|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 729 Week:

February 07 –February 13, 2022 Presentation:

February 18, 2022 Youtube

Tops Yougov’s Best Buzz Rankings 2021 In India According

To 55% Of Turkish People Their Electricity Expenses Are Very Difficult For

Them Young

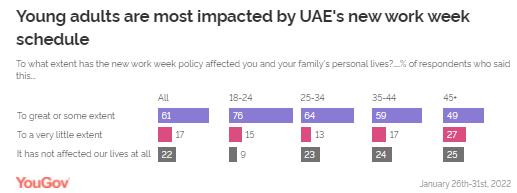

Adults Are Affected The Most By UAE's New Work Week Policy About

Four In 10 Moroccans Have Not Heard Of Climate Change Public

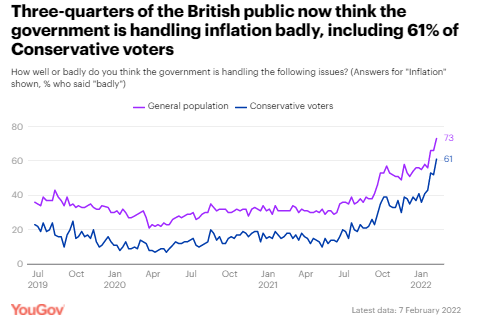

Criticism Of Conservatives’ Handling Of The Economy Continues To Grow Consumer

Confidence Slips As Britons’ Household Finance Concerns Increase 31%

Of Parents Declare That Their Children Have Been, At Least Once, Victim Of

Cyber Violence 1

In 10 French People Are Boycotting The Winter Olympics This Year New

Media Consumption Habits – But Which Ones Will Stick After The Pandemic Two-Thirds

Of Black Protestants (65%) Approve Of The Job That Biden Is Doing As

President Nearly

Half (46%) Of Canadians Say They “May Not Agree With Everything” Trucker

Convoy Says Or Does Conspiracy

Theories People Around The World Believe In 2021 Across 24 Countries INTRODUCTORY NOTE

729-43-21/Commentary:

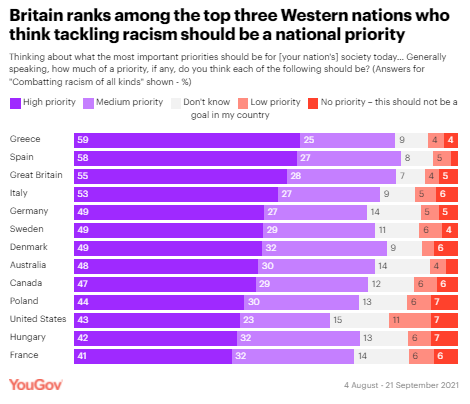

43%

Of Americans Think Tackling Racism Should Be A “High Priority” For The U S,

Survey Of 13 Western Countries

Nations

across the world face a vast array of issues and problems, from defence to

societal issues and climate change. All of which could be argued to be just

as pressing of an issue as the others, so with so much to juggle, what should

their focus be? Data from

the YouGov-Cambridge

Globalism Project shows how people living in major

western nations think their governments should prioritise certain goals. Should tackling racism be a priority for the West? The death of

George Floyd in May 2020 brought discussions of societal racism across the

Western world to the forefront once again, with major protests across the

United States, UK, and Europe. The YouGov-Cambridge

Globalism Project shows that large majorities in all

countries surveyed believed it should be a medium or high priority for their

nations. Britain is

among the top three of the nations surveyed who think combatting racism

should be a “high priority” (55%), and a further 28% think it should be a

“medium priority”. Only the Spanish (58%) and Greeks (59%) are more likely

than Brits to think fighting racism should be a high priority for their

nations. The United

States, on the other hand, is third from bottom among the countries included

in the survey. While some 43% of Americans think tackling racism should be a

“high priority” for the US, another 18% think it should be a low priority or

not a goal at all.

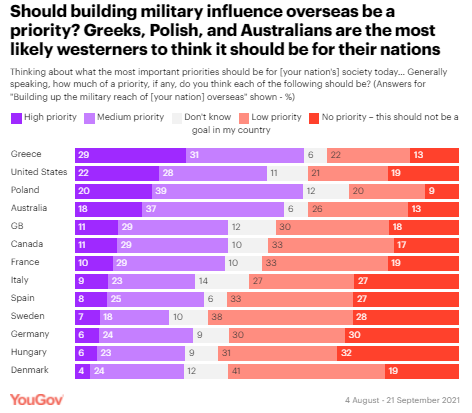

Should Western nations build up their military forces? With an

ever-growing Russian military presence on the borders of Eastern Europe, how

much of a priority do people in the West feel their military presence

overseas should be? The survey,

carried out last summer, found that those closer to the east are among the

keenest to see a build-up of their nation’s forces, including nearly one in

three Greeks (29%) and 20% of Poles who say that it should be a high priority

for their country. Despite

already having one of the biggest militaries, 22% of those in the United

States think increasing their military reach overseas should be a high

priority, and a further 28% think it should be a medium priority. However,

some 19% of Americans think it should not be a goal at all. Among

Britons, one in nine (11%) think building the reach of the British military

should be a high priority goal for the UK, compared to 18% who think it

should not be a goal at all. Hungarians (32%) and Germans (30%) are among the

most likely to think their countries should not focus on their military

influence overseas at all.

Should reducing immigration be a priority for the West? Immigration

has become a pressing issue across Europe in recent years, as people flee

from conflict and unrest in other parts of the globe. Repeated crossings of

the English Channel by migrants have become a particular point of contention

between the British and French – but is it a priority issue? There is a

general consensus across major western nations that it is – however some

nations are more divided than others. The Greeks (58%) and French (44%) are

the most likely to say reducing immigration should be a high priory target

for their nations – as do similar numbers of Swedes (43%), Hungarians (42%),

and Italians (42%). Around a

third of Britons (32%) think reducing immigration should be a high priority

for the UK, while 23% think it should be a medium priority. On the other

hand, 20% say it should be a low priority, and 17% say it should not be a

goal at all. Poles (24%)

and Canadians (23%) are the least likely to say their nations should make

cutting immigration numbers a high focus target.

Should the West prioritise the equality of women? Issues such

as the MeToo movement and the gender pay gap have revealed that the sexes are

not perhaps as equal as many like to think they are. Approaching two thirds

of Greeks think that pursuing and promoting women's equality should be a

“high priority” target for their country, while 62% of Spaniards think the

same and so do 55% of Italians. While most

people in each nation surveyed think promoting women's equality should be a

high or medium priority, Britain and the United States come bottom of the

list in terms of those who think it should be a high priority (both 37%). A

quarter of those in the United States (26%) think this should be either a low

priority or not one at all.

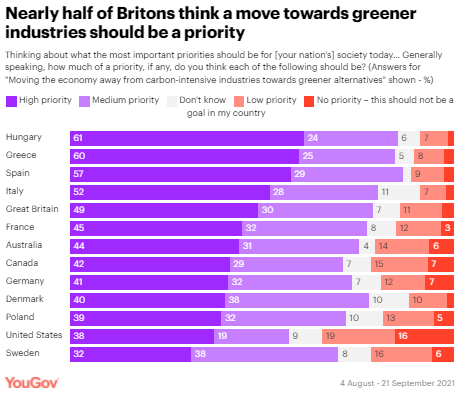

Should being carbon neutral be a priority for the West? In 2021, the

industrialised nations of the world came together for the COP-26 climate

change conference. While it might not have achieved all of its aims, the

build-up certainly helped increase awareness around the issue. Asked

shortly before the conference kicked off, the YouGov-Cambridge

Globalism Project found most people across the nations

surveyed to be in favour of moving their economy towards greener alternatives

and away from carbon-heavy industries – with Hungarians the most likely to

say this should be a high priority (61%). Sentiment is similar among Greeks

and Spaniards with 60% and 57% respectively thinking a green economy should

be a high priority goal for their nations. Among

Britons, 49% say moving towards an eco-friendlier economy should be a high

priority target for the UK, while a further 30% think it should be of medium

priority. Only 14% think it should be either a low priority goal or not one

at all. Across the pond, 38% of Americans think changing their economy away

from polluting industries should be a high priority target. Another 34% think

it should be a low priority target if one at all – the highest among the

nations asked.

(YouGov UK) February 08,

2022 ASIA (India) Youtube

Tops Yougov’s Best Buzz Rankings 2021 In India YouTube has dethroned its parent company

Google to become the top-ranked brand in YouGov’s Best Buzz Rankings 2021 in India (51.4). Google, which had

previously held the top spot (in 2018 & 2019) dropped down one place to

second (50.1) in the 2021 rankings. YouGov’s BrandIndex measures the public’s

perception of brands on a daily basis across a range of metrics. The annual

Buzz rankings are compiled using Buzz scores from the entire years’ worth of

data. Buzz scores measure whether people have heard anything positive or

negative about a brand during the previous two weeks and the scores are

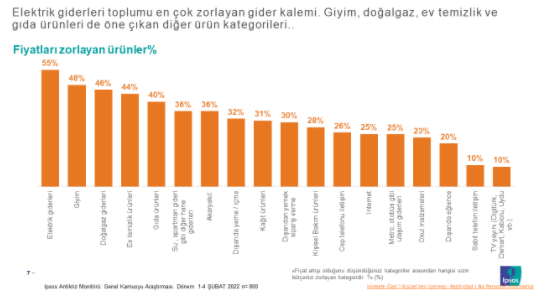

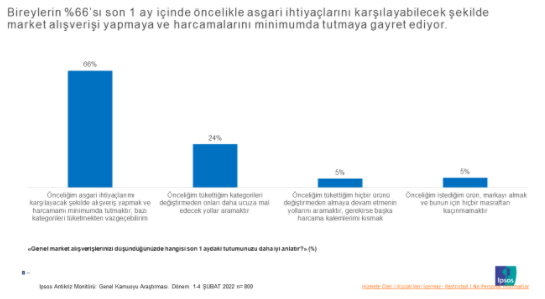

reported as NET scores. (YouGov India) February 10, 2022 (Turkey) According To 55% Of Turkish People Their Electricity

Expenses Are Very Difficult For Them 55% of individuals state that their

electricity expenses are very difficult for them. In addition to electricity

expenses, other expense items that force the citizens to come to the fore are

clothing, natural gas, household cleaning and food products. However, in

general, it is seen that all kinds of expense items force individuals. While

66% of individuals try to meet their minimum needs in grocery shopping and

keep their expenses to a minimum by giving up some categories. (Ipsos Turkey) 7 February 2022 MENA (UAE) Young Adults Are Affected The Most By UAE's New Work Week

Policy As the UAE moved to a new week work schedule

this year, YouGov’s latest survey reveals young adults in the country seem to

be most affected by this transition. Across different age groups, a higher

proportion of young adults aged 18-24 claim to be affected by this change (at

76%) as compared to older adults aged 35-44 (59%) or 45+ (49%). Currently, a

majority (79%) in the UAE claim their organization has made a switch to the

new workday policy. Of these, the proportions claiming to follow a

four-and-a-half-day workweek (Mon- Fri noon) and a new five-day work week

(Monday-Friday) are similar (47% and 53%, respectively). (YouGov MENA) AFRICA (Morocco) More Than Two-Thirds (68%) Of Moroccans “Agree” Or

“Strongly Agree” That Immigrants Strengthen The Country’s Cultural Diversity More than two-thirds (68%) of Moroccans

“agree” or “strongly agree” that immigrants strengthen the country’s cultural

diversity. More than half (52%) of citizens say immigrants help fill vacant

jobs (52%), and only about one-third (35%) see immigrants as increasing

levels of crime and insecurity. More than eight in 10 citizens express

tolerant attitudes toward immigrants and foreign workers, saying they would

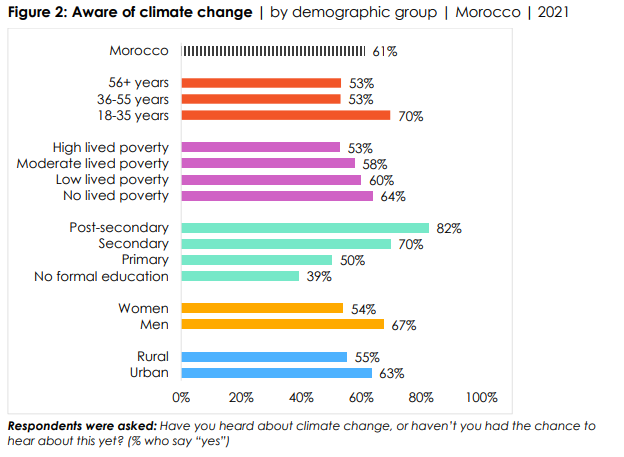

like (22%) or would not mind (59%) having them as neighbors. (Afrobarometer) 9 February 2022 About Four In 10 Moroccans Have Not Heard Of Climate Change More than six in 10 Moroccans (61%) say

they have heard of climate change, a 7- percentage-point increase compared to

2018 (54%) . Men and highly educated, economically well-off, young and urban

citizens are more likely to be aware of climate change than women and less

educated, poorer, older, and rural respondents. (Afrobarometer) 11 February 2022 WEST

EUROPE (UK) Public Criticism Of Conservatives’ Handling Of The Economy

Continues To Grow The economy is now seen by Britons as the most important

issue facing the country, jumping 12 points since last week from

45% to 57%. This is the highest percentage of people picking the issue since

March last year. Last week the issue was tied in first place but is now

15-points ahead over second-placed health (42%), with the environment

languishing in a distant third, at 27%. The percentage of Britons who say the

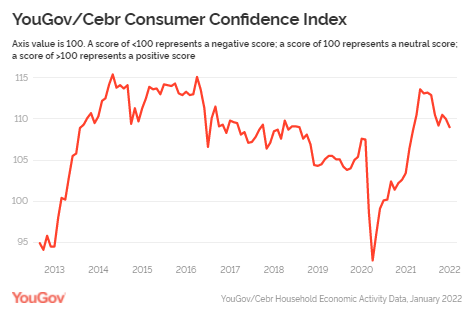

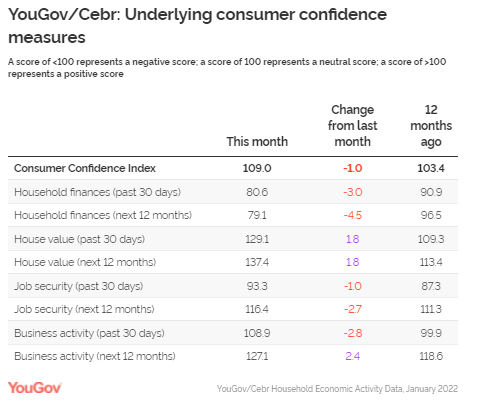

government are handling the economy badly has gone up seven points since last week, from 57% to 64%. (YouGov UK) February 09, 2022 Consumer Confidence Slips As Britons’ Household Finance

Concerns Increase The (then-speculative) increase in UK

energy bills has already had an impact on consumer confidence, according to

the newest analysis from YouGov and the Centre for Economics and Business

Research (Cebr). While the overall index saw a decline of just one point from

110 to 109.0, scores across every metric except home value measures and

business activity for the year ahead fell – in some cases, dramatically

so. (YouGov UK) February 09, 2022 Starmer And Labour Remain Unconvincing To Older Voters

Almost Half (49%) Of The Over-55 Electorate Would Vote Conservative With recent events taking their toll on the

Conservative party, a new YouGov looks at how the party is holding up among

their most important supporters: older people. According to our data, almost

half (49%) of the over-55 electorate would vote Conservative, while just over

a quarter (28%) would vote Labour. Only 10% would vote Lib Dem, 5% Green, 4%

Reform UK, and 3% for other parties. (YouGov UK) February 11, 2022 (France) 31% Of Parents Declare That Their Children Have Been, At

Least Once, Victim Of Cyber Violence More than 4 out of 10 French people have

already been victims of online violence. Although this phenomenon

particularly concerns 18-24-year-olds, 87% of whom declare having suffered a

situation of cyber violence, it is not confined to this age group and affects

the entire French population. If social networks and instant messaging

appear to be the spaces most conducive to cyber violence, they are found in

all digital spaces, from forums to dating applications, via SMS. (Ipsos France) February 9, 2022 1 In 10 French People Are Boycotting The Winter Olympics

This Year In general, the Winter Olympics

mobilize the attention of two thirds of French people, 51% say they generally

consider this event, if only for a few events, and 16% inquire at

least about the results. A passion for the Winter Olympics which is first

and foremost the fact of men, since ¾ of them say they have been let

down by this event in general. As for the diplomatic boycott (following the

allegations of human rights violations directed against China), although

supported by 53% of public opinion, this does not translate into

action: only 1 French out of 10 declares that he will boycott the Games

this year. (Ipsos France) February 10, 2022 (Germany) New Media Consumption Habits – But Which Ones Will Stick

After The Pandemic The current

Global Media Outlook Report from YouGov shows that the trends

from the past year are continuing. However, not

all of the global developments were felt so clearly in Germany after the first year of the pandemic

. At that time, less than a third of the adults surveyed in this country

used streaming services – far below average. However, at 36 percent, the

proportion of video-on-demand users is now at the level of the global average

from 17 markets that the study compares with each other. (YouGov Germany) February 14, 2022 NORTH AMERICA (USA) 58% Americans Favor Vaccine Requirement For Air Travel, But

Fewer Back Requiring Vaccines To Dine Or Shop Nearly two years after the coronavirus outbreak took hold in the United States,

Americans are increasingly critical of the response to COVID-19 from elected

officeholders and public health officials. Amid debates over how to address

the surge in cases driven by the omicron variant, confusion is now the most

common reaction to shifts in public health guidance: 60% of U.S. adults say

they’ve felt confused as a result of changes to public health officials’

recommendations on how to slow the spread of the coronavirus, up 7 percentage

points since last summer. (PEW) FEBRUARY 9, 2022 Two-Thirds Of Black Protestants (65%) Approve Of The Job

That Biden Is Doing As President Roughly two-thirds of Black Protestants

(65%) approve of the job that Biden is doing as president, according to

a Pew Research Center survey conducted Jan. 10-17. That is down

sharply from 92% in March 2021, shortly after he took office. Today, 47% of

religious “nones” – respondents who describe their religious identity as

atheist, agnostic or “nothing in particular” – approve of Biden’s

performance, down from 71% in April 2021 and 65% in March 2021. The share of

“nones” who now approve of Biden is the lowest it has been since his

inauguration, falling below the previous low of 55% in September 2021. (PEW) FEBRUARY 10, 2022 For (43%) Black Americans, Family And Friends Are A Primary

Source Of Information On U S Black History Nearly nine-in-ten Black Americans say they

are at least somewhat informed about the history of Black people in the

United States, with family and friends being the single largest source of

information about it, according to a recent Pew Research Center survey of Black adults. About half of Black Americans (51%) say

they are very or extremely informed about the history of Black people in the

U.S. Nearly four-in-ten (37%) say they are somewhat informed, while 11% say

they are a little or not at all informed. (PEW) FEBRUARY 11, 2022 (Canada) Nearly Half (46%) Of Canadians Say They “May Not Agree With

Everything” Trucker Convoy Says Or Does Nearly half (46%) of Canadians say they

“may not agree with everything the people who have taken part in the truck

protests in Ottawa have said, but their frustration is legitimate and worthy

of our sympathy.” The proportion of 18-34-year-olds who adopt this point of

view is 61%, while those aged 35-54 (44%) and 55+ (37%) are much less likely

to agree. Regionally, those in Alberta (58%) and Saskatchewan and Manitoba

(58%) are most likely to align with this argument, while a sizeable minority

in Quebec (47%), Ontario (44%), Atlantic Canada (43%), and British Columbia

(36%) agree. Politically, most Conservative voters (59%) are on this side of

the argument, while a minority of Bloc (44%), NDP (43%) and Liberal (30%)

voters are also aligned. (Ipsos Canada) 11 February 2022 AUSTRALIA Roy Morgan Business Confidence Plunges 18.7pts To 101.5 In

January As Omicron Variant Sweeps Australia The plunge in January came as the Omicron

variant swept Australia causing the infection of over 2 million Australians

with COVID-19 and forcing millions more into isolation for being close

contacts of confirmed cases. The disruption to businesses caused problems

throughout the economy and led to breakdowns in supply chains which are only

now being gradually rectified. On a State-based level there were monthly

decreases across the board in January led by NSW, down 17.1pts (-13.7%) to

107.6, Victoria, down 22.6pts (-19%) to 96.3, Queensland, down 23.4pts

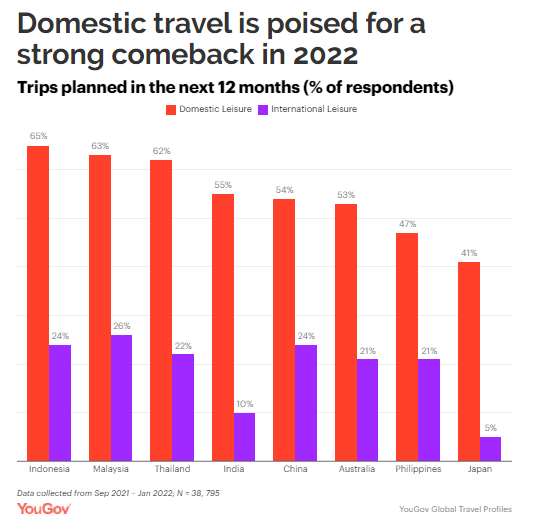

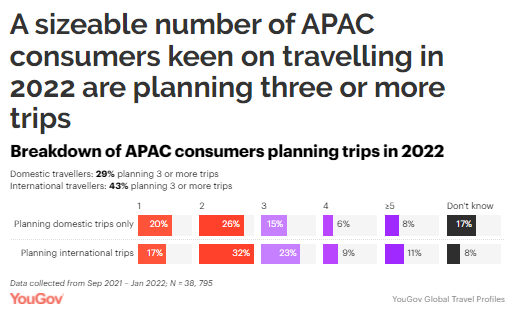

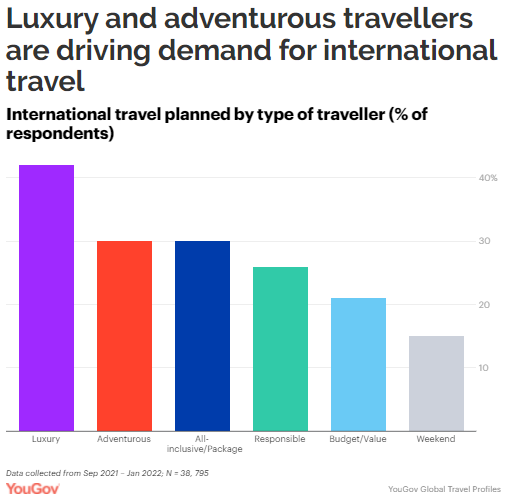

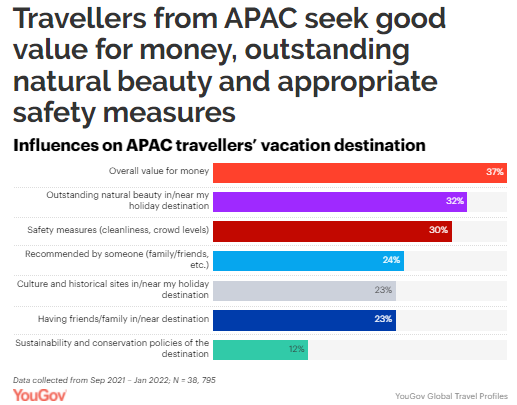

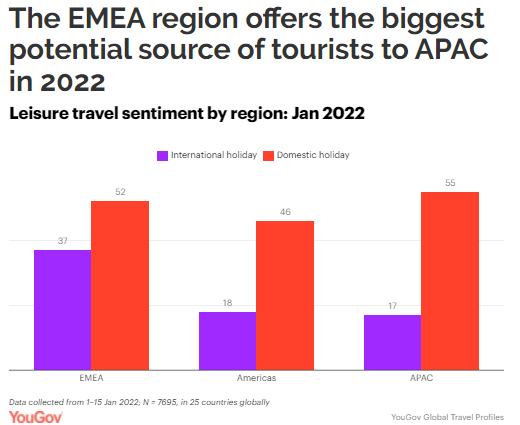

(-20.2%) to 92.5 and South Australia, down 12.3pts (-11.2%) to 97.4. (Roy Morgan) February 10 2022 MULTICOUNTRY STUDIES With The Emergence Of The Omicron Variant 25% Of APAC

Consumers Are Delaying Their Travel Booking, Survey Carried out In 25

Countries Latest data from YouGov Global Travel Profiles shows that over half of APAC

consumers have domestic leisure trips planned for 2022. This ranges from more

than 60% of consumers in Indonesia, Malaysia and Thailand, over 50% of

consumers in China, India and Australia, and more than 40% of consumers in

the Philippines and Japan. Demand for international travel, while lower, is

above 20% in most APAC markets – except for China (10%) and Japan (5%). This

data gives travel marketers a head start as they assign their spending for

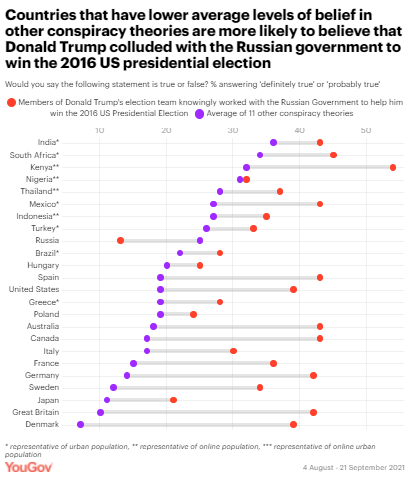

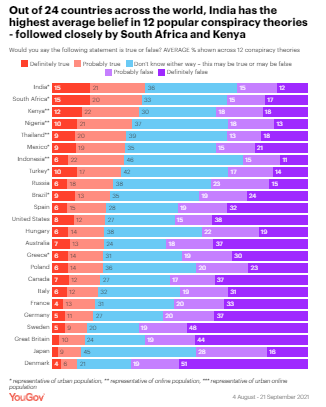

the first quarter of 2022. (YouGov Philippines) February 7, 2022 Source: https://ph.yougov.com/en-ph/news/2022/02/07/APAC-2022-travel-outlook-forecast/ Conspiracy Theories People Around The World Believe In 2021

Across 24 Countries The theory that a single group of people

who secretly control events and rule the world together, outside of official

governments, had the highest average levels belief across all 24 countries

out of our list of 12 popular conspiracy theories. Support for this theory

was particularly prevalent in Kenya, Nigeria, and South Africa, with 72%, 69%

and 61% respectively saying they thought it was definitely or probably true.

A further 17% of Kenyans, 22% of Nigerians and 27% of South Africans said

they didn’t know either way: that it might be true, or it might be false. (YouGov UK) 43% Of Americans Think Tackling Racism Should Be A “High

Priority” For The U S, Survey Of 13 Western Countries Britain is among the top three of the

nations surveyed who think combatting racism should be a “high priority”

(55%), and a further 28% think it should be a “medium priority”. Only the

Spanish (58%) and Greeks (59%) are more likely than Brits to think fighting

racism should be a high priority for their nations. The United States, on the

other hand, is third from bottom among the countries included in the survey.

While some 43% of Americans think tackling racism should be a “high priority”

for the US, another 18% think it should be a low priority or not a goal at

all. (YouGov UK) February 08, 2022 Globally, The Proportion Of Adults Who Are Likely To Use

Each Type Of Media Is Increasing, A Study In 17 Markets Globally, a larger proportion have

increased their use of digital media such as websites / apps, social media

and streaming of video services. The biggest change is noticeable in the

use of websites / apps, something that 42% has spent more time on. At

the same time, we see that an increasing proportion of global consumers have

reduced their use of traditional media. For example, 19% spend less time

listening to the radio, 18% read fewer newspapers or magazines and a

corresponding proportion watch less linear television. (YouGov Sweden) February 9, 2022 Source: https://yougov.se/news/2022/02/09/det-globala-medielandskapet-2022/ ASIA

729-43-01/Polls Youtube Tops

Yougov’s Best Buzz Rankings 2021 In India

YouTube has dethroned its parent company

Google to become the top-ranked brand in YouGov’s Best Buzz Rankings 2021 in India (51.4). Google, which had

previously held the top spot (in 2018 & 2019) dropped down one place to

second (50.1) in the 2021 rankings. YouGov’s BrandIndex measures the public’s

perception of brands on a daily basis across a range of metrics. The annual

Buzz rankings are compiled using Buzz scores from the entire years’ worth of

data. Buzz scores measure whether people have heard anything positive or

negative about a brand during the previous two weeks and the scores are

reported as NET scores.

Amidst a tough year with global backlash

for its new privacy policy, WhatsApp recorded a decline in its Buzz scores

and dropped down two places to fourth (44.7). On the other hand, Instagram

strengthened its position in the Indian market and climbed up three places to

sixth (36.5) in the 2021 rankings. Online delivery app Flipkart also recorded

an improvement to its Buzz scores, moving up one place to seventh (36.3),

while Zomato slipped down from seventh in 2019 to ninth in 2021 (35.0). Air India’s successful acquisition by the

TATA group generated a lot of noise, placing the national carrier in the list

of buzziest brands of the year- in eighth (35.4). Lastly, MakeMyTrip moved

down to tenth place (35.0), completing the top ten list in India. YouGov BrandIndex has also released the ten

“most improved” brands of the past year. In 2021, growing concerns over

privacy gave a huge boost to encrypted messaging services. Telegram emerged

as the most improved brand of the past year in India, with a change of +7.0.

Tata Motors is the second most improved

brand, with a change in score of +4.5. Along with being one of the top ten brands

of 2021, Air India is also the third most improved brand of the past year

(+3.5). Indigo is another airline that appears on the list of improvers this

year, in fifth (+3.0). With stay-at-home restrictions during the

pandemic accelerating the adoption of online retailing in India, it’s not

surprising to see online fashion brand Myntra feature as the sixth (2.8) most

improved brand of the past year. The improvers list also features leading

banks like YES Bank (3.2) and Punjab National Bank (2.7), consumer

electronics giant- Samsung (2.2), and smartphone brands such as Vivo (2.2)

and Realme (2.1) (YouGov India) February 10, 2022 Source: https://in.yougov.com/en-hi/news/2022/02/10/youtube-tops-yougovs-best-buzz-rankings-2021-india/ 729-43-02/Polls According To

55% Of Turkish People Their Electricity Expenses Are Very Difficult For Them

Electricity Expenses Are The Most Difficult

Expenses For The Society In This Period 55% of individuals state that their

electricity expenses are very difficult for them. In addition to electricity

expenses, other expense items that force the citizens to come to the fore are

clothing, natural gas, household cleaning and food products. However, in

general, it is seen that all kinds of expense items force individuals.

Majority of Society Trying to Reduce Their

Spending on Grocery Shopping While 66% of individuals try to meet their

minimum needs in grocery shopping and keep their expenses to a minimum by

giving up some categories if necessary, 24% are looking for ways to make the

products they consume cheaper.

The Opinions of Half of the Society on

House Income Aren't Very Positive While 54% of individuals state that their

household income has decreased in the last 12 months, their expectations for

their personal economy in the next few months are not positive either. Also,

57% say their personal economy will get worse in the next few months. The

rate of those who think that their personal economy will be better for the

future is only 6%.

Majority of Society Thinks The Current

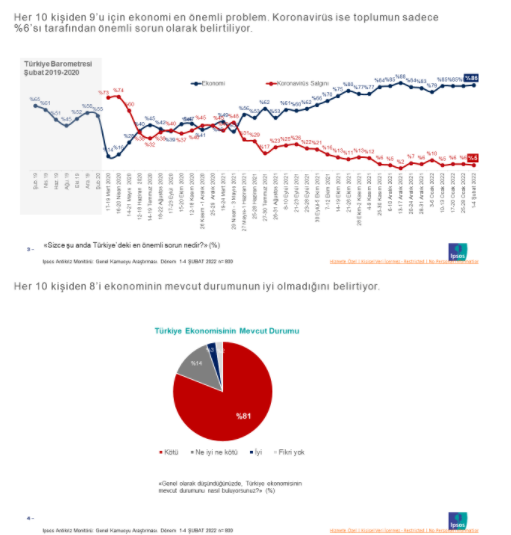

Situation Of The Turkish Economy Is Not Good The rate of those who think that the

current situation of the Turkish economy is not good is 81%. Only 3% think

the economy is good.

Economy The Most Important Problem of

Society As of June 2021, the rate of mentioning the

economy as the most important problem was ahead of the epidemic. Today, the

economy is the most important problem for 9 out of 10 people. Even the rapid

transmission in the epidemic or the increase in the number of cases does not

cause the Coronavirus Outbreak to be seen as a significant problem. Only 5%

of individuals consider the epidemic to be the most important problem.

Ipsos Turkey CEO Sidar Gedik made the

following evaluations about the data; We continue to receive the answer to

the question, which is the most important problem of the country, economy by

far. At this point, in order to clarify the approach a little more, we asked

an interesting question the previous week, we said, would you destroy the

epidemic or fix the economy if you had the opportunity to solve only one

problem, and we got the answer to this question, again, economy by a large

margin. Looking at the results of this week, we can say that the most

important problem of the country, the economy, has become our only problem,

so important that we forget almost all other problems. While the rate of

those who say that the coronavirus epidemic is the most important problem is

5%, those who say that the economy is the most important problem are 86%.

That's why this week we focused on the economy topic. The majority think that their personal

economic situation will worsen in the near future. Nearly one-third think

their personal economy will stay the same or get better in the near future.

However, when we evaluate the national economy and personal economy questions

together, we see that some of this group, who is more hopeful about their own

situation, is not satisfied with the state of the country's economy. 54% of respondents in our survey state that

their household income has decreased in the last 12 months. In parallel with

the question of personal economy, about 40% of people in this question state

that the household income did not change much or increased during the same

period. If we remember that the rate of those who say that the most important

problem of the country is the economy is 86%, we can say that a significant

part of those who have not experienced any loss in household income see the

economy as a problem. We see that the item that affects the

citizens the most in price increases is the electricity bill. With the effect

of the winter season, clothing costs are another item. Other inevitable

monthly invoice items such as natural gas and water also have a significant

impact. Two out of every three people who participated in our research state

that they can stop consuming certain product categories in order to save

money in grocery shopping. The economy has turned into a problem

independent of political preferences. We understand this from the fact that

eight out of every ten people describe the state of the country's economy as

bad, according to the latest published research, no political party or

alliance has 80% of the votes, citizens are dissatisfied with the economy

regardless of their vote preference. (Ipsos Turkey) 7 February 2022 Source: https://www.ipsos.com/tr-tr/bireyleri-en-cok-zorlayan-gider-kalemi-elektrik MENA

729-43-03/Polls Young Adults

Are Affected The Most By UAE's New Work Week Policy

YouGov's latest study shows the impact of

the new work week policy on the lives of UAE residents As the UAE moved to a new week work

schedule this year, YouGov’s latest survey reveals young adults in the

country seem to be most affected by this transition. Across different age

groups, a higher proportion of young adults aged 18-24 claim to be affected

by this change (at 76%) as compared to older adults aged 35-44 (59%) or 45+

(49%).

Currently, a majority (79%) in the UAE

claim their organization has made a switch to the new workday policy. Of

these, the proportions claiming to follow a four-and-a-half-day workweek

(Mon- Fri noon) and a new five-day work week (Monday-Friday) are similar (47%

and 53%, respectively). However, the former transition is more prevalent in

the public sector, while the latter is dominant among private-sector

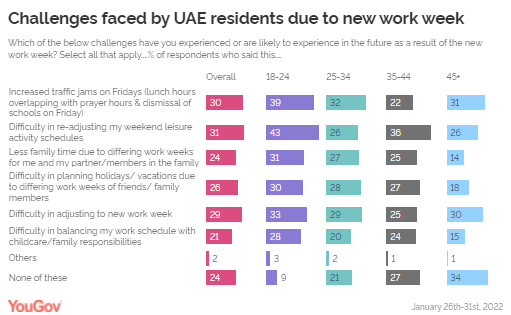

employees. When asked about the challenges they are

experiencing as a result of this shift, almost a third (31%) of working

respondents expressed their difficulty in readjusting their weekend leisure

schedules, and a similar percentage (30%) said they are experiencing traffic

jams on Fridays. Difficulty in adjusting to new work week

(29%), trouble in planning holidays (26%), and less family time (24%) due to differing

work weeks are stated as some other issues that people in UAE are currently

facing or are likely to face in future. Data shows young adults between 18-24 years

seem to be experiencing all the above-mentioned challenges much more than the

other age groups.

Despite the challenges, a majority (61%) of

UAE residents said they are happy with the new work week policy, with

respondents aged 35-44 years appearing happier than others with this

development (at 67%). When asked

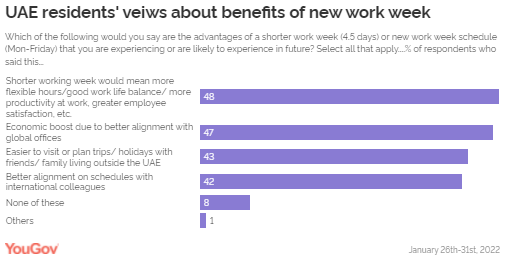

about the benefits of the new work policy, almost

half (48%) of the respondents stated that shorter work weeks lead to better

work-life balance or higher productivity. Despite claiming to be most

impacted by the transition, more than half of 18–24-year-olds (54%)

recognised this as an advantage.

Nearly half of all respondents (47%) think

that the new policy will boost the economy as it eliminates the weekend gap,

making UAE look more attractive to foreign talents and investments. At a personal level, two in five (42%)

see it as an opportunity to better align their schedules with international

colleagues, while almost the same number (43%) say that it will be now easier

for them to visit or plan holidays with friends and family staying abroad. (YouGov MENA) Source: https://mena.yougov.com/en/news/2022/02/11/young-adults-are-affected-most-uaes-new-work-week-/ AFRICA

729-43-04/Polls More Than Two-Thirds

(68%) Of Moroccans “Agree” Or “Strongly Agree” That Immigrants Strengthen The

Country’s Cultural Diversity

A majority of Moroccans express welcoming

attitudes toward immigrants, saying they strengthen the country’s cultural diversity

and help fill job vacancies, according to the latest Afrobarometer survey. Most citizens say they would not mind

having immigrants as neighbours, and a majority disagree with the idea that immigrants

increase crime or insecurity. By a 3-to-1 margin, citizens say the

government should not limit the cross-border movement of people and goods. But in reality, most citizens say they find

it difficult to move across international borders to work or trade in other countries in the region.

While the Arab Maghreb Union (AMU) has been working to allow free movement of goods,

persons, and services within the sub-region, Morocco is yet to allow free entry from

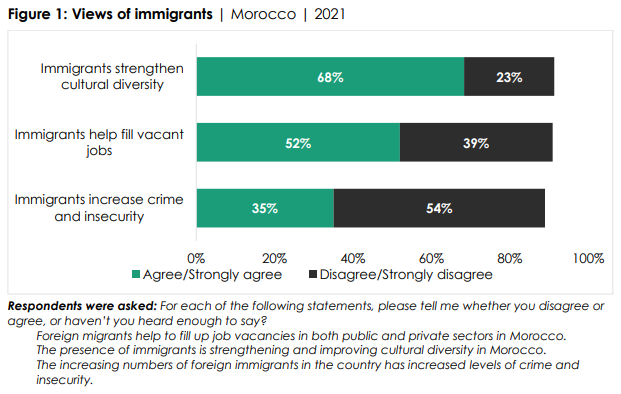

other AMU member states. Key findings ▪ More than two-thirds (68%) of

Moroccans “agree” or “strongly agree” that immigrants strengthen the country’s cultural

diversity. More than half (52%) of citizens say immigrants help fill vacant jobs (52%), and

only about one-third (35%) see immigrants as increasing levels of crime and

insecurity (Figure 1).

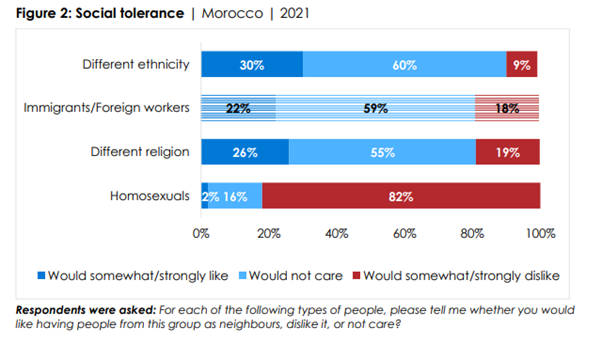

▪ More than eight in 10 citizens

express tolerant attitudes toward immigrants and foreign workers, saying they would like (22%) or

would not mind (59%) having them as neighbours (Figure 2).

(91%) and different religion (81%), but

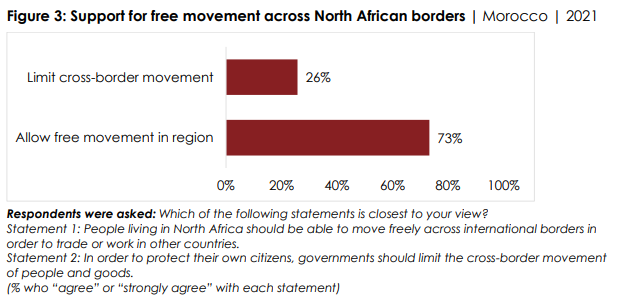

fewer than two in 10 (18%) are tolerant toward people in same-sex relationships. ▪ Almost three-fourths (73%) of

Moroccans say North Africans should be able to move freely across international borders in

order to trade or work in other countries (Figure 3).

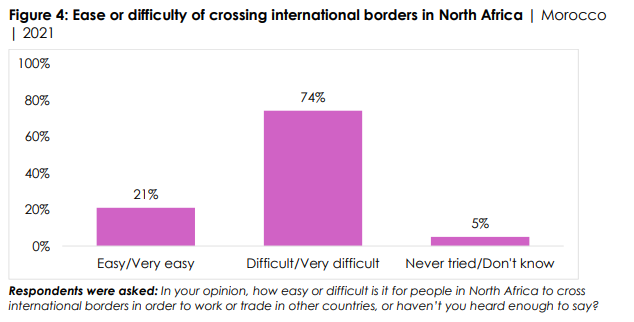

▪ But in practice, the same

proportion (74%) say it is difficult for people to cross borders in the region (Figure 4).

(Afrobarometer) 9 February 2022 729-43-05/Polls About Four

In 10 Moroccans Have Not Heard Of Climate Change

Moroccans’ awareness of climate change and

its negative impact on the country has improved over the past three years,

according to the latest Afrobarometer study. Even so, about four in 10 citizens have not

heard of climate change. And among those who are familiar with the concept, half do not

see its effects as harmful. As the country battles more frequent

droughts, the government has taken steps to fight climate change, including strategies to

meet half of Morocco’s electricity needs through renewable energy (solar, wind, and

hydropower) by 2030. The 2019 Climate Vulnerability Index ranked

Morocco 57th out of 182 countries in exposure, sensitivity, and ability to adapt to the

negative effects of climate change. Key findings ▪ More than six in 10 Moroccans (61%)

say they have heard of climate change, a 7- percentage-point increase compared to 2018

(54%) (Figure 1).

▪ Men and highly educated,

economically well-off, young and urban citizens are more likely to be aware of climate change than

women and less educated, poorer, older, and rural respondents (Figure 2).

▪ Among those who have heard of

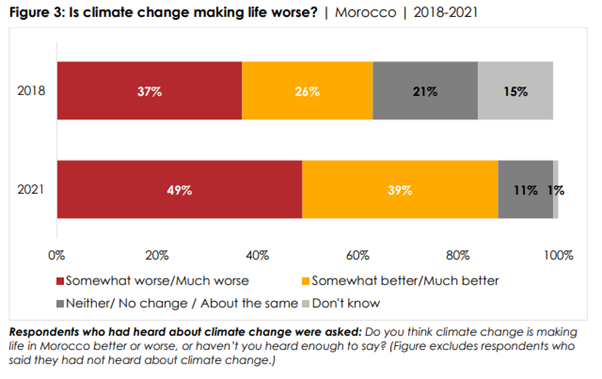

climate change, half (49%) say it is making life in Morocco “somewhat worse” or “much worse,” a

12-percentage point increase from 2018 (37%). But the share who think climate

change is making life better also increased, from 26% to 39% (Figure 3).

(Afrobarometer) 11 February 2022 WEST

EUROPE

729-43-06/Polls Public Criticism Of Conservatives’ Handling Of The Economy Continues

To Grow

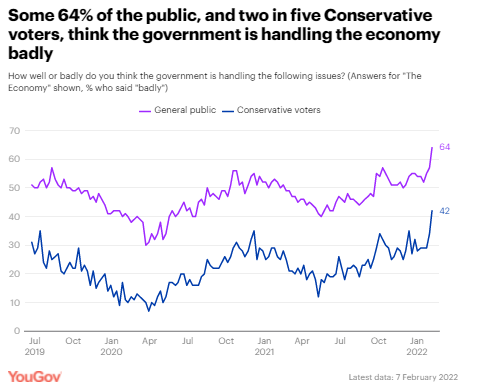

The economy is now

seen by Britons as the most important issue facing the country, jumping

12 points since last week from 45% to 57%. This is the highest percentage of

people picking the issue since March last year. Last week the issue was tied

in first place but is now 15-points ahead over second-placed health (42%),

with the environment languishing in a distant third, at 27%.

While the Conservative party are still seen as the best political

party to manage the economy overall - with

30% saying so, compared to 22% for Labour - Britons are becoming

more and more sceptical about how well the government is handling the economy

and surrounding issues such as taxation and inflation. The percentage of Britons who say the government are handling the

economy badly has gone

up seven points since last week, from 57% to 64%. This pattern is

mirrored among 2019 Conservative voters, with an increase from 34% saying

badly last week to 42% now.

There has been widespread public concern over inflation, with some

predicting cost increases as large as 7% in coming months. Public attitudes

to how the government is handling inflation, have seen a similarly negative

shift to the wider economy. The number of Britons who say inflation is being

handled badly has

increased by seven points in the last week, from 66% to 73%. Again, this is

mirrored with a nine-point jump amongst Conservative voters, with a strong

majority now thinking it is being managed badly (61%, vs 30% who think the

government is doing well).

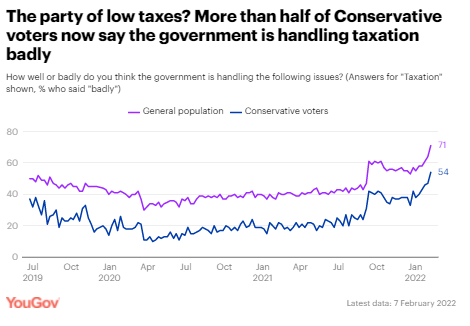

Concern over the state of the UK’s economy also includes the

forthcoming National Insurance rise. This is reflected in attitudes to the

government handling of taxation, with

another seven-point increase in Britons labelling it ‘bad’, from 64% last

week to 71% now. We also witness discontent growing further amongst

Conservative voters, with 54% now saying badly (up from 47%).

(YouGov UK) February 09, 2022 729-43-07/Polls Consumer Confidence Slips As Britons’ Household Finance Concerns

Increase

The (then-speculative) increase in UK energy bills has already had an

impact on consumer confidence, according to the newest analysis from YouGov

and the Centre for Economics and Business Research (Cebr). While the overall

index saw a decline of just one point from 110 to 109.0, scores across every

metric except home value measures and business activity for the year ahead

fell – in some cases, dramatically so.

YouGov collects consumer confidence data every day, conducting over

6,000 interviews a month. Respondents answer questions about household

finances, property prices, job security, and business activity, both over the

past 30 days and looking ahead to the next 12 months. While the

rising energy price cap (reportedly set to cost millions of Britons as much as £693 per year)

was announced in early February, January saw plenty of speculation that bills would significantly

increase across the country. Against this backdrop, confidence in household

finances took an immediate blow: scores for the past month deteriorated from

83.7 to 80.6, while outlook deteriorated from 83.6 to 79.1.

Business activity measures were a mixture of good and bad news. While

scores for the past month went from 111.7 to 108.9 (perhaps indicating a

post-Christmas slump), scores for the next 12 months increased from 124.7 to

127.1: an increase of 2.4 points that effectively wipes out the 2.4 point

loss of confidence from December 2021. Along with business owners, homeowners also had reason to be cheerful

in January 2022 – with house prices at their highest level since 2005. For

the third month in a row, measures for the past month and the 12 months ahead

increased; in February 2022, both rose by 1.8 points.

Darren Yaxley, Head of Reputation Research at YouGov: “Consumers’ economic outlook at the start of the

year reveals a complicated picture. Although the headline consumer confidence

slipped by a point in January, there was a lot going on under the surface

that shaped their economic optimism. While consumers’ outlook for their

household finances has not been as bleak since the autumn of 2013 homeowners’

views of the property market have not been this strong since September 2014.

Both are likely to be shaped over the coming months by announcements that

took place at the start of February, after this data was collected – the

announcement of the increase in the energy price cap and the Bank of England

raising interest rates.” Sam Miley, Senior Economist at Cebr: “This month’s drop in the YouGov/Cebr Consumer Confidence Index

highlights the impact of the rising cost of living on household sentiment.

Away from the headline indicator, consumers’ assessment of their finances

over the coming year provides for a particularly stark reading - reaching a

near nine-year low. Rising inflation and the planned uplift to National

Insurance contributions are just two likely factors behind this weaker

outlook. This sentiment is also mirrored in Cebr’s latest forecasts, with

real disposable incomes expected to fall year-on-year and the household

savings ratio set to narrow significantly.” (YouGov UK) February 09, 2022 729-43-08/Polls Starmer And Labour Remain Unconvincing To Older Voters Almost Half

(49%) Of The Over-55 Electorate Would Vote Conservative

With recent events taking their toll on the Conservative party, a new

YouGov looks at how the party is holding up among their most important

supporters: older people. According to our data, almost half (49%) of the over-55 electorate

would vote Conservative, while just over a quarter (28%) would vote Labour.

Only 10% would vote Lib Dem, 5% Green, 4% Reform UK, and 3% for other parties.

However, there is some evidence of a decent-sized swing in vote

intention from the Conservatives to Labour – 5% of 2019 Conservative voters

in this age group now intend to vote Labour. Further, similarly to the

national picture, almost a quarter Conservative 2019 voters now either do not

know who they vote for (19%) or would not vote at all (4%). Indeed, just 62% of older voters who backed Boris Johnson’s party at

the last election still intend to vote Conservative again now. So, despite still maintaining a 21-point lead among older voters, the

Conservatives are nonetheless struggling to hold on to significant numbers of

one of their most loyal tribes. Current YouGov vote intention figures among the country as a whole

show sizeable Labour leads, with data from 2 February showing the

Conservatives nine points behind their main rivals. That represents a

difference of -30 points in terms of leads between the over 55s and the

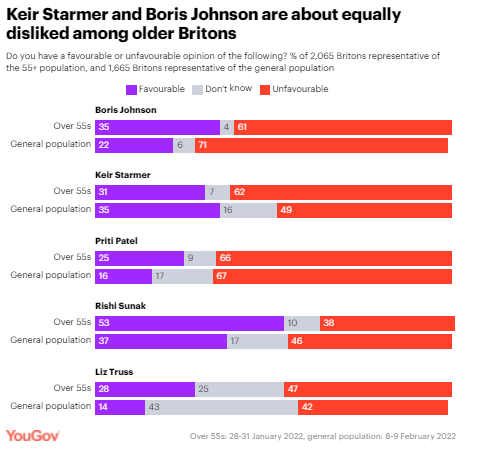

general population as a whole. Keir Starmer and Boris Johnson are about

equally disliked among older Britons While the over 55s do have a negative view of the Conservative party

(net -13), they have much stronger disdain for the Labour party (-35). The

difference is much smaller when we look at the two respective leaders,

however; older people are negative about both Johnson (net -26) and Starmer (-31). That Johnson is much less popular than his own party among older

voters suggests that there could yet still be further damage done to the

Conservative party brand should the prime minister remain in power but fail

to improve his own personal ratings.

In terms of prospective Conservative replacements for Johnson as

party leader, older people are positive about Rishi Sunak (net +15), but

negative about Liz Truss (-19), Jeremy Hunt (-23), and Michael Gove (-32). As with voting intention, over 55s tend to be more favourable toward

Johnson and the Conservatives than the national rate. Latest YouGov figures

have net favourability for Boris Johnson at -52, and the Conservatives at

-41. That’s a full 26-point difference on Johnson, and a 28-point net

difference for his party. Meanwhile, the general population is more positive (or, less

negative) about both Keir Starmer (-19), and the Labour party (-16). Those

national figures are 12 points higher for Starmer and 16 points higher for

Labour. (YouGov UK) February 11, 2022 729-43-09/Polls 31% Of Parents Declare That Their Children Have Been, At Least Once,

Victim Of Cyber Violence

An alarming finding The data collected from the French on cyberviolence and cyberbullying

paint an alarming picture: 41% of French people say they have been

victims of cyberviolence and 31% admit to having committed

it . Online violence is an extremely widespread phenomenon that

particularly targets young people and people belonging to minority

groups. They have serious consequences on the life and health of the

victims, sometimes even attempting suicide for more than 1 in 10 victims, and

yet remain largely minimized and unpunished.. The fight against this violence

still relies mostly on the victims, who, for lack of satisfactory remedies in

terms of reporting and legal proceedings, develop self-defense strategies

that tend to restrict their freedom of expression.

Cyberviolence and cyberbullying are a

massive phenomenon that does not only concern the youngest. More than 4 out of 10 French people have already been victims of

online violence. Although this

phenomenon particularly concerns 18-24 year olds, 87% of whom declare having

suffered a situation of cyberviolence, it is not confined to this age group

and affects the entire French population. If social networks

and instant messaging appear to be the spaces most conducive to

cyberviolence, they are found in all digital spaces, from forums to dating

applications, via SMS.

Cyber-violence has serious consequences on

the health and life of those who are victims of it. The psychological and social consequences

of cyberviolence are numerous and significant for the victims, even more when

it comes to children, women and people belonging to minority groups.. Victims

of online violence report very heavy impacts, whether socio-economic or

health-related. Thus 22% have unsubscribed from social networks, 11% say

they have lost their job or failed in their studies following the violence,

41% of them have felt depressed or desperate, 17% have thought about suicide

and 16% that they deserved what was happening to them. The recurrence of

online attacks amplifies the consequences for the victims: almost half (45%)

of people who have been victims of the dissemination of degrading or intimate

photos and videos on several occasions have thought about

suicide. Belonging to a minority group and being a woman are also

factors that increase the impact of violence. Ignorance of the law and the trivialization

of this violence encourage impunity. If the vast majority of French people are aware of what cyberbullying

is, the fact that these actions fall under the law is often less known. Barely more than a quarter of French people

recognize all the acts of cyberviolence listed as such . It is the people most familiar with social networks

(young people, people present on many networks) who have the most difficulty

in recognizing these situations as cyberviolence. In

addition, 73% of French people say they do not know the criminal risks

incurred when an act of cyberviolence or cyberharassment is committed. Remedies that appear to be insufficient and

reports that remain a dead letter. The majority, whether or not they have been victims of cyberbullying, the French do not know who to contact in the event

of cyberviolence or cyberbullying. More than half of French

people say they do not know (59%) or did not know (52%) how to react or who

to contact as a victim of an act of cyberviolence. While 1 in 5 victims

say they have gone to the police or the gendarmerie to file a complaint, less

than half of these complaints (47%) have given rise to legal proceedings and

two thirds (67%) of those who have took the step of filing a complaint were

refused this deposit. In addition, the support of social media platforms

in the fight against cyberbullying is mostly perceived as insufficient.Nearly two-thirds (65%) of French people believe

that the platforms do not do enough in the fight against online violence . If

more than 1 in 3 French people say they have already taken the step of

reporting content or a profile considered malicious or inappropriate, in more

than half (58%) of cases, either the social network did not respond , or his

answer was unsatisfactory.

Self-censorship as a means of self-defense. Among the 6 out of 10 French people using

the networks who say they do not publish anything, 1 out of 10 declares that

they refuse to do so for fear of the consequences despite their desire to

publish . As for the people who publish,

they say they are careful; only a minority publish content without

restriction. The online presence is therefore designed defensively and

the fact of having been a victim several times amplifies the tendency to

self-censorship. Posts about religious beliefs, political opinions,

sexual orientation, and nude photos (eg, bathing suits) are where social

media users say they restrict themselves the most. Essential levers to fight against

cyberviolence according to the French. Strengthening prevention and rights

education seems essential to the French to improve information for the public

and in particular for the youngest. They also

recommend highlighting 3018, the emergency number for young victims of

digital violence, or simplifying the filing of complaints to better support

victims. On the other hand, the lifting of anonymity or pseudonymity is

not considered to be an important lever, and for good reason, since in the

majority of cases the victims know the identity of the perpetrator of the

violence. (Ipsos France) February 9, 2022 729-43-10/Polls 1 In 10 French People Are Boycotting The Winter Olympics This Year

Between diplomatic boycott and sporting interest, the French are

divided In general, the Winter Olympics mobilize the attention of two

thirds of French people, 51% say they generally consider this event, if

only for a few events, and 16% inquire at least about the

results. A passion for the Winter Olympics which is first and foremost

the fact of men, since ¾ of them say they have been let down by this

event in general. And it ended again for the 2022 edition of these Winter Olympics in

Beijing, with a majority of the French public who are receptive to this

event: 10% of those questioned will have to follow every day and 46% a

few trials. Conversely, a third of French people do not say they are

interested in this event. As for the diplomatic boycott (following the allegations of human

rights violations directed against China), although supported by 53% of

public opinion, this does not translate into action: only 1 French out

of 10 declares that he will boycott the Games this year. The events that mobilize the most attention: alpine skiing, biathlon,

figure skating As soon as we ask the French people who have to follow these Winter

Olympics in Beijing about the key events, three disciplines are of particular

interest: alpine skiing comes first with 47% of intention to follow, biathlon

and figure skating completing the podium, with 40% attention level for

each. The level of interest in these 3 major sports is also more

pronounced among those aged 55 and over ; it should be noted

that figure skating also interests more women (59% who intend to watch

the events) than men (26% only). Among the other events that would have also provided strong

audiences, we also find ski jumping (39% follow-up intention), freestyle

skiing (31%), cross-country skiing (28%) or snowboarding. , the latter sport

attracting more young people (16-24 years). Will French athletes shine? it is the wish of many For the French who plan to follow the Beijing Olympics, the

predictions for this 2022 edition are mostly between 5 to 15 medals: 46%

hope that France will collect between 5 and 10 charms, and 36% rather

anticipate 10 to 15 medals. The most optimistic even seeing the French athletes win the 15 medals

(10% of them) (Ipsos France) February 10, 2022 Source: https://www.ipsos.com/fr-fr/1-francais-sur-10-boycotte-les-jo-dhiver-cette-annee 729-43-11/Polls New Media Consumption Habits – But Which Ones Will Stick After The

Pandemic

Everything is becoming more and more digital - and the pandemic is

amplifying this development. This is reflected in media consumption,

among other things. For traditional media around the world, lockdowns

and changing daily routines have meant that pre-pandemic downtrends have

accelerated. Radio listeners, for example, shrank because commuters no longer

made many car journeys. Meanwhile, video streaming services like Netflix

and Amazon Prime have surged, as have podcasts -- mostly driven by the

younger generation. The current Global Media Outlook Report from YouGov

shows that the trends from the past year are continuing. However, not all of the global developments were felt so clearly in

Germany after the first year of the pandemic . At that time,

less than a third of the adults surveyed in this country used streaming

services – far below average. However, at 36 percent, the proportion of

video-on-demand users is now at the level of the global average from 17

markets that the study compares with each other. Growth driver video on demand But which trends will continue and which will reverse when

pandemic-related restrictions are lifted or eased? YouGov also provides

data on this. In the case of video streaming subscriptions in Germany,

growth will therefore continue: fewer respondents say they want to cancel

their subscription than respondents say they can imagine taking out a new

subscription this year. Globally, it is evident that growth can also be expected from

existing customers. 71 percent of those surveyed consumed the same or

more video-on-demand in 2021. Of these respondents, almost all (86

percent) say they plan to maintain or increase this level of usage; more

than a third (36 percent) anticipate greater use this year. Comparable trends can be seen in music streaming, social media use,

website and app use, and podcast listening. It is noticeable: These are

all non-linear, digital online offers. The proportion of those who, on

the other hand, used traditional media offerings such as television, radio

and newspapers and magazines (offline and online) at least as much as in the

previous year and want to increase their use this year is significantly

lower. One in three wants to listen to more

podcasts But that should not hide the fact that traditional media can still

have very high usage rates. Above all, linear television is watched a

lot worldwide as well as in Germany. But the greatest growth can be expected in digital media

consumption. Media producers and advertisers can assume that the new

consumption habits caused by the pandemic will not change anytime soon and

that video streaming in particular will continue to grow. There is great

potential in the audio sector, with 17 percent of respondents who currently

do not have a paid music streaming subscription but could imagine subscribing

to a service this year. It should also not be neglected that 30 percent

of those surveyed stated that they wanted to increase their podcast

consumption in 2022. The pandemic will continue to increase media consumption worldwide

for some time to come. Looking ahead, however, it can be assumed that

the trend will flatten out. If you would like to take a look at the full

Global Media Outlook Report 2022, you can download it here . (YouGov Germany) February 14, 2022 Source: https://yougov.de/news/2022/02/14/neue-gewohnheiten-beim-medienkonsum-aber-welche-bl/ NORTH

AMERICA

729-43-12/Polls 58% Americans Favor Vaccine Requirement For Air Travel, But Fewer

Back Requiring Vaccines To Dine Or Shop

Nearly two years after the coronavirus

outbreak took hold in the United States, Americans are increasingly

critical of the response to COVID-19 from elected officeholders and public

health officials. Amid debates over how to address the surge in cases driven by the

omicron variant, confusion is now the most common reaction to shifts in

public health guidance: 60% of U.S. adults say they’ve felt confused as a

result of changes to public health officials’ recommendations on how to slow

the spread of the coronavirus, up 7 percentage points since last summer.

Americans are now almost evenly divided over how well public health

officials, such as those at the Centers for Disease Control and Prevention,

are responding to the outbreak, with about half (49%) saying they are doing

an only fair or poor job and half (50%) saying they are doing an excellent or

good job. Positive ratings of public health officials have fallen 10 points

since August and are well below ratings for their initial response to the

outbreak in early 2020. Evaluations of elected leaders at all levels of government have also

moved lower. A majority (60%) now describes the job Joe Biden is doing

responding to the coronavirus as only fair or poor. The share of Americans

who say Biden is doing an excellent or good job (40%) is down 7 points since

August and is now only slightly higher than the share who said Donald Trump

did an excellent or good job responding to the coronavirus outbreak over the

course of his presidency (36%). The new Pew Research Center survey finds that 78% of U.S. adults say

they have received at least one dose of a COVID-19 vaccine, including 73% who

say they are fully vaccinated – having received either two Pfizer or Moderna

vaccines or one Johnson & Johnson. Among fully vaccinated adults, 66% say

they’ve received an additional COVID-19 “booster shot” within the past six

months (this group makes up 48% of all U.S. adults). When it comes to the

decision to get a vaccine:

Among Republicans, the decision to get a vaccine, as well as broader

views on the outbreak, differ across key demographics and characteristics.

For instance, age and education strongly shape the vaccine decision among

Republicans:

With vaccines widely available, businesses and institutions are

grappling with whether to require proof of COVID-19 vaccination to

participate in a range of activities. The survey finds:

Partisan gaps on vaccine requirements are among the largest of any

seen in the survey. Majorities of Republicans oppose vaccine requirements for

all five activities listed in the survey, while majorities of Democrats favor

them. For instance, 76% of Democrats favor requiring proof of COVID-19

vaccination to attend a sporting event or concert, compared with just 26% of

Republicans. Not surprisingly, unvaccinated adults broadly oppose all vaccine

requirements, while those who have received a vaccine support most of these

measures. Views on vaccine requirements highlight how partisanship and vaccine

status are intertwined, yet both factors play a role shaping views. Among

Republicans, those who have received a vaccine are more open to vaccination

requirements than those who have not received a vaccine. On air travel, for

example, 43% of Republicans who have received a vaccine say they would favor

requiring proof of vaccination to travel by plane. Just 9% of Republicans who

have not received a vaccine favor this. One big change seen in the new survey is the increased comfort

Americans express around everyday activities. Large shares now say they are

comfortable visiting with close family and friends in their home (85%) and

going to the grocery store (84%). Majorities also say they feel comfortable

visiting a hair salon or barbershop (73%) or eating out in a restaurant

(70%). Comfort levels with most activities in the survey are roughly 20

percentage points higher than in November of 2020, before the availability of

COVID-19 vaccines in the U.S.

In part, these gaps in comfort tie to the finding that adults who

have not received a vaccine are less concerned

than vaccinated adults about getting a serious case of the coronavirus

themselves. This has been the case throughout the outbreak. Levels of

personal concern about the disease have been one of the core factors tied to

the decision of whether or not to get vaccinated since vaccines became widely

available. These are among the principal findings from Pew Research Center’s

survey of 10,237 U.S. adults conducted from Jan. 24 to 30, 2022, on the

coronavirus outbreak and Americans’ views of a COVID-19 vaccine. Vaccination rates among U.S. adults The rise in cases spurred by the omicron variant put renewed focus on

vaccination rates in the U.S. as well as the role booster shots play in

limiting the impacts from the coronavirus.

Overall, 78% of U.S. adults say they have received at least one dose

of a COVID-19 vaccine, including 73% who say they are fully vaccinated (5%

say they’ve received one shot, but need one more). According to the Centers

for Disease Control and Prevention (CDC), “fully vaccinated” means having

received two doses of Pfizer or Moderna vaccines or one dose of the Johnson

& Johnson. Two-in-ten U.S. adults say they have not received a vaccine for

COVID-19. These estimates generally align with other national public opinion

surveys, including those conducted by the Kaiser

Family Foundation. When it comes to booster shots, the current survey finds that 66% of

adults who are fully vaccinated against COVID-19 say they have also received a booster shot

within the last six months. This group makes up 48% of all U.S. adults. There continue to be sizable differences across groups in the shares

who say have received at least one

dose of a COVID-19 vaccine (78% of all U.S. adults).

Among the largest differences is partisan affiliation: Democrats and

those who lean to the Democratic Party are 26 percentage points more likely

than Republicans and Republican leaners to say they’ve received a COVID-19

vaccine (90% vs. 64%). White evangelical Protestants continue to be less likely than other

major religious groups to say they have gotten vaccinated for COVID-19. About

six-in-ten White evangelical Protestants (62%) have received at least one

dose of a COVID-19 vaccine, compared with 77% of White non-evangelical

Protestants, 80% of religiously unaffiliated adults and 85% of Catholics. Those with higher levels of education and income are more likely than

those with lower levels to say they have received a vaccine for COVID-19. And

those with health insurance are 16 points more likely than those without to

have gotten a vaccine. Some demographic differences in vaccination status are more

pronounced within one

partisan group than another. For instance, 80% of Republicans ages 65 and

older say they have received a COVID-19 vaccine, compared with far fewer

Republicans 18 to 29 (52%). There is a much more modest gap between the

shares of Democrats 65 and older and those 18 to 29 who say they’ve received

a vaccine (94% vs. 88%). See

the Appendix for more details on vaccination status within partisan

groups. Partisan differences in the share who’ve

received a booster shot or would be willing to do so every six months Among those who are fully vaccinated against COVID-19, Democrats and

Democratic leaners are more likely to say they’ve received a booster shot

within that last six months than Republicans and GOP leaners.

About three-quarters of fully vaccinated Democrats (73%) say they

have received a COVID-19 booster shot within the last six months. This group

makes up 62% of all Democrats. Among fully vaccinated Republicans, 55% say they have received a

COVID-19 booster shot within the last six months (33% of all Republicans). Public health experts are continuing to evaluate

whether to recommend regular COVID-19 booster shots.

The survey finds that 64% of adults who have received a COVID-19

vaccine say they would probably be willing to get a vaccine booster about

every six months, if public health officials recommended it; 35% of

vaccinated adults say they probably would not be willing to get a booster shot every six months

or so. Among adults who have received a COVID-19 vaccine, Democrats and

Democratic-leaning independents are far more likely than Republicans and

Republican leaners to say they’d be willing to get a booster shot regularly

(77% vs. 42%). High marks for hospitals and medical

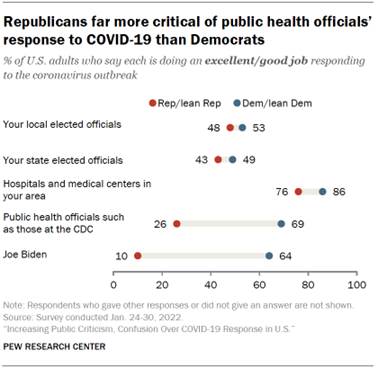

centers, but criticism of top officials’ COVID-19 response grows

A large majority of Americans (81%) continue to say hospitals and medical

centers in their area are doing an excellent or good job responding to the

coronavirus. Ratings are far less positive for the performance of public health

officials and elected officeholders at the state, local and federal level. Half of Americans now say public health officials, such as those at

the CDC, are doing an excellent or good job responding to the outbreak, down

from a high of 79% early in the outbreak and from 60% last August. The same share (50%) say their local elected officials are doing an

excellent or good job responding to the coronavirus outbreak, and 46% say

this about their state elected officials. Ratings for both groups are down

since August and are much lower than they were at earlier stages of the

outbreak. Four-in-ten say Joe Biden is doing an excellent or good job dealing

with the coronavirus, compared with 60% who say he is doing an only fair or

poor job. Positive ratings for Biden’s performance dealing with the

coronavirus have continued to decrease, down 7 percentage points since August

and 14 points since February 2021, shortly after his inauguration as

president. The share of Americans with a positive view of Biden’s handling of

the coronavirus outbreak is now nearing that for Trump after he left office

(36%).

Republicans are especially critical of the response to the

coronavirus outbreak by public health officials. Just 26% of Republicans and

Republican leaners say public health officials, such as those at the CDC, are

doing an excellent or good job; a majority (73%) say they are doing an only

fair or poor job. By contrast, 69% of Democrats and Democratic leaners rate

the job health officials are doing as excellent or good. This contrasts with views of public health officials measured in the

early stages of the coronavirus outbreak. For instance, in May of 2020,

during Trump’s administration, 68% of Republicans and 75% of Democrats said

public health officials were doing an excellent or good job responding to the

outbreak.

Partisans continue to offer starkly different ratings of Biden’s

response to the coronavirus outbreak: 64% of Democrats now say he is doing an

excellent or good job, while 89% of Republicans say instead that he is doing

an only fair or poor job. Partisan gaps are more modest in ratings of state and local elected

officials, and majorities of both Republicans (76%) and Democrats (86%) say

hospitals and medical centers in their area are doing an excellent or good

job responding to the coronavirus outbreak. Changing public health guidance sparks confusion,

concern Americans have encountered a number of changes to public health

guidelines about how to slow the spread of the coronavirus in the U.S. over

the past two years.

When asked how they’ve felt about these changes, confusion is the top

reaction Americans express: 60% say they have felt confused by changes in

recommendations on how to slow the spread of the coronavirus, up 7 percentage

points from the share who said this in August 2021. Nearly as many (57%) say changes in health officials’ recommendations

on how to slow the spread made them wonder if public health officials were

holding back important information. And 56% say it made them feel less

confident in the recommendations. The share saying they’ve felt less

confident in public health officials’ recommendations is up 5 points since

August. Changing health guidance has also prompted some positive reactions

from the public: 56% say they’ve felt that these changes made sense because

scientific knowledge is always being updated. Still, the share who say

they’ve felt this way is down 5 points since last summer. Fewer Americans

(43%) say changes to health officials’ recommendations on how to slow the

spread of the coronavirus made them feel reassured that officials were

staying on top of new information, down 8 points since August. Vaccinated adults express much more positive reactions to changing

public health guidance on how best to slow the spread of the coronavirus than

adults who have not received a vaccine. Partisan affiliation also strongly

shapes views, with Democrats taking a more positive view of changes in

recommendations than Republicans.

Two-thirds (66%) of adults who have received a COVID-19 vaccine say

changes in recommendations have made sense because scientific knowledge is

always being updated; just 26% of adults who have not received a vaccine

express this view. Negative reactions register more widely with adults who have not

received a vaccine than those who have. Still, 50% of vaccinated adults say

changes in guidance on how to slow the spread of the coronavirus have made

them less confident in health officials’ recommendations, and 58% say they’ve

made them feel confused. Democrats and Democratic leaners are 38 points more likely than

Republicans and Republican leaners to say changes in officials’ coronavirus

recommendations have made sense because scientific knowledge is always being

updated (74% vs. 36%). About three-quarters of Republicans say changes in

guidance have made them wonder if public health officials were holding back

important information and made them less confident in health officials’

recommendations (about four-in-ten Democrats express each of these

reactions). The partisan gap is more modest when it comes to confusion: 69% of

Republicans and 53% of Democrats say they’ve felt confused due to changes in

public health officials’ coronavirus recommendations. Americans now more comfortable with a range

of daily activities

Americans are now much more comfortable with a range of daily

activities than they were in November 2020, before the availability of

COVID-19 vaccines in the U.S. Most Americans (85%) now say they feel comfortable visiting with a

close friend or family member inside their home, up 20 percentage points from

the share who said this in November 2020. About as many (84%) say they feel

comfortable going to the grocery store. Majorities also say they are now comfortable going to a hair salon or

barbershop (73%) or eating out in a restaurant (70%). In late 2020, far

smaller shares of Americans felt comfortable doing these activities (53% and

44%, respectively). Still, fewer than half say they feel comfortable attending an indoor

sporting event or concert (43%) or a crowded party (34%), though these

percentages have risen substantially since November 2020. The 20% of U.S. adults who have not received a vaccine are less

likely than vaccinated adults to see the coronavirus outbreak as a major

threat to their own personal health. Consistent with lower levels of concern,

unvaccinated adults tend to express more comfort

with public activities than those who have received a COVID-19 vaccine.

For example, about six-in-ten (62%) of those who are not vaccinated

say they feel comfortable attending an indoor sporting event or concert,

compared with 37% of vaccinated adults. Unvaccinated adults are 29 points

more likely than vaccinated adults to say they’re comfortable attending a

crowded party and somewhat more likely to say they’re comfortable eating in a

restaurant and going to a hair salon or barbershop. Large shares of both vaccinated and unvaccinated adults now say

they’re comfortable visiting with a close friend or family member inside

their home and going to the grocery store.

Partisan affiliation also shapes views on this question, with

Republicans and those who lean to the Republican Party more likely than

Democrats and Democratic-leaning independents to say they feel comfortable

engaging in a variety of activities. A majority of Republicans (62%) say they are comfortable attending an

indoor sporting event or concert, compared with about three-in-ten Democrats

(27%). There’s a similar gap in comfort with attending a crowded party. Large shares of both Republicans and Democrats say they are

comfortable visiting with a close friend or family member inside their home

or going to the grocery store, though the size of the majority is about 10

points higher among Republicans than Democrats in both cases. Mask wearing increased with the arrival of

the omicron variant A separate early-January survey found the share of U.S. adults who

say they have worn a mask all or most of the time in stores and businesses

over the last month increased from 53% in August of 2021 to 61% in January.

Those who have received a COVID-19 vaccine (70%) continue to be far more likely

than those who have not (32%) to say they’ve been wearing a mask in public

places regularly. See

Appendix for more details. Majority of Americans favor vaccine requirement

for air travel, but not for shopping or dining

A majority of U.S. adults (58%) favor requiring proof of COVID-19

vaccination before being allowed to travel by air. Slightly more Americans favor (53%) than oppose (46%) a vaccine

requirement to go to a sporting event or concert. By 52% to 47%, more also favor than oppose requiring proof of

COVID-19 vaccination for attending public colleges and universities in

person. Support for this proposal is 5 percentage points lower than it was in

August of 2021. Americans lean against requiring proof of vaccination to eat inside

of a restaurant (53% oppose, 46% favor), and 59% oppose requiring proof of

vaccination to shop inside stores and businesses. Support for both of these

proposals has also declined slightly since last summer.

Unsurprisingly, Americans who have not received a coronavirus vaccine

are overwhelmingly against vaccine requirements, with around eight-in-ten or

more opposing each of these measures. There continue to be large partisan differences in how Americans view

vaccination requirements. Majorities of Democrats favor requiring proof of

vaccination status to do each of the five activities listed, while majorities

of Republicans oppose requirements in each of these cases. For example, eight-in-ten Democrats and independents who lean toward

the Democratic Party favor requiring those traveling by airplane to show

proof of vaccination, while only about three-in-ten (31%) Republicans and

Republican leaners say they favor this.

Among Republicans, opposition to vaccine requirements is far more

widespread among those who have not received a COVID-19 vaccine than among

those who have. For instance, 43% of vaccinated Republicans favor requiring

proof of COVID-19 vaccination for air travel, compared with just 9% of

unvaccinated Republicans who say this. (Overall, 64% of Republicans and

Republican leaners have received at least one dose of a COVID-19 vaccine; 33%

have not.) (PEW) FEBRUARY 9, 2022 729-43-13/Polls Two-Thirds Of Black Protestants (65%) Approve Of The Job That Biden

Is Doing As President

About a year into his presidency, Joe Biden’s job

approval rating is much lower among the U.S. public overall – and

among most demographic groups – than it was in the early months of his

administration. The changes in Biden’s job ratings also are evident among

several Christian subgroups and religiously unaffiliated Americans. While his

rating continues to be low among White Christians, especially White

evangelical Protestants, there have been sizable declines in positive ratings

from Black Protestants and the religiously unaffiliated – two groups that are

among the Democratic Party’s most

loyal constituencies. Roughly two-thirds of Black Protestants (65%) approve of the job that

Biden is doing as president, according to a Pew

Research Center survey conducted Jan. 10-17. That is down sharply

from 92% in March 2021, shortly after he took office.

Religiously unaffiliated adults also are increasingly skeptical about

Biden’s job performance. Today, 47% of religious “nones” – respondents who

describe their religious identity as atheist, agnostic or “nothing in

particular” – approve of Biden’s performance, down from 71% in April 2021 and

65% in March 2021. The share of “nones” who now approve of Biden is the

lowest it has been since his inauguration, falling below the previous low of

55% in September 2021. Although the surveys analyzed here include respondents from many

religious backgrounds, including Jews, Muslims, Hindus, Buddhists and others,