|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 744 Week:

May 23 – May 29, 2022 Presentation:

June 03, 2022 4

In 5 (80%) Islamabadis Believe That The Federal Capital Is In Need Of A Good

Transport System Nine

In Ten S’pore Adults Still Wear A Mask Outdoors, Despite No Longer Being

Mandated To Almost

7 In 10 Nigerians Describe The Current State Of Security In The Country As

Dreadful 44%

Saying They Had Been Forced To Cut Back On Their Clothing Purchases Four

In 10 Britons Are Worried About Catching Coronavirus On An Airplane 59%

Of Britons Want Johnson To Resign In Wake Of Gray Report Public

Concern About Inflation Reaches Its Highest Level For 40 Years One

In Five Britons Now Say They Are Struggling Or Unable To Make Ends Meet Less

Than Half (45%) Of Teachers Would Enter The Profession If Given The Choice

Again Cryptocurrencies

And NFTs: What Do The Spanish Think Iceland’s

Cost Of Living Discount For The Over-60s Boosts Brand Health Americans

Knowledge About International Affairs Americans'

Recent Attitudes Toward Guns 52%

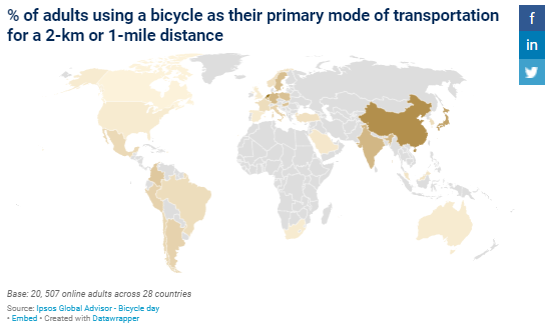

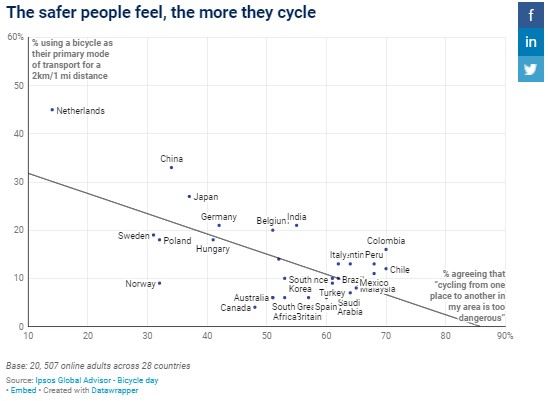

Globally Say Cycling In Their Area Is Too Dangerous, A 28 Country Survey Globally,

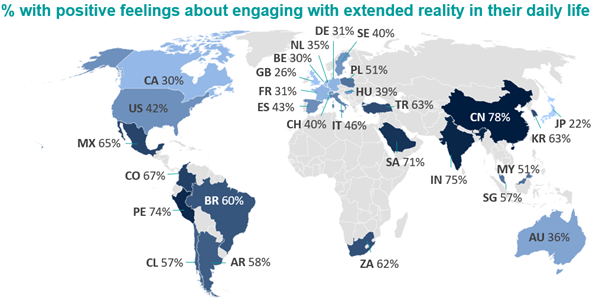

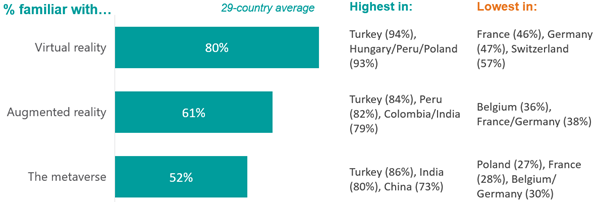

About Half Of Adults Across 29 Countries Say They Are Familiar With The

Metaverse (52%) INTRODUCTORY NOTE This weekly report consists of twenty

two surveys. The report includes five

multi-country studies from different states across the globe. 744-43-23/Commentary: Nine In Ten

S’pore Adults Still Wear A Mask Outdoors, Despite No Longer Being Mandated To

Singapore

saw its most significant easing of safe management measures in end-April

as caps

on group sizes, capacity limits, and mandates on wearing a mask outdoors were

removed, among others. While people in Singapore

no longer have to wear a mask outdoors, nine in ten

continue to (93%), with Gen Zs (98%) and Baby Boomers (97%) most likely to do

so. Conversely, Millennials were most likely to say they never wear a mask

when outdoors (11%). A closer

look at the frequency of outdoor mask-wearing indicates that the largest

proportion of Singapore adults say they wear a mask outdoors all the time

(49%), with Baby Boomers significantly more likely to say so (58%). A fewer

one in five Singapore residents say they sometimes (20%) or often wear a mask

outdoors (24%).

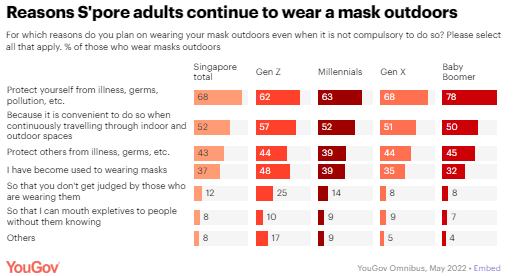

Protecting

oneself from illness and germs was the top reason for continuing to wear a

mask outdoors among the general population (68%) and all age groups. Around

half also felt that doing so was the most convenient way to travel between

outdoor and indoor settings (52%), since masks are still required when

indoors. Protecting others from germs was the third most popular reason cited

for wearing a mask outdoors despite it not being compulsory (43%). Just under

four in five say they continue to wear their masks because they have become

used to doing so (37%). Gen Zs were most likely to express this opinion, with

almost half feeling this way (48%). Gen Zs were

also most likely to say they do not remove their masks to not get judged by

those who are wearing them, with a quarter saying so (25%) compared to a

fewer one in ten of the general population (12%).

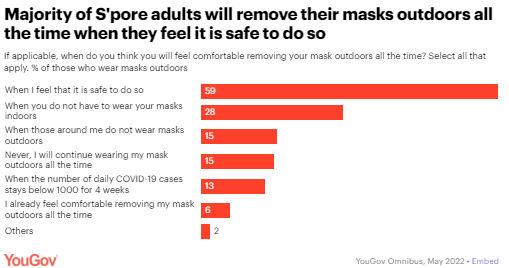

As for when residents

will feel comfortable removing their masks outdoors all the time, majority

said they would only do so once they feel it is safe (59%). Almost three in

ten said they would make the change if the rules making mask-wearing indoors

compulsory are removed (28%). A further

one in seven would always remove their mask outdoors when those around them

do the same (15%), or when the daily case count falls below 1,000 for four

weeks (13%), while another seventh say they will never change their

mask-wearing behaviour (15%). One in

twenty already feel safe removing their masks outdoors, but do not do it all

the time (6%).

(YouGov

Singapore) May 27, 2022 Source: https://sg.yougov.com/en-sg/news/2022/05/27/nine-ten-spore-adults-still-wear-mask-outdoors-des/ SUMMARY

OF POLLS

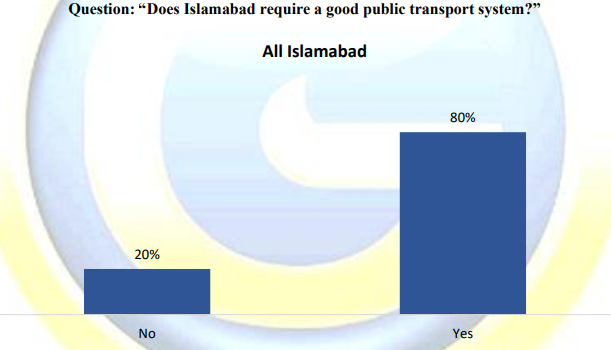

ASIA (Pakistan) 4 In 5 (80%) Islamabadis Believe That The

Federal Capital Is In Need Of A Good Transport System According to a survey conducted by Gallup

& Gilani Pakistan, 4 in 5 (80%) Islamabadis believe that the federal

capital is in need of a good transport system. A

full report on the survey can be found here. A nationally representative

sample of adult men and women from across the capital was asked the following

question, “Does Islamabad require a good public transport system?” In

response to this question, 80% said yes and 20% said no. (Gallup Pakistan) May 26, 2022 (Singapore) Nine In Ten S’pore Adults Still Wear A

Mask Outdoors, Despite No Longer Being Mandated To Singapore saw its most significant easing

of safe management measures in end-April as caps on group sizes, capacity limits, and

mandates on wearing a mask outdoors were removed, among others. While people in Singapore

no longer have to wear a mask outdoors, nine in ten

continue to (93%), with Gen Zs (98%) and Baby Boomers (97%) most likely to do

so. Conversely, Millennials were most likely to say they never wear a mask

when outdoors (11%). (YouGov Singapore) May 27, 2022 AFRICA (Nigeria) Almost

7 In 10 Nigerians Describe The Current State Of

Security In The Country As Dreadful A new public opinion poll conducted by

NOIPolls has revealed that 68 percent of adult Nigerians nationwide have

described the current state of security in the country as insecure. This is

not far-fetched as the country has been besieged with all kinds of security

challenges ranging from kidnapping, banditry, herdsmen attack, terrorism, and

the activities of separatists’ movements. Additionally, analysis across

geo-political zones showed that the South-East (78 percent) and the North-West

(75 percent) zones had the larger proportion of adult Nigerians who made this

assertion. (NOI Polls) May 27, 2022 WEST

EUROPE (UK) 44%

Saying They Had Been Forced To Cut Back On Their

Clothing Purchases As the cost-of-living crisis continues to

bite, a new YouGov survey reveals how many Britons have been forced to make

spending reductions on 24 areas of household spending. Clothing tops the

list, with 44% saying they had been forced to cut back on their clothing

purchases since November. This most common form such cuts take is people

reducing their spending by buying clothes less frequently (29%), although 10%

are switching to cheaper alternatives and 8% say they have been forced to

stop spending money on clothes altogether. (YouGov UK) May 23, 2022 Four

In 10 Britons Are Worried About Catching Coronavirus On

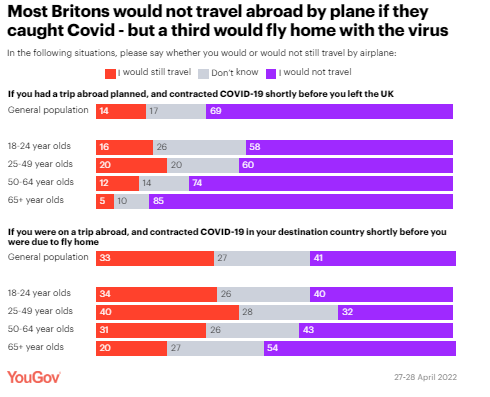

An Airplane YouGov research reveals that most Britons

would not take a flight abroad if they caught Covid before they left the

country, despite not being legally required to – although a third would bring

the virus back to the UK if they contracted it before flying home. Just one

in seven Britons (14%) say they would still fly if they had a trip abroad

planned and contracted Covid-19 shortly before they left the UK, with seven

in 10 (69%) saying they would not travel, and 17% unsure. (YouGov UK) May 23, 2022 59% Of Britons Want Johnson To

Resign In Wake Of Gray Report The much-awaited Sue Gray report has been published, revealing the

details of many gatherings taking place in Downing Street in contravention to

the lockdown rules in place at the time. Few Britons want him to, however, as

most Britons continue to think Johnson should resign (59%). This has changed

little from the 57% it was on 4 April, when it was announced Johnson had

received a fixed penalty notice. Three in ten (30%) currently think Johnson

should remain in office, the same as the proportion who thought so in early

April. (YouGov UK) May 25, 2022 Public Concern About Inflation Reaches Its Highest Level

For 40 Years The May 2022 Ipsos Issues Index confirms

that public concern about inflation and prices continues to rise. Forty-one

per cent of the British public mention cost-of-living issues as a big concern

for the country, up from 32% last month. This is the highest level of public

concern recorded since the Issues Index became a regular monthly poll in the

early eighties, although still behind the peaks it reached in the 1970s and

very beginning of the 1980s. In April 1980, 69% saw inflation as a big

concern, but by the next recorded measure in September 1982 this had fallen

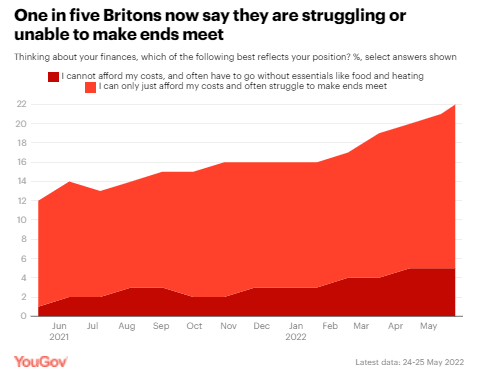

to 32%. (Ipsos MORI) 25 May 2022 One In Five Britons Now Say They Are Struggling Or Unable To Make Ends Meet A new YouGov survey reveals the extent of

the damage to people’s finances, with the number of people saying they are

struggling or unable to make ends meet doubling in the last year. One in six

Britons (17%) say of their household financial situation: “I can only just

afford my costs and often struggle to make ends meet”. This figure has risen

from 11% in mid-May 2021. A further 5% say “I cannot afford my costs, and

often have to go without essentials like food and heating”, a figure that was

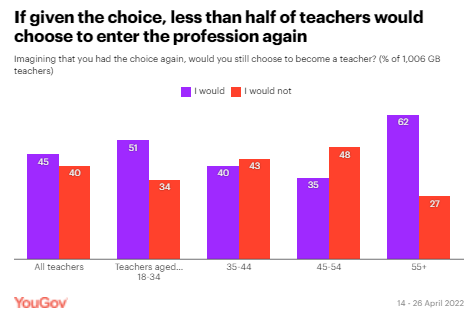

1% last year. (YouGov UK) May 26, 2022 Less Than Half (45%) Of Teachers Would

Enter The Profession If Given The Choice Again It may be

unsurprising then, that a new YouGov survey of teachers suggests many may be

feeling disillusioned with their career choice. Fewer than half (45%) say

that if they could choose again, they would still choose to become teachers.

Two in five (40%) would not choose to become a teacher again. The youngest

and the oldest teachers are the happiest with their choice of career, being

the most likely to say they would repeat it. Half of teachers aged 18 to 34

(51%) and 62% of those aged 55 and above say they would make the same choice

to teach again. (YouGov UK) May 27, 2022 Half Of Britons Believe Prince Charles Will Be A

Good King, Even As Two-Thirds Want The Queen To Remain Monarch For As Long As

Possible As the Prince of Wales takes on more roles,

such as reading the Queen’s Speech at the opening of State Parliament, new

research by Ipsos shows half of Britons expect Prince Charles to do a good

job as King (49%), while 1 in 5 do not (20%). This is similar to the public’s views earlier this year in March. While

Britons are more likely to expect good things from the heir than not,

expectations for Prince William are even higher. Three-quarters believe the

second in-line to the throne will be a successful monarch (74%), only 7%

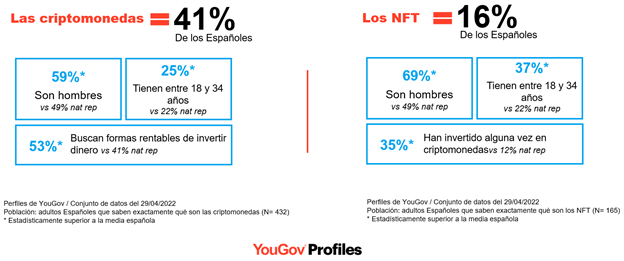

think he will do a bad job. (Ipsos MORI) 27 May 2022 (Spain) Cryptocurrencies And NFTs: What Do The

Spanish Think Cryptocurrencies and NFT's attract more and

more Spaniards, who decide to learn about and invest in them. A study

carried out in May 2022 by YouGov Spain highlights that: Despite

the fact that 90% of Spaniards have ever heard of cryptocurrencies,

only 41% claim to know exactly what it is, and only 12% have already invested

in cryptocurrencies. The same goes for NFTs, with only 16% claiming to

know exactly what they are and 6% of the population have already invested in

NFTs. (YouGov Spain) (Iceland) Iceland’s Cost Of Living Discount

For The Over-60s Boosts Brand Health Iceland recently announced that, starting

from May 24, customers over the age of 60 would receive a 10% discount on

their grocery shopping in the store every Tuesday. The move is motivated by

the concerns older shoppers have experienced around the cost-of-living crisis

– which has seen energy bills and food prices

rise, among other things, in recent months. Iceland’s intervention is a timely

intervention for older consumers who may struggle to keep up with rising

costs – and a potential PR coup for a brand that’s already closely identified

with lower grocery prices. (YouGov UK) May 27, 2022 NORTH AMERICA (USA) Americans Knowledge About International Affairs A new Pew Research Center survey shows,

Americans are less familiar with other topics. Despite the U.S. government labeling the events in Xinjiang, China, as genocide, only

around one-in-five Americans are aware that it is the region in China with

the most Muslims per capita. And only 41% can identify the flag of the second

most populous country in the world, India. Americans give more correct than

incorrect answers to the 12 questions in the study. The mean number of

correct answers is 6.3, while the median is 7. (PEW) MAY 25, 2022 One-Third Of Americans Say The

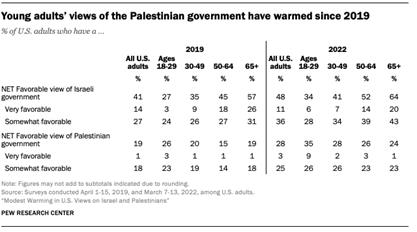

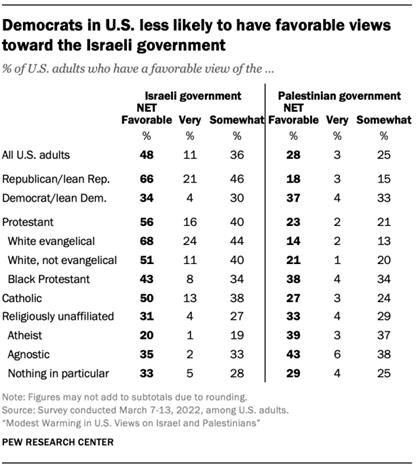

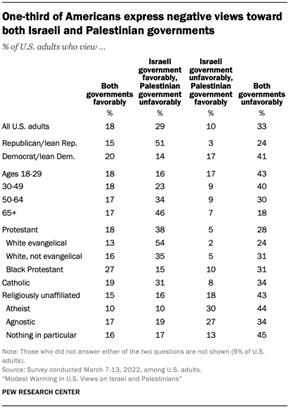

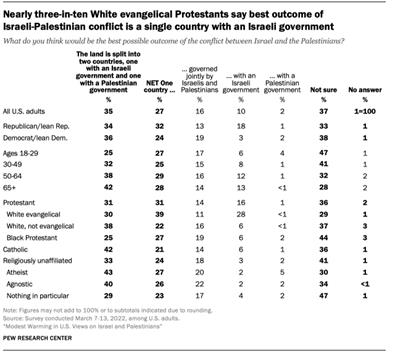

Best Possible Outcome Between Israel And The Palestinians Is A Two-State Solution In recent years, U.S. public opinion has

become modestly more positive toward both sides in the Israel-Palestinian

conflict, according to a new Pew Research Center survey. Overall, Americans

continue to express more positive feelings toward the Israeli people than

toward the Palestinian people – and to rate the Israeli government more

favorably than the Palestinian government. But these gaps are much

larger among older Americans than among younger ones. Indeed, U.S. adults

under 30 view the Palestinian people at least as warmly (61% very or somewhat

favorable) as the Israeli people (56%) and rate the Palestinian government as

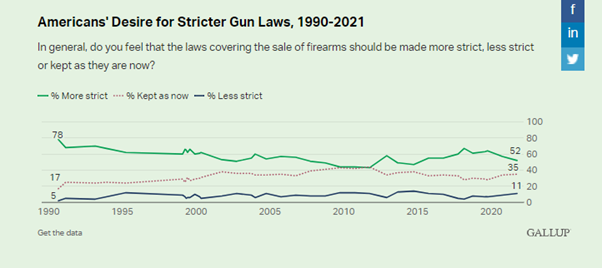

favorably (35%) as the Israeli government (34%). (PEW) MAY 26, 2022 Americans' Recent Attitudes Toward Guns As Americans are reeling from two mass

shootings that have occurred within 10 days of each other in the U.S., an

intense gun control debate has reignited across the country. Gallup's most

recent polling about guns was conducted in October 2021 and January 2022.

Both polls found a slight decrease in support for stricter gun laws compared

with the prior year's measures. Typically, Americans' support for stricter

gun laws has risen in the aftermath of high-profile mass shootings and fallen

during periods without such events. Additionally, changes in the party of the

president may also influence preferences for gun laws. (Gallup) MAY 26, 2022 (Canada) Ballot-Box Bonus Likely For

Progressive Conservatives As Their Voters Are Most Certain To Turn Out, Most

Committed To Their Choice The ten-point advantage that the

Progressive Conservatives have over the Liberals in the popular vote has the

potential to grow on election day with the Tories likely to receive a

ballot-box bonus at the polls, according to a new Ipsos poll conducted on behalf

of Global News. Overall, six in ten (61%) Ontarians say they’re completely

certain to vote on election day. This is close to the 58% turnout of the 2018

provincial election. Those who have declared their support for the

Progressive Conservatives are most likely (74%) to say they’re certain to

vote this time, ahead of NDP (71%), Liberal (65%) and Green Party (42%)

voters. (Ipsos Canada) 26 May 2022 AUSTRALIA Eight Magazine Categories Enjoy Strong Growth In 2021-22

Led By General Interest, Health & Family,

Motoring And Sports – All With Readership Up Year On Year Now 10.9 million Australians aged 14+

(51.5%) read print magazines, virtually unchanged on a year ago, according to

the results released today from the Roy Morgan Australian Readership report

for the 12 months to March 2022. This market broadens to 14.8 million

Australians aged 14+ (70%) who read magazines in print or online either via

the web or an app, a small drop of 3.7 per cent from a year ago. These are

the latest findings from the Roy Morgan Single Source survey of 65,365

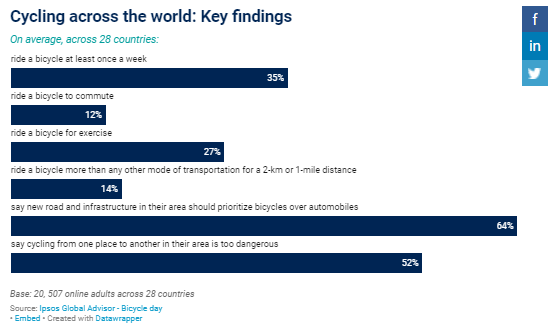

Australians aged 14+ in the 12 months to March 2022. (Roy Morgan) May 24 2022 MULTICOUNTRY STUDIES 52% Globally Say Cycling In Their

Area Is Too Dangerous, A 28 Country Survey A new Ipsos survey finds that most

adults across 28 countries consider cycling plays an important role in the

reduction of carbon emissions (on average, 86% do so) and in the

reduction of traffic (80%). However, half (52%) say cycling in their

area is too dangerous. The prevalence of cycling to run errands or to

commute is highest in countries where it is most widely perceived as a safe

mode of transportation such as China, Japan, and the Netherlands. In most

countries surveyed, a solid majority of citizens are in favor of giving

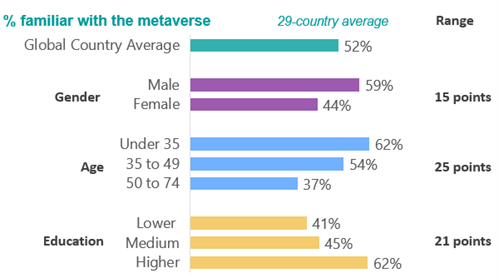

bicycles priority over automobiles in new infrastructure projects. (Ipsos MORI) 24 May 2022 Source: https://www.ipsos.com/en-uk/global-advisor-cycling-across-the-world-2022 Globally, About Half Of Adults

Across 29 Countries Say They Are Familiar With The Metaverse (52%) Less than half the Australian population

(44%) are familiar with the metaverse, while only 36% express positive

feelings about engaging with extended reality in daily life, a new global

survey conducted by Ipsos for the World Economic Forum finds. Globally, about

half of adults across 29 countries say they are familiar with the metaverse

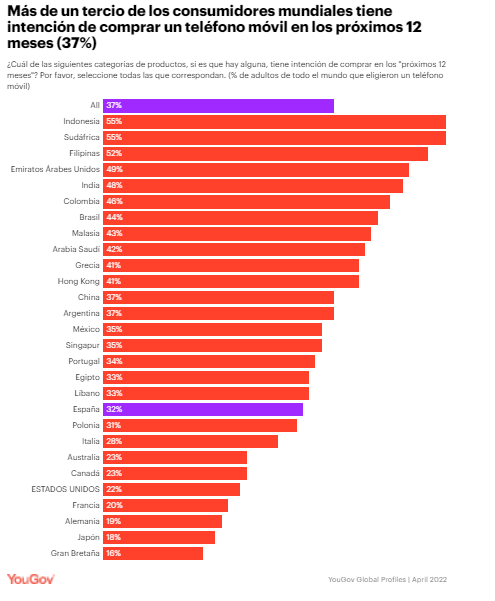

(52%) and 50% have positive feelings about engaging with it. (Ipsos Australia) 25 May 2022 In A Study Carried Out In 28 Countries, Consumers Are Asked

What Products They Intend To Buy In The Next 12

Months YouGov's latest tool, Global Profiles,

reveals the products consumers say they most intend to buy in the next 12

months. Global Profiles analyzes the thoughts, feelings, behaviors and habits of consumers, as well as global

trends and media consumption in 43 different markets. In this study, carried

out in 28 countries from among all the markets surveyed in Global Profiles,

consumers are asked what products they intend to buy in the next 12 months. The

data indicates that the sector should stock up on mobile phones, as the

highest percentage of consumers selected this category as the product they are most interested in buying (37%). (YouGov Spain) Source: https://es.yougov.com/news/2022/05/25/global-que-probabilidad-tienen-los-consumidores-de/ Re-Thinking The Drivers Of Regular

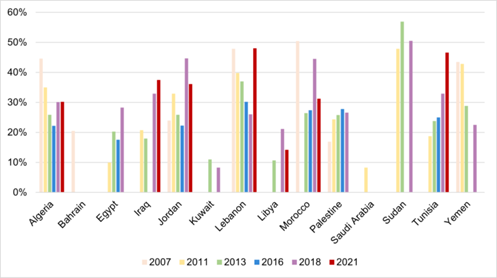

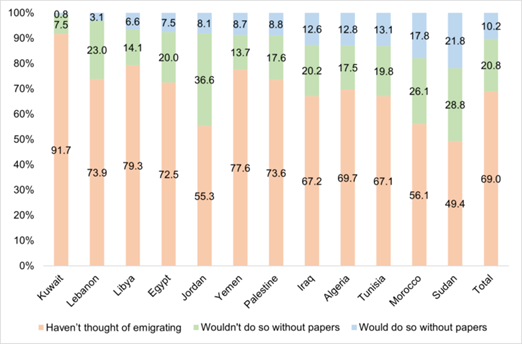

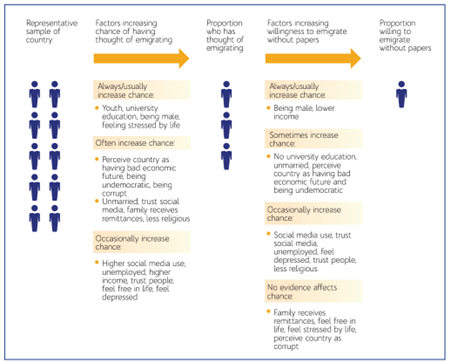

And Irregular Migration: Evidence From The MENA Region Across 12 Countries Based on data from the Arab Barometer,

which has conducted international standard social scientific surveys across

the Middle East and North Africa every two years since 2006 with sample sizes

of around 2400 per country based on area probability sampling and

face-to-face interviews. Uniquely, the penultimate, 2018/19 round of surveys

asked not only about desire to migrate but also about willingness to do so

irregularly, as well as a range of socio-demographic, attitudinal and

behavioral indicators. (Arabbarometer) May 26, 2022 Regarding Choice Of Holiday During

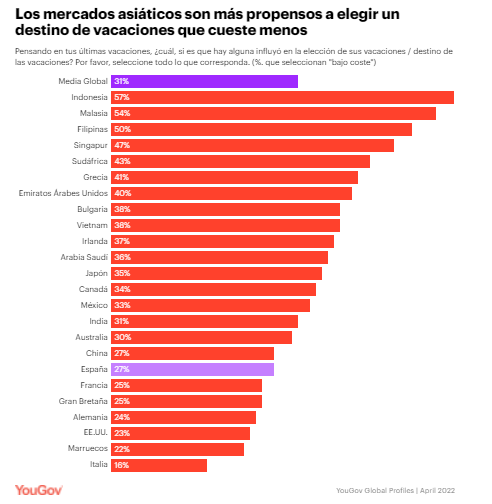

Most Recent Trip, Just Over A Third Of Global Respondents Choose Low Cost As

A Contributing Factor (31%) Among 24 Countries Data from YouGov's new tool, Global

Profiles, reveals the factors consumers take into account

when choosing a holiday destination. Individually, most Asian markets

outperform the global public. Indonesia (57%), Malaysia (54%), the

Philippines (50%) and Singapore (47%) are significantly more likely than

global consumers to say that low cost is an important factor. Consumers

from Vietnam (38%) and Japan (35%) have a lower percentage, but still more

than the global public. (YouGov Spain) Source: https://es.yougov.com/news/2022/05/26/global-en-que-medida-influye-el-coste-en-el-destin/ ASIA

744-43-01/Polls 4 In 5 (80%) Islamabadis Believe That The Federal Capital Is In Need Of A Good

Transport System

According to a survey conducted by Gallup

& Gilani Pakistan, 4 in 5 (80%) Islamabadis believe that the federal

capital is in need of a good transport system. A

full report on the survey can be found here. A nationally representative

sample of adult men and women from across the capital was asked the following

question, “Does Islamabad require a good public transport system?” In

response to this question, 80% said yes and 20% said no.

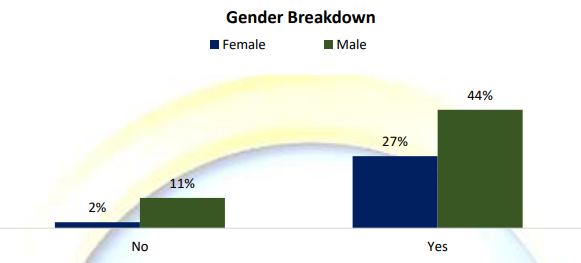

Gender Breakdown More males (44%) compared

to females (27%) believe that the federal capital is in

need of a good public transport system.

(Gallup Pakistan) May 26, 2022 Source: https://gallup.com.pk/wp/wp-content/uploads/2022/05/26-May-2022-English-2.pdf 744-43-02/Polls Nine In Ten S’pore Adults Still Wear A Mask Outdoors, Despite No Longer Being

Mandated To

Singapore saw its most significant easing

of safe management measures in end-April as caps on group sizes, capacity limits, and

mandates on wearing a mask outdoors were removed, among others. While people in Singapore

no longer have to wear a mask outdoors, nine in ten

continue to (93%), with Gen Zs (98%) and Baby Boomers (97%) most likely to do

so. Conversely, Millennials were most likely to say they never wear a mask

when outdoors (11%). A closer look at the frequency of outdoor

mask-wearing indicates that the largest proportion of Singapore adults say

they wear a mask outdoors all the time (49%), with Baby Boomers significantly

more likely to say so (58%). A fewer one in five Singapore residents say they

sometimes (20%) or often wear a mask outdoors (24%).

Protecting oneself from illness and germs

was the top reason for continuing to wear a mask outdoors among the general

population (68%) and all age groups. Around half also felt that doing so was

the most convenient way to travel between outdoor and indoor settings (52%),

since masks are still required when indoors. Protecting others from germs was

the third most popular reason cited for wearing a mask outdoors despite it

not being compulsory (43%). Just under four in five say they continue

to wear their masks because they have become used to doing so (37%). Gen Zs

were most likely to express this opinion, with almost half feeling this way

(48%). Gen Zs were also most likely to say they do

not remove their masks to not get judged by those who are wearing them, with

a quarter saying so (25%) compared to a fewer one in ten of the general population

(12%).

As for when residents will feel comfortable

removing their masks outdoors all the time, majority said they would only do

so once they feel it is safe (59%). Almost three in ten said they would make

the change if the rules making mask-wearing indoors compulsory are removed

(28%). A further one in seven would always remove

their mask outdoors when those around them do the same (15%), or when the

daily case count falls below 1,000 for four weeks (13%), while another

seventh say they will never change their mask-wearing behaviour (15%). One in twenty already feel safe removing

their masks outdoors, but do not do it all the time (6%).

(YouGov Singapore) May 27, 2022 Source: https://sg.yougov.com/en-sg/news/2022/05/27/nine-ten-spore-adults-still-wear-mask-outdoors-des/ AFRICA

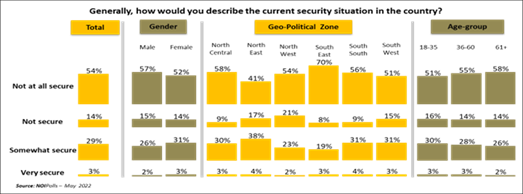

744-43-03/Polls Almost 7 In 10 Nigerians Describe The Current State Of Security In The Country

As Dreadful

A new public opinion poll conducted by

NOIPolls has revealed that 68 percent of adult Nigerians nationwide have

described the current state of security in the country as insecure. This is

not far-fetched as the country has been besieged with all kinds of security

challenges ranging from kidnapping, banditry, herdsmen attack, terrorism, and

the activities of separatists’ movements. Additionally, analysis across

geo-political zones showed that the South-East (78 percent) and the

North-West (75 percent) zones had the larger proportion of adult Nigerians

who made this assertion. Further findings revealed the most common

security challenges faced in each region. For instance, Nigerians residing in

the North-West mostly complained of kidnapping (32 percent) and armed

banditry (17 percent), terrorism (21 percent) in the North-East, and herdsmen

and farmer’s (20 percent) clash in the North-Central. Also, ritual killings

(8 percent) in the South-West, armed robbery in the South-East and

South-South amongst numerous security challenges. More so, the Poll revealed that 77 percent

of adult Nigerians do not know any security helpline they can call during an

emergency. This implies that most Nigerians may not be able to report any

emergency security issue when the need arises. Therefore, this urges the

security agencies to make sure citizens can report ongoing emergency

situations, emphasizing the need for this all-important mechanism to be put

in place to ensure effective feedback mechanisms between Nigerians and security

agencies. During this survey, most of the respondents

complained of not remembering the eleven digits security mobile numbers

provided by the Nigerian Police and advocated on the spot that the Nigerian

Police should have a three (3) digits number for Nigerians to call.

Information technology (IT) plays a critical role in strengthening security

against potential future attacks hence, it is vital for Nigerian security

operatives to strategize with relevant stakeholders and adopt the use of 3

digits security helpline. This will enable Nigerians share information more

readily as soon as they identify potential threats. Interestingly, a significant proportion of

Nigerians (84 percent) disclosed that they are willing to report any security

challenge in their localities mainly to save lives and properties (54

percent). It is, therefore, advised that security agencies synergize with

citizens for effective communication between them and the citizenry to

systematically improve on the security challenges currently ravelling the

country as information from the locals can go a long way in preventing

security threats. These are key findings from the State of Security Poll

conducted by NOIPolls in the week commencing 9th May 2022. Survey Background The menace of insecurity has continued to

rear its ugly head in our country Nigeria, causing loss of lives, destruction

of properties, instilling the undesirable element of fear and trepidation

amongst the populace. The insecurity situation in Nigeria today is arguably

the worst since after the civil war and has continued to rise unabated

despite government intervention in terms of spending trillions of Naira in

fighting insecurity. The insecurity in Nigeria is multi-faceted and has

manifested itself in many forms. From banditry and kidnapping in the

North-West, terrorism in the North-East, herdsmen crisis in the

North-Central, pipeline vandalism in the South-South to separatist agitations

occurring in SouthWestern and South-East regions. It is estimated that a staggering 8,372 people

have died due to insecurity challenges in 2021 alone which include banditry,

kidnapping, herdsmen attack, separatist movement activities and terrorism

related activities.[1] Many Nigerians are nurturing

different degrees of injuries as a resultant effect of the menace of

insecurity with some people incapacitated for life. It is estimated that the

North has the highest fatality percentage put at 79.2 percent while the South

has 20.8 percent[2]. The major cause of insecurity can be

attributed to the high rate of unemployment in the country which has left the

idle youths as susceptible and willing tools in the hands of the perpetrators

who use them to cause mayhem on ordinary but unsuspecting Nigerians.[3] Other causes include indoctrination,

brainwashing, substance abuse amongst other vices. The provision of

employment to graduates and their counterparts through creating empowerment

opportunities is very significant in curbing this menace while constant

electricity supply will no doubt boost employment and increase productivity

as well. Government must also adopt a multi-stakeholder approach to solving

security challenges in the country where traditional and community leaders,

pressure groups, civil society organizations, academics, media personnel, and

security experts will have synergy in areas of intelligence gathering,

information sharing, and early warning signals in matters related to security

around their communities. To that effect, there is a need for the

establishment of community policing within each divisional Police

headquarters for effective management of insecurity[4]. Against this background, NOIPolls

conducted this survey to feel the pulse of Nigerians regarding the current

security challenges in the country. Survey Findings The first question sought to gauge the

perception of adult Nigerians with regards to the current security realities.

The result revealed that 68 percent of Nigerians disclosed that the country

is not secure. Nigerians residing in the South-East zone (70 percent) had

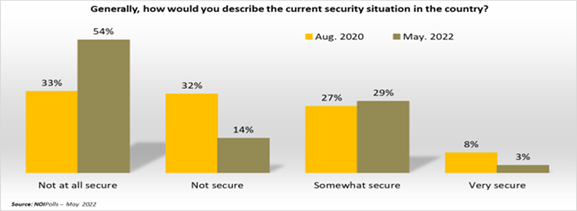

more respondents who made this assertion. Trend analysis shows a 21 percent increase

in the proportion of Nigerians who stated that the country is not secure at

all when current findings are compared with result obtained in 2020.

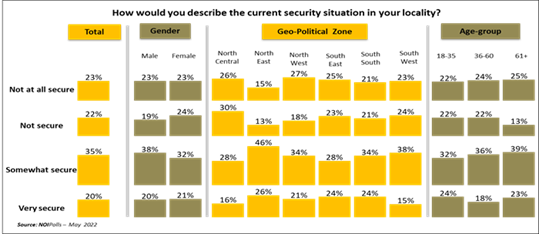

Similarly, respondents were asked to

describe security situation in their locality and the poll result revealed

that 45 percent of respondents described the current security situation in

their locality as insecure. Nigerians from the NorthCentral zone (56 percent)

account for the highest number of respondents who stated this.

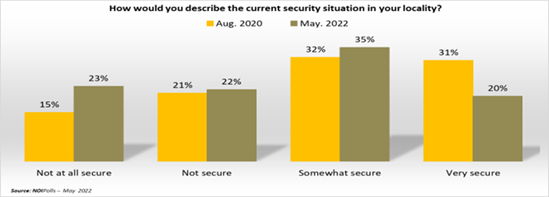

Trend analysis indicates an 8 percent

increase in the number of Nigerians who mentioned that the current security

situation in their respective locality is not at all secure when current

findings are compared with the result obtained in 2020.

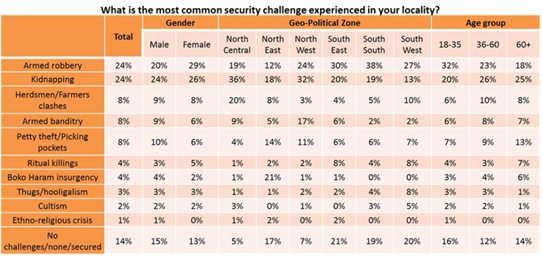

The poll sought to know the common security

challenges in the respondents’ localities and the poll result revealed that

armed robbery and kidnapping both tied at 24 percent as the main security

challenge in localities in Nigeria with the South-South region (38 percent)

leading with the challenge of armed robbery, while the North Central region

(36 percent) is leading in terms of kidnapping. Other security challenges

include herdsmen and farmers clashes and armed banditry tied at (8 percent)

with the North-West region (17 percent) leading in this regard.

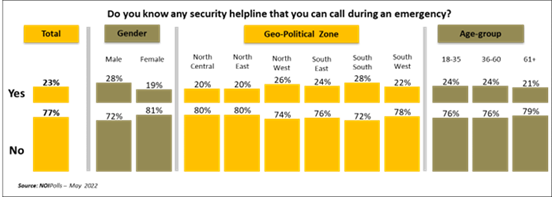

Additionally, the poll sought to know if

Nigerians are aware of any security helpline to call in terms of emergency,

and the poll result revealed that only 23 percent of Nigerians are aware of

the security helpline during emergencies whereas 77 percent of Nigerians

stated otherwise. This needs to be corrected as having knowledge of the

security helpline would go a long way in reporting some security

challenges.

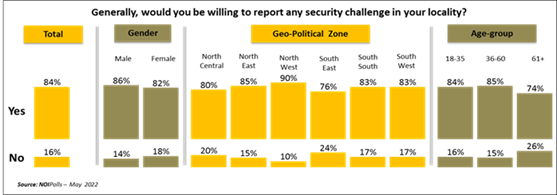

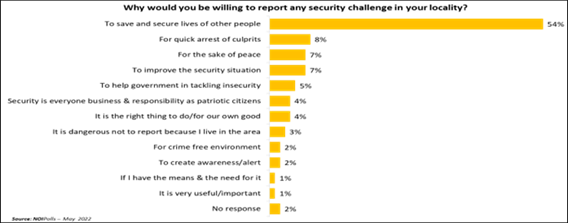

Interestingly, the poll revealed that an

overwhelming proportion of the respondents disclosed that they are willing to

report any security challenges within their locality. This is heart-warming

and it is advised that security agencies synergies with the locals especially

for security threat reports and information from the locals.

Respondents were further probed and out of

the 84 percent who mentioned that they were willing to report security

threats in their localities, slightly more than half of them (54 percent)

stated that they would do so to save and secure lives of other people. Other

reasons given includes to make quick arrest of the culprits (8 percent), to

ensure that there is peace (7 percent) and improve the security situation (7

percent) amongst other reasons.

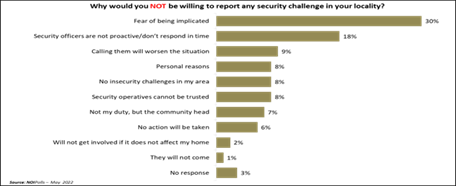

Correspondingly, respondents who stated

that they are not willing to report security challenges in their locality

were asked to give reasons for their opinion. The poll result revealed that

30 percent stated that they will not report because of fear of being

implicated while 18 percent stated that they will not report because security

officers do not respond in time when they are called upon. Other reasons

include calling them will worsen the situation (9 percent), personal reasons,

no security challenges in my area and security operatives cannot be trusted,

and they all tied at 8 percent.

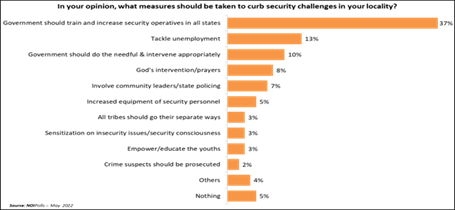

With regards to solution, 37 percent of the

respondents suggested that the government should train and increase security

operatives in all states of the country. While 13 percent recommended that

unemployment issues be tackled, 10 percent want the government to intervene

appropriately amongst other useful solutions.

Conclusion In conclusion, the poll results have

established that most Nigerians disclosed that the country is currently not

secure. It is gratifying to note that most adult Nigerians nationwide (84 percent)

stated that they are willing to report any security threat in their

respective localities. However, it is sad to know that 77 percent do not know

the security helplines to call during emergencies. This is a wake-up call for

security agencies to adopt a three-digit number as helpline for Nigerians to

call during security emergency. This will further improve and ensure

effective feedback mechanisms between the citizens and security agencies.

Finally, it is advised that security agencies and stakeholders take advantage

of this survey result which has clearly shown the willingness of Nigerians to

report crime in their respective localities. (NOI Polls) May 27, 2022 WEST

EUROPE

744-43-04/Polls 44% Saying They Had Been Forced To Cut Back On Their Clothing Purchases

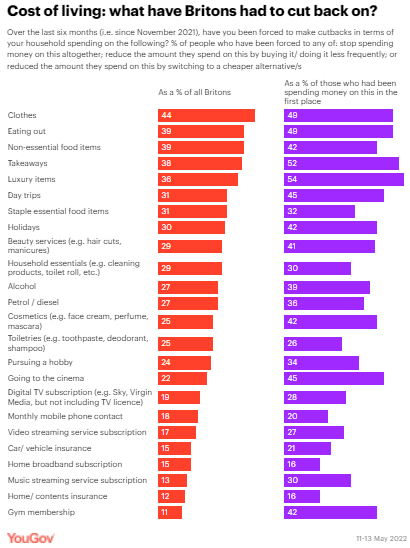

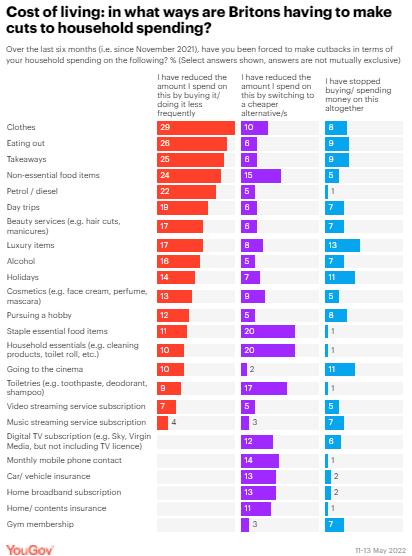

As the cost-of-living crisis continues to bite, a new YouGov survey

reveals how many Britons have been forced to make spending reductions on 24

areas of household spending. Clothing tops the list, with 44% saying they had been forced to cut

back on their clothing purchases since November. This most common form such

cuts take is people reducing their spending by buying clothes less frequently

(29%), although 10% are switching to cheaper alternatives and 8% say they

have been forced to stop spending money on clothes altogether. (These answers in this question are not

mutually exclusive, so do not sum to the overall 44% as some people are

making more than one type of cutback.)

How many people have had to cut back on

food and drink spending because of the cost of living? More indulgent forms of food spending also come close to the top of

the list, with 39% saying they’ve had to cut back on eating out, the same

number saying they have done so for non-essential food items, and 38% no

longer able to spend as much on takeaways. As for alcohol, a quarter of Britons (27%) say they have had to spend

less on booze since November, including 7% who have had to cut it out

entirely for cost reasons. When it comes to staple essential food items, 31% say they’ve been

forced to cut back their spending. This is primarily people switching to

cheaper alternatives (20%), although 11% say they are spending money on food

less frequently now.

How many people have had to cut back on

household essentials spending because of the cost of living? The number of Britons have had to cut back on household essentials

like cleaning products and toilet roll is virtually the same as the number

who have had to cut back on staple foods, both in terms of how many are

affected overall (29%) and how that breaks down in terms of the types of cuts

being made. A quarter of Britons (25%) have had to reduce spending on toiletries

like toothpaste and shampoo, with cutbacks most likely to take the form of

switching to cheaper alternatives (17%). How many people have had to cut back on

beauty spending because of the cost of living? One in four Britons (25%) have also been forced to make cutbacks on

their cosmetics spend, including one in three women (35%) and 15% of men. A similar number of Britons (29%) have also had to reduce spending on

beauty services like hair cuts and manicures, with women again much more

likely to have had to do so as men (38% vs 20%). How many people have had to cut back on

leisure spending because of the cost of living? Aside from the aforementioned 39% of Britons

who have had to cut back on eating out, three in ten Britons have also been

forced to spend less on day trips (31%) and holidays (30%). This includes 11%

who say they’ve had to scrap their holiday plans entirely since November. A further one in five (22%) have been forced to curtail spending on

trips to the cinema, and 24% now have to spend less

on pursuing their hobbies. How many people have had to cut back on

subscriptions because of the cost of living? Many types of subscription spending come low down on the list of

cutbacks, even when you account for the smaller numbers of Britons who are

spending money on them in the first place. One in five Britons (19%) say they have been forced to cut back on

their digital TV subscription – this represents 28% of everyone who has such

a subscription in the first place. A similar 18% have cut back on their mobile phone contract

(representing 20% of those with a mobile phone contract), and 15% have cut

back on their home broadband subscription (16% of all those with a

subscription).* When it comes to streaming, 17% have had to cut back on video

streaming subscriptions and 13% on music streaming subscriptions (equivalent

to 27% and 30% of those with such subscriptions in the first place). Gym memberships have been hit much harder. While only 11% of Britons

overall have said they had to cut back on their gym spending, this represents

42% of those who spent money on gym membership in the first place. How many people have had to cut back on

insurance because of the cost of living? Fewer Britons have felt they have to leave themselves less well

protected as a result of cost of living increase, so

far at least. One in eight Britons (12%) say they’ve had to reduced their spending on home or contents insurance, and

15% say the same of their car insurance. These figures represent 16% and 21%

respectively of those who were spending on these forms of insurance in the

first place. How many people have had to cut back on

petrol and diesel because of the cost of living? One in five Britons appear to be driving less as a

result of the rising cost of living, with 22% saying they have been

forced to do so less frequently. They form the bulk of the 27% of Britons who

have had to reduce spending on petrol and diesel in some way (which itself is

the equivalent to 36% of those who were spending money on fuel in the first

place). (YouGov UK) May 23, 2022 744-43-05/Polls Four In 10 Britons Are Worried About Catching Coronavirus On An Airplane

Can you still fly if you catch Covid? Travel restrictions for all

passengers entering the UK, including passenger locator forms and compulsory

tests, were

lifted on 18 March, but for travellers leaving the UK the rules depend

mostly on the destination country. As with domestic

Covid-19 restrictions, the UK government has moved towards guidance,

rather than legal requirements, hoping that those who come down with Covid

will voluntarily stay home and mask up around other people. YouGov research reveals that most Britons would not take a flight

abroad if they caught Covid before they left the country, despite not being

legally required to – although a third would bring the virus back to the UK

if they contracted it before flying home. Just one in seven Britons (14%) say they would still fly if they had

a trip abroad planned and contracted Covid-19 shortly before they left the

UK, with seven in 10 (69%) saying they would not travel, and 17% unsure.

However, if Britons contracted the virus while on holiday abroad,

they are more split on whether they would fly home. A third of the public

(33%) say they would still fly home if they caught Covid shortly before they

were due to return to the UK, while 41% say they would not travel, and 27%

unsure. Britons aged between 25 and 49 are most likely to say they would

still fly if they caught Covid-19. One in five (20%) would still travel

abroad with the virus, while two in five (40%) would fly home with it. In

contrast, just 5% of Britons aged 65 and older would still take a trip abroad

if they contracted the virus, while 20% would return home on a plane if they

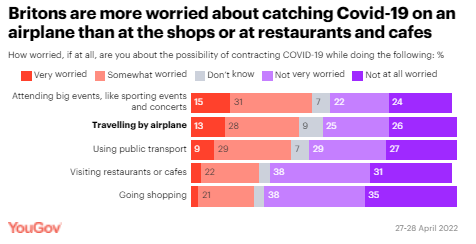

came down with Covid. Britons are more worried about catching

Covid-19 on an airplane than at the shops or at restaurants and cafes Several major UK carriers have removed

mask requirements on flights, following the government’s lead on

the ‘living

with covid’ plan. It’s well known that Covid-19 thrives

in enclosed, crowded spaces with little airflow – and what could fit

that description better than a packed plane? Britons are about as worried about contracting Covid-19 on a plane

(41%) as they are about catching it on public transport (38%), and less

worried about catching the virus at restaurants or cafes (26%), or at the

shops (24%). Sporting events and concerts are more of a concern than flights

at 46%.

However, more Britons are unconcerned about the possibility of

catching Covid on a plane (51%) than are worried about it. A third of Britons who plan to fly abroad

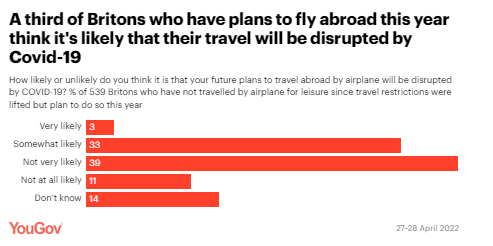

this year expect their travel to be disrupted by Covid-19 A perfect storm of rising cases and reduced restrictions caused

chaos in major UK airports over the Easter break as staff absences

due to Covid-19 led to hundreds of cancelled flights. Many Britons feel they are taking a chance in booking a holiday this

year. For those Britons who have made plans to fly abroad for a break this

year, around a third (36%) think Covid-19 disruption is very or somewhat

likely. Half (50%) think their odds are better, considering it not very

likely or not at all likely that the pandemic could upset their plans.

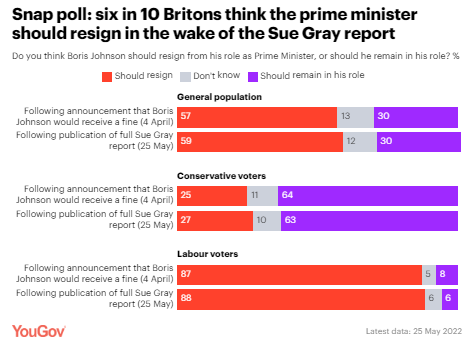

(YouGov UK) May 23, 2022 744-43-06/Polls 59% Of Britons Want Johnson To Resign In Wake Of Gray Report

The much-awaited Sue

Gray report has been published, revealing the details of many

gatherings taking place in Downing Street in contravention to the lockdown

rules in place at the time. Boris Johnson took to the despatch box to accept

responsibility for the report’s findings, including excessive drinking and

disrespect of custodial staff. However, Johnson continues to be stalwart in

the face of ‘partygate' accusations, stating he will "get on with the

job". Few Britons want him to, however, as most Britons continue to think

Johnson should resign (59%). This has changed little from the 57% it was on 4

April, when it was announced Johnson had received a fixed penalty notice.

Three in ten (30%) currently think Johnson should remain in office, the same

as the proportion who thought so in early April.

Despite the report, Johnson continues to hold the support of

Conservative voters, with 63% wanting him to remain in office. However, some

still 27% think their party leader should resign, compared to 25% in early

April. Unsurprisingly, Labour voters continue to be highly in favour of

Johnson’s resignation (88%, versus 87% previously). In a

statement to the House of Commons, Johnson defended his previous

comments about the gatherings, stating he believed them to be work events,

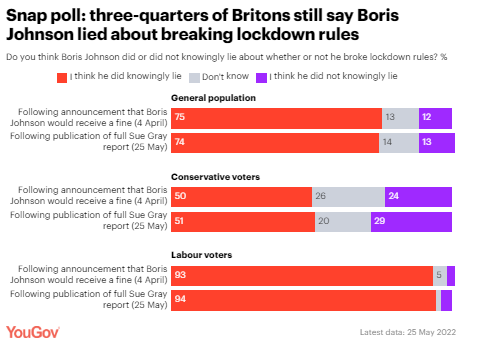

and insisted he did not mislead the House. Few believe his claims and justifications, however. Three quarters of

the public (74%) say they think Johnson knowingly lied about whether or not he broke lockdown rules. Only 13% think the

prime minister was not knowingly lying.

Even Conservative voters do not believe their party leader was being

truthful. Half (51%) currently think Johnson knowingly lied, representing

little change from early April (50%). Despite their support for his

continuation in office, only 29% of Conservative voters think Johnson did not

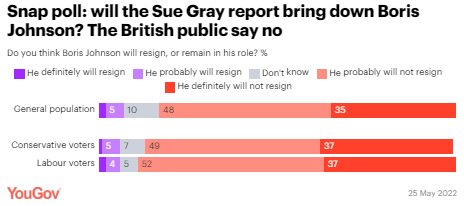

knowingly lie about his breaches of the COVID-19 lockdown rules. Finally, only a tiny minority think the Gray

report is enough to end Johnson’s premiership, with just 7% thinking it is

likely Johnson will resign in the wake of the report. The

vast majority of the public (83%) instead think he will not – including

35% who think he “definitely will not resign” as a result.

(YouGov UK) May 25, 2022 744-43-07/Polls Public Concern About Inflation Reaches Its Highest Level For 40 Years

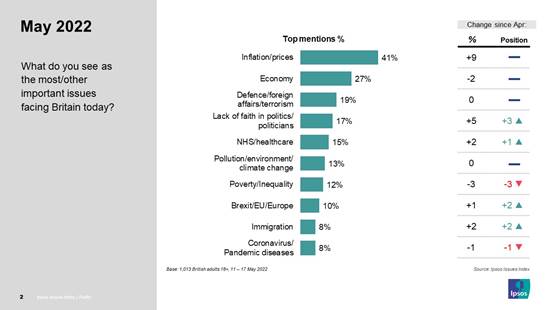

The May 2022 Ipsos Issues Index confirms that public concern about

inflation and prices continues to rise. Forty-one per cent of the British public mention cost-of-living

issues as a big concern for the country, up from 32% last month. This is the

highest level of public concern recorded since the Issues Index became a

regular monthly poll in the early eighties, although still behind the peaks

it reached in the 1970s and very beginning of the 1980s. In April 1980, 69%

saw inflation as a big concern, but by the next recorded measure in September

1982 this had fallen to 32%. The wider economy and defence and foreign affairs issues remain the

second- and third-most cited issues this month on similar scores to April:

just over a quarter are worried about the economy (27%) and one in five about

defence (19%). There has been a five-percentage-point increase in concern about a

lack of faith in politicians and politics this month, making it the

fourth-biggest issue for the country with 17% mentioning it. As with last month, both Brexit and the COVID-19 pandemic remain

lower on the list of public concerns. Only around one in ten of the public

mention either issue as one of the biggest concerns

for Britain. On eight per cent, COVID-19 ranks as the tenth-biggest issue

alongside immigration, education and petrol prices.

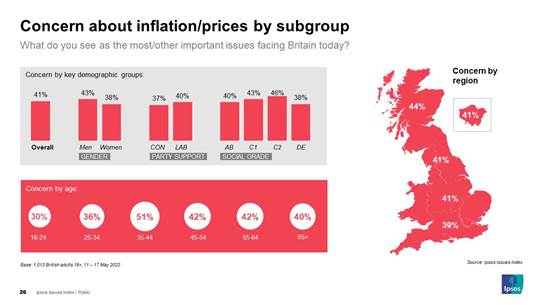

Inflation has become the biggest issue for a wide range of groups; it

is the biggest concern for people of all ages and social grades. Some groups

stand out as especially likely to mention this as a concern: those aged 35-44

(51%) and people who own their home on a mortgage (49%) in

particular are significantly more likely than average to mention

inflation as a worry. Those with higher household incomes are also particularly likely to

mention prices and inflation. Among households with an income over £50,000

per year 48% mention this as an issue, significantly higher than the national

average of 41% (concern among those on lower incomes is around the national

average, at 44% among those earning £25-£50,000 per year and 42% for those

under £25,000).

Mike Clemence, a researcher at Ipsos, said: Concern about inflation is now clearly the

biggest issue facing the country, for people of all ages, social grades and incomes. The proportion worried about the cost

of living this month is the highest level we’ve recorded in more than 40

years of the Index. Against this backdrop other issues appear

to have less traction – and we know that the public expects prices to

continue to rise and are already changing their behaviours in response, so

the focus on the cost of living crisis is unlikely

to go away any time soon. (Ipsos MORI) 25 May 2022 744-43-08/Polls One In Five Britons Now Say They Are Struggling Or Unable To Make Ends Meet

With the rising cost of living continuing to dominate the list

of people’s concerns, the government is set to announce a raft of

measures aimed at easing Britons’ financial burden. A new YouGov survey reveals the extent of the damage to people’s

finances, with the number of people saying they are struggling or unable to

make ends meet doubling in the last year. One in six Britons (17%) say of their household financial situation:

“I can only just afford my costs and often struggle to make ends meet”. This

figure has risen from 11% in mid-May 2021. A further 5% say “I cannot afford my costs, and often have to go

without essentials like food and heating”, a figure that was 1% last year. One in three Britons (37%) describe their financial situation as “I

do not often have money for luxuries, but can normally comfortably cover the

essentials”, while an identical figure say they are either “relatively” or

“very” comfortable financially.

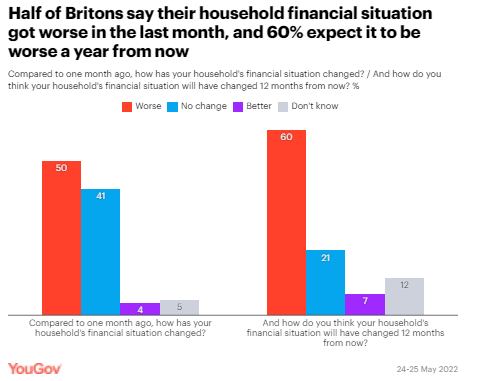

While most Britons don’t consider themselves to have moved between

these semantic financial categories, they nevertheless report that their

situation is getting worse. Half of Britons (50%) say their household financial situation has

deteriorated in the last month, while 41% say there has been no change. Only

4% say things have improved for them. More still expect their finances to get worse in the next year (60%),

with just 21% expecting to tread water, and 7% thinking they will get better.

Some have

suggested that the government’s decision to introduce the cost of

living measures is a cynical attempt to distract people from the latest

developments in the ‘partygate’ saga. Regardless of whether this is true, if

the government wants to win the next election it would do well to recognise

that its own voters are being hammered by the cost of

living crisis. Half of 2019 Conservative voters (48%) say their finances have become

worse in the last month, and 60% expect them to deteriorate in the next 12

months. Labour voters are faring worse still, with 57% saying they got worse

last month and 64% expecting them to fall further over the next year. The number of Tories saying they are struggling or failing to make

ends meet has also increased from 11% a year ago to 16% now. Among Labour

voters, this figure has doubled from 13% to 26%. (YouGov UK) May 26, 2022 744-43-09/Polls Less Than Half (45%) Of Teachers Would Enter The Profession If Given The Choice Again

Figures from the University of Essex

Institute for Social and Economic Research show the number of male teachers

has fallen

to its lowest point on record. Low recruitment and poor retention of

existing teachers has been partly blamed on pay, with staff suffering a

15% real-term pay cut since 2010. This all follows the stresses and

increased workload brought on during

the pandemic. It may be unsurprising then, that a new

YouGov survey of teachers suggests many may be feeling disillusioned with

their career choice. Fewer than half (45%) say that if they

could choose again, they would still choose to become teachers. Two in five

(40%) would not choose to become a teacher again.

The youngest and the oldest teachers are

the happiest with their choice of career, being the most likely to say they

would repeat it. Half of teachers aged 18 to 34 (51%) and 62% of those aged

55 and above say they would make the same choice to teach again. Teachers aged 35 to 44 are split 40% to 43%

over whether they would become teachers again or not. Those aged 45 to 54 are

the least likely to say they would still choose to become a teacher, at 35%,

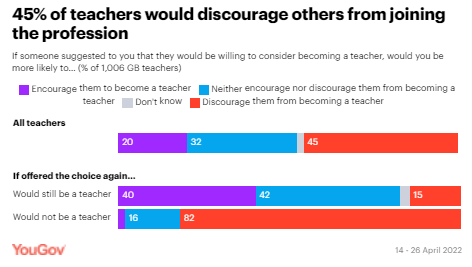

compared to nearly half (48%) who say they would not. Teachers would generally discourage others

from entering the profession Not only would many teachers opt-out if

given the choice again, but they would also discourage others from going into

teaching, by 45% to 20% who would encourage it. One in three (32%) neither

encourage nor dissuade someone from considering joining the profession.

Among those who would not choose to become

a teacher again, the vast majority (82%) say they would attempt to dissuade

others from a career in teaching. Only 2% say they would encourage others to

teach. However, even among those who would choose

to teach again, only 40% would encourage others to do so, while 15% would

actively discourage them from following in their footsteps. Another four in

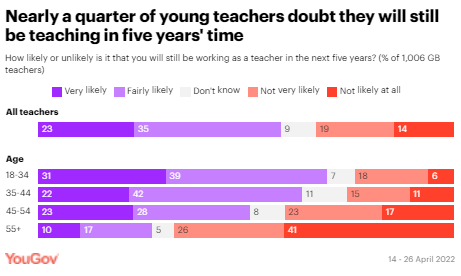

ten (42%) would neither encourage nor discourage them from doing so. Nearly a quarter of young teachers doubt

they will be teaching in five years Given pandemic stress and stagnated wages,

are teachers considering throwing in the towel? Just under six in ten (58%) say they will

likely be teaching in five years, although only 23% think that it is

"very likely" they will remain in the profession. A third (33%) say

it is unlikely they will still be teaching in five years, including 14% who

think it "very unlikely".

Approaching a quarter of the youngest

teachers (24% of those aged 18-34) say it is unlikely they will be teaching

in five years, with 35 to 44 similarly likely to consider quitting (26%). Of those aged 45 to 54, only 51% expect to

continue teaching for another five years, with 40% expecting not to. Among those teachers who would not choose a

career in teaching again, only 40% expect they will still be teaching in five

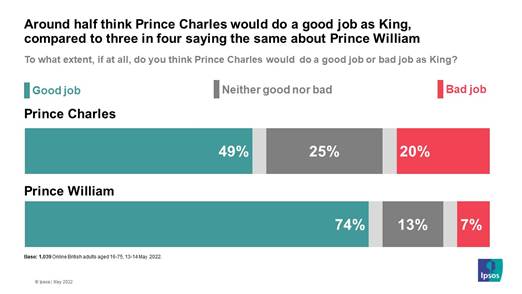

years, while 52% think it is unlikely they will be. (YouGov UK) May 27, 2022 744-43-10/Polls Half Of Britons Believe Prince Charles Will Be A Good King, Even As Two-Thirds Want The

Queen To Remain Monarch For As Long As Possible

As the Prince of Wales takes on more roles, such as reading the

Queen’s Speech at the opening of State Parliament, new research by Ipsos

shows half of Britons expect Prince Charles to do a good job as King (49%),

while 1 in 5 do not (20%). This is similar to

the public’s views earlier this year in March.

While Britons are more likely to expect good things from the heir

than not, expectations for Prince William are even higher. Three-quarters

believe the second in-line to the throne will be a successful monarch (74%),

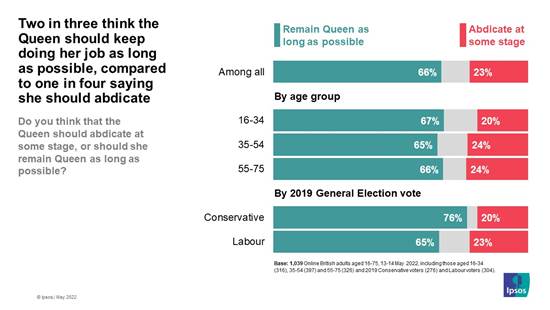

only 7% think he will do a bad job. Despite favourable ratings for Prince Charles and Prince William,

most are in no rush to see any change of monarch. Two-thirds (66%) say the

Queen should remain in her position for as long as possible while only 23%

believe she should abdicate. Overall, Britons are more likely to say the

Queen has had a positive impact on the country than a bad one. Almost half

(46%) say Britain is better since the Queen came to the throne compared to

20% who say it is the same and 23% who believe it is worse.

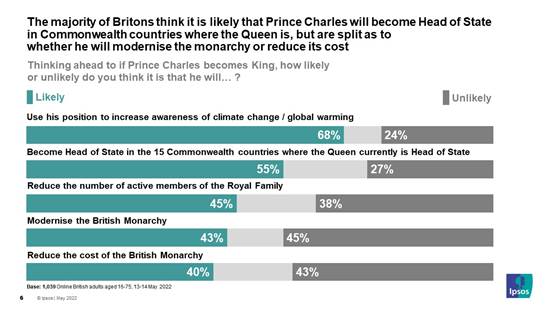

Looking ahead to the reign of King Charles III, what do Britons expect

him to achieve if he does take the throne? Seven in 10 (68%) say he is likely

to use his position to raise the awareness of climate change and the need to

fight it, including 36% who say he is very likely to do so. Over half (55%)

say he is likely to become Head of State in the 15 Commonwealth countries

where the Queen currently holds this position (including the UK), around a

quarter believe this is unlikely (27%).

Regarding the monarchy itself, almost half (45%) believe he is likely

to reduce the number of active members of the Royal Family, however opinion

is split on this with 38% who say he is unlikely to do so. Similarly, Britons

are divided as to whether Prince Charles is likely to modernise the monarchy,

43% believe this is probable while 45% do not. Around 4 in 10 (40%) say he is likely to reduce the cost of the

monarchy, 43% disagree. This could be an increasingly important achievement

in the eyes of the British public. With the ongoing cost of living crisis,

opinion is now split as to whether the Royal Family is an expensive luxury

that the country cannot afford. Around 4 in 10 (38%) say this is the case

while 36% disagree. Almost a quarter (23%) neither agree nor disagree.

There is a clear age difference on this question – 18-34

year olds are more likely to agree than disagree that the Royal Family

is an expensive luxury (by 48% to 22%), but this position is reversed among

55-75 year olds who disagree by a similar margin (53% to 22%). Kelly Beaver, Chief Executive at Ipsos in

the UK, said: It is promising to see Britons more

confident than not that Prince Charles will do a good job as King, and that

hopes are even higher for his son Prince William, even while a majority hope

the Queen will remain in place for as long as possible. There is also

clearly an expectation that Charles will use his position to increase

awareness of climate change. However, with opinion split as to whether

the country can afford the Royal Family – particularly amongst young people –

there are other issues that may be more of a test for

the Prince of Wales, particularly whether he will be able to modernise the

Royal Family, and demonstrate to the public that it is carrying out its

duties as cost-effectively as possible. (Ipsos MORI) 27 May 2022 744-43-11/Polls Cryptocurrencies And NFTs: What Do The Spanish Think

Cryptocurrencies and NFT's attract more and more Spaniards, who

decide to learn about and invest in them. A study carried out in May

2022 by YouGov Spain highlights that: Despite the fact that 90% of Spaniards

have ever heard of cryptocurrencies, only 41% claim to know exactly what it

is, and only 12% have already invested in cryptocurrencies. The same

goes for NFTs, with only 16% claiming to know exactly what they are and 6% of

the population have already invested in NFTs. As for the profile of

Spaniards who claim to know precisely what cryptocurrencies and NFTs are, the

majority are men between 18 and 34 years old.

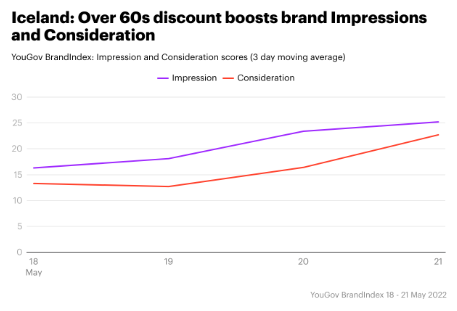

(YouGov Spain) Source: https://es.yougov.com/news/2022/05/27/criptomonedas-y-nfts-que-opinan-los-espanoles/ 744-43-12/Polls Iceland’s Cost Of Living Discount For The Over-60s Boosts Brand Health

Iceland recently announced that, starting from May 24, customers over

the age of 60 would receive a 10% discount on their grocery shopping in the

store every Tuesday. The move is motivated by the concerns older shoppers

have experienced around the cost-of-living crisis – which has

seen energy bills and food prices rise, among other things, in recent months. Mere days after the announcement, the move looks to have been

well-received by the general public. YouGov

BrandIndex shows that, between May 18 (the day

before Iceland made the announcement) and May 21, Buzz scores – which measure

whether people have heard anything positive or negative about a brand in the

past two weeks and nets the scores – doubled from 3.2 to 7.2 (+4). This

improved overall sentiment towards Iceland: Impression scores rose from 16.3

to 25.2 (+8.9), and the metric tracking consumer recommendations jumped from

9.0 to 15.6 (+6.6).

For Iceland customers, the discount has improved overall happiness

with the brand: Satisfaction scores saw an increase of 8.4 points, going from

19.3 to 27.7. And whether people are Iceland customers or not, they’re more

likely to think about picking up their groceries from the budget chain:

Consideration scores, which ask consumers which brands they’d shop from out

of a list of supermarkets, leapt from 13.3 to 22.7 (+9.4). Index scores, a

measure of overall brand health, saw a six-point rise from 10.1 to 16.5

(+6.4). Discounts tend to go down well even at the best of times, and in

terms of domestic finances, these are among the worst: YouGov/CEBR’s regular

consumer confidence tracker shows that public optimism around household’s

future financial situation is at an all-time low. Iceland’s intervention is a timely

intervention for older consumers who may struggle to keep up with rising

costs – and a potential PR coup for a brand that’s already closely identified

with lower grocery prices. (YouGov UK) May 27, 2022 NORTH

AMERICA

744-43-13/Polls Americans Knowledge About International Affairs

Americans know a great deal about certain global leaders and

institutions. For example, nearly eight-in-ten U.S. adults can look at a

photo of Kim Jong Un and correctly identify him as the leader of North Korea,

and nearly two-thirds know that Boris Johnson is the current prime minister

of the United Kingdom. A slim majority also know that Ukraine is not a member

of the North Atlantic Treaty Organization (NATO). However, as a new Pew Research Center survey shows, Americans are

less familiar with other topics. Despite the U.S.

government labeling the events in Xinjiang, China, as genocide, only

around one-in-five Americans are aware that it is the region in China with

the most Muslims per capita. And only 41% can identify the flag of the second

most populous country in the world, India.

On average, Americans give more correct than incorrect answers to the

12 questions in the study. The mean number of correct answers is 6.3, while

the median is 7. But the survey finds that levels of international knowledge

vary based on who is answering. Americans with more education tend to score

higher, for example, than those with less formal education. Men also tend to

get more questions correct than women. Older Americans and those who are more

interested in foreign policy also tend to perform better. Political party groups are roughly similar in their overall levels of

international knowledge, although conservative Republicans and liberal

Democrats tend to score higher on the scale than do their more moderate

counterparts. International knowledge is also related to people’s general interest

in foreign policy: Those who report being very or somewhat interested in the

topic answer a mean of 7.4 questions correctly, compared with only 4.6

correct questions for those who are not too or not at all interested in

foreign policy. Those who follow international news also tend to have higher

international knowledge than those who are less engaged. Those who have

visited at least one country outside of the United States also score higher

on the international knowledge scale than those who have not traveled abroad,

even after accounting for differences in education and income. Part of the goal of the survey was simply to understand these

factors: what Americans know about international affairs and, more

specifically, how knowledge varies across demographic subgroups. But another

goal of the survey was also to understand how knowledge might affect

attitudes. We find that people who know more about an issue often have different

views about that issue. For example, people who are aware that Ukraine is not

a member of NATO are more likely to have a favorable view of NATO and more

likely to say that the U.S. benefits a great deal from its membership in the

organization relative to those who do not know Ukraine is not a member

nation. This same group is also more likely to have negative views of Russia,

to have no confidence at all in Russian President Vladimir Putin and to

describe Russia as an enemy. Similarly, the survey also finds that those who know the capital of

Afghanistan are more critical of the U.S. withdrawal and how it was handled

than those who do not know the capital. Those who are aware of where the U.S.

Embassy in Israel is located (following the 2018

move) are also more likely to say U.S.-Israel relations are good than

those who do not know. But there are few differences between the 17% of

Americans who know that Xinjiang is the region of China with the most Muslims

per capita and those who do not when it comes to views of China or Chinese

President Xi Jinping. Beyond the issue of how specific knowledge questions are related to

attitudes about that topical area – e.g., how knowledge about NATO is related

to views about NATO – we can also explore, more generally, whether people who

have more international knowledge feel differently about myriad global issues

than those with less international knowledge. To do this, we can use the

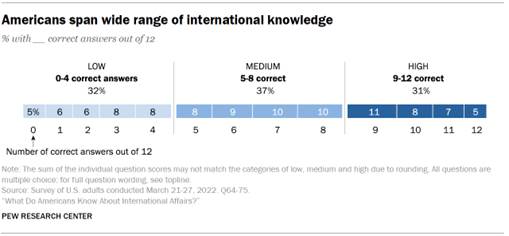

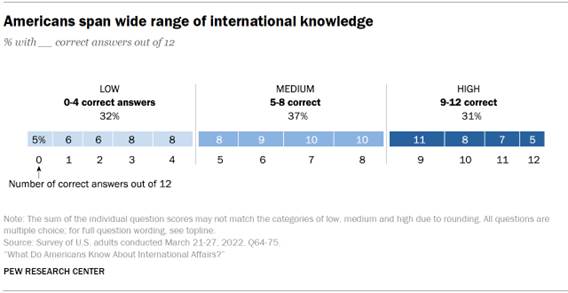

entire 12-question scale, breaking people into groups of high (those who

answered 9-12 questions correctly), medium (5-8 questions) and low knowledge

(0-4 questions). Around a third of the American public falls into each of

these three groups, respectively.

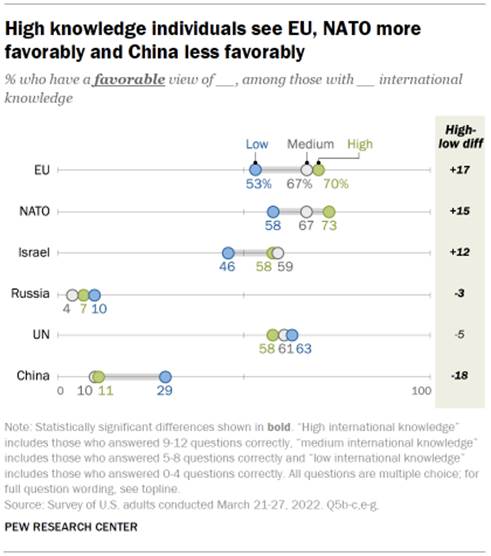

Generally speaking, we see that

international knowledge is related to attitudes about a host of issues.

People with higher levels of knowledge have more positive views of the

European Union (EU), NATO and Israel. They also have more confidence in

Ukrainian President Volodymyr Zelenskyy, French President Emmanuel Macron,

German Chancellor Olaf Scholz and U.S. President Joe Biden.

When it comes to both Russia and China, though, those with higher

levels of knowledge tend to be more critical. They are more likely to see the

two countries unfavorably, to describe both countries as enemies of the U.S.

and to have little or no confidence in Putin and Xi. And, whereas Americans

overall are equally likely to describe China and the U.S. as the

world’s top economy, people with high levels of international knowledge are

significantly more likely than those with less knowledge to say the U.S. is

the world’s leading economic power – mirroring the gross

domestic product assessments compiled by the International Monetary

Fund. These are among the key findings of a new survey conducted by Pew

Research Center on the Center’s nationally representative American Trends

Panel among 3,581 adults from March 21 to 27, 2022. The survey also finds

that when it comes to the four questions that we have previously asked,

Americans’ level of international knowledge is similar – or higher – than it

was in the past.1 In

the case of identifying the leader of North Korea or the euro currency

symbol, American knowledge has not changed significantly since the questions

were last asked in 2015 and 2013, respectively. But when it comes to

identifying the U.S. secretary of state, more can identify Secretary Antony

Blinken (51%) than could identify Secretary Rex Tillerson (44%) in June 2017.2 More

Americans are also able to identify the British prime minister now (65%) than

were able to do so in 2017 (56%) – though this most recent survey was

conducted following a scandal that kept Johnson in

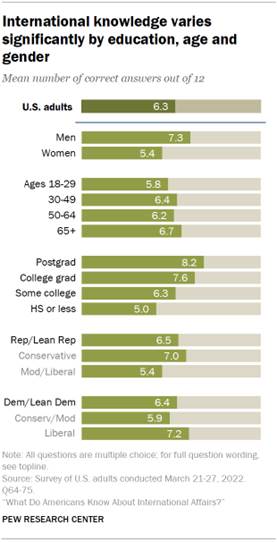

the news. International knowledge varies markedly

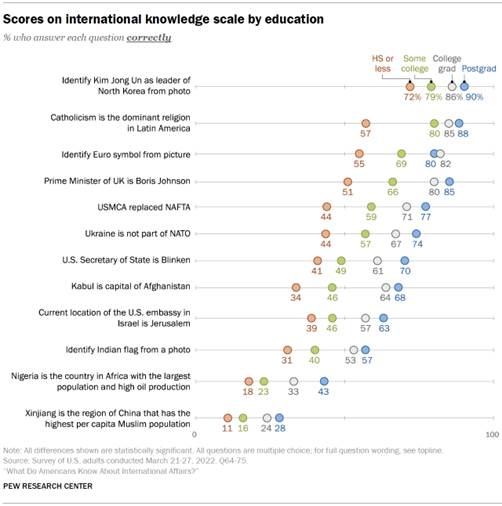

across demographic groups Americans with more education tend to score higher on the

international knowledge scale compared with those with less education.

College graduates get an average of 8.0 out of 12 international knowledge

questions right, including around half (49%) who get at least nine of the 12

correct. Within this group, people who have a postgraduate degree do

especially well, averaging 8.2 questions correct, including 55% who get at

least nine questions right. Scores are lower among Americans with less education. Among people

who have some college experience, the average number of correct answers is

6.3. Those who have a high school diploma or less education get 5.0 questions

right, on average. These large education differences are consistent with past

Center surveys on science

knowledge and religious

knowledge.

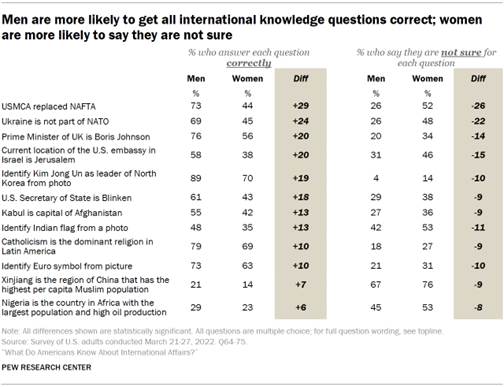

Men tend to perform better on the

international knowledge scale than women Overall, men tend to score higher on the knowledge scale than women.

On average, men answer 7.3 questions correctly out of 12, compared with an

average of 5.4 correct answers for women. In fact, for each of the 12

questions individually, a higher share of men than women answer correctly.

This mirrors previous findings for both scientific

knowledge and religious

knowledge in which men tended to score higher than women. Multiple studies have

found that men

are more likely than women to guess on knowledge questions, even if

they don’t know the answer. If given the option, women

are often more likely than men to say they don’t know. Indeed, on each of

the 12 items tested in this survey, women are more likely than men to say

they are not sure of the correct answer. On only four questions are women

more likely to give an incorrect answer.

While men are more likely than women to answer each item correctly,

this gap is larger on some questions than others. The largest gap between men

and women is identifying the predecessor of the USMCA trade agreement. Nearly

three-in-four men correctly answer NAFTA, compared with 44% of women. About

half (52%) of women say they are not sure which trade agreement preceded the

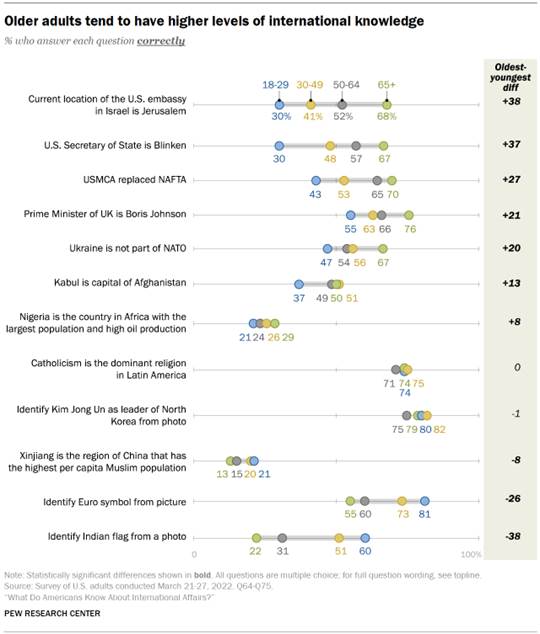

USMCA. Older Americans have higher levels of

international knowledge than younger ones Overall, compared with younger Americans, older Americans – those

ages 65 and older – perform best on the international knowledge scale,

averaging 6.7 questions correctly relative to 6.2 for those ages 50 to 64,

6.4 for those 30 to 49, and 5.8 for those under 30. Around a third of this

oldest age group answers at least nine of the 12 questions correctly, placing

them in the “high” knowledge category, while only around a quarter of the

youngest age group falls into the same group. Across nearly all of the 12 questions, older

adults are more likely than younger adults to answer them correctly. The gap

is largest when it comes to three specific questions: current location of the

U.S. embassy in Israel, prime minister of the UK and secretary of state of

the U.S. In all three cases, the oldest age group is more than 20 percentage

points more likely to answer correctly than the youngest group. But there are

also three questions where younger adults noticeably outperform their older

counterparts. Two of them are questions that relate to pictures: one

identifying the euro symbol and the other identifying the Indian flag.

Younger adults are also more likely to correctly identify the region of China

with the highest per capita Muslim population. While younger people are somewhat more likely to say they are not

sure when it comes to six of the questions, they are also more likely to give incorrect

answers for seven of the 12 questions. For example, when it comes to

identifying the current U.S. secretary of state, 51% of those under age 30

said they were not sure, compared with 37% of those 30 to 49 and around

three-in-ten or fewer of those ages 50 and older. But this youngest age group

is also more likely

to be wrong: 19% chose an incorrect multiple-choice answer from the list

provided, while only 10% of those ages 65 and older chose an incorrect

answer.

International knowledge highest at ends of

the political spectrum

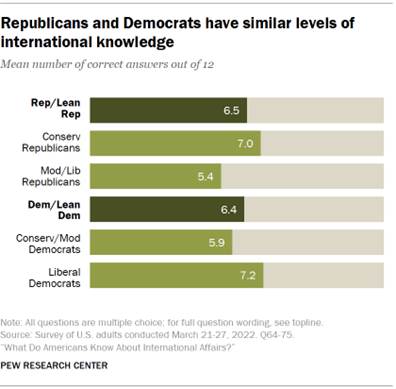

Republicans and Democrats have roughly the same levels of

international knowledge. On the 12-point scale, Republicans and

Republican-leaning independents answer an average of 6.5 questions correctly,

while Democrats and Democratic leaners get an average of 6.4 right. There are, however, a few questions where members of one party

perform markedly better than the other. More Republicans and GOP leaners know

that the

USMCA trade agreement replaced NAFTA and that the

U.S. Embassy in Israel moved to Jerusalem in 2018 – both changes

made under former U.S. President Donald Trump and pillars of his

international policy. Republicans are also more likely to know the capital of

Afghanistan. On the other hand, Democrats and Democratic-leaning independents

are more likely to correctly identify the flag of India and the euro symbol.

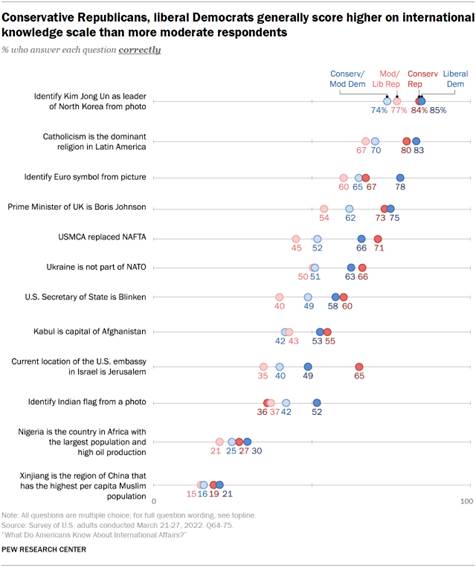

Generally, though, there are greater differences within parties than between them. Those at the ends of

the political spectrum – conservative Republicans and liberal Democrats –

score more than a point higher, on average, than the more moderate groups.

While these groups both tend to be more likely to follow international news

and interested in foreign affairs, this difference in knowledge persists even

after statistically controlling for these factors. Liberal Democrats answer

all but one of the 12 questions correctly at a higher rate than conservative

and moderate Democrats. The same is true for conservative Republicans

relative to liberal and moderate Republicans on three-quarters of the scale

items. These patterns are largely

consistent with measures of scientific knowledge conducted by the

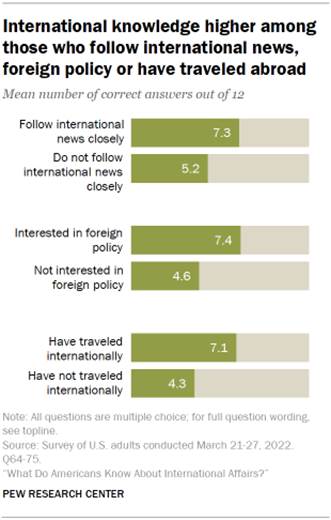

Center. International engagement tied to higher

international knowledge Perhaps unsurprisingly, Americans who are more internationally

engaged on a variety of fronts are more likely to have higher international

knowledge than Americans who are not as engaged. For example, Americans who

say they follow international news very or somewhat closely answer an average

of 7.3 questions correctly; Americans who follow international news less

closely answer only 5.2 questions correctly, on average. Only when it comes

to identifying the flag of India are those who follow international news

closely and those who do not equally likely to answer correctly. Following

international news is a significant factor in international knowledge even

after controlling for education and other key demographics including age, race and gender.

Interest in foreign policy also plays a part in international

knowledge. Those who say they are very or somewhat interested in foreign

policy answer a mean of 7.4 questions correctly, compared with only 4.6

correct questions for those who are not too or not at all interested in

foreign policy. In some cases, the difference between those who are

interested in foreign policy and those who are not can be quite large. On the

question of which trade agreement the USMCA

replaced, 72% of those interested in foreign policy correctly answer NAFTA,

while only 37% of those not interested in foreign policy are able to identify

the correct answer. Once again, interest in foreign policy remains a

significant factor in international knowledge even after controlling for

education.3 These differences don’t just extend to hypothetical interest.

Americans who have visited at least one other country outside of the U.S.

answer an average of 7.1 questions correctly, compared with an average score

of 4.3 correct for those who have never visited another country. And while

international travel is associated with more education and higher incomes,

this gap is significant even when controlling for those factors. International knowledge and attitudes about

foreign countries and leaders Based on the individual performance of the 12 international knowledge

questions, we are able to divide people into three

roughly equal groups: those who answered at least nine of the 12 questions

correctly (31%) are termed “high” knowledge; those who answered five to eight

questions correctly (37%) or the “medium” knowledge group; and those who

answered fewer than five questions correctly (32%) or the “low” knowledge

group.

Performance on the international knowledge scale relates to views of

other countries and multinational entities. Those who have a high score on

the knowledge scale are more likely than those with a low score to hold favorable

views of the EU, NATO and Israel. For example, 73%

of those who answer at least nine of 12 questions correctly hold a favorable

view of NATO, compared with 58% of those who answer four or fewer questions

correctly. However, knowledge is not related to views of the United Nations:

Those with high levels of international knowledge are as likely to feel

favorable toward the UN as those with low levels of international knowledge. Americans who score better on the international knowledge scale

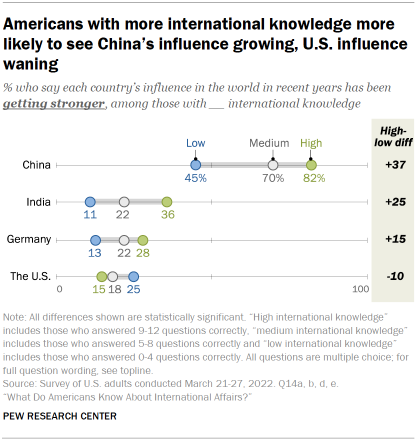

differ in their assessments of countries’ place in the world. High scorers

are 37 percentage points more likely than those who have a low score to say

China’s influence in the world in recent years has been increasing. They are

also significantly more likely to say India and Germany’s influence has been

growing stronger. Conversely, they are 10 points less likely than Americans

who answered four or fewer questions correctly to say the United States’

influence in the world has increased. Evaluations of world leaders similarly differ by performance on the

international knowledge scale. Confidence in Ukrainian President Zelenskyy is

higher among Americans who answer at least nine questions correctly, compared

with those with four or fewer correct responses. The same relationship holds

for views of German Chancellor Scholz, French President Macron and U.S.

President Biden. High scores on the knowledge scale relate to more critical

evaluations of Russia. While a majority of Americans

see Russia very unfavorably,

those with a high level of knowledge are 10 points more likely than those

with low knowledge to have a very negative view of the country. These