|

BUSINESS

& POLITICS IN THE WORLD GLOBAL

OPINION REPORT NO.756 Week: August 15 –August 21,

2022 Presentation: August 26, 2022 Support

For Restart Of Hamaoka Nuclear Power Plant In Japan Surges Sharply Online

Grocery Shopping Journey In Today's Economic Conditions In Turkey IRI’s

Most Recent Polling Found That 74% Of Iraq Is Distrust Political

Parties Nigerian

Women Face Persistent Disadvantages, Limited Support For Gender Equality Tanzanians

Overwhelmingly (77%) Endorse The Government’s Right To Collect Taxes Support

For Political Parties In South Africa, Two Years Before The Next National

Election Grocery

Price Inflation Hits New Peak As Brits Navigate £533 Annual Increase Two-Thirds

Say The Government Is Not Providing Enough Support On The Cost Of Living Nearly

Half Of Britons Agree That British Workers Need To Work Harder Gamescom

2022 – Digitalization And The Future Of Video Game Conventions Republicans

More Likely Than Democrats To See Politicians Without Government Experience

Positively Most

Republicans (64%) Say The Decision Of U S Military Exit From Afghanistan Was

Wrong Since

2011, 40% Or More Of U S Adults Have Identified As Political Independents In

Nearly Every Year 4

Out Of 10 Colombians Feel That They Lack Money At The End Of The Month CNC

Measured Support For The Names Of The Colombian President's Cabinet Canadians

Show Little Confidence In Hockey Canada Culture Change Amid Sex Abuse

Allegations Global

Consumer Confidence Continues Its Descent In August, A Survey Across 23

Countries INTRODUCTORY NOTE

756-43-23/Commentary:

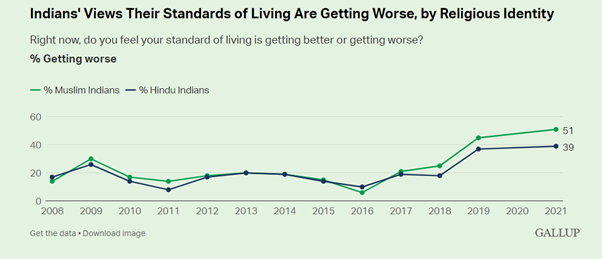

51%

Of Muslim Indians Say Their Standard Of Living Is Getting Worse, Compared

With 39% Of Hindu Indians

Seventy-five years after India's independence and

its partition into a predominantly Hindu India and predominantly Muslim

Pakistan, Gallup surveys in India show the country's large remaining Muslim

minority and its Hindu majority are living in two Indias. Over the past several years, both Muslim Indians and

Hindu Indians have been struggling more economically, but their economic pain

has not been evenly distributed, and Muslim Indians are far more pessimistic

about their future prospects. In 2021, a slim majority of Muslim Indians

(51%) said their standard of living was getting worse, compared with 39% of

Hindu Indians.

Muslim Indians have been the target of

discrimination and prejudice since Indian independence, despite legal

protections for the group. Discrimination and bias targeting the Indian

Muslim population have reportedly intensified in recent years, making the

group more susceptible to negative impacts from economic issues. For both groups, perceptions that standards of

living were worsening shot up between 2018 and 2019, as the Indian economy

entered a deep slowdown. Among Muslim Indians, the percentage jumped to 45%

in 2019, up from 25% the previous year. And among Hindu Indians, the

percentage saying the same hit 37% in 2019, an increase of 19 percentage

points from 2018. For much of Gallup's trend, there was a relatively

small gap between the two groups in perceptions that their living standards

were worsening. Until 2019, this area had no more than an eight-point gap.

The current 12-percentage-point gap between Muslim and Hindu Indians in

perceptions that living standards were getting worse is the largest in

Gallup's trend. Muslim Indians Have

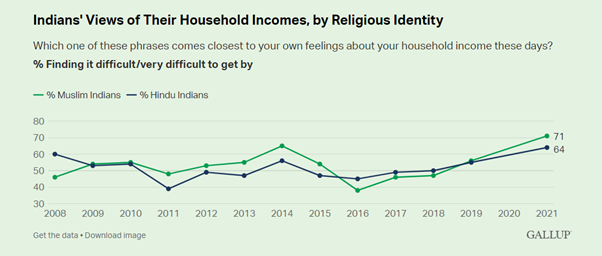

Tougher Time Making Ends Meet Clear majorities of both Muslim and Hindu Indians

say they are finding it difficult or very difficult to get by on their

present household incomes. However, Muslim Indians in 2021 were more likely

to say so than Hindu Indians, 71% vs. 64%. As with perceptions of the trajectory of standards

of living, views on household income have soured sharply since 2018. In 2018,

47% of Muslim Indians and 50% of Hindu Indians said they were finding it

difficult to get by; this jumped to 56% and 55%, respectively, in 2019 and

rose even more in 2021.

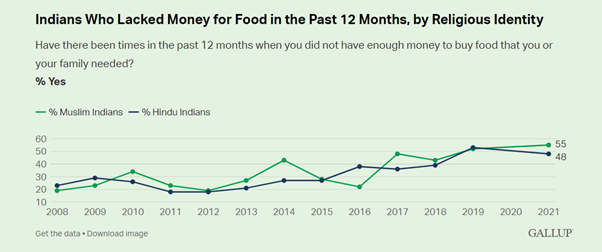

Muslim Indians Struggle

More to Afford Food In the face of rising inflation, sizable percentages

of Muslim Indians (55%) and Hindu Indians (48%) said there were times in the

past year that they did not have enough money to afford food, but Muslim

Indians were more likely to say so. As with the other two measures, Indians'

difficulties in this area have only intensified since the slowdown of India's

economy began in 2018 and the onset of the pandemic. In 2018, 43% of Muslim Indians and 39% of Hindu

Indians said they had lacked money for food at some point in the previous 12

months. This increased to 52% among Muslim adults and 53% among Hindu adults

in 2019. However, in 2021 there was a modest increase to 55% among Muslim

Indians and a decline to 48% for Hindu Indians.

Bottom Line The continued marginalization of Muslim Indians as

the country attempts to recover from the pandemic will likely impact the

country as a whole. There are roughly 200 million Indian Muslims, and failing

to address the economic pain they are disproportionately feeling may set the

stage for economic stagnation and political instability for years to come in

India. (Gallup) AUGUST 15, 2022 Source: https://news.gallup.com/poll/396887/economic-pain-uneven-india-muslim-hindu-populations.aspx SUMMARY

OF POLLS

ASIA

756-43-01/Polls Support For

Restart Of Hamaoka Nuclear Power Plant In Japan Surges Sharply

Here’s a turnup for the

books. Instead of being fiercely opposed to plans to restart the Hamaoka

nuclear power plant in Omaezaki, Shizuoka Prefecture, a rapidly

rising number of residents of nearby cities now embrace the project,

according to surveys by the municipalities. Opponents long outnumbered

those in favor of a restart as a result of the 2011 Fukushima nuclear

disaster triggered by the magnitude-9.0 Great East Japan Earthquake and the

towering tsunami it spawned. But local sensibilities

have undergone a sea change over recent uncertainties about the ability of

electric utilities to maintain stable power supplies during peak periods such

as during the blazing heat of summer and the frigid winter months. The three cities of

Kakegawa, Makinohara and Kikugawa canvass the opinions of residents annually

over moves to resume operations at the facility operated by Chubu

Electric Power Co. The detailed questions and answer options are

different depending on municipalities. The results of Kakegawa’s

study, released July 11, show that 24 percent of respondents said the

“reactors should be decommissioned” while 12 percent thought they should “be

continuously suspended.” This brought the total of local residents who view a

restart in negative terms at 36 percent. However, 33 percent

said the reactors “should be brought back online if their safety can be

assured.” In last

year’s survey, 32 percent and 13 percent, respectively, called for the

reactors’ decommissioning and continual suspension. Both figures were down this

year. The rate of support for a

restart was 29 percent in the previous poll, but this time the percentage

exceeded that of those in favor of decommissioning for the first time. “More young people today

have little knowledge of the accident at the Fukushima No. 1 nuclear power

plant, which explains the higher ratio of supportive individuals,” noted

Kakegawa Mayor Takashi Kubota. “The outcome was also no doubt influenced by

rising energy prices and Chubu Electric’s campaign to foster greater

understanding over the issue of a restart.” Makinohara made its

findings publicly available in June, revealing that 36 percent of respondents

backed the plant’s restart while 32 percent opposed it. It was the first time

for supporters to outnumber objectors since the surveys started in 2011. In Makinohara’s first

survey, those against had a more than 30-point advantage over

the support rate. The disparity remained as high as 10 points last year,

but the support ratio has now surged dramatically. “Factors behind the trend

are apparently hikes in electricity rates stemming from the war in Ukraine,

the strained power supply and people’s anxiety over calls for saving

electricity,” said Makinohara Mayor Kikuo Sugimoto. Kikugawa announced in June

that pro and against rates both stood at 38 percent for the first-ever such

result. Naysayers far outnumbered

supporters in all the three cities in the aftermath of the Fukushima nuclear

crisis. Though the difference began to shrink in the years that followed, the

disagreement ratio was still considerably higher until 2021. The mayors of the three

cities are cautious about the resumption of the reactors’ operations,

and the citizen survey results have been cited as one of the reasons for

their stances. Their approach may change

in the future, but municipal heads are still wary. “The current situation,

where the plan for reactor restarts has yet to gain the full approval of

residents, has not changed,” Kubota said. (Asahi Shimbun) August 15, 2022 Source:

https://www.asahi.com/ajw/articles/14687320 756-43-02/Polls 51% Of Muslim

Indians Say Their Standard Of Living Is Getting Worse, Compared With 39% Of

Hindu Indians

Seventy-five years after India's independence and

its partition into a predominantly Hindu India and predominantly Muslim

Pakistan, Gallup surveys in India show the country's large remaining Muslim

minority and its Hindu majority are living in two Indias. Over the past several years, both Muslim Indians and

Hindu Indians have been struggling more economically, but their economic pain

has not been evenly distributed, and Muslim Indians are far more pessimistic

about their future prospects. In 2021, a slim majority of Muslim Indians

(51%) said their standard of living was getting worse, compared with 39% of

Hindu Indians.

Muslim Indians have been the target of

discrimination and prejudice since Indian independence, despite legal

protections for the group. Discrimination and bias targeting the Indian

Muslim population have reportedly intensified in recent years, making the

group more susceptible to negative impacts from economic issues. For both groups, perceptions that standards of

living were worsening shot up between 2018 and 2019, as the Indian economy

entered a deep slowdown. Among Muslim Indians, the percentage jumped to 45%

in 2019, up from 25% the previous year. And among Hindu Indians, the

percentage saying the same hit 37% in 2019, an increase of 19 percentage

points from 2018. For much of Gallup's trend, there was a relatively

small gap between the two groups in perceptions that their living standards

were worsening. Until 2019, this area had no more than an eight-point gap.

The current 12-percentage-point gap between Muslim and Hindu Indians in

perceptions that living standards were getting worse is the largest in

Gallup's trend. Muslim Indians Have

Tougher Time Making Ends Meet Clear majorities of both Muslim and Hindu Indians

say they are finding it difficult or very difficult to get by on their

present household incomes. However, Muslim Indians in 2021 were more likely

to say so than Hindu Indians, 71% vs. 64%. As with perceptions of the trajectory of standards

of living, views on household income have soured sharply since 2018. In 2018,

47% of Muslim Indians and 50% of Hindu Indians said they were finding it

difficult to get by; this jumped to 56% and 55%, respectively, in 2019 and

rose even more in 2021.

Muslim Indians Struggle

More to Afford Food In the face of rising inflation, sizable percentages

of Muslim Indians (55%) and Hindu Indians (48%) said there were times in the

past year that they did not have enough money to afford food, but Muslim

Indians were more likely to say so. As with the other two measures, Indians'

difficulties in this area have only intensified since the slowdown of India's

economy began in 2018 and the onset of the pandemic. In 2018, 43% of Muslim Indians and 39% of Hindu

Indians said they had lacked money for food at some point in the previous 12

months. This increased to 52% among Muslim adults and 53% among Hindu adults

in 2019. However, in 2021 there was a modest increase to 55% among Muslim

Indians and a decline to 48% for Hindu Indians.

Bottom Line The continued marginalization of Muslim Indians as

the country attempts to recover from the pandemic will likely impact the

country as a whole. There are roughly 200 million Indian Muslims, and failing

to address the economic pain they are disproportionately feeling may set the

stage for economic stagnation and political instability for years to come in

India. (Gallup) AUGUST 15, 2022 Source: https://news.gallup.com/poll/396887/economic-pain-uneven-india-muslim-hindu-populations.aspx 756-43-03/Polls Online Grocery

Shopping Journey In Today's Economic Conditions In Turkey

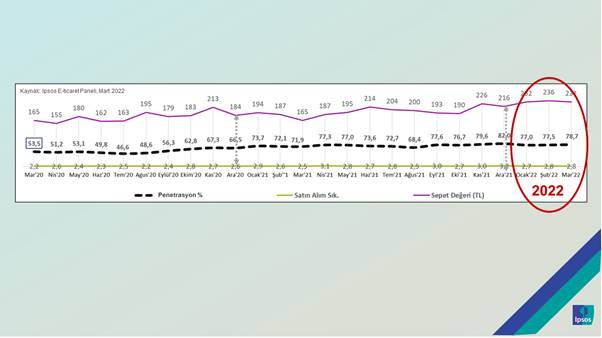

According to the Ipsos

E-Commerce Panel April'21-March'22 data, online shoppers paid 210 TL for each

basket while shopping an average of 2 times a month. When we compare the

general online shopping behaviors with the previous 12-month period, we see

that the number of preferred channels has increased from 6 to 7 and the

number of categories from 12 to 17 recently. Online shoppers paid an

average of 92 TL to a shopping cart while shopping for FMCG approximately 1

time per month during the period April'21-March'22. When we compare FMCG

shopping behavior with the previous 12-month period, the number of categories

purchased increases from 7 to 10. In summary, online transformation manifests

itself not only with the increase in the number of shoppers, but also as a

diversity of channels and categories.

Online

shopping provides practicality and time saving, as well as supporting the

budget with campaigns specific to online sites. In the ranking of the most

important reasons for choosing online shopping, campaigns specific to online

sites are in the first place both last year and this year. Last year, the

"desire to shop for confidence in the pandemic" was immediately

followed by it, but this year, with the changing agenda, this need is not in

the top five.

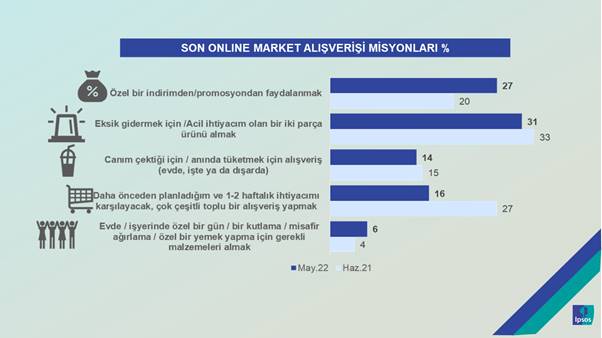

Economic

impacts have recently shaped the shopping mission. Those who say that the

last online shopping mission is to benefit from a special discount and

campaign are increasingly one of the main motivations with the mission of

eliminating the deficiency. The mass shopping mission is lower this period. Shopping online to consume

instantly is a more common behavior among young people.

Peki

ne olursa online alışverişçiler fiziksel market yerine online

alışverişi daha çok kullanacaklarını

söylüyorlar? Online

alışverişçiler haftalık alışverişlerinin

içinde hala fiziksel market alışverişine de büyük yer

ayırıyorlar. Online kanal kullanımlarının 1,5

katı sıklıkta fiziksel kanallardan alışveriş

yapılıyor. Fiziksel alışveriş

sıklığını arttıranlar özellikle de

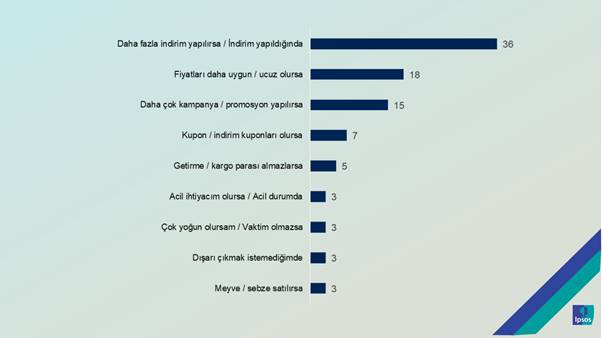

erkekler. Mevcuttan daha sık

online alışveriş yapmanın baş şartı daha

fazla indirim, daha uygun fiyatlar, daha fazla kampanya. Tüketiciler mevcut

ekonomik şartlarda online kanallardan bütçelerine daha fazla destek

bekliyor. Fiyat indirimi, kampanya, promosyon, indirim kuponu gibi ceplerini

etkileyen nedenleri dile getirenler online alışverişçilerin

toplamda %65’ini oluşturuyor.

Ipsos,

Turkey CEO Sidar Gedik made the following evaluations about the data; It's

been a long time since online shopping stopped being a question mark. Let's

not forget that the most valuable company in the world is Amazon. On the other hand, while

digitalization in the shopping world is advancing at its natural pace in its

own path, the Covid-19 outbreak and the quarantine practices it has brought

have suddenly caused a gear increase. During the "Stay at Home"

period, the last barriers in the minds of our country's consumers began to

break down and the proportion of online shoppers increased exponentially. As the months progressed,

we saw that this level of online shopping volume was not temporary, and we

did not abandon online shopping when we started to shop at home. In March 2020, 54% of

individuals using the internet were shopping online, and by 2022, this rate

has increased 1.5 times, and eight out of every ten internet users are now

shopping online. In the pre-pandemic

period, while online shoppers were more limited in the fast-moving consumer

goods category, we saw significant increases here with the pandemic. It

should be said that there is a stable picture in this category. Why is it that online

shopping continues to be popular even though the pandemic conditions are

over? When we examine the reasons for preference of consumers, we see that

promotions / campaigns stand out. One of the leading reasons is to be able to

shop more affordably thanks to the possibility of more convenient price

comparison during online shopping. Promotional, more affordable, affordable

shopping... From this point of view, we can state that online shopping is a

method of combating economic difficulties for consumers. Online retailers have

been, and continue to be, a lifeline to consumers, first in the pandemic and

then in the era of high inflation. (Ipsos Turkey) 15 August 2022 Source:

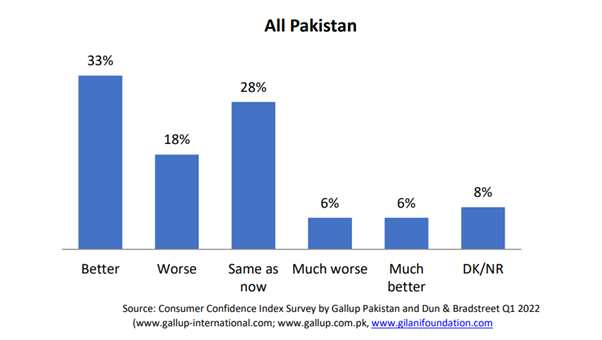

https://www.ipsos.com/tr-tr/gunumuz-ekonomik-sartlarinda-online-market-alisveris-yolculugu 756-43-04/Polls 39% Pakistanis

Are Hopeful That Their Household’s Financial Situation Will Improve In The Next 6 Months

According to

Dun&Bradstreet and Gallup Pakistan Consumer Confidence Index, 39%

Pakistanis are hopeful that their household’s financial situation will

improve in the next 6 month. A nationally representative sample of adult men

and women from across the four provinces was asked the following question,

“How is your household’s financial situation in comparison to last 6 months?”

In response to this question, 18% said ‘worse’, 33% said ‘better’, 28% said

‘same as before’, 6% said ‘much worse’ and 6% said ‘much better’. Gallup

Pakistan and D&B Consumer Confidence Index is a quarterly report tracking

the pulse of consumers in Pakistan. The report is produced since 2020 and all

8 reports are available on demand. Please write to Bilal I Gilani, Executive

Director Gallup Pakistan: bilal.gilani@gallup.com.pk The full report of

Gallup Pakistan and D&B Consumer Confidence Index Q1 2022 can be found on

this link: https://gallup.com.pk/post/33476 Question: “What do you expect

your household’s financial situation to be in next 6 months?

(Gallup Pakistan) August 19, 2022 Source:

https://gallup.com.pk/wp/wp-content/uploads/2022/08/August-19-english.pdf MENA

756-43-05/Polls IRI’s Most

Recent Polling Found That 74% Of Iraq Is Distrust Political Parties

Since 2003, Iraq has faced numerous challenges in

its democratic transition. Despite this, Iraqis have demonstrated remarkable

resilience and a commitment to democracy. This was clearly seen in the 2019

Tishreen (October) Movement, an unprecedented wave of demonstrations against

endemic corruption, sectarianism, lack of public services and jobs, and

malign foreign influence. The youth-led movement called for early elections

to bring an end to the dominate post-2003 political class. In response to pressure

from the streets, the Iraqi government enacted several reforms aimed at

placating protesters, including overhauling the country’s electoral system. This

new electoral framework moved Iraq to a single, nontransferable vote system

based on multi‐seat constituencies – a shift that created a window of

opportunity for independent candidates and could make members of Parliament

(MPs) more accountable. Despite the new framework,

there has been a gradual erosion of confidence in Iraq’s political parties

and an increase in anti-establishment sentiment as prominent parties have

demonstrated they are unwilling and unable to address basic citizen concerns.

The International Republican Institute’s (IRI) most

recent polling, which was fielded prior to the parliamentary

elections, found that 74% of Iraqis distrust political parties. This

repudiation of the political status quo coupled with electoral law changes

enabled political outsiders to present themselves as serious contenders in

the most recent elections on October 10, 2021. One of the noteworthy

results was the success of independent candidates who were active in the

Tishreen protests, and, despite some ideological differences, share many

common goals – chief among them, addressing citizen demands. Seven-hundred

eighty-four independent candidates ran in the elections, attaining over 1.6

million votes (19% of the total valid votes), and winning 43 seats in

Parliament. While not all 784 candidates can be considered truly independent,

as incumbent parties sought to exploit the electoral law changes and run

candidates that held secret political affiliations, the majority are

independent and mobilized voters largely because of their political

impartiality. In comparison, just three independents won parliamentary seats in

Iraq’s 2018 elections. Post-elections, Iraq’s

Council of Representatives now has a small, but significant contingent of

independents. In other contexts, the emergence of independent MPs can signify

a splintering of parliament, as strong, large parties are needed to form

majority governments and create an opposition/majority dynamic. However, in

Iraq, independent, reform-minded MPs represent a step toward rebuilding a

credible political process. While independent MPs do not have the resources

enjoyed by large parties, they can still serve as credible voices, amplifying

their constituents’ concerns and holding fellow MPs accountable. Though independent MPs are

considered more credible simply because they are anti-establishment, Iraqis

remain skeptical of politicians at large, and because many of these MPs are

“first-timers,” they do not yet have an established track record to draw upon

to deepen this credibility. Understanding this, IRI is working to bring civil

society organizations (CSOs) and independent, reform-minded MPs together to

identify key community issues and create a roadmap for solving them through

joint initiatives. A chairwoman of a local CSO, who attended an IRI

roundtable discussion with CSO representatives and newly elected MPs in

January 2022, said of the importance of civil society-government engagement,

“Our shared goal [with the MPs] of enhancing democracy and people’s

involvement in monitoring the government obligates us to work together to

mobilize public opinion and raise awareness regarding the issues we agree

need to be addressed [in our communities].” Nine months after the

elections, bitter disputes between entrenched political parties have

paralyzed Iraq’s government formation. Independent MPs now have an

opportunity to work with nascent, reform-minded parties to earn their

constituents’ trust by pushing through key citizen-centered legislation. As

their credibility grows, these MPs will diversify Iraq’s political sphere and

rebuild trust in political parties. IRI will continue to support civil

society as they engage with willing, reform-minded partners in government to

address citizen demands. If concerns are heard and good-faith efforts are

made to respond, Iraqis’ trust in the political process will improve, which

will increase voter turnout in future elections and strengthen reformers’

voices within Iraqi institutions. (International Republican Institute) August 19, 2022 Source:

https://www.iri.org/news/iraqs-parliament-how-independents-are-contributing-to-political-pluralism/ AFRICA

756-43-06/Polls Nigerian Women

Face Persistent Disadvantages, Limited Support For Gender Equality

The United Nations

Sustainable Development Goals (SDGs) describe gender equality as “not only a

fundamental human right, but a necessary foundation for a peaceful,

prosperous, and sustainable world” (United Nations, 2022). Highlighted as SDG

5, it is also a cross-cutting principle underlying most of the other goals in

pursuit of development whose benefits are enjoyed equally by women and men.

In Nigeria, gender equality remains a challenge despite some government

efforts to address it, including the Better Life for Rural Women Programme

and the creation of the Federal Ministry of Women Affairs and Social

Development (National Population Commission, 2014). In addition to

traditional rules and practices that treat men preferentially (Adeosun &

Owolabi, 2021), the country’s male-dominated Parliament has repeatedly

rejected or failed to act upon proposed legislation to promote women’s

rights. Most recently, in March 2022, the National Assembly voted down five

bills aimed mostly at increasing women’s political leadership opportunities,

prompting public protests in several cities (Premium Times, 2022). The

Federal Executive Council approved a revised National Gender Policy in March

designed to promote gender equality, good governance, and accountability

across the country’s three tiers of government (Guardian, 2022), though it

awaits implementation. This dispatch reports on a special survey module

included in the Afrobarometer Round 9 (2021/2022) questionnaire to explore

Africans’ experiences and perceptions related to gender. (For findings on

gender-based violence, see Mbaegbu & Duntoye, 2022.) In Nigeria, survey

findings show that women remain at a disadvantage compared to men when it

comes to hiring, land ownership, control over key assets, and participation

in household financial decisions. Popular support for gender equality is

limited, especially among men. While most citizens say women should have the

same chance as men of being elected to public office, many also consider it

likely that female candidates will suffer criticism and harassment. Most

Nigerians say the government is doing a poor job of promoting women’s rights

and opportunities. Afrobarometer surveys Afrobarometer is a pan-African, nonpartisan

survey research network that provides reliable data on African experiences

and evaluations of democracy, governance, and quality of life. Eight rounds

of surveys have been completed in up to 39 countries since 1999. Round 9

surveys (2021/2022) are currently underway. Afrobarometer conducts

face-to-face interviews in the language of the respondent’s choice. The

Afrobarometer team in Nigeria, led by NOIPolls, interviewed a nationally

representative, random, stratified probability sample of 1,600 adult Nigerians

between 5 and 31 March 2022. A sample of this size

yields country-level results with a margin of error of +/-2.5 percentage

points at a 95% confidence level. Previous standard surveys were conducted in

Nigeria in 2000, 2003, 2005, 2008, 2013, 2015, 2017, and 2020. Key findings § Survey findings show significant gender imbalances in

Nigerian society: o Women are less likely than men to have post-secondary

education (17% vs. 29%) and more likely than men to have no formal schooling

(20% vs. 12%). o Women are less likely than men to own assets such as a

mobile phone (73% vs. 87%), a bank account (51% vs. 68%), and a motor vehicle

(14% vs. 40%). o Women are less than half as likely as men to say they have

control over how household money is spent (22% vs. 56%). § Slim majorities

say women should have the same rights as men to get a paying job (53%) and to

own and inherit land (51%). Men are far less likely than women to endorse

gender equality in hiring and land rights. § Fewer than half

of Nigerians say that in practice, women enjoy equal rights when it comes to

getting a job (43%) and owning/inheriting land (30%). § Six in 10

Nigerians (61%) say women should have the same chance as men of being elected

to public office. o But while about eight in 10 citizens (79%) think a woman

will gain standing in the community if she runs for office, almost half (47%)

say it’s likely she will be criticised or harassed, and 38% say she will

probably face problems with her family. § Only one-fourth

(26%) of citizens say the Nigerian government is performing “fairly well” or

“very well” in promoting equal rights and opportunities for women. More than

half (54%) say the government should do more to advance gender equality.

Education and control of assets While Nigerian women are just as likely as

men to have secondary schooling (44% of women vs. 43% of men) or primary

schooling (19% vs. 17%), they trail significantly when it comes to

post-secondary education. While three in 10 men (29%) have attained some

level of tertiary education, the same is true for just 17% of women (Figure

1). Women are more likely than men to lack formal education altogether (20%

vs. 12%). Women are also considerably less likely than men to claim personal

ownership of key household assets. Fewer women than men say they own a mobile

phone (73% vs. 87%), a bank account (51% vs. 68%), a radio (46% vs/ 76%), a

television (43% vs. 57%), a motor vehicle (14% vs. 40%), and a computer (9%

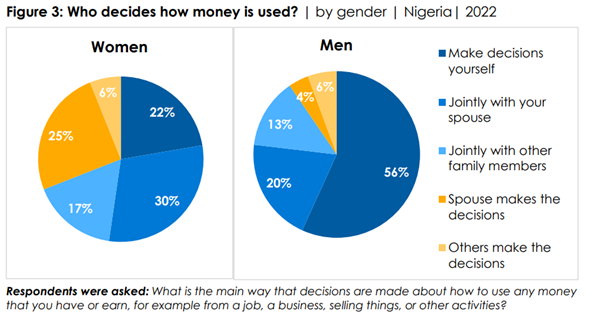

vs. 14%) (Figure 2). When it comes to who makes decisions about how household

money is spent, women are less than half as likely as men to say they make

the decisions themselves (22% vs. 56%) (Figure 3). More women than men report

that they make such decisions jointly with their spouse (30% vs. 20%) or

jointly with other family members (17% vs. 13%). Women are three times as

likely as men to say that the spouse or others make the decisions (31% vs.

10%), leaving them without a voice in household financial decisions.

Rights to a job and land Do Nigerians want gender

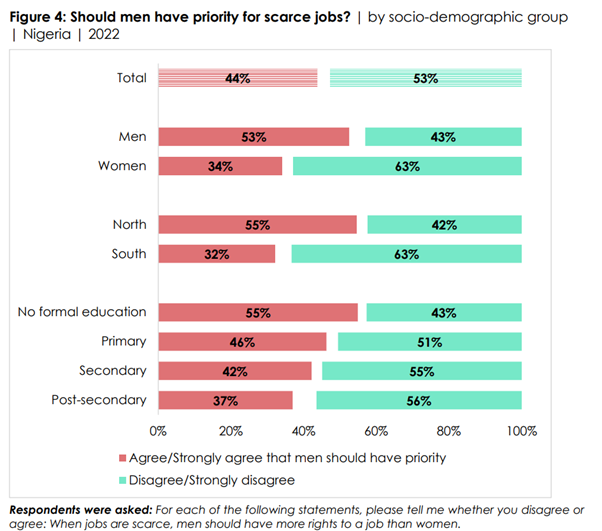

equality when it comes to jobs and land? And if so, how close to equality are they? More than four in 10

Nigerians (44%) say that men should be given priority over women in hiring when jobs are

scarce, while 53% reject this form of gender discrimination (Figure 4). Men (43%) trail women

(63%) in prioritising equality in hiring, as do Northerners (42%) compared to Southerners

(63%). Support for equality increases with respondents’ education level, ranging from 43% of

those with no formal schooling to 56% of those with post-secondary

qualifications.

Only a slim majority (51%)

of Nigerians think women should have the same rights as men to own and

inherit land. Here, too, men are much less likely than women to believe in

equality (39% vs. 64%) (Figure 5).

Given less-than-solid

support for gender equality in hiring and land ownership, it may not be

surprising that a majority of Nigerians report that in practice, women do not

enjoy the same rights as men. Only 43% of citizens say women have the same

chance as men to get a paying job, and even fewer (30%) see equality when it

comes to owning and inheriting land (Figure 6). Perceptions of gender

equality differ significantly by demographic group. Women are less likely

than men to report equal opportunities in hiring (39% vs. 47%), though they

are actually more likely than men to say they enjoy the same rights to land

ownership and inheritance (32% vs. 27%);. Similarly, Northerners are less

likely than Southerners to say women enjoy equal rights in hiring (38% vs.

49%) but more likely to see land rights as equal (34% vs. 25%). While rural

and urban residents differ little on these questions, younger adults are less

likely to perceive gender equality in hiring their elders. Respondents with

no formal education are most likely to perceive gender equality in land

ownership (42%) and least likely to see job opportunities as equal (34%).

Finally, poor citizens are less likely to think women enjoy equal

opportunities to get a job (40%- 42%) than their better-off counterparts

(51%-53%).

In our country today,

women and men have equal opportunities to get a job that pays a wage or

salary. In our country today, women and men have equal opportunities to own

and inherit land. (% who “agree” or “strongly agree”) Gender equality in

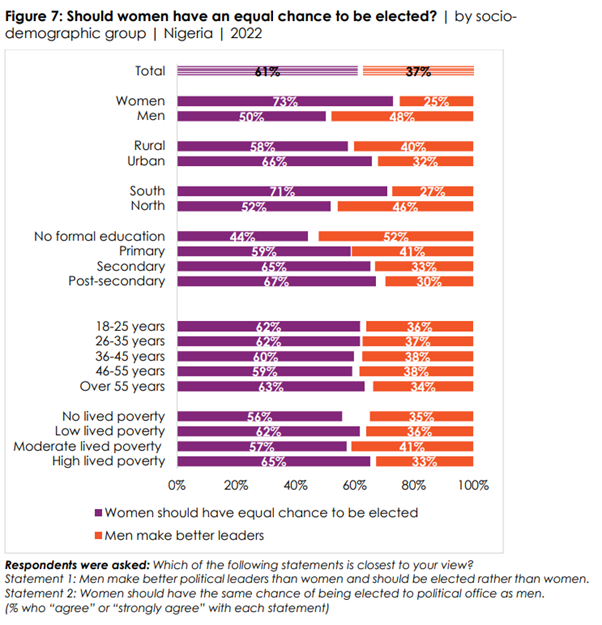

political participation Most strategies for achieving gender equality call

for more women in political leadership. In Nigeria, more than six in 10

citizens (61%) citizens say women should have the same chance as men to be elected

to public office, rejecting the idea that men make better political leaders

and should thus be given priority as candidates (Figure 7). But far fewer men

(50%) than women (73%) support gender equality in politics. And residents in

rural areas (58%) and the North (52%) trail their counterparts in cities

(66%) and the South (71%) in endorsing equal rights for female candidates.

Support for equality increases with respondents’ education level, ranging

from just 44% among citizens with no formal schooling to 67% among those with

post-secondary qualifications.

Even if she believes that

voters will give her the same consideration as a male candidate, a woman may

examine potential consequences before deciding to toss he hat in the ring.

Close to eight in 10 Nigerians (79%) say it is “somewhat likely” or “very likely”

that a woman and her family will gain standing in the community if she runs

for elected office (Figure 8). But findings are more mixed on other potential

consequences. Almost half (47%) of respondents consider it likely that others

in the community will criticise her, call her names, or harass her for

seeking public office, while 38% think she might face problems with her

family. The fact that slim majorities see it as unlikely that a woman will

face community criticism/harassment (51%) or family problems (59%) as a

result of running for office may or may not be enough to overcome some

women’s reservations about contesting.

Government performance in

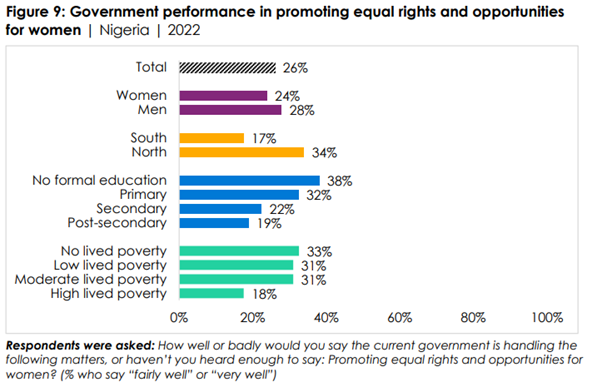

promoting equal rights and opportunities Only one-fourth (26%) of Nigerians

say their government is doing a “fairly” or “very” good job of promoting

equal rights and opportunities for women (Figure 9), while 70% disapprove of

the government’s performance. Men (28%) are more likely than women (24%) to

give the government a passing grade on gender equality. Approval ratings are

higher in the North than in South (34% vs. 17%) and vary by respondents’

education and economic levels. Citizens with at least a secondary education

(19%-22%) are much less likely to be satisfied with the government’s efforts

than those with primary (32%) or no formal education (38%). On the other

hand, only 18% of citizens experiencing high levels of lived poverty approve

of the government’s efforts on gender equality, compared to 31%- 33% of

better-off respondents.

In line with their negative

ratings of the government’s performance, more than half (54%) of citizens

think the government could do “somewhat more” or “much more” to promote equal

rights and opportunities for women. About one in seven (15%) say the

government is doing about the right amount, while 29% say it should reduce

its gender-equality efforts. Women and men offer similar appraisals of the

government’s level of effort (Figure 10).

Conclusion Survey findings

show that in Nigeria, women remain at a distinct disadvantage when it comes

to education, control over assets, and financial decision-making. And while

slim majorities endorse gender equality in hiring and land ownership, most

Nigerians acknowledge that this is not the reality. Giving women a fair shot

at being elected to public office wins majority support, but at the same

time, a significant segment of the population think women may face problems

in the community and at home if they run for office. Citizens overwhelmingly

give the government a poor grade on its efforts to promote gender equality,

and a majority say more needs to be done. But that may require the engagement

of more citizens who support and demand equal rights and opportunities for

women in employment, land ownership, political leadership, and other fields. 16 August 2022 756-43-07/Polls Tanzanians

Overwhelmingly (77%) Endorse The Government’s Right To Collect Taxes

Paying

taxes is a fundamental civic duty meant to be exercised by citizens for their

welfare and

national development (Prichard, 2010). Tax revenues account for more than 85%

of Tanzania’s

domestic revenues and about 70% of government expenditures (Bank of Tanzania,

2021). The

government has initiated several measures to improve tax compliance,

including updating

tax-collection technology, enhancing outreach of tax services and education

to the

public, restructuring the Tanzania Revenue Authority, and strengthening

enforcement measures

(Mzalendo & Chimilila, 2020). The government recently introduced a tax on

mobile-money

transactions, whose proceeds are intended to support the improvement of social-services

delivery, including the construction of classrooms and health centres, particularly

in underserved areas (Mshomba, 2021). Afrobarometer survey findings show that most

Tanzanians see tax collection as legitimate and believe that the government uses tax

revenues for the well-being of its citizens. Yet a majority report that citizens “often” or

“always” avoid paying their taxes, and most say it is difficult to know what taxes and fees they

are supposed to pay and how government uses tax revenues. Tanzanias

are divided on whether they favour higher taxes to support more government services,

but a large majority say they would welcome higher taxes to fund programmes targeting

young people. Afrobarometer

surveys Afrobarometer

is a pan-African, nonpartisan survey research network that provides reliable data

on African experiences and evaluations of democracy, governance, and quality

of life. Eight

rounds of surveys have been completed in up to 39 countries since 1999. Round

9 surveys

(2021/2022) are currently underway. Afrobarometer conducts face-to-face

interviews in the

language of the respondent’s choice. The

Afrobarometer team in Tanzania, led by REPOA, interviewed a nationally

representative sample

of 2,398 adult Tanzanians in March 2021. A sample of this size yields

country-level results

with a margin of error of +/-2 percentage points at a 95% confidence level.

Previous surveys

were conducted in Tanzania in 2001, 2003, 2005, 2008, 2012, 2014, and 2017. Key

findings Tanzanians overwhelmingly (77%)

endorse the government’s right to collect taxes. Yet

almost half (46%) say people in the country “often” or “always” avoid paying

their taxes.

Two-thirds (65%) of Tanzanians say it is “difficult”

or “very difficult” to find out what taxes and fees they are supposed to pay.

And even more (70%) report that it is hard to find out how the government

uses the tax

revenues it collects. o Even

so, 76% of citizens say the government generally uses tax revenues for the well-being

of its citizens.

Strong majorities say it is fair to tax rich people at higher rates than

ordinary citizens (69%),

but also that small traders and others in the informal sector should be made

to pay

taxes on their businesses (68%).

More Tanzanians think that tax rates for both ordinary people and the rich

are “about right”

than say they are too low or too high.

Citizens are about evenly divided as to whether it would be better to pay

higher taxes

if it meant more government services (46%) or to pay lower taxes with fewer services

(49%).

But two-thirds (66%) endorse paying higher taxes to support programmes to

help young

people. Support

for taxationMore than three-quarters (77%) of Tanzanians “agree” or “strongly

agree” that tax authorities always have the right to collect taxes

(Figure 1).

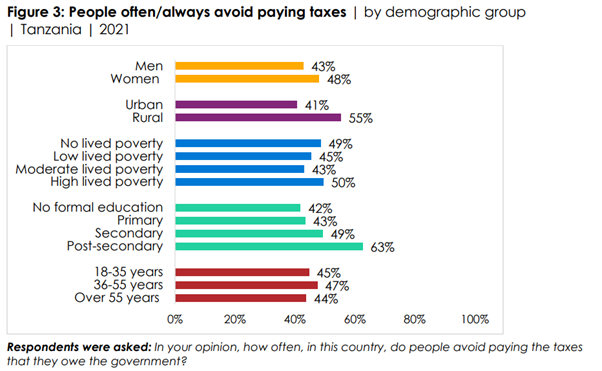

Frequency of tax evasion Despite their

endorsement of taxation, almost half (46%) of Tanzanians say people “often”

or “always” avoid paying the taxes they owe the government. The same

proportion (46%) say this “never” or “rarely” happens (Figure 2). Respondents

with post-secondary education (63%) are more likely to believe that people

often evade their taxes than their less educated counterparts (42%-49%), as

are urban residents (55%) compared to rural residents (41%). Differences by

gender, age, and economic status are small (Figure 3).

Access to tax information Among potential

barriers to tax compliance may be uncertainty about which taxes and fees one

is supposed to pay and a lack of knowledge about how the government uses tax

revenues. Tanzanians pay a variety of taxes, both directly and indirectly.

These include income tax, corporate tax, pay-as-you-earn (PAYE) taxes, export

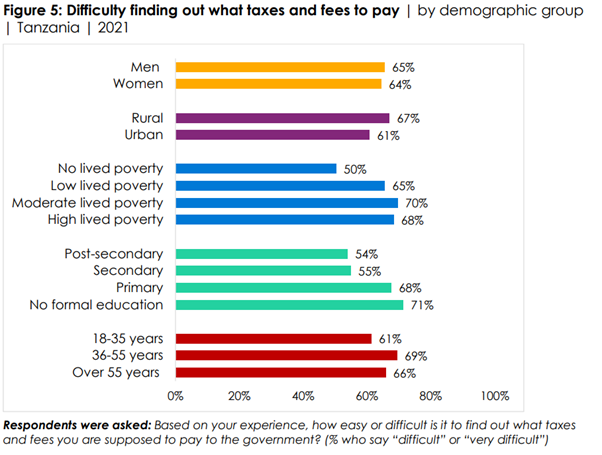

and import taxes, and value-added tax. Two-thirds (65%) of Tanzanians say it

is “difficult” or “very difficult” to find out what taxes and fees they are

supposed to pay to the government. Only 29% see it as easy, while 6% say they

“don’t know” (Figure 4). Rural residents (67%) and citizens with no formal

education (71%) or only primary schooling (68%) are particularly likely to

report difficulties in finding out what taxes and fees they owe (Figure 5). Young

and economically better-off respondents1 report fewer difficulties.

Similarly, seven in 10 respondents (70%) say it is “difficult” or “very

difficult” to find out how the government uses the tax revenues it collects

(Figure 6). Difficulties in determining how the government spends taxpayers’

money are especially common among rural residents (72%), citizens

experiencing moderate or high lived poverty (72%-75%), and those with primary

education or less (69%-72%) (Figure 7).

Despite

limited information about which taxes to pay and how the government uses its

tax revenues,

more than three-quarters (77%) of respondents believe that the government generally uses collected taxes for the

well-being of its citizens (Figure 8).

Views on levels of taxation In addition,

seven in 10 respondents (69%) “agree” or “strongly agree” that it is fair to

tax rich people at higher rates than ordinary citizens to help pay for

government programs to benefit the poor (Figure 9). Nonetheless, more than

two-thirds (68%) of respondents also say that the government should make sure

that small traders and other people working in the informal sector pay taxes

on their businesses.

Tanzanians are divided in their views on

taxation levels, but pluralities say ordinary citizens and rich people both

pay “about the right amount”of taxes (Figure 10). Only 33% think ordinary

people pay too much, and just 13% say wealthy people pay too little in taxes.

Tanzanians are also sharply divided as to

whether it would be better to pay higher taxes if it meant more services from

the government (46%) or to pay lower taxes with fewer services (49%) (Figure

11). Poor citizens (38%) and those with no formal education (36%) are least

likely to favour paying higher taxes in exchange for more government

services.

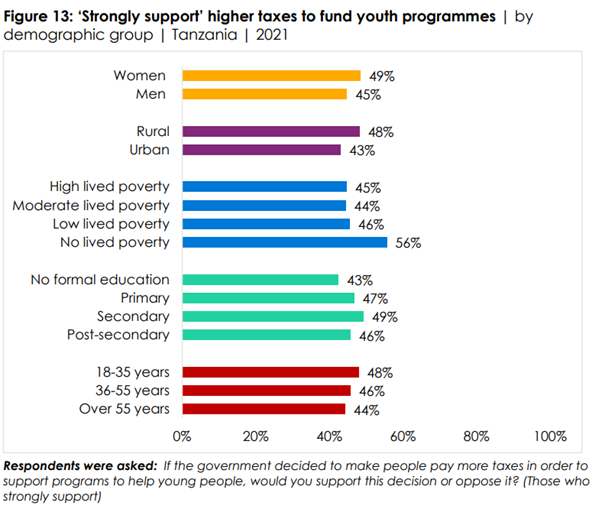

However, two-thirds (66%) of Tanzanians say

they would support paying higher taxes to support programmes to help young

people. Almost (47%) say they would “strongly support” such an initiative

(Figure 12). “Strong support” for higher taxes to fund youth programmes is

especially common among wealthy respondents (56%) and rural residents (48%)

(Figure 13).

If the

government could increase its spending on programmes to help young people, Tanzanians

say they would prioritise job-creation initiatives (cited by 37% of

respondents), followed

by education (22%), business loans (22%), job training (10%), and social

services for youth (9%). Conclusion Most

Tanzanians say the government has the right to collect taxes. But almost half

also report that

citizens frequently avoid paying their taxes, and a majority say it is

difficult to find out what

taxes they owe and how tax revenues are used. While stronger enforcement of

tax compliance may be one response, these findings also point to a need to

improve information flow to taxpayers and transparency by the government. Any

proposal to raise taxes appears likely to generate lively public debate

unless the purpose is to help young people – a priority on which a majority

of citizens agree 17

August 2022 756-43-08/Polls Support For

Political Parties In South Africa, Two Years Before The Next National

Election

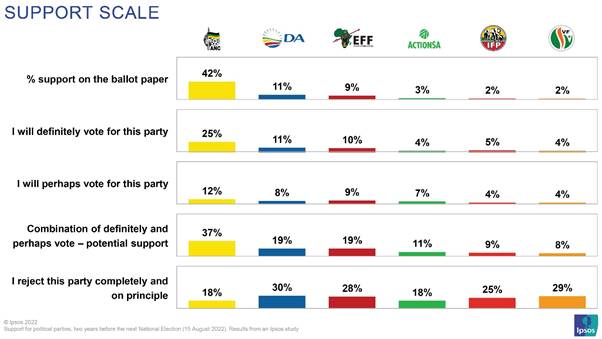

When it comes to the

question “If there were national elections

tomorrow, which political party or organisation will you vote for?”,

the interviewer hands the electronic interviewing device to the respondent

who can then indicate his/her choice of political party on a page resembling

a ballot paper, in an imitation of a secret vote. We believe this aids

respondents to give honest answers, without influence from others, and it

empowers those in very traditional, prescriptive or paternalistic households

to express their own opinions. However, this long before

an election it can be very informative to look at one of the other questions

in the study. Ipsos asks all respondents to give an opinion on each of six

political parties. Seven different opinions

are put to respondents. These seven opinions encompass a spectrum of views,

from “I reject this party completely and

on principle” to “I will

definitely vote for this party” – with five other opinions

in-between. Respondents also have the opportunity to say that they do not

know the party and therefore they can’t express an opinion .

Looking at the combination

of the “definitely vote” and “perhaps vote” opinions, all political

parties, except the ANC, show a healthy potential support - more than that

received on the ballot papers. These results should be motivating to all

opposition parties in the sense that their messages potentially have a much

larger resonance with the electorate than shown by the straightforward “who

would you vote for” question. The question, however,

will be how to translate this latent support into actual votes. “As an opposition political party, you need to prove

you are a credible alternative without complaining about everything the

government does or does not do. Provide voters with other workable

alternatives and be another option – a political party needs to be a positive

force, this attracts support”, says Mari Harris, Ipsos SSA Knowledge

Director. 15 August 2022 Source:

https://www.ipsos.com/en-za/support-political-parties-two-years-next-national-election WEST

EUROPE

756-43-09/Polls Grocery Price Inflation

Hits New Peak As Brits Navigate £533 Annual Increase

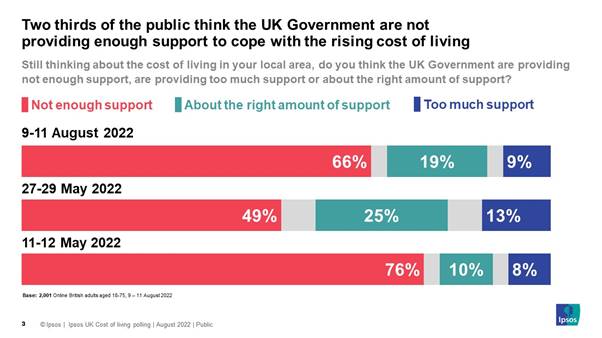

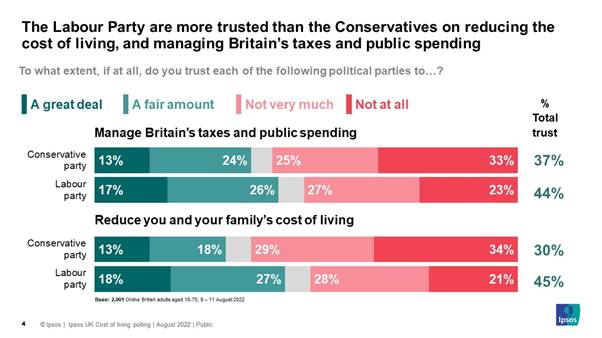

16 August 2022 756-43-10/Polls Two-Thirds Say The

Government Is Not Providing Enough Support On The Cost Of Living

Slightly more Britons say they trust the Labour

party to manage Britain’s taxes and public spending than the Conservative

party, however both are trusted by minorities. While 44% say they trust

Labour to look after taxes and public spending (an increase from 35% last

month but in line with levels seen earlier in the year), 37% say the same for

the Conservatives. The gap is even wider when it comes to reducing people’s

cost of living. Forty-five per cent trust Labour to reduce their/their family’s

cost of living, while 3 in 10 (30%) say the same for the Conservatives. This

includes the majority (55%) of 2019 Conservative voters saying they do not

trust the Conservatives on the cost of living.

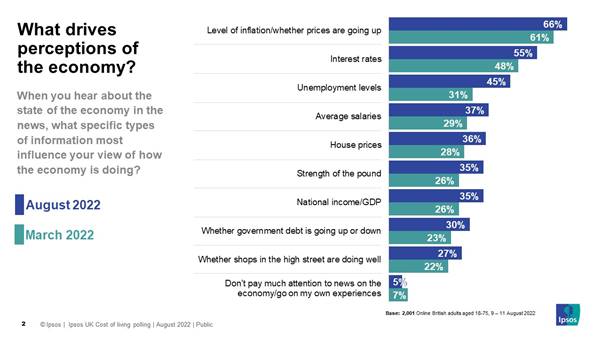

When it comes to perceptions of the economy,

people’s views are most likely to be influenced by news about levels of

inflation/whether prices are going up (66%, +5 since March) or interest rates

(55%, +7). Just under half are influenced by news about unemployment rates

(45%) but this has risen from nearer three in ten (31%) in March.

Trinh Tu, Managing

Director of Public Affairs at Ipsos in the UK, said: As the cost of living

continues to rise, it will come as no surprise to see high levels of the

public saying the government is not providing enough support.

What is notable is the rising levels of dissatisfaction with the

government among Conservative voters. The Labour party are now pulling ahead

as the party most trusted to reduce the cost of living and manage Britain’s

taxes and public spending, but still only by a minority, highlighting Keir

Starmer’s own challenges as he finally sets out Labour’s plans to relieve

cost of living pressures. 16 August 2022 Source: https://www.ipsos.com/en-uk/two-thirds-say-government-not-providing-enough-support-cost-living 756-43-11/Polls Two-Thirds Of Parents

Worry Exams And Assessments Won’t Reflect What Their Child Is Capable Of Due

To The Pandemic

Looking back over the pandemic, parents say their

children missed seeing their friends at school most (63%) while they also

missed learning in the classroom (45%) and subjects not easily done at home,

such as PE and Food Technology (36%). Around a third of parents said their

child(ren) missed extracurricular clubs at school (34%) or seeing their

teachers (32%). Few children missed school lunches/meals at school (17%),

according to their parents, while around a quarter missed getting outside at

break times and lunches (23%). Trinh Tu, Managing

Director of Public Affairs at Ipsos in the UK, said: Now that most aspects of

life seem to have returned to normal, at least as much as we could hope for,

it’s clear education still has a long way to go to catch up. With most

parents of school-age children worried, not only about their children

catching-up on missed schoolwork, but specifically on how their exam and

assessment results will reflect them, it is clear measures need to be taken

to make sure the pandemic does not continue to put students at a

disadvantage. 17 August 2022 756-43-12/Polls Nearly Half Of Britons

Agree That British Workers Need To Work Harder

The sentiment that British workers need to work

harder is shared more strongly by those who voted Conservative in the 2019

General Election than by those who voted Labour: 58% of Conservative voters

agree that British workers need to work harder compared to 30% of Labour

voters. Britons are further divided along political lines

when asked how they feel the British work ethic has evolved over the past 20

years: nearly 1 in 2 2019 Conservative voters (47%) feel the average working

person in Britain puts in less effort than in the past, compared to 23% of

2019 Labour voters. Despite this, Conservative voters are more likely

than Labour voters to agree that British people have the necessary skills to

compete in the global workforce (68% compared to 54% Labour voters), and that

there are enough jobs in Britain that allow workers to utilise their skills

(71% compared to 42% Labour voters). Amongst the British public overall,

agreement with these statements is 58% and 56%, respectively. How Britain compares to

its past, its peers and its foreign counterparts The British public is split on how the British work

ethic has evolved over the past 20 years: 1 in 3 say they think people put in

more effort today than 20 years ago (35%), with a similar proportion (33%)

saying they think people put in less effort today. Younger people are

more likely than older ones to say that more effort is being put in today

than in the past. Half of working Britons (52%) say they put “a lot of

effort” into their current job, with a further 31% saying they put in “a

moderate amount of effort.” When asked how they think the effort they put

into their current job compares to the average working person in Britain,

half (49%) think they put in more effort, with a further 4 in 10 (37%) saying

they put in about the same level of effort. Fewer than 1 in 10 (8%) say

they put in less effort than the average working person in Britain. When asked about how the British work ethic compares

to the work ethic of other nations, half (48%) agree that the average working

person in Britain has a worse work ethic than their equivalent in China, and

2 in 5 (40%) say a worse work ethic than a worker in India. Opinions are

mixed on how the British work ethic compares to those of workers in the US, EU,

and most other countries: Trinh Tu, Managing

Director of Public Affairs at Ipsos in the UK, said: Whilst many of us believe

that British workers have the skills to compete globally and the

opportunities to put these skills to use, we are visibly divided by political

party line and age when it comes to perceptions of whether British workers

are trying hard enough or putting in the same effort as in the past. However,

we do not have these doubts when it comes to our personal effort, with the

majority of us believing we work hard and half of us claiming we work harder

than our peers. 19 August 2022 Source: https://www.ipsos.com/en-uk/nearly-half-britons-agree-british-workers-need-work-harder 756-43-13/Polls Over A Quarter Of

Conservative Party Members (28%) Deem It Significant That The Next Party

Leader May Be Female

In just over two weeks, the country will know who

the next prime minister and Conservative leader is. Since the start of July when the Conservative

leadership race kicked off, the public have seen the potential list of

figures be whittled down to the final two candidates, Rishi Sunak and Liz

Truss. The initial eight candidates represented the most diverse

leadership contest of a major party in UK history, with four being women

and four individuals of ethnic minority. The most recent YouGov poll of Conservative party

members puts Truss 32 points ahead of Sunak, meaning the foreign secretary is

well on course for a promotion to being the third woman prime minister. But how significant do Tory party members consider

such a feat to be?

A further 67% of party members place little to no

significance on the likelihood of an ethnic minority leader.

With Sunak and Truss appearing in the regular churn

of TV debates, hustings and interviews over the past couple of months, nine

in ten (91%) party members say they have been following the campaign closely,

of which 41% say they have kept up with it ‘very closely’. Just 9% say that

they are not up-to-date with coverage. August 19, 2022 756-43-14/Polls Gamescom 2022 –

Digitalization And The Future Of Video Game Conventions

Ubisoft scores with

Gamescom participation The economic relevance of the video game market and

the e-sports sector has been increasing for years, and the number of gamers

and e-sports fans worldwide is growing rapidly. As we discussed in a previous article, gaming has

gained tremendous popularity in recent years. Companies can reach millions of

consumers in attractive target groups through marketing and collaboration.

Almost a quarter of Germans now identify as "gamers" and one in ten

consumers who consider themselves gamers regularly follow e-sports broadcasts

- and the trend is rising. The potential for companies at video game

conventions should therefore not be underestimated. Some of the most popular

gaming franchises for this audience include Nintendo, Ubisoft, EA, and Sony

Entertainment. Ubisoft is looking for a direct exchange with the community at

Gamescom and confirmed its participation months ago. The company can thus score points in the eyes of the

target group: Since the announcement of the participation at the end of June

2022, we have observed a significant increase in reputation and impression

values among German gamers in the BrandIndex. The show offers publishers,

franchises and hardware manufacturers direct access to their target audiences

and especially vendors, such as Prime Matter, who will be there for the first

time, and indie manufacturers will use the platform this year to present

themselves to a large audience. Large players are missing Although Gamescom will be back in presence for the

first time this year after the Corona forced break, it is striking that some of the biggest video-game players will not be there,

especially Nintendo and Sony Entertainment, but also EA and some hardware

companies have cancelled their participation. The reasons for the

cancellations can only be speculated. A possible reason for Nintendo, Sony

Entertainment and Co. is likely to be the digital marketing activities and

online showcases successfully expanded during the Corona forced breaks.

Compared to trade fairs, these represent a more cost-effective alternative,

tailored to the respective company and the target group. However, the

Gamescom organizers do not have to worry about the attractiveness of their

trade fair due to the lack of players: A look at the list of participants for this year as

well as the supporting program on the exhibition grounds and in Cologne's

inner city can expect an exciting and entertaining program – and a lot of

business. Gaming conventions as

important industry events Whether Gamescom or E3: Gaming conventions are an

important part of the gaming and e-sports industry, whether as a traditional

trade fair or hybrid models. Hybrid models in particular offer the

opportunity to reach the highly digital target group of gaming enthusiasts

and e-sports fans even more broadly. Especially here, the gaming conventions

with their diverse streaming offers could already score points before Corona,

as they were already hybrid in this sense, when direct transmissions were not

yet standard at other events. At the same time, fans are eagerly awaiting the

chance to experience the scene in person again after the corona-related

failures and restrictions and to exchange ideas with like-minded people. The

anticipation will also apply to the trade visitors. Because Gamescom is, even

if the outdoor appeal of the fair often comes from the audience, which puts

an entire city in video-game fever for a few days, a very important business

event for the industry. August 15, 2022 Source: https://yougov.de/news/2022/08/15/gamescom-2022-digitalisierung-und-die-zukunft-der-/ NORTH

AMERICA

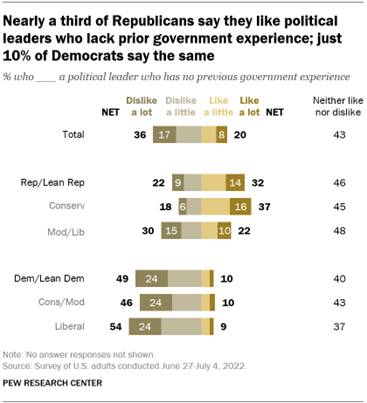

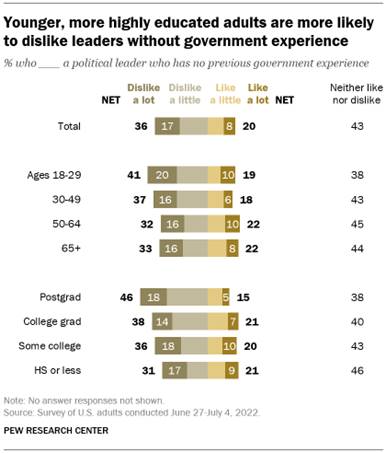

756-43-15/Polls Republicans More Likely

Than Democrats To See Politicians Without Government Experience Positively

Early in the 2016 presidential campaign, Republicans

in the United States were more likely than Democrats to value experience and

a proven record in a presidential candidate. But that

changed with the rise of political newcomer Donald Trump.

How we did this Nearly half of Democrats (49%) hold negative views

of political leaders without previous government experience, including 24%

who dislike such leaders a lot.

Just 10% of Democrats say they like inexperienced political leaders, while

40% neither like nor dislike them. Republicans’ views are more divided. While 32% say

they like political leaders with no prior government experience, 22% dislike

them and 46% neither like nor dislike such leaders. Conservative Republicans are more likely than

moderate or liberal Republicans to favor leaders without prior government

experience. Among conservative Republicans, about twice as many say they like

leaders without previous government experience (37%) as say they dislike this

type of leader (18%). Among moderate and liberal Republicans, a larger share

say they dislike (30%) than like (22%) leaders without government experience. Nearly identical shares of liberal Democrats (9%)

and conservative or moderate Democrats (10%) say they like political leaders

without prior government experience. However, liberal Democrats are 8

percentage points more likely than conservative or moderate Democrats to say

they dislike this type of leader (54% vs. 46%). Younger adults and those with higher educational

attainment are more likely to have negative views of political leaders

without previous government experience than older adults and those with less

formal education.

Adults ages 18 to 49 are more than twice as likely

to say they dislike leaders without previous experience (39%) as they are to

say they like such leaders (18%). Among adults ages 50 and older, the

difference is smaller: 32% say they dislike and 22% say they like leaders

without prior government experience. And while adults at all levels of educational

experience are more likely to dislike than like leaders without prior

government experience, those with a postgraduate degree are especially likely

to say they dislike this type of leader. Nearly half of adults with a

postgraduate degree (46%) say they dislike such leaders, compared with 38% of

those with college degrees but no postgraduate experience. About three-in-ten

adults with a high school education or less (31%) and 36% of those with some

college education but no degree say the same. AUGUST 16, 2022 756-43-16/Polls Most Republicans (64%) Say

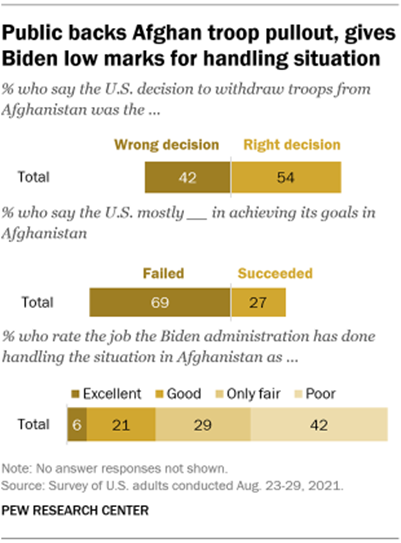

The Decision Of U S Military Exit From Afghanistan Was Wrong

In August 2021, the United States withdrew

the last of its troops from Afghanistan, ending its military presence

there after nearly 20 years. The U.S. exit from Afghanistan resulted in the

Taliban regaining control of the country and created a refugee crisis as

many Afghans fled. It also raised fears that terrorists might use Afghanistan

as a safe haven, as was the case with Ayman al-Zawahiri, the al-Qaida leader

who was discovered in the nation’s capital, Kabul, and killed

in a U.S. drone strike late last month. How we did this At the time of the military

evacuation, 54% of Americans said the decision to withdraw U.S. troops from

Afghanistan was the right one, according

to a

survey conducted in August 2021. Around

four-in-ten Americans (42%) said the decision was the wrong one. There was a

sharp partisan divide on this topic. While 70% of Democrats and

Democratic-leaning independents said the decision to withdraw troops was the

right decision, about half as many Republicans and GOP leaners (34%) shared

this view. Most Republicans (64%) instead said the decision was wrong.

In the same survey, 69% of U.S. adults said the

United States mostly failed in achieving its goals in Afghanistan. About a

quarter (27%) said the U.S. succeeded. There was partisan agreement on this

question: About seven-in-ten in both parties said the U.S. mostly failed to

achieve its goals. Americans harbored doubts about the war in

Afghanistan even before the withdrawal of U.S. troops. In a spring

2019 survey, 59% of U.S. adults said that considering the costs versus

the benefits to the United States, the war in Afghanistan was not worth

fighting, while 36% said it was. The balance of opinion was about the same

among U.S. military veterans. Both during and after the

troop withdrawal, large majorities of Americans expressed negative views of

the Biden administration’s handling of the situation in Afghanistan. In

both August and September 2021, about seven-in-ten or more said that the

administration had done an only fair or poor job dealing with the situation

there, with around four-in-ten or more saying it had done poorly. In both

surveys, fewer Americans said the administration had done an excellent or

good job. In the September survey, for instance, only 24% said this.

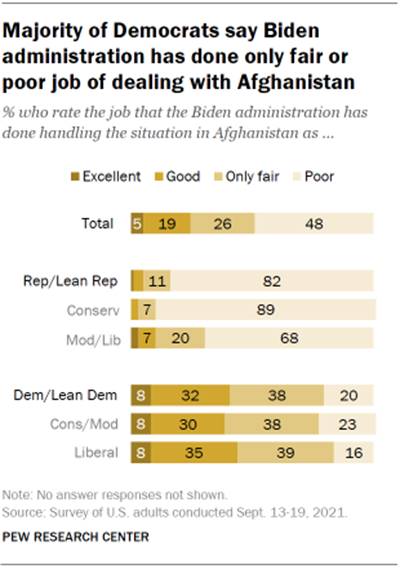

A large majority of Republicans (82%) said in

September 2021 that the administration had done a poor job handling the

situation in Afghanistan. Conservative Republicans were 21 percentage points

more likely than moderate and liberal Republicans to say this (89% vs. 68%). One-in-five Democrats also said the Biden

administration had done a poor job dealing with the Afghanistan situation.

About twice as many said the administration had done an only fair job (38%)

or an excellent or good job (40%). Veterans and non-veterans were

also divided on this question. While similar shares of veterans (76%) and

non-veterans (74%) said in September 2021 that the Biden administration had

done an only fair or poor job dealing with the situation in Afghanistan,

veterans were more likely than non-veterans to say the administration handled

it poorly (60% vs. 47%). Only about a quarter or fewer in either group said

the administration had done an excellent or good job, with very few giving it

an excellent rating (4% of veterans and 5% of non-veterans). As is the case

with the general public, veterans’ views on these issues are deeply divided

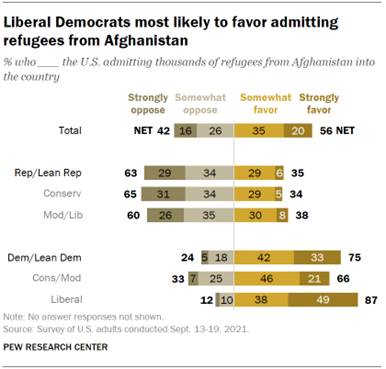

along party lines. Last September, a majority

of Americans (56%) said they favored admitting thousands of Afghan refugees

into the U.S., according

to the same survey, which was conducted after the U.S. evacuated

thousands of Afghans from the country. About four-in-ten (42%) opposed

this move.

These views were deeply divided by partisanship. At

the time, 63% of Republicans either strongly (29%) or somewhat (34%) opposed

the U.S. admitting thousands of refugees from Afghanistan into the country.

About a third (35%) said they favored admitting these refugees. By contrast, three-quarters of Democrats were in

favor of admitting refugees, including a third who strongly favored it.

Liberal Democrats (87%) were more likely than conservative and moderate

Democrats (66%) to support this. About half of liberal Democrats (49%) said

they strongly favored admitting refugees from Afghanistan. Despite majority support for admitting refugees,

Americans were divided on whether the government was conducting adequate

security screenings for those arriving in the U.S. from Afghanistan. About

four-in-ten Americans (43%) said they were very or somewhat confident that

the government was conducting adequate security screenings, while 55% were

not too confident or not at all confident. Democrats were more likely than

Republicans to express confidence in the government’s security

screenings. In a spring

2022 survey of 18 countries, people

viewed the U.S. decision to withdraw all troops from Afghanistan as

the right one, but many said the withdrawal itself was not handled

well. A median of 52% across the surveyed countries said the

troop pullout was the right choice, compared with a median of 39% who said it

was the wrong choice. Public opinion in these countries

was more negative when it came to how the U.S. exit from Afghanistan was handled.

A median of 56% said it was not handled well, while a median of 33% said it

was. In only two surveyed countries, Poland and Malaysia, did half or more of

adults approve of the way the situation in Afghanistan was handled. Most Americans said in

August 2021 that Taliban

control of Afghanistan is a threat to

the security of the United States. Nearly half (46%) said

Taliban control represented a major threat to the U.S., and another 44% saw

it as a minor threat. Republicans (61%) were far more likely than Democrats

(33%) to view a Taliban-controlled Afghanistan as a major security threat.

In a

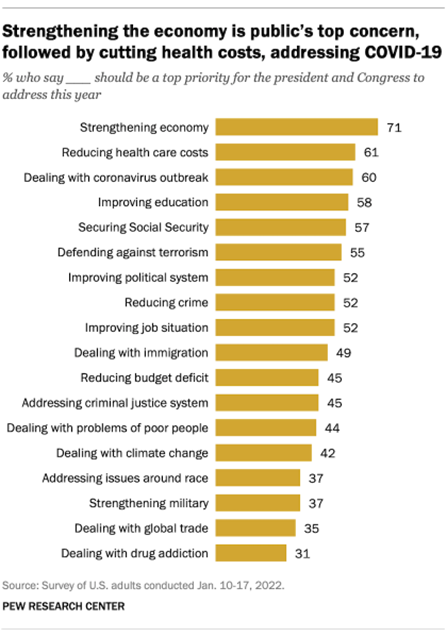

January 2022 survey, 55% of Americans

said that defending against terrorism should be a top priority for the president and Congress to

address this year. Of the 18 issues asked about, defending

against terrorism was among the top priorities identified. The survey

preceded the U.S. military’s drone strike on al-Qaida leader Ayman

al-Zawahiri in Kabul in July. Americans tend to prioritize the

terrorism issue differently based on factors including age and partisanship.

About three-quarters of adults ages 65 and older (76%) said that defending

against terrorism should be a top priority for the president and Congress, compared with

32% of those under 30. And roughly two-thirds of Republicans (65%) said

it should be a top priority, compared with 48% of Democrats. AUGUST 17, 2022 756-43-17/Polls Since 2011, 40% Or More Of

U S Adults Have Identified As Political Independents In Nearly Every Year

Historically, Americans have had weak attachments to

the two major U.S. political parties in young adulthood, but as they get

older, they usually became more likely to identify as a Republican or a

Democrat. That historical pattern, evident in the Silent and baby boom

generations, appears to be changing. Generation X and millennials, who are

now middle aged or approaching it, have maintained or even expanded their

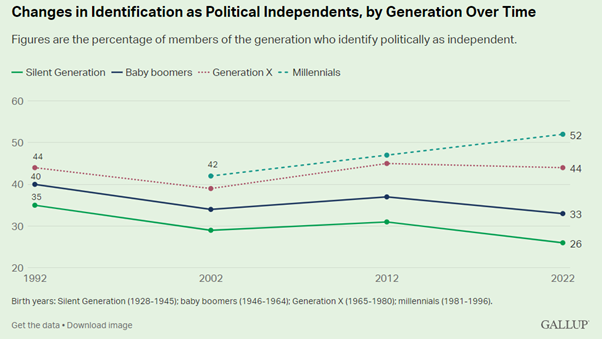

identification as political independents in recent decades.

Members of Generation Z who have reached adulthood

match millennials in the percentage of political independents, at 52%. The data also reveal that each younger generation

has had a greater proportion of independents throughout their lives than the

prior generation did, even at similar stages in their life. For example, the

44% of Generation X (now aged 42 to 57) that currently identifies as independent

is 10 points higher than the 34% of baby boomers who said they were

independents in 2002 (when they were aged 38 to 56). These emerging generational patterns of party

identification help explain why independent

identification has reached levels in the past decade never seen before in

Gallup polling. Since 2011,

40% or more of U.S. adults have identified

as political independents in nearly every year. Before that year,

that level had never been reached. Independent Identification

Varies Inversely With Republican Identification Whereas younger generations tend to

be more politically independent than older generations, older Americans are

much more likely to identify as Republicans. In fact, Republican identification is most common

among the oldest generation of Americans -- the Silent Generation, at 39% --

and is less common at each lower rung on the generational ladder, down to 17%

among Generation Z. Democratic Party identification is more uniform

across the five generational groupings, ranging between 27% and 35%.

These results are based on aggregated data from 2022

Gallup surveys to date, encompassing more than 6,000 interviews with U.S.

adults and at least 500 in each generation. The results for 2022 are similar

to those for 2021, which are based on even larger samples. Gallup also analyzed its 1992, 2002 and 2012 data to

show how party identification has changed among the generations over time.

The most notable changes in recent decades are that the Silent Generation has

become increasingly Republican and less independent, while independent

identification among Generation X and millennials has held steady or

increased, compared with when the groups first entered adulthood. The following sections show the trends in party

identification for each generation over the past 30 years. There are no trend

data for Generation Z because no one in that generation had reached adulthood

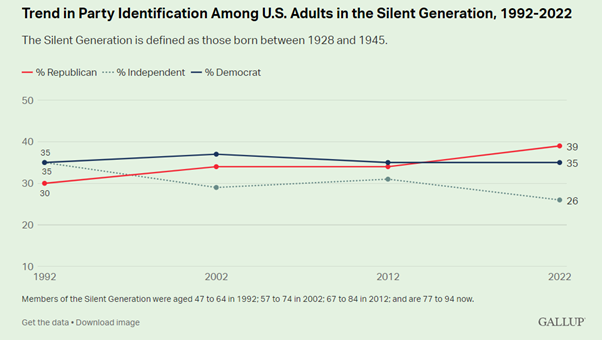

until 2015. Silent Generation Members of the Silent Generation

were born between 1928 and 1945 and, therefore, are primarily between the

ages of 77 and 94

today. The group has been less likely to identify as independents than other

generations over the past 30 years and is even less likely to do so today. Since 1992, the percentage of Silent Generation

members who identify as political independents has decreased from 35% to 26%,

which has been accompanied by an equal increase in Republican identification. Over the past 30 years, the proportion of Silent

Generation people who identify as Democrats has been relatively stable.

Baby-Boom Generation The pattern in party identification among baby boomers, born

between 1946 and 1964 and aged 58 to 76 today, is largely similar to that for

the Silent Generation. Fewer baby boomers today (33%) than in 1992 (40%)

identify as political independents, with most of that change offset by an

increase in Republican identification, from 29% to 35%. The 32% of baby

boomers who identify as Democrats is largely unchanged over the past 30

years. Baby boomers' party preferences have been evenly

split over the past three decades.

Generation X Generation X, whose members were

born between 1965 and 1980 and are aged 42 to 57 today, has a higher

proportion of independents than preceding generations and, unlike those

generations, that percentage has not shrunk over time. In 1992, when only about half of Gen X had reached

adulthood, 44% identified as independents. Ten years later, when all

generation members were at least 22 years old, a slightly smaller percentage,

39%, said they were independent. But in both 2012 and 2022, the proportion of

Generation X members who are independent has returned to the mid-40% range. The adult members of Generation X in 1992 were more

likely to identify as Republicans than Democrats, 32% to 24%. This group came

of age when Republicans held the White House for 12 years between 1981 and

1992. Over time, and as more of Generation X reached adulthood, Republicans

and Democrats have claimed roughly equal proportions of the generation,

including 30% of the former and 27% of the latter this year.

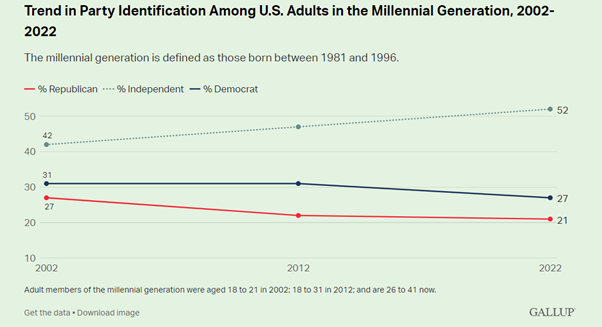

Millennial Generation Millennials, born between 1981 and

1996 and aged 26 to 41 today, have become increasingly independent since

2002, when the oldest members of the generation were first turning 18. That

year, 42% of adult millennials were independent. Ten years later, when all but the youngest millennials

were adults, 47% identified as independent. Now, a 52% majority of the group

does. Millennials have been more likely to identify as

Democrats than Republicans over the past 20 years, but fewer align with either

party than did 10 and 20 years ago.

Bottom Line Younger generations of U.S. adults

are much more likely than older generations to identify as independents and,

to this point, Generation X and millennials have become no less likely to do

so as they have

gotten older, in contrast to the generations that preceded them. The youngest adults, those in Generation Z, are as

likely as millennials to think of themselves as independents. In fact, like

millennials, more describe themselves this way than identify with either

political party. These population trends appear at odds with the

political parties' actions, as they have seemingly tried to appeal more to

their own bases than to the larger group of unaffiliated voters. This

disconnect may explain low

levels of trust in government and poor

views of both parties in general. While Republican messaging in

recent decades may have increased the party's support among older generations

of Americans in recent decades, it may have cost the party support among

younger generations, with only about one in five adults younger than 41

identifying as Republican. The trends to date for Generation X and millennials

do not preclude their showing declining political independence as they

continue to age. However, even if those generations become less likely to

identify as independents in the future, they will still likely have higher

proportions of independents than members of their preceding generations had