|

BUSINESS

& POLITICS IN THE WORLD GLOBAL

OPINION REPORT NO.759-760 Week: September 05 –September

18, 2022 Presentation: September 23,

2022 759-760-43-41/Commentary:

Americans Consume Violent Video Games More Often Than Germans Military

Reserves, Civil Defense Worry Taiwan As China Looms More

Than Half (55%) Japanese, Said They Support Hosting The Winter Games 7

Out Of Every 10 Turkish People Have A Credit Card 3

In 5 People In Karachi Do Not Read Newspaper Six

In 10 (59%) Ugandans Say The Government Is Doing A Poor Job Of Addressing

Climate Change Mauritians

Embrace Covid-19 Vaccination Despite Low Levels Of Trust In Vaccine Safety By

50% to 22% Britons are disappointed that Liz Truss will be the next PM 7

In 10 Britons Agree That The UK Is In Decline Londoners

Support Decriminalization Of Cannabis By 50% To 33% Three

Quarters Of Britons (76%) Say They Were Upset At The Passing Of Queen

Elizabeth II Three

In Five Britons Expect Charles III To Be A Good King For

The First Time, Britons Are More Likely To Think Ukraine Is Winning The War

Than Russia Overall

Consumer Confidence Is Negative For The First Time Since May 2020 Over

Two Thirds (70%) Of Irish Voters Are Struggling To Make Ends Meet 57%

Of French People Say They Have Already Experienced A Situation Of Poverty 6

Out Of 10 French People Now Consider That An Electric Vehicle Would Be

Adapted To Their Travels 68%

Of Children Would Like Their Ideal Parent To Have A Job That Allows Them To

Have Time For Family Russians

Began To Save More On Expensive Purchases And Less On Food Partisan

Differences Are Common In The Lessons Americans Take Away From Covid-19 Six-In-Ten

Adults Say A Pathway To Legal Status For Immigrants Should

Be An Important Goal Modeling

The Future Of Religion In America Poilievre

Running Away As Clear Favourite Among Conservative Party Supporters Canadians

Conflicted On Future Role Of Monarchy As Half (54%) Say Canada Should End

Ties To Monarchy Australian

Unemployment Increases To 9.2% In August As Workforce Swells To 14.8 Million

Australians ANZ-Roy

Morgan Consumer Confidence Up By 1.1pts To 86.1 – Highest For Three Months Since

Early June An

Increasing Majority Of Australians, 60% Believe Australia Should Remain A

Monarchy Americans

Consume Violent Video Games More Often Than Germans Citizens

Lukewarm On Leaders’ Cold War, Survey Across 9 Middle East And North African

Countries Majority

Across 34 Countries Describe Effects Of Climate Change In Their Community As

Severe Ninety-Seven

Percent Of People Globally Want To Take Action On Sustainability, In 32

Countries International

Views Of The UN In 16 Surveyed Nations Are Mostly Positive 62%

Of Finns And 40% Of Swedes Approve Of U S Leadership INTRODUCTORY NOTE

759-760-43-41/Commentary:

Americans

Consume Violent Video Games More Often Than Germans

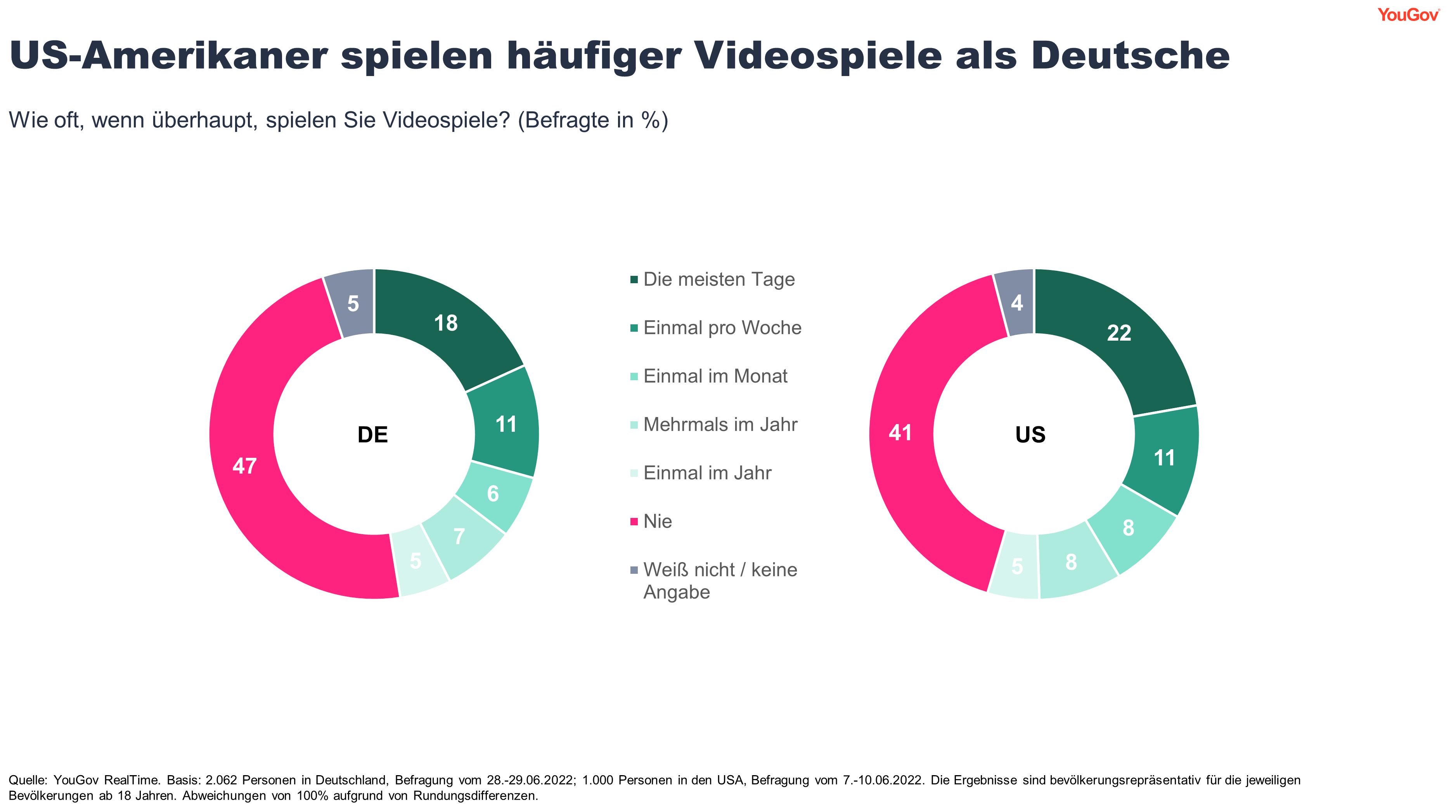

Almost one in five Germans (18 percent) plays video

games most days of the week. In the U.S., this is said a little more, 22

percent. That they never play video games, say 47 percent in Germany, in the

USA 41 percent. The data therefore show that Americans are more likely to

play video games than Germans. On September 12, the U.S. celebrates its

annual National Video Games Day. On the occasion of this, YouGov conducted

surveys on the subject of video games in Germany as well as in the USA and

LINK in Switzerland and compared the results with each other.

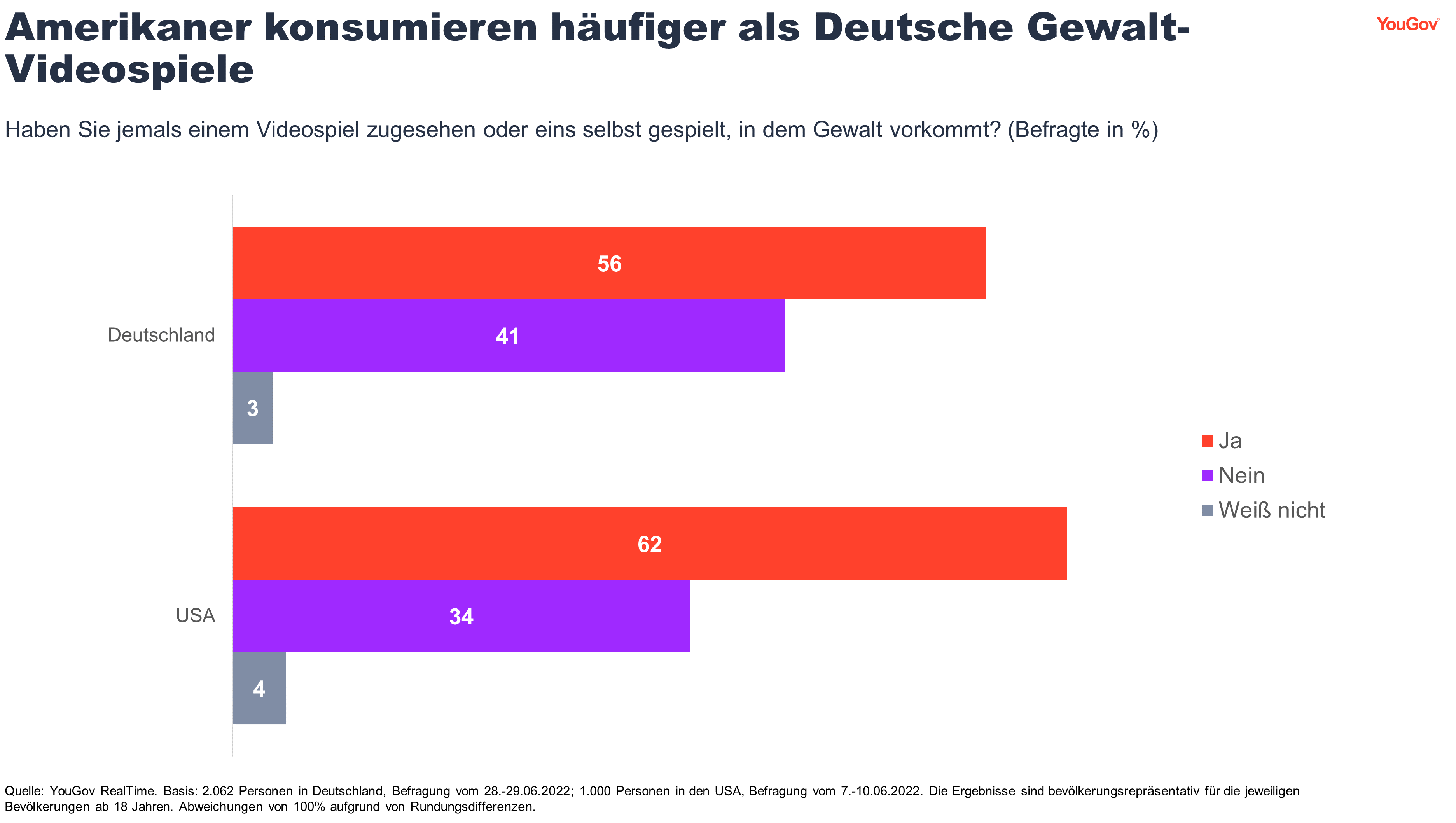

Americans consume violent

video games more often than Germans In the US, three out of five respondents who play

video games at least once in a while say they have watched or played a video

game in which violence occurs (62 percent). In Germany, 56 percent of those

who play at least once in a while say so.

In Deutschland sind es besonders die 18- bis

24-Jährigen, die nach eigenen Angaben schon einmal ein gewaltbeinhaltendes

Videospiel konsumiert haben (80 Prozent vs. 33 Prozent der Befragten ab 55

Jahren). Außerdem treffen Männer diese Aussage häufiger als Frauen (67

Prozent vs. 42 Prozent unter Frauen). Für Schweizer sind

Videospiele am ehesten Ursache für Gewalt Die Befragten aller drei Länder wurden außerdem

gebeten, verschiedene Aussagen zu Videospielen und ihren Effekten zu

bewerten. Am häufigsten sind Befragte in der Schweiz der Meinung (61

Prozent), dass Videospiele Ursache für Gewalt und Aggressionen in der realen

Welt sein können. In Deutschland sagen dies 57 Prozent. In den USA trifft nur

noch knapp jeder Zweite diese Aussage (48 Prozent). Amerikaner stimmen hingegen am häufigsten zu, dass

Videospiele hingegen ein nützliches Ventil für Frustrationen und Aggressionen

sein können (57 Prozent). In der Schweiz sagen dies 49 Prozent der Befragten,

in Deutschland nur knapp weniger, 46 Prozent.

These are the results of current YouGov surveys, for

which 2,062 people in Germany were surveyed between 27 and 29 June 2022 and

1,000 people in the USA between 7 and 10 June 2022. The results are

representative of the respective populations aged 18 and over. From 13 to 19

July 2022, link surveyed 1,208 language-assimilated people aged 15–79 living

in german, French and Italian-speaking Switzerland. The sample was quoted and

weighted representatively by age, gender and region. (YouGov Germany) September 9, 2022 Source: https://yougov.de/news/2022/09/09/amerikaner-haufiger-als-deutsche-zeugen-oder-spiel/ ASIA (Taiwan) Military Reserves, Civil

Defense Worry Taiwan As China Looms About 73 percent of

Taiwanese say they would be willing to fight for Taiwan if China were to

invade, according to surveys by Kuan-chen Lee at the Defense

Ministry-affiliated Institute for National Defense and Security Research, a

number that has remained consistent. Taiwan’s reserves are meant to back up

its 188,000-person military, which is 90 percent volunteers and 10 percent

men doing their four months of compulsory military service. On paper,

the 2.3 million reservists enable Taiwan to match China’s 2 million-strong

military. (Asahi Shimbun) September 5, 2022 (Japan) More Than Half (55%) Japanese,

Said They Support Hosting The Winter Games A majority of respondents

to a new nationwide survey support holding the 2030 Winter Olympics and

Paralympics in Sapporo. More than half, or 55 percent, said they support

hosting the Winter Games while 38 percent replied that they don’t, in the

survey conducted by The Asahi Shimbun on Sept. 10 and 11. In addition,

about 70 percent of all the respondents in their 30s or younger support

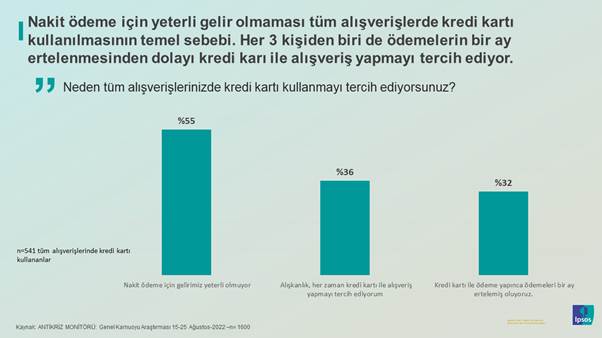

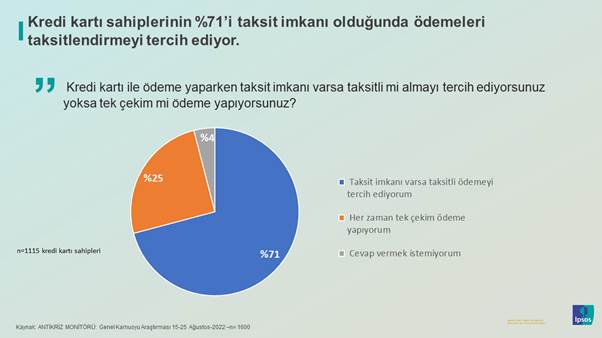

holding the 2030 Games in Sapporo. (Asahi Shimbun) September 13, 2022 (Turkey) 7 Out Of Every 10 Turkish

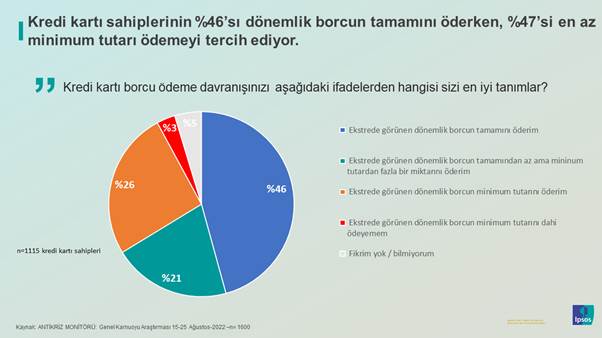

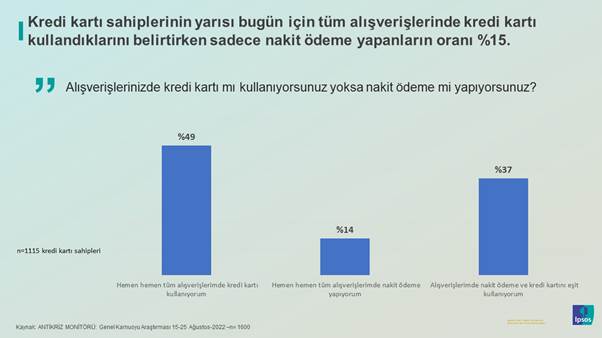

People Have A Credit Card 61% of individuals have

their own credit card. 9% have an additional card they are using. In total,

the rate of individuals using credit cards is 70%. While the rate of

cardholders who say they pay the full amount of their periodic card debt is

46%, 21% say that they deposit a little less of the periodic debt. The rate

of those who pay the minimum amount is 26%.9 out of every 10 people use

credit profit on their purchases. The rate of individuals who use credit

cards in almost all purchases is 49%. (Ipsos Turkey) 7 September 2022 (Pakistan) 3 In 5 People In Karachi Do Not

Read Newspaper A representative sample of

adult men and women from Karachi was asked the following question, “Do you

read the newspaper?” In response to this question, 34% said ‘Yes’ while 66%

said ‘No.’ The number of people who said ‘Yes’ increased as the level of

education increased amongst the respondents with 67% Professionals/Doctors

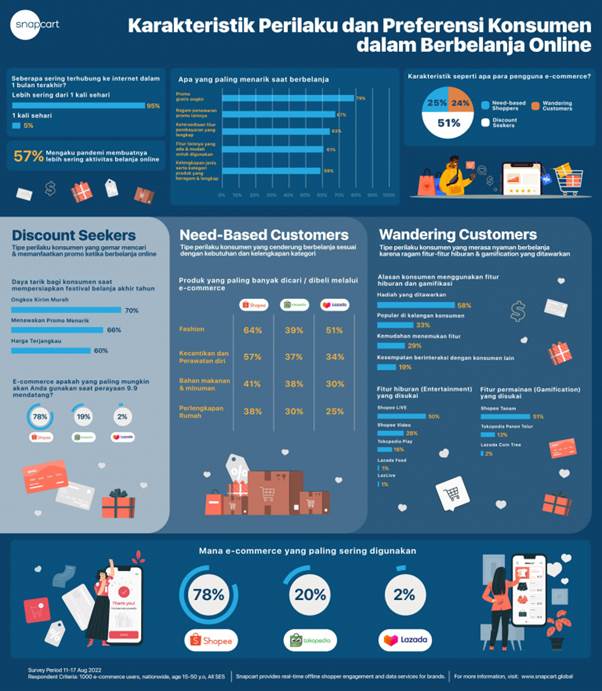

answering ‘Yes’ compared to only 18% of illiterate people. (Gallup Pakistan) September 14, 2022 (Indonesia) Consumer Behavior

Characteristics And Preferences In Online Shopping; 78% Of Indonesian

Consumers Choose Shopee Online shopping trends are increasingly in

demand and growing, especially after the presence of the pandemic. Snapcart

conducted consumer research to find out more about 'Consumer Behavior

Characteristics and Preferences in Online

Shopping' for the past 3 months. This research was conducted

using an online method

which was attended by 1000 respondents from the age of 20–35 years, spread

across various regions in Indonesia. Among the 3 main players, data shows

that Shopee has been successfully selected as the most frequently used e-commerce platform. Where 78% of

consumers currently choose Shopee, followed by Tokopedia (20%) and Lazada

(2%). (Snapcart) September 8, 2022 AFRICA (Nigeria) More Than 7 In 10 Adult

Nigerians Are Not Registered To Any Political Party Ahead Of The 2023 General

Elections A new public opinion poll

conducted by NOIPolls has revealed that 74 percent of adult Nigerians

interviewed disclosed that they are not registered to any political party in

the country. This assertion cuts across gender, geographical locations, and

age-group. On the flipside, 20 percent of adult Nigerians admitted that they

are registered members of different political parties, and have membership

cards whereas, 6 percent are registered members but do not have a membership

card. (NOI Polls) September 6, 2022 (Uganda) Six In 10 (59%) Ugandans Say

The Government Is Doing A Poor Job Of Addressing Climate Change Almost six in 10 Ugandans

(57%) say droughts have become more severe over the past 10 years; only half

as many (28%) say the same about floods. More than half (56%) of Ugandans

have heard of climate change. Among those who are aware of climate change:

More than eight in 10 (84%) say it is making life in Uganda worse. More than

three-fourths (78%) believe that ordinary citizens can help curb climate

change (71%). Eight in 10 (80%) want the government to take immediate action

to limit climate change, even if it is expensive, causes job losses, or takes

a toll on the economy. (Afrobarometer) 6 September 2022 (Mauritius) Mauritians Embrace Covid-19

Vaccination Despite Low Levels Of Trust In Vaccine Safety Effects of the COVID-19

pandemic: o More than half (53%) of Mauritians say they or a member of their

household became ill with COVID-19 or tested positive for the virus. About

one-fourth (27%) say someone in their household lost a job, business, or

primary source of income due to the pandemic. Attitudes toward vaccines: o

More than nine in 10 Mauritians (95%) say they have been vaccinated against

COVID-19. Among those who have not been vaccinated, almost two-thirds say

they are “very unlikely” (41%) or “somewhat unlikely” (23%) to try to get

vaccinated. (Afrobarometer) 13 September 2022 WEST EUROPE (UK) By 50% to 22% Britons are

disappointed that Liz Truss will be the next PM Asked in the immediate

aftermath of the result, 50% of Britons say they are disappointed that she is

to be the next prime minister, including a third (33%) who are ‘very

disappointed’. This is considerably more than the 22% who say they are very

or fairly pleased. Four in ten Conservative voters (41%) say they are

pleased with Liz Truss’s impending promotion, but a third (34%) report being

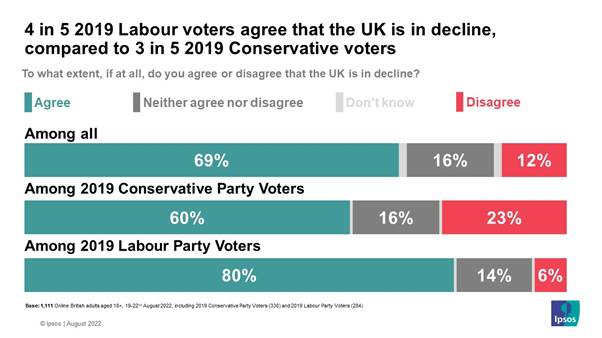

disappointed. (YouGov UK) September 05, 2022 7 In 10 Britons Agree That The

UK Is In Decline New research by Ipsos,

taken 19th-22nd August, shows 7 in 10 Britons agree that the UK is currently

in decline (69%) while only around 1 in 10 (12%) disagree. This

reflects a similar sentiment found in December 2020 where almost 2 in 3

Britons aged 18-75 said the same (65%). Those who voted Labour in the 2019

General Election are significantly more likely to believe the UK is in

decline than those who voted Conservative: 80% vs. 60% respectively.

Similarly, 82% of those who voted Remain in the 2016 EU Referendum believe

the country is in decline while 64% of those who voted Leave say the

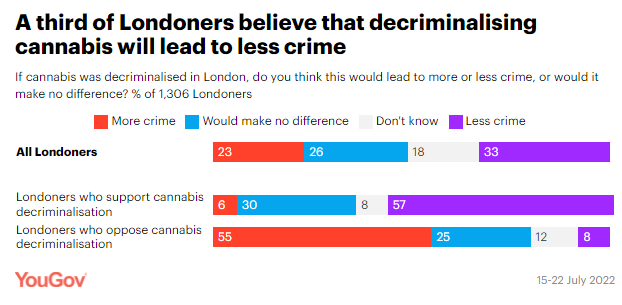

same. (Ipsos MORI) 7 September 2022 Londoners Support Decriminalization Of Cannabis

By 50% To 33% New YouGov data finds that

Londoners support decriminalising cannabis within the boundaries of the

capital by 50% to 33%. However opinion is divided across party lines, with

64% of the capital’s Labour voters supporting such a move compared to only

34% of Conservative voters. Younger Londoners are also notably more likely to

support a change in the law, with 52% of 18-24s and 56% of 25–49-year-olds

supporting decriminalisation, versus 45% of 50-64 year olds and 34% of those

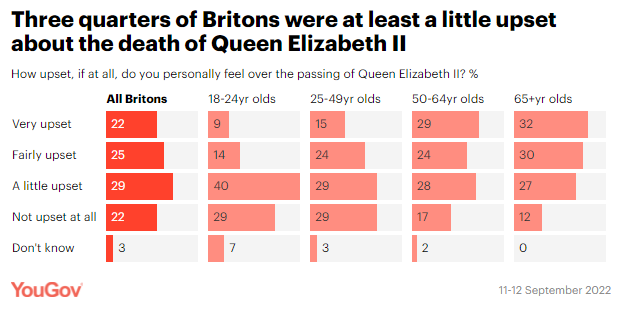

aged 65 and over. (YouGov UK) September 07, 2022 Three Quarters Of Britons (76%)

Say They Were Upset At The Passing Of Queen Elizabeth II With Queen Elizabeth II

passing away on Thursday at the age of 96, after 70 years on the throne, a

new YouGov/Times survey takes the first look at how it has affected Britons,

and how they rate her reign now that it has come to an end. Three quarters of

Britons (76%) say they were upset at the passing of Queen Elizabeth II,

including half who said they were “very” (22%) or “fairly” (25%) upset. One

in five (22%) say they weren’t upset at all. A separate YouGov survey found that 44% of Britons say they

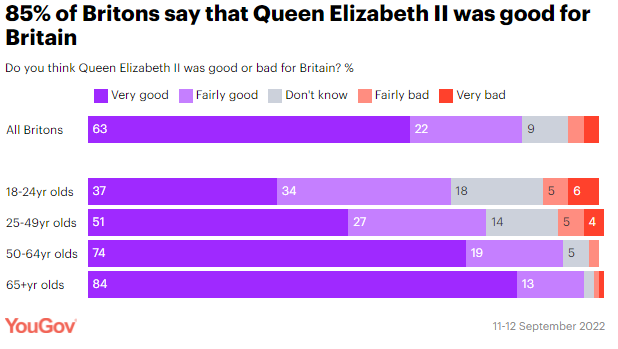

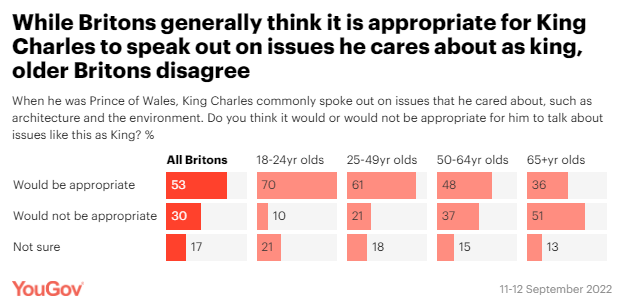

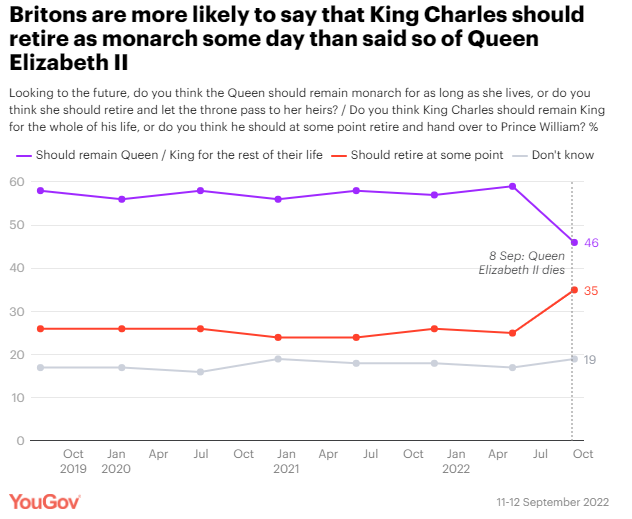

cried, became teary or welled up at the news Her Majesty had died. (YouGov UK) September 13, 2022 Three In Five Britons Expect Charles III To Be A

Good King Asked how they anticipate

his reign, 63% say they think Charles will do a good job as king, with only

15% thinking he will do a bad one. This is a marked improvement for the new

monarch: in a survey in May Britons were split 32% to 32% on

whether or not the-then Prince Charles would make a good king. One of King

Charles’s first acts as monarch was to address the nation about the passing

of his mother. Three in five Britons say they saw or heard the King’s speech,

with almost universal approval – 94% of those say it was a good speech. (YouGov UK) September 13, 2022 For The First Time, Britons Are

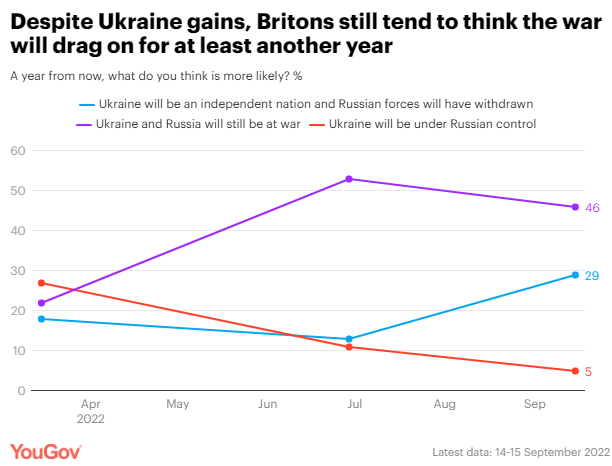

More Likely To Think Ukraine Is Winning The War Than Russia In recent days Ukrainian

forces have made significant gains in retaking large areas in

the east of the country from Russian forces. Although British headlines

have been dominated by the death of Queen Elizabeth II, it appears that this

news from Ukraine has cut through: new YouGov political data tracking Britons’ response to

the war in Ukraine, has seen a significant shift in opinion when it comes to

who is ‘winning’. For the first time since the conflict began in February,

Britons are more likely to think that Ukraine has the advantage (31%) than

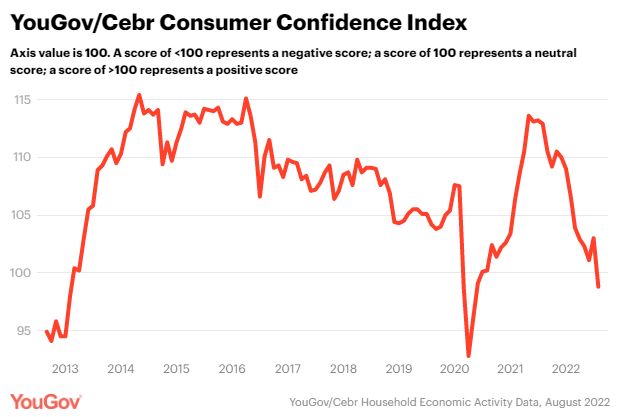

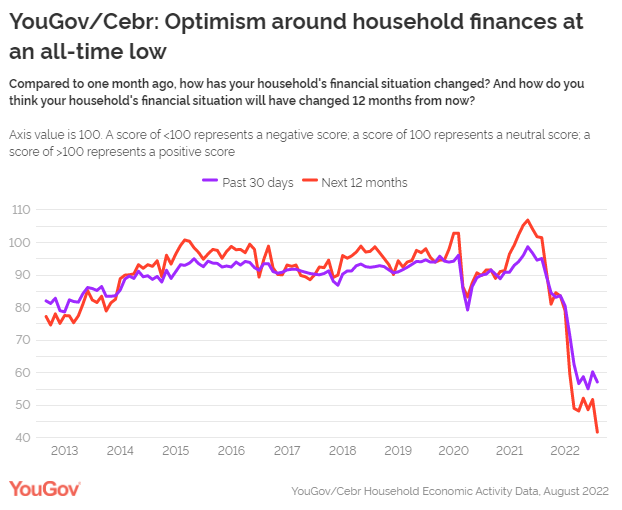

Russia (14%). (YouGov UK) September 16, 2022 Overall Consumer Confidence Is

Negative For The First Time Since May 2020 August saw confidence

among UK consumers become negative for the first time since June 2020,

according to new analysis from YouGov and the Centre for Economics and

Business Research (Cebr). With UK energy bills set to continue increasing and

inflation rising all over the world, the overall index fell by 4.2 points in

August: the largest decline since the early stages of the COVID-19 pandemic. (YouGov UK) September 16, 2022 (Ireland) Over Two Thirds (70%) Of Irish Voters Are

Struggling To Make Ends Meet The importance of the

rising cost of living to voters, and how it is dealt with by the government,

is laid bare in today’s poll. Over two thirds (70%) of all voters now suggest

they are struggling to make ends meet. This is before we move into

winter with the associated higher impact of increased energy costs, and

before increased interest rates have delivered further hikes in repayments

for those on variable rates. (RedC) September 12, 2022 (France) 57% Of French People Say They

Have Already Experienced A Situation Of Poverty Today, poverty is not a

distant dimension but a reality observed by a majority of French

people. 65% of them know at least one person facing poverty in their

family or friendly environment, an increase of 10 points in one year. 57% of

French people even say they have already experienced a situation of poverty

at some point in their lives and 85% fear that future generations will have

to live more situations of poverty than themselves, a record level. The

French are therefore fully aware of this reality and are openly worried about

it. (Ipsos France) September 7, 2022 Out Of 10 French People Now

Consider That An Electric Vehicle Would Be Adapted To Their Travels 6 out of 10 French people

now consider that an electric vehicle would be adapted to their travels. More

than half of French people (53%) project themselves behind the wheel of an

electric vehicle within 5 years. 91% of electric vehicle drivers say they are

satisfied with their choice. In the current context of inflation and rising

fuel prices, and while sales of new electric vehicles have increased by 30%*

over the first 8 months of 2022, the electric car is increasingly emerging as

a relevant solution for the French. (Ipsos France) September 16, 2022 (Italy) 68% Of Children Would Like

Their Ideal Parent To Have A Job That Allows Them To Have Time For Family 55% of the 8-14 year olds

surveyed say that patience/tolerance are absolutely the main traits that

the ideal parent should have. This is followed by positivity/sense of humor

(48%), generosity (26%), courage and kindness (both 25%). Even for

parents, patience/tolerance are essential characteristics for the ideal

parent (49%) as well as positivity and a sense of humor (41%). The

subsequent qualities, however, do not coincide with those indicated by the

boys. They are education/good manners (32%), self-confidence and

determination (31%). (BVA Doxa) September 09, 2022 (Romir) Russians Began To Save More On

Expensive Purchases And Less On Food In the 34th week, the

number of Russians who save on food and essential goods decreased (18% - 34

weeks vs 26% - 33 weeks). Among those who do overcome economic difficulties

by reducing spending on food and essential goods, 62% switched to goods at

discounts and promotions. The most popular way to overcome economic

difficulties in the period from 22 to 28 August was to abandon expensive

purchases and durable goods. From second place the previous week, this

pattern moved to first place. The share of Russians saving on expensive

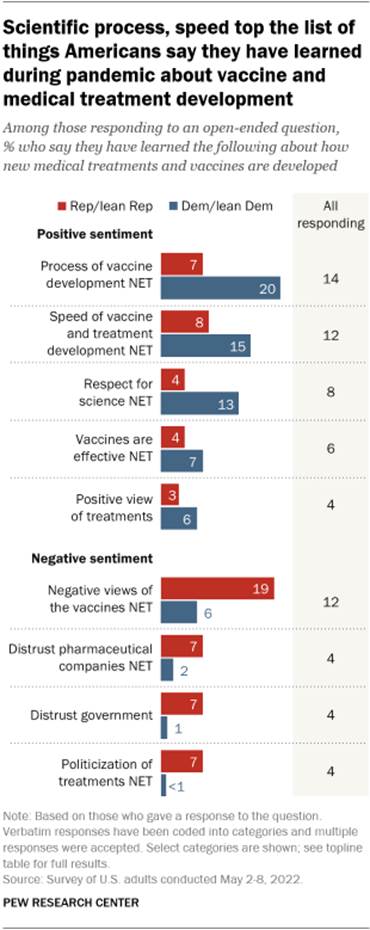

purchases increased from 45% to 56%. (Romir) September 05, 2022 NORTH AMERICA (USA) Partisan Differences Are Common In The Lessons

Americans Take Away From Covid-19 A recent Pew Research

Center survey asked U.S. adults to say, in their own words, what they have

learned from the COVID-19 pandemic. One set of respondents were asked what

they learned about the development of vaccines and medical treatments, while

another set were asked what they think the country should learn to be better

prepared for a future outbreak of disease. Nearly as many – 12% of those who

responded – mentioned the speed of vaccine development. As one respondent put

it: “I learned that vaccine development can be expedited much more than I

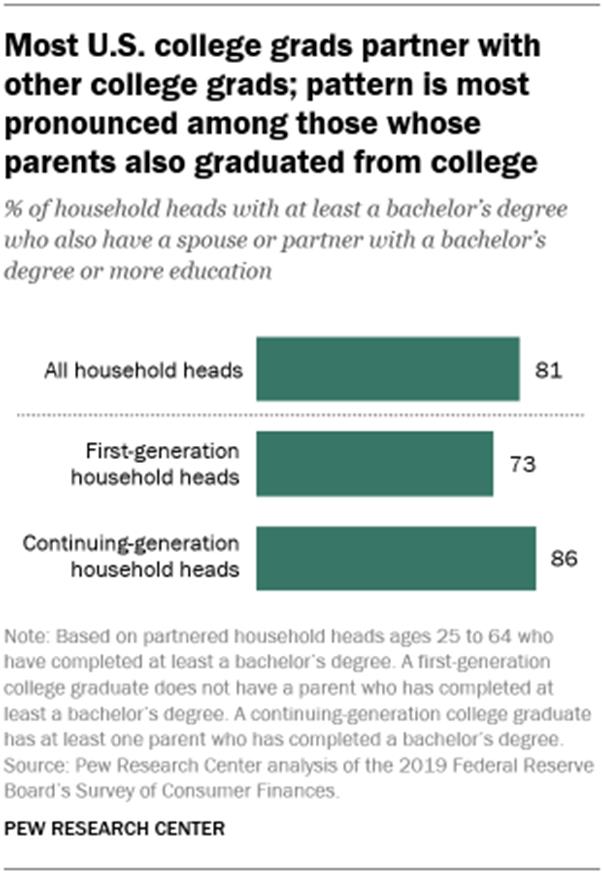

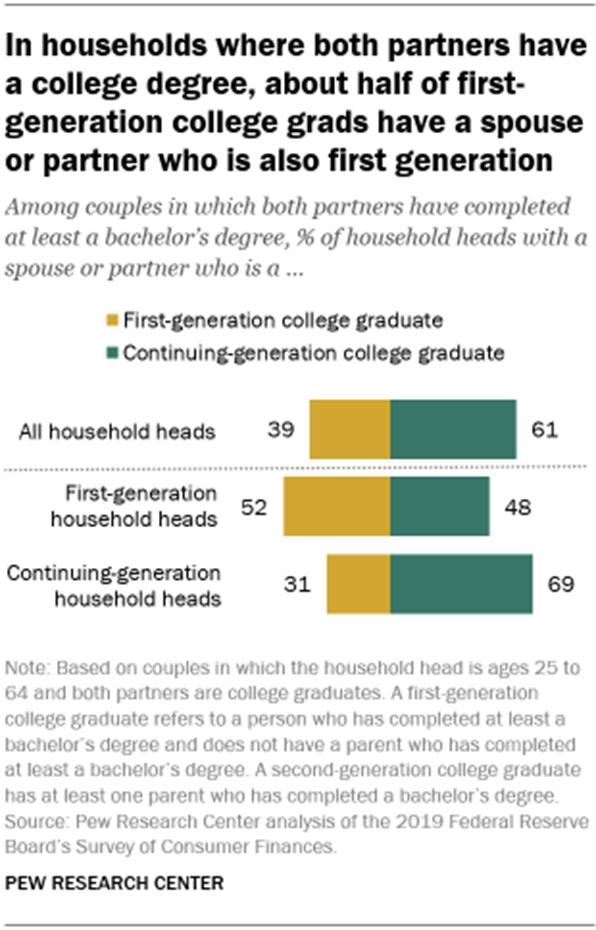

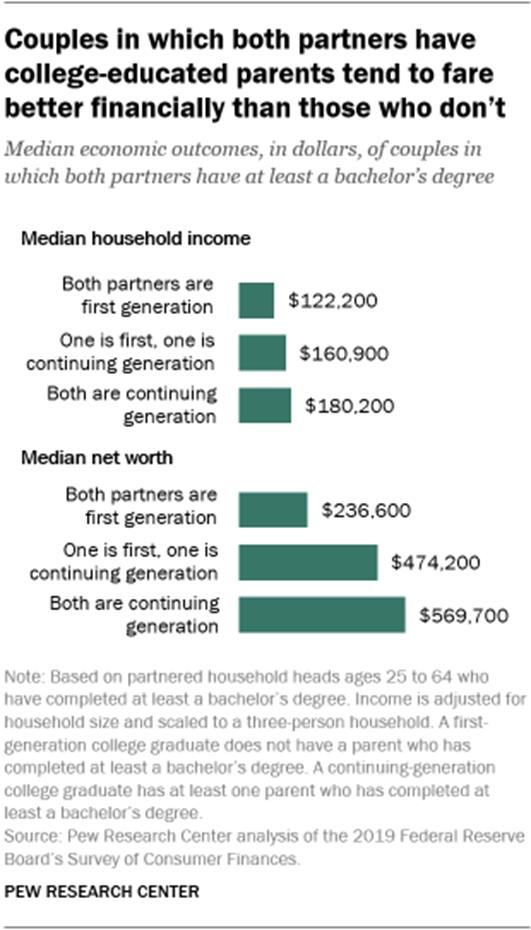

previously thought.” (PEW) SEPTEMBER 6, 2022 College Grads In U S Tend To Partner With Each

Other – Especially If Their Parents Also Graduated From College A new Pew Research Center analysis

of government data shows that this pattern is even more pronounced for adults

whose parents also graduated from college. Some 86% of household heads with a

four-year college degree – and at least one parent with a degree – have a

spouse or partner who is also a college graduate. By comparison, the same is

true for a smaller share of household heads who are first-generation college

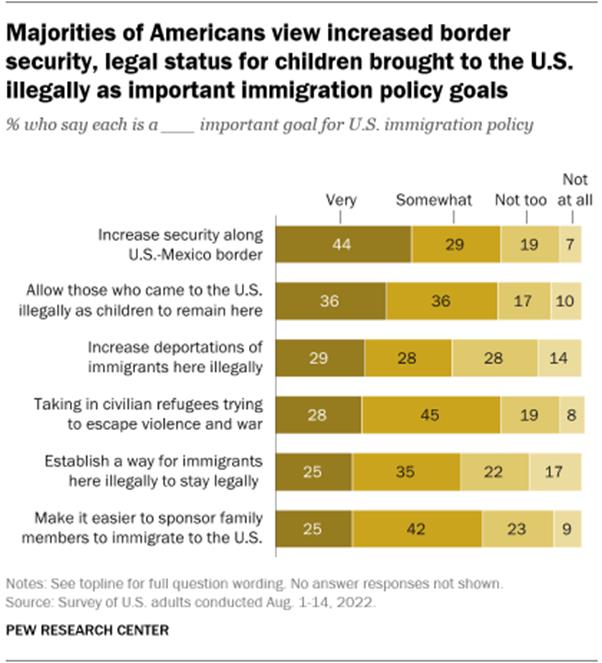

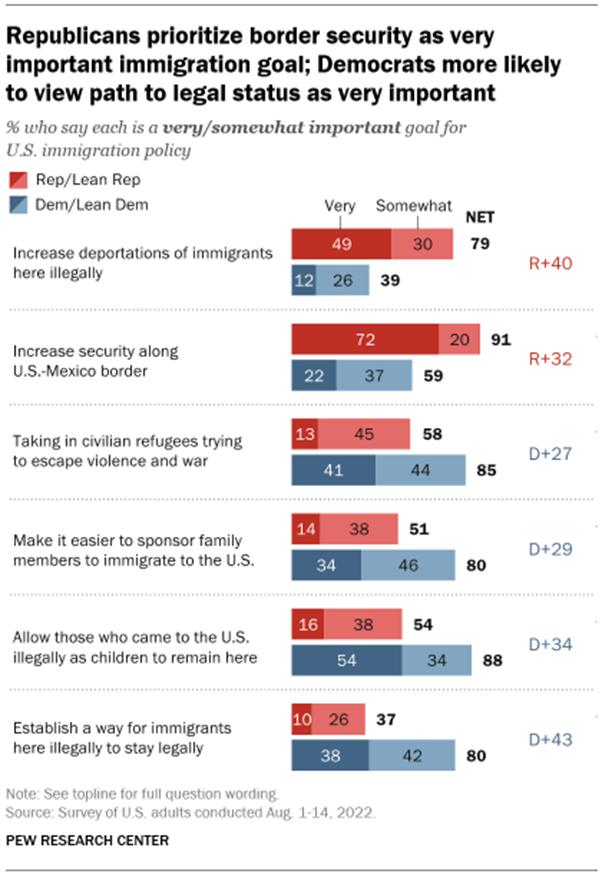

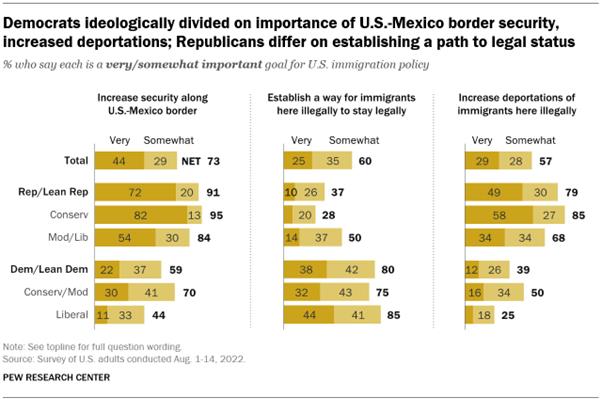

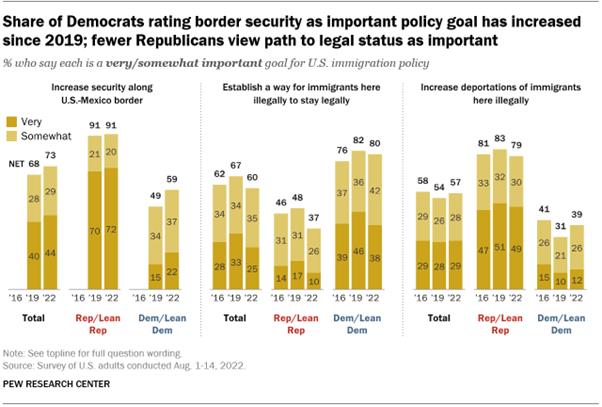

graduates (73%). (PEW) SEPTEMBER 7, 2022 Six-In-Ten Adults Say A Pathway To Legal Status

For Immigrants Should Be An Important Goal As the number of

people apprehended for illegally crossing the

southern border has

reached record annual levels, about three-quarters of Americans (73%) say

increasing security along the U.S.-Mexico border to reduce illegal crossings

should be a very (44%) or somewhat (29%) important goal of U.S. immigration

policy. Nearly all Republicans and Republican-leaning independents (91%) say

border security should be an important goal, while a smaller majority of

Democrats and Democratic leaners (59%) say the same, according to the survey

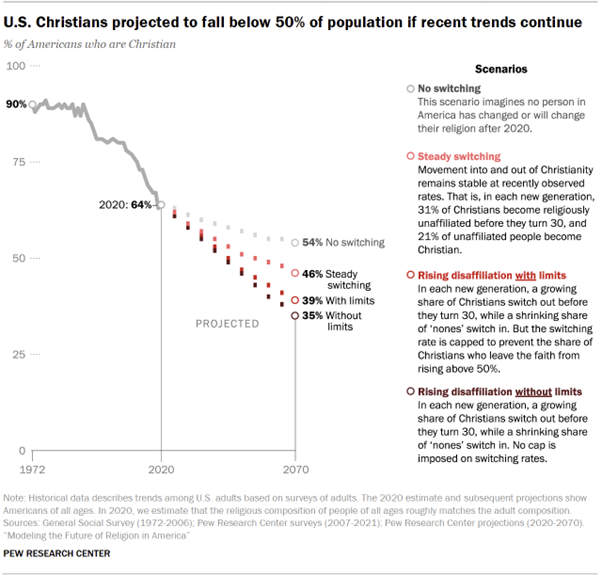

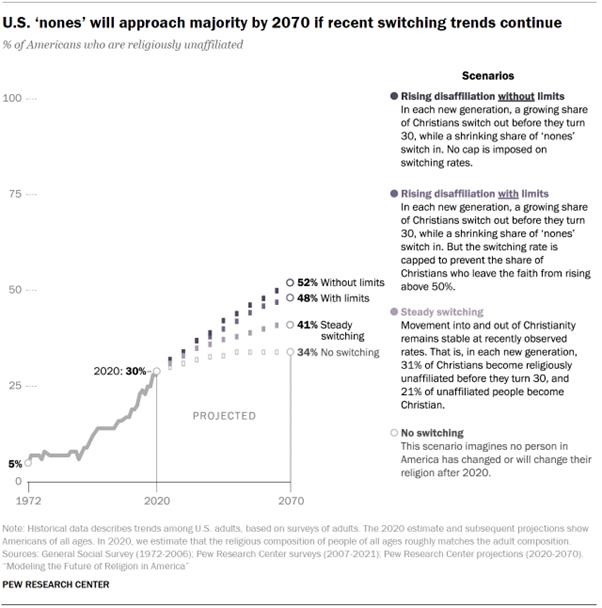

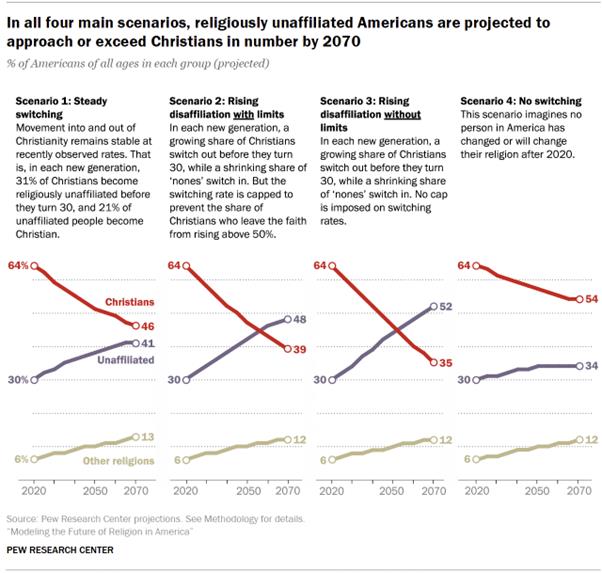

of 7,647 U.S. adults conducted Aug. 1 to 14. (PEW) SEPTEMBER 8, 2022 Modeling The Future Of Religion In America Since the 1990s, large

numbers of Americans have left Christianity to join the growing ranks of U.S.

adults who describe their religious identity as atheist, agnostic or “nothing

in particular.” This accelerating trend is reshaping the U.S. religious

landscape, leading many people to wonder what the future of religion in

America might look like. The Center estimates that in 2020, about 64% of

Americans, including children, were Christian. People who are religiously

unaffiliated, sometimes called religious “nones,” accounted for 30% of the

U.S. population. Adherents of all other religions – including Jews, Muslims,

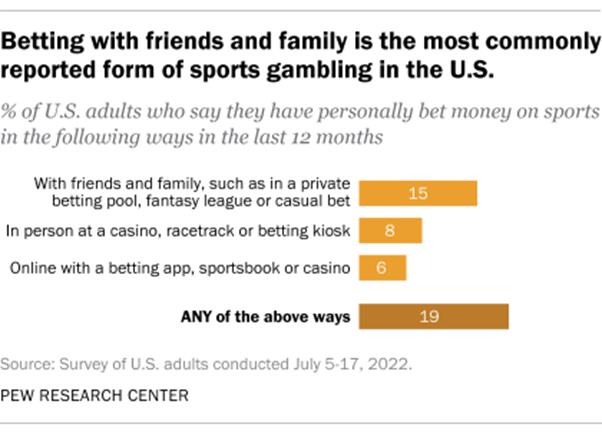

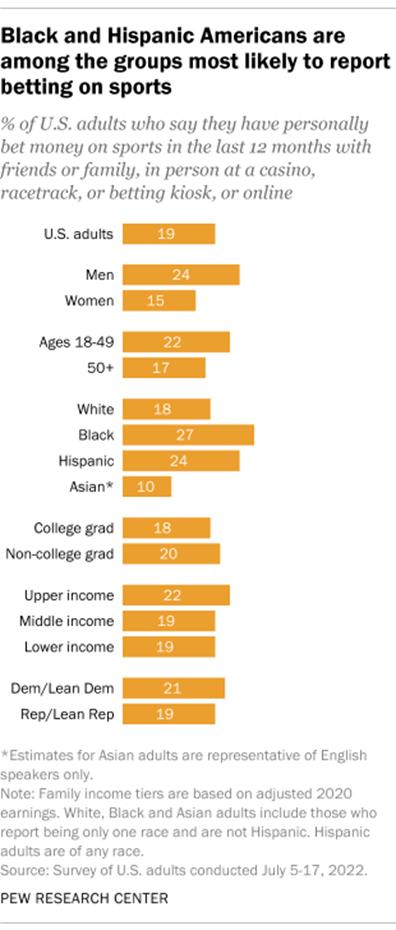

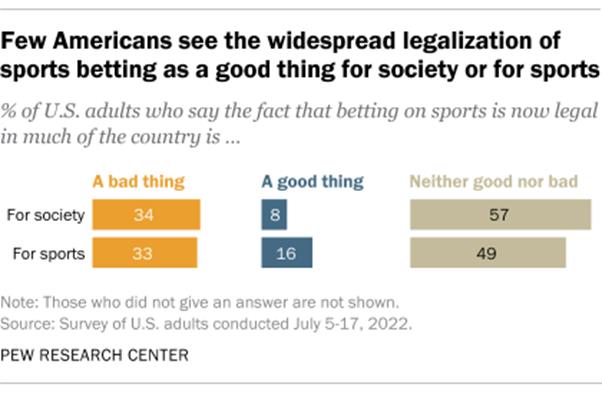

Hindus and Buddhists – totaled about 6%.1 (PEW) SEPTEMBER 13, 2022 As More States Legalize The Practice, 19% Of U S

Adults Say They Have Bet Money On Sports In The Past Year Around one-in-five U.S.

adults (19%) say they have personally bet money on sports in some way in the

last 12 months, whether with friends or family, in person at a casino or

other gambling venue, or online with a betting app, according to a new Pew

Research Center survey. Men are more likely than women (24% vs. 15%) to say

they have bet on sports in some form in the past year, as are adults under

the age of 50 when compared with those 50 and older (22% vs. 17%). There are

also differences by race and ethnicity: Black (27%) and Hispanic adults (24%)

are more likely than White (18%) and Asian American adults (10%) to report

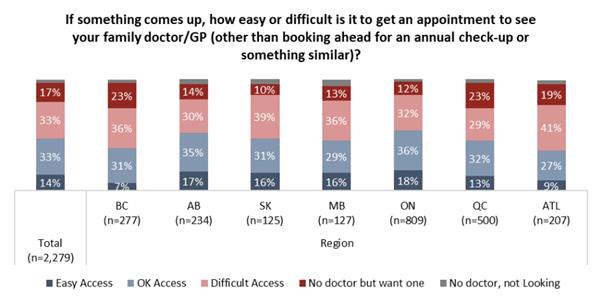

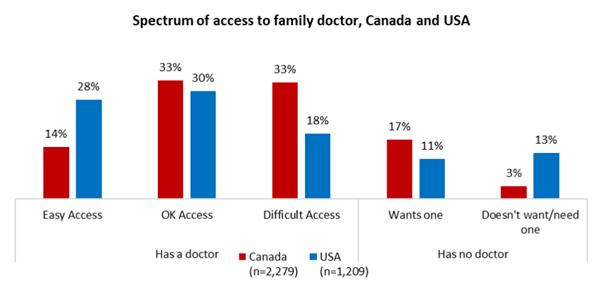

doing so. (PEW) SEPTEMBER 14, 2022 (Canada) Half Of Canadians Either Can’t Find A Doctor Or

Can’t Get A Timely Appointment With The One They Have The latest study from the

non-profit Angus Reid Institute – the second in a three-part health care

series – finds half of Canadians either unable to see the doctor they have

within a week (33%) or trying but unable to find a doctor at all (17%). Few,

14 per cent, say they have a doctor, and can get an appointment quickly,

while one-in-three say it usually takes longer than they’d like, but if it

were urgent, they could get an appointment promptly. (Angus Reid Institute) September 8, 2022 Poilievre Running Away As Clear Favourite Among

Conservative Party Supporters Regardless of their party

membership status, a full majority (57%) of Conservative voters now have a

favourable impression of Pierre Poilievre, up 8 points since a similar poll

was conducted in mid July. Conversely, only two in ten (20%) have an

unfavorable impression of the frontrunner, down 9 points since earlier in the

summer. Just one in four (23%, +1) Tory voters say they don’t know enough

about him to venture an opinion either way. (Ipsos Canada) 6 September 2022 Canadians Conflicted On Future Role Of Monarchy

As Half (54%) Say Canada Should End Ties To Monarchy Canadians are conflicted

on the future role of the monarchy with roughly half believing we should

sever ties to the monarchy, according to a new Ipsos poll conducted on behalf

of Global News. Canadians are clear on one thing: eight in ten (82%)

believe Queen Elizabeth II did a good

job in her role as monarch, with this final approval rating coming

in 3 points higher than it did in 2021. However, underscoring the uncertainty

of the future of the monarchy in Canada, only a slim majority (56%) agree

(10% strongly/46% somewhat) that they are confident that King Charles III will do a good job in

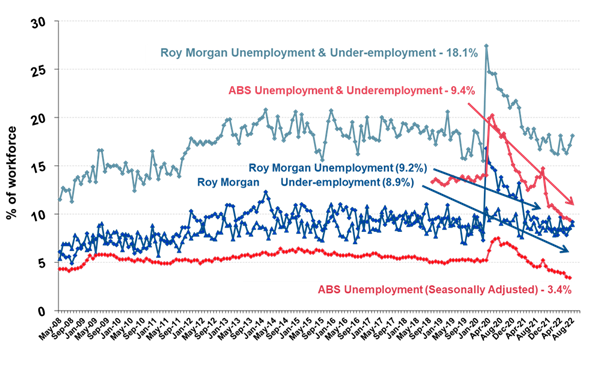

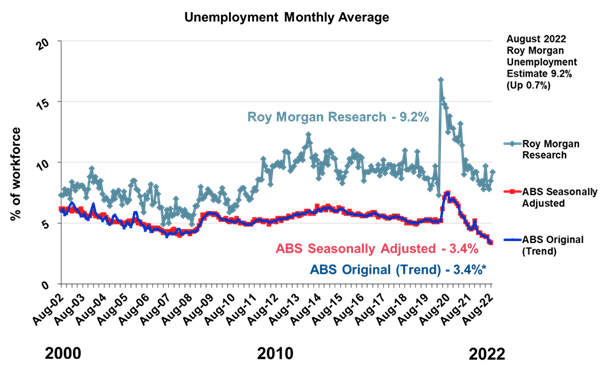

his role as monarch. (Ipsos Canada) 16 September 2022 AUSTRALIA Australian Unemployment Increases To 9.2% In

August As Workforce Swells To 14.8 Million Australians Unemployment in August

increased 117,000 to 1.36 million Australians (9.2% of the workforce) while

under-employment was up 59,000 to 1.33 million (8.9% of the workforce).

Overall unemployment and under-employment increased 176,000 to 2.69 million

(18.1% of the workforce). The workforce was

up 164,000 in August driven by increasing employment and unemployment:The

workforce in August was 14,850,000 (up 164,000 from July) – comprised of

13,487,000 employed Australians (up 47,000) and 1,363,000 unemployed

Australians looking for work (up 117,000). (Roy Morgan) September 05, 2022 ANZ-Roy Morgan Consumer Confidence Up By 1.1pts

To 86.1 – Highest For Three Months Since Early June There were small

improvements across the index this week with four improving slightly and only

one declining. On a State-by-State basis all mainland States except NSW

increased from a week ago. Now 23% of Australians (unchanged) say their

families are ‘better off’ financially than this time last year compared to

40% (down 1ppt), that say their families are ‘worse off’ financially. Only 8%

(unchanged) of Australians expect ‘good times’ for the Australian economy

over the next twelve months compared to 31% (down 1ppt), that expect ‘bad

times.’ (Roy Morgan) September 06, 2022 An Increasing Majority Of Australians, 60%

Believe Australia Should Remain A Monarchy This special Roy Morgan

SMS Poll was conducted by SMS on Monday September 12, 2022, with an

Australia-wide cross-section of 1,012 Australians. The survey was conducted

entirely after Prince Charles took the oath on the weekend to become King

Charles III. Analysis of the results by gender shows that nearly two-thirds

of women (66%) favour the Monarchy compared to only 34% that favour a

Republic with an elected President. However, the results for men are far

evenly split with 54% in favour of the Monarchy compared to 46% that would

prefer a Republic. (Roy Morgan) September 13, 2022 MULTICOUNTRY STUDIES Americans Consume Violent Video Games More Often

Than Germans Almost one in five Germans

(18 percent) plays video games most days of the week. In the U.S., this is

said a little more, 22 percent. That they never play video games, say 47

percent in Germany, in the USA 41 percent. The data therefore show that

Americans are more likely to play video games than Germans. On September 12,

the U.S. celebrates its annual National Video Games Day. On the occasion of

this, YouGov conducted surveys on the subject of video games in Germany as

well as in the USA and LINK in Switzerland and compared the results with each

other. (YouGov Germany) September 9, 2022 Source:

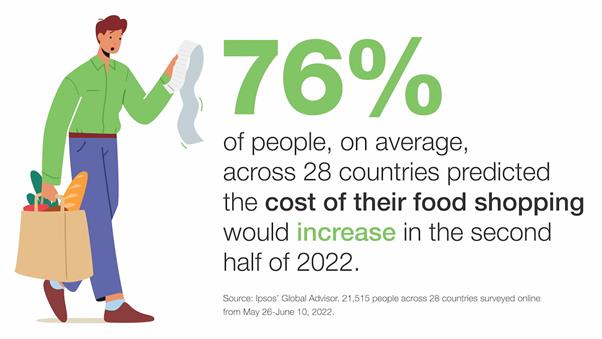

https://yougov.de/news/2022/09/09/amerikaner-haufiger-als-deutsche-zeugen-oder-spiel/ The Vast Majority (76%) Of Those Surveyed Across

28 Countries Anticipated The Cost Of Their Food Shopping Will Increase In The

Second Half Of 2022 The vast majority (76%)

of those

surveyed in

late May and early June for the Ipsos Global Inflation Monitor, on average,

across 28 countries anticipated the cost of their food shopping will increase

a little/a lot in the second half of 2022. Only 7% thought food prices will

decrease a little/a lot from July-December. In the U.S., inflation dipped a

bit to 8.5% in July, according to the U.S. Bureau of Labor Statistics, but

food prices climbed 10.9% year-over-year. (Ipsos Global) 7 September 2022 Source:

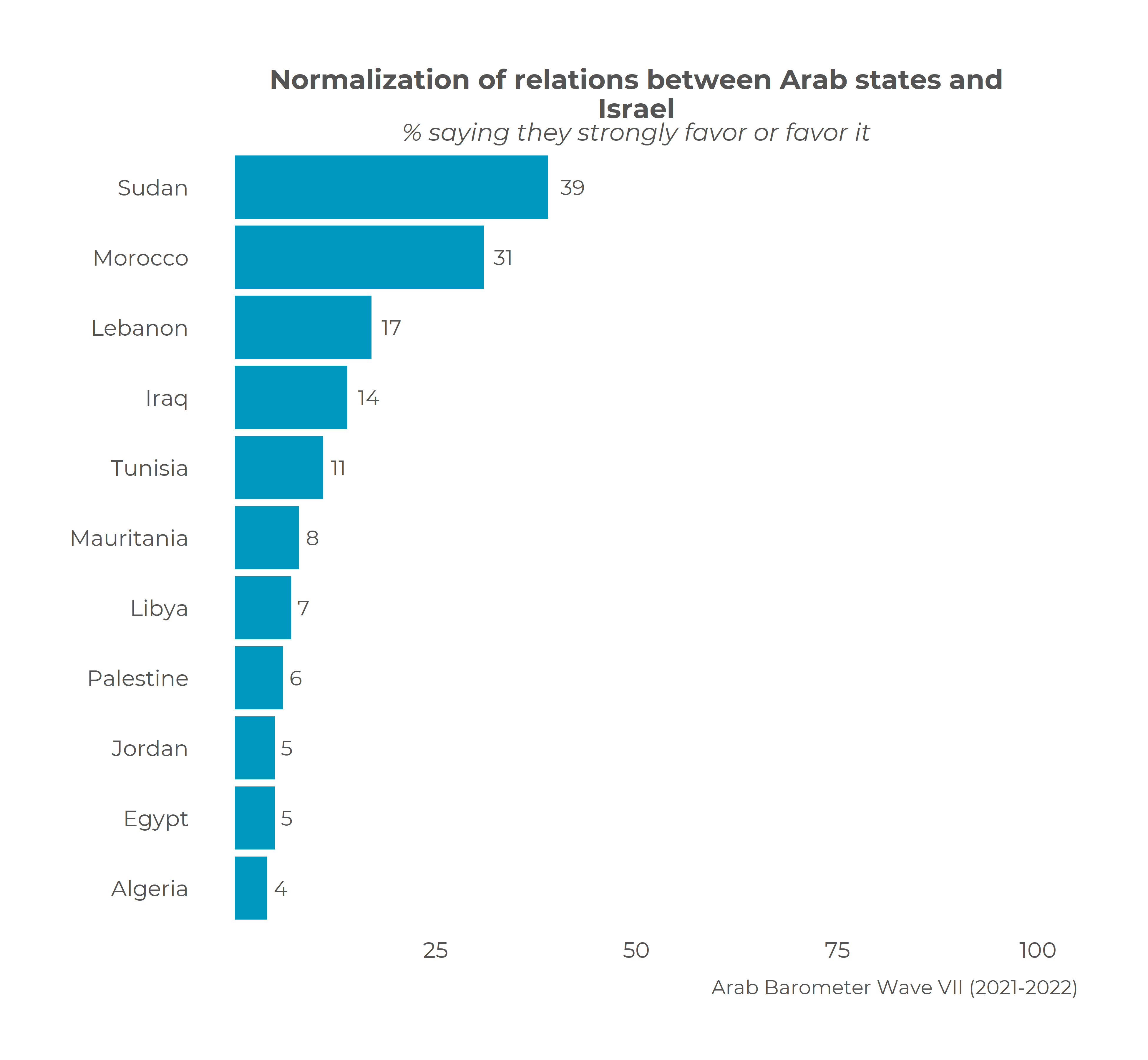

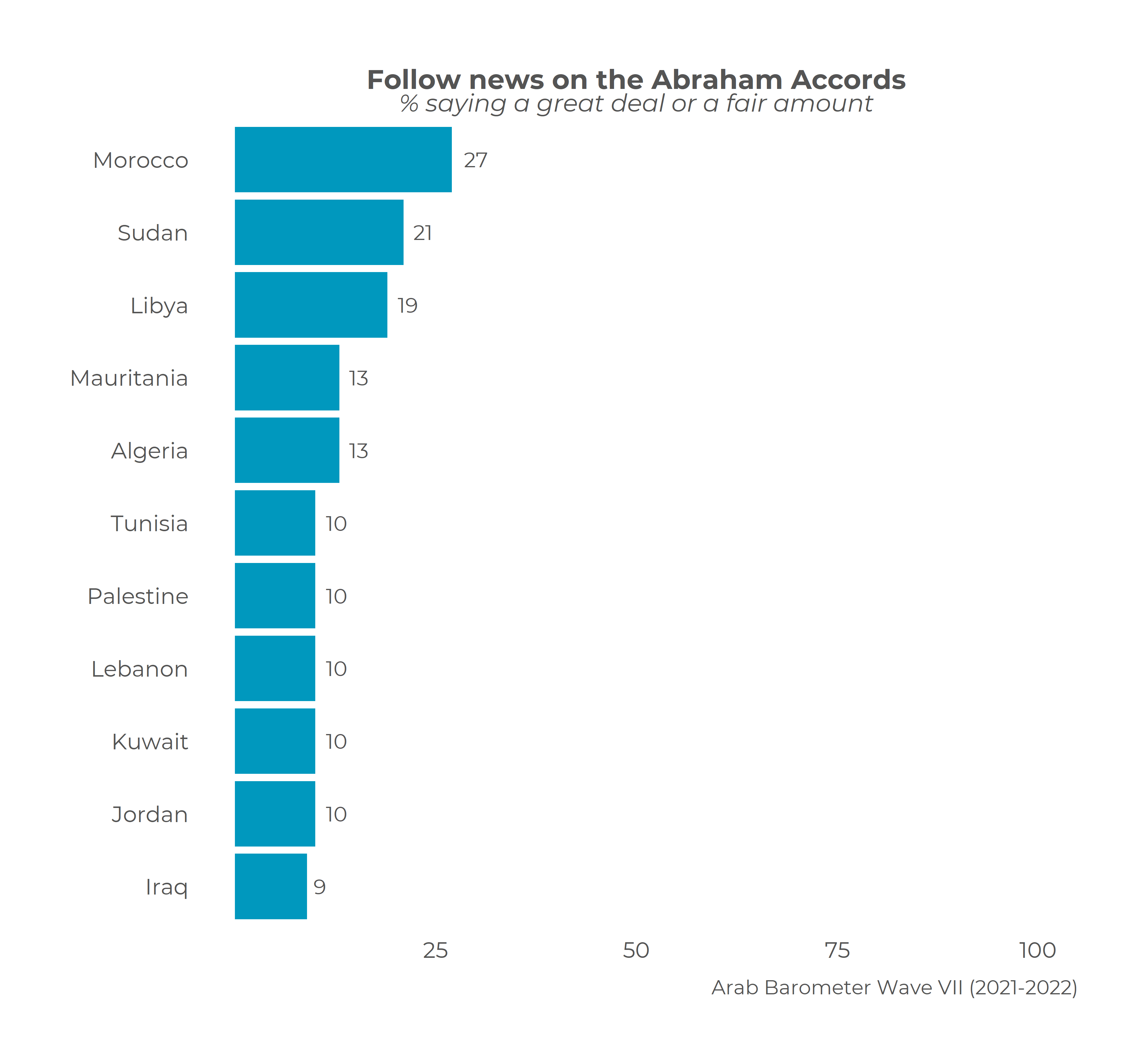

https://www.ipsos.com/en/high-food-prices-are-taking-bite-out-budgets In Nine Of The 11 Countries Surveyed, Fewer Than

One-In-Five Say They Support Normalization Agreements With Israel There is broad rejection

among ordinary citizens across MENA of the U.S.-backed Abraham Accords and a

broader peace deal with Israel. Although at most about a quarter of citizens

in the region say they follow news on this issue a great deal or fair amount,

including just one-in-ten in Tunisia, Palestine, Lebanon, Jordan, and Iraq,

these peace agreements are widely rejected overall. In nine of the 11

countries surveyed, fewer than one-in-five say they support normalization

agreements with Israel, including fewer than one-in-ten in Mauritania (8

percent), Libya (7 percent), Palestine (6 percent), Jordan (5 percent), and

Egypt (5 percent). (Arabbarometer) September 12, 2022 Source:

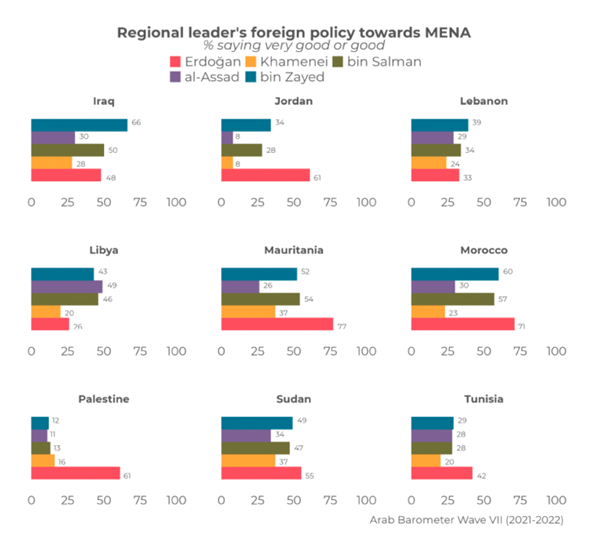

https://www.arabbarometer.org/2022/09/how-do-mena-citizens-view-normalization-with-israel/ Citizens Lukewarm On Leaders’ Cold War, Survey

Across 9 Middle East And North African Countries Of the five regional

leaders Arab Barometer asked citizens to evaluate, Syrian President Bashar

al-Assad and Iranian Supreme Leader Ali Khamenei typically are the least

popular. Assad tends to be more popular than Khamenei, however. Only in

Palestine (16 percent versus 11 percent) and Mauritania (37 percent versus 26

percent) is Khamenei significantly more popular than Assad. In recent years,

Iran has focused building relationships with African countries, which has

included starting bilateral talks with Mauritania. Meanwhile, Assad notably

comes in as the most popular regional leader in Libya with 49 percent of

Libyans saying his policies are “good” or “very good.” In Tunisia, Assad’s

approval (28 percent) is tied with that of bin Salman (28 percent) and bin

Zayed (29 percent). (Arabbarometer) September 15, 2022 Source:

https://www.arabbarometer.org/2022/09/citizens-lukewarm-on-leaders-cold-war/ 32% Of Canadians And 46% Of Americans Said They

Would Rate Their Mental Health Excellent Or Very Good 50% of Canadians and 51%

of Americans say their mental health is currently excellent or very good, representing an

improvement in mental health compared to during the pandemic.* 36% of

Canadians and 26% of Americans say their mental health worsened during the COVID-19

pandemic. Respectively, 55% and 58% say it stayed about the same. Canadians

and Americans indicate that their current greatest source of stress is their personal finances (22% of Canadians,

18% of Americans) or inflation (16%

of Canadians, 18% of Americans). 13% of Canadians and 14% of Americans are

currently seeing a mental health

professional. (Leger Opinion) September 14, 2022 Source:

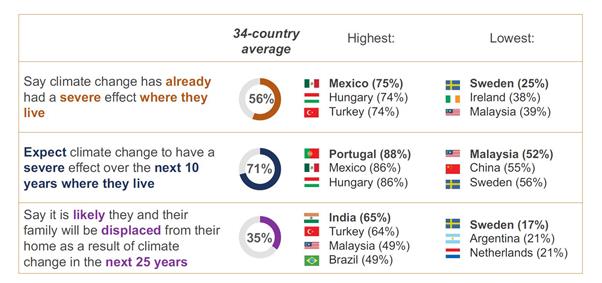

https://blog.legeropinion.com/en/surveys/north-american-tracker-september-14-2022/ Majority Across 34 Countries Describe Effects Of

Climate Change In Their Community As Severe On average across 34

countries, more than half of all adults surveyed (56%) say climate

change has already had a severe effect in the area where they live. More than

seven in ten (71%), including a majority in every single country, expect

climate change will have a severe effect in their area over the next 10 years.

One-third (35%) expect to be displaced from their home as a result of climate

change in the next 25 years. Majorities in 22 of 34 countries report their

area has already been severely impacted by climate change. (Ipsos MORI) 15 September 2022 Ninety-Seven

Percent Of People Globally Want To Take Action On Sustainability, In 32

Countries Faced with a

cost-of-living crisis, consumers are having make difficult choices. While

most want to take action on sustainability, rising and premium pricing is

making it hard. Ninety-seven percent of people globally are prepared to make

changes but 65% say their increased cost of living prevents them from doing

so. While all consumers are happy to reduce their food waste, take

reusable bags when shopping and recycle, they also expect brands to play

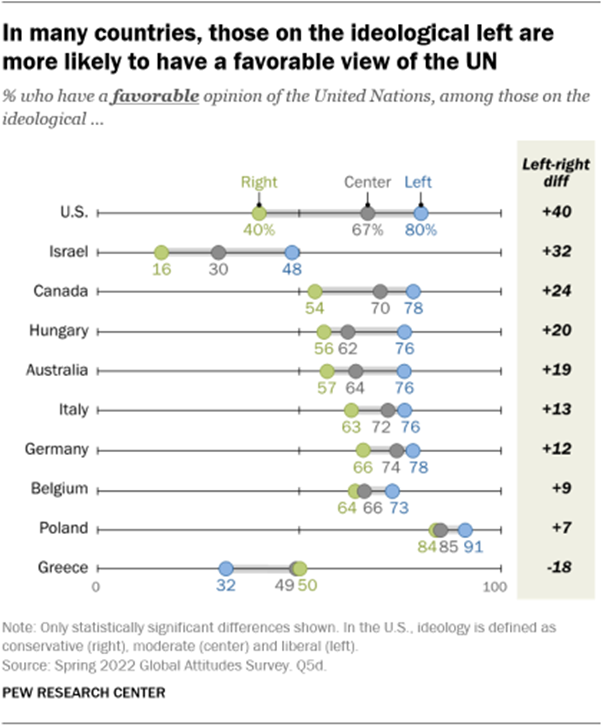

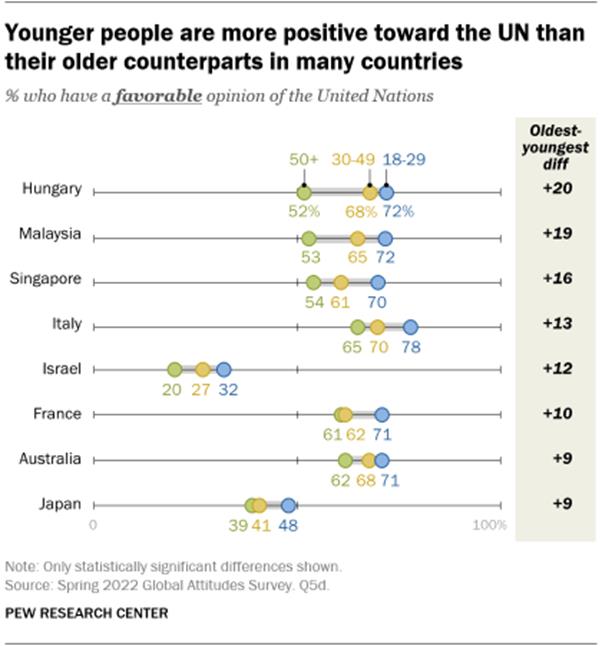

their part on packaging and waste. (Kantar) 15 September 2022 International Views Of The UN In 16 Surveyed

Nations Are Mostly Positive As global leaders descend

on New York in the coming days for the annual United

Nations General Assembly, international attitudes toward the

world’s leading multilateral organization are largely positive. Across 19

advanced economies surveyed by Pew Research Center this spring, a median of 65% say they have a favorable

view of the UN. Still, the institution gets mixed reviews in a few nations,

and it is frequently less popular among those on the political right. (PEW) SEPTEMBER 16, 2022 Source:

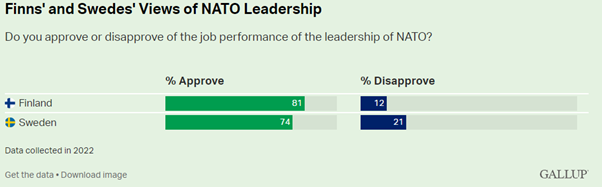

https://www.pewresearch.org/fact-tank/2022/09/16/international-views-of-the-un-are-mostly-positive/ 62% Of Finns And 40% Of Swedes Approve Of U S

Leadership Gallup surveys suggest

there are also few hurdles among the publics in these countries, with strong

majorities in Finland (81%) and Sweden (74%) approving of the alliance's

leadership. More than six in 10 Finns express approval of U.S. leadership in

2022, which is up from 52% in 2021 and represents a new high. Swedes are less

ebullient than Finns about U.S. leadership, but they are even more negative

about Russia's leadership. In 2022, 40% of Swedes approve of U.S. leadership,

down from 52% in 2021. (Gallup) SEPTEMBER 16, 2022 Source:

https://news.gallup.com/poll/401102/finns-swedes-approve-nato-leadership.aspx ASIA

759-760-43-01/Polls Military

Reserves, Civil Defense Worry Taiwan As China Looms

Chris Chen, a former

captain in Taiwan’s military, spent a lot of time waiting during his weeklong

training for reservists in June. Waiting for assembly, waiting for lunch,

waiting for training, he said. The course, part

of Taiwan’s efforts to deter a Chinese invasion, was jam-packed

with 200 reservists to one instructor. “It just became all

listening, there was very little time to actually carry out the

instructions,” Chen said. Russia’s invasion of

Ukraine has underscored the importance of mobilizing civilians when

under attack, as Ukraine’s reserve forces helped fend off the invaders.

Nearly halfway around the world, it has highlighted Taiwan’s weaknesses on

that front, chiefly in two areas: its reserves and civilian defense force. While an invasion doesn’t

appear imminent, China’s recent large-scale military exercises in

response to a visit by U.S. House Speaker Nancy Pelosi to Taiwan

have made the government in Taipei more aware than ever of the hard power

behind Beijing’s rhetoric about bringing the self-ruled island under its

control. Experts said that civilian

defense and reserve forces have an important deterrent effect, showing a

potential aggressor that the risks of invasion are high. Even before the

invasion of Ukraine in March, Taiwan was working on reforming both. The

question is whether it will be enough. Yet, the reserve system

has long been criticized. Many, like Chen, felt the seven days of training

for the mostly former soldiers was a waste of time that did not prepare them

well enough. “In Ukraine, if in the

first three days of the war it had fallen apart, no matter how strong your

military is, you wouldn’t have been able to fight the war,” Wang said. “A

resilient society can meet this challenge. So that when you are met with

disasters and war, you will not fall apart.” Taiwan reorganized its reserve

system in January, now coordinated by a new body called the All Out Defense

Mobilization Agency, which will also take over the civil defense system in an

emergency. One major change was the

pilot launch of a more intensive, two-week training instead of the standard

one week, which will eventually be expanded to the 300,000 combat-ready

reservists. The remaining reservists can play a more defensive role, such as

defending bridges, Wang said. Dennis Shi joined the

revamped training for two weeks in May at an abandoned building site on

Taiwan’s northern coast. Half the time it was raining, he said. The rest, it

was baking hot. The training coincided with the peak of a COVID-19

outbreak. Wearing raincoats and face masks, the reservists dug trenches and

practiced firing mortars and marching. “Your whole body was

covered in mud, and even in your boots there was mud,” Shi said. Still, he said he got more

firing time than during his mandatory four months of service three years ago

and felt motivated because senior officers carried out the drills with them. “The main thing is when

it’s time to serve your country, then you have to do it,” he said. There are plans to reform

the civil defense force too, said Wang, though much of the discussion has not

been widely publicized yet. The Civil Defense Force,

which falls under the National Police Agency, is a leftover from an era of

authoritarian rule before Taiwan transitioned to democracy in the 1980s and

1990s. Its members are mostly people who are too old to qualify as reservists

but still want to serve. “It hasn’t followed the

passage of the times and hasn’t kept pace with our fighting ability,” Wang

said. Planned changes include a

requirement to include security guards employed by some of Taiwan’s largest

companies in the force, and the incorporation of women, who are not required

to serve in the military. The Ukraine war, at least

initially, shook some people’s confidence in the willingness of America to

come to Taiwan’s assistance in the event of an attack. Whereas 57 percent

said last September they believed the U.S. would “definitely or probably”

send troops if China invaded, that dropped to 40 percent in March. The U.S. policy

of strategic ambiguity leaves it murky as to whether the U.S. would

intervene militarily. Pelosi said during her visit that she wants to help the

island defend itself. Outside of government

efforts, some civilians have been inspired to do more on their own. Last week, the founder of

Taiwanese chipmaker United Microelectronics, Robert Tsao, announced he would

donate 1 billion New Taiwan Dollars ($32.8 million) to fund the training of a

3-million-person defense force made up of civilians. More than 1,000 people

have attended lectures on civil defense with Open Knowledge Taiwan, according

to T.H. Schee, a tech entrepreneur who gives lectures and organizes civil

defense courses with the volunteer group, which aims to make specialized

knowledge accessible to the public. Others have signed up for

first aid training, and some for firearms courses, though with air guns as

Taiwan’s laws do not allow widespread gun ownership. These efforts need

government coordination, said Martin Yang, a spokesperson for the Taiwan

Military and Police Tactical Research and Development Association, a group of

former police officers and soldiers interested in Taiwan’s defense. “The civil sector has this

idea and they’re using their energy, but I think the government needs to come

out and coordinate this, so the energy doesn’t get wasted,” he said. Yang is critical of the

government’s civil defense drills, citing annual exercises in which civilians

practice taking shelter. “When you do this

exercise, you want to consider that people will hide in the subway, they need

water and food, and may have medical needs. You will possibly have hundreds

or thousands of people hiding there,” Yang said. “But were does the water and

food come from?” In July, the New Taipei

city government organized a large-scale drill with its disaster services and

the Defense Ministry. Included for the first time was urban warfare, such as

how first responders would react to an attack on a train station or a port. The drills had the feeling

of a carnival rather than serious preparation for an invasion. An MC

excitedly welcomed guests as Korean pop music blared. Recruiters for the

military, the coast guard and the military police set up booths to entice

visitors, offering tchotchkes such as toy grenade keychains. Chang Chia-rong guided VIP

guests to their seats. The 20-year-old expressed a willingness to defend

Taiwan, though she hadn’t felt very worried about a Chinese invasion. “If there’s a volunteer

squad, I hope that I can join and defend my country,” she said. “If there’s a

need, I would be very willing to join.” September 5, 2022 Source:

https://www.asahi.com/ajw/articles/14711125 759-760-43-02/Polls More Than Half

(55%) Japanese, Said They Support Hosting The Winter Games

The International Olympic

Committee (IOC) will decide the site of the 2030 Winter Olympics and

Paralympics at its general conference next year. However, the survey broken

down by Hokkaido residents only showed that almost an equal percentage either

support or don't support holding the sporting events in Sapporo. In comparison, in a

survey conducted of Tokyo residents in December 2012, 60 percent of

respondents supported holding the 2020 Games in the Japanese capital and 27

percent didn’t. The survey was conducted

before Tokyo was chosen as the site of the 2020 Summer Olympics and

Paralympics, which were postponed to 2021 due to the COVID-19 pandemic. Although a simple

comparison could be misleading as the surveys were conducted on different

audiences or for other reasons, it seems that local residents are less

enthusiastic about hosting the Olympics in Sapporo than Tokyo people were 10

years ago. The Asahi Shimbun

conducted the survey on Sept. 10 and 11 of voters across Japan using the

random digit dialing method. With the RDD method,

landline and mobile phone numbers are generated by a computer at random to be

contacted. The newspaper collected

valid responses from 1,462 voters. Of these, there were 581 people with

landline phones and 881 people with mobile phones. The paper contacted

landline phone numbers of 1,103 households that had an eligible voter,

meaning the response rate among these was 53 percent. It also called 2,046

mobile phone numbers with eligible voters, meaning the response rate among

these was 43 percent. September 13, 2022 Source:

https://www.asahi.com/ajw/articles/14717681 759-760-43-03/Polls 7 Out Of Every

10 Turkish People Have A Credit Card

7

out of every 10 people in Turkey have a credit card

Nearly

Half of Individuals Who Use Credit Cards Pay All of Their Periodic Card Debts

The

use of credit cards in shopping is a very common behavior. 14% of People Who

Prefer Only Cash Payments

Installment

Payment Preference for Credit Card Purchases is 71%. If there is an installment

payment opportunity, 71% of credit card holders prefer installment payment in

their shopping. 25% say they always pay one shot. Ipsos,

Turkey CEO Sidar Gedik made the following evaluations about the data; Three

out of every ten people who participated in our research do not have a credit

card. This actually shows that there is still a way to go in the credit card

market. One out of every two

people who have a credit card say they make "all their purchases"

with a credit card. A product that requires credit card conscious use. When

used within the financial capacity of the individual, it can undoubtedly

provide various advantages, for example, seven out of every ten card holders

benefit from installment shopping opportunities. On the other hand, more than

half of those who make all their purchases with credit cards state that the

reason for this behavior is the lack of income for cash payment. In the fight

against high inflation, the credit card is like a double-edged knife. There

is a chance that the end of the rope will escape, 29% of credit card users

are close to this situation, they can either pay the minimum payment amount

or even cannot pay it. 7 September 2022 Source:

https://www.ipsos.com/tr-tr/her-10-kisiden-7sinin-kredi-karti-var 759-760-43-04/Polls 3 In 5 People

In Karachi Do Not Read Newspaper

According to a survey

conducted by Gallup & Gilani Pakistan, more than half (66%) of Karachi’s

population does not read the newspaper. A

representative sample of adult men and women from Karachi was asked the

following question, “Do you read the newspaper?” In response to this

question, 34% said ‘Yes’ while 66% said ‘No.’ The number of people who said

‘Yes’ increased as the level of education increased amongst the respondents

with 67% Professionals/Doctors answering ‘Yes’ compared to only 18% of

illiterate people. The number of people who read newspaper also increased

with age, 31% of the people aged 18-23 read the newspaper while 35% of those

aged 50+ read it. Question: “Do you read the newspaper?”

September 14, 2022 Source:

https://gallup.com.pk/wp/wp-content/uploads/2022/09/14th-Sep-Eng.pdf 759-760-43-05/Polls Consumer

Behavior Characteristics And Preferences In Online Shopping; 78% Of Indonesian

Consumers Choose Shopee

Nowadays, online shopping is not just a

solution or the main alternative that provides convenience, but has become

part of people's lifestyle. This is also supported by a Snapcart survey, it

is recorded that as many as 95% of consumers connect with the internet more

than 1 time a day in the past month, and another 5% at least access the

internet 1 time a day. 57% also admit that the pandemic that lasts for 2

years has made them do online shopping activities more often. Seeing this, e-commerce players in Indonesia are

competing to strengthen their competitiveness through innovations and the

latest features in order to attract more users. "Technology offers

many new ways and solutions in carrying out daily life, one of which is to

meet needs. This can be seen from the data that shows online shopping

activities that are getting closer to people's lives. Various user needs

that continue to develop into opportunities and reasons for e-commerce players in

Indonesia to strengthen their attractiveness through discount offers, the

birth of innovative features to complete product choices. This is also what

we see that ultimately shapes the character or behavioral preferences of

people in shopping online," said Astrid

Wiliandry, Director of Snapcart Indonesia, in Jakarta (8/9).

Characteristics

of User Online Shopping Behavior The segmentation of the

character of shopping behavior does not only depart from differences in

preferences, priority needs to lifestyle. Another factor tied up in this

regard is what every e-commerce player offers. Data shows the reasons people

shop online at

selected e-commerce include

the free shipping promo (79%), a variety of attractive promo offers (67%),

the availability of complete payment features (63%), other existing and

easy-to-use features (61%) and complete types and categories of products that

are diverse and complete (58%). This also affects the

character of people's online shopping behavior, especially in the level of

trust to decisions when shopping. Recorded in Indonesia itself, there

arethree types of consumer behavior observed and occupy the top three;

including 51% of discount seekers or

discount seeker consumers who shop driven by various

promotional offers; 25% answered as need-based

customers and 24% chose the

type of wandering customers.

This type of discount seekers consumers are

people who like to find and take advantage of promos when shopping online. Through this survey, this type

of consumer behavior occupies the first position. Promos and discounts are

still the main magnet for consumers in Indonesia when shopping online.

Consumers usually hunt for promos such as Discount Vouchers, cheap shipping costs, Cashback, Flash Sales and various

other promos in each campaign. Welcoming the 4th quarter,

which is also the momentum of the year-end shopping

festival, it is a space for these e-commerce players to present a special

program studded with promos that can be utilized by discount seeker consumers,

especially towards the shopping festival at 9.9. Interestingly, 3 factors

that are attractive to consumers when preparing for online shopping during the year-end

festival include Cheap Shipping Costs (70%), Attractive Promo Offers (66%),

and Affordable Prices (60%). "The year-end

festival has opened with the arrival of the 9.9 twin numbers campaign. The

presence of various programs was enthusiastically welcomed by consumers,

where they began to prepare themselves, especially for shopping on the peak

day of the campaign. The programs presented include Shopee 9.9 Super Shopping

Day, Lazada 9.9 Trendy Brands Sale and Tokopedia's KEBUT campaign. Based on

the variety of promos offered during the opening campaign of the ongoing

year-end shopping festival, 78% chose Shopee as the e-commerce to be used, followed

by Tokopedia (19%) and Lazada (2%).

In the Need Based Customers type of

behavior, individuals tend to shop according to their needs. Where the thing

that is sought is the completeness of product choices and categories that can

meet daily and complementary needs. The factors that influence decisions when

shopping for this segmentation are usually related to the ease of accessing a

product, recommendations, and product

reviews, as well as a variety of categories with a complete selection

of products offered by brand partners

and sellers who are members of the platform. Categories and a complete

selection of products are one of the main indicators or steps for an

individual with this type of behavior to choose a platform for online

shopping. The distribution of respondents' preferences in choosing preferred e-commerce for product

categories in the last 3 months can be seen in the following data:

Along with the development

of technology accompanied by lifestyle changes, e-commerce players in

Indonesia continue to innovate to create new features as a complement. This

feature offers entertainment that strengthens consumer engagement making it possible for

them to return to shopping on the platform.

"We see the aspect that makes people feel comfortable shopping online is

the choice of features available. The Wandering

Customers type, which is

one of the biggest visitors to e-commerce sites. They really

don't always shop. However, their presence largely determines the popularity

of an e-commerce site, added Astrid

Wiliandry. One of the magnets to attract Wandering Consumers' behavioral types is

the presence of interesting entertainment features that encourage them to be

active, such as games and instant video." Astrid said. Similar to the

completeness of products and categories, the many interesting entertainment

features make users more active and creative. Through surveys that have been

conducted, the reason consumers use entertainment and gamification features

is to be interested in the gifts offered (58%), popular among consumers

(33%), ease of finding features (29%), and the opportunity to interact with

other consumers (19%). Through surveys,

gamification features that are favored by consumers are Shopee Tanam (51%),

Tokopedia Egg Harvest (13%) and Lazada Coin Tree (2%). Meanwhile, for the

preferred entertainment features, consumers choose Shopee LIVE (50%), Shopee

Video (28%), followed by Tokopedia Play (16%), Lazada Feed (1%), and LazLive

(1%). September 8, 2022 AFRICA

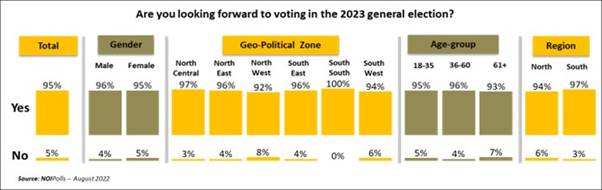

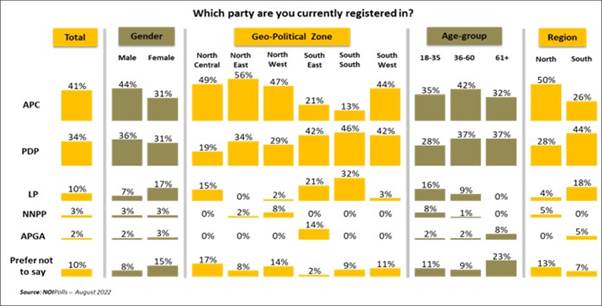

759-760-43-06/Polls Furthermore, finding

revealed that the All-Progressive Congress (APC) has the larger share (41

percent) of respondents who are registered members. In addition, 34 percent

of the respondents stated that they are registered members of the People’s

Democratic Party (PDP), while 10 percent are registered with Labour Party

(LP) ahead of the 2023 general elections. Also, 10 percent of the respondents

preferred not to disclose their party affiliations. Finally, of the 89

percent of adult Nigerians who claimed that they are registered to vote in

the upcoming 2023 general elections, 95 percent acknowledged that they are

looking forward to voting in the 2023 general elections. These are the key findings

from the countdown to the 2023 general election polls conducted in the week

commencing 15th August 2022. This is the second in the series of the monthly

election polls conducted by NOIPolls as Nigerians countdown to the actual

elections in 2023. Survey Background Nigeria has a multi-party

system with sometimes three or four stronger parties that are electorally

successful. In line with the provisions of the 1999 Federal Constitution as

amended and the subsisting Electoral Act, the Independent Electoral

Commission (INEC) is expected to conduct another round of general elections

in Nigeria early in February 2023[1]. With about 26 weeks to the

2023 general elections in Nigeria, the outline of the 18 political parties

registered and accredited by INEC for the 2023 presidential election would

reflect the political events of 2022. Already, presidential, gubernatorial,

and senatorial primaries have been conducted across all the political parties

in Nigeria to select party representatives ahead of the 2023 general

elections. While the major parties, APC and PDP, based on their spread across

state and national assembly, are seriously canvassing the support of other

Political Parties especially in the Presidential race, emerging political

parties are also creating momentum in the political space. However, the ultimate

deciding factor remains with the electorates. Against this background,

NOIPolls conducted its Election Series poll to seek the views of

Nigerians on their awareness of the existing political parties ahead of the

2023 general elections. This is the second in the series of monthly election

polls conducted by NOIPolls as Nigerians countdown to the 2023 general elections.

The first being – Citizen’s Trust in Electoral Integrity, was conducted

in July 2022. Survey Findings The first question

revealed that an overwhelming majority of adult Nigerians nationwide (89

percent) claimed that they have registered to vote in the upcoming 2023

general elections. This assertion cuts across gender, geo-political zones,

and age-group with at least 83 percent representation. On the contrary, 11

percent stated otherwise.

The poll findings further

revealed that 95 percent of those who claimed to have registered to vote

expressed their enthusiasm in voting during the 2023 general elections. This

view also cuts across gender, geographical locations, and age-group with a

minimum of 92 percent representation. However, 5 percent of said they are not

looking forward to vote in the 2023 general elections.

Furthermore, to gain

insight on the proportion of adult Nigerians who are registered members of

political parties, respondents were asked: Are you currently a registered

member of any political party? The results revealed that a huge proportion of

adult Nigerians are not registered to any political party in the country.

Analysis by gender shows there are more female (82 percent) than male (66

percent) respondents who mentioned that they are not registered to any

political party in the country. On the flipside, 20

percent of adult Nigerians admitted that they are registered members of

different political parties, and have membership cards, although 6 percent

claim they are registered members but do not have membership cards.

Subsequently, respondents

who claimed to be registered members were further probed to ascertain the

political party they represent. The finding revealed that the All-Progressive

Congress (APC) has the larger share (41 percent) of respondents who are

registered members regardless of those who own a membership card. Analysis by

region indicates that APC has more registered members form the northern

region (50 percent) than in the southern region (26 percent). More findings revealed

that 34 percent of the respondents stated that they are registered members of

the People’s Democratic Party (PDP), while 10 percent are registered with

Labour Party (LP) ahead of the 2023 general elections. Analysis by region

also revealed that both the PDP and LP have more registered members from the

southern region with 44 percent and 18 percent respectively.

In the same vein,

respondents who are not registered were further probed to know the political

party they are likely to register with. The poll result revealed that the PDP

(13 percent) and LP (13 percent) both have the same proportion of respondents

who are likely to register with them, while 8 percent mentioned APC, 2

percent stated NNPP. Further analysis showed

that 41 percent of the respondents refused to disclose the political party

they would register with, while 13 percent stated that they are not willing

to register with any political party in the country.

Conclusion The poll findings have

revealed that a huge proportion of adult Nigerians are not registered with

any political party in the country. On the flipside, 20 percent of adult

Nigerians admitted that they are registered members of different political

parties, and they have a membership card whereas, 6 percent are registered

members but do not have a membership card. Furthermore, the poll

result showed that the All-Progressive Congress (APC) has a greater

proportion (41 percent) of respondents who are registered members regardless

of those who own a membership card. More findings revealed that 34 percent of

the respondents stated that they are registered members of the People’s

Democratic Party (PDP), while 10 percent are registered with Labour Party

(LP) ahead of the 2023 general elections. Finally, given that adult Nigerians

have the voting right to elect their leaders, 95 percent of the registered

voters have acknowledged that they are looking forward to voting in the 2023

general elections. September 6, 2022 Source:

https://noi-polls.com/political-party-affiliation-poll-election-poll/ 759-760-43-07/Polls Six In 10

(59%) Ugandans Say The Government Is Doing A Poor Job Of Addressing Climate

Change

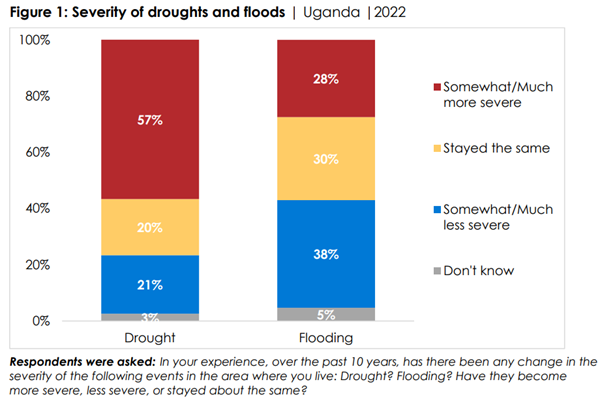

Key findings § Almost six in 10 Ugandans (57%) say droughts have become

more severe over the past 10 years; only half as many (28%) say the same

about floods. § More than half

(56%) of Ugandans have heard of climate change. Among those who are aware of

climate change: o More than eight in 10 (84%) say it is making life in Uganda

worse. o More than three-fourths (78%) believe that ordinary citizens can

help curb climate change (71%). o Eight in 10 (80%) want the government to

take immediate action to limit climate change, even if it is expensive,

causes job losses, or takes a toll on the economy. o Only small

minorities are satisfied with efforts by the government (4%), business and

industry (5%), ordinary citizens (9%), and developed countries (11%) to fight

climate change. o Ugandans assign primary responsibility for limiting climate

change to the government (46%) and to ordinary citizens (43%). § Six in 10 (59%)

say the government is doing a poor job of addressing climate change. Severity

of extreme weather conditions Before asking about climate change,

Afrobarometer asked respondents about their experiences with extreme weather

conditions. Almost six in 10 Ugandans (57%) say droughts have become

“somewhat more severe” or “much more severe” in their region over the past 10

years. Two in 10 (21%) say droughts have become less severe, and about the

same proportion (20%) report no change (Figure 1). In contrast, a plurality

(38%) of respondents say that the severity of floods has decreased, while 28%

say they have gotten worse. Compared to survey findings in 2017, the

proportion of Ugandans who say drought has gotten more severe has dropped by

30 percentage points, from 87% to 57% (Figure 2). In contrast, the share of

citizens who report more severe flooding has more than doubled since 2017

(12%).

Rural residents are more

likely than urban residents to report increasingly severe droughts (59% vs.

49%), perhaps reflecting a greater awareness of the effects of a lack of

rainfall in more agricultural areas (Figure 3). Geographically, the Karamoja

sub-region (94%) stands out as most affected by increasingly severe drought,

followed by the Lango (86%), Acholi (73%), and Eastern (71%) sub-regions. Only about four in 10

residents in the Buganda (43%), Tooro (38%), and Kigezi (36%) subregions

report worsening drought. These findings are in line with other reports that

show Karamoja as the region most vulnerable to drought and worst hit by

climate change (Africa Farmers Media Centre, 2016; USAID, 2017; Monitor,

2021). Perceptions of more severe drought vary widely by respondents’

economic status, ranging from 39% of well-off citizens to 68% of those

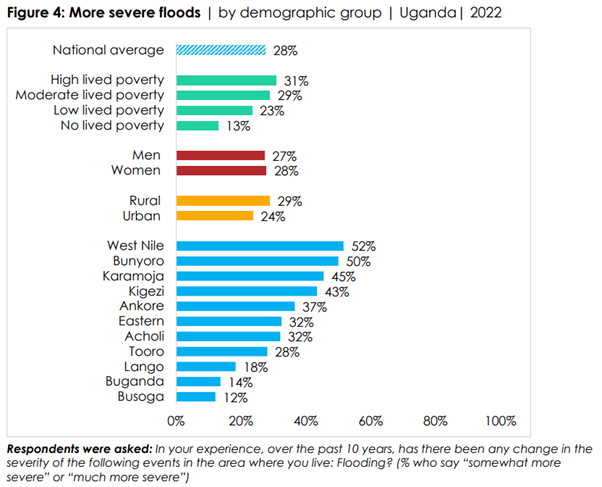

experiencing high “lived poverty.”1 With regard to more severe flooding, the

patterns are quite different across the sub-regions. Worsening floods are of

greatest concern to citizens in West Nile (52%) and Bunyoro (50%), while they

are of least concern in Buganda (14%) and Busoga (12%) (Figure 4).

Climate change Awareness

of climate change Lack of awareness is a major obstacle to climate change

adaptation in developing countries (Shahid & Piracha, 2016). In Uganda,

56% of citizens say they have heard of climate change (Figure 5). This

reflects a large decline from 78% in 2017, perhaps reflecting a stillemerging

understanding of climate change, with awareness that may fluctuate in

response to whether media attention is focused on extreme weather events or

other topics, such as the COVID-19 pandemic. Although worsening drought is

widely felt in the Karamoja and Acholi sub-regions, relatively few residents

in these areas (50% and 37%, respectively) are aware of climate change

(Figure 6). In the Lango and Eastern sub-regions, both experience of

increasing drought and awareness of climate change (79% and 59%,

respectively) are relatively high. Economically well-off citizens (65%) are

more likely to be familiar with the term “climate change” than those

experiencing lived poverty (55%-56%). As expected, awareness increases with

an individual’s level of education, with the most educated respondents (71%)

far more likely to have heard of climate change than the uneducated (42%).

More men (60%) than women (52%) are aware of the concept. Awareness of

climate change increases with age, ranging from 53% of those aged 18-30 to

60% of those in the 50-and-above category.

Awareness of climate

change increases with respondents’ consumption of news via most media

platforms. Among those who never or seldom (less than once a month) get news

from the radio, television, the Internet, or newspapers, 47%-54% have heard

of climate change (Figure 7). But awareness of climate change is

significantly higher among respondents who frequently get news from

newspapers (65%), television (61%), the Internet (60%), and radio (59%).

Social media is an exception, showing no difference between frequent users

and non-users (both 56%).

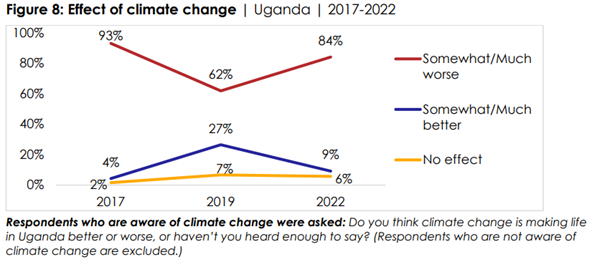

Effects of climate change

Among citizens who are aware of climate change, more than eight in 10 (84%)

say it is making life in Uganda “somewhat worse” (30%) or “much worse” (54%)

(Figure 8). Perceptions of the adverse effects of climate change increased

sharply between 2019 (62%) and the most recent survey, rebounding from a

significant drop between 2017 and 2019. Like increasing drought, the negative

impact of climate change is most widely felt in the Karamoja (94%) and Lango

(93%) sub-regions (Figure 9). Older citizens (89%) are more likely to report

negative effects than younger respondents (82%-83%). The poorest citizens

(87%) are more likely to feel the adverse effects of climate change than the

economically well-off (79%). Individuals with post-secondary education (67%)

are far less likely to feel the negative impacts of climate change than their

counterparts (84%-87%).

Who is responsible for

addressing climate change? For Ugandans, addressing climate change is a

collective responsibility. About eight in 10 respondents who are aware of

climate change (78%) “agree” or “strongly agree” that citizens can help curb

climate change (Figure 10). And a similar proportion (80%) want their

government to take steps now to limit climate change, even if it is

expensive, causes job losses, or takes a toll on the economy. In fact, in

Ugandans’ eyes, the government (46%) and ordinary people (43%) share primary

responsibility for fighting climate change and reducing its impact. Very few

survey respondents assign this responsibility to business and industry (3%),

developed countries (2%), and traditional leaders (2%) (Figure 11). Are

stakeholders doing enough to limit climate change? Respondents answer with a

resounding “No.” Only small minorities say the government (4%), business and

industry (5%), citizens (9%), and developed countries (11%) are making enough

of an effort to fight climate change (Figure 12). Large majorities believe

more needs to be done, including 79% who say the government needs to do “a

lot more.”

When asked to assess how

well the government is addressing the problem of climate change, fewer than

one-third (30%) of all survey respondents describe the government’s

performance as “fairly” or “very” good, while six in 10 (59%) give the

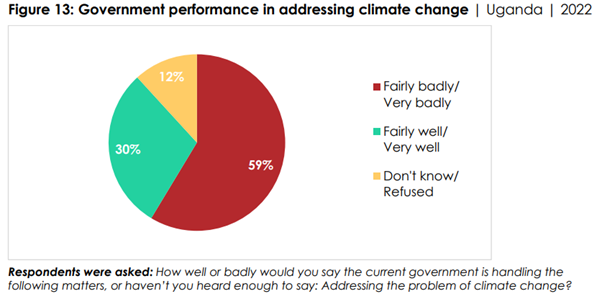

government a failing grade on this issue (Figure 13). Approval of the

government’s efforts declines as respondents’ level of lived poverty

increases, dropping from 50% of the wealthy to just 23% of the poorest

(Figure 14). Lango is the only sub-region where approval almost equals

disapproval.

Conclusion As Ugandans

continue to experience the deleterious effects of climate change, findings

from the most recent Afrobarometer survey suggest that broad support for

concerted climate action is building – at least among those citizens who have

heard of climate change. Large majorities of those familiar with climate

change say it is making life worse and requires immediate government action,

even if such policies and programmes are expensive, cause job losses, or take

a toll on the economy. But overwhelming majorities also say they expect greater

efforts by other stakeholders, including business and industry, more

developed countries, and ordinary citizens. Since more than four in 10

Ugandans say they have not yet heard of climate change, one step toward

building momentum for climate action may be targeted interventions to educate

more citizens about the threat they face. 6 September 2022 759-760-43-08/Polls Mauritians

Embrace Covid-19 Vaccination Despite Low Levels Of Trust In Vaccine Safety

Key findings § Effects of the COVID-19 pandemic: o More than half (53%)

of Mauritians say they or a member of their household became ill with

COVID-19 or tested positive for the virus. About one-fourth (27%) say someone

in their household lost a job, business, or primary source of income due to

the pandemic. § Attitudes toward

vaccines: o More than nine in 10 Mauritians (95%) say they have been

vaccinated against COVID-19. o Among those who have not been vaccinated,

almost two-thirds say they are “very unlikely” (41%) or “somewhat unlikely”

(23%) to try to get vaccinated. o A majority of vaccine-hesitant

citizens cite concerns about negative side effects and vaccine safety as

their main reasons. o Only 36% of citizens say they trust the government

“somewhat” or “a lot” to ensure the safety of COVID-19 vaccines. § Government

response to COVID-19: o More than half (52%) of Mauritians say the government

has done “fairly well” or “very well” in managing the response to the

pandemic. o About the same proportion (51%) say they are satisfied with the

government’s efforts in providing relief to vulnerable households. o Fewer

than half think the government has done a good job of minimising disruptions

to children’s education (46%) and of ensuring that health facilities are

adequately resourced (47%). o More than two-thirds (69%) of Mauritians

believe that “some” or “a lot” of the resources intended for the COVID-19

response have been lost to corruption. o More than six in 10 Mauritians (62%)

approve of using security forces to enforce public health mandates during an

emergency like the pandemic, and almost half (45%) would accept postponing

elections. But most (79%) disapprove of censoring media reporting during a

public health emergency. §

Looking ahead: o Mauritians are divided in their views on whether the

government is prepared to deal with future public health emergencies (52%

yes, 43% no) and whether it needs to invest more in such preparations (43%

yes, 40% no). Effects of COVID-19 More than half of Mauritians (53%) say they

or a member of their household became ill with or tested positive for

COVID-19, while about one-fourth (27%) of citizens say someone in their

household lost a job, business, or primary source of income due to the

pandemic (Figure 1).

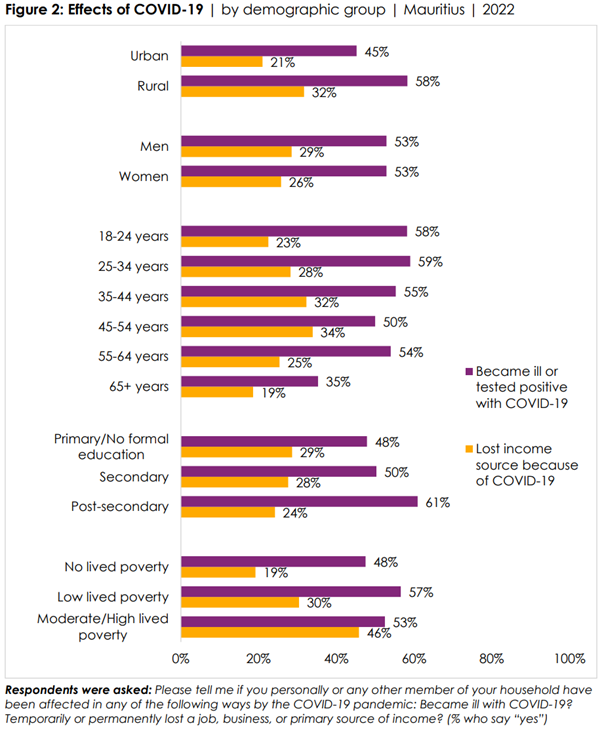

The effects of COVID-19 appear

to have been more widely experienced in rural areas than in cities. Rural

residents are significantly more likely than urbanites to report losing an

income source (32% vs. 21%) and becoming ill with or testing positive for

COVID-19 (58% vs. 45%) (Figure 2). Illness and/or positive COVID-19 tests are

somewhat more common among younger respondents than among their elders and

increase in frequency with respondents’ education level, ranging from 48% of

those with no formal/primary education to 61% of those with postsecondary

qualifications. Loss of an income source is more common among poorer citizens

(46% of those experiencing moderate/high lived poverty, compared to 19% of

the wealthy).

Attitudes toward

vaccination More than nine in 10 citizens (95%) say they have been vaccinated

against COVID-19. Only 5% say they have not received the shot (Figure 3).

Among those who have not been vaccinated, almost two-thirds say they are

“very unlikely” (41%) or “somewhat unlikely” (23%) to try to get vaccinated (Figure

4).

Among citizens who say

they are unlikely to get vaccinated, the most frequently cited reasons have

to do with vaccine safety, including the belief that the vaccine may cause

bad side effects (27%), mistrust of the vaccine or worries about getting a

fake or counterfeit vaccine (24%), or concerns that the vaccine was developed

too quickly (21%). Others say they already had COVID-19 and believe they are

immune (8%) or that the vaccine is not effective (8%) (Figure 5). It is

important to note that because of the small samples of respondents who say

they have not been vaccinated (N=56) and those who say they are unlikely to

try to get vaccinated (N=38), these results have large margins of error and

should be interpreted with caution.

Even though most

Mauritians say they have received a vaccination against COVID-19, fewer than

four in 10 citizens say they trust the government “somewhat” (29%) or “a lot”

(7%) to ensure the safety of the vaccines, while a majority express “just a

little” trust (47%) or no trust at all (15%) (Figure 6).

Government response to

COVID-19 While trust in the government’s ability to ensure vaccine safety is

relatively weak, more than half of Mauritians (52%) describe the government’s

overall performance in managing the response to the COVID-19 pandemic as

“fairly” or “very” good, while 46% say it has done a poor job (Figure 7). On

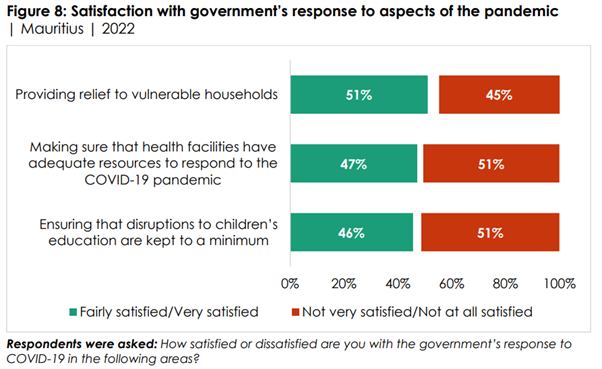

specific aspects of the COVID-19 response, a slim majority (51%) say they are

“fairly satisfied” or “very satisfied” with the government’s efforts to

provide assistance to vulnerable households. Close to half of citizens

express satisfaction with the government’s efforts to ensure that health

facilities are adequately resourced to deal with the pandemic (47%) and to

ensure that disruptions of children’s education are held to a minimum (46%)

(Figure 8).

COVID-19 relief assistance

Almost half (47%) of Mauritians report that their household received COVID-19

relief assistance from the government, while 52% say they did not (Figure 9).

Rural households were considerably more likely to benefit from government

assistance than those in urban areas (56% vs. 36%) (Figure 10). Government

assistance more frequently benefited households experiencing moderate/high

lived poverty (61%) than those in other economic categories (41%-50%). Senior

citizens are particularly unlikely to report having received pandemic-related

assistance (35% of those aged 65 or older). More than half (55%) of citizens

say that COVID-19 relief was distributed “somewhat fairly” or “very fairly”

while 37% say the distribution was unfair (Figure 11).

Corruption related to

COVID-19 Despite expressing significant satisfaction with the fairness of

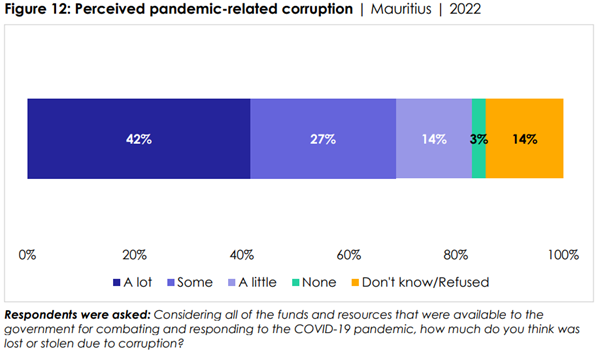

government relief assistance, more than two-thirds (69%) of Mauritians say

they believe that “some” or “a lot” of the resources intended for the

COVID-19 response have been lost to corruption (Figure 12). Only 3% think

that none of these resources have been embezzled.

Limit democratic freedoms

during a pandemic? Lockdowns and other pandemic-related restrictions in some

countries have raised questions about the extent to which citizens are

willing to forego certain freedoms, even temporarily, to protect public

health. In Mauritius, a solid majority (62%) of citizens “agree” or “strongly

agree” that it is justified for the government to use the armed forces or the

police to enforce public health mandates during an emergency like the

pandemic (Figure 13). When it comes to postponing elections during a public

health crisis, 45% consider this acceptable, while 37% “disagree” or

“strongly disagree.” But Mauritians overwhelmingly (79%) disapprove of

censoring media reporting during a public health emergency.

Looking ahead After

experiencing the COVID-19 pandemic, how prepared will Mauritius’ government

be to deal with future public health emergencies? More than half (52%) of

citizens think their government will not be prepared, including 28% who think

it will be “very unprepared” (Figure 14). Only 43% believe that the

government will be “somewhat” or “very” ready for the next public health

crisis.

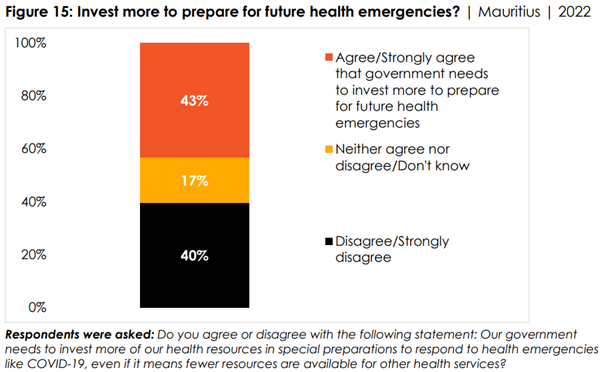

Mauritians are similarly

divided on whether the government needs to invest more in preparing for

future public health emergencies, even if it means that fewer resources are

available for other health services: 43% say yes, 40% say no (Figure 15).

Conclusion Afrobarometer

survey findings suggest that while the Mauritian government enjoys majority

approval of its overall COVID-19 response, it faces the challenge of public

distrust. Few citizens trust the government to ensure the safety of COVID-19

vaccines, and more than twothirds believe that “some” or “a lot” of the

resources intended to help with the pandemic were lost to corruption. These

concerns do not appear to have undermined vaccine uptake or citizens’

satisfaction with government relief efforts. But they are challenges to be

addressed now, rather than in the heat of the next public health emergency.

Similarly, questions about the government’s preparedness for future health

emergencies and the need to invest more health resources in preparing for

such crises require attention now. On both questions, Mauritians are far from

a consensus. 13 September 2022 WEST

EUROPE

759-760-43-09/Polls By 50% to 22% Britons are

disappointed that Liz Truss will be the next PM

Foreign secretary Liz Truss today was victorious