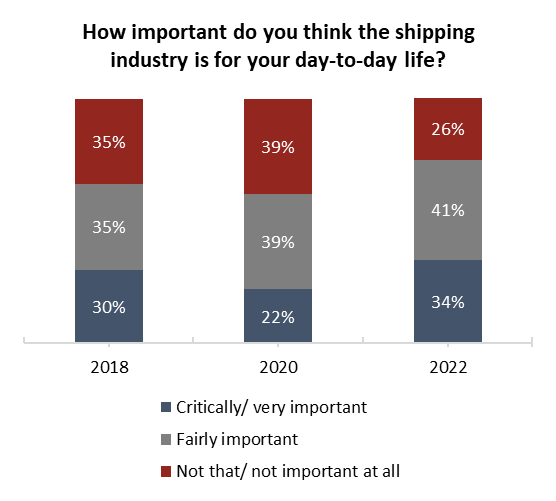

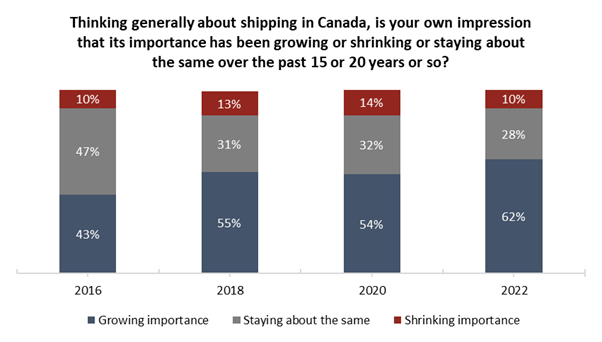

Seas Centre for Responsible Marine Shipping, finds a growing proportion of Canadians saying marine

shipping is “very” or “critically” important to their

day-to-day-life – and a shrinking proportion who believe it not

to be important at all.

Indeed, four-in-five (82%) say global issues such as

inflation, Russia’s invasion of Ukraine, and the COVID-19

pandemic have increased their awareness of how the global

network of goods works.

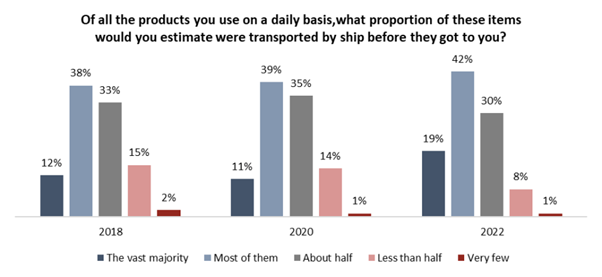

An estimated 70 to 80 per cent of items used daily by

Canadians are brought

by ship. Canadians are much more aware of this fact now than

they have been in recent years. In 2018, half of Canadians

voiced an awareness that most or the vast majority of products

they used daily were transported by ship. Now three-in-five

(61%) say the same.

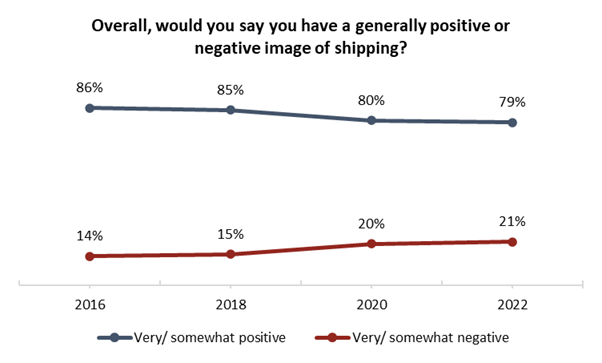

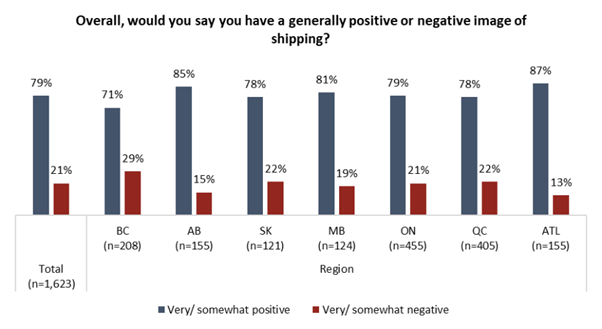

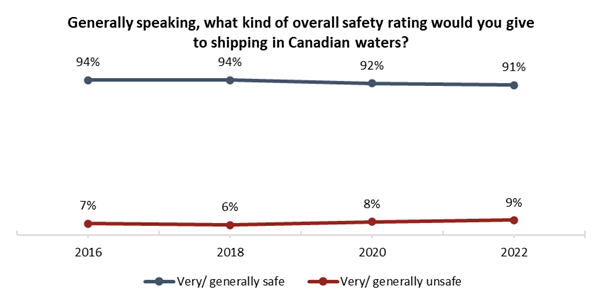

While Canadians give the shipping industry a high

mark on safety (91% believe it to be very or generally safe),

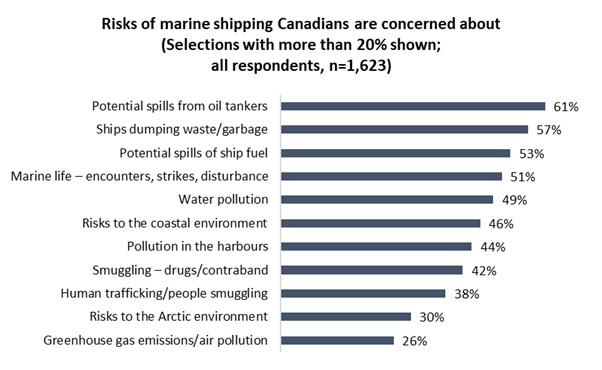

there remain common concerns about the impacts of shipping.

Three-in-five (61%) worry about potential spills from oil

tankers. A similar number (57%) fear the risk of ships dumping

garbage. Half (53%) say the prospect of ships spilling their own

fuel is a concern.

Although the potential for spills from tankers is the

top risk for Canadians, overall residents are more confident

than not when it comes to the shipping of petroleum products in

general (60% confidence) and liquefied natural gas (LNG) more

specifically (67% confidence).

More

Key Findings:

About

ARI

The Angus

Reid Institute (ARI) was founded in October 2014 by

pollster and sociologist, Dr. Angus Reid. ARI is a national,

not-for-profit, non-partisan public opinion research foundation

established to advance education by commissioning, conducting,

and disseminating to the public accessible and impartial

statistical data, research and policy analysis on economics,

political science, philanthropy, public administration, domestic

and international affairs and other socio-economic issues of

importance to Canada and its world.

About

Clear Seas

Clear