|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 738-739 Week:

April 11 – April 24, 2022 Presentation:

April 29, 2022 McDonald's

Tops YouGov’s 2022 Dining And QSR Rankings In Malaysia Economy

Is Turkey's Most Important Problem For 9 Out Of 10 People Today Eco-Labels

In Singapore, How Aware Are Consumers Of These Green Certification Marks Six

In Ten People In S'pore Prefer Sustainable Brands, With Those Aged 18 - 24

Most Likely To Say So Iraq

Pulse: Unrest Amid The Covid-19 Pandemic Majority

Of Namibians Say The Country Is A Safe Place To Live, But Levels Of Fear Are

On The Rise Three

In Four Malawians (74%) Believe “A Lot” In The Existence Of Witchcraft Seven

In Ten (72%) Of Britons Would Support The Construction Of A Wind Farm In

Their Local Area More

Than One In Two Britons Support Ban On Whipping Racehorses Should

Selective Breeding Of Dogs With Health Issues Be Banned Majority

Of Britons Say Boris Johnson Should Resign, In Aftermath Of ‘Partygate’ Fines By

37% To 19% Britons Would Prefer Emmanuel Macron Win The French Presidential

Election YouGov

Food Study Shows That Three In Four Britons (75%) Eat Meat Eight

In 10 Britons Say Boris Johnson Lied About Lockdown Parties Most

Britons Now See Rishi Sunak As Untrustworthy And Are Split Over His

Competence 59%

Of Britons Say They Feel Worse Off Since The Last General Election 6

In 10 Would Rather Be A Citizen Of Britain Than Any Other Country In The

World 82%

Of French People Say They Are Worried About The Risks Of A Cyberattack In The

World Boost

For Macron As He Opens Up 8-Point Lead Over Le Pen Final

Study Of The French Elections: Macron Leads 56% To 44% Germans

More In Favor Of Extending The Lifetime Of The Last Nuclear Power Plants Italians

And April 25: The Liberation Between The Past And The Present Race

Is Central To Identity For Black Americans And Affects How They Connect With

Each Other Covid-19

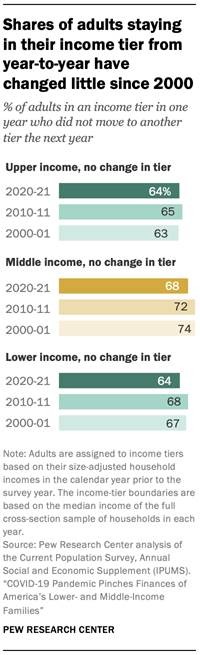

Pandemic Pinches Finances Of America’s Lower- And Middle-Income Families How

The American Middle Class Has Changed In The Past Five Decades Most

Americans Who Are Familiar With Title IX, Say It’s Had A Positive Impact On

Gender Equality Most

(64%) Canadian Farmers “Cautiously Optimistic” About the Next 12 Months Africans

Divided On Russia's Leadership Before Ukraine War A Survey In 19 Nations What

Makes People Happiest 30-Country Ipsos Survey A

Global Median Of 33% Approved Of Russia's Leadership In 2021 Among 116

Countries Incidence

Of Smoking In Pakistan Is Lower Than The Global Average 61%

Across 27 Countries Think The War In Ukraine Poses A Significant Risk To

Their Country The

Image Of U S Leadership Is In A Much Stronger Position, Result Of A Study

Across 34 Nations Europeans

Express Wide Support For A Greener Energy Market, According To A Poll Across

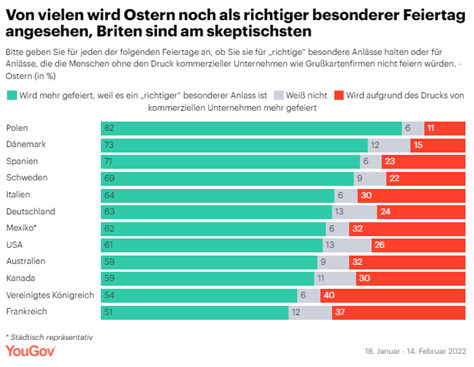

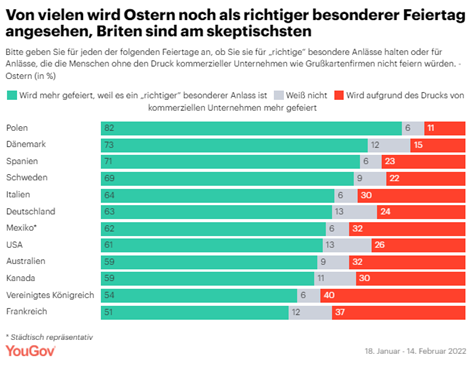

7 Countries INTRODUCTORY NOTE 738-739-43-45/Commentary: Worldwide Celebration Of Easter French And

British Are Most Critical Of Easter Celebrations In Terms Of

Commercialization, A YouGov Poll In 12 Countries Around The World

Easter is

still considered a special or traditional occasion in many countries, after

all Easter is one of the most important festivals in Christianity. Easter

commemorates Christ's resurrection, who sacrificed himself for the sins of

mankind. But are people celebrating this Easter out of their own

traditional interest, or is Easter really just a commercial interest as

consumers feel encouraged to buy and give consumer goods to mark the holiday? A recent

YouGov poll of 13,000 respondents in 12 countries reveals that the majority

of people around the world still think Easter is celebrated for all the right

reasons: as a special holiday. Respondents

from Catholic Poland (82 percent) most often see the Easter holidays as a

real reason to celebrate. Only 11 percent think the celebration of

Christ's resurrection is too commercialized. Danes are second most

likely to think that Easter is still celebrated because of a special occasion

(73 percent) and not because of commercial pressures. The Spaniards (71

percent) and the Swedes (69 percent) follow in third and fourth place. In Germany,

63 percent are of the opinion that the festival is a real

celebration. However, one in four Germans (24 percent) considers the

festival to be too commercialized. The French and British are most

critical of Easter celebrations in terms of commercialization. Only half

of the French (51 percent) think the festival is being celebrated as a

"right" special occasion, while 37 percent think it's more of a

commercialization by companies. In a global comparison, the British are

most likely to think that the festival is too commercialized (40 percent).

(YouGov

Germany) April 12,

2022 Source: https://yougov.de/news/2022/04/12/ist-ostern-zu-kommerzialisiert/ SUMMARY

OF POLLS

ASIA (Malaysia) McDonald's Tops YouGov’s 2022 Dining And QSR Rankings In

Malaysia McDonald's tops YouGov’s 2022 Dining

and QSR rankings in Malaysia. The American hamburger restaurant's Index score

of 45.4 places it ahead of 34 other popular quick service restaurants in the

market. McDonald’s also ranked first in last year’s QSR rankings (50.9), but

its score has fallen by 5.5 points this year. KFC, which achieved an

Index score of 39.4, takes the second spot. The American fried chicken

restaurant also ranked second in 2021, although its score has fallen by 7.5

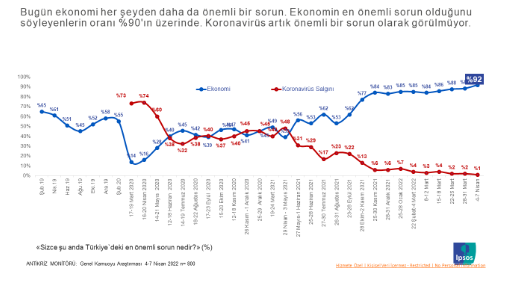

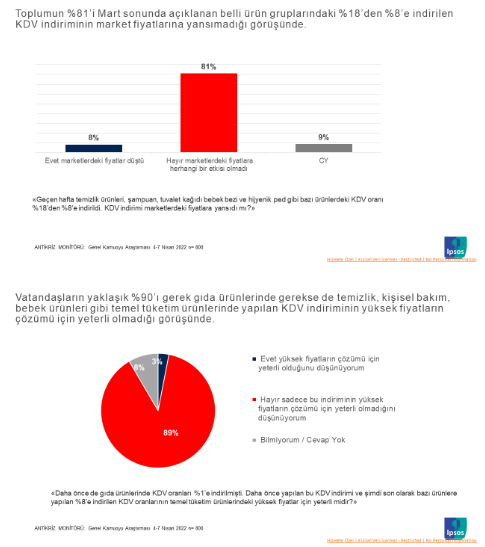

points this year (from 46.9). (YouGov Malaysia) April 12, 2022 (Turkey) Economy Is Turkey's Most Important Problem For 9 Out Of 10

People Today 91% of the society thinks that the economy

is Turkey's most important problem. With the decrease in the effect of the

epidemic, the epidemic is no longer seen as a significant problem. The

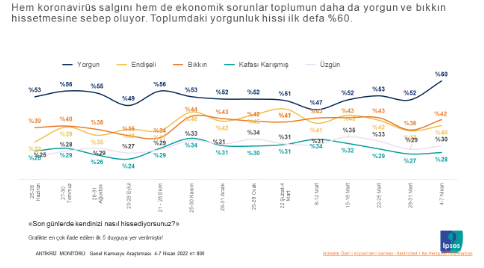

epidemic and economic problems also affect the mood of the society.

Especially with the increase in economic problems, individuals feel more

tired and bored. The feeling of fatigue is at 60% for the first time. It is

of the opinion that the VAT discount on some basic consumption products at

the end of March is not reflected in the prices in the market. And 9 out of

10 people think that the VAT discounts are not an adequate solution to the

high prices in the market. (Ipsos Turkey) 11 April 2022 (Singapore) Eco-Labels In Singapore, How Aware Are Consumers Of These

Green Certification Marks Environmental labelling certifications and eco-labels have made it simpler for consumers

today to identify products that are manufactured and/or can be used with

lower environmental impact. Latest data from YouGov RealTime Omnibus, as of April 2022, reveals that more than

nine in ten consumers in Singapore are aware of the NEA Energy Label (95%) and PUB Water Efficiency Label (96%), of

which more than one-third are “very familiar” and more than half are “quite”

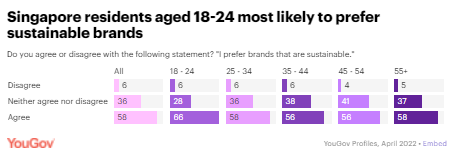

or “slightly familiar” with each label. (YouGov Singapore) Six In Ten People In S'pore Prefer

Sustainable Brands, With Those Aged 18 - 24 Most Likely To Say So Latest data from audience segmentation

tool YouGov Profiles reveals that as many as six in ten

people in Singapore say they prefer brands that are sustainable (58%),

reiterating that environmentally conscious behaviour from brands weighs heavily

on the mind of the consumer. Furthermore, those aged 18-24 are significantly

more likely to be sustainable shoppers, with two-thirds of those in this

demographic preferring sustainable brands (66%). A notable half of

sustainable shoppers aged 25-34 say they spend more when they are members of

loyalty programmes (55%), accounting for the greatest proportion of

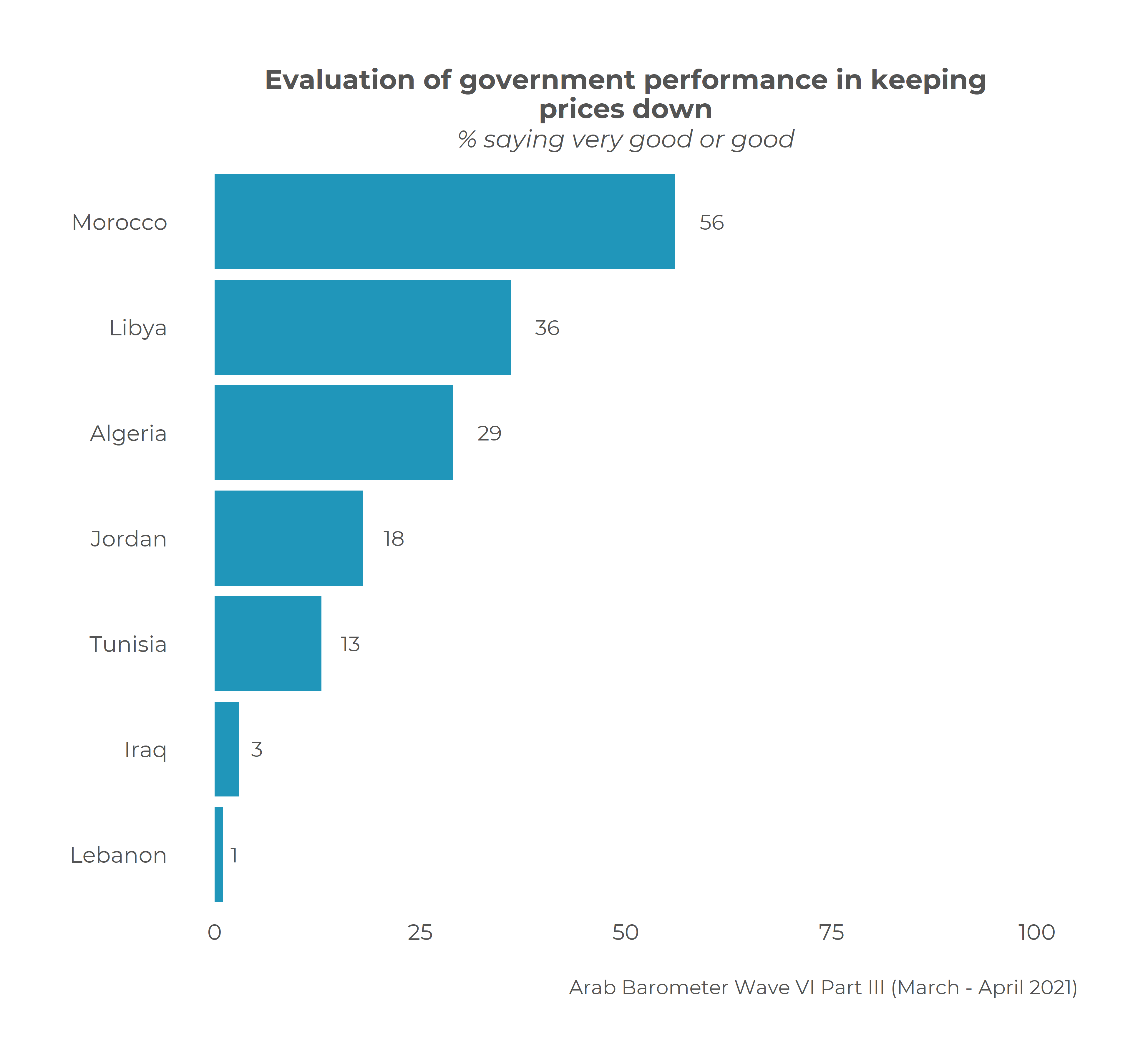

sustainable shoppers who say so. (YouGov Singapore) April 20, 2022 MENA (Iraq) Iraq Pulse: Unrest Amid The Covid-19 Pandemic The latest Arab Barometer’s (AB) survey

(Wave VI which was– conducted between March and April of 2021) attempts to

contribute to this debate. The findings of this survey display public

discontent over political life, dissatisfaction with education and health

systems and economic performances, and concerns about civil liberties. The

public views corruption as one of the main challenges that hinder progress in

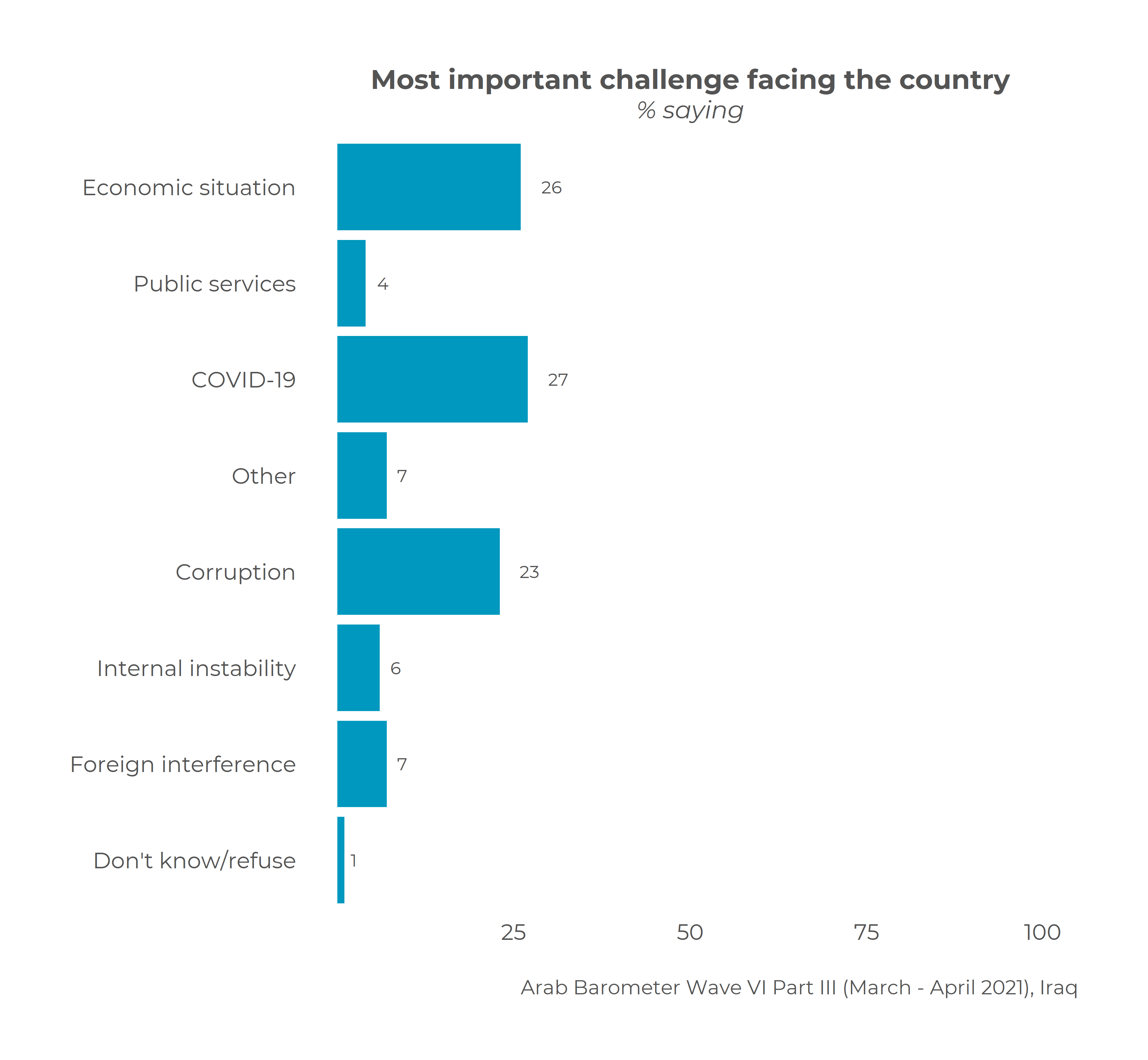

the country. Nearly a quarter (23%) of Iraqis say that corruption is the most

important challenge facing their country; the highest of all countries

included in the AB spring 2021 survey. (Arabbarometer) April 19, 2022 AFRICA (Namibia) Majority

Of Namibians Say The Country Is A Safe Place To Live, But Levels Of Fear Are

On The Rise Three out of four Namibians consider their

country a safe place to live, a recent Afrobarometer survey indicates. The

same proportion of citizens say safety and security have improved in Namibia

over the past five years – even as increasing numbers report fear of crime.

More than half of Namibians say they experienced fear of crime in their homes

and felt unsafe walking in their neighborhoods during the past year. Three-fourths

(74%) of respondents say Namibia is a "somewhat safe" (39%) or

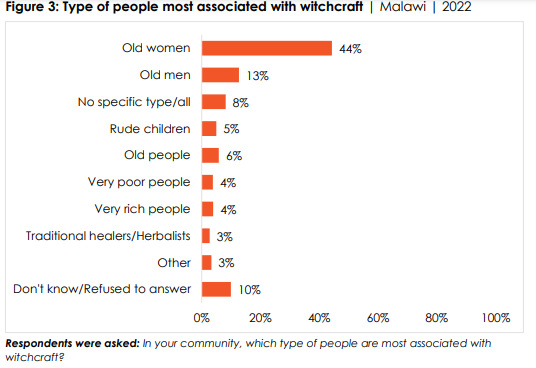

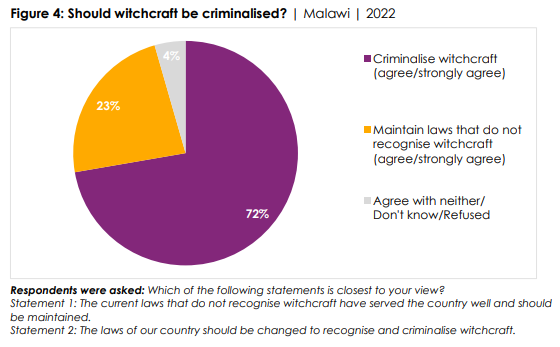

“very safe” (35%) country to live in. (Afrobarometer) 11 April 2022 (Malawi) Three In Four Malawians (74%) Believe “A Lot” In The

Existence Of Witchcraft Most Malawians strongly believe that

witchcraft exists and support changing the law to criminalize its practice, a

new Afrobarometer survey shows. Educated citizens are more likely to believe

in the existence of witchcraft than those with no formal education. Most

Malawians associate witchcraft with using magic to kill people, make them

sick or bring them misfortune. The survey shows that the elderly, especially

elderly women, are at the greatest risk of being victims of witchcraft

accusations. Almost three-fourths (72%) of Malawians say witchcraft should be

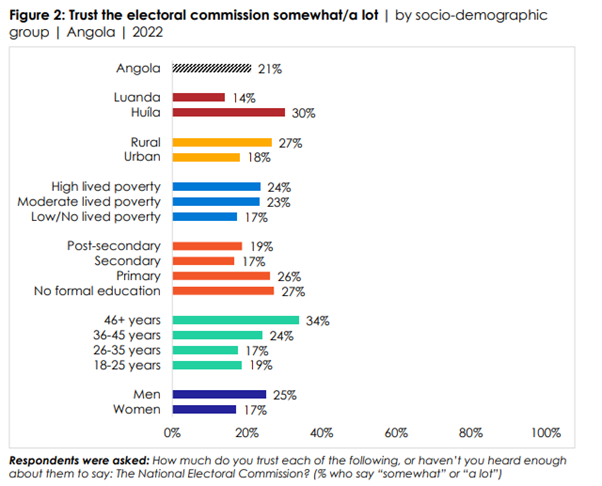

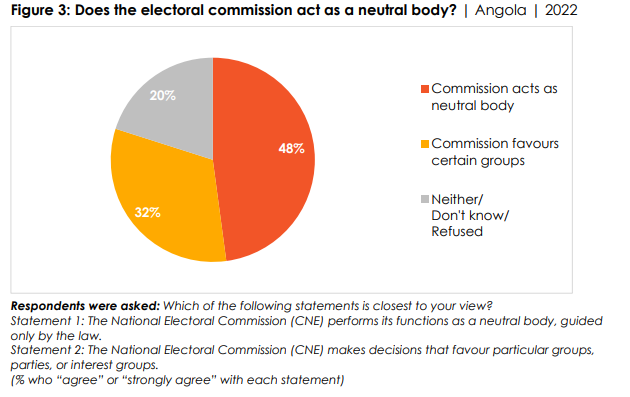

criminalized. (Afrobarometer) 14 April 2022 (Angola) Only One In Five Angolans (21%) Say They Trust The National

Electoral Commission (CNE) Somewhat Or A Lot As Angolans approach general elections in

August, only one in five citizens say they trust the National Electoral

Commission, a new Afrobarometer survey shows. Only one in five Angolans (21%)

say they trust the National Electoral Commission (CNE) “somewhat” or “a lot,”

a 6-percentage-point decline compared to 2019. Levels of trust are higher

among men (25% vs. 17% of women) and among older respondents (34% of those

aged 46 and over vs. 17%-19% of 18- to 35-year-olds). (Afrobarometer) 22 April 2022 WEST

EUROPE (UK) Seven in ten (72%) of Britons would support the

construction of a wind farm in their local area A new YouGov survey finds, however, that

Britons are perhaps more open to onshore wind than anticipated. Seven in ten

(72%) of Britons would support the construction of a wind farm in their local

area – including 33% who would "strongly" back one. Only 17% would

oppose a new wind farm in their area. This compares to just 34% who would

support a nuclear power plant in their area. Half (50%) would oppose the

creation of a new nuclear site near them, with some 28% strongly opposed to

the suggestion. (YouGov UK) April 11, 2022 More Than One In Two Britons Support Ban On Whipping Racehorses New research from Ipsos UK, released ahead

of this weekend’s Grand National, reveals that more than one in two Britons

aged 16-75 (55%) want jockeys banned from using the whip whilst three in ten

(31%) believe horse racing is unacceptable. Men (54%) and women (55%) are

united in supporting a ban on the whip. However, there is a gender divide

about whether horse racing as a sport is acceptable or not - 38% of women

believe horse racing is unacceptable compared with 24% of men. (Ipsos MORI) 12 April 2022 Should Selective Breeding Of Dogs With Health Issues Be

Banned YouGov asked the British public whether

they would support or oppose a ban in the UK on the selective breeding of

certain types of dogs. Half of the respondents were asked whether they would

support a ban on selective breeding where it results in serious health

issues, like breathing problems or increased cancer risk, and the other half

were asked whether they would support a ban on selective breeding of

brachycephalic (flat-faced) dogs, like pugs and French bulldogs. Seven in 10

(71%) would support banning selective breeding where it results in dogs with

serious health issues, with just 20% opposed and 9% unsure. (YouGov UK) April 13, 2022 Majority Of Britons Say Boris Johnson Should Resign, In

Aftermath Of ‘Partygate’ Fines New polling of the British public on

Tuesday (12th) and Wednesday (13th) this week in the aftermath of the Prime

Minister being issued with a Fixed Penalty Notice shows that Britons think

Boris Johnson should resign by a 2:1 margin. 54% would support the Prime

Minister resigning and 27% would oppose. Support for his resignation is

unchanged from a similar poll taken April 1st to 3rd, which asked what people

thought he should do if he received a fine. Meanwhile, there are some signs

Conservative voters from 2019 are rallying behind the Prime Minister. 48% now

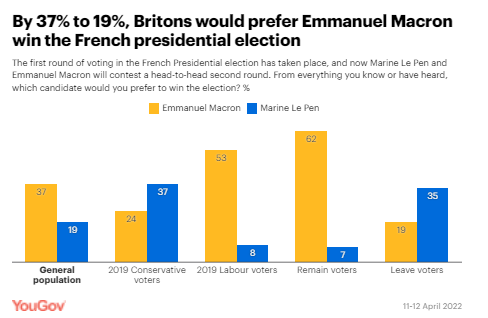

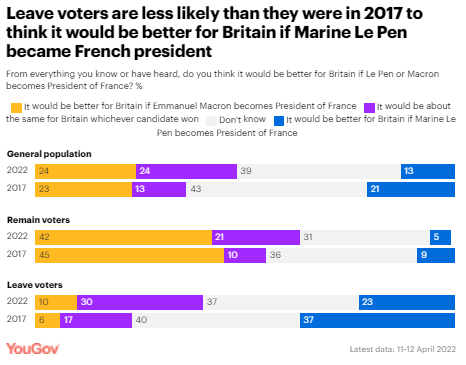

oppose his resignation compared to 37% at the beginning of the month. (Ipsos MORI) 14 April 2022 By 37% To 19% Britons Would Prefer Emmanuel Macron Win The

French Presidential Election The French public went to the polls over

the weekend for the first round of their presidential election. The results

are a repeat of 2017, with centrist Emmanuel Macron facing off against

far-right Marine Le Pen in a run-off vote next weekend. Here in Britain,

Macron is the preferred candidate, by 37% to Le Pen’s 19%. The largest

portion of the public (44%), however, do not seem to be au fait with French

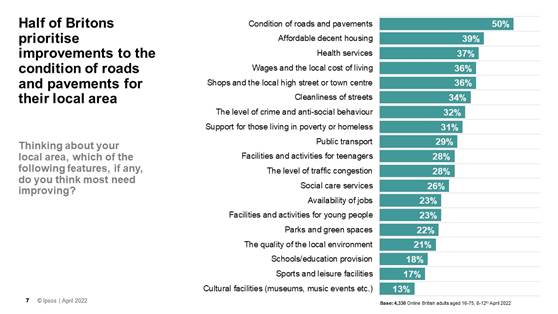

politics, answering “don’t know”. (YouGov UK) April 15, 2022 4 In 10 (39%) Britons Say Affordable Decent Housing Needs

To Be Improved Ahead Of The Local Elections On 5th May Ahead of the local elections across parts

of the country next month, new research by Ipsos shows half of Britons say

the conditions of roads and pavements are most in need of improvement (50%)

in their local area, while 4 in 10 (39%) say affordable decent housing needs

to be enhanced. The public’s priorities also include improvements in health

services (37%), wages and local cost of living (36%), shops and the local

high street/town centre (36%), and cleanliness of streets (34%) in their

local area. (Ipsos MORI) 20 April 2022 YouGov Food Study Shows That Three In Four

Britons (75%) Eat Meat The YouGov Food Study shows that three in

four Britons (75%) eat meat, with this being more the case for men (82%) than

women (69%). Six percent describe themselves as vegetarian (8% of women and

3% of men), while a further 11% say they are flexitarian. Two percent of

Britons are vegans and 3% are pescatarians. Our study shows that the younger

Britons are, the less likely are they to eat meat: 75% of those aged 16-24

eat meat, compared to 95% of those 60 and older. (YouGov UK) April 20,

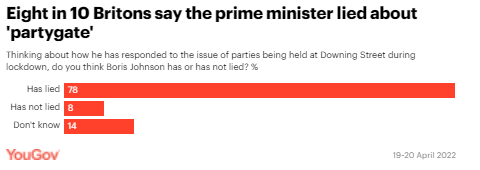

2022 Eight In 10 Britons Say Boris Johnson Lied

About Lockdown Parties New polling from YouGov / The Times reveals

more than three quarters of Britons (78%) think Boris Johnson has lied in his

response to the issue of parties being held at Downing Street during

lockdown. Just 8% think he has not lied, and 14% are unsure. Half of those

who currently intend to vote Conservative (51%) say Boris Johnson has lied

about ‘partygate’, with a quarter (25%) saying he has not lied and a further

25% unsure. Those who backed the party in the 2019 general election are more

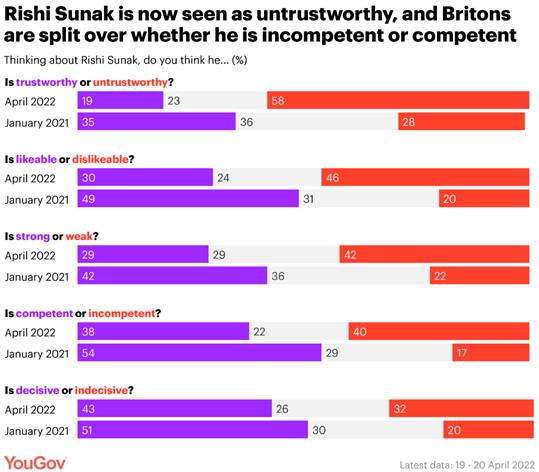

likely still to think that the prime minister has lied, at 61%. (YouGov UK) April 21, 2022 Most Britons Now See Rishi Sunak As

Untrustworthy And Are Split Over His Competence New YouGov polling shows a dramatic shift

in the tone of the public’s perceptions of Rishi Sunak. Half of the

population now consider him to be “untrustworthy” (58%) – a figure up 30pts

compared to January 2021 (28%). While only 19% of the public currently

consider Sunak trustworthy, Conservative voters are split 38% to 40% on

whether the Chancellor is trustworthy or not. Indeed, while this change is

far from positive, Sunak does again retain a lead over Boris Johnson, who is seen as untrustworthy by far more

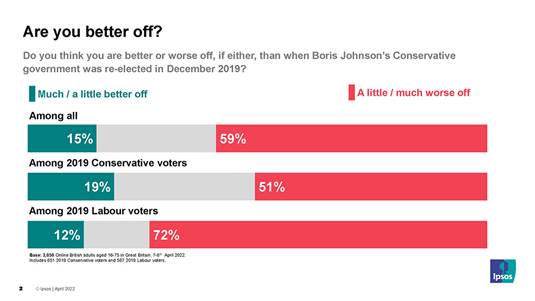

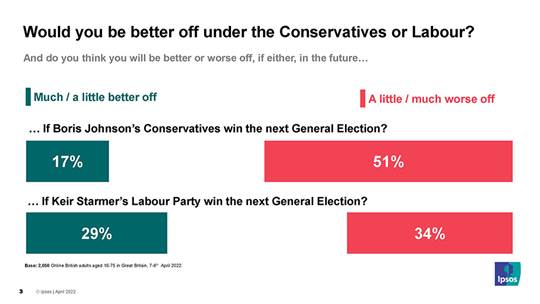

people (74%) than Sunak, with 12% saying he is trustworthy. (YouGov UK) April 21, 2022 59% Of Britons Say They Feel Worse Off

Since The Last General Election New polling from Ipsos, taken on April 7th

and 8th, shows that 59% of Britons think they are worse off than when the

Conservatives won the last General Election. 15% say they are better off and

the rest say neither or don’t know. 17% said they would be better off if

Boris Johnson’s Conservatives won the next General Election. 51% said they

would be worse off. 29% said they would be better off if Keir Starmer’s

Labour Party won the next General Election. 34% said they would be worse off. (Ipsos MORI) 22 April 2022 6 In 10 Would Rather Be A Citizen Of

Britain Than Any Other Country In The World New research from Ipsos, ahead of St.

George’s Day on 23rd April, shows a majority of British citizens agree with

the statement, “I would rather be a citizen of Britain than of any country in

the world,” 6 in 10 (60%) agree while only 13% do not. This is broadly in

line with the results six years ago in 2016. Older Britons (70% of

55-75 year olds) and 2019 Conservative voters (76%) are most likely to agree. (Ipsos MORI) 24 April 2022 (France) 82% Of French People Say They Are Worried About The Risks

Of A Cyberattack In The World The study reveals that two out of

three French people consider that in France, the risk of nuclear disaster or

industrial accident due to a cyberattack is significant. In a

particularly uncertain geopolitical context, the French are worried about the

global risks of cyberattacks, a weapon that has become increasingly common in

modern conflicts. 82% of French people say they are worried about the

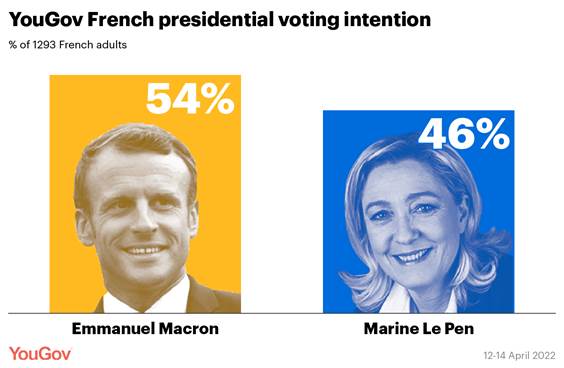

risks of a cyberattack in the world and 79% in France. (Ipsos France) April 13, 2022 Boost For Macron As He Opens Up 8-Point Lead Over Le Pen With the race to win the French presidency

reaching its final stage, the two second round candidates – Emmanuel Macron

and Marine Le Pen – are competing for every vote in what is expected to be a

tight and tough contest. Second round vote intention figures ahead of last

Sunday’s ballot showed Macron with a two-point lead, but today’s new

YouGov/DataPraxis poll puts the incumbent eight points ahead, with 54% of

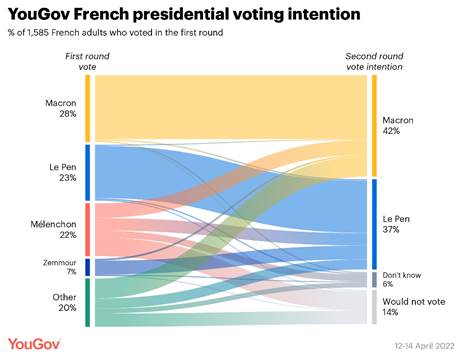

current vote intention compared to 46% for Le Pen. (YouGov UK) April 15, 2022 Final Study Of The French Elections: Macron Leads 56% To

44% Our YouGov / Data Praxis study reveals 12

points ahead for Emmanuel Macron (56% against 44% for Marine Le

Pen). Such a result would represent a drop of 10 points from Emmanuel

Macron's 2017 vote share – nevertheless, he achieves a clear victory over his

opponent. One of the decisive factors in the second round is the voting

choice of voters who supported Jean-Luc Mélenchon (22%). According to

our data, one in five voters (18%) who voted for Mélenchon intend to vote for

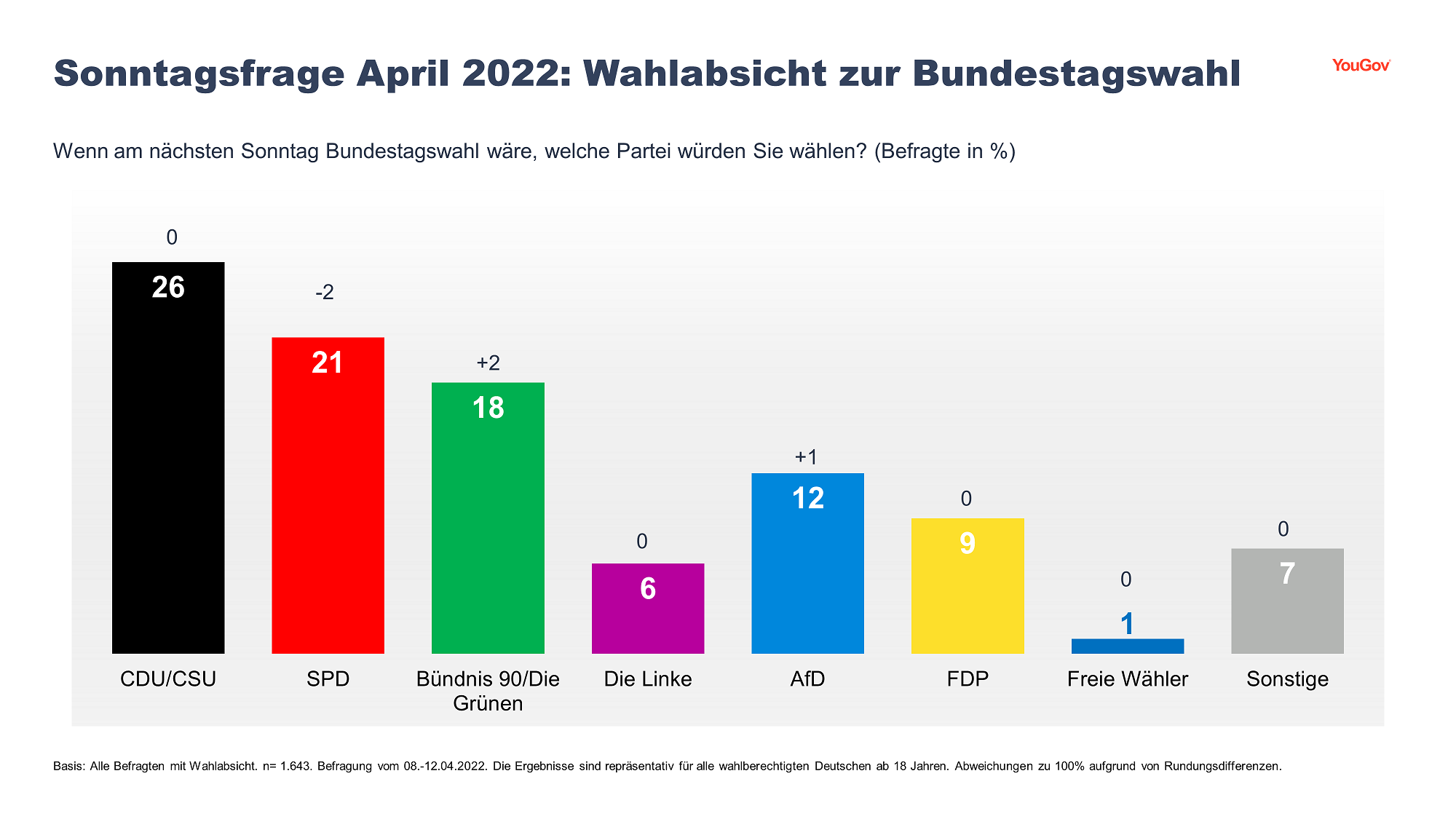

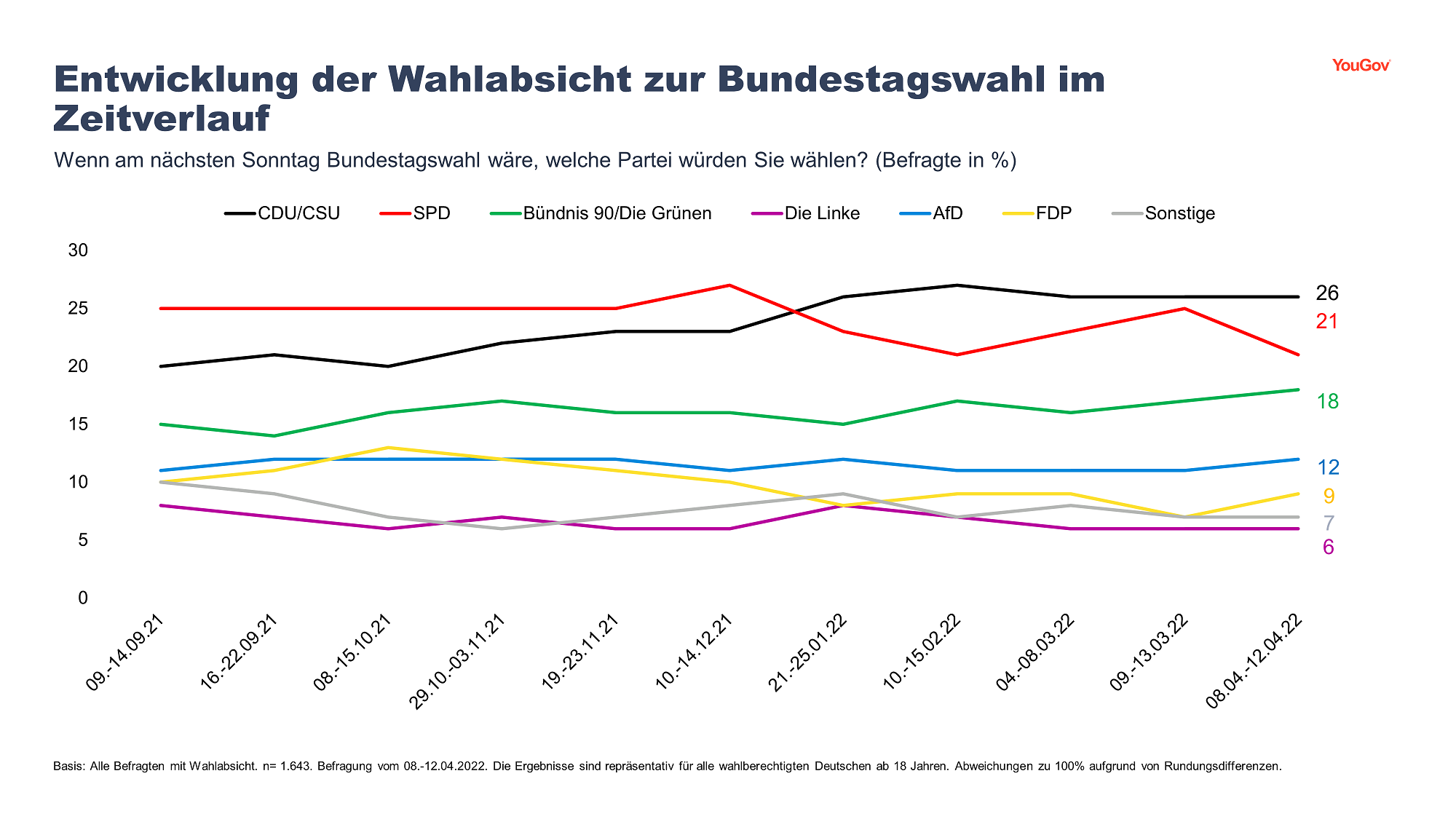

Le Pen vs 38% for Macron. (YouGov France) April 22, 2022 (Germany) 26 Percent Of German Citizens Who Are Eligible To Vote Say

They Will Vote For The CDU/CSU If The General Election Is Next Sunday As in the previous month, 26 percent of

German citizens who are eligible to vote say they will vote for the CDU/CSU

if the general election is next Sunday. The SPD would currently vote for

21 percent, 2 percentage points less than in the previous month. This

increases the Union's lead again slightly to 5 percentage points. The FDP

remains unchanged at 9 percent, the left still at 6 percent. 12 percent

of German voters would vote for the AfD if there were a federal election next

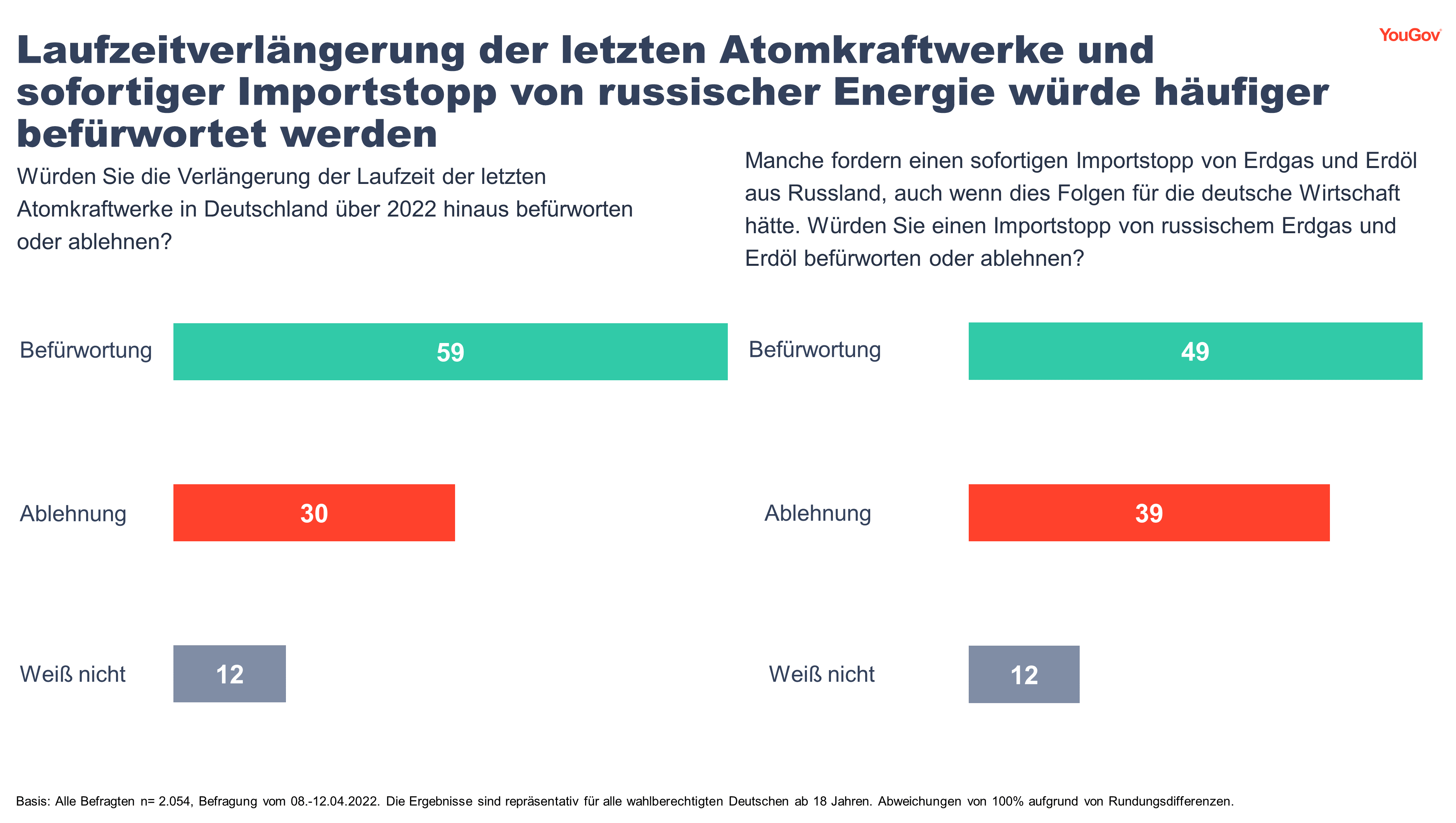

Sunday (11 percent in the previous month). (YouGov Germany) April 14, 2022 Germans More In Favor Of Extending The

Lifetime Of The Last Nuclear Power Plants 49 percent of the German population would

support an immediate ban on imports of natural gas and oil from Russia, even

if this had consequences for the German economy. Two out of five

respondents (39 percent) would reject this. 59 percent of German voters made

this statement. On the other hand, 30 percent would reject an extension

of the term, most frequently Green Party voters (56 percent). The most

common endorsement would come from Union voters (77 percent). (YouGov Germany) April 22, 2022 (Italy) Italians And April 25: The Liberation

Between The Past And The Present April 25 is the Liberation

Day , in memory of April 1945 which saw the end of the

Nazi-Fascist occupation in Italy. 52 % of Italians celebrate it, while 43% do not, and a

further 6% say they are uncertain. The most common ways to celebrate

are family celebrations (61%),

watch themed TV programs (28%),

share themed posts on social media (19%), or participate

in events and parades

(17%); a percentage, the latter, which reaches 23% in the North-West,

where the main events are held, including the parade in Milan, which will

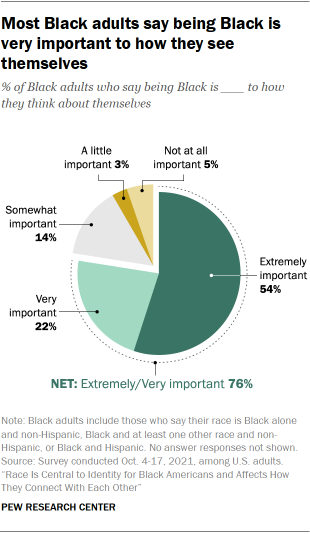

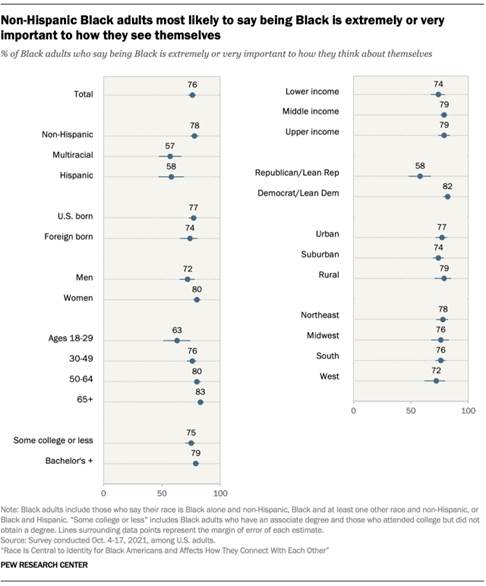

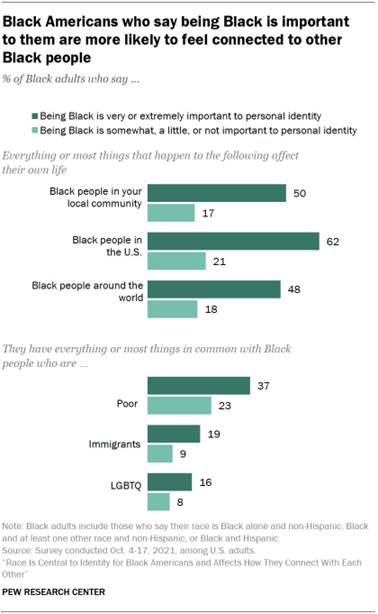

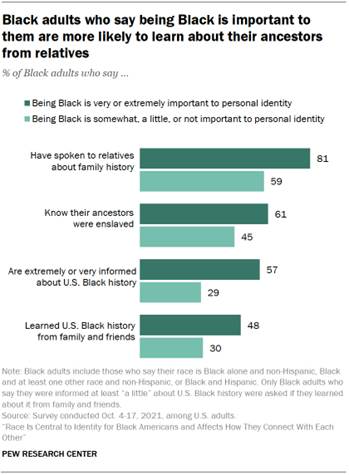

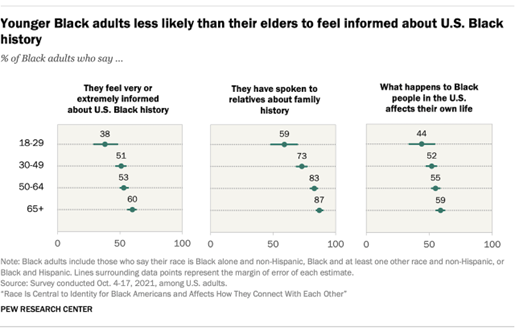

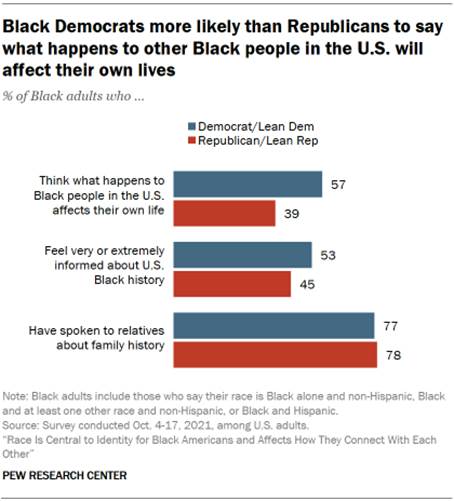

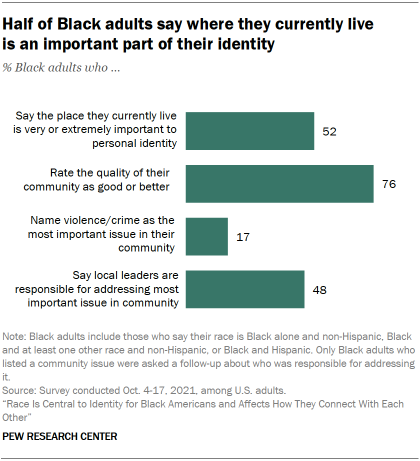

return in 2022 after 2 years of absence. (YouGov Italy) April 21, 2022 NORTH AMERICA (USA) Race Is Central To Identity For Black Americans And Affects

How They Connect With Each Other A majority of non-Hispanic Black Americans

(78%) say being Black is very or extremely important to how they think about

themselves. This racial group is the largest among Black adults, accounting for 87% of the adult population,

according to 2019 Census Bureau estimates. But among other Black Americans,

roughly six-in-ten multiracial (57%) and Hispanic (58%) Black adults say

this. Specifically, 76% of Black adults ages 30 to 49, 80% of those 50 to 64

and 83% of those 65 and older hold this view, while only 63% of those under

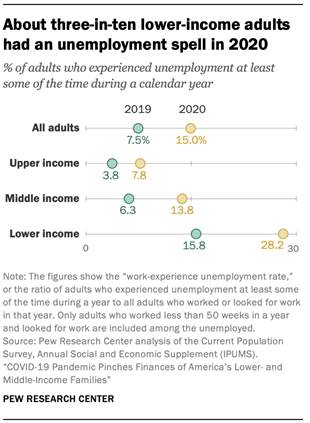

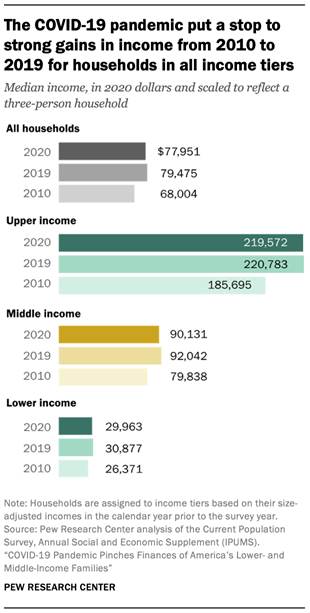

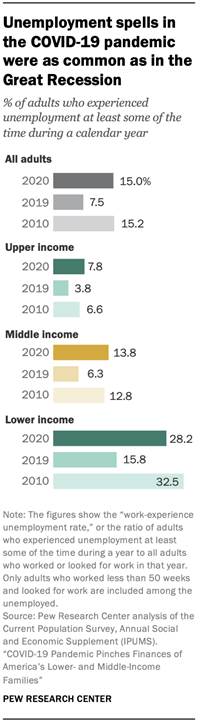

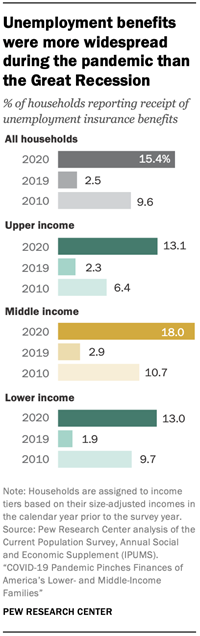

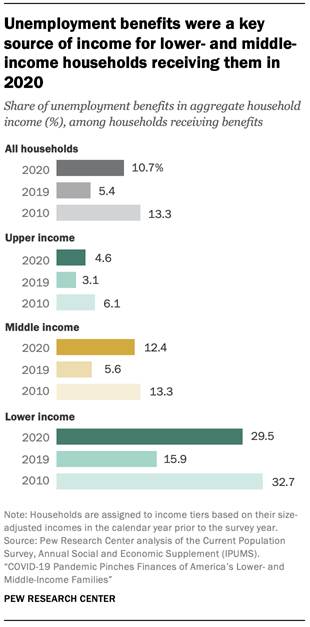

30 do. (PEW) APRIL 14, 2022 Covid-19 Pandemic Pinches Finances Of America’s Lower- And

Middle-Income Families From 2019 to 2020, the median income of

lower-income households decreased by 3.0% and the median income of

middle-income households fell by 2.1%. In contrast, the median income of

upper-income households in 2020 was about the same as it was in 2019,

according to a new Pew Research Center analysis of government data. The

median incomes of households in all income tiers had increased at about the

same pace – an annual average rate of 1.8% for lower-income families, 1.6%

for middle-income families and 1.9% for upper-income families, after

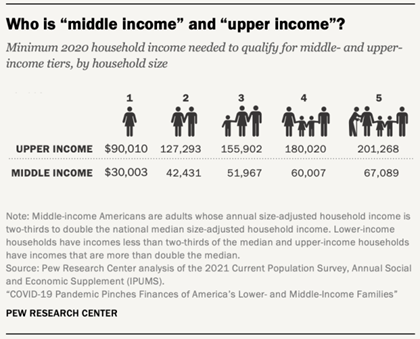

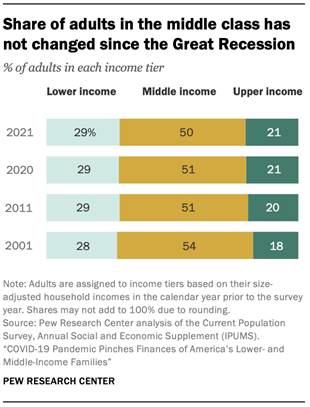

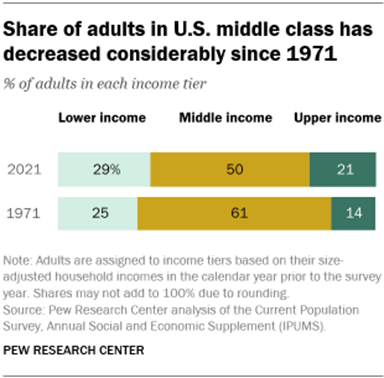

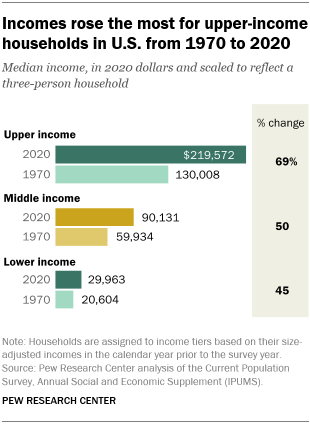

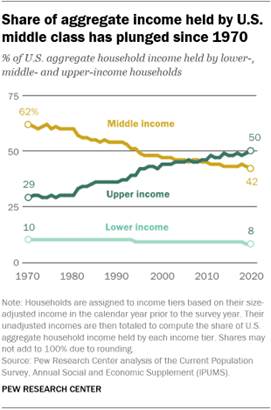

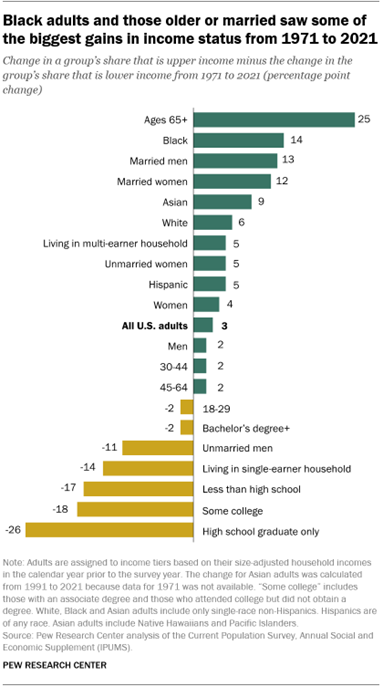

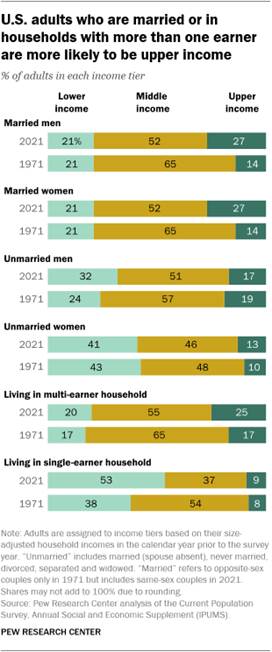

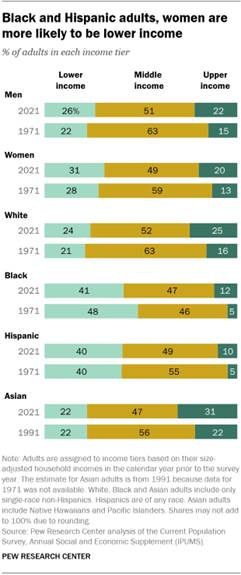

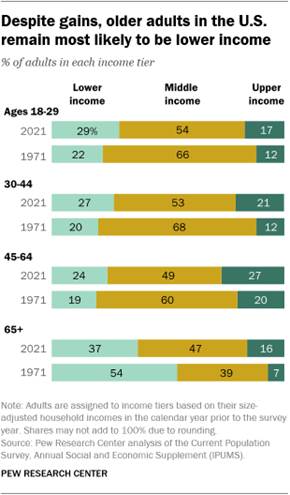

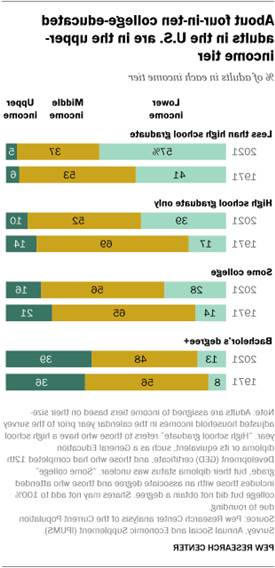

adjusting for inflation. (PEW) APRIL 20, 2022 How The American Middle Class Has Changed In The Past Five

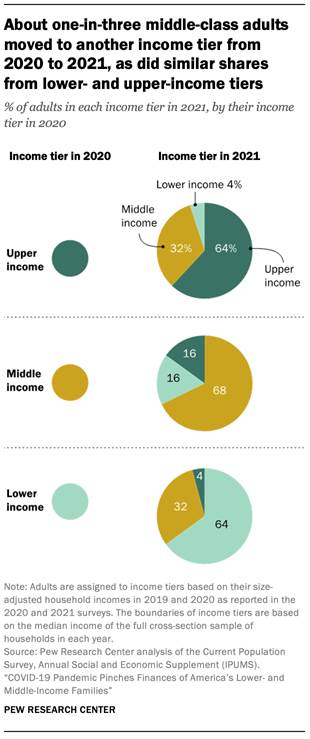

Decades The middle class, once the economic stratum

of a clear majority of American adults, has steadily contracted in the past

five decades. The share of adults who live in middle-class households fell from

61% in 1971 to 50% in 2021, according to a new Pew Research Center analysis

of government data. The median income for lower-income households grew more

slowly than that of middle-class households, increasing from $20,604 in 1970

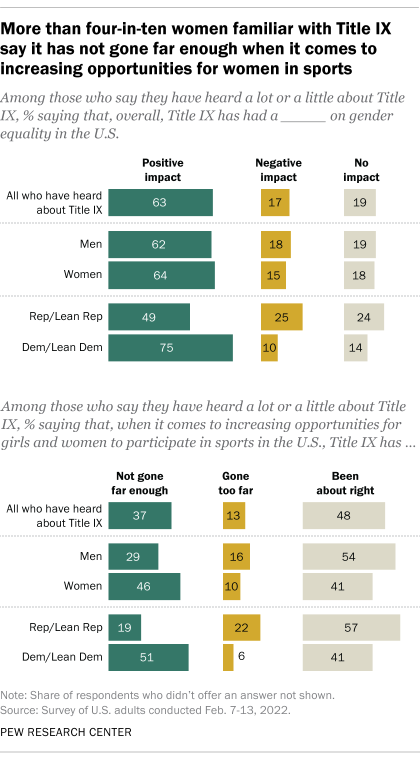

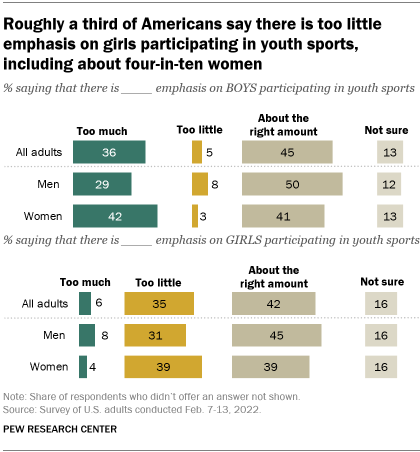

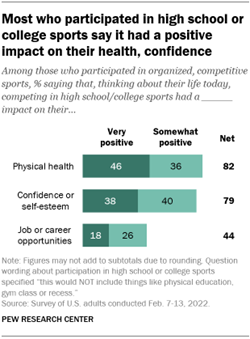

to $29,963 in 2020, or 45%. (PEW) APRIL 20, 2022 Most Americans Who Are Familiar With Title IX, Say It’s Had

A Positive Impact On Gender Equality Fifty years after the passage of Title IX, which prohibits high schools and colleges

that receive federal funding from discriminating based on sex, most Americans

who have heard about the law say it’s had a positive impact on gender

equality in the United States (63%). Still, 37% of those who are familiar with

Title IX say it has not gone far enough in increasing opportunities for women

and girls to participate in sports, according to a February Pew Research

Center survey of U.S. adults. (PEW) APRIL 21, 2022 (Canada) Most (64%) Canadian Farmers “Cautiously Optimistic” About

the Next 12 Months Despite the degree of uncertainty that the

future hold, most Canadian farmers remain “cautiously optimistic” (64%) about

the next twelve months, while 17% are very optimistic, according to the new

RBC Agriculture Poll conducted by Ipsos. Only one in five farmers is

pessimistic (7% mostly/12% somewhat) about the next year. Moreover, seven in

ten (71%) agree (32% strongly) that they’re making progress on recruiting and

promoting a diverse workforce, including women in all levels. In fact, six in

ten (61%) farmers say that their leadership team includes women. (Ipsos Canada) 12 April 2022 Canadians Believe Poilievre Has Edge Over Rest Of

Conservative Field, But Are Less Certain That They Want Him To Win Canadians don’t have a particularly

favourable impression of any of the declared or likely candidates for the

leadership of the Conservative Party of Canada. Moreover, according to a new

Ipsos poll conducted for Global News, out of the 11 candidates tested, a majority

of Canadians say they don’t know enough about 9 of them to have an opinion

one way or the other, leaving only Pierre Poilievre and Jean Charest as the

candidates that most Canadians are familiar with – for better or for worse. (Ipsos Canada) 20 April 2022 AUSTRALIA Real Unemployment In Australia Is Far Higher Than Claimed

By The ABS, And High Under-Employment Keeps A Lid On The Wage Growth Of

Workers The first Omicron wave began in early

December and led to infections peaking in mid-January at over 700,000 before

declining rapidly over the next few weeks and bottoming in February. A second

Omicron wave began in early March and is still ongoing with tens of thousands

of new cases every day. The forced isolation of many employees is in turn

forcing businesses to hire more workers on part-time hours. In March

part-time employment increased by 289,000 to a near-record high of over 4.7

million. (Roy Morgan) April 14 2022 8 In 10 Australians Are Concerned About Climate Change With

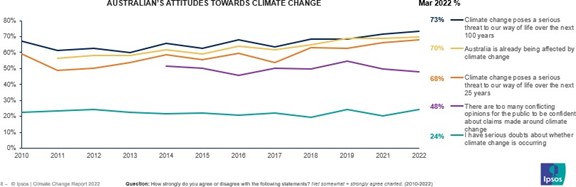

A Clear Public Expectation Of Government Action Australians are concerned about climate change (83%)

and 70% consider that Australia is

already being affected by climate change, primarily with more

frequent and extreme natural disaster events which is a steady increase in

concern and up from 56% in 2011. Interestingly, the proportion of people

expressing doubt about whether climate change is actually occurring has

remained relatively steady over the same period, with 24% currently

expressing this view. The level of doubt is significantly higher in NSW with

this figure rising to one in three (32%). (Ipsos Australia) 20 April 2022 MULTICOUNTRY STUDIES Biden Ended His First Year In Office With A 45% Median

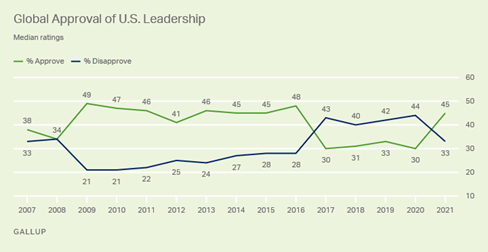

Approval Rating Across A Total Of 116 Countries And Territories A new Gallup report details that by early August 2021,

median approval of U.S. leadership worldwide stood at 49% across 46 countries

and territories surveyed by that point. This approval rating matched the

record-high rating when former President Barack Obama first took office in

2009. However, the United States' overall rating slipped in the second half

of the year. Across 70 additional countries and territories surveyed during

and after the U.S. withdrawal from Afghanistan, median approval stood at 43%. (Gallup) APRIL 12, 2022 Source: https://news.gallup.com/poll/391661/approval-ratings-retreat-afghanistan-withdrawal.aspx Worldwide Celebration Of Easter French And British Are Most

Critical Of Easter Celebrations In Terms Of Commercialization, A YouGov Poll

In 12 Countries Around The World A recent YouGov poll of 13,000 respondents

in 12 countries reveals that the majority of people around the world still

think Easter is celebrated for all the right reasons: as a special holiday. In

Germany, 63 percent are of the opinion that the festival is a real

celebration. However, one in four Germans (24 percent) considers the

festival to be too commercialized. The French and British are most

critical of Easter celebrations in terms of commercialization. Only half

of the French (51 percent) think the festival is being celebrated as a

"right" special occasion, while 37 percent think it's more of a

commercialization by companies. In a global comparison, the British are

most likely to think that the festival is too commercialized (40 percent). (YouGov Germany) April 12, 2022 Source: https://yougov.de/news/2022/04/12/ist-ostern-zu-kommerzialisiert/ Africans Divided On Russia's Leadership Before Ukraine War

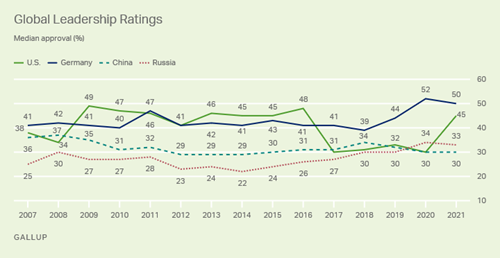

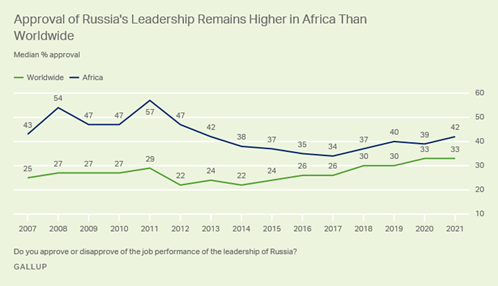

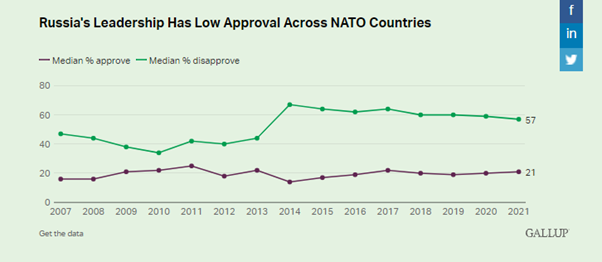

A Survey In 19 Nations Overall, median approval of Russia's

leadership stood at 42% across Africa in 2021, which is lower than the

approval ratings of the leadership of the U.S. (60%), China (52%) and Germany

(49%). However, approval of Russia's leadership remains consistently higher

in Africa than the global median of 33%. Africans have held a more positive

view of Russia for some time, reaching a peak of 57% approval in 2011, before

opinions started declining over the past decade. Line graph. Trend line

showing median approval ratings of Russia's leadership across Africa and

worldwide, from 2007 to 2021. In 2021, a median of 42% of Africans approved

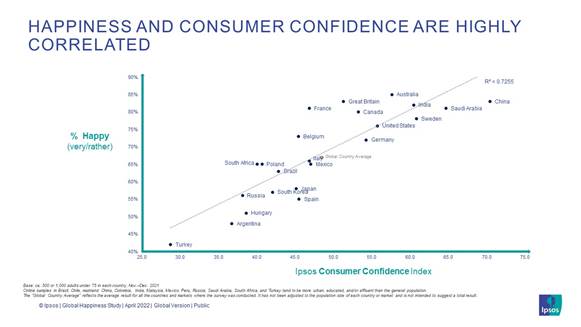

of Russia's leadership, versus 33% approval worldwide. (Gallup) APRIL 13, 2022 Source: https://news.gallup.com/poll/391718/africans-divided-russia-leadership-ukraine-war.aspx What Makes People Happiest 30-Country Ipsos

Survey An Ipsos global survey run at the end of

2021, prior to the current war in Ukraine and at the beginning of the cost of

living crisis, found that happiness amongst Britons had returned to pre-COVID

levels, with 83% of people reporting to be very or rather happy (82% in 2019,

prior to the pandemic). This is considerably higher than the global average

of 67%, across 30 countries. Happiness is most prevalent in the

Netherlands and Australia, with 86% and 85% respectively describing

themselves as “very” or “rather” happy. China and Great Britain (both 83%),

India (82%), France and Saudi Arabia (both 81%), and Canada (80%) follow. (Ipsos MORI) 14 April 2022 Source: https://www.ipsos.com/en-uk/what-makes-people-happiest-health-family-and-purpose A Global Median Of 33% Approved Of Russia's Leadership In

2021 Among 116 Countries Before Russia's invasion of Ukraine this

year, Russia's leadership remained relatively unpopular in most parts of the

world, with a global median approval rating of 33% in 2021. As unimpressive

as this current rating seems, it's still a marked improvement from the 22%

median approval rating in 2014, notably the last time Russia invaded Ukraine

and ended up annexing Crimea. After Crimea, Russia's global reputation slowly

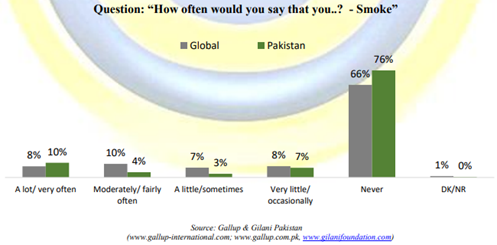

started to improve, reaching as high as 34% in 2020. (Gallup) APRIL 15, 2022 Source: https://news.gallup.com/poll/391775/russia-leadership-not-highly-popular-ukraine-war.aspx Incidence Of Smoking In Pakistan Is Lower Than The Global Average According to a Gallup Pakistan Survey in

Pakistan (and similar surveys done by Worldwide Independent Network of Market

Research (WIN) across the world), the incidence of smoking in Pakistan is

lower than the global average; a quarter of the male adult population and 7%

of the female population claim to smoke in Pakistan. A nationally

representative sample of adult men and women from across the four provinces

was asked the following question, “How often would you say that you...? -

Smoke” In response to this question in Pakistan, 10% said very often, 4% said

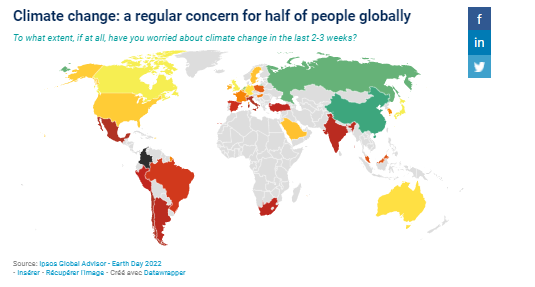

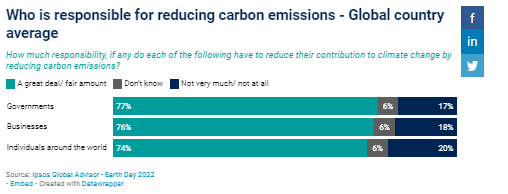

fairly often, 3% said sometimes, 7% said occasionally and 76% said never. (Gallup Pakistan) April 15, 2022 Source: https://gallup.com.pk/wp/wp-content/uploads/2022/04/15-April-2022-English-1.pdf An Average Of 39% Agree That Their Government Has A Clear

Plan In Place To Tackle Climate Change In A 30 Country Survey 68% think government and businesses need to

act now or risk failing future generations. Just 39% agree that their

government has a clear plan in place to tackle climate change. Climate change

sits 8th on a list of concerns for the public. The public believe there is a

shared responsibility among government (77%), businesses (76%) and

individuals (74%) to tackle climate change. Some business sectors are seen as

having a greater responsibility for reducing their contribution to climate

change – particularly energy companies (82%), car manufacturers (80%),

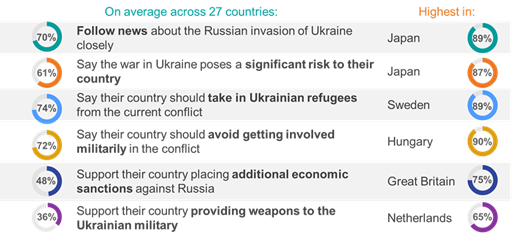

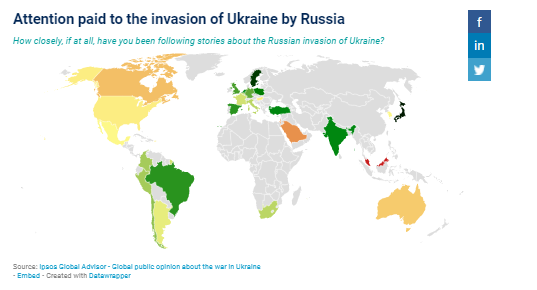

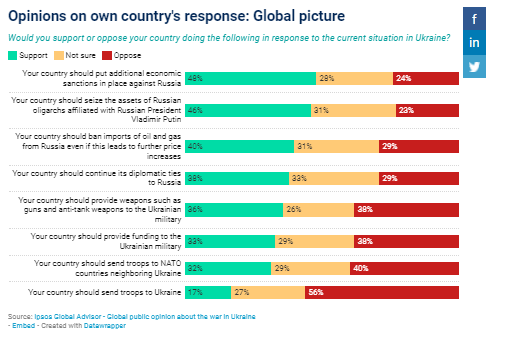

airlines (77%) and public transport providers (77%). (Ipsos South Africa) 18 April 2022 Source: https://www.ipsos.com/en-za/global-advisor-earth-day-2022 61% Across 27 Countries Think The War In Ukraine Poses A

Significant Risk To Their Country A new Ipsos survey finds that, on average

across 27 countries, 70% of adults report closely following the news

about Russia’s invasion of Ukraine and 61% think it poses a significant risk

to their country. Majorities in every one of the countries surveyed

support taking in Ukrainian refugees and oppose getting involved militarily

in the conflict. However, opinions on economic sanctions and providing

weapons to the Ukrainian military differ widely across countries. Those who

follow the news about the war in Ukraine represent between 57% and 77% of

those surveyed in all but three of the 27 countries. The only exceptions

are Japan (89%) and Sweden (83%) at one end of the spectrum and Malaysia

(49%) at the other end. (Ipsos South Africa) 19 April 2022 Source:

https://www.ipsos.com/en-za/war-in-ukraine-april-2022 Globally Respondents Strongly Support The Notion Of

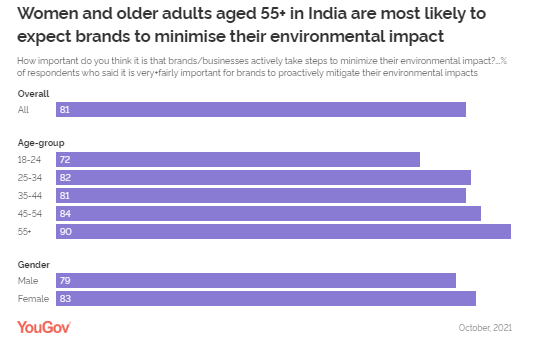

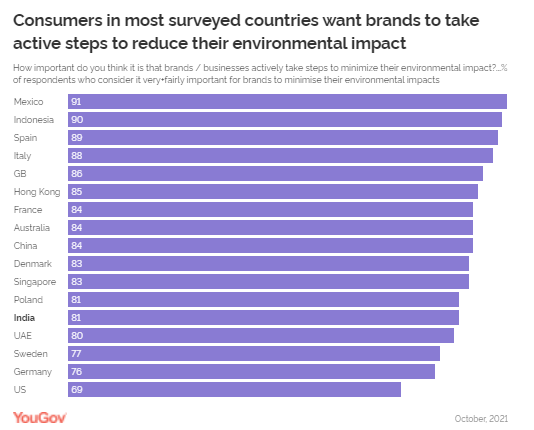

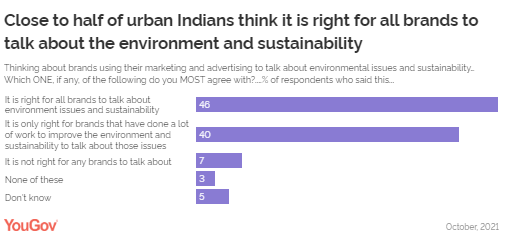

Businesses/Brands Taking Steps To Reduce Their Environmental Impact, A Study

In 17 Nations On the occasion of World Earth Day,

YouGov’s international study which polled more than 19,000 people across 17

countries, reveals that a majority (81%) of urban Indians said it’s

“important” (46% “very” and 35% “fairly”) for brands or businesses to

actively take steps to minimise their impact on the environment. A larger

proportion of female respondents said this, indicating that women feel more

strongly about this issue than men in the country (83% vs 79%). Similarly,

the older adults aged 55+ are most likely among the different age groups to

advocate this view. (YouGov India) Source: https://in.yougov.com/en-hi/news/2022/04/20/most-urban-indians-want-brands-take-active-measure/ The Image Of U S Leadership Is In A Much Stronger

Position, Result Of A Study Across 34 Nations Gallup surveys show median approval of U.S.

leadership across Asia shot from 31% in 2020 to 41% in 2021, and the U.S. now

essentially ties Germany for the most-positively viewed leadership in the

region. Unlike approval of the U.S., Germany's 2021 approval rating was

mostly unchanged from previous years, while Russia (33%) and China (27%) were

also on a similar footing to where they have ranked in the past. China's

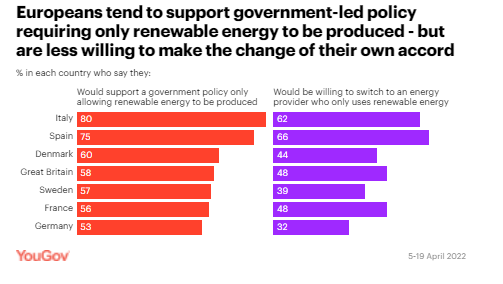

approval continued to drift slightly lower in 2021. (Gallup) APRIL 22, 2022 Source: https://news.gallup.com/poll/391940/germany-lead-approval-ratings-asia.aspx Europeans Express Wide Support For A Greener Energy Market,

According To A Poll Across 7 Countries New YouGov EuroTrack polling across seven

European countries suggests that there is significant public appetite for

substantial policy changes that would see a much greener energy market,

something that climate change activists have been pushing for a long time. Across

all countries polled, a majority would support a government policy that ruled

that only renewable energy can be produced. Italians and Spaniards feel

particularly strongly about this, with 80% of Italians, and 75% of Spaniards

supporting such a policy. The Germans need more persuading, with just 53%

supporting this proposal. (YouGov UK) April 22, 2022 ASIA

738-739-43-01/Polls McDonald's Tops YouGov’s 2022 Dining And

QSR Rankings In Malaysia

McDonald's tops YouGov’s 2022 Dining

and QSR rankings in Malaysia. The American hamburger restaurant's Index score

of 45.4 places it ahead of 34 other popular quick service restaurants in the

market. McDonald’s also ranked first in last year’s QSR rankings (50.9), but

its score has fallen by 5.5 points this year. KFC, which achieved an Index score of 39.4,

takes the second spot. The American fried chicken restaurant also ranked

second in 2021, although its score has fallen by 7.5 points this year (from

46.9). Domino’s Pizza, which achieved an Index

score of 28.1, clinched the third position. The American pizzeria rose one

spot from 2021, when its previous score of 28.3 placed it in fourth

Subway achieved an Index score of 27.8

to come in fourth. The American sandwich restaurant rose one spot from 2021,

when it was fifth (27.7). Pizza Hut, which achieved an Index score of

27.8, rounds out the top five. The American pan pizza restaurant dropped two

spots from last year (30.0), after its score fell by 2.2 points this year. (YouGov

Malaysia) April 12,

2022 Source: https://my.yougov.com/en-my/news/2022/04/12/malaysia-best-quick-service-restaurants-2022/ 738-739-43-02/Polls Economy Is Turkey's Most Important Problem

For 9 Out Of 10 People Today

Economy is

Turkey's Most Important Problem for 9 out of 10 People Today 91% of the

society thinks that the economy is Turkey's most important problem. With the

decrease in the effect of the epidemic, the epidemic is no longer seen as a

significant problem.

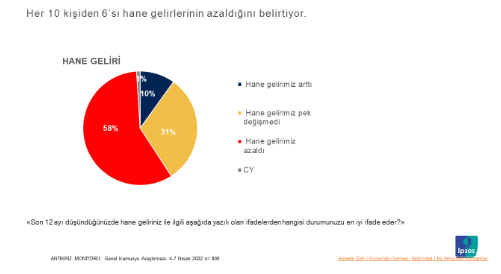

6 out of 10

People Have Decreased Household Income 58% of

individuals say their household income has decreased in the last 12 months.

Those who say that their household income has increased are only 10% of the

society.

Society

Feels More Tired and Bored The epidemic

and economic problems also affect the mood of the society. Especially with

the increase in economic problems, individuals feel more tired and bored. The

feeling of fatigue is at 60% for the first time.

It is of the

opinion that the VAT discount on some basic consumption products at the end

of March is not reflected in the prices in the market. And 9 out of 10 people

think that the VAT discounts are not an adequate solution to the high prices

in the market. The rate of

those who think that reducing the VAT rate from 18% to 8% on some products

such as cleaning products, shampoo, toilet paper, baby diapers and sanitary

pads does not reflect on the prices in the market, is 81%. The rate of those

who think that this discount is reflected in the prices is only 8%. The rate

of those who think that the VAT reduction on both food products and other

products is not an adequate solution for the high prices of basic consumer goods

is very high.

Sidar Gedik,

CEO of Ipsos Turkey, made the following evaluations about the data; For about a

year, the economy stood out as the most important problem of our country.

With the weakening of the effect of the epidemic in recent months, the

economy has come to a position where all other problems are suppressed. As a

result of inflation that continues to rise, six out of ten people state that

their household's purchasing power has decreased in the past year. Naturally,

when we ask what is the biggest problem of our country, almost no other

problem comes to mind. In order to

cope with price increases, the government, producers and consumers are taking

various measures on their part. Among the measures taken by the government,

there are also VAT reductions. However, eight out of ten citizens do not

think that these discounts are reflected in the labels. And nine out of ten

believe that VAT reductions will not be enough to combat high prices. In

other words, some of us say that even if the discounts are reflected on the

label, it will not be enough. In the last

2 years, we have been really tired in the fight against the epidemic and the

economy. Six out of ten people feel tired, we've never felt so tired. I hope

the spring months will bring not only psychological relief, but also some

economic relief with the reduction of heating costs. (Ipsos

Turkey) 11 April

2022 Source: https://www.ipsos.com/tr-tr/toplum-kendini-daha-yorgun-ve-bikkin-hissediyor 738-739-43-03/Polls Eco-Labels In Singapore, How Aware Are

Consumers Of These Green Certification Marks

Environmental

labelling certifications and eco-labels have

made it simpler for consumers today to identify products that are

manufactured and/or can be used with lower environmental impact. But how

aware are consumers in Singapore of these green marks? Ahead of Earth Day on

April 22, latest research from YouGov throws a spotlight on this. Eco-label awareness in Singapore: Common green marks

YouGov

polled consumers on their familiarity with five eco-labels used in Singapore.

They included the:

Eco-label awareness in Singapore: General population Latest data

from YouGov

RealTime Omnibus,

as of April 2022, reveals that more than nine in ten consumers in Singapore

are aware of the NEA Energy

Label (95%) and PUB

Water Efficiency Label (96%), of which more than one-third

are “very familiar” and more than half are “quite” or “slightly familiar”

with each label. More than

three-fifths are also aware of the Singapore

Green Label (63%), but less than one-third recall ever seeing

the EPEAT Label (29%)

and UL GREENGUARD Label (22%). Eco-label awareness in Singapore: Across age groups The youngest

consumers aged 18-24 years are much more likely than other age groups to be

very familiar with the NEA Energy

Label (55%) and PUB

Water Efficiency Label (47%), while consumers aged 25-34

years were most likely to be very familiar with the EPEAT (9%) and UL GREENGUARD Labels (8%). However,

with the Singapore Green Label,

while consumers aged 25-44 years were most likely to be familiar (11%),

consumers aged 18-24 years were least likely to be familiar (3%). Consumers

aged 55+ years are more likely than other age groups to be completely

unfamiliar with the NEA Energy Label (9%), EPEAT Label (80%) and UL GREENGUARD Label (85%). The Singapore Green Label had the widest

variance in unaware consumers when segmented by age, from just over a quarter

of consumers aged 35-44 years (27%) to more than half of consumers aged 18-24

years (53%). (YouGov

Singapore) Source: https://sg.yougov.com/en-sg/news/2022/04/19/ecolabels-singapore-consumer-awareness/ 738-739-43-04/Polls Six In Ten People In S'pore Prefer

Sustainable Brands, With Those Aged 18 - 24 Most Likely To Say So

Sustainability

has become a global buzzword, especially as consumers are increasingly

cognisant of the impact that the brands they support have on the environment.

Latest data from audience segmentation tool YouGov

Profiles reveals that as many as six in ten

people in Singapore say they prefer brands that are sustainable (58%),

reiterating that environmentally conscious behaviour from brands weighs

heavily on the mind of the consumer. Furthermore, those aged 18-24 are

significantly more likely to be sustainable shoppers, with two-thirds of

those in this demographic preferring sustainable brands (66%).

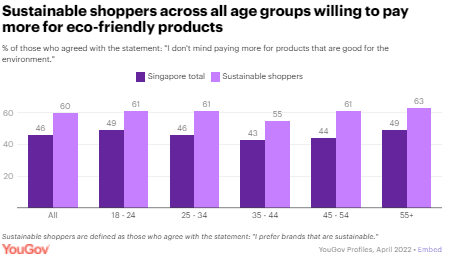

The data

also indicates that sustainable shoppers (defined as those who agree with the

statement, “I prefer brands that are sustainable”) could be less price

sensitive in their purchases. On the whole, while one in five Singapore

residents say they would shop specific brands without looking at the price

(22%), this increases to one in four among sustainable shoppers (26%). Looking

specifically at price sensitivity toward products that are good for the

environment, where less than half of the general population would be willing

to pay more for eco-friendly products (46%), this increases to six in ten

among sustainable shoppers (60%). Such behaviour is consistent across age

demographics and highest in sustainable shoppers above the age of 55 (63%),

indicating that paying a premium for environmentally friendly products is not

a concern for the sustainable shopper.

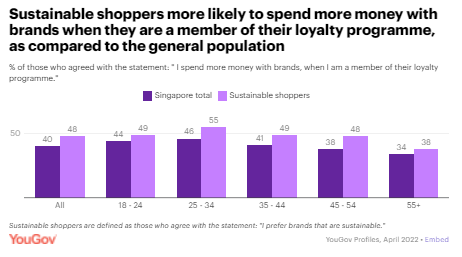

Another

factor that contributes to spending among sustainable shoppers is that of

loyalty programmes. Shoppers who prefer sustainable brands are significantly

more likely to spend more with brands when they are a member of their loyalty

programme (48%), as compared to the general population (40%). A notable

half of sustainable shoppers aged 25-34 say they spend more when they are

members of loyalty programmes (55%), accounting for the greatest proportion

of sustainable shoppers who say so. While that

is the case, the biggest behavioural disparity between sustainable shoppers

and the general population is among those aged 45-54, with just under half of

sustainable shoppers saying they tend to spend more when members of a brand’s

loyalty programme, as compared to four in ten of the general population

(38%).

(YouGov

Singapore) April 20,

2022 Source: https://sg.yougov.com/en-sg/news/2022/04/20/six-ten-people-spore-prefer-sustainable-brands-tho/ MENA

738-739-43-05/Polls Iraq Pulse: Unrest Amid The Covid-19

Pandemic

Nearly 19

years have passed since the removal of Saddam Hussein from power and the

establishment of the second republic of Iraq. While the structures of the

State and the political system have been deeply and extensively reshaped, the

impact of this transformation on the life of Iraqis remains debated. The

latest Arab Barometer’s (AB) survey (Wave VI which was– conducted between

March and April of 2021) attempts to contribute to this debate. The findings

of this survey display public discontent over political life, dissatisfaction

with education and health systems and economic performances, and concerns about

civil liberties. In October

2019, the cabinet of then-Prime Minister Adel Abdul al-Mahdi faced a major

wave of popular protests in Baghdad which rapidly spread to other Iraqi urban

centers. Demands revolved around socio-economic reforms and the end of the

corrupt and sectarian political system. The brutality of the response brought

by the police and militias changed the protesters’ attitude to demanding

political reforms and a new social contract for the Iraqi state. Al-Mahdi

submitted his resignation on the 1st of December 2019 and in

May 2020, the Council of Representatives (CoR) asked former intelligence

chief, Mustafa al-Kadhimi, to form a provisional government. Al-Kadhimi was

able, to some extent, to intensify the fight against corruption and meet some

of the popular demands. He strengthened the anti-corruption policies and

established a special committee to investigate allegations of corruption and

unusual crimes, with the help of the Commission of Integrity. Genuine

improvements as a result of these measures may not be obvious right

away. The public

views corruption as one of the main challenges that hinder progress in the

country. Nearly a quarter (23%) of Iraqis say that corruption is the most

important challenge facing their country; the highest of all countries

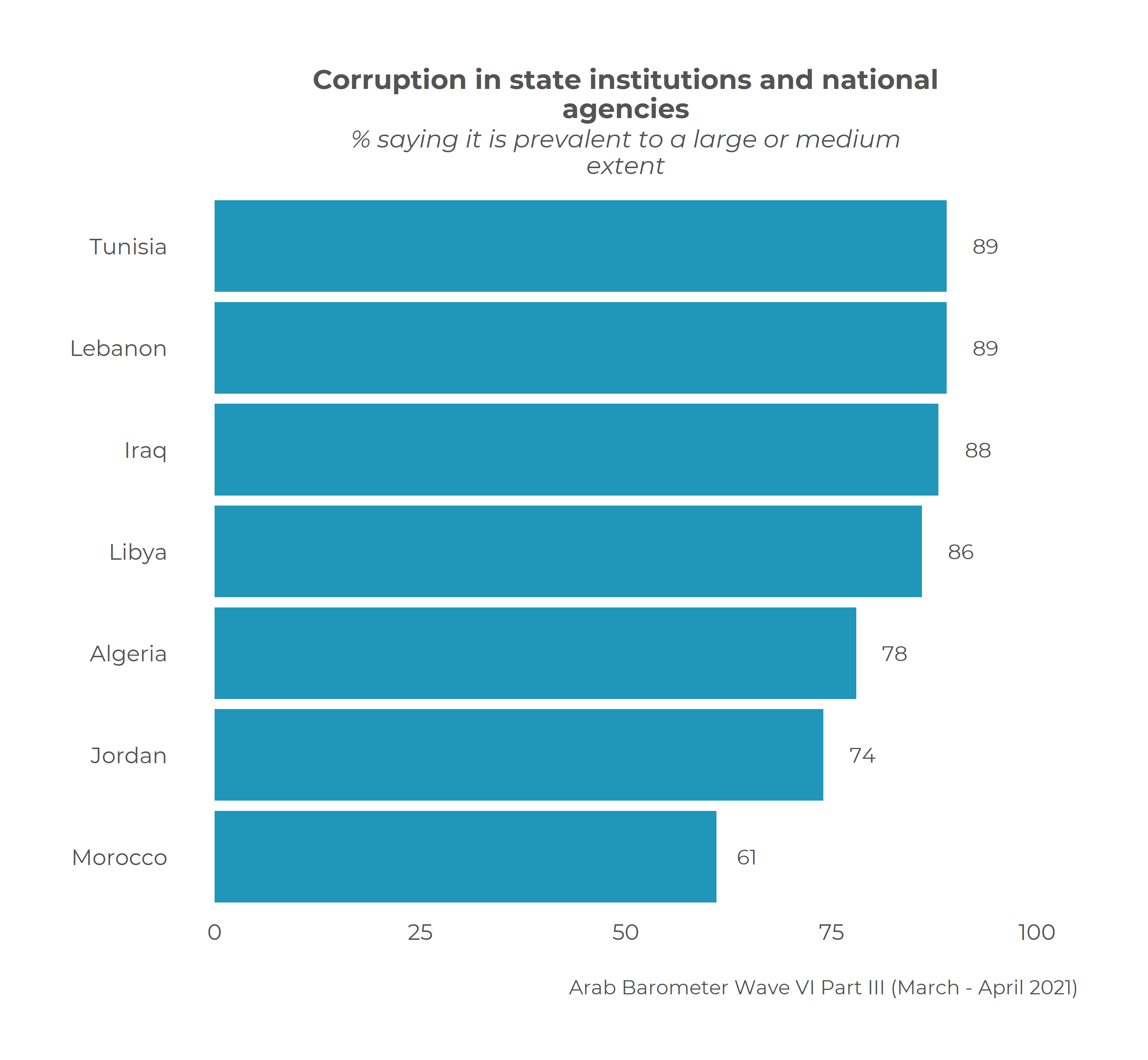

included in the AB spring 2021 survey. The widespread corruption is a source

of agreement in the country, with 88% of Iraqis saying it is prevalent to a

large of medium extent in state institutions and national agencies. The

country had general elections in October 2021, but no government has been

formed yet, causing a major political vacuum.

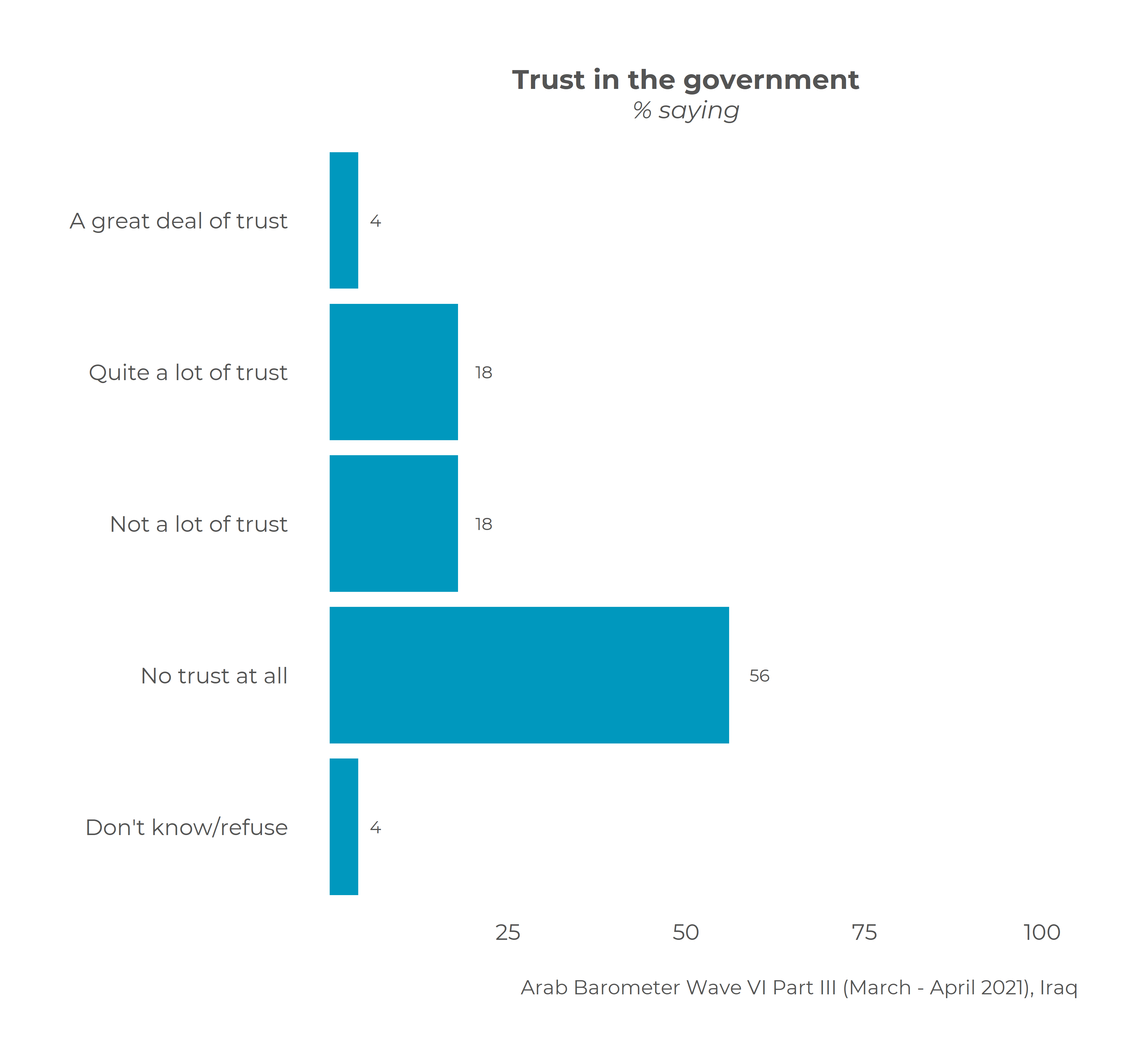

Trust in

state institutions is low. When AB conducted the sixth wave survey in Iraq

(March 2021), al-Kadhimi’s provisional government was already facing multiple

challenges, including the Covid-19 pandemic, the need to address the demands

of protesters, and the preparation for legislative elections. Around a fifth

of Iraqis (22%) express their trust in the government, while more than half

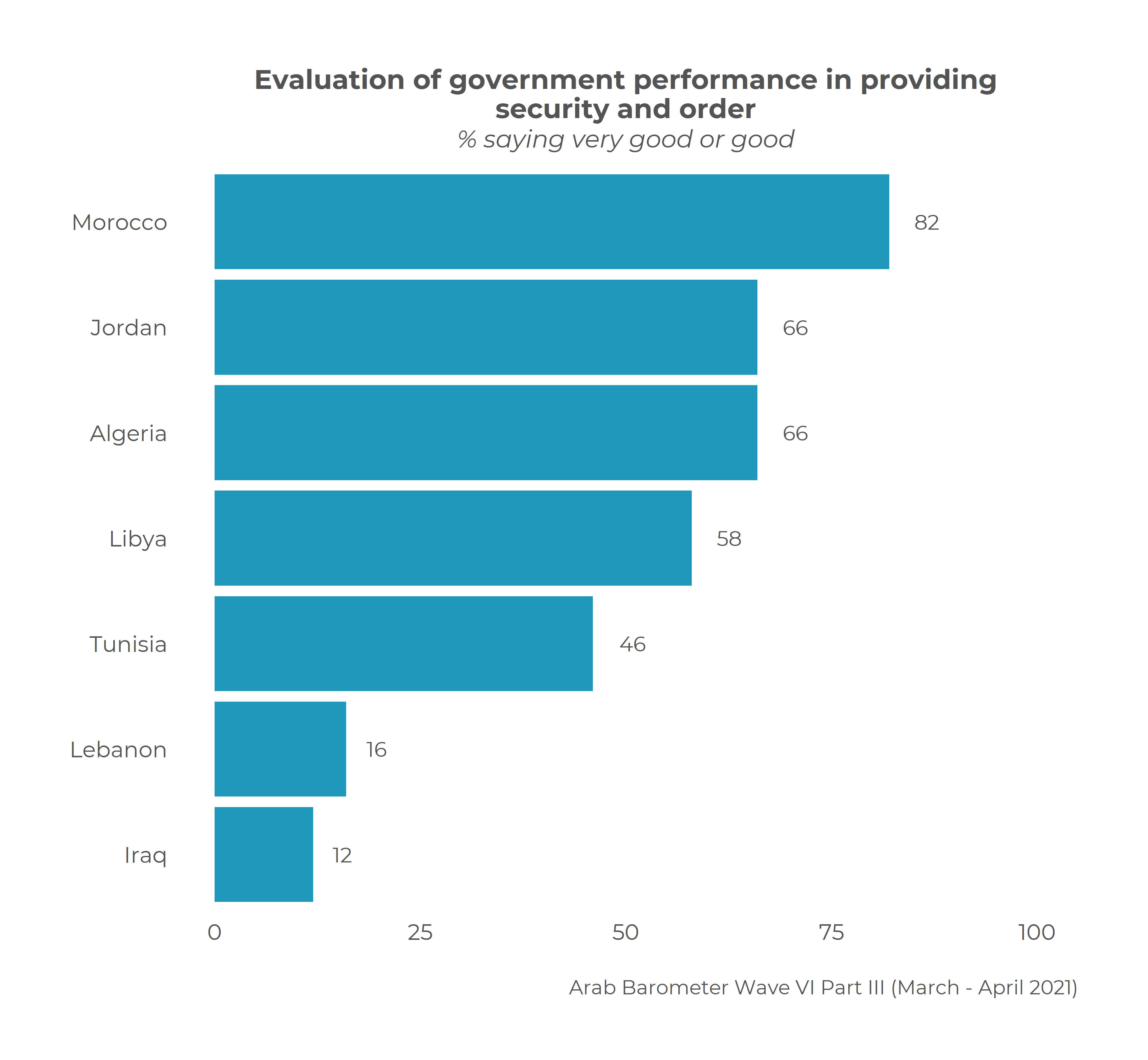

of the population (56%) say they have no trust at all in it. As for

performance, the Iraqi government ranked among the lowest in the AB survey

for providing security and order (12% – lowest), controlling inflation (3% –

second lowest), and combating COVID-19 (6% – lowest)

Trust in the

legal system is also low. The Federal Supreme Court (FSC) – which is the

highest judicial body in Iraq and notably tasked to interpret and enforce the

constitution – has never been approved by CoR. The establishment of the

Court, required in Article 92-2 of the 2005 constitution, must be vetted by a

two-thirds resolution by CoR. However, the Court was formed by the

provisional government of Ayad Allawi (2004-2005). Therefore, there is an

argument that the FSC was not established in accordance with the rule of law

and its decisions are often a source of contestation, especially between the

Kurdistan Regional Government (KRG) and the Federal Government (FG). KRG

views the Court as unconstitutional and is reluctant to implement its verdicts.

KRG-FG relations are based on closed-door consensuses instead. For instance,

in February 2022, FSC declared that a 2007 oil and gas law of Iraq’s

Kurdistan Region (KRI) is unconstitutional. The decision sparked a political

dispute between the FG and KRG with the latter declaring that FSC is

unconstitutional. Finally, there are constant criticisms of the Court’s

political neutrality, especially when it comes to ruling on questions that

involve high political profiles. The Central

Criminal Court has not been able to resolve major corruption and fraud cases.

It has violated basic fair trial criteria of Islamic State-related cases. In

January 2020, the UN Assistance Mission for Iraq (UNAMI) concluded that the

Court’s hearings are “ineffective legal representation,” and lack “adequate

time and facilities to prepare a case”. As for trust

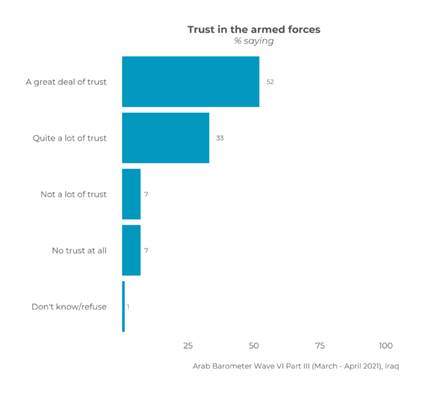

in the armed forces, the Iraqi army was able to regain some of the trust it

lost after its humiliating defeat at the hands of the Islamic State in Iraq

and Syria (ISIS) in Mosul in the summer of 2014. The army includes popular

figures who fought heroically against IS – such as the commander of the Iraqi

Counter-Terrorism Service (ICTS), Lieutenant General Abdel-Wahab

as-Saa’di. According to the AB survey, 85% of Iraqis say they have a great

deal of trust or quite a lot of trust in their armed forces. However, the

army faces the challenge to integrate the Popular Mobilisation Forces (PMF)

militia. The official consolidation of the PMF under the formal security

system from December 2017 has politicised the army. This perception was

evident in fall 2019 when former Prime Minister al-Mahdi, arguably pressured

by the PMF, stripped off Lieutenant General Abdel-Wahab as-Saa’di of his

power as the commander of the ICTS and assigned him to an administrative

position at the Ministry of Defence. As-Saa’di saw the move as a humiliation

to his military rank and feat of arms, and reportedly stated that he would

rather go to jail than accept the decision. Mahdi’s decision was allegedly

the trigger that sparked the protests of October 2019. In May 2020,

Prime Minister Mustafa al-Kadhimi reappointed as-Saa’di as the commander of

the ICTS, but the growing influence of the PMF inside the army might

eventually decrease the public trust of the army.

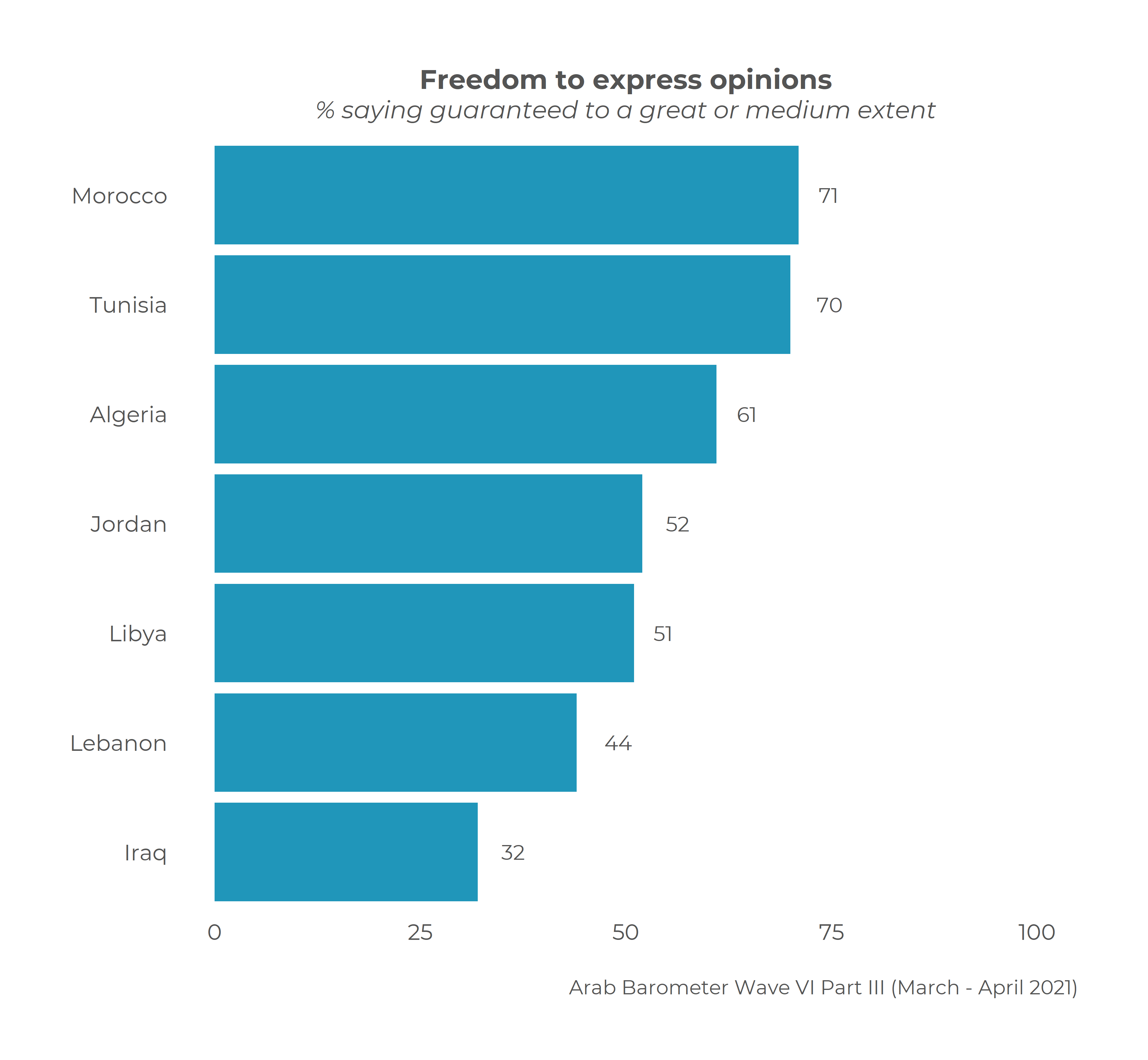

Civil

liberties in Iraq are routinely abused. For instance, suspected IS members

are denied fair trials, and there is evidence of torture in Iraqi jails. The

policing measures against the October 2019 protests caused about 500 deaths

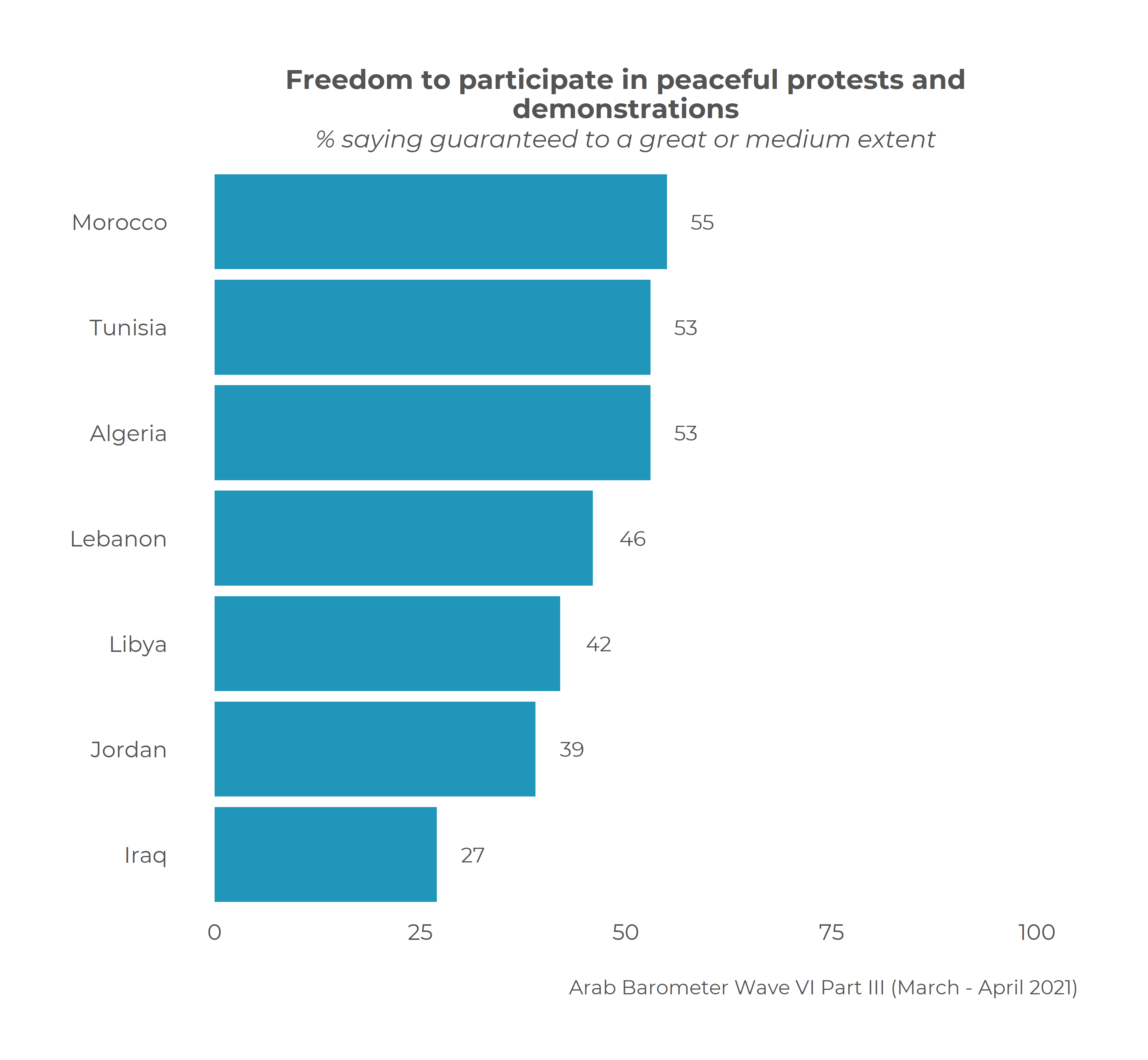

and over 7,000 injuries. This infringement perhaps explains why as few as 27%

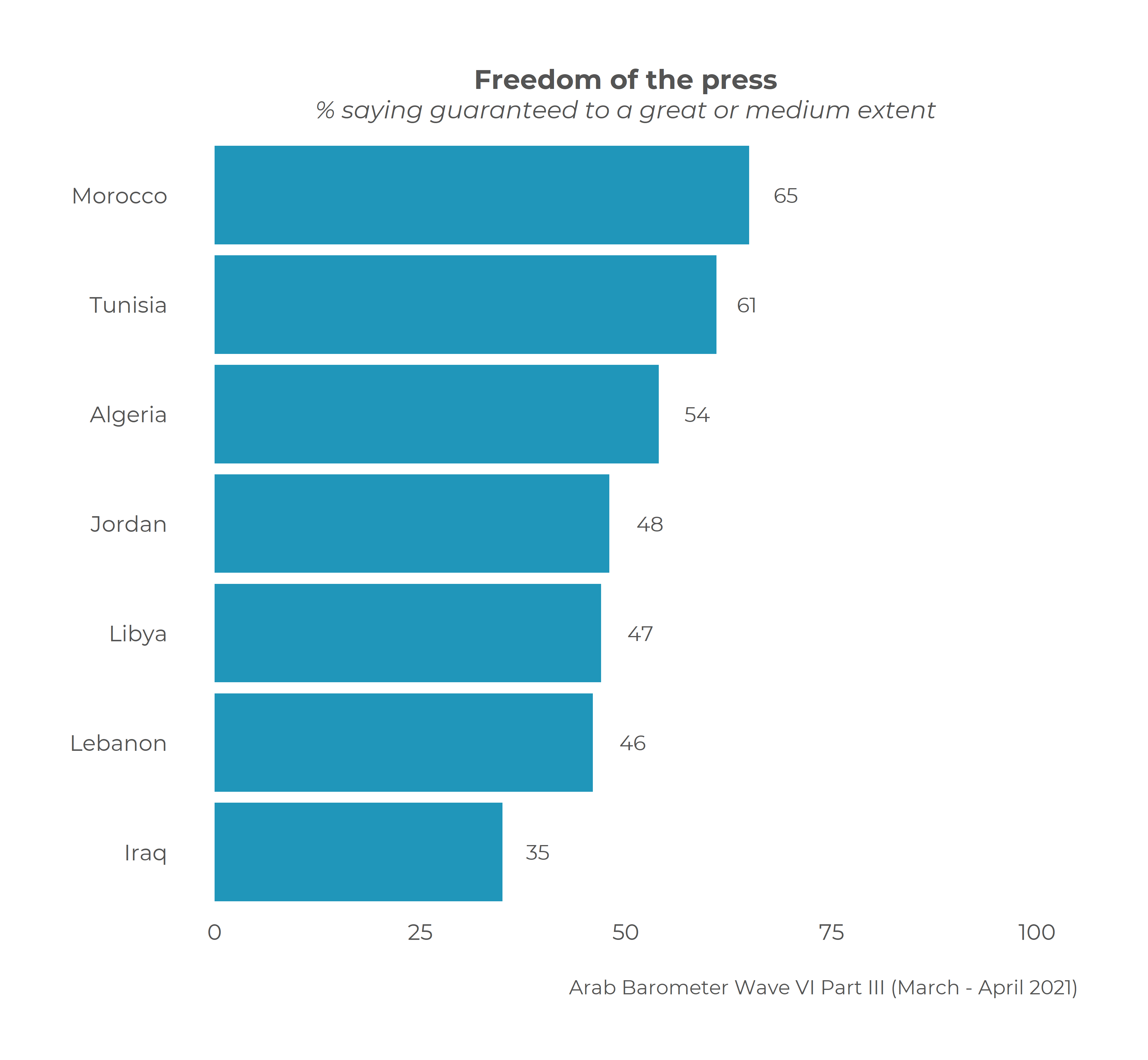

of people say that the freedom to participate in peaceful protests is

guaranteed, the lowest percentage among the countries included in the AB

survey. In addition, the authorities have jailed 3,000 demonstrators.

Militias are frequently harassing LGBTQ+ people. Only a third of Iraqis say

that freedom of expression (32%) and freedom of the press (35%) are

guaranteed, which are the lowest among all countries included in the survey.

Women’s

rights are regularly violated. For instance, domestic violence cases

increased in numbers during the Covid-19 pandemic (UN women 2020). In

addition, women experience discrimination in the labor market. On the one

hand, they lack means of transportation to access the job market. On the

other, priority for employment is often given to men, while women are

expected to take care of the household. This issue is especially challenging

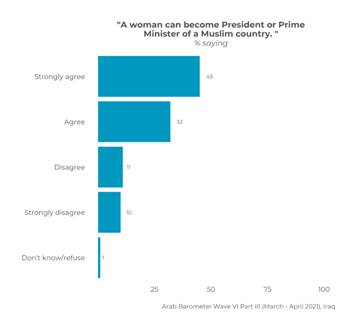

in rural areas. That said, most Iraqis (77%) do not object to women becoming

presidents or prime ministers of the country. Moreover, the majority agree

that university education is crucial across gender.

Iraq’s

economy remains heavily dependent on oil. The drop in oil prices in 2020

caused a decrease in Iraq’s GDP. While Iraq embraces the market economy,

political instability, corruption, and the Iraqi investment law have hindered

the establishment of the private sector. Hence, public dissatisfaction over

the economic performance of the FG is high, especially given that

al-Kadhimi’s government is not able to control corruption and smuggling

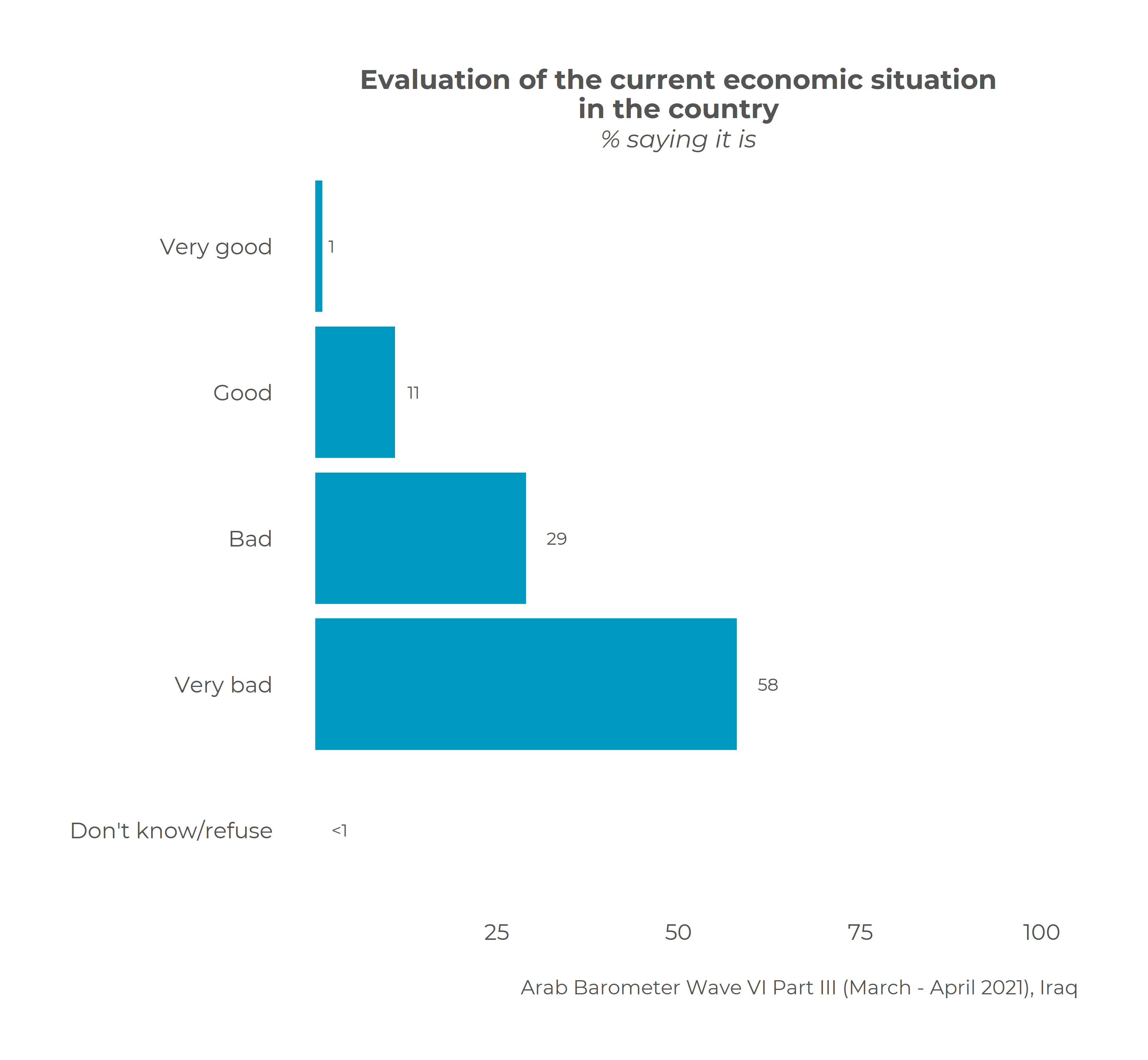

activities across the borders with Iran and Syria. Only 12% of Iraqis

evaluate the current economic situation as very good or good With the

decline of oil prices, poverty rose further during the Covid-19 pandemic,

especially among internally displaced persons (IDPs). In addition,

international reports show that more than 4 million individuals in Iraq are

in need of humanitarian assistance. Moreover, unemployment rates have

increased from 8% in 2012 to nearly 14% in 2020. When asked about the most

important issue the government should be focusing on to improve economic

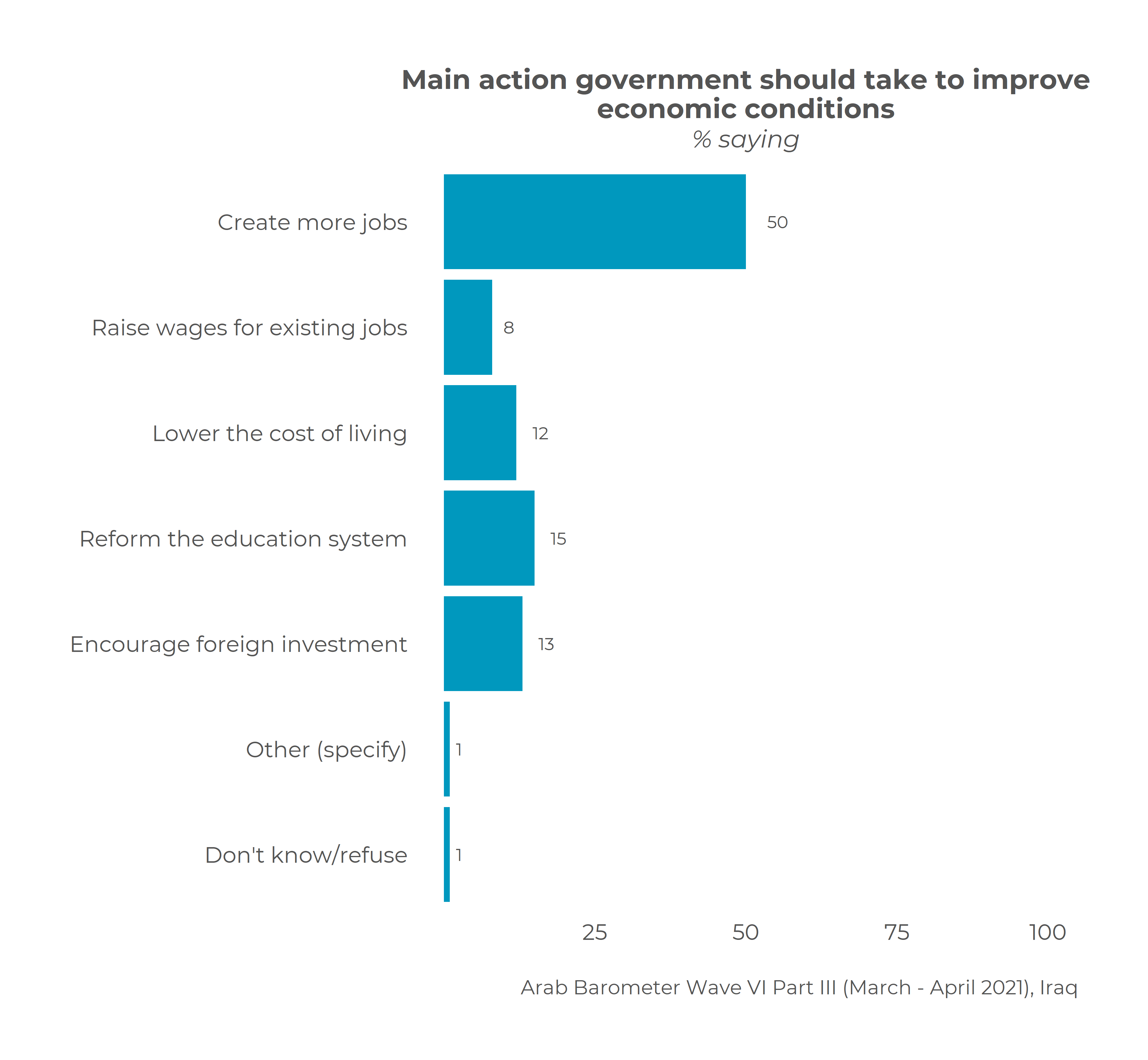

conditions, Iraqis often point to the need to create more job opportunities

(50%).

The country

confirmed its first case of Covid-19 in March 2020. According to the World

Health Organization (WHO), Iraq had 2,313,370 confirmed cases of COVID-19 and

25,105 deaths between 3 January 2020 and 15 March 2022. A total of 17,014,009

vaccination doses has been delivered as of March 2022. Like

anywhere else, the pandemic had a major impact in the poor and rural areas.

Public’s dissatisfaction with the FG reached new heights because of the

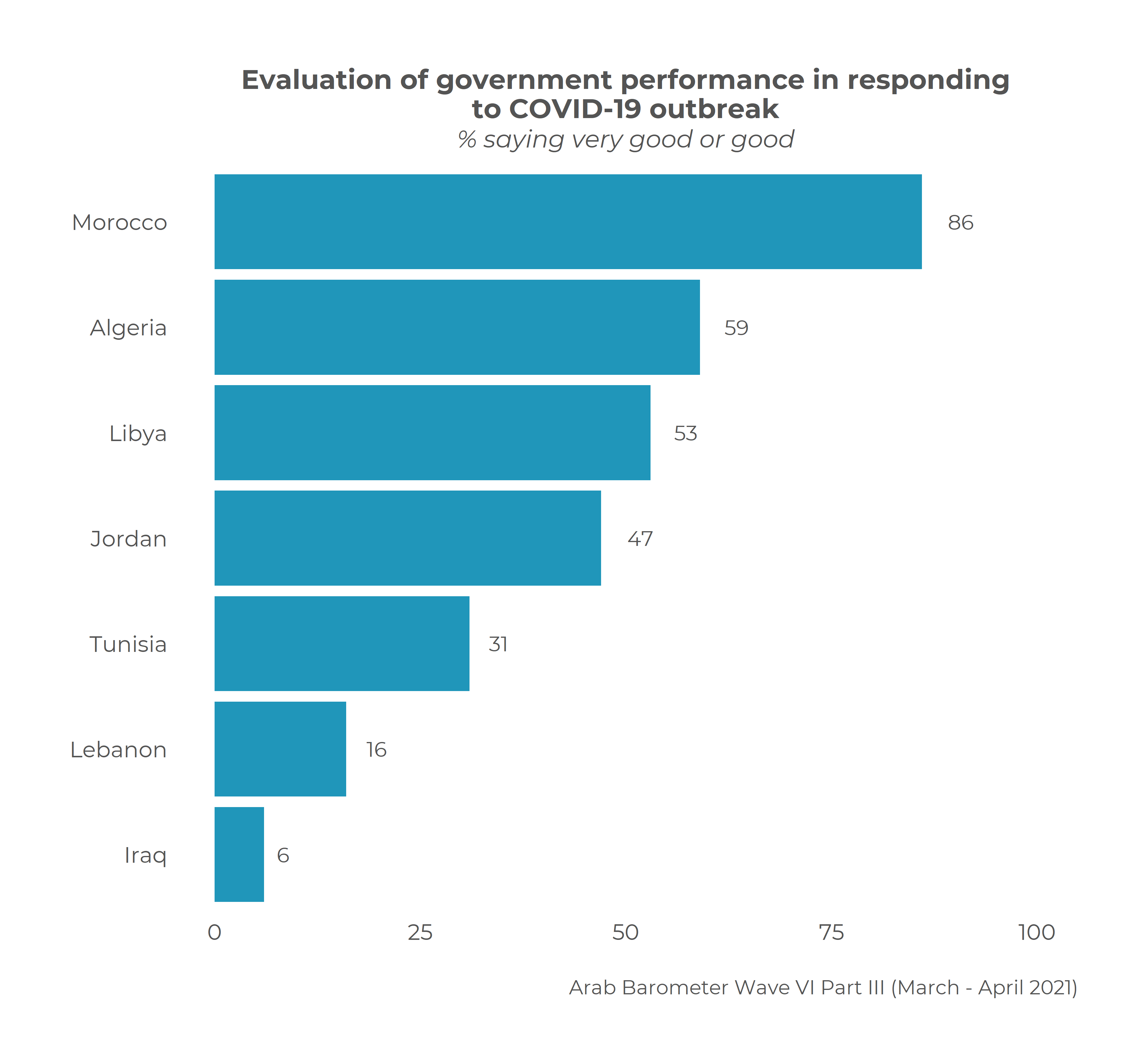

mishandling of the Covid-19 outbreak. As mentioned above, only 6% of Iraqis

say the government is doing a very good or a good job in responding to the

COVID-19 outbreak. While it was able to impose a broad lockdown, the

government could not provide resources to track, test, and treat Covid-19

cases. Moreover, hospitals were swamped, with limited medical oxygen supplies

and prices of hygiene products and masks soaring. The government was unable

to secure alternative sources of income for those who lost their businesses

or jobs due to confinement measures, nor was it able to secure relief aid to

the public in general. The pandemic

weakened KRG’s Syrian refugee policy. And due to unresolved budget concerns

with the FG and the economic constraints created by the pandemic, the KRG

reduced the pay of many civil servants by around 20%, which caused unrest and

protests in 2020. (Arabbarometer) April 19,

2022 Source: https://www.arabbarometer.org/2022/04/11258/ AFRICA

738-739-43-06/Polls Majority Of Namibians Say The Country Is A Safe Place To Live, But Levels

Of Fear Are On The Rise

Three out of four Namibians consider their

country a safe place to live, a recent Afrobarometer survey indicates. The same proportion of citizens say safety

and security have improved in Namibia over the past five years – even as increasing

numbers report fear of crime. More than half of Namibians say they

experienced fear of crime in their homes and felt unsafe walking in their neighbourhoods

during the past year. Citizens facing a security threat are most

likely to seek assistance first from the police, according to the survey. About one in four

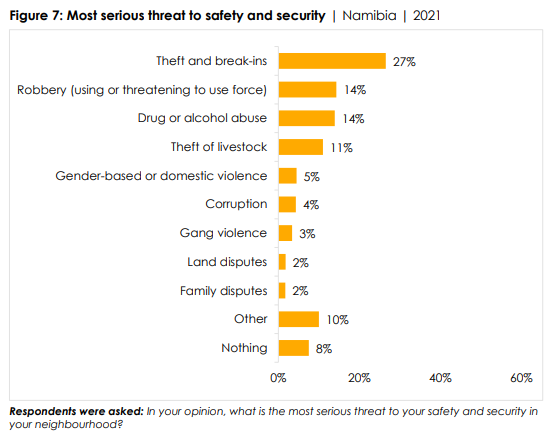

say they go to other family members first. Theft and break-ins rank as the most

serious threat to safety and security in the eyes of Namibians, followed by robberies and drugs

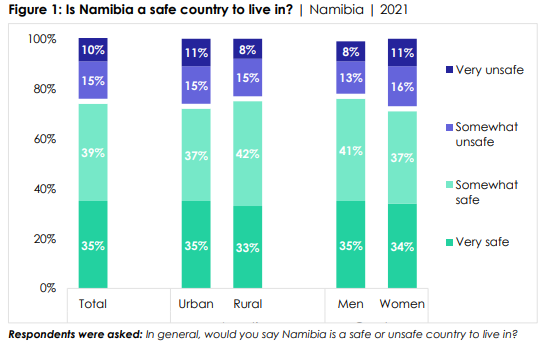

and alcohol. Key findings ▪ Three-fourths (74%) of respondents

say Namibia is a "somewhat safe" (39%) or “very safe” (35%) country to live in (Figure 1).

o Urban and rural residents differ little

in the degree of safety they feel. o Women are somewhat more likely than men

to view Namibia as unsafe, 27% vs. 21%. ▪ The same proportion (74%) say

Namibia has become "much more safe" (38%) or "somewhat more safe" (36%) over

the past five years (Figure 2).

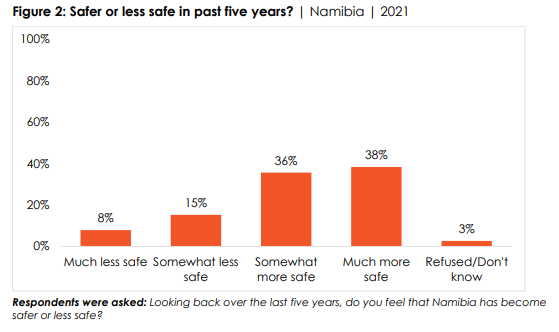

▪ At the same time, more than half

(52%) of Namibians say they experienced fear of crime in their own homes “just once or

twice,” “several times,” “many times,” or “always” during the past year, the

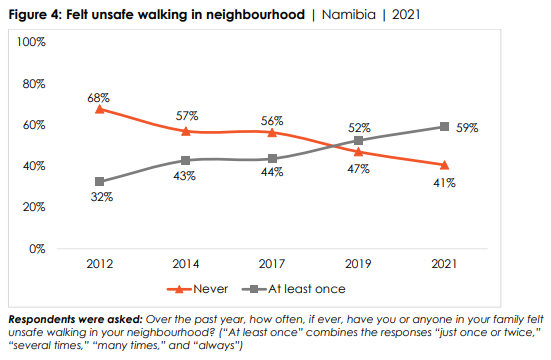

highest number recorded over the past two decades (Figure 3).

▪ Nearly six out of 10 respondents

(59%) say they felt unsafe walking in their neighbourhoods at least once during the

past year, the highest number since 2012 (Figure 4).

▪ When faced with a security concern,

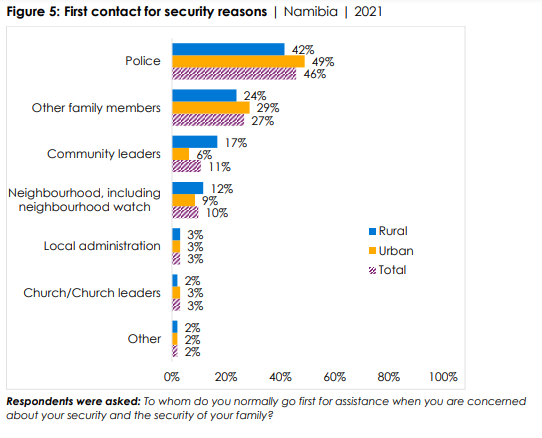

almost half (46%) of citizens say they turn first to the police. About one-fourth (27%) seek assistance

first from family members, while only one in 10 (11%) go to community

leaders first (Figure 5).

o Rural residents are more likely than

their urban counterparts to reach out to a community leader for assistance (17% vs.

6%). o Older citizens also turn more frequently

to community leaders (17%) than do younger persons (8%-13%) (Figure 6).

▪ Theft and break-ins rank as the

biggest perceived threat to safety and security in communities, cited by 27%

of Namibians, followed by robberies (14%), drugs/alcohol (14%), and livestock

theft (11%) (Figure 7).

(Afrobarometer) 11 April 2022 738-739-43-07/Polls Three In Four Malawians (74%) Believe “A Lot” In The Existence Of

Witchcraft

Most Malawians strongly believe that

witchcraft exists and support changing the law to criminalise its practice, a new Afrobarometer

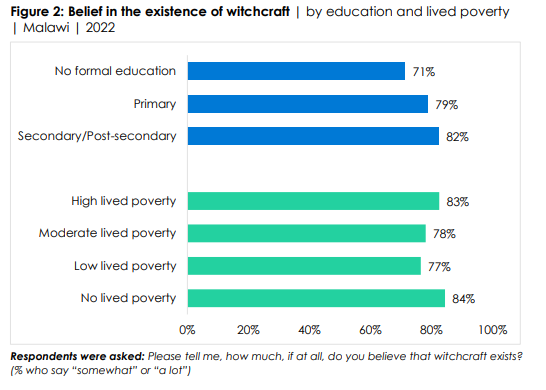

survey shows. Educated citizens are more likely to

believe in the existence of witchcraft than those with no formal education. Most Malawians associate

witchcraft with using magic to kill people, make them sick, or bring them misfortune. The survey shows that the elderly,

especially elderly women, are at greatest risk of being victims of witchcraft accusations. A majority of Malawians favour changing the

law to criminalise witchcraft, providing support for the findings and recommendations of the

Special Law Commission on the Review of the Witchcraft Act in Malawi. These findings also suggest a need for

raising public awareness and instituting measures to protect segments of the population at risk

of being accused of witchcraft. Key findings ▪ Three in four Malawians (74%)

believe “a lot” in the existence of witchcraft. Only 14% say it doesn’t exist (Figure 1).

▪ Educated citizens (82%) are more

likely to believe in the existence of witchcraft than those with no formal education (71%)

(Figure 2).

▪ More than six in 10 Malawians (63%)

say that in their communities, elderly people are most often associated with witchcraft

(Figure 3).

▪ Almost three-fourths (72%) of

Malawians say witchcraft should be criminalised (Figure 4).

(Afrobarometer) 14 April 2022 738-739-43-08/Polls Only One In Five Angolans (21%) Say They Trust The National Electoral

Commission (CNE) Somewhat Or A Lot

As Angolans approach general elections in

August, only one in five citizens say they trust the National Electoral Commission, a new

Afrobarometer survey shows. While about half of Angolans say the

commission does its job in a neutral fashion, trust in the election management body has declined from

already low levels recorded three years ago. Angola will conduct its fourth peacetime

general election in August. The first three elections, which the Movimento Popular de Libertação

de Angola (MPLA) won by significant majorities, were marred by suspicions of electoral

fraud involving the National Electoral Commission. Key findings Only one in five Angolans (21%)

say they trust the National Electoral Commission (CNE) “somewhat” or “a lot,” a

6-percentage-point decline compared to 2019 (Figure 1).

o Levels of trust are higher among men (25%

vs. 17% of women) and among older respondents (34% of those aged 46 and over

vs. 17%-19% of 18- to 35-year-olds) (Figure 2).

urban areas (18%), as do citizens with

primary or no formal education (26%-27%) compared to those with secondary or

post-secondary qualifications (17%-19%). Only 14% of residents in the Luanda

Province say they trust the commission. About half (48%) of Angolans say

the electoral commission exercises its function in a neutral manner, while close to one-third

(32%) think it favours particular groups (Figure 3). o The perception of the electoral

commission as a neutral body increases with respondents’ education level, ranging from

just 37% of those with no formal schooling to 56% of those with

post-secondary qualifications (Figure 4).

(Afrobarometer) 22 April 2022 WEST

EUROPE

738-739-43-09/Polls Seven In Ten (72%) Of Britons Would Support The Construction Of A

Wind Farm In Their Local Area

Amidst a backdrop of soaring fuel costs,

and questions about whether we should be sourcing power from countries

like Russia the government has published a new

energy strategy for the UK. The plans could see eight new nuclear power plants built at existing

sites across the UK. This represents a stark change from recent years when

plans for several plans fell through, including

a plant on Anglesey and one near Sellafield. Onshore wind is also a feature of the new energy strategy and

reportedly played a role in delaying the policy paper.

Given historic complaints that onshore wind farms aren't particularly

appealing to the eye, the government will be looking for "supportive

communities" to host new schemes. A new YouGov survey finds, however, that Britons are perhaps more

open to onshore wind than anticipated. Seven in ten (72%) of Britons would

support the construction of a wind farm in their local area – including 33%

who would "strongly" back one. Only 17% would oppose a new wind

farm in their area.

This compares to just 34% who would support a nuclear power plant in

their area. Half (50%) would oppose the creation of a new nuclear site near

them, with some 28% strongly opposed to the suggestion. Britons would back local new nuclear in

return for cheaper energy bills Aversion to nuclear power is certainly not a new phenomenon. Indeed,

the war in Ukraine may have raised old fears as both sides fought for control

of the former

plant at Chernobyl. However, Britons are willing to accept new nuclear in their area

under certain conditions. The government's energy

strategy suggests that communities willing to host onshore wind

farms would do so for a guaranteed reduction in their energy bills. When offered the same incentive of lower bills for a local nuclear

power plant, support almost doubles to two-thirds (67%). Only 21% would

oppose a nuclear plant under these circumstances. A further 61% would support

the creation of new nuclear in their area if it meant the UK was less

dependent on Russian energy sources, and 58% would if it led to more progress

on the UK's ‘net zero’ goal.

While most Britons generally support the construction of a wind farm

close to them, support further increases if it meant lower energy bills

(83%), less dependence on external energy (81%), and progress towards

net-zero (77%). (YouGov UK) April 11, 2022 738-739-43-10/Polls More Than One In Two Britons Support Ban On Whipping Racehorses

New research from Ipsos UK, released ahead of this weekend’s Grand

National, reveals that more than one in two Britons aged 16-75 (55%) want

jockeys banned from using the whip whilst three in ten (31%) believe horse

racing is unacceptable. Men (54%) and women (55%) are united in supporting a ban on the whip.

However, there is a gender divide about whether horse racing as a sport is

acceptable or not - 38% of women believe horse racing is unacceptable

compared with 24% of men. There is also a generational split – while 55–75-year-olds are among

the most likely to believe the sport is acceptable (41%), they are also among

the most likely to support a ban on the whip (61%). Overall, around as many people say they are interested in following

horseracing as say they are not interested but have objections to it (both

22%) – the majority say they are either not interested but have no objections

to it (23%) or have no views on horseracing at all (31%). Whipping horses has long been controversial and the British Horse

Racing Authority is reviewing the current rules, which allow eight strokes of

the whip with hands off the reins at any time during a jumps race, such as

the Grand National and seven on the Flat. Seven out of ten adults (71%) admitted not knowing very much about or

nothing at all about the current regulations surrounding the use of whips by

jockeys in the UK, but, after they had been explained , 20% supported use of

the whip under those conditions whilst 43% opposed it. Among those who

initially supported a ban on the whip, one in four (23%) believed jockeys

should be allowed to use it once the regulations had been explained to them. Despite some people’s reservations about the sport, 39% say they

regularly or occasionally bet on some of the biggest events in the horse

racing calendar, The Grand National, the Cheltenham Festival and Royal Ascot,

and 41% might follow them on TV or radio. People in the North of England

(47%) are most likely to put money down and, overall, young people more

likely to bet, with half of under 35s enjoying at least an occasional wager,

compared to a third of 35–75-year-olds. Kelly Beaver, CEO of Ipsos UK, said: Horse racing is a historic part of British

society and culture and the Grand National is one of the most popular days in

the sporting calendar, but we are seeing concern for equine welfare, even

though only a minority have objections to the sport. (Ipsos MORI) 12 April 2022 Source: https://www.ipsos.com/en-uk/more-one-two-support-ban-whipping-racehorses 738-739-43-11/Polls Should Selective Breeding Of Dogs With Health Issues Be Banned

Norway made headlines earlier this year by effectively banning

the breeding of British bulldogs and Cavalier King Charles spaniels, –

stating the practice violates animal welfare laws. British bulldogs and King

Charles spaniels are brachycephalic dogs (meaning they have flat faces) and

can commonly suffer from severe breathing problems and health issues. The

Norwegian court chose to focus on the two specific brachycephalic breeds,

intending to set a strong legal precedent for discontinuing the breeding of

other flat-faced dogs. Britons would support banning the breeding

of dogs with health issues – but support is lower if you name the specific

dogs YouGov asked the British public whether they would support or oppose

a ban in the UK on the selective breeding of certain types of dogs. Half of

the respondents were asked whether they would support a ban on selective

breeding where it results in serious health issues, like breathing problems

or increased cancer risk, and the other half were asked whether they would

support a ban on selective breeding of brachycephalic (flat-faced) dogs, like

pugs and French bulldogs. Seven in 10 (71%) would support banning selective breeding where it

results in dogs with serious health issues, with just 20% opposed and 9%

unsure. However, support for banning selective breeding falls to 57% when the

public are asked if they would support banning the breeding of brachycephalic

dogs, like pugs and French bulldogs – with a quarter (25%) opposed and 18%

unsure. French bulldogs – which are prone to the

breathing problems common to flat-faced dogs – are the second most

common dog in the UK, with nearly 40,000

new dogs registered in 2020. Pugs are bred for their bulging eyes,

wrinkly skin and squished face, which has made them an internet favourite –

but also leaves the dogs with significant

health problems. While all age groups are generally in favour of a ban on breeding

flat-faced dogs, older Britons are more likely to support a ban on breeding

dogs like pugs and French bulldogs – 65% of those aged 65 and over would

support such a ban, with 24% opposed. On the other hand, 52% of 18 to 24-year-olds

would support such a ban, with 31% opposed. (YouGov UK) April 13, 2022 738-739-43-12/Polls Majority Of Britons Say Boris Johnson Should Resign, In Aftermath Of

‘Partygate’ Fines

New polling of the British public on Tuesday (12th) and Wednesday

(13th) this week in the aftermath of the Prime Minister being issued with a

Fixed Penalty Notice shows that Britons think Boris Johnson should resign by

a 2:1 margin. 54% would support the Prime Minister resigning and 27% would

oppose. Support for his resignation is unchanged from a similar poll taken

April 1st to 3rd, which asked what people thought he should do if he received

a fine. Meanwhile, there are some signs Conservative voters from 2019 are

rallying behind the Prime Minister. 48% now oppose his resignation compared

to 37% at the beginning of the month. Half, 51%, also think Chancellor Rishi Sunak should now resign

compared to 25% who oppose this. Conservative voters from 2019 are more split

on the Chancellor than the PM with 37% supporting his resignation and 40%

opposing it. How closely are the public following the

story?

Johnson / Sunak job approval

What impacts public perceptions of Johnson?

Keiran Pedley, Director of Politics at

Ipsos said: These numbers reflect a complex picture for

the Prime Minister. Whilst the public think he should resign over ‘partygate’

fines by a two to one margin, there are some signs that 2019 Conservative

voters are rallying around him, at least to an extent. Meanwhile, whilst

public interest in the ‘partygate’ affair has understandably grown given

recent events, the public still say they are following stories about the

rising cost of living and the Russian invasion of Ukraine more closely, with

both considered important factors in how he is judged politically. (Ipsos MORI) 14 April 2022 738-739-43-13/Polls By 37% To 19% Britons Would Prefer Emmanuel Macron Win The French

Presidential Election

The French public went to the polls over the weekend for the first

round of their presidential election. The results are a repeat of 2017, with

centrist Emmanuel Macron facing off against far-right Marine Le Pen in a

run-off vote next weekend. Here in Britain, Macron is the preferred candidate, by 37% to Le

Pen’s 19%. The largest portion of the public (44%), however, do not seem to

be au fait with French politics, answering “don’t know”. The results show that Conservative voters and Leave voters would

prefer to see Marine Le Pen emerge victorious. Those who backed the Tories in

2019 support Le Pen over Macron by 37% to 24%, while those who voted to leave

the EU in 2016 prefer her by 35% to 19%. Remain and Labour voters overwhelmingly back Macron, by 62% to 7% and

53% to 8%, respectively.

The latest

YouGov France voting intention figures currently suggest that the

French president holds an eight point lead over his rival. Fewer people think a Le Pen presidency

would be better for Britain than did in 2017 A quarter of Britons (24%) don’t think it really makes a difference

for the UK whichever candidate wins. The same number think a Macron

re-election would be better for Britain, while 13% think we would benefit

most from a Le Pen presidency. Four in ten (39%) aren’t sure either way. This represents an 8pt decrease for Le Pen compared to when

we asked the same question prior to the 2017 presidential election. Back

then, 21% said Marine Le Pen being elected would be better for Britain. About

the same number said a Macron presidency would be better for the UK back then

(23%) as do now, while fewer people thought it made little difference who won

in 2017 (13%).

The drop in the number of people thinking a Le Pen presidency would

benefit Britain more seems to be coming primarily from Leave voters, of whom

23% feel this way now compared to 37% in 2017. By contrast, the increase in the number of people who don’t think it

will make much difference either way comes from across the Brexit spectrum.

There has been an 11pt increase in the number of Remain voters who think it

makes little difference to Britain who wins (from 10% to 21%), and likewise a

13pt increase among Leave voters (from 17% to 30%). (YouGov UK) April 15, 2022 738-739-43-14/Polls 4 In 10 (39%) Britons Say Affordable Decent Housing Needs To Be

Improved Ahead Of The Local Elections On 5th May

Ahead of the local elections across parts of the country next month,

new research by Ipsos shows half of Britons say the conditions of roads and

pavements are most in need of improvement (50%) in their local area, while 4

in 10 (39%) say affordable decent housing needs to be enhanced.

The public’s priorities also include improvements in health services

(37%), wages and local cost of living (36%), shops and the local high

street/town centre (36%), and cleanliness of streets (34%) in their local

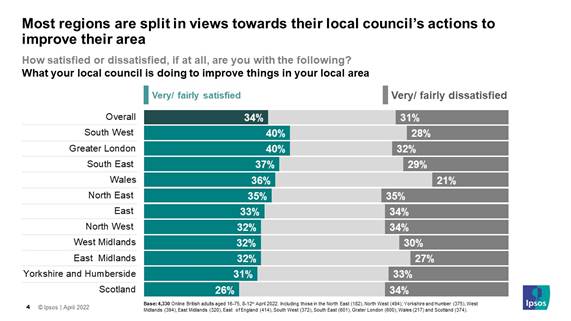

area. Public opinion is split when it comes to satisfaction with their

local council’s actions to improve their local area. Around a third (34%) are

satisfied while 31% are not. Those in the South West and London are slightly

more likely to be satisfied with this (both 40%) while those in Scotland are

least satisfied (26%).

Despite split opinion on their local council, most are satisfied with

their neighbourhood as a place to live (75%), and satisfaction is even lower

when it comes to the UK Government, only 24% are happy with what it is doing

to improve things in their area. Most regions are more likely to say their local council provides poor

than good value for money, overall, 39% say it is poor compared to only 26%

who say good value. The pattern is similar in most regions, with 4 in 10 or

more dissatisfied with the value provided by their local councils in

the East Midlands (45%), Yorkshire and Humberside (44%) and Scotland and the

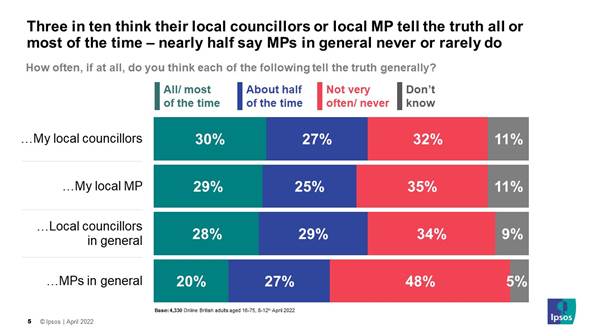

North East (both 43%). Local councillors are seen as more trustworthy than MPs in general,

however there is a gap between people’s own MP and MPs as a whole. Almost 6

in 10 (57%) trust their own local councillors to tell the truth

all/most/about half of the time while the same proportion say the same for

local councillors in general. Just over a third (35%) say they trust their

local MP not often/never while this increases to almost half when asked about

MPs in general (48%).

Gideon Skinner, Head of Political Research

at Ipsos, said: Nationally, much of the attention is being

paid to the cost of living crisis, Ukraine and ‘party-gate’, but when it

comes to the upcoming council elections more local factors will also have a

role to play. Although most people are pretty happy with where they

live they still want to see improvements, particularly on roads, housing,

high streets and the local cost of living – all of which are regular bugbears

for local residents. And these can all vary by where you live – for

example, crime is a particular issue in London, while in the rest of the South

East traffic congestion is a bigger priority. While the public look

more favourably towards local councils than central government when it comes