|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 747-749 Week:

June 13 – July 03, 2022 Presentation:

July 15, 2022 60%

Of Major Firms Say Japan’s Economy Is Expanding 68%

Of Candidates Favor Bolstering Japan’s Defense S'pore

Residents Anticipate Their Cost Of Living To Increase, Plan To Cut

Non-Essential Spending Thailand’s

Most Talked-About Brand: May 2022 Internet

Access Of All Adult South Africans, 85% One

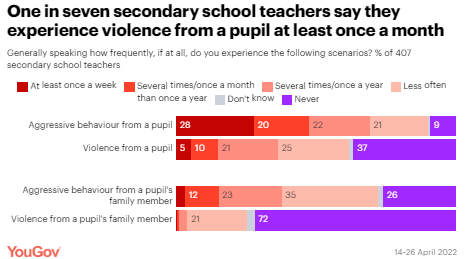

In Seven Secondary School Teachers Say They Face Violence From Pupils At

Least Once A Month Seven

In Ten People Say The Early Years Should Be More Of A Priority For Society War

In Ukraine: Britons Continue To Support Sanctions But Are Wary Of Costs At

Home Two-Thirds

Of People Believe The NHS Should Provide Fertility Treatment The

Conservative Celtic Fringe: Tories In Trouble In The Leave-Voting South West 72%

Of Britons Support Introducing Rent Controls In England Among

Unwed Britons Shows That They Tend To Want To Get Married (40%) Conservatives

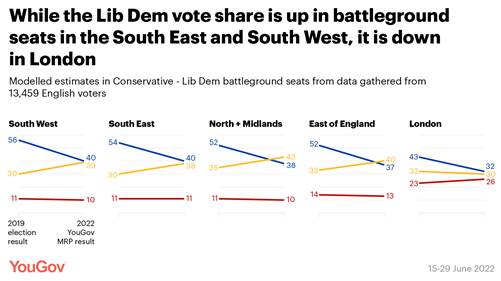

Set To Lose 26 Of Their 64 Lib Dem Battleground Seats Shopper

Barometer 2022: 58% Of French People Do Their Daily Shopping To Within €10 Boom

In Holiday Departures: Three Out Of Four French People Intend To Leave This

Summer More

Than One In Two French People Do Not Know That Myopia Is A Disorder Affecting

Far Vision About

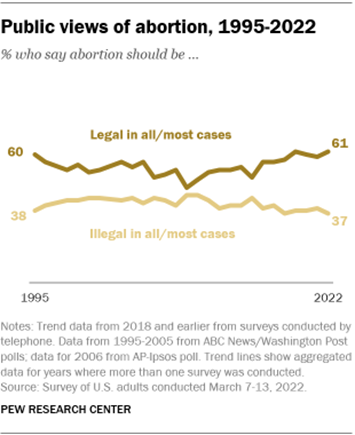

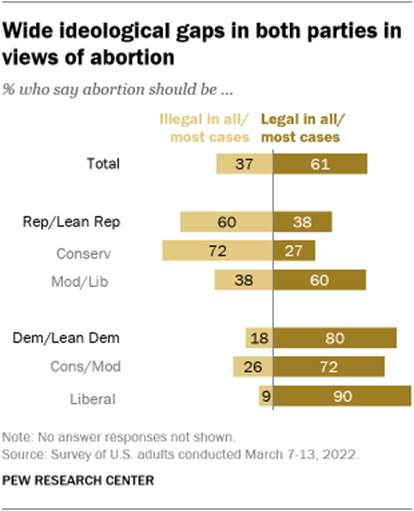

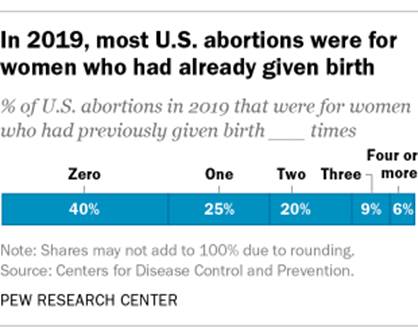

Six-In-Ten Americans Say Abortion Should Be Legal In All Or Most Cases 57%

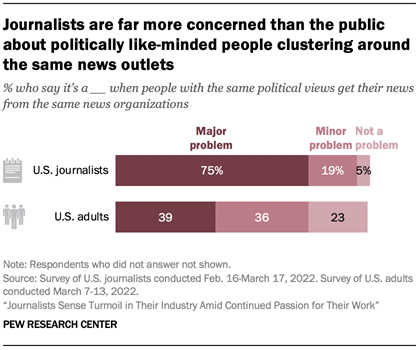

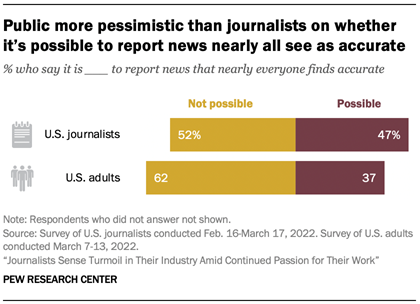

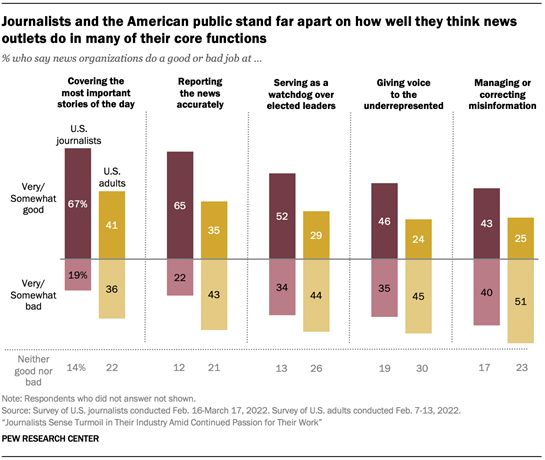

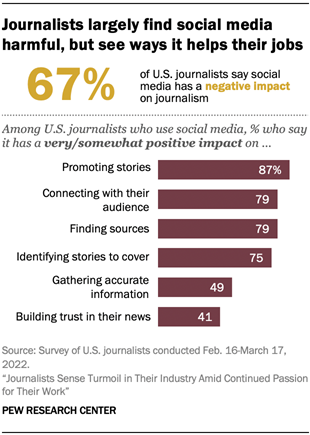

Journalists Are Highly Concerned About Future Restrictions On Press Freedom Hispanic

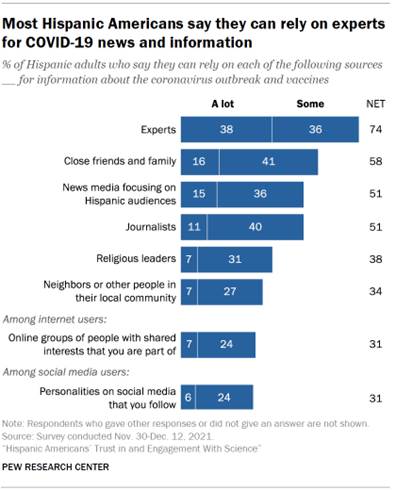

Americans’ Trust In And Engagement With Science U S

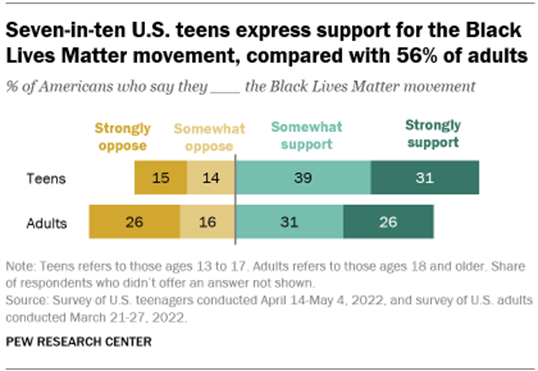

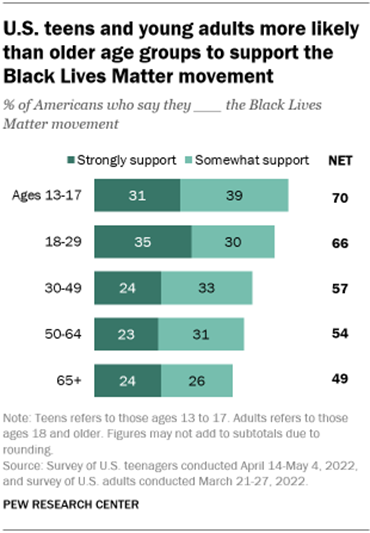

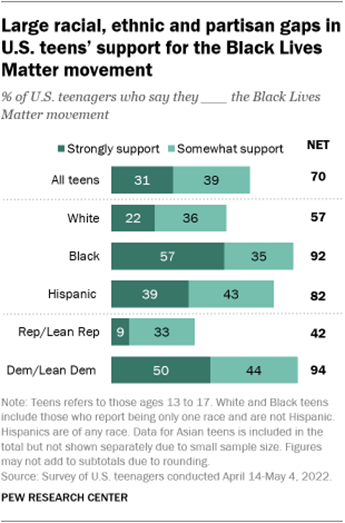

Teens Are More Likely Than Adults To Support The Black Lives Matter Movement Politics

On Twitter: One-Third Of Tweets From U S Adults Are Political Belief

In God In U S Dips To 81%, A New Low Nearly

Half Of States Now Recognize Juneteenth As An Official Holiday Two-Thirds

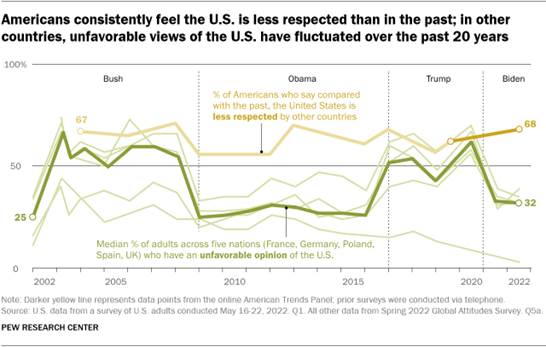

(68%) Of Americans Continue To Think The U S Is Less Respected Today Than In

The Past 61%

Of U S Adults Say Abortion Should Be Legal Australians’

Personal Financial Assets Up 13.5% Compared To Pre-Pandemic At Value Of

$10.62 Trillion Half

Of Australia's Retail Investors Started Using Investment Apps/Platforms From

2020 Or Later ANZ

Roy Morgan New Zealand Consumer Confidence Down 1.8pts To 80.5 In June 2022 A

Global Average Of 78% Among 28 Countries Support Refugee Reception Inflation

All Over The World Is High And Getting Higher, Results From Survey Of 38

States Three

Out Of Five Global Consumers Of 18 Markets Say They Prefer Buying Local Foods

(60%) Global:

How Often Do Consumers Order Take-Away Food; Views Of People From 22

Countries International

Attitudes Towards The U S, NATO And Russia In A Time Of Crisis, A Survey In

18 Nations 45%

Of Global Consumers Use Their Phones To Shop Online On A Daily Basis, A

Survey From 43 Nations Globally

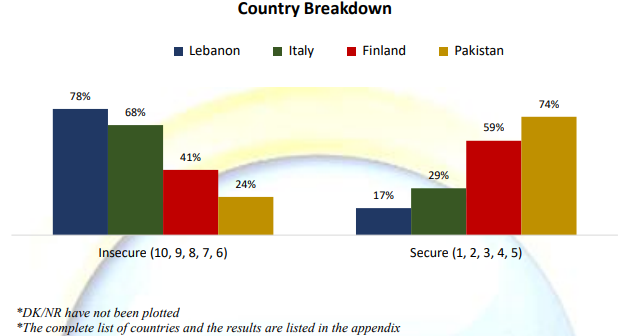

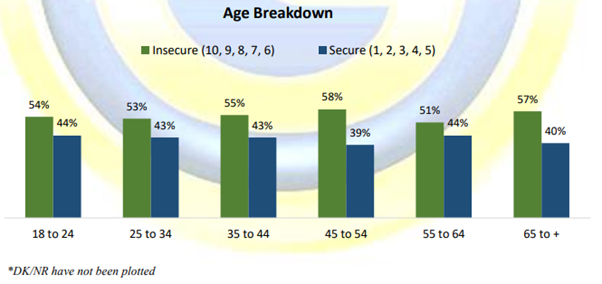

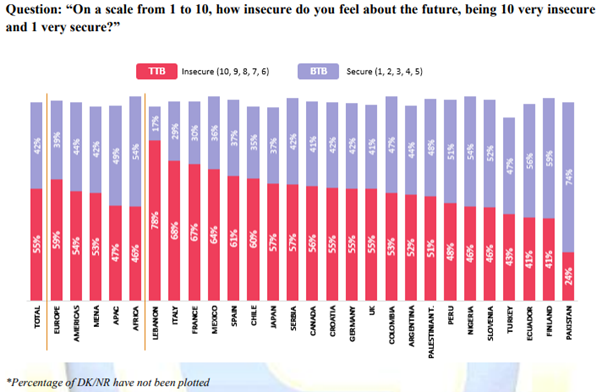

42% Of People Feel Secure About Their Future, View Of People From 24

Countries On

Average Across 30 Countries, Two In Three Adults (67%) Consider Themselves

Happy Large

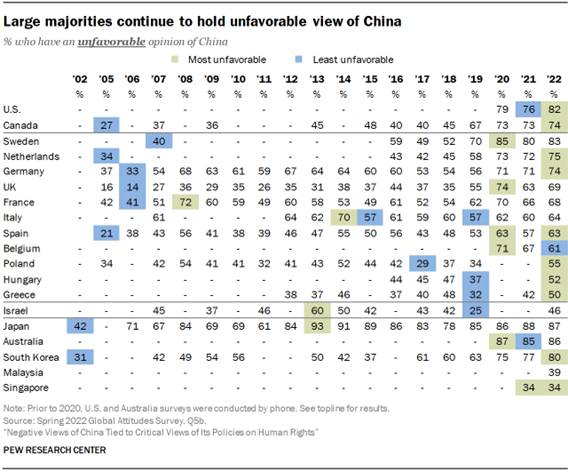

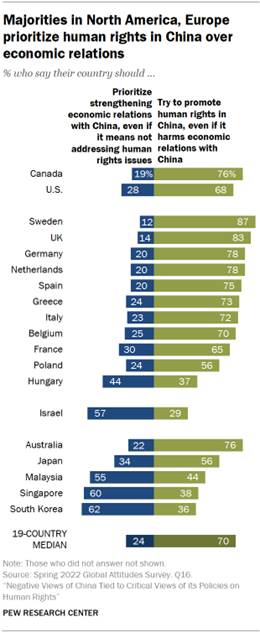

Majorities In Most Of The 19 Countries Surveyed Have Negative Views Of China INTRODUCTORY NOTE 747-749-43-51/Commentary: One In Seven Secondary School Teachers Say

They Face Violence From Pupils At Least Once A Month

Teachers in

Britain say disruptive and violent pupils ruin

teachers’ lives, causing physical injury and

career-ending psychological harm. Recently, a London teacher received

£850,000 in compensation after being punched in the face and

kicked by a pupil with a history of violence. Teachers

experience regular aggression and even violence from school children,

according to new YouGov research. One in seven secondary school teachers

(15%) say they experience violence from a pupil at least once a month,

including 5% who say they are subject to attacks at least once a week.

In addition,

around half of secondary school teachers (47%) say they experience aggressive

behaviour from a student at least once a month, including three in 10 (28%)

who say this happens at least once a week. One in 14 (7%) teachers say they

deal with aggressive pupils every single day. Teachers

also have to deal with the belligerent behaviour of angry parents – one in

seven (15%) teachers say parents are aggressive with them on at least a

monthly basis. (YouGov UK) June 15,

2022 ASIA (Japan) 60% Of Major Firms Say Japan’s Economy Is Expanding A new survey found that more than half of

major firms in Japan believe that the nation's economy is expanding, although

an overwhelming number fear the impact of rising prices. In the survey,

conducted by The Asahi Shimbun, the firms reported that the lifting of

novel coronavirus restrictions on social activities has led to a resumption

of economic and social activities and consumer spending is growing. In the

findings, 61 of 100 leading companies from across Japan said the

domestic economy is “expanding” or “expanding moderately.” (Asahi Shimbun) June 21, 2022 68% Of Candidates Favor Bolstering Japan’s

Defense The survey was conducted by The Asahi

Shimbun and a team led by Masaki Taniguchi, a professor of political science

at the University of Tokyo. Sixty-eight percent of candidates in the July 10

Upper House election favor strengthening Japan’s defense, nearly double the

37 percent of three years ago, reflecting fears about Russia’s invasion of

Ukraine, a survey showed. Among candidates of the ruling Liberal Democratic

Party, a record 99 percent were in favor or somewhat in favor of

strengthening defense. That was even higher than the 95 percent in 2013 when

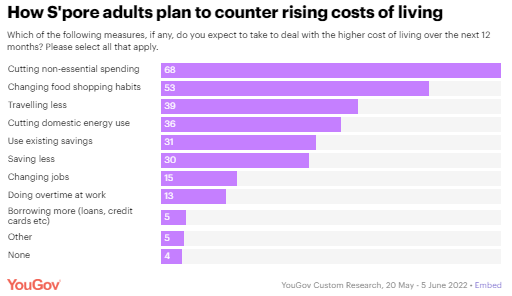

the Upper House election was held under then Prime Minister Shinzo Abe. (Asahi Shimbun) June 24, 2022 (Singapore) S'pore Residents Anticipate Their Cost Of Living To

Increase, Plan To Cut Non-Essential Spending With inflation hitting a thirteen-year-high

in Singapore last month, it comes as no surprise that residents

have begun to feel the pinch. Latest data from YouGov suggests that majority

also expect the cost of living to rise over the next 12 months (83%), with

more likely to say this will be a substantial increase (51%) rather than a

minor one (32%). Older adults appear to anticipate a greater impact, with

those aged 45-54 (60%) and above 55 (57%) most likely to say that the cost of

living will increase substantially. On the other hand, those aged 18-24 (45%)

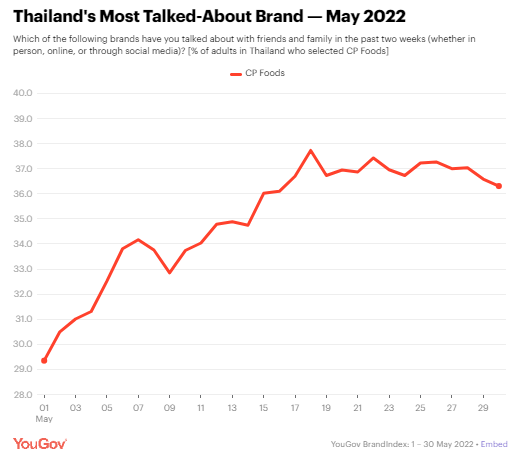

and 25-34 (37%) were most likely to say cost would increase slightly. (YouGov Singapore) (Thailand) Thailand’s Most Talked-About Brand: May 2022 Data from YouGov BrandIndex, which tracks consumer perceptions toward

brands on a daily basis worldwide, shows that Word of Mouth (WOM) Exposure of

the food company rose 6.9 percentage points over the four-week

period. According to data from YouGov BrandIndex, CP Foods’ WOM Exposure

score rose from 29.4 on 1 May to 36.3 by 30 May. WOM exposure is a BrandIndex

metric that measures the percentage of people who have spoken with their

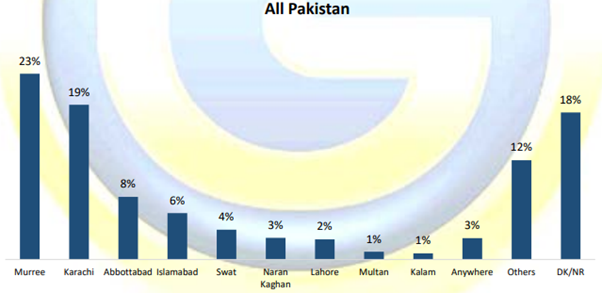

family or friends about a particular brand in the previous two weeks. (YouGov Thailand) (Pakistan) Murree (23%) Is Popular Tourist Destination Followed By

Karachi (19%) Among Pakistanis Planning To Travel This Summer According to a survey conducted by Gallup

& Gilani Pakistan, Murree (23%) is popular tourist destination followed

by Karachi (19%) among Pakistanis planning to travel this summer. A

nationally representative sample of adult men and women from across the

country was asked the following question, “Do you have any plans to travel

this summer? For example, taking your family and children out of the city? If

yes, where are you planning to go?” In response to this question, 23% said

Murree, 19% said Karachi (Gallup Pakistan) July 1, 2022 MENA (Egypt) Views On Inflation In Egypt Inflation is the top concern for people in

Egypt. The majority (96%) believe that prices have increased over the past 12

months, and as a result, so has their spending. People have experienced price

increases across most categories, with food & beverage topping the list,

followed by fashion items, and utilities. People believe that the key

contributors to this inflation is linked to the retailers and traders

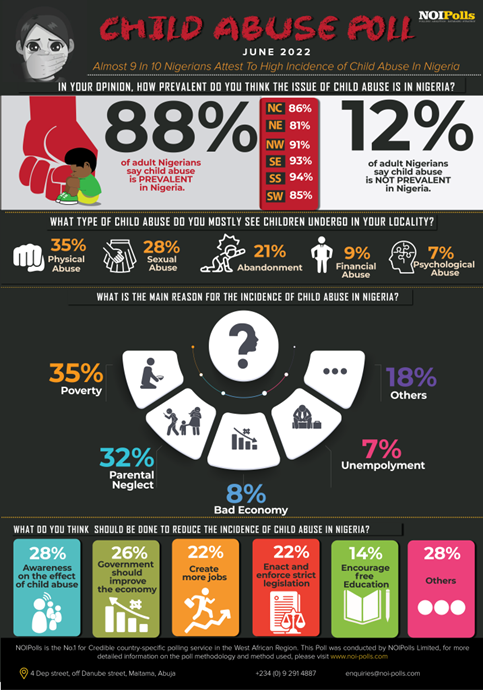

increasing their prices, wars and conflicts, and the increase in global oil prices. (Ipsos Egypt) 27 June 2022 AFRICA (Nigeria) Almost 9 In 10 Nigerians Attest To High Incidence Of Child

Abuse In Nigeria A new public opinion poll conducted by

NOIPolls has revealed that child abuse is prevalent in Nigeria, as disclosed

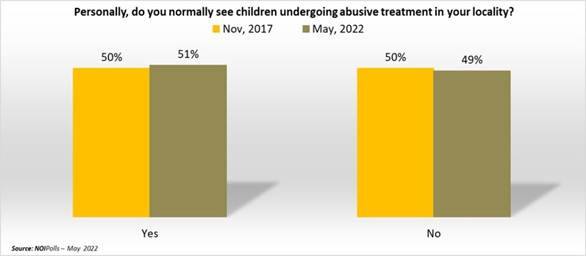

by 88 percent of adult Nigerians nationwide. Also, the poll revealed that 51

percent of adult Nigerians acknowledeged that they had personally seen

children undergo abusive treatment in their localities. The South-South (57

percent) and North-West (56 percent) zones had more respondents who made this

assertion. This is indeed a worrisome figure and everything possible must be

done to curtail this act as soon as possible. (NOI Polls) June 16, 2022 Young Adults Aged 15 – 29 Years Old Are Most Known Abusers

Of Drugs & Substances In Nigeria A new public

opinion poll conducted by NOIPolls has revealed that most abusers of drugs

and substances in the country are young Nigerians aged between 15 and 29

years as stated by 88 percent of adult Nigerians interviewed. This figure leaves

much to be desired as the menace of drug and substance abuse continue to

ravage and destroy the lives of many youths. The Chairman of the National

Drug Law Enforcement Agency (NDLEA), Buba Marwa, lamented over the pervasive

abuse of (cannabis) substance in the country, revealing that about 10.6

million Nigerians are actively abusing the substance. (NOI Polls) June 23,

2022 (South

Africa) Internet Access Of All Adult South Africans, 85% Young people in South Africa are definitely

well-connected, with 98% having access to a cellphone, albeit not always a

smart phone. In addition, a remarkably high proportion (92%) of young people

between the ages of 18 and 24 have also indicated that they have access to

the internet, although many of them do not have access at home, work, or an

educational institution, most have access via their mobile phones. (Internet

access of all adult South Africans is 85% - also mainly via mobile phone.) (Ipsos South Africa) 15 June 2022 WEST

EUROPE (UK) One In Seven Secondary School Teachers Say They Face

Violence From Pupils At Least Once A Month Teachers in Britain say disruptive and

violent pupils ruin teachers’ lives, causing physical injury and career-ending

psychological harm. Recently, a London teacher received £850,000 in compensation after being punched in the face and

kicked by a pupil with a history of violence. Teachers experience regular

aggression and even violence from school children, according to new YouGov

research. One in seven secondary school teachers (15%) say they experience

violence from a pupil at least once a month, including 5% who say they are

subject to attacks at least once a week. (YouGov UK) June 15, 2022 Seven In Ten People Say The Early Years Should Be More Of A

Priority For Society Nine in ten agree the early years are

important in shaping a person’s future life but less than a fifth recognise

the unique importance of the 0-5 period. Seven in ten think the early years

should be more of a priority for society. Majority of public recognise a

person’s future mental health and wellbeing most likely part of adult life to

be affected by their early childhood. Community support networks found to be

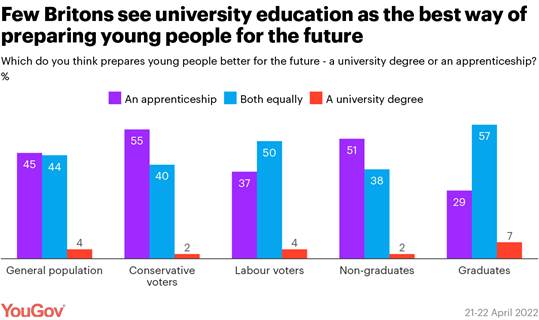

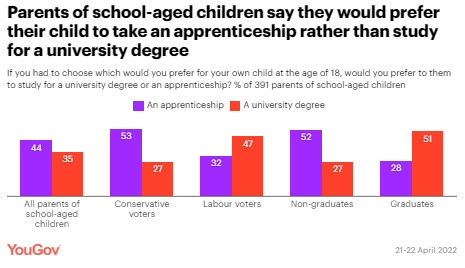

a crucial for parents. (Ipsos MORI) 16 June 2022 Half (45%) Of The Public Say Apprenticeships Are Better

Than University Degrees For Preparing Young People For The Future Britons see apprenticeships as at least

equally good as university degrees for young people, new polling from

YouGov/The Times shows. Approaching half (45%) of the public say

apprenticeships are better than university degrees for preparing young people

for the future, while 44% say both are equally good. Just 4% of Britons think

a university degree is best – despite university degrees having significantly higher uptake

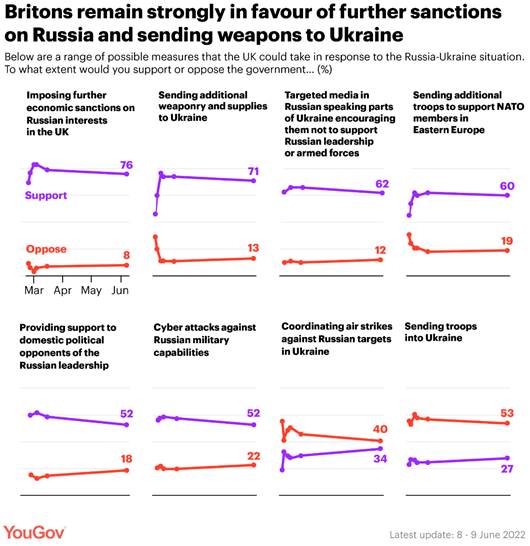

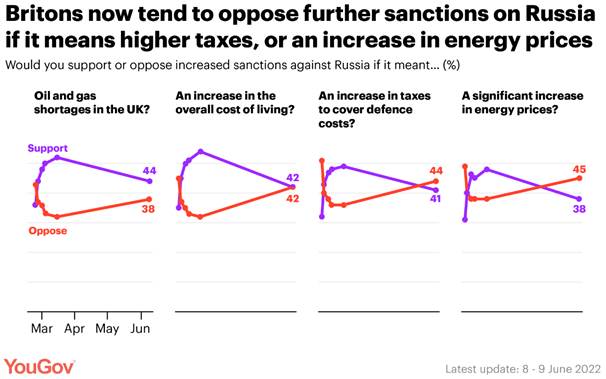

among young people than apprenticeships. (YouGov UK) June 17, 2022 War

In Ukraine: Britons Continue To Support Sanctions But Are Wary Of Costs At

Home As the conflict in Ukraine drags past the

100-day mark, it seems increasingly likely that fighting will drag on

in a protracted war of attrition. Britons continue to back a wide range of

supporting measures for Ukraine, bar direct military conflict between British

and Russian forces. Three-quarters of people (76%) currently support

increased economic penalties against Russian interests in the UK, within the

margin of error for the 79% in the previous survey on 14-15 March. (YouGov UK) June 20, 2022 Two-Thirds Of People Believe The NHS Should Provide

Fertility Treatment The Progress Educational Trust (PET) and

Ipsos explored UK adults’ attitudes and beliefs around fertility treatment

and genomics in medicine. Survey participants were introduced to fertility

treatment as ‘medical intervention to help people conceive’. Respondents

showed support for the NHS offering fertility treatment for people who are

infertile and wish to conceive, with two-thirds (67%) saying that this

treatment should be offered (31% saying ‘Yes, definitely’ and 36% saying

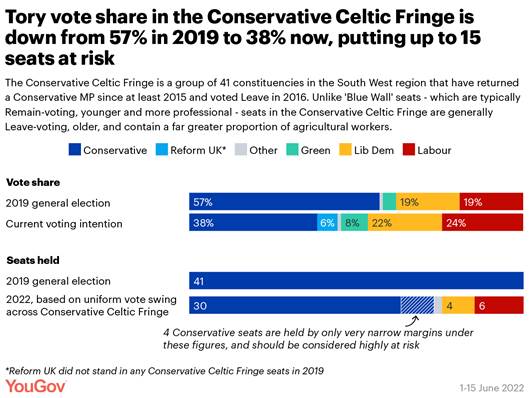

‘Yes, probably’). (Ipsos MORI) 22 June 2022 The Conservative Celtic Fringe: Tories In Trouble In The

Leave-Voting South West Across the South West of England sit a raft

of Leave-voting, ageing, and sparsely populated constituencies which have

been held by the Conservatives since at least 2015, when a blue sea swept the

region, propelling David Cameron to a Westminster majority. Latest YouGov

figures suggest that, if an election were being held now, the Conservatives

would lose 11 seats in their Celtic Fringe, with a further four on the cliff

edge of falling into opposition hands. (YouGov UK) June 23, 2022 72% Of Britons Support Introducing Rent Controls In England New research by Ipsos shows most Britons

expect house prices in their local area will be higher in 12 months’ time,

and a similar proportion expect an increase in the average across Britain.

Around a quarter expect prices to rise a lot. Two-thirds (66%) believe

average house prices will increase in their local area while 69% say the same

for the country’s average. Those in the East of England (76%), South of

England (70%), West Midlands (66%) and Scotland (66%) are most likely to

expect prices to rise. (Ipsos MORI) 27 June 2022 Among Unwed Britons Shows That They Tend To Want To Get

Married (40%) A new YouGov survey among unwed Britons

shows that they tend to want to get married (40%), compared to 28% who say

they will not, and a further 29% who are unsure. There is also little

difference between the genders. Among unwed men, 38% want to marry versus 27%

who do not, compared to 42% of unwed women who want to tie the knot and 29%

who do not. (YouGov UK) June 28, 2022 Conservatives Set To Lose 26 Of Their 64 Lib Dem

Battleground Seats Now new YouGov MRP modelling shows that the

Conservatives would be set to lose no fewer than 24 Con-Lib Dem battleground

constituencies to the Liberal Democrats if an election were being held

tomorrow (with Labour picking up another two). Of the 64 English seats which

the Conservatives hold and the Liberal Democrats won above 20% of the vote at

the 2019 general election, our MRP model suggests that the Tories would lose

a number of high-profile contests to the Liberal Democrats including Esher

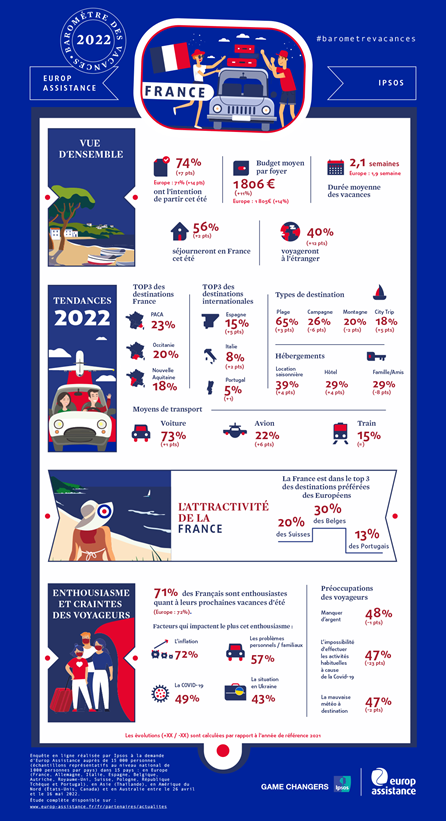

and Walton (YouGov UK) July 02, 2022 (France) Shopper Barometer 2022: 58% Of French People Do Their Daily

Shopping To Within €10 The budgetary room for maneuver of the

French has fallen sharply: 58% of them now do their shopping for around

€10 or less, an increase of 12 points since 2021 . Between energy and consumer

goods, the price increase is felt by nearly 9 out of 10 French

shoppers, half of whom consider it very significant. As a

result, visits to local businesses (convenience stores, food shops,

municipal markets) and organic businesses are falling, where 89% of

shoppers continue to visit large format hypermarkets and supermarkets. (Ipsos France) June 14, 2022 Boom In Holiday Departures: Three Out Of Four French People

Intend To Leave This Summer Record rate of departure intentions: 74% of

French people intend to go on vacation this summer (vs. 71% of Europeans). 56%

of them intend to spend their holidays on French territory. 40% plan to go

abroad: Spain (15%), Italy (8%), Portugal (5%). 23% have not yet chosen their

destination, and 55% have not yet booked. The coast remains the favorite

destination of 65% of French holidaymakers. (Ipsos France) June 14, 2022 More Than One In Two French People Do Not

Know That Myopia Is A Disorder Affecting Far Vision Only the hereditary character (65%) and the

time spent in front of the screens (68%) are factors mainly identified by the

French. The others remain little known: - ethnic origin : 86% of French people

are unaware of this risk factor even though we now know that certain populations

are more predisposed to myopia than others (for example, the Chinese and the

Eskimos vs the Indians) ; - the time

devoted to reading each day (unrecognized by 74% of those

questioned): however, prolonged reading in poor conditions (insufficient

lighting, distance of less than 30 cm, absence of regular breaks, etc.) leads

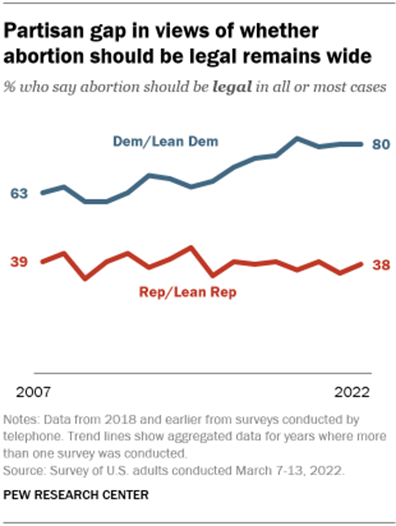

to a strong demand on near vision can promote myopia. (Ipsos France) NORTH AMERICA (USA) About Six-In-Ten Americans Say Abortion Should Be Legal In

All Or Most Cases Today, a 61% majority of U.S. adults say

abortion should be legal in all or most cases, while 37% think abortion

should be illegal in

all or most cases. These views are relatively unchanged in the past few

years. The latest Pew Research Center survey, conducted March 7 to 13, finds deep

disagreement between – and within – the parties over abortion. In fact, the

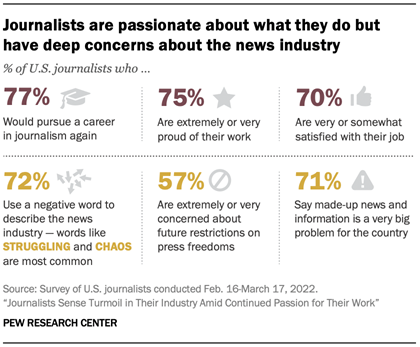

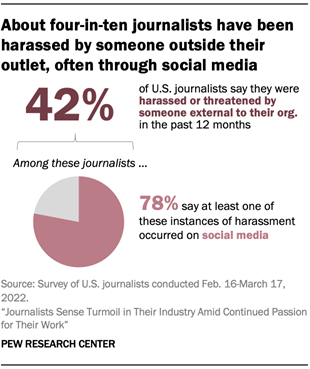

partisan divide on abortion is far wider than it was two decades ago. (PEW) JUNE 13, 2022 57% Journalists Are Highly Concerned About Future

Restrictions On Press Freedom Seven-in-ten journalists surveyed say they

are “very” or “somewhat” satisfied with their job, and an identical share say

they often feel excited about their work. Even larger majorities say they are

either “extremely” or “very” proud of their work – and that if they had to do

it all over again, they would still pursue a career in the news industry.

About half of journalists say their job has a positive impact on their

emotional well-being, higher than the 34% who say it is bad for their

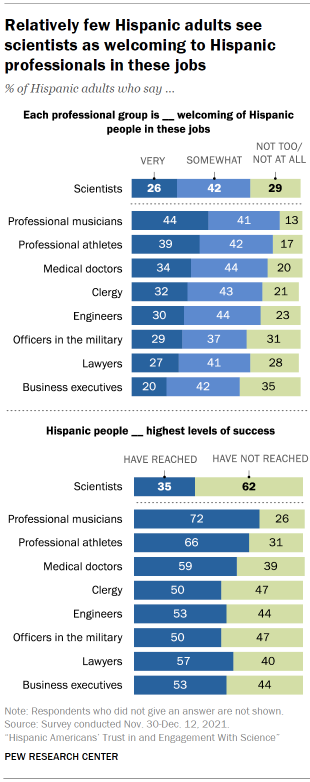

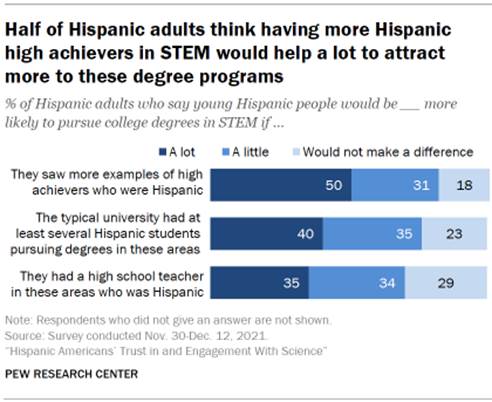

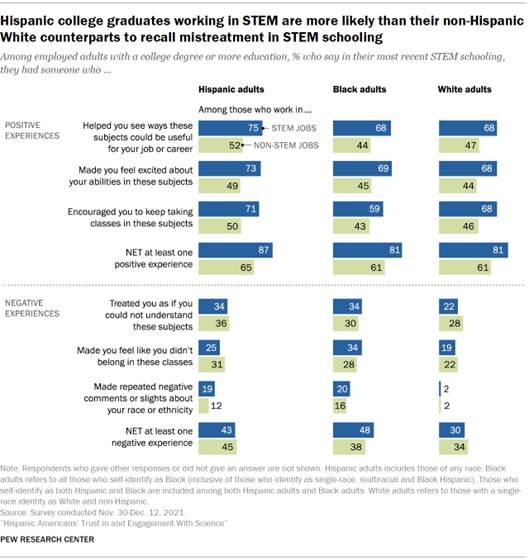

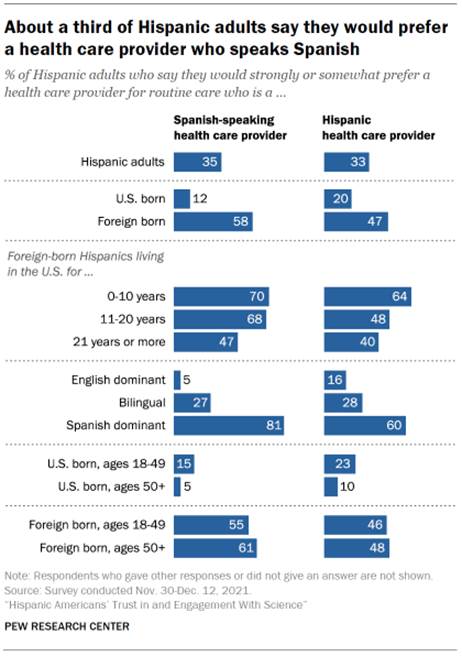

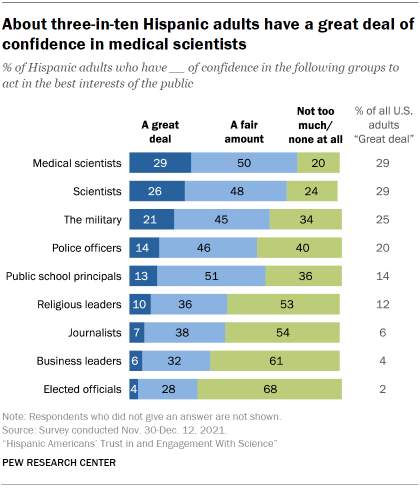

emotional well-being. (Gallup) JUNE 14, 2022 Hispanic Americans’ Trust In And Engagement With Science A new Pew Research Center survey,

accompanied by a series of focus groups, takes an in-depth look at Hispanic

Americans’ views and experiences with science spanning interactions with

health care providers and STEM schooling, their levels of trust in scientists

and medical scientists, and engagement with science-related news and

information in daily life. The survey findings suggest that most Latinos see

scientific professions as potentially “unwelcoming” to Latino people. For

example, just 26% of Latinos feel that scientists as a professional group are

very welcoming of Latinos in these jobs; another 42% say they are somewhat

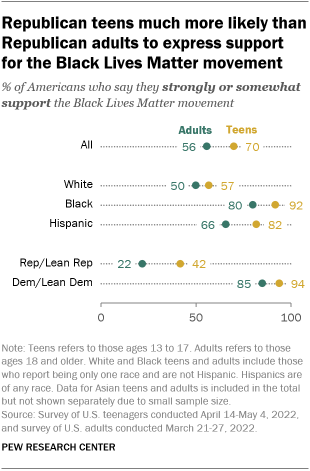

welcoming. (PEW) JUNE 14, 2022 U S Teens Are More Likely Than Adults To Support The Black

Lives Matter Movement Seven-in-ten U.S. teens say they at least

somewhat support the Black Lives Matter movement, including 31% of teenagers

who strongly support it, according to a survey conducted in April and May

among American teens ages 13 to 17. By comparison, a little over half of U.S.

adults (56%) said in a March survey that they support the Black Lives Matter

movement, similar to the 55% who said the same in September 2021 and September 2020. Around a quarter of adults (26%) strongly

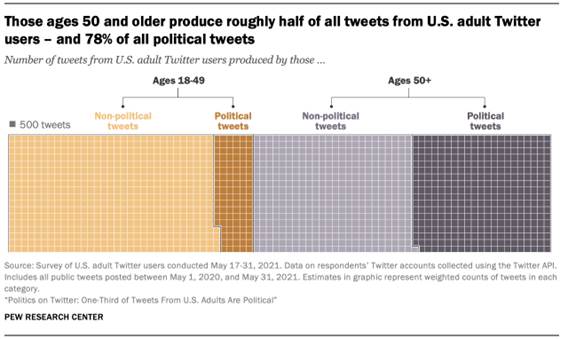

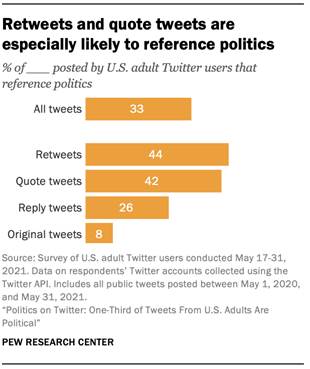

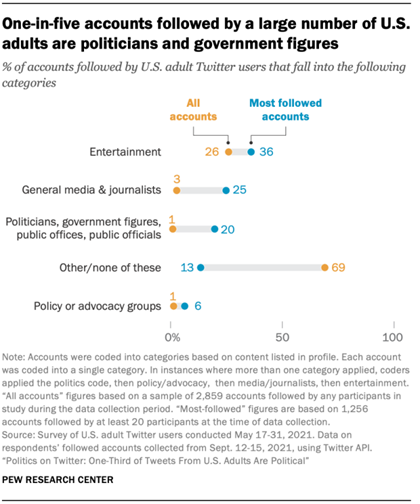

support the movement. (PEW) Politics On Twitter: One-Third Of Tweets From U S Adults

Are Political Roughly one-quarter of American

adults use Twitter. And when they share their views on the

site, quite often they are doing so about politics and political issues. A

new Pew Research Center analysis of English-language tweets posted between May

1, 2020, and May 31, 2021, by a representative sample of U.S. adult Twitter

users finds that fully one-third (33%) of those tweets are political in

nature. Americans ages 50 and older make up 24% of the U.S. adult Twitter

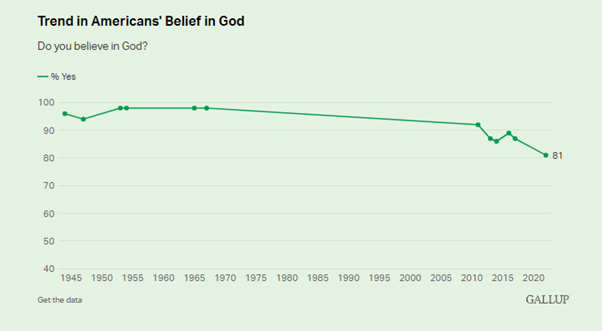

population but produce nearly 80% of all political tweets. (PEW) JUNE 16, 2022 Belief In God In U S Dips To 81%, A New Low The vast

majority of U.S. adults believe in God, but the 81% who do so is down six

percentage points from 2017 and is the lowest in Gallup's trend. Between 1944

and 2011, more than 90% of Americans believed in God. Gallup has also in

recent years asked other questions aimed at measuring belief

in God or

a higher power. All find the vast majority of Americans saying they believe;

when given the option, 5% to 10% have said they were "unsure." (Gallup) JUNE 17, 2022 Nearly Half Of States Now Recognize Juneteenth As An

Official Holiday Juneteenth is a combination of the words

June and nineteenth. It commemorates the day, more than two months after the

end of the Civil War – and more than two years after Abraham Lincoln issued

the Emancipation Proclamation. At the state level, at least 24 states and the

District of Columbia will legally recognize Juneteenth as a public holiday

this year – meaning state government offices are closed and state workers

have a paid day off, according to a Pew Research Center analysis of state

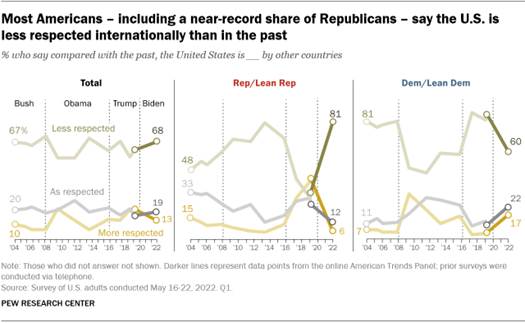

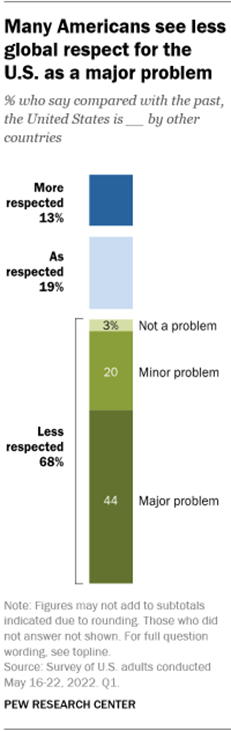

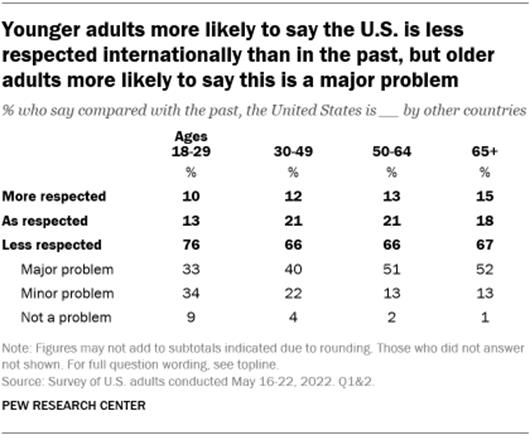

human resource websites, state legislation and news articles. (PEW) JUNE 17, 2022 Two-Thirds (68%) Of Americans Continue To Think The U S Is

Less Respected Today Than In The Past A majority of Americans have long held the view that the United States is

less respected by

other countries today than it was in the past, and around two-thirds of U.S.

adults (68%) say that’s the case today, according to a new Pew Research Center survey. Only 13% think the U.S. garners more

respect internationally now than in the past, while 19% think it’s as

respected as ever. But the consistency of overall U.S. public opinion on this

question masks large swings among Republicans and Democrats. Around eight-in-ten

Republicans and Republican-leaning independents (81%) currently believe the

U.S. is less respected than in the past – among the highest GOP percentages

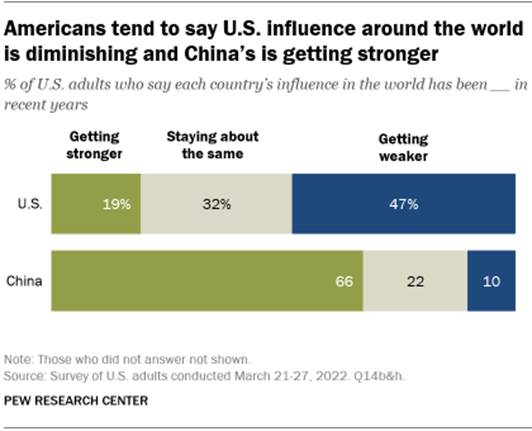

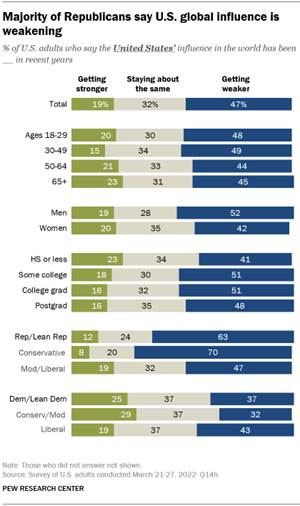

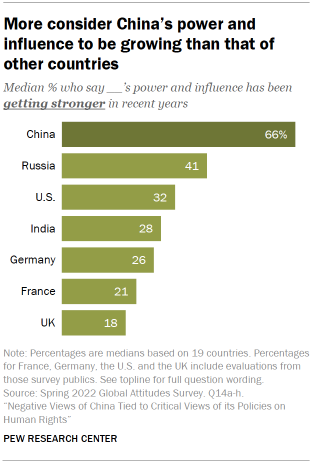

measured in Center surveys dating back to 2004. (PEW) JUNE 22, 2022 Nearly Half Of Americans (47%) Say That The United States’

Influence In The World Has Been Getting Weaker Nearly half of Americans (47%) say that the

United States’ influence in the world has been getting weaker in recent

years. Only about one-in-five say U.S. influence has been getting stronger,

while 32% say U.S. influence has been staying about the same. This is in

stark contrast with views of China: Two-thirds of U.S. adults say that the

country’s influence has been getting stronger in

recent years. Roughly one-in-five Americans say China’s global influence is

holding steady, and only one-in-ten say China’s influence has been weakening. (PEW) JUNE 23, 2022 61% Of U S Adults Say Abortion Should Be

Legal Pew Research Center has conducted many

surveys about abortion over the years, providing a lens into Americans’ views

on whether the procedure should be legal, among a host of other questions. In

our most recent survey, 61% of U.S. adults say abortion should be

legal all or most of the time, while 37% say it should be illegal all or most

of the time. With the U.S. Supreme Court’s decision in Dobbs

v. Jackson Women’s Health Organization overturning Roe v. Wade, the

1973 case that effectively legalized abortion nationwide, here is a look at

the most recent available data about abortion from sources other than public

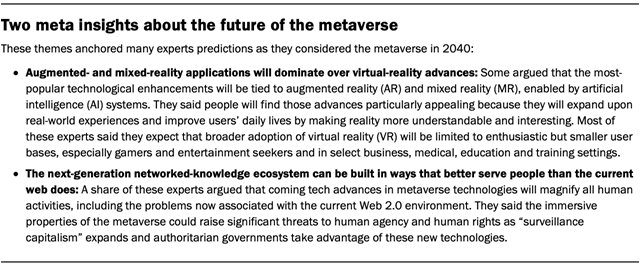

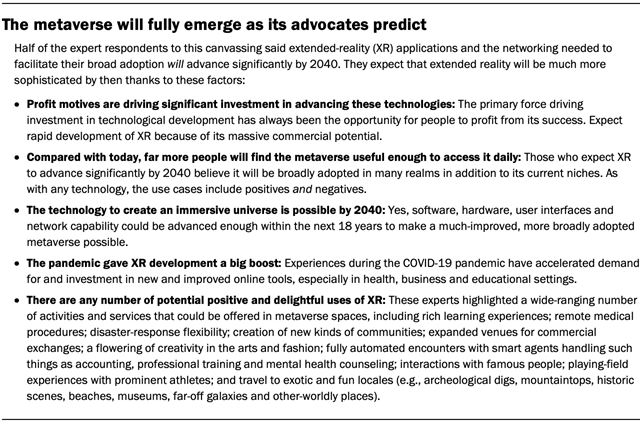

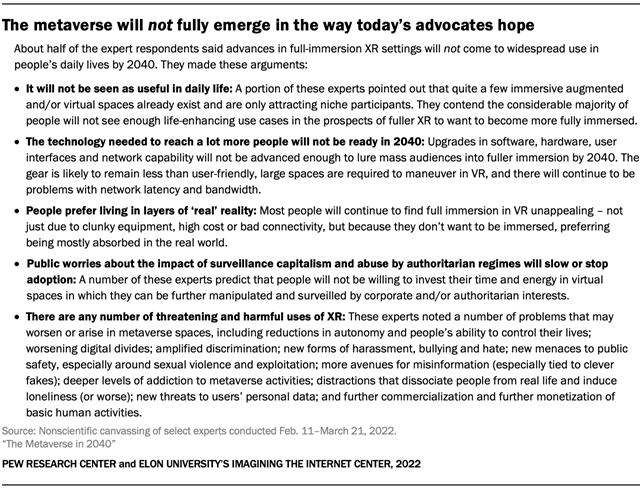

opinion surveys. (PEW) JUNE 24, 2022 The Metaverse In 2040 In all, 624 technology innovators,

developers, business and policy leaders, researchers and activists provided

open-ended responses to a question seeking their predictions about the

trajectory and impact of the metaverse by 2040. The results of this nonscientific

canvassing: 54% of these

experts said that they expect by 2040 the metaverse WILL be a much-more-refined and

truly fully-immersive, well-functioning aspect of daily life for a half

billion or more people globally. (PEW) JUNE 30, 2022 (Canada) Forced Sale: As Many As One In Four (23%) Homeowners Who

Have A Mortgage Say They Would Be Forced To Sell Their Home, If Interest

Rates Were To Increase Further A new Ipsos poll conducted on behalf of

Manulife Bank reveals that as many as one in four (23%) homeowners who have a

mortgage believe they are at risk of being forced to sell their home if

interest rates were to increase further. Additionally, two-thirds (66%) do

not view home ownership in their local community as being affordable and

eighteen percent (18%) of homeowners believe they can no longer afford the

house they own. These figures suggest that many might have been priced out of

the housing market or are at risk of being priced out of the market,

including even some of the current homeowners. (Ipsos Canada) 14 June 2022 Seven in Ten (69%) Are Concerned They Cannot Afford

Gasoline If there is one topic that is on the minds

of car owners is the price of gas. Cost increases in crude oil over the

Russian-Ukrainian war, tax surges, and hikes in transportation costs for

distribution are all fueling pump prices, and Canadians are feeling the

impact in their wallets. According to a recent Ipsos poll conducted on behalf

of Global News, as much as 69% of Canadians are concerned about the

affordability of fuel, and 50% think they cannot afford to fill their gas

tanks. As gas prices continue to climb, some Canadians are even considering

purchasing electric vehicles within the next year to avoid dependence on

fuel. (Ipsos Canada) 28 June 2022 AUSTRALIA Australians’ Personal Financial Assets Up 13.5% Compared To

Pre-Pandemic At Value Of $10.62 Trillion New data from Roy Morgan’s Banking and Finance Report shows Australians’ personal financial

assets (Traditional Banking, Wealth Management, Owner-Occupied Homes &

Direct Investments) sat at $10.62 trillion in the year to March 2022. This

result represents an increase of $1.27 trillion (+13.5%) from two years ago

pre-pandemic. However, the total value of Australians’ personal financial

assets fell by $145 billion (-1.3%) after reaching a peak of $10.77 trillion

a year ago in March 2021. This is the same month that government stimulus

programs including the $90 billion JobKeeper program and the ‘boosted’

JobSeeker payments ended. (Roy Morgan) June 28 2022 Half Of Australia's Retail Investors Started Using

Investment Apps/Platforms From 2020 Or Later RealTime Omnibus research by YouGov in March 2022 found

that CommSec Pocket enjoys

the highest awareness among major investing apps in Australia – over two in

five Australians who know of at least one investment platform say they have

heard of it (43%). About a third of Australians are also aware of Raiz (35%) and Spaceship (32%). Meanwhile, a

quarter have heard of Superhero (24%),

and around a fifth of Swyftx (22%), SelfWealth (21%) and Stake (21%). But among 65+

year-olds, awareness of Spaceship drops

to fifth place (9%), after Swftyx (17%)

and SelfWeath (14%).

However, among 25-34 year-olds, Spaceship (44%)

is the most well-known platform, and is slightly ahead of CommSec Pocket (42%) and Raiz (40%). (YouGov Australia) June 29, 2022 (New Zealand) ANZ Roy Morgan New Zealand Consumer

Confidence Down 1.8pts To 80.5 In June 2022 ANZ-Roy Morgan New Zealand Consumer

Confidence was down 1.8pts to 80.5 in June, a touch above its record low, but

still deep within the “something to worry about” zone. The proportion of

people who believe it is a good time to buy a major household item, the best

indicator for spending, was up 7% points to 28% while there were now 49%,

down 2% points, who said now is a bad time to buy a major household item.

This is a decent bounce, with the net indicator up 9 points to -21, but it’s

too early to call this a recovery. This indicator is still dire in an

absolute sense. (Roy Morgan) July 01 2022 MULTICOUNTRY STUDIES A Global Average Of 78% Among 28 Countries Support Refugee

Reception A new Ipsos survey carried out for World

Refugee Day, celebrated on June 20, reveals that Brazilians are among those

who most support the right to refuge. When asked whether people should

be able to take refuge in other countries or their own, 86% of Brazilians

said they accepted. In the global ranking, Brazil is only behind Sweden,

which has an acceptance rate of 88%. The global average of the 28

countries surveyed is 78%. (Ipsos Brazil) 14 June 2022 Source: https://www.ipsos.com/pt-br/brasileiros-estao-entre-os-que-mais-apoiam-acolhimento-refugiados Half Of The World's Population, On Average, Say They Are

Familiar With The Metaverse (52%), A Study In 29 Countries To what extent do people know about the

metaverse? How will these new technologies impact our lives? What is the

attitude towards them?To answer these questions, Ipsos has carried out a

study in 29 countries, in collaboration with the World Economic Forum , between April 22 and May 6, 2022

through its Global Advisor platform. This study reveals that half of the

world's population, on average, say they are familiar with the metaverse

(52%) and have positive feelings about adopting these new technologies in

their daily lives (50%). However, we see how these data vary greatly

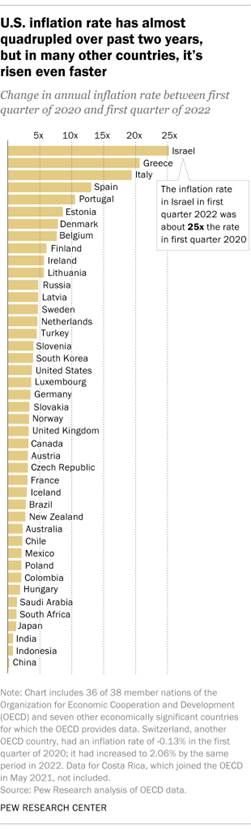

from one country to another and between demographic groups. (Ipsos Spain) June 15, 2022 Source: https://www.ipsos.com/es-es/metaverso-realidad-extendida-junio-2022 Inflation All Over The World Is High And Getting Higher,

Results From Survey Of 38 States Inflation in the United States was

relatively low for so long that, for entire generations of Americans, rapid

price hikes may have seemed like a relic of the distant past. Between the

start of 1991 and the end of 2019, year-over-year inflation averaged about

2.3% a month, and exceeded 5.0% only four times. The data covers 37 of the 38

OECD member nations, plus seven other economically significant countries.) Among the countries studied, Turkey had by

far the highest inflation rate in the first quarter of 2022: an eye-opening

54.8%. Turkey has experienced high inflation for years, but it shot up in

late 2021 as the government pursued unorthodox economic policies, such as cutting interest rates rather

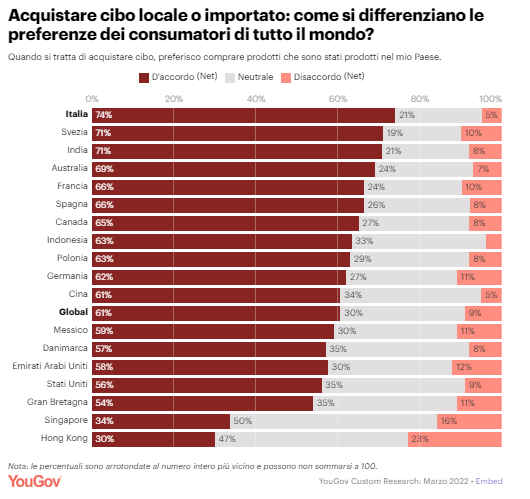

than raising them. (PEW) JUNE 15, 2022 Three Out Of Five Global Consumers Of 18 Markets Say They

Prefer Buying Local Foods (60%) Of the 18 main markets examined, consumers

in Italy are the most satisfied with their local products: in fact, just

under three quarters prefer to buy food produced in their own country

(74%). Only 5% of Italians disagree with this statement, while just over

2 out of 10 consumers are neutral in this regard (21%). In the European

market, consumers who prefer local agricultural and aquaculture products are

in Sweden (71%), France (67%) and Spain (67%). On the other hand,

consumers in Denmark (57%) and Great Britain (54%) are the least likely to

buy locally sourced food, even if the majority of them continue to prefer

them over imported products. (YouGov Italy) Source: https://it.yougov.com/news/2022/06/15/global-cibo-locale-e-cambiamento-climatico-come-re/ Global: How Often Do Consumers Order

Take-Away Food; Views Of People From 22 Countries The latest data from YouGov's new tool,

Global Profiles, a powerful profiling and media targeting tool, with over

1000 questions in 43 countries, reveals the frequency with which consumers

buy take-away food - and as many as 1 in 3 orders multiple times per week. We

selected 22 countries for this survey and found that Taiwan (10%) and

Thailand (9%) are the markets where people are most likely to buy take-out

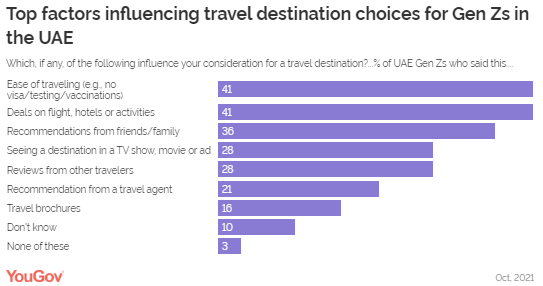

more than once a day. (YouGov Italy) Source: https://it.yougov.com/news/2022/06/21/global-con-quale-frequenza-i-consumatori-ordinano-/ Three-Quarters Of Gen Zs Across The Globe

In 25 Countries, Plan To Undertake Some Form Of Travel In The Next 12 Months As global travel opens up after two years

of restrictions amidst the pandemic, YouGov’s latest report “Youth of Today, Travel of Tomorrow”

reveals more than two in five Gen Zs (those aged 18-24 years) in the UAE

(43%) said they intend to travel abroad for leisure in the next 12 months,

with intent for international travel within this cohort being one of the

highest across the globe. The report aims to understand Gen Zs globally,

explores what matters to them as well as uncovers their expectations from

travel, and identifies the best ways to connect and engage with this

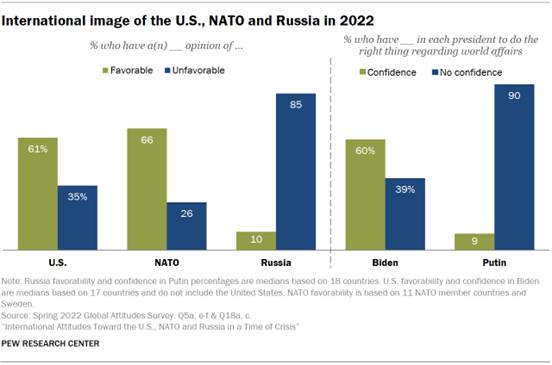

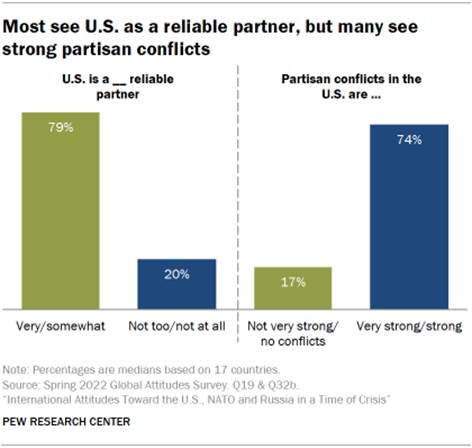

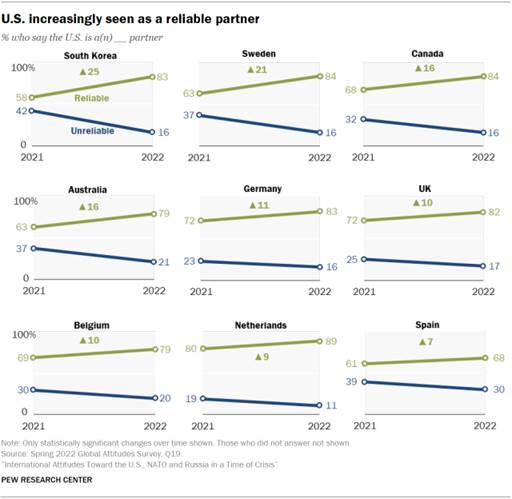

generation of travellers. (YouGov MENA) June 22, 2022 Source: https://mena.yougov.com/en/news/2022/06/22/gen-zs-uae-have-strong-desire-international-travel/ International Attitudes Towards The U S,

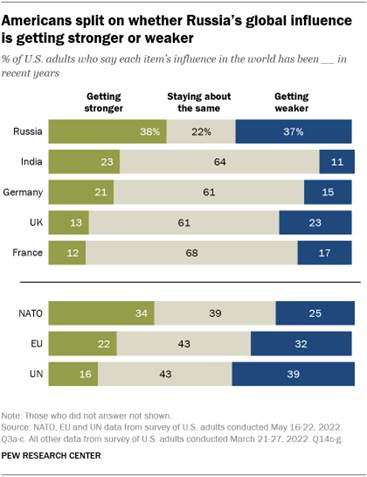

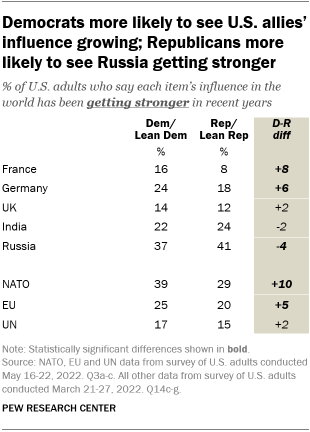

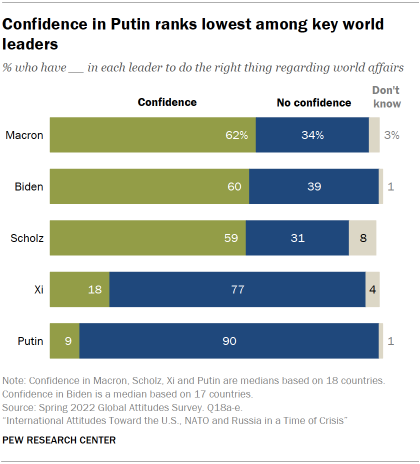

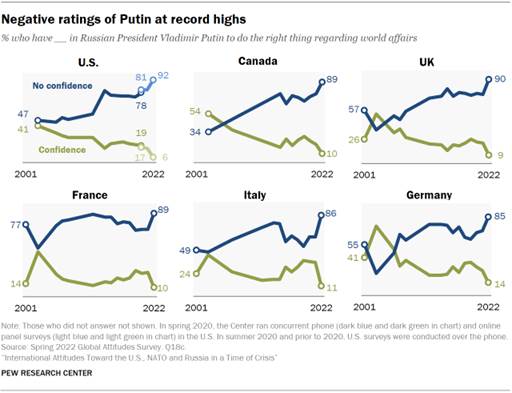

NATO And Russia In A Time Of Crisis, A Survey In 18 Nations Ratings for Russia, which were already

negative in most of the nations surveyed, have plummeted further following

the invasion. In 10 countries, 10% or less of those polled express a

favorable opinion of Russia. Positive views of Russian President Vladimir

Putin are in single digits in more than half of the nations polled. Large

majorities in most countries see America as a reliable partner to their

country, and the share of the public holding that view has risen over the

past year in most nations where trends are available. For instance, 83% of

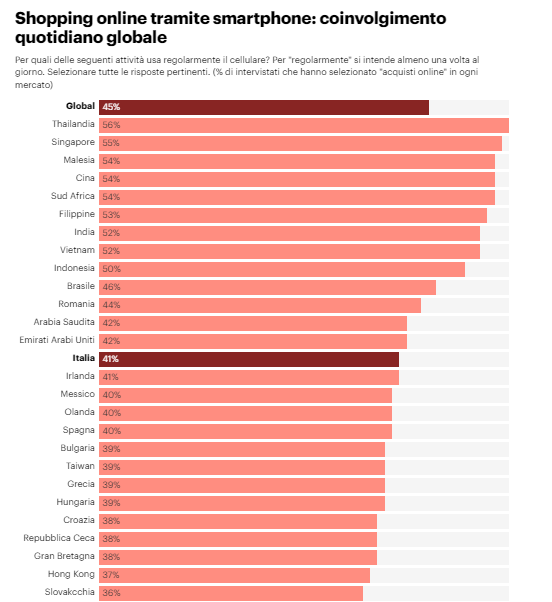

South Koreans consider the U.S. a reliable partner, up from 58% in 2021. (PEW) JUNE 22, 2022 45% Of Global Consumers Use Their Phones To

Shop Online On A Daily Basis, A Survey From 43 Nations In fact, data from YouGov Global Profiles -

an audience intelligence tool with attitudinal and behavioral data on

consumers in 43 markets - reveals that more than 2 in 5 people worldwide use

their phone to shop online every day (45%). . In Europe, daily mobile

purchases are more frequent in Romania (44%), Italy (41%) , Ireland (41%), the Netherlands (40%) and

Spain (40%). In comparison, Switzerland, France and Belgium are the

European countries least likely to report shopping online with their mobile

phone every day. Nearly 2 in 5 Brits say they shop on mobile every day

(38%). (YouGov Italy) June 23, 2022 Source: https://it.yougov.com/news/2022/06/23/global-il-45-dei-consumatori-globali-usa-il-telefo/ Globally 42% Of People Feel Secure About

Their Future, View Of People From 24 Countries According to a Gallup Pakistan Survey in

Pakistan (and similar surveys done by Worldwide Independent Network of Market

Research (WIN) across the world), significantly more than the global average

of 42%, every 2 in 3 Pakistanis feel secure about their future. These

findings emerge from an international survey conducted across the globe by

The Worldwide Independent Network of Market Research (WIN). (Gallup Pakistan) June 24, 2022 Source: https://gallup.com.pk/wp/wp-content/uploads/2022/06/24-June-2022-English-1.pdf Over Half Of Consumers Globally (51%) Agree That 5g Will

Bring Many Benefits To Their Lives In 28 Markets The latest data from our new YouGov

Global Profiles tool, a powerful profiling and media

targeting tool, with over 1000 questions in 43 countries, reveals consumers'

attitudes towards 5G and how they think it can improve their daily lives. In

this article we examine 28 markets among all those analyzed by Global

Profiles and the data shows that, overall, just over half of consumers globally (51%) agree that 5G will bring

many benefits to their lives . (YouGov Italy) June 24, 2022 Source: https://it.yougov.com/news/2022/06/24/global-come-i-vantaggi-percepiti-del-5g-variano-da/ On Average Across 30 Countries, Two In Three Adults (67%)

Consider Themselves Happy A new Ipsos survey finds that, on average

across 30 countries, two in three adults (67%) consider themselves

“happy.” Among the countries surveyed, happiness is most prevalent

in the Netherlands and Australia, with 86% and 85% respectively

describing themselves as “very” or “rather” happy. China and Great Britain

(both 83%), India (82%), France and Saudi Arabia (both 81%), and Canada (80%)

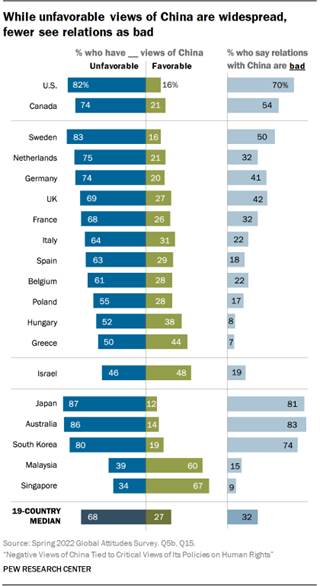

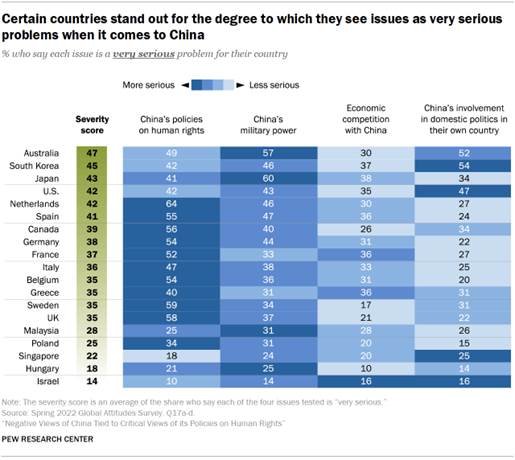

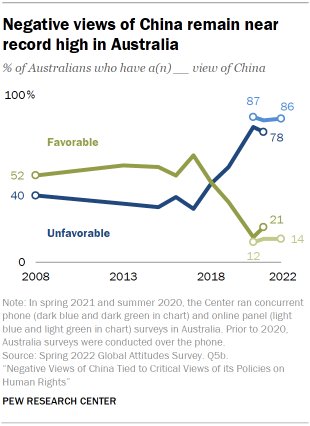

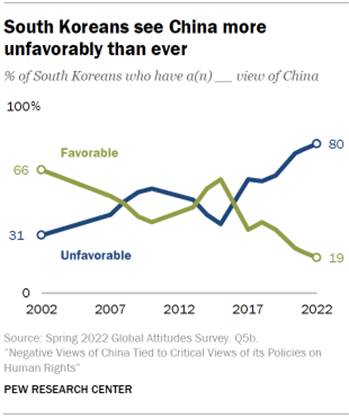

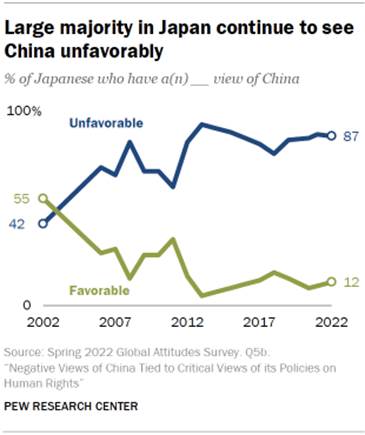

follow. (Ipsos Denmark) 27 June 2022 Source: https://www.ipsos.com/en-dk/what-makes-people-happiest-health-family-and-purpose Large Majorities In Most Of The 19 Countries Surveyed Have

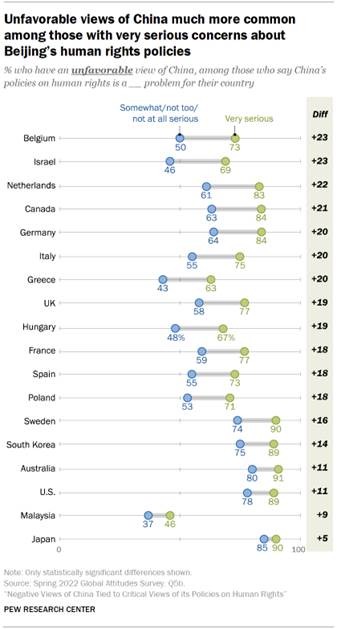

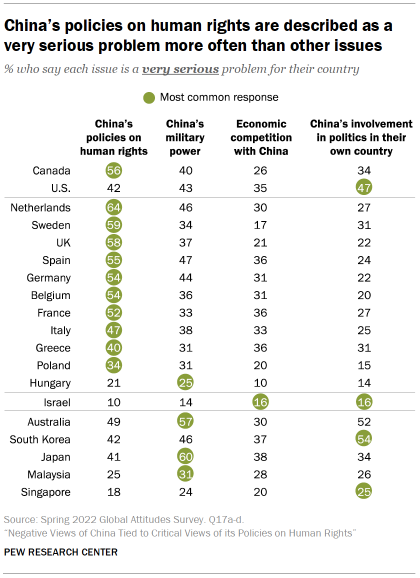

Negative Views Of China Negative views of China remain at or near

historic highs in many of the 19 countries in a new Pew Research Center

survey. Unfavorable opinions of the country are related to concerns about

China’s policies on human rights. Across the nations surveyed, a median of

79% consider these policies a serious problem, and 47% say they are a very serious problem. Among the

four issues asked about – also including China’s military power, economic

competition with China and China’s involvement in domestic politics in each

country – more people label the human rights policies as a very serious

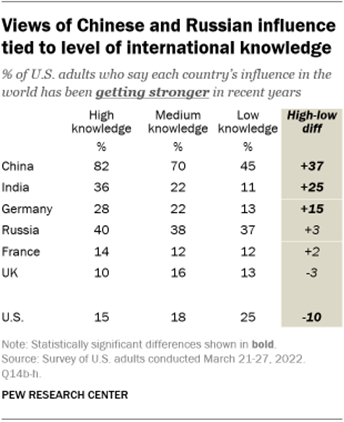

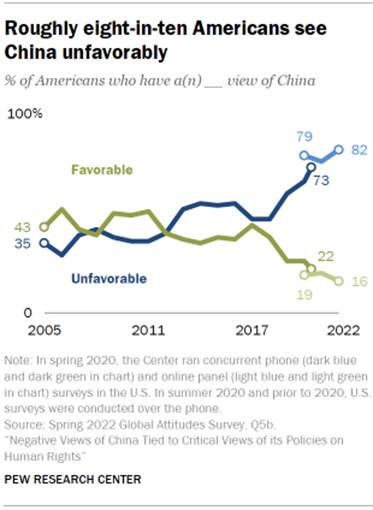

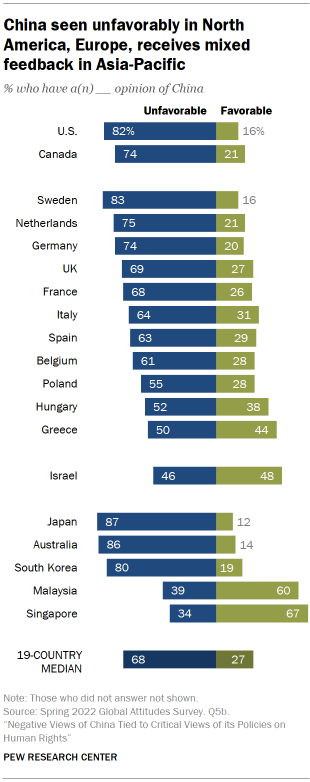

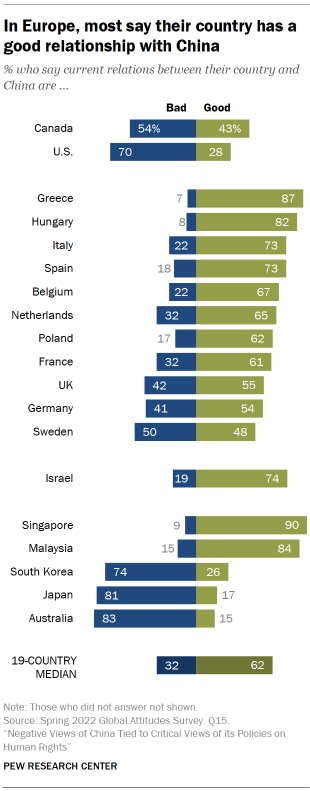

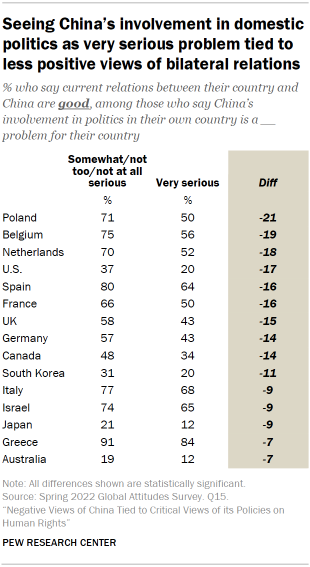

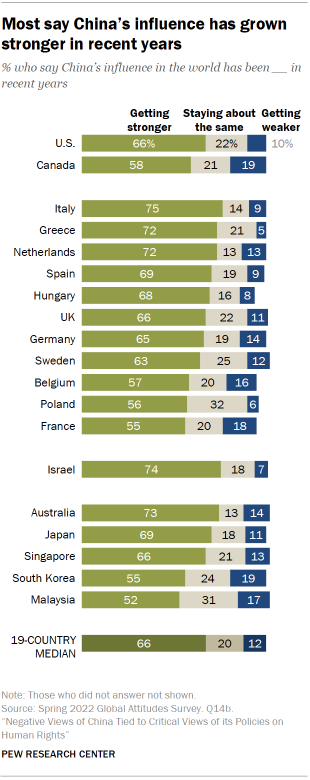

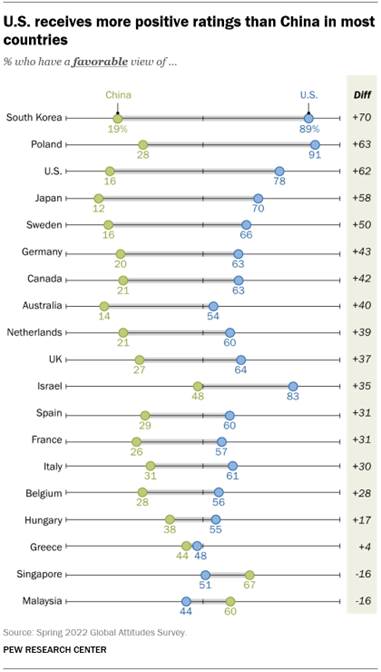

problem than say the same of the others. (PEW) JUNE 29, 2022 Across 19 Countries, More People See The U S Than China

Favorably – But More See China’s Influence Growing In 19 countries surveyed by Pew Research

Center this spring, people see the United States and President Joe Biden more

favorably than China and its president, Xi Jinping. But when it comes to perceptions

of each country’s relative influence in the world, much larger shares in most

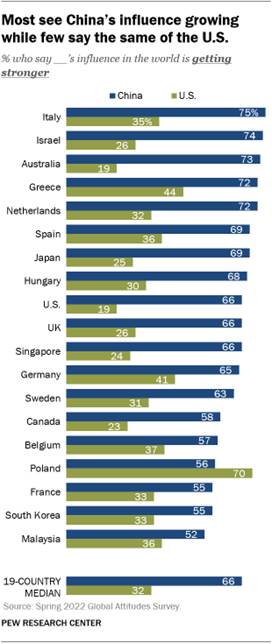

nations see China’s influence growing than say the same of the U.S. The U.S.

is generally seen more positively than China. In most countries,

majorities have a favorable view of the U.S., while fewer than around a third

tend to say the same of China. However, attitudes vary widely within the

Asia-Pacific region. In South Korea, 89% have a favorable view of China, 70

percentage points more than the 19% who say the same of China. (PEW) JUNE 29, 2022 ASIA

747-749-43-01/Polls 60% Of Major Firms Say Japan’s Economy Is Expanding

The Shinkansen platform at JR Tokyo Station

is crowded with families and passengers with large luggage on April 29 as the

Golden Week holiday period this year was the first time in three years that

restrictions on activities were not imposed. (Tatsuya Shimada) A new survey found that more than half of

major firms in Japan believe that the nation's economy is expanding, although

an overwhelming number fear the impact of rising prices. In the survey, conducted by The Asahi

Shimbun, the firms reported that the lifting of novel coronavirus

restrictions on social activities has led to a resumption of economic and

social activities and consumer spending is growing. However, an emerging concern is the speed

of rising prices for crude oil and raw materials following Russia’s invasion

of Ukraine. The Asahi Shimbun has been conducting the

survey on how major firms view the domestic economy twice annually. The most

recent survey was carried out from May 30 to June 10. In the findings, 61 of 100 leading

companies from across Japan said the domestic economy is “expanding” or

“expanding moderately.” Breaking the number down, 59 said the

economy is expanding moderately while two said it is expanding. Thirty-seven

said it is leveling off, while only one firm said it is receding moderately. When asked to choose up to two reasons why

they feel the economy is expanding, 53 of the 61 firms attributed it to

consumer spending. Retsu Togashi, executive managing officer

of Mitsui Fudosan Co., said that hotel occupancy rates have returned to

pre-pandemic levels. “Reservations during the summer vacation

period are coming in at a much faster pace than the past two years during the

pandemic,” he said. The government lifted pre-emergency

measures to prevent the spread of COVID-19 across Japan in March. It is

gradually easing restrictions on foreign visitors entering the country. Kazuo Sato, managing executive officer of

Nippon Life Insurance Co., expressed optimism, saying, “If the restrictions

on activities continue to be lifted, personal consumption will recover on the

back of high levels of savings.” When asked about the outlook for consumer

spending over the next three months, 66 firms said it will recover. But the number was down from 75 who

expressed confidence in the previous survey conducted last fall. The number

of firms that expect consumer spending will continue to seesaw increased by

seven. When asked to choose up to two concerns

about the domestic economy, 12 firms cited, “the prolonged impact of the

coronavirus pandemic,” down sharply from the previous 67. The concern had

been at the top in the four previous surveys since 2020. On the other hand, the largest number of

firms, 76, cited "rising prices for oil and raw materials," up more

than 50 percent from the previous 49. This was the top concern this time. Fifty-four firms said that they plan to or

may raise prices from June to December following the soaring prices of raw

materials and natural resources. (Asahi Shimbun) June 21, 2022 Source: https://www.asahi.com/ajw/articles/14649979 747-749-43-02/Polls 68% Of Candidates Favor Bolstering Japan’s Defense

Sixty-eight percent of candidates in the

July 10 Upper House election favor strengthening Japan’s defense, nearly

double the 37 percent of three years ago, reflecting fears about Russia’s

invasion of Ukraine, a survey showed. The latest figure is the largest over the

20 years of similar surveys conducted ahead of national elections. The survey was conducted by The Asahi

Shimbun and a team led by Masaki Taniguchi, a professor of political science

at the University of Tokyo. Questionnaires were mailed from mid-May to

545 candidates, and responses were received from 512 by the evening of June

22. Candidates were given five choices to

questions about strengthening defense and revising the Constitution: favor,

somewhat favor, neither, somewhat oppose, and oppose. Among candidates of the ruling Liberal

Democratic Party, a record 99 percent were in favor or somewhat in favor of

strengthening defense. That was even higher than the 95 percent in 2013 when

the Upper House election was held under then Prime Minister Shinzo Abe. A similar trend was found among candidates

of junior coalition partner Komeito, which had long prided itself on being a

pacifist party. Although only 13 percent were in favor of

such a change in defense three years ago, the figure skyrocketed to 83

percent this time around. Among candidates of the main opposition

Constitutional Democratic Party of Japan, those in the favor of strengthening

the nation’s defense increased from 2 percent three years ago to 31 percent. Similarly, the figure rose from 67 percent

to 89 percent among candidates of Nippon Ishin (Japan Innovation Party), and

from 21 percent to 95 percent for the Democratic Party for the People. Candidates were also asked whether Japan

should possess the capability to strike enemy bases when there was the

possibility that they could attack Japan. Among candidates of the LDP, which included

possessing that capability in its campaign platform, 77 percent were either

in favor or somewhat in favor. But the figure was only 4 percent among

Komeito candidates, with 75 percent saying neither and 21 percent either

opposed or somewhat opposed. On the question about constitutional

revision, 61 percent of all candidates either favored or somewhat favored

such a move, a large increase from the 44 percent of three years ago. Candidates were also asked how the

Constitution should be amended. The largest ratio, at 66 percent, said the

legal existence of the Self-Defense Forces must be defined. By party, 97 percent of LDP candidates

favored constitutional revision, a figure even higher than the 93 percent of

three years ago when Abe, a strong advocate of constitutional revision, was

still prime minister. Among Komeito candidates, the percentage of

respondents choosing neither dropped from 74 to 50, while those favoring such

a move surged from 17 percent to 42 percent. Among opposition parties, all Nippon Ishin

candidates supported constitutional revision, the same trend as three years

ago. There was a sharp increase among DPP candidates,

from 26 percent to 86 percent, while there was decrease among CDP candidates

from 7 percent to 4 percent. All Japanese Communist Party and Social

Democratic Party candidates opposed constitutional revision, while 85 percent

of Reiwa Shinsengumi candidates were opposed. (Asahi Shimbun) June 24, 2022 Source: https://www.asahi.com/ajw/articles/14652834 747-749-43-03/Polls S'pore Residents Anticipate Their Cost Of Living To Increase, Plan To

Cut Non-Essential Spending

With inflation hitting a thirteen-year-high

in Singapore last month, it comes as no surprise that residents

have begun to feel the pinch. Latest data from YouGov suggests that majority

also expect the cost of living to rise over the next 12 months (83%), with

more likely to say this will be a substantial increase (51%) rather than a

minor one (32%). Older adults appear to anticipate a greater

impact, with those aged 45-54 (60%) and above 55 (57%) most likely to say

that the cost of living will increase substantially. On the other hand, those

aged 18-24 (45%) and 25-34 (37%) were most likely to say cost would increase

slightly.

When asked about measures they would take

to counter rising costs, almost seven in ten residents said they would cut

back on non-essential expenses like dining out (68%). Other measures

residents are most likely to undertake include changing food shopping habits

(53%), travelling less (39%), and cutting domestic energy use (36%). One in three said they would either tap

into their existing savings (31%) or save less (30%), while a further one in

seven would switch jobs (15%) or work overtime (13%).

Amid rising costs, Singapore adults are not

hopeful about the future, with three in eight expecting their personal

finances to either get worse (35%) or remain the same (35%) over the next 12

months. Fewer are optimistic, with just two in ten expecting their financial

situations to improve (23%). Notably, younger adults are more confident

in their future financial situations, with those aged 18-24 (42%) and 25-34

(33%) most likely to say that their financial situations will improve in the

next 12 months. On the other hand, those above the age of 55 are most likely

to say their financial situations will worsen (42%).

(YouGov Singapore) Source: https://sg.yougov.com/en-sg/news/2022/06/23/spore-residents-anticipate-their-cost-living-incre/ 747-749-43-04/Polls Thailand’s Most Talked-About Brand: May 2022

CP Foods (Charoen

Pokphand Foods Public Company Limited) saw the biggest boost in the number of

people talking about it of any brand we track in Thailand, over the month of

May. Data from YouGov BrandIndex, which tracks consumer perceptions toward

brands on a daily basis worldwide, shows that Word of Mouth (WOM) Exposure of

the food company rose 6.9 percentage points over the four-week period. In late May, the agro-industrial and food

conglomerate showcased its new plant-based “Meat Zero” product at the

ThaiFex–Anuga World of Food Asia 2022, which was named the exhibition’s Taste

Innovation Show winner, as well as its Benja chicken and Cheeva pork fresh

meat products.

This comes as Singapore increases imports of chicken from

Thailand,

after the city-state's major poultry supplier Malaysia banned exports of chicken from

June 1 to

address surging prices and supply shortages. Additionally, CP Foods also recently

announced a partnership with electrical systems company Gunkul Engineering,

to develop a range of cannabidiol-infused food and beverage

products.

On 9 May 2022, Thailand became the first Asian country to

legalize the growing of marijuana and its consumption in food and drinks, although the smoking of marijuana remains

outlawed. (For a recent analysis of the Thai consumer market for cannabis

products, read the latest

YouGov research here).

According to data from YouGov BrandIndex,

CP Foods’ WOM Exposure score rose from 29.4 on 1 May to 36.3 by 30 May. WOM

exposure is a BrandIndex metric that measures the percentage of people who

have spoken with their family or friends about a particular brand in the

previous two weeks. (YouGov Thailand) Source: https://th.yougov.com/en-th/news/2022/06/13/Thailand-Most-Talked-About-Brands-May-2022/ 747-749-43-05/Polls Murree (23%) Is Popular Tourist Destination Followed By Karachi (19%)

Among Pakistanis Planning To Travel This Summer

According to a survey conducted by Gallup

& Gilani Pakistan, Murree (23%) is popular tourist destination followed

by Karachi (19%) among Pakistanis planning to travel this summer. A

nationally representative sample of adult men and women from across the country

was asked the following question, “Do you have any plans to travel this

summer? For example, taking your family and children out of the city? If yes,

where are you planning to go?” In response to this question, 23% said Murree,

19% said Karachi, 8% said Abbottabad, 6% said Islamabad, 4% said Swat, 3%

said Naran Kaghan, 2% said Lahore, 1% said Multan, 1% said Kalam, 3% said

anywhere, 12% said others and 18% said don’t know or gave no response.

Question: “Do you have any plans to travel this summer? For example, taking

your family and children out of the city? If yes, where are you planning to

go?” (The question was asked to only those who said they plan to travel

outside the city this summer)

(Gallup Pakistan) July 1, 2022 Source: https://gallup.com.pk/wp/wp-content/uploads/2022/07/July-1st.pdf MENA

747-749-43-06/Polls Views On Inflation In Egypt

Inflation is the top concern for people in

Egypt. The majority (96%) believe that prices have increased over the past 12

months, and as a result, so has their spending. People have experienced price

increases across most categories, with food & beverage topping the list,

followed by fashion items, and utilities. People believe that the key

contributors to this inflation is linked to the retailers and traders

increasing their prices, wars and conflicts, and the increase in global oil

prices. On the other hand, only 15% have taken

measures to deal with inflation, with consumers most likely to buy only

necessities, buy fewer items per shopping trip, and eat more home-cooked

meals. Looking at the future, around half are

optimistic that prices will start stabilizing within the next 12 months, and

3 in 10 believe it could take up to 3 years. (Ipsos Egypt) 27 June 2022 Source: https://www.ipsos.com/en-eg/views-inflation-egypt AFRICA

747-749-43-07/Polls Almost 9 In 10 Nigerians

Attest To High Incidence Of Child Abuse In Nigeria

A new public opinion poll conducted by

NOIPolls has revealed that child abuse is prevalent in Nigeria, as disclosed

by 88 percent of adult Nigerians nationwide. Also, the poll revealed that 51

percent of adult Nigerians acknowledeged that they had personally seen

children undergo abusive treatment in their localities. The South-South (57

percent) and North-West (56 percent) zones had more respondents who made this

assertion. This is indeed a worrisome figure and everything possible must be

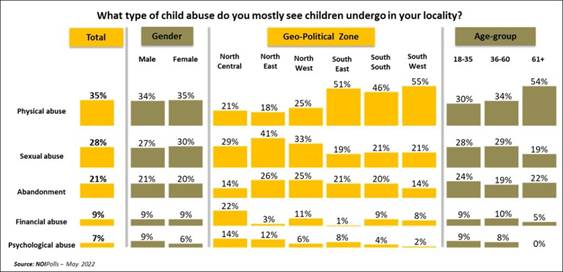

done to curtail this act as soon as possible. The poll result also unearthed the types of

child abuse children undergo in their locality and they include physical

abuse (35 percent), sexual abuse (28 percent) and abandonment (21 percent)

amongst other types. A higher percentage of adult Nigerians nationwide cited

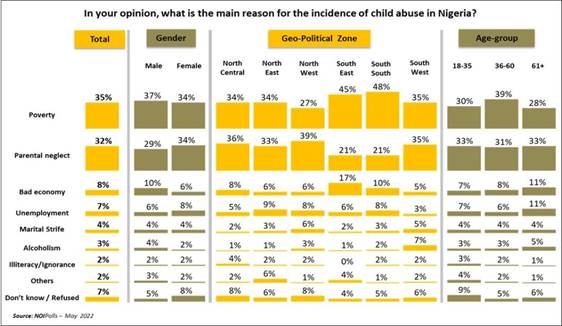

poverty (35 percent) and parental neglect (32 percent) as the main causes of

child abuse in the country. Impairing the future of children by

abusing their freedoms and rights is equal to impairing their

development, our national development and our

tomorrow’s society. Hence, it is essential that the issue of child abuse is

properly dealt with at individual , family, organizational

and governmental levels for development and

tomorrow’s good. It is therefore pertinent that awareness on

the effect of child abuse (28 percent), improving the economy (20 percent),

job creation, enacting and enforcing strict legislation on child abuse (22

percent each) as recommended by the respondents be adopted by key players as

a way of reducing the incidence of child abuse in the country. These are some

the key findings from the child abuse poll conducted by NOIPolls

in the week commencing 16th May,

2022. Survey Background The menace of child abuse has been an age

long practice that has derailed the lives of many children from the rightful

path of positive development thereby giving them a bleak, hopeless and

undesirable future. It is a menace that has been allowed to thrive for long

due to ineffective policies put in place by stakeholders thereby leading to

undesirable outcomes for the children involved in such menace. Child abuse is

any intention to harm or mistreat a child under 18 years. It is not just

physical violence directed at a child but any form of maltreatment by an

adult which is violent or threatening to a child. Child abuse can be meted on

a child by parents, family members, care givers, nursery workers, teachers

and sports coaches. Child abuse can occur in different forms which include

physical, emotional, abandonment, psychological, sexual and financial. A world health organization report

stated that nearly 3 in 4 children or 300 million children aged 2-4 years

regularly suffer physical punishment and or psychological violence at the

hands of parents or caregivers, it also stated that one in 5 women and 1 in

31 men report having been sexually abused as a child aged 0-17 years and

additionally, 120 million girls and young women under 20 years of age have

suffered some form of forced sexual contact[1]. UNICEF statistics show that abuse in all

its forms is a daily reality for many Nigerian children and only a fraction

receive help. It further stated that Six out of 10 children experience some

form of violence, and one in four girls and 10 percent of boys have been

victims of sexual violence[2]. It is believed that child abuse can be

precipitated by factors such as poverty, unemployment, marital strife,

alcoholism, difficult pregnancy and delivery, lack of knowledge of child

development and a lot of other factors. It’s effect can better be imagined as

it includes extreme stress which can impair the development of the nervous

and immune system. Other effects include perpetrating or being a victim of

violence, depression, obesity, high-risk sexual behaviors, unintended

pregnancy, alcohol and drug misuse. Measures to prevent and curb the menace

of child abuse include parental and caregiver support, educating the children

and encouraging life skills approaches, creating programs to prevent sexual

abuse and exploitation, encouraging interventions to build a positive school

climate, imbibing norms and value approaches, implementation and enforcements

of laws to prohibit violent punishment and to protect the child. Implementing

these solutions proffered will go a long way in curbing the menace of child

abuse. Against this backdrop, NOIPolls conducted a survey on child abuse to

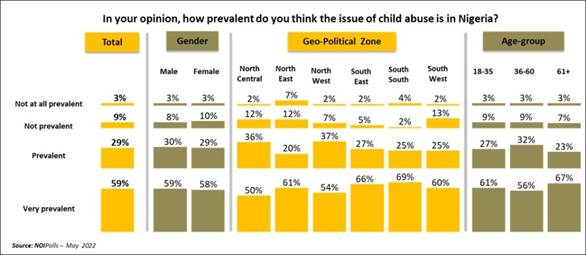

gauge the pulse of Nigerians. Survey Findings The first question sought to gauge the

opinion of adult Nigerians regarding the prevalence of child abuse. The poll

result reveal that majority of adult Nigerians (88 percent) stated that child

abuse is prevalent across the country. This incidence cuts across gender,

geographical locations and age-group with at least 81 percent representation.

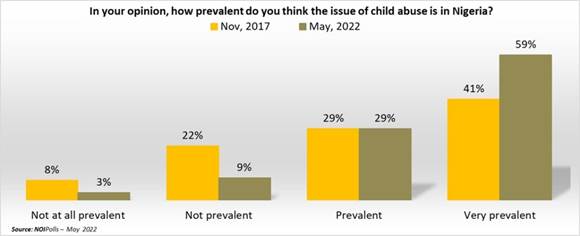

Trend analysis shows an 18 percent increase

in the proportion of Nigerians who stated that child abuse is prevalent in

Nigeria when current findings are compared with the result of the poll

conducted in 2017.

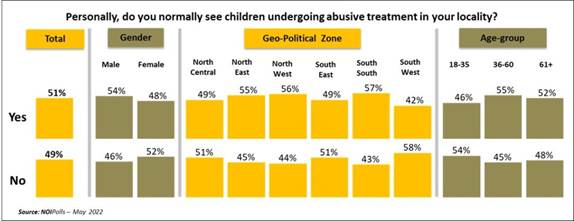

With regards to practice, the poll revealed

almost a split as 51 percent of adult Nigerians acknowledged that they have

personally seen children undergone abusive treatment within their locality.

Nigerians residing in the South-South (57 percent) and North-West (56

percent) zones accounted for respondents with this assertion.

Trend analysis shows a 1 percent increase in

the proportion of adult Nigerians who mentioned that they have seen children

undergone abusive treatment when current result is compared to the result

obtained in 2017

Interestingly, the poll revealed that

physical abuse (35 percent), sexual abuse (28 percent) and abandonment (21

percent) are the top three abuse children go through in their locality. The

South-West zone (55 percent) had more Nigerians who mentioned physical abuse

while the North-East zone accounted for a larger share of respondents who

stated sexual abuse (41 percent) and abandonment (21 percent).

Additionally, when respondents were asked

to state reasons for child abuse, the poll showed that 35 percent of the

respondents reported that poverty is one of the main reasons for child abuse

in Nigeria. The South-East and the South-West zones had more respondents with

this assertion. This is closely followed by parental neglect and bad economy.

Furthermore, respondents were asked if they

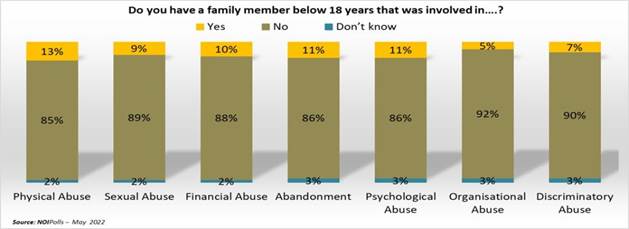

know any family member below 18 who has experienced some form of child abuse.

The poll result revealed that 13 percent of respondents know a family member

who was involved in physical abuse while 9 percent stated they know a family

member involved in sexual abuse. Others include financial abuse (10 percent),

abandonment and psychological abuse (11 percent each) amongst other abuses.

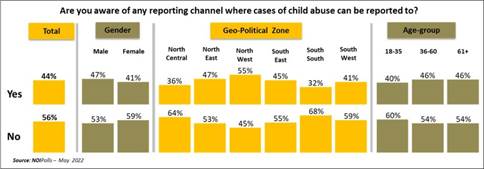

Subsequently, the poll revealed that 44

percent of adult Nigerians are not aware of any reporting channel for child

abuse cases. Nigerians residing in the North-West had more respondents who

disclosed this. On the contrary, 56 percent claimed to know where they can

report cases of child abuse.

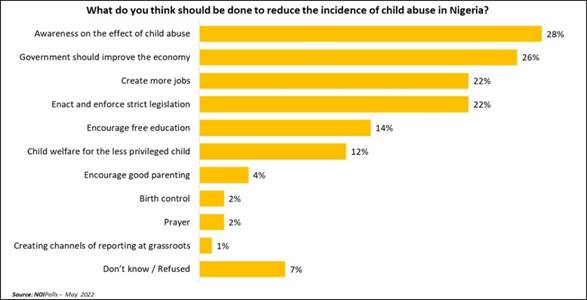

Awareness on the effect of child abuse (28

percent), improving the economy (20 percent), job creation, enact and enforce

strict legislation ( 22 percent each) were some of the recommendations made

by the respondents as a way of reducing the incidence of child abuse in the

country. Other mentions includes encouraging free education (14 percent),

child walfare for the less privileged children (12 person) and encourage good

parenting (4 percent) amongst others.

Conclusion In conclusion, the poll results have shown

a high prevalence of child abuse in the country. Given this high prevalence

and the proportion of Nigerians who have witnessed an incidence of child

abuse in their locality, it is ensential that the Federal, State, Local

government and other stakeholders synergize and champion the course of

violence against children and focus on an enlightenment campaign as

recommended by 28 percent of the respondents. Also, strengthening and

enforcing relevant legislative and policy frameworks in the course of

protecting the Rights of the Nigerian Child as advocated by 22 percent of the

respondents is key. Finally, in order to achieve the Sustainable

Development Goal, SDG, to end all forms of violence against children by 2030,

it is imperative for the Federal Government to persuade the remaining 11

States in Nigeria that are yet to pass the Child Right Act of 2003 to do so

urgently so as to fully criminalize the despicable act, therefore providing

Nigerian children the opportunity where they are nurtured in a safe and

secure environment. (NOI Polls) June 16, 2022 Source: https://noi-polls.com/child-abuse-poll-report/ 747-749-43-08/Polls Young Adults Aged 15 – 29

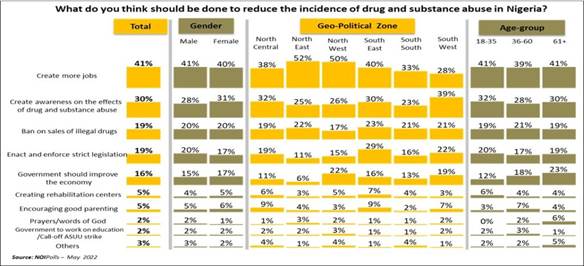

Years Old Are Most Known Abusers Of Drugs & Substances In Nigeria

A new public

opinion poll conducted by NOIPolls has revealed that most abusers of drugs

and substances in the country are young Nigerians aged between 15 and 29

years as stated by 88 percent of adult Nigerians interviewed. This figure

leaves much to be desired as the menace of drug and substance abuse continue

to ravage and destroy the lives of many youths. The Chairman of the National

Drug Law Enforcement Agency (NDLEA), Buba Marwa, lamented over the pervasive

abuse of (cannabis) substance in the country, revealing that about 10.6 million

Nigerians are actively abusing the substance.[1] He made this statement in 2021 in

Abuja during the launch of War Against Drug Abuse in commemoration of the United

Nations International Day against drug abuse and illicit drug trafficking. More

findings indicated that the most abused illicit drug or substances in Nigeria

is marijuana, as cited by 41 percent of the respondents. This is followed by

Codeine (22 percent) and Alcohol (17 percent) amongst other drugs and

substances mentioned. Furthermore, when asked about the causes of drug and

substance abuse, the top three causes cited are peer pressure and

unemployment, both at 33 percent each, parental neglect (26 percent) and

poverty (17 percent). With regards

to curbing this menace, while 41 percent recommended that jobs should be

created to engage those involved in this act, 30 percent suggested that there

should be awareness campaigns on the effect of drug and substance abuse.

There is an urgent need to give young Nigerians evidence-based information on

addiction and other drug-related harm, this will curtail drug experimentation

and the growing culture of intoxication. Finally, the government and

stakeholders involved in the fight against drug and substance abuse should

expedite action and stamp out this menace to avoid the unwanted and

unwarranted ravenous consequence on those involved in the abuse of drugs and

substance. These are

key findings of the drug and substance abuse poll conducted on the week

commencing 16th May 2022. SURVEY

BACKGROUND On June

26th, the International Day against Drug Abuse and Illicit Trafficking was

commemorated. This day is set aside by the United Nations to recap the goals

established by stakeholder states towards eradicating drug abuse and

attaining an international society that is free of drug abuse. This is done

mainly by creating awareness and educating youths and adults on the hazardous

and social effects of substance abuse, and to guard against it. The theme for

the 2022 commemoration was “Addressing drug challenges in health and

humanitarian crises”. Drug abuse

is a menace that has derailed the lives of many people into oblivion and

untimely death due to its adverse effects on the body. It has festered for

such a long time and has continued to stamp its catastrophic effects on its

users for such a long spell. Drug abuse is the use of illegal drugs, the use

of prescription drugs or over-the-counter drugs for purposes other than those

for which they are meant to be used, or in excessive amounts. Drug abuse may

lead to social, physical, emotional, and job-related problems. Examples

of drugs taken and abused include alcohol, tobacco, cannabis,

methamphetamines, synthetic drugs, cocaine and non-medical use of

prescription drugs. According to

world drug report by the United Nations office on Drugs and Crime, 275

million people used drugs worldwide while 36 million people suffered from

drug use disorders.[2] The report further stated that in the

last 24 years, cannabis potency had increased by as much as four times in

different parts of the world. Additionally, in the last 10 years, the number

of drug users has increased by 22 percent owing to global population growth.

The report further stated that 5.5 percent of population aged 15 and 64 years

have used drugs at least once, while 36.3 million people or 13 percent of the

total number of persons who used drug, suffer different and adverse effects

of drug use disorder. More so, in Nigeria, there are around 14.3 million drug

users and 3 million of them suffer drug use disorder. It is further believed

that globally, over 11 million people are estimated to inject drugs, half of

whom are living with hepatitis C and opioids continue to account for the

burden of disease attributed to drug use[3]. The factors

that lead people into drug abuse include absence of social support, use of

drugs amongst peers, socio-economic status, stress, and ability to cope with

it. It also includes parental and familial involvement, history of abuse or

neglect, and a history of compulsive behaviour. The risk factors of substance

abuse include social pressure, adverse childhood experiences, use of drugs

that are highly addictive, mental health problem as well and family history[4]. More so, the effect of drug abuse can be

devastating, and it includes depression, anxiety, panic disorder, increased

aggression, paranoia, and hallucination.[5] Against this backdrop, NOIPolls

conducted its latest poll on drugs and substance abuse in Nigeria to explore

the awareness of Nigerians regarding the most abused drugs and substance in

Nigeria; the predominant age group of abusers; causes of drugs and substance

abuse, as well as possible solutions. Survey

Findings The first

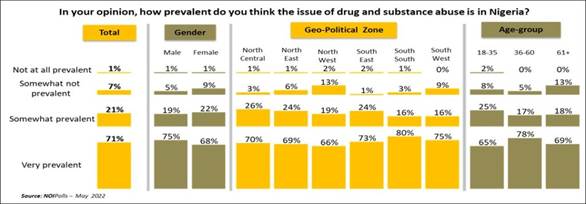

question sought to know the prevalence rate of drug and substance abuse, and

the poll result revealed that 92 percent of adult Nigerians nationwide attest

that drug and substance abuse is prevalent. On the other hand, 8 percent

stated that drug and substance abuse is not prevalent.

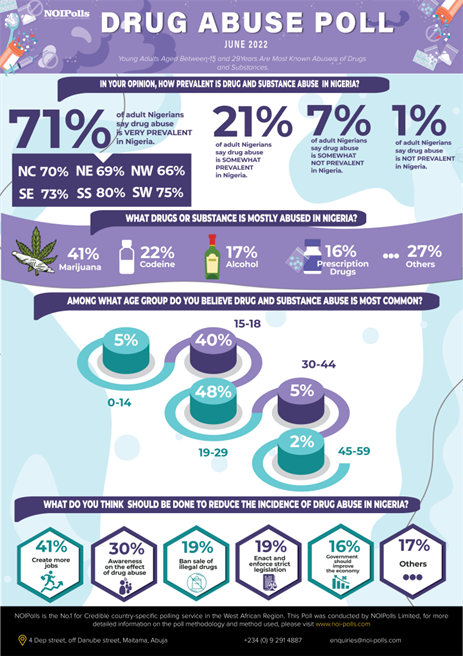

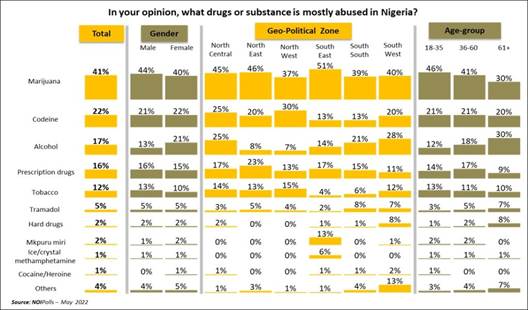

The poll

results also sought to know the opinion of Nigerians regarding the drug or

substance that is mostly abused. The findings showed that 41 percent of the

respondents stated that Marijuana is the most abused drug or substance and

South-East region (51 percent) has the larger proportion of respondents who

stated this. This is followed by 22 percent of the respondents who say

codeine is mostly abused, and the North-West region (30 percent) had more

respondents who made this assertion. Other drugs and substances cited include

Alcohol (17 percent), prescription drugs (16 percent), tobacco (12 percent),

tramadol (5 percent) and hard drugs (2 percent) amongst others.

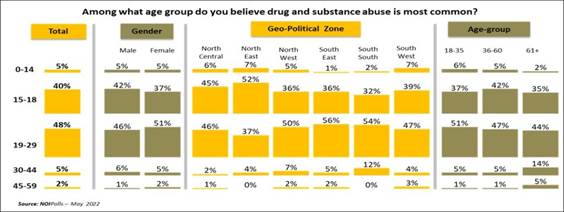

Subsequently,

insight on age-group revealed that those aged between 15 – 29 years accounted

for the largest proportion (88 percent; (15 – 18 years) 40 percent + (19 – 29

years) 48 percent) of Nigerians associated with the abuse of various drugs

and substances in the country.

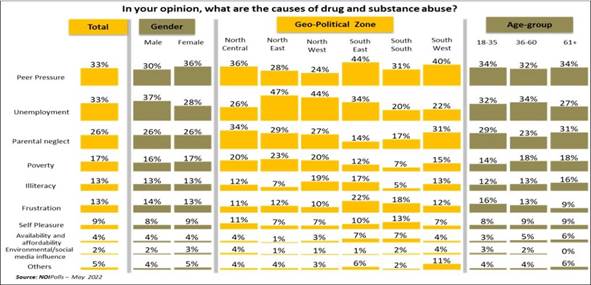

Furthermore,

the poll revealed that peer pressure and unemployment (33 percent each) are

perceived as the main cause of drug and substance abuse in the country. This

is followed by parental neglect and poverty, as mentioned by 26 percent and

17 percent of the respondents respectively. Other causes of drugs and

substance abuse revealed from findings include ‘illiteracy’ (13 percent),

‘frustration’ (13 percent), and ‘self-pleasure’ (9 percent) amongst other

causes.

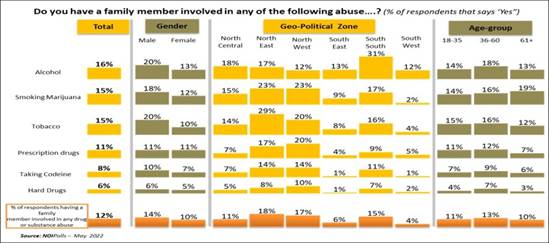

Also,

respondents were asked if they have a family member involved in drug and

substance abuse, and the poll result revealed that 16 percent of the

respondents stated that their family members are involved with alcohol abuse.

Similarly, while 15 percent stated that their family members are involved in

smoking marijuana, another 15 percent mentioned tobacco and 11 percent of the

respondents also stated that their family members are involved in taking

prescription drugs.

With regards

to curbing this menace, 41 percent of the respondents suggested that jobs

should be created, while 30 percent recommended that awareness on the effects

of drug and substance abuse should be created. Other solutions proffered

include ban of the sale of illegal drugs, and the need to enact and enforce

strict legislation, both of which tied at 19 percent. 16 percent of

respondents also stated that government should improve the economy.

Conclusion In

conclusion, findings from the poll have revealed that 92 percent of Nigerians

admitted that there is a high prevalence of drugs and substance abuse in the

country especially amongst teenagers and young adults aged between 15 and 29

years. The poll also indicated that the top three drugs or substances mostly

abused are Marijuana, Codeine, and alcohol. With regards

to curbing this menace, while 41 percent recommended that jobs should be

created to engage those engaged in this act, 30 percent suggested that an

awareness on the effect drug and substance abuse will help curb the threat.

There also is an urgent need to give young Nigerians evidence-based

information on addiction and other drug-related harm. This will curtail drug

experimentation and the growing culture of intoxication. Finally, government

and stakeholders involve in the fight against drug and substance abuse should

expedite action and stamp out this menace to avoid the unwanted and

unwarranted ravenous consequence on those involved in the abuse of drugs and

substance. (NOI Polls) June 23,

2022 Source: https://noi-polls.com/drug-and-substance-abuse-poll-release/ 747-749-43-09/Polls Internet Access Of All Adult South Africans, 85%

Young people in South Africa are definitely

well-connected, with 98% having access to a cellphone, albeit not always a

smart phone. In addition, a remarkably high proportion (92%) of young people

between the ages of 18 and 24 have also indicated that they have access to

the internet, although many of them do not have access at home, work, or an

educational institution, most have access via their mobile phones. (Internet

access of all adult South Africans is 85% - also mainly via mobile phone.) Young South African adults do very well

when it comes to being able to understand different languages, especially

English that is seen as a lingua franca among them – no doubt fuelled by the

important role played by English in using either a mobile phone or the

internet. These are some of the findings of a

Khayabus study that Ipsos undertook at the end of 2021. A total of 3,600

interviews were conducted with adult South Africans from the last week of

November to the end of December 2021. During the height of the Covid-19 pandemic

countless jobs were lost, many of them by young people, therefore it is

relevant to have a look at the current work status of the young people in our

country – are they making inroads into the labour market and finding work? Unfortunately, looking at the next graph,

it is clear that young people do not feature much in different categories of

occupations when compared to the figures for all adults in South Africa. Far

more young people will have to gain access to the formal employment market in

the country for this situation to change. Perhaps this explains a bit of the fact

that a higher proportion of young people between the ages of 18-24 are

receiving government grants than in the population as a whole:

Somewhat surprisingly, the opinions

expressed by young people and all adult South Africans were almost on a par,

looking at those who either strongly agree or agree with a few opinions on

politics, political parties, and elections in our country: Apart from the fact that these figures look

rather similar it is a worry that less than half of South Africans in all

adult age groups agree with these opinions. It shows the phenomenon that

developed over the last number of years that voters became more and more

disillusioned in political parties (and politicians). This feeling of

disillusionment manifested in the low turnout of last year’s local government

election. The disillusionment can possibly explain

why less than half feel that elections are free and fair or are expressing

the will of the people – these are basic features of a democracy that are not

obvious to South Africans and also not clear to young South Africans. Even more

worrying is the opinion that, despite the assurances of the South African

constitution, only just more than a third agrees that all South Africans have

equal rights. Looking forward, a similar proportion of

young people and all South Africans (45%) expressed the view that they have

confidence in a happy future for people of all population groups in this

country. Although this is not exactly a low score, it is disappointing that

less than half of people feel this way. All in all, these findings support a view

that the “democratic project” in South Africa needs a lot more positive

support – from civil society, from concerned South Africans, but also from

government. (Ipsos South Africa) 15 June 2022 Source: https://www.ipsos.com/en-za/youth-features-politics-and-future WEST

EUROPE

747-749-43-10/Polls One In Seven Secondary School Teachers Say They Face Violence From

Pupils At Least Once A Month

Teachers in Britain say disruptive and violent pupils ruin

teachers’ lives, causing physical injury and career-ending psychological

harm. Recently, a London teacher received

£850,000 in compensation after being punched in the face and kicked

by a pupil with a history of violence. Teachers experience regular aggression and even violence from school

children, according to new YouGov research. One in seven secondary school

teachers (15%) say they experience violence from a pupil at least once a

month, including 5% who say they are subject to attacks at least once a week.

In addition, around half of secondary school teachers (47%) say they

experience aggressive behaviour from a student at least once a month,

including three in 10 (28%) who say this happens at least once a week. One in

14 (7%) teachers say they deal with aggressive pupils every single day. Teachers also have to deal with the belligerent behaviour of angry

parents – one in seven (15%) teachers say parents are aggressive with them on

at least a monthly basis. (YouGov UK) June 15, 2022 747-749-43-11/Polls Seven In Ten People Say The Early Years Should Be More Of A Priority

For Society

The Royal Foundation Centre for Early Childhood has today unveiled

the findings of new research into early childhood development, as The Duchess

of Cambridge and the Centre host a roundtable with the early years sector,

Ministers and senior civil servants to discuss the results and the broader

importance of early childhood development to society. Conducted by Ipsos UK on behalf of The Royal Foundation Centre for

Early Childhood, the research comes two years after The Duchess’s landmark

survey – ‘5 Big Questions on the Under-Fives’ – which attracted the largest

ever response to a public survey of its kind with over 500,000 responses in

one month, sparking a national conversation on the early years. The research published today delves even deeper into public

perceptions of early childhood, focusing on three key areas: the