BUSINESS & POLITICS IN THE

MUSLIM WORLD

Global Opinion Report No. 488

June 04 - 10, 2017

Contents

Visegrad Four Poll Reveals Vulnerabilities

to Russian Influence

Ukraine Poll: Majority Want Donbas to

Remain in Ukraine

Russia: Saved on clothes and vacation but

lashed out on household appliances and smartphones

UK: Ipsos MORI Final Election Poll 2017

Final call poll: Tories lead by seven

points and set to increase majority

The local vs the national: the NHS comes

into conflict with Brexit in terms of voters’ priorities

UK: Sizing blunders won’t impact brand

perception despite media backlash

Majority of Londoners trust Sadiq Khan to

make the right decisions on terrorism

Is the NHS Labour’s secret weapon in the

election?

Confidence in Economy in May Lowest Since

November 2016

Democratic Edge in Party Affiliation Up to

Seven Points

Exchange Purchasers Rate Health Coverage

Less Positively

US Abortion Attitudes Stable; No Consensus

on Legality

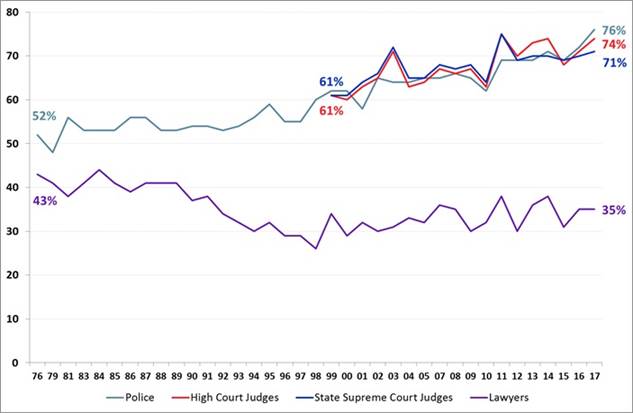

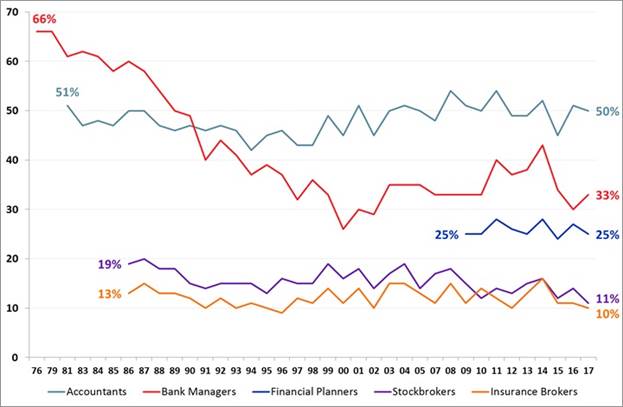

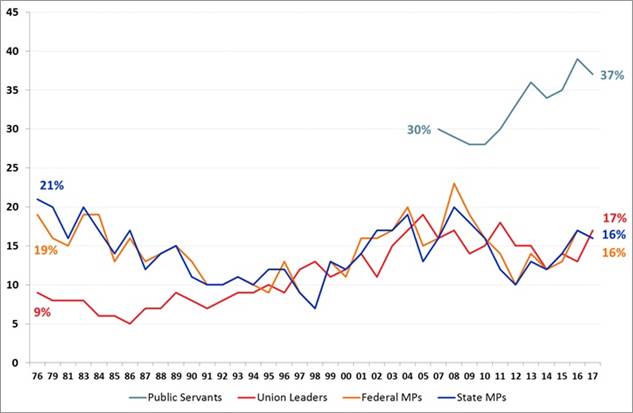

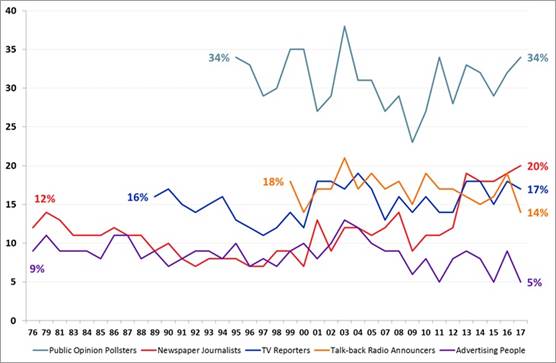

Roy Morgan Image of Professions Survey 2017

Over 2.6 million Australians were

unemployed or under-employed in May

Number Of Potential

Migrants Worldwide Tops 700 Million

Global Publics More Upbeat About the

Economy

The Internet of Things Connectivity Binge:

What Are the Implications?

INTRODUCTORY NOTE

This week report

consists of eighteen surveys, three of these are multi-country studies while

the rest are national surveys from different states across the globe.

488-43-19

Commentary: Number Of Potential Migrants Worldwide Tops 700 Million

Number Of Potential Migrants Worldwide Tops 700

Million

WASHINGTON,

D.C. -- After cooling off in the wake of the Great Recession, worldwide,

people's desire to migrate permanently to another country showed signs of

rebounding between 2013 and 2016. Gallup found 14% of the world's adults --

which translates to nearly 710 million people -- saying they would like to move

to another country if they had the opportunity. This is up from 13% -- or about

630 million adults -- between 2010 and 2012.

WASHINGTON,

D.C. -- After cooling off in the wake of the Great Recession, worldwide,

people's desire to migrate permanently to another country showed signs of

rebounding between 2013 and 2016. Gallup found 14% of the world's adults --

which translates to nearly 710 million people -- saying they would like to move

to another country if they had the opportunity. This is up from 13% -- or about

630 million adults -- between 2010 and 2012.

JUNE 8, 2017

Global Desire to Migrate Rebounds in

Some Areas

Percentage of those who live in

these regions who desire to migrate

|

Desire to migrate,2010-2012 |

Desire to migrate,2013-2016 |

Change |

|

|

% |

% |

pct. pts. |

|

|

Sub-Saharan Africa |

30 |

31 |

+1 |

|

Europe (outside European Union) |

21 |

27 |

+6* |

|

Latin America and Caribbean |

18 |

23 |

+5* |

|

Middle East and North Africa |

19 |

22 |

+3* |

|

European Union |

20 |

21 |

+1* |

|

Commonwealth of Independent States |

15 |

14 |

-1 |

|

Australia/New Zealand/Oceania |

9 |

10 |

+1 |

|

Northern America |

10 |

10 |

0 |

|

South Asia |

8 |

8 |

0 |

|

East Asia |

8 |

7 |

-1 |

|

Southeast Asia |

7 |

7 |

0 |

|

Global |

13 |

14 |

+1* |

|

Latest estimate based on World

Poll surveys in 156 countries and areas between 2013 and 2016; * =

Significant change |

|||

|

GALLUP WORLD POLL |

|||

Gallup's latest findings on adults'

desire to move to other countries are based on a rolling average of interviews with

586,806 adults in 156 countries between 2013 and 2016. The 156 countries

represent 98% of the world's adult population. The analysis period overlaps the

years of the European migrant crisis that began in 2015. The previous findings were

based on a rolling average of interviews with 521,182 adults in 154 countries

between 2010 and 2012.

While still not back at the 16%

Gallup measured worldwide between 2007 and 2009,

the desire to migrate has increased in a number of regions as global economic

conditions have continued to slowly recover and as conflict, famine and

disaster have driven people from their homes in some parts of the world. Desire

increased the most in non-European Union countries in Europe, in Latin America

and the Caribbean, and in the Middle East and North Africa.

Yet in other places, desire has not

changed much at all. In all regions of Asia, for example, the percentage of

adults who would like to move to another country permanently remained flat. The

10% of adults in Northern America -- the U.S. and Canada together -- who would

like to migrate also was unchanged. And in sub-Saharan Africa, where residents

remain the most likely worldwide to express the desire to migrate permanently,

desire hovered near 30%.

In 31 countries and areas throughout

the world, at least three in 10 adults say they would like to move permanently

to another country if they could. These countries and areas are found in every

region except Asia, Oceania and Northern America. In many of these populations,

desire to migrate has increased significantly, likely pushed higher for a host

of reasons -- for example, the civil war in Syria, chronic high unemployment

rates in Albania and Italy, and the Ebola outbreak in Sierra Leone.

Highest Desire to Migrate

Percentage of the total adult

population that wants to migrate

|

Desire to migrate,2010-2012 |

Desire to migrate,2013-2016 |

|

|

% |

% |

|

|

Sierra Leone |

51 |

62* |

|

Haiti |

53 |

56 |

|

Albania |

36 |

56* |

|

Liberia |

53 |

54 |

|

Congo (Kinshasa) |

37 |

50* |

|

Dominican Republic |

49 |

50 |

|

Honduras |

41 |

48* |

|

Armenia |

40 |

47* |

|

Syria |

32 |

46* |

|

El Salvador |

34 |

46* |

|

Ghana |

40 |

45 |

|

Nigeria |

41 |

43 |

|

Jamaica |

43 |

40 |

|

Congo (Brazzaville) |

38 |

39 |

|

Togo |

41 |

39 |

|

Sudan |

29 |

37 |

|

Guinea |

33 |

36 |

|

Bosnia and Herzegovina |

20 |

36* |

|

Puerto Rico |

N/A |

35 |

|

Moldova |

32 |

35 |

|

Senegal |

31 |

34 |

|

Gabon |

30 |

34 |

|

Macedonia |

35 |

34 |

|

Kosovo |

29 |

34 |

|

Uganda |

37 |

33 |

|

Italy |

21 |

32* |

|

Cyprus |

25 |

32* |

|

Guatemala |

30 |

31 |

|

Ivory Coast |

N/A |

30 |

|

Lesotho |

25 |

30 |

|

Peru |

32 |

30 |

|

* Significant change |

||

|

GALLUP WORLD POLL |

||

U.S. Still Top Desired Destination

for Potential Migrants

The U.S. continues to be the most

desired destination country for potential migrants, as it has since Gallup

started tracking these patterns a decade ago. One in five potential migrants

(21%) -- or about 147 million adults worldwide -- name the U.S. as their

desired future residence. Germany, Canada, the United Kingdom, France,

Australia and Saudi Arabia appeal to at least 25 million adults each. These

same countries have been top desired destinations for the past 10 years. In

fact, roughly 20 countries attract more than two-thirds of all potential

migrants worldwide.

Top Desired Destinations Worldwide

Among those who say they would like

to move

|

% Potential migrants naming this

country |

Estimated number of adults (in

millions) |

|

|

United States |

21 |

147 |

|

Germany |

6 |

39* |

|

Canada |

5 |

36 |

|

United Kingdom |

5 |

35* |

|

France |

5 |

32 |

|

Australia |

4 |

30 |

|

Saudi Arabia |

3 |

25* |

|

Spain |

3 |

20 |

|

Italy |

2 |

15 |

|

Switzerland |

2 |

13 |

|

Japan |

2 |

12 |

|

United Arab Emirates |

2 |

12* |

|

Singapore |

1 |

10 |

|

South Africa |

1 |

8 |

|

Sweden |

1 |

8 |

|

Russia |

1 |

7 |

|

New Zealand |

1 |

7 |

|

China |

1 |

7 |

|

Netherlands |

1 |

6 |

|

Brazil |

1 |

6 |

|

Turkey |

1 |

5* |

|

South Korea |

1 |

5 |

|

* = Significant change |

||

|

GALLUP WORLD POLL, 2013-2016 |

||

While the number of potential

migrants who say they would like to move to the U.S. hasn't changed

significantly from previous years, the number who say the same about Germany

has risen from 28 million to 39 million in the most recent analysis period. This

increase coincides with the height of Europe's migrant crisis between 2015 and

2016 -- during which Germany's Chancellor Angela Merkel promised there would be

"no limit" to the number of refugees her country would accept.

The United Kingdom, on the other hand,

lost some of its appeal as a desired destination, as immigration became one of

the driving forces behind the country's eventual "Brexit" in

mid-2016. Approximately 35 million potential migrants named the United Kingdom

as a desired destination between 2013 and 2016, down from about 43 million

between 2010 and 2012.

Bottom Line

After tailing off shortly after the

Great Recession, the desire to migrate inched back upward in a number of

regions, likely reflecting an improving economic climate that can make the idea

of leaving one's own country less risky to entertain. But it also could reflect

the increasing unrest in some parts of the world, where war, famine, disaster

and disease are making it impossible for people to stay.

In the most recent analysis period,

the U.S. remained the top desired destination for potential migrants, as it has

for the past decade that Gallup has been measuring these attitudes. It is

possible that the U.S. will lose some of its allure under the new Trump

presidential administration, which aims to make it tougher for migrants to come

to the United States and for existing migrants to stay. It is evident from the

changes in the numbers of potential migrants who would like to move to Germany

and the United Kingdom that a government's stance and policy toward immigration

can contribute to the country's being more attractive or less attractive to

potential migrants.

Dato Tsabutashvili contributed to

this article.

SURVEY METHODS

Results are based on aggregated

telephone and face-to-face interviews with 586,806 adults, aged 15 and older,

in 156 countries from 2013 to 2016. The 156 countries surveyed represent 98% of

the world's adult population. One can say with 95% confidence that the margin

of sampling error for the entire sample, accounting for weighting and sample

design, is less than ±1 percentage point.

Source: http://www.gallup.com/poll/211883/number-potential-migrants-worldwide-tops-700-million.aspx?g_source=world&g_medium=newsfeed&g_campaign=tiles

SUMMARY OF POLLS

EAST EUROPE

Visegrad

Four Poll Reveals Vulnerabilities to Russian Influence

A poll of

residents in the Czech Republic, Hungary, Poland and Slovakia released by the

International Republican Institute’s (IRI) Center for Insights in Survey

Research indicates waning commitment to Euro-Atlantic institutions and

vulnerabilities to Russian influence.

The four countries surveyed were chosen because of their status as the

“Visegrad Four (V4),” an alliance of young European Union members committed to

increasing cooperation on shared interests.

(IRI)

MAY 24, 2017

Ukraine

Poll: Majority Want Donbas to Remain in Ukraine

A new poll by

the International Republican Institute’s (IRI) Center for Insights in Survey

Research reveals that an overwhelming majority of Ukrainians think the war-torn

Donbas region should remain part of Ukraine. The survey contained an

over-sample of respondents from the Ukrainian-controlled areas of the Donbas, a

majority of whom also affirmed their wish for the entire region to stay in

Ukraine. (IRI)

JUNE 7, 2017

Russia:

Saved on clothes and vacation but lashed out on household appliances and

smartphones

In spite of

Russians’ statements about driving for the economy, they don’t refuse to make

big-budget purchases. In comparison with the previous year only the share of

those who has purchased clothes and shoes has drastically decreased. Only one

percent less Russians than last year splashed out on the entertainment and

vacation. (ROMIR)

June 06, 2017

WEST EUROPE

UK:

Ipsos MORI Final Election Poll 2017

Ipsos MORI’s

final election poll for the Evening Standard indicates that Theresa May and the

Conservatives are on course to win the 2017 General Election. (Ipsos Mori)

June 08, 2017

Final

call poll: Tories lead by seven points and set to increase majority

Labour won the

battles of the election campaign, but the Conservatives still look almost

certain to win the war. The final call poll for the Times has voting intention

figures of CON 42%, LAB 35%, LDEM 10%, UKIP 5%. (YouGov)

June 07, 2017

The

local vs the national: the NHS comes into conflict with Brexit in terms of

voters’ priorities

With the

Conservatives adopting a campaign on Brexit and other national issues, and many

Labour candidates adopting an exclusively local approach, YouGov looks at how

the public’s national vs local perspectives differ. (YouGov)

June 7, 2017

UK:

Sizing blunders won’t impact brand perception despite media backlash

Over the last

couple of weeks, two high-profiles fashion brands have encountered criticism

for the way they labelled women’s clothing. (YouGov)

June 07, 2017

Majority

of Londoners trust Sadiq Khan to make the right decisions on terrorism

While Donald

Trump may criticise Khan, Londoners trust their mayor more than they trust

Theresa May or Jeremy Corbyn on terrorism. (YouGov)

June 05, 2017

Is

the NHS Labour’s secret weapon in the election?

The NHS remains

a key election battleground. In Ipsos MORI’s Political Monitor, the public say

that the NHS and the EU/Brexit are the main issues that will help them decide

which party to vote for at the election (43% and 42% respectively). (Ipsos Mori)

June 08, 2017

NORTH AMERICA

Confidence

in Economy in May Lowest Since November 2016

WASHINGTON, D.C.

-- Though still historically high, Americans' confidence in the economy fell to

a six-month low in May, largely dragged down by Democrats' worsening economic

attitudes. Gallup's U.S. Economic Confidence Index averaged a score of +3 in

May, down slightly from April (+5) but eight points below January's record

monthly high (+11). (Gallup USA)

JUNE 6, 2017

Democratic

Edge in Party Affiliation Up to Seven Points

WASHINGTON, D.C.

-- In an encouraging sign for the Democratic Party's election prospects in

2018, its edge in party affiliation over the Republican Party has grown to

seven percentage points, the largest it has been in over two years. During the

late summer and fall of 2016, Democrats averaged a three-point advantage.

(Gallup USA)

JUNE 6, 2017

Exchange

Purchasers Rate Health Coverage Less Positively

WASHINGTON, D.C.

-- U.S. adults who purchased their health insurance coverage through a federal

or state healthcare exchange -- about 15% of those who report having insurance

-- rate the quality of their coverage lower than do those who purchased their

coverage via another source. Both groups are generally positive about their

insurance, but the 74% of exchange purchasers who consider the quality of their

coverage to be "excellent" or "good" is marginally lower

than the 81% of those whose coverage stems from another source who say the

same. (Gallup USA)

JUNE 8, 2017

US

Abortion Attitudes Stable; No Consensus on Legality

WASHINGTON, D.C.

-- Stability remains the name of the game in U.S. abortion attitudes. Half of

Americans say abortion should be "legal only under certain

circumstances," identical to a year ago, while 29% still say it should be

legal in all circumstances. The smallest proportion -- 18% this year vs. 19% in

2016 -- say it should be illegal in all circumstances. (Gallup USA)

JUNE 9, 2017

AUSTRALASIA

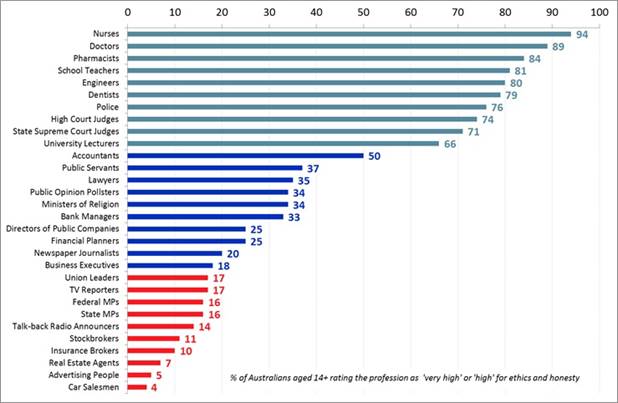

Roy

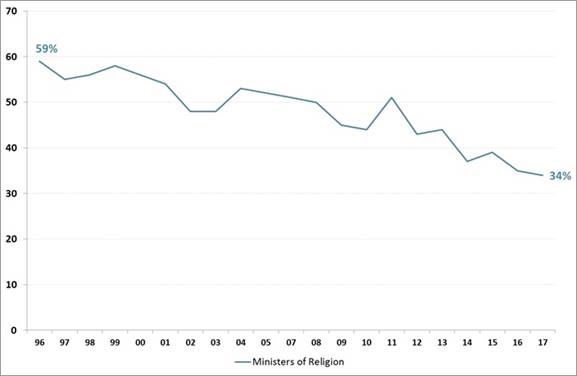

Morgan Image of Professions Survey 2017

Health

professionals have continued their domination of Australia’s most highly

regarded professions with 94% of Australians (up 2% from 2016) rating Nurses

‘very high’ or ‘high’ for their ‘ethics and honesty’. Nurses have topped the

annual survey for 23 years running since being included for the first time in

1994. (Roy Morgan)

June 07 2017

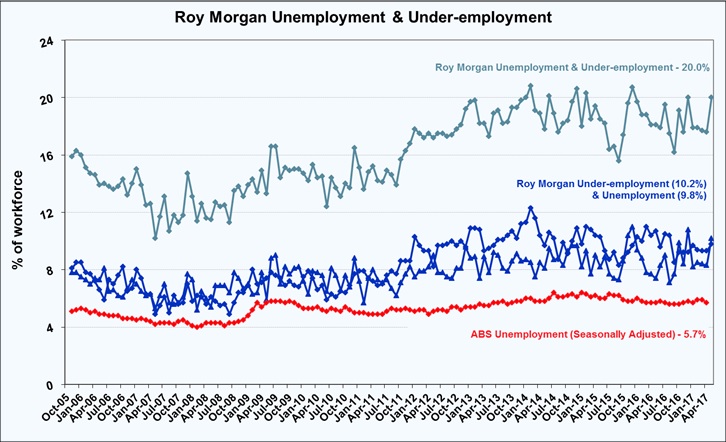

Over

2.6 million Australians were unemployed or under-employed in May

Australia’s real

unemployment for May was 9.8% (1.284 million Australians looking for work). In

addition 1.338 million Australians were under-employed in May (10.2% of the

workforce). This is a total of 2.622 million Australians (20% of the workforce)

looking for work or looking for more work. (Roy Morgan)

June 09 2017

MULTI-COUNTRY

STUDIES

Number

Of Potential Migrants Worldwide Tops 700 Million

WASHINGTON, D.C.

-- After cooling off in the wake of the Great Recession, worldwide, people's

desire to migrate permanently to another country showed signs of rebounding

between 2013 and 2016. Gallup found 14% of the world's adults -- which

translates to nearly 710 million people -- saying they would like to move to

another country if they had the opportunity. This is up from 13% -- or about

630 million adults -- between 2010 and 2012. (Pew Research Center)

JUNE 8, 2017

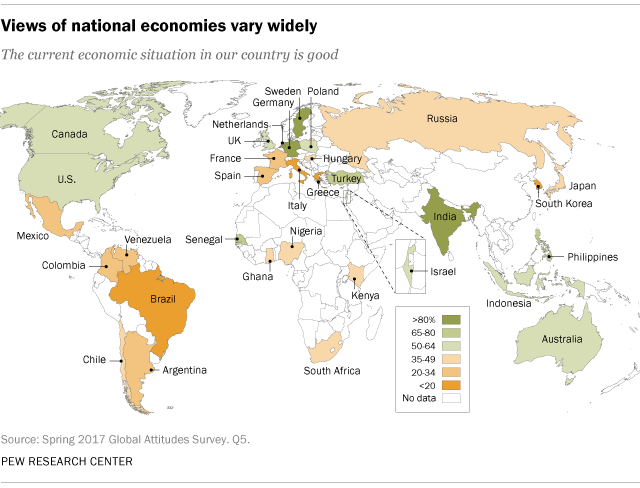

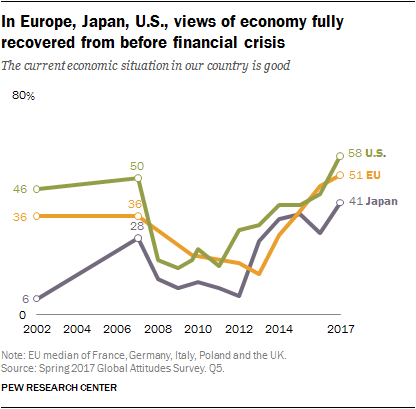

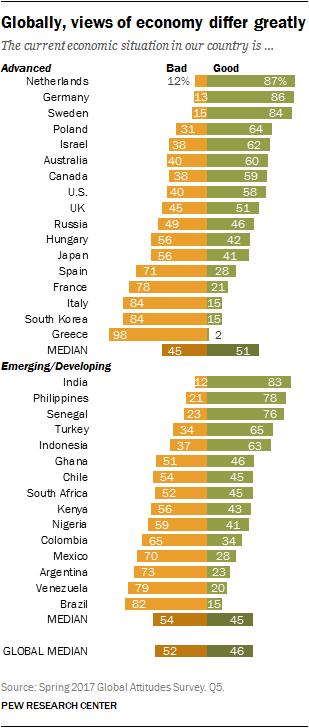

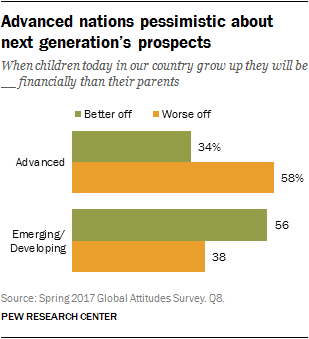

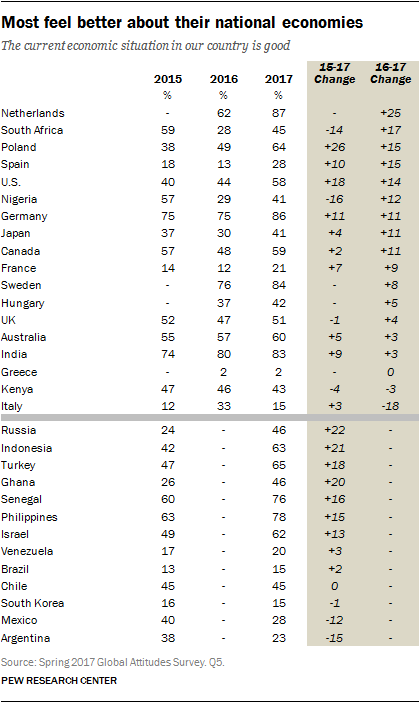

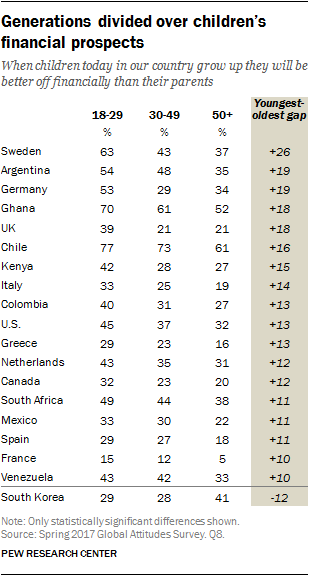

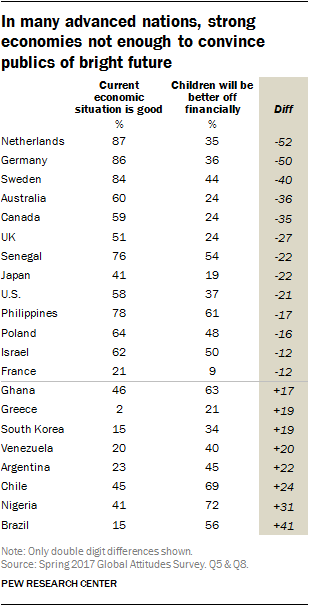

Global

Publics More Upbeat About the Economy

Nearly a decade

after the worst economic downturn since the Great Depression, economic spirits

are reviving. Many Europeans, Japanese and Americans feel better today about

their economies than they did before the financial crisis. More broadly, in 11

of 18 countries from across the globe that were surveyed in both 2016 and 2017,

publics feel more positive about their economy than they did a year ago. (Pew

Research Center)

JUNE 8, 2017

CYBER WORLD

The

Internet of Things Connectivity Binge: What Are the Implications?

Despite wide

concern about cyberattacks, outages and privacy violations, most experts

believe the Internet of Things will continue to expand successfully the next

few years, tying machines to machines and linking people to valuable resources,

services and opportunities. (Pew Research Center)

JUNE

6, 2017

EAST EUROPE

488-43-1/Multi-country

study

Visegrad Four Poll Reveals Vulnerabilities to Russian Influence

A poll of residents

in the Czech Republic, Hungary, Poland and Slovakia released by the

International Republican Institute’s (IRI) Center for Insights in Survey

Research indicates waning commitment to Euro-Atlantic institutions and

vulnerabilities to Russian influence. The four countries surveyed were

chosen because of their status as the “Visegrad Four (V4),” an alliance of

young European Union members committed to increasing cooperation on shared interests. (IRI)

MAY 24, 2017

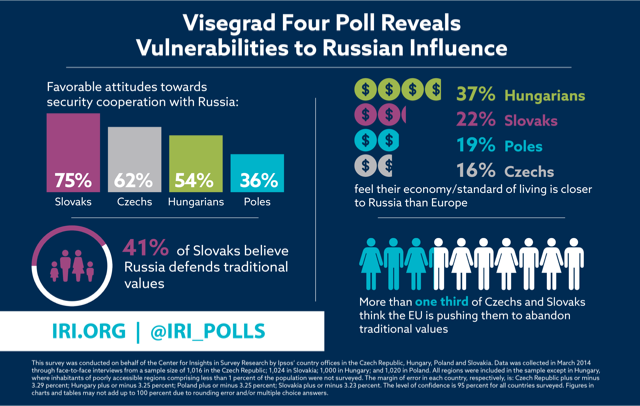

“This poll reveals a number of disturbing trends in the heart of Europe, including waning support for core transatlantic institutions like NATO, tensions over the nature of European identity, and discontent with socioeconomic challenges,” said Jan Surotchak, IRI Regional Director for Europe. “After investing twenty years and hundreds of millions of dollars in building a ‘Europe Whole and Free,’ it is vital that the U.S. recognize the threat of increased Russian influence in Europe, which has the potential to undermine a key pillar of transatlantic peace and security.”

While NATO and the U.S. presence in Europe have historically been cited as a key pillar of European peace and security, in Slovakia an alarming 60 percent of respondents feel that the U.S. presence increases tensions and insecurity. A majority of respondents in all four countries either strongly or somewhat support neutrality towards both NATO and Russia (Slovakia: 73 percent; Czech Republic: 61 percent; Hungary: 58 percent; Poland: 53 percent). Seventy-five percent of Slovaks believe that Russia should be a security partner, followed by 59 percent of Czechs, 54 percent of Hungarians, and 35 percent of Poles.

The survey also reveals ambivalence about the nature of European identity. More than one-third of respondents in the Czech Republic (40 percent) and Slovakia (36 percent) feel that the European Union is pushing them to abandon traditional values, while 41 percent of Slovaks believe that “Russia has taken the side of traditional values” (Czech Republic: 27 percent; Hungary: 18 percent; Poland: 14 percent).

Reflecting dissatisfaction with the state of the economy and public services, a significant portion of respondents feel that their socioeconomic status is closer to that of Russia than Europe. Thirty-nine percent of Hungarians think that their social benefits have more in common with Russia than Europe, followed by 26 percent in Slovakia, 24 percent in Poland and 15 percent in the Czech Republic. Similarly, 37 percent of Hungarians say that their economy and standard of living is more akin to Russia’s than Europe (Slovakia: 22 percent; Poland: 19 percent; Czech Republic: 16 percent).

In addition to the widening number of respondents who identify with Russia on key issues such as identity, the poll also indicates vulnerability to Russian disinformation among respondents who get their news from nontraditional media outlets. In Slovakia, a combined 76 percent either do not believe that Russia is engaged in efforts to mislead people (38 percent), or do not care if Russia funds these outlets (38 percent).

This multinational poll was commissioned as part of IRI’s Beacon Project, an initiative that equips European stakeholders with the tools to counter Russian disinformation and meddling more effectively. "These results correspond closely with data from the Beacon Project's >versus< media monitoring tool, which has revealed a correlation between socio-economic disparities within the V4 countries and vulnerabilities to Russian influence,” said IRI Regional Program Director Miriam Lexmann. “With its data-driven approach, the Beacon Project helps European political and civil society leaders to address vulnerabilities that the Kremlin seeks to exploit.”

Methodology

This survey was conducted on behalf of the Center for Insights in Survey Research by Ipsos’ country offices in the Czech Republic, Hungary, Poland and Slovakia, respectively. Data was collected in early march through face-to-face interviews from a sample size of 1,016 in the Czech Republic; 1,024 in Slovakia; 1,000 in Hungary; and 1,020 in Poland. All regions were included in the sample except in Hungary, where inhabitants of poorly accessible regions comprising less than 1 percent of the population were not surveyed. The margin of error in each country, respectively, is: Czech Republic plus or minus 3.29 percent; Hungary plus or minus 3.25 percent; Poland plus or minus 3.25 percent; Slovakia plus or minus 3.23 percent. The level of confidence is 95 percent for all countries surveyed. Figures in charts and tables may not add up to 100 percent due to rounding error and/or multiple choice answers.

488-43-2/POLL

Ukraine Poll: Majority Want Donbas to Remain in Ukraine

A new poll by the

International Republican Institute’s (IRI) Center for Insights in Survey

Research reveals that an overwhelming majority of Ukrainians think the war-torn

Donbas region should remain part of Ukraine. The survey contained an

over-sample of respondents from the Ukrainian-controlled areas of the Donbas, a

majority of whom also affirmed their wish for the entire region to stay in

Ukraine. (IRI)

JUNE 7, 2017

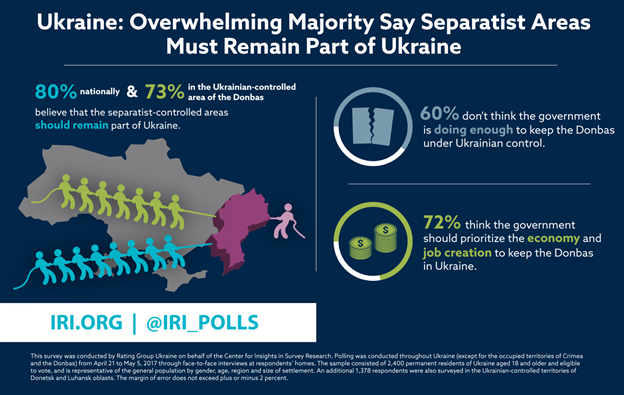

“Three years into the ongoing conflict in eastern Ukraine, which has claimed the lives of 10,000 and displaced more than 1.7 million people, Ukrainians are resolute in their desire to restore their territorial integrity and their rejection of the illegal occupation by Russian-backed separatists,” said IRI Regional Director for Eurasia Stephen Nix. “This data is critical, as it suggests that the Ukrainian people will not accept the division of their country.”

A combined 80 percent of Ukrainians nationwide and a combined 73 percent in the Donbas region believe that separatist-controlled areas of the Donbas should remain under Ukrainian control. Only six percent nationwide and four percent in the Donbas believe that these areas should either be separated from Ukraine or become part of Russia.

Despite this consensus on the future of the Donbas, a combined 60 percent of those surveyed in the Donbas do not feel that the government is taking sufficient steps to retain control of the liberated areas of the region. Only a combined 10 percent in the Donbas believe the authorities are doing enough—a 14 percent decrease since IRI’s previous oversample of the region in November 2015.

Seventy-two percent of Donbas residents cited job creation and economic improvements as the best ways to keep the Donbas part of Ukraine. “This represents a clear call to action for Ukrainian authorities,” Nix said. “Citizens in the Donbas must be made to feel that they can expect to enjoy a more stable and prosperous future as part of Ukraine. Improving the quality of life of citizens will yield greater stability for the region in the long term.”

Methodology

This survey was conducted by Rating Group Ukraine on behalf of the Center for Insights in Survey Research. Polling was conducted throughout Ukraine (except for the occupied territories of Crimea and the Donbas) from April 21 to May 5, 2017 through face-to-face interviews at respondents’ homes. The sample consisted of 2,400 permanent residents of Ukraine aged 18 and older and eligible to vote, and is representative of the general population by gender, age, region and size of settlement. An additional 1,378 respondents were also surveyed in the Ukrainian-controlled territories of Donetsk and Luhansk oblasts.

The margin of error does not exceed plus or minus 2 percent. The average response rate was 64.2 percent. Charts and graphs may not add up to 100 percent due to rounding. This survey was funded by the Government of Canada.

488-43-3/POLL

Russia: Saved on clothes and vacation but lashed out on household appliances and smartphones

In spite of Russians’ statements about

driving for the economy, they don’t refuse to make big-budget purchases. In

comparison with the previous year only the share of those who has purchased

clothes and shoes has drastically decreased. Only one percent less Russians

than last year splashed out on the entertainment and vacation. (ROMIR)

June 06, 2017

On another expenditure side the increase was observed, especially in

household appliances and electronics, smartphone and tablet purchases, in

purchase and service of a vehicle, in apartment, house and summer house

purchases. The respondents traditionally show the modesty in plans on tangible

expenditures in the next months. This isn’t, however, about an overwhelming

economy as it was two years ago. Even more, the share of Russians who are going

to lash out on holiday trips has increased.

This April within the regular all-Russian opinion poll Romir research holding asked respondents about big-budget purchases they’ve made within the period of the last six months and they are going to make in the following six months. Such polls have been held since 2011 what helps to monitor the dynamics of big-budget purchases of Russians.

Let us recall that two years ago when the crisis began Russians made loud statements about the intention to the overwhelming economy. According to the result of the last year poll, the overwhelming economy wasn’t realized. In 2016 only the share of those who purchased apartments, vehicles and jewelry decreased. On another expenditure side the increase was observed.

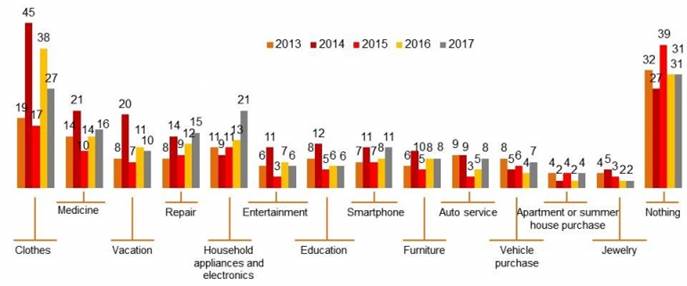

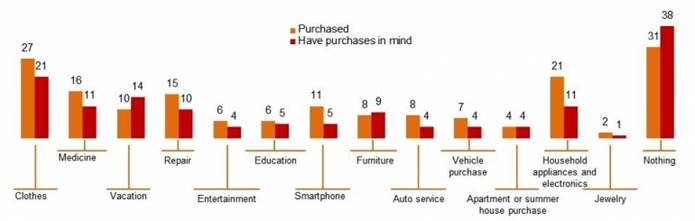

According to the results of the poll, it has emerged that however hard and crisis Russians called 2016, it hasn’t had a significant impact on making big-budget purchases (see Diagram 1).

Diagram 1. Heavy expenditure in 2013-2017 (%).

Data source: Romir, 2017

Thus, in comparison with the previous year only the share of those who has purchased clothes and shoes has drastically decreased – from 38% to 27%. Only one percent less Russians than last year splashed out on the entertainment (6%) and vacation (10%). On another expenditure side the increase was observed, especially in household appliances and electronics (21%), smartphone and tablet purchases (11%), in purchase (7%) and service (8%) of a vehicle, in apartment, house and summer house purchases (4%).

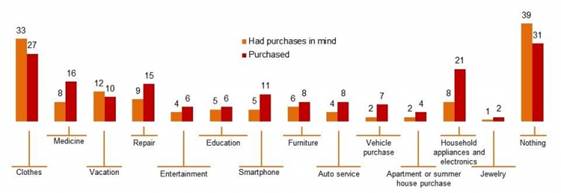

Diagram 2. What they've purchased within the period of the last 6 months in comparison to what they had been planning to purchase (%).

Data source: Romir, 2017

As Diagram 2 shows, claimed one-year plans on big-budget purchases went separate ways with the reality increasing in spendings. Russians were lucky to save only on clothes and shoes – 33% had purchases in mind and 27% really made purchases. 12% of Russians had plans of spending much money on their vacation but only 10% executed their plans. Plans and the reality almost coincided in terms of tuition fees (5% and 6%), entertainment spending (4% and 6%), furniture purchase (6% and 8%) and jewelry (1% and 2%). All other were exceeded provided that in some cases at a double and more rate.

Thus, for instance, purchases of household appliances and electronics serve as shining examples. Last year 8% of respondents had plans on making such purchases but the share of HAE buyers actually increased to 21%. The same is true for smartphone and tablet purchases. 5% of Russians were going to buy them but 11% did it after all. No one is impervious to smartphone breakdown, so the purchases of new phones sometimes become cost implications.

The vehicle situation also attracts attention. While only 2% talked about the purchase of vehicle last year, in fact the number of buyers increased threefold to 7%. 8% of Russians put their vehicle in costly repair though only 4% were set to do it. However, such type of expenditure is hard to predict – it could be the situation which claimed urgent investments in vehicle repair.

The overdraft also happened in medical expenses. Last year 8% of the respondents laid out expenditures on medicine and treatment but as many as 16% of Russians really made purchases. Unfortunately, references to a doctor can’t be always planned, thus we can see the increase in unexpected expenses. 9% of the respondents had plans of repairing apartments, houses and summer houses that is less than finally did it (15%). Someone was likely to repair immediately sanitaryware or heating appliances or someone probably invested in design improvement.

Thus, taking into account the increase in real spending in comparison with plans, it is not surprising that the share of Russians who didn’t have plans on making big-budget purchases also decreased from 39% to 31%. Please note that the number of Russians who didn’t make big-budget purchases returned to pre-crisis level last year and now remains this level. The share of those who economize was higher only in 2015. Then more than a half of Russians (59%) didn’t lay plans on major purchases.

Diagram 3. What they've purchased within the period of the last 6 months and what they are planning to purchase (%).

Data source: Romir, 2017

Nowadays 38% of Russians said about the lack of plans on buying anything expensive (see Diagram 3). It is a regular index which is identical to the last year’s index. In other expenditure terms the decrease in spending is declared, possibly in comparison with purchases made in the period of last six months.

In fact, within such volumes of household appliance buying it is not surprising that the share of potential buyers has decreased (11%). Similar plans are declared in terms of spending on clothes (21%), apartment repair (10%), smartphone purchase (5%) and repair and purchase of a vehicle (4% each).

The only item of expenditure which Russians are trying to increase in comparison with last year is spending on vacation and travelling (14%). If it really would happen, then it can be said that there is a remedial trend on tourism market. In 2015 Russians saved money under many items including vacation. Last year our compatriots would like to spend their vacation abroad but under closed Turkey and Egypt many of them were likely to refuse travelling taking into account more expensive domestic tourism. This year we believe Russians will spent more money on travelling than last year.

*The all-Russian survey of Romir surveyed a representative sample of 1500 respondents aged 18 and over, residing in cities and villages and in all federal districts. The sample represents the adult population of Russia.

WEST EUROPE

488-43-4/poll

UK: Ipsos MORI Final Election Poll 2017

Ipsos MORI’s final

election poll for the Evening Standard indicates that Theresa May and the

Conservatives are on course to win the 2017 General Election. (Ipsos Mori)

June 08, 2017

CON 44; LAB 36; LIB DEM 7; UKIP 4

Ipsos MORI’s final 2017 election poll for the Evening Standard indicates that Theresa May and the Conservatives are on course to win the 2017 General Election. Our headline estimate of voting intention is Conservative 44%, Labour 36%, Liberal Democrats 7%, UKIP 4%, and Greens 2%. The age pattern seen throughout the election continues, with young people more likely to vote Labour than Conservative (by 49% to 28% among 18-34s), while the 65+ say they will vote Conservative by 60% to 23% for Labour.

One in five of voters (19%) say they might still change their mind before they vote (similar to our final poll in the 2015 election). Labour supporters are marginally more likely to say they could change their mind, one in five (19%) compared to 13% of Conservative voters (and 33% of Liberal Democrats).

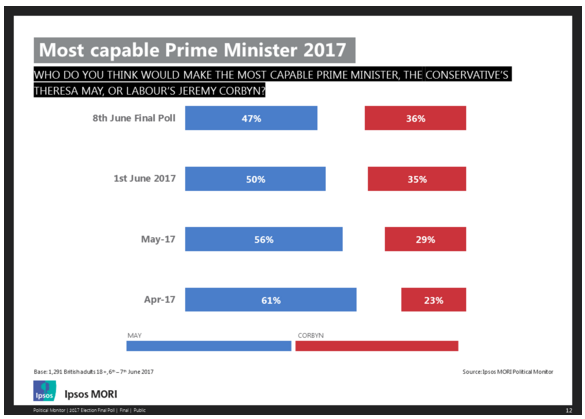

Theresa May leads Jeremy Corbyn in the final days of the campaign when it comes to who the public think would be the most capable Prime Minister. Just under half think Mrs May would be the most capable (47% - down three points from last week) while over one in three choose Mr Corbyn (36% - little change). Again, young people prefer Mr Corbyn (by 54% to 29% among 18-34s) while older voters still opt for Mrs May (by 65% to 21% among those aged 65+).

Gideon Skinner, Head of Political Research at Ipsos MORI, said:

The Conservatives had a

wobble last week, but have regained a clear lead in the last few days.

Theresa May’s advantage over Jeremy Corbyn is also lower than it was at the

start of the campaign, but she and her party have kept their support among key

voting groups such as older people. Having said that, one in five voters

say they might still change their mind, so there are still votes to fight for.

Technical Note:

Ipsos MORI interviewed a representative sample of 1,291 adults aged 18+ across Great Britain. Interviews were conducted by telephone 6th June – 7th June 2017. Data are weighted to the profile of the population (by age, gender, region, work status/sector, social grade, car in household, child in household, tenure, education (updated) and newspaper readership), and voting intention figures are based on all registered, and an adjustment for turnout overclaim based on age, and now also including tenure. As in all our final polls in recent general elections, we have reallocated refusals to the voting intention question on the basis of their newspaper readership.

488-43-5/POLL

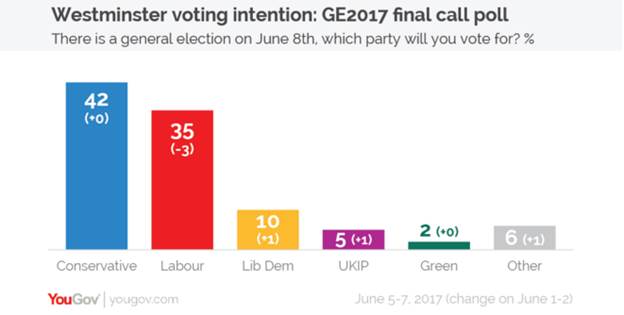

Final call poll: Tories lead by seven points and set to increase majority

Labour won the

battles of the election campaign, but the Conservatives still look almost

certain to win the war. The final call poll for the Times has voting intention

figures of CON 42%, LAB 35%, LDEM 10%, UKIP 5%. (YouGov)

June 07, 2017

Polls only predict shares of the vote – translating that into seat numbers and government majorities is more difficult – it depends on whether a party is winning or losing votes in the right places. The seven point Conservative lead is the same as at the previous election, but we think it is likely they will nevertheless be returned with an increased majority.

Our Scottish polling for the Times suggest the Tories are outperforming there and will win a good handful of seats from the SNP, and there is also a widespread expectation that they will perform disproportionately well in Labour-held seats that voted for Brexit.

At the start of the election campaign our polls showed a huge Conservative lead. Over the last six weeks that has been gradually whittled away, mostly through increases in Labour support. Whatever the differences between polls (and we are not blind to the fact that there is lots of variation between the figures different pollsters are showing), every company has told the same story of a shrinking Tory margin. But as we go into Election Day, the Conservatives still look set to secure a solid lead in votes and an overall majority. The question is how large.

![]()

As this is our final call before the election we made two minor changes to our method. The first is that rather than asking people which party they’d vote for, we showed respondents a list of the people actually standing in their constituency and asked which one they would vote for. Hopefully this will help pick up any tactical vote considerations and remove any issue of people saying they would vote UKIP or Green in seats where UKIP or the Greens are not actually standing.

Secondly we have reallocated those respondents who say don’t know, but who also say they are very likely to vote (voters who my colleague Adam McDonnell described earlier in the campaign as “true undecided”). We assume uncertain voters who say they “don’t know” at this stage won’t actually vote, but those who say they are 8+/10 certain to vote we have reallocated back to the party they voted for in 2015.

From the beginning of the campaign and throughout we have characterised this as an experimental election for pollsters. All of us called the election wrong in 2015, and while there is a broad consensus that the cause of the problem was inadequate sampling – the sort of people who did polls were too engaged, too political and too likely to vote – different companies have taken different approaches towards solving the problem.

Given one can hardly run a “test election”, tomorrow will be the first time those methods are tried out. The honest truth is that as pollsters we don’t yet know whether those methods have worked yet – one can only hope that some do and the industry as a whole can learn from the ones that succeed and move on from those that did not.

For now, YouGov’s final call for the 2017 election is for a seven point Conservative lead, leading to an increased Conservative majority in the Commons.

488-43-6/POLL

The local vs the national: the NHS comes into conflict with Brexit in terms of voters’ priorities

With the

Conservatives adopting a campaign on Brexit and other national issues, and many

Labour candidates adopting an exclusively local approach, YouGov looks at how

the public’s national vs local perspectives differ. (YouGov)

June 7, 2017

One of the features of this election

has been the attempt by Labour candidates to separate the local from the

national. With reports that the party’s leader is very unpopular on the

doorstep, Labour candidates have been trying to convince voters to think about

their local candidate when voting rather than Jeremy Corbyn.

The Conservatives meanwhile are

centring their campaign solely on Theresa May and her ability to negotiate

Brexit and handle other national issues like defence and security.

Framing things this way raises an

interesting question: how far does the importance of an issue at a national

level diverge from how it is seen at a local level? What issues would a

candidate looking to fight a local campaign be better off tackling compared to

a candidate campaigning on national issues?

To find out, YouGov asked

respondents three sets of open-ended questions exploring the most important

issues at a local and national level:

·

The

single most important issue facing the local area/country as a whole

·

The

single most important issue in the local area/country as a whole in deciding

how people will vote in the election

·

The

single most important issue they would prioritise if they were their local

MP/Prime Minister

Across the three sets of questions,

when it comes to the most important issues facing the country Brexit comes top,

at between 31-36%. However, this figure drops off significantly when

respondents were talking about their local area, gaining only 8%-13%.

By contrast, while health is in

second place when it comes to national issues (at 14%-16%) it moves up to first

place when respondents think about their local concerns (21%). Those aged 65+

were the group most likely most likely to rank health as their number one local

concern.

Some issues are much more

polarising. Housing gains more resonance as a local issue than a national one

(7%-11% vs 0%-1%), whereas defence and security gains more traction at a

national than local level (9%-18% vs 2%-3%).

![]()

To an extent, this research backs up

the phrase that “all politics is local.” However, in a general election – where

the party leaders are front and centre, fighting for airtime on the six o’clock

news – the campaign is national. Both parties will hope that they have picked

the right battles to win the right seats. We will know for sure on Friday.

488-43-7/POLL

UK: Sizing blunders won’t impact brand perception despite media backlash

Over the last couple

of weeks, two high-profiles fashion brands have encountered criticism for the

way they labelled women’s clothing. (YouGov)

June 07, 2017

Online

fashion retailer Asos came under fire for advertising a pair of UK size 10

shorts as a size large, while a similar incident involving H&M hit the

headlines in late May.

YouGov brand tracking data helps us

to understand how the respective stories had an impact on the public’s

perception of the brands.

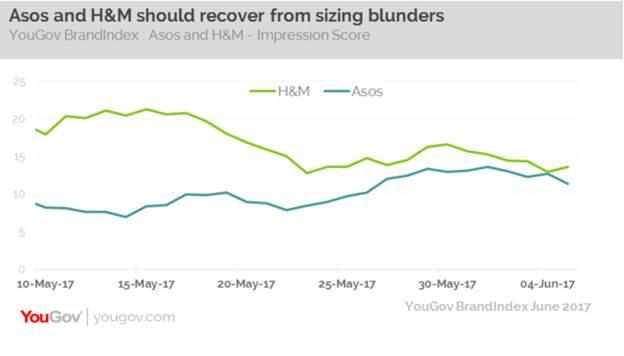

Asos’s Buzz score among all

respondents (that measures whether or not someone has heard something positive

about the brand in the past two weeks) dropped from +3 to 0 in the period

surrounding the error. Among those that would consider using the brand, the

drop in score was even greater – down from +22 to +16.

Looking at H&M, its score among

all respondents dropped from +4 to +1, while among considerers it fell from +18

to +9.

However, as with several crises

YouGov has tracked, the brands have minimized damage by responding in a

measured way. Asos in particular managed the situation well by reacting quickly

to assure people it had resolved the issue.

This is evidenced in Asos’s

Impression score – that measures whether people have a positive or negative

impression of the brand – which has in fact grown, after an initial dip

following the news stories.

In fact, the brand has dealt with

the story so efficiently that it’s Index score (an overall measure of brand

health) has risen from +6 to +9 in the past two weeks, indicating that Asos has

in fact managed to use the crisis to help draw attention to some of the

positive traits (or offers) it wishes to publicise.

It is a slightly different story for

H&M. It has fared less well among women – with the brand’s impression score

has dropping from +20 to +15. However, encouragingly its Index has not been

unduly damaged.

So, despite facing a media backlash,

and a potential Twitter storm, both brands have managed to steer themselves

away from trouble and remain in a good position, showing a good example of how

to respond to an emerging scandal.

488-43-8/POLL

Majority of Londoners trust Sadiq Khan to make the right decisions on terrorism

While Donald Trump

may criticise Khan, Londoners trust their mayor more than they trust Theresa

May or Jeremy Corbyn on terrorism. (YouGov)

June 05, 2017

London mayor Sadiq Khan came in for criticism from US president Donald Trump on Sunday after Khan called on Londoners not to be alarmed by an increased and armed police presence that day following the terror attack on London Bridge.

Taking the Mayor’s comments out of context, Trump tweeted “At least 7 dead and 48 wounded in terror attack and Mayor of London says there is "no reason to be alarmed!"

Despite the US president’s suggestions to the contrary, a YouGov survey conducted last week found that the majority of Londoners (51%) trust Khan to make the right decisions about keeping Britain safe from terrorism. Only three in ten Londoners (30%) say they don’t trust the Mayor of London to make the right call on terrorism.

In fact, Londoners trust their mayor more than they trust Theresa May and Jeremy Corbyn to make the right call on terrorism. Both the Prime Minister and Leader of the Opposition are less trusted than trusted on this topic. While 42% trust May and 41% trust Corbyn, 46% don’t trust the Prime Minister and 47% don not trust the Labour leader.

This is not the first time YouGov has found Londoners backing their mayor on the subject of terrorism. In response to an attack in New York last year, Londoners supported Khan by 69% to 22% in the face of media criticism when he said that being prepared for terror attacks are “part and parcel” of living in a big city.

Nor is this the only occasion where Trump and Khan have clashed. In response to previous criticism from the Mayor that the president’s views on Islam were ignorant, Trump challenged Khan to an IQ test. A subsequent YouGov survey found that British people expect that the Mayor would have beat Trump handily in such a test. Using a scoring system that based on the responses given by the public, giving incrementally lower multipliers for 'far above average', 'slightly above average', 'average' and so on, Sadiq Khan scored 67.9 compared to Trump’s 45.1.

488-43-9/POLL

Is the NHS Labour’s secret weapon in the election?

Given

that it is such an important issue to the public, it is not surprising that

Labour is making the NHS a centrepiece of its election campaign, says Kate

Duxbury.

The NHS remains a

key election battleground. In Ipsos MORI’s Political Monitor, the public say

that the NHS and the EU/Brexit are the main issues that will help them decide

which party to vote for at the election (43% and 42% respectively). (Ipsos

Mori)

June 08, 2017

Given that it is such an important issue to the public, it is not surprising that Labour is making the NHS a centrepiece of its election campaign. These messages seem to be cutting through: our May Issues Index shows a jump in concern about the NHS, leaving it as the most important issue facing Britain (61%, the highest score since April 2002 – and with interviews mostly completed before the cyber attacks).

Labour has traditionally performed better than the Conservatives on healthcare. Our most recent polling, completed before the manifestoes were released, returns a 15 percentage point lead on healthcare for Labour, with 40% saying Labour has the best policies and 25% that the Conservatives do. Healthcare is the only one of the top five policy areas in which Labour has a lead (the Tories lead on Brexit, the economy, education and immigration).

![]()

Not only does Labour have a lead, but the Conservatives are open to challenge. The public are worried about the future of the NHS. Recent polling for the Health Foundations shows that around half think the general standard of care provided by the NHS will get worse over the next few years (48%) and only 14% think it will get better. The British public are more pessimistic about healthcare than other public services and they are also more pessimistic than any of the 23 countries included in our Global Trends Survey.

Although the public are worried about the future of the NHS, they remain positive about how the NHS is delivering. Data from The King’s Fund’s British Social Attitudes survey show that overall satisfaction with the running of the NHS remains consistently high; in 2016, 63% said they were satisfied and 22% said they were dissatisfied, showing no statistically significant change from 2015. And in Ipsos MORI’s own Global Trends Survey, the British are among the most positive countries about the quality of healthcare they can access.

So despite Labour having a lead in the polls on healthcare and high levels of concern about the future of the NHS, exacerbated by a succession of difficult winters, satisfaction has held up. And Labour’s 15 percentage point lead on healthcare is not as clear-cut as it may sound. The Prime Minister is more trusted on healthcare than her own party (34% trust May versus 25% for the Conservatives) – and there is little to choose between Corbyn and May (37% trust Corbyn versus 34% for May). And not only that, but Conservative supporters are just as likely to say the NHS is a key issue facing the country as Labour supporters – and of course they may prefer Conservative policies on the issue. So just because the NHS is seen as the top issue, that doesn’t mean all of that will work to Labour’s advantage.

How might this play out in the ballot box? Until patient and public perceptions of the NHS reach a tipping point that we have not yet seen, it is unlikely to be the deciding factor in the ballot box. It wasn’t in the 2015 general election, when the NHS was again seen as the most important issue facing Britain. But our Issues Index, reporting a 15-year high in concern about the NHS, suggests we are edging ever closer to that tipping point.

Labour’s manifesto pledges for the NHS are ticking off the list of key concerns for the public. Increased funding, a commitment to meeting waiting time targets, scrapping pay caps for NHS staff, addressing the postcode lottery – and the list goes on – are all pledges that play well with voters. Now we must wait to see whether the public can be persuaded that the NHS is in enough trouble that it should determine who they vote for.

NORTH AMERICA

488-43-10/POLL

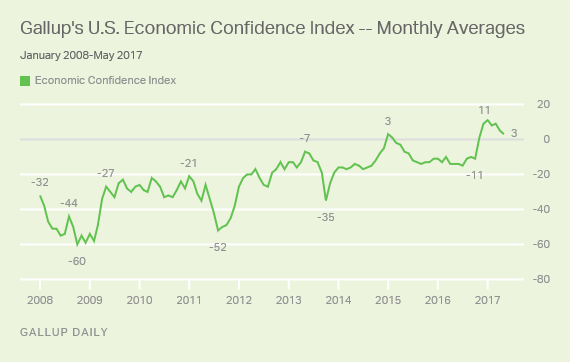

Confidence in Economy in May Lowest Since November 2016

WASHINGTON, D.C. --

Though still historically high, Americans' confidence in the economy fell to a

six-month low in May, largely

dragged down by Democrats'

worsening economic attitudes. Gallup's U.S. Economic Confidence Index averaged

a score of +3 in May, down slightly from April (+5) but eight points below

January's record

monthly high (+11).

(Gallup USA)

JUNE 6, 2017

Gallup's U.S. Economic Confidence Index is the average of two components: how Americans rate current economic conditions and whether they believe the economy is improving or getting worse. The index has a theoretical maximum of +100 if all Americans were to say the economy is doing well and improving, and a theoretical minimum of -100 if all were to say the economy is doing poorly and getting worse.

Confidence in early June appears to be no different from that in May, with the latest weekly average also +3 for the week ending June 4.

Since the November presidential election, many Americans' attitudes about the economy have dramatically improved. Both the weekly and monthly averages of Gallup's U.S. Economic Confidence Index now consistently produce positive figures rather than negative ones, as it largely did before the election.

The sharp uptick in economic confidence after the election was largely attributable to surging confidence among Republicans, but President Donald Trump's business background or his economic proposals may have also convinced other Americans that the economy would prosper under his leadership. U.S. financial markets have seemed to subscribe to this line of thinking, with several indexes reaching all-time highs in 2017.

Over the past few months, however, confidence has fallen as economic attitudes of self-identified Democrats have worsened -- a trend that continued in May as Democrats' monthly index score fell to -26. This represents a five-point dip from April's average and the lowest monthly index score for Democrats since November 2011 (-29), when confidence was recovering from the tumble it took during the standoff between Congress and former President Barack Obama over raising the federal debt ceiling.

However, independents' economic ratings have also dipped in recent months. After peaking at +5 in January, independents' index score fell into negative territory in April, when it averaged -1. It remained negative last month, with May's score reaching -3.

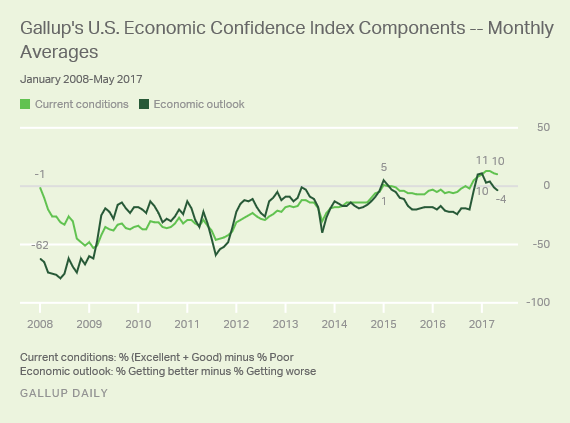

Current Conditions Component Remains Positive, but Economic Outlook Is Negative

Even as some Americans become more pessimistic about the economy overall, attitudes about the economy's current conditions have been relatively stable. Last month, 32% of Americans assessed the economy as "excellent" or "good," while 22% said the economy was "poor." Overall, the current conditions component averaged +10 in May, similar to +11 in April and three points shy of the nine-year high (+13) the measure hit in February and March.

Meanwhile, perceptions about the economy's outlook have more clearly deteriorated. In May, slightly more Americans (49%) said the economy was "getting worse" than said it was "getting better" (45%). The economic outlook component stood at -4 for the month, representing a slight dip from April when the component averaged -1, and it is down notably from its record high in January of +11.

Bottom Line

While Americans' confidence in the economy remains stronger than it was before the 2016 presidential election, it is not as strong as it was earlier this year.

Republicans' confidence rose more sharply than Democrats' fell in the weeks after Trump's election. However, polarization being as it is, it seemed likely that Democrats would become increasingly pessimistic about the economy as the Obama administration (and its influence on the economy) fell farther in the rearview mirror. In May, this happened to some degree, with confidence among Democrats falling to its lowest level since November 2011. However, Democrats still express more confidence in the economy now than Republicans typically did when Barack Obama was president.

SURVEY METHODS

Results for this Gallup poll are based on telephone interviews conducted May 1-31, 2017, on the Gallup U.S. Daily survey, with a random sample of 15,181 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia. For results based on the total sample of national adults, the margin of sampling error is ±1 percentage point at the 95% confidence level. All reported margins of sampling error include computed design effects for weighting.

Each sample of national adults includes a minimum quota of 70% cellphone respondents and 30% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

488-43-11/POLL

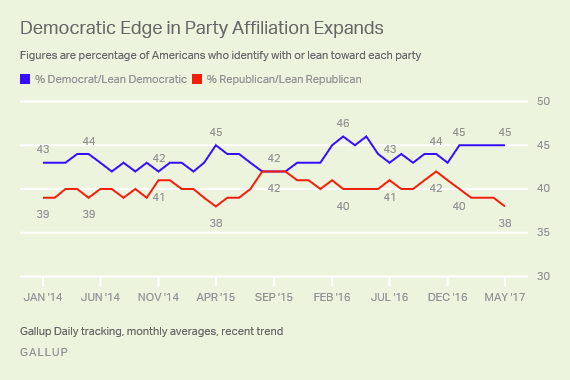

Democratic Edge in Party Affiliation Up to Seven Points

WASHINGTON, D.C. --

In an encouraging sign for the Democratic Party's election prospects in 2018,

its edge in party affiliation over the Republican Party has grown to seven

percentage points, the largest it has been in over two years. During the late

summer and fall of 2016, Democrats averaged a three-point advantage.

JUNE 6, 2017

These results are based on Gallup Daily tracking throughout May. Overall, 45% of U.S. adults self-identify as Democrats or say they are independents who lean Democratic, while 38% identify as Republicans or lean Republican.

The growing Democratic advantage in recent months is mostly attributable to a decline in Republican affiliation rather than an increase in Democratic affiliation. Since November, the percentage of Republicans and Republican leaners has fallen four percentage points, while there has been a one-point rise in Democratic identification or leaning. The Republican decline has been offset mostly by a three-point increase in the percentage of Americans with no party preference or leaning.

President Donald Trump's unpopularity is likely a factor in the Republican Party's falling fortunes. The president's job approval ratinggenerally has held near 40% since February -- well below average forpresidents historically, and especially for those in their first few months in office.

Democrats last had a seven-point advantage in Gallup's Daily tracking trend in April 2015, about the time several national figures, including Hillary Clinton, were announcing their candidacy for president. Gallup polling from that time found Clinton to be the best-liked of the potential candidates in both parties, although the poll was conducted just as news of her use of a private email server was emerging. That controversy continued to mount and dogged her candidacy throughout the campaign.

The last time Democrats had a lead larger than seven points in Gallup's tracking trend was September 2009, President Barack Obama's first year in office, when the lead was nine points. That month, 47% of Americans identified as Democrats or leaned Democratic, and 38% identified as Republicans or leaned Republican. Democrats consistently enjoyed double-digit advantages in 2008 and 2009 as the unpopular Republican President George W. Bush finished out his term and was replaced by the highly popular Obama.

After his first year in office, Obama rarely managed majority approval ratings, and the gap in party affiliation between the two parties was generally small.

Implications

Party identification and political independents' party leanings are major predictors of individual vote choice. At the national level, party affiliation is related to the outcomes of midterm elections. The current seven-point Democratic edge in party affiliation is similar to what it was in 1998 and 2006, the two strongest Democratic years among the most recent midterm elections.

If Democrats can maintain a significant advantage in Americans' party preference over the next 17 months, it would serve them well in the 2018 midterm elections.

The opposition party to the president usually fares better than the president's party in midterm elections, and the opposition has done especially well when the president has low job approval ratings. With Trump's approval ratings stuck near 40%, Republicans are understandably nervous about the party's prospects in 2018.

However, the current party affiliation data indicate that Democrats are not necessarily expanding their base as much as they are benefiting from a decline in the Republican base. Expanding their own base would strengthen Democrats' ability to offset usual Republican advantages in voter turnout and put them in a better position to win the seats they need to have a majority in one or both houses of Congress.

These data are available in Gallup Analytics.

SURVEY METHODS

Results for this Gallup poll are based on telephone interviews conducted May 1-31, 2017, on the Gallup U.S. Daily survey, with a random sample of 15,219 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia. For results based on the total sample of national adults, the margin of sampling error is ±1 percentage point at the 95% confidence level. All reported margins of sampling error include computed design effects for weighting.

Each sample of national adults includes a minimum quota of 70% cellphone respondents and 30% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

488-43-12/POLL

Exchange Purchasers Rate Health Coverage Less Positively

WASHINGTON, D.C. --

U.S. adults who purchased their health insurance coverage through a federal or

state healthcare exchange -- about 15% of those who report having insurance --

rate the quality of their coverage lower than do those who purchased their

coverage via another source. Both groups are generally positive about their

insurance, but the 74% of exchange purchasers who consider the quality of their

coverage to be "excellent" or "good" is marginally lower

than the 81% of those whose coverage stems from another source who say the

same.

JUNE 8, 2017

Quality

of Coverage, by Source

Overall,

how would you rate your primary health insurance coverage -- as excellent,

good, only fair or poor?

|

Purchased

from exchange |

Purchased

elsewhere |

|

|

% |

% |

|

|

Coverage

is excellent/good |

74 |

81 |

|

Coverage

is fair/poor |

26 |

19 |

|

GALLUP DAILY, MARCH 8-MAY 7,

2017 |

||

Fewer insurance providers and increased premiums on some state exchanges in 2017 could be driving perceptions that the quality of coverage purchased on exchanges lags behind that acquired from other sources.

Since 2008, Gallup has tracked the share of U.S. adults without health insurance -- a percentage that fell to a record low of 10.9% in each of the last two quarters of 2016. The current results are based on 24,156 interviews with U.S. adults aged 18 and older on Gallup's Daily tracking poll from March 8 to May 7 of this year. Gallup not only asked individuals to identify the source of their health insurance coverage -- including if they purchased insurance on an Affordable Care Act (ACA) exchange -- but to rate the quality of their coverage.

Least-Healthy Americans Most Likely to Purchase From Exchanges

In addition to asking about their health insurance coverage, Gallup asked adults to rate their own physical health on a five-point scale between "excellent" and "poor." Those who assess their own physical health as "poor" are the most likely to have purchased their coverage through an ACA exchange. In fact, individuals with the poorest self-reported health are more than twice as likely as individuals with excellent health to have purchased coverage through an exchange.

Exchange

Purchases, by Physical Health

Did

you get your primary health insurance from a state or federal health insurance exchange,

such as healthcare.gov, or not?

|

Excellent

health |

Very

good health |

Good

health |

Fair

health |

Poor

health |

|

|

% |

% |

% |

% |

% |

|

|

Purchased

from state or federal exchange |

12 |

15 |

16 |

15 |

27 |

|

Purchased

elsewhere |

88 |

85 |

84 |

85 |

73 |

|

GALLUP DAILY, MARCH 8-MAY 7,

2017 |

|||||

The discrepancy in exchange purchases between those in poor and excellent health could stem, in part, from differing incentives for those two groups. For example, healthy individuals without coverage through an employer or other source may decide to pay the penalty for not carrying coverage -- an option less viable for adults in poor health who do not qualify for coverage under another source.

Quality

of Coverage Among Exchange Purchasers, by Physical Health

Overall,

how would you rate your primary health insurance coverage -- as excellent,

good, only fair or poor?

|

Excellent

health |

Very

good health |

Good

health |

Fair

health |

Poor

health |

|

|

% |

% |

% |

% |

% |

|

|

Coverage

is excellent/good |

79 |

76 |

78 |

69 |

62 |

|

Coverage

is fair/poor |

21 |

24 |

22 |

31 |

39 |

|

GALLUP DAILY, MARCH 8-MAY 7, 2017 |

|||||

Among those who purchased coverage on an exchange, adults with the poorest health also rate the quality of their coverage the lowest. While 62% of individuals in poor physical health say their coverage is excellent or good, nearly eight in 10 adults who rate their physical health as "excellent," "very good" or "good" say the same.

To sustain robust exchanges, healthcare markets must attract enough healthy purchasers whose lower cost burden helps offset the steeper costs of less-healthy purchasers. Yet, these results suggest that not only are adults with the poorest health the most likely to purchase coverage on exchanges, but they also receive the lowest-quality coverage.

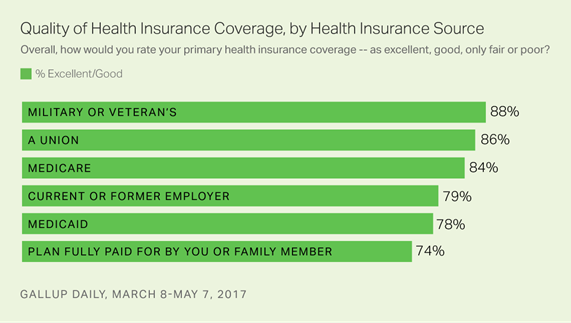

Military/Veteran's Coverage Rated Highest, Self-Purchased Plans Lowest

Among all health insurance sources, adults with military or veteran's insurance rate their coverage most highly, with nearly nine in 10 reporting that their coverage is excellent or good. Union-sponsored health insurance and Medicare also receive high marks -- 86% and 84% of individuals with coverage from these sources, respectively, rate it as excellent or good.

Nearly three-quarters of those with a plan fully paid for by themselves or a family member -- many of whom bought through exchanges -- say their health insurance coverage is excellent or good. By comparison, about four in five adults who receive their insurance through an employer or Medicaid rate their coverage highly.

Higher-Income, Older Americans Rate Coverage Highest

Across key demographic groups, adults aged 65 and older grade their health insurance coverage the most positively. Nearly nine in 10 in this age group -- the vast majority of whom receive Medicare coverage -- consider their insurance to be excellent or good. By comparison, three-quarters of those aged 25 to 65 rate their coverage this highly.

Relatively small differences separate the evaluations of healthcare coverage quality across gender, race and income groups. However, whites, women and higher-income Americans evaluate their coverage slightly more positively.

Health

Insurance Coverage Quality, by Demographics

|

Coverage

excellent/good |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

% |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GENDER |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Men |

78 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Women |

81 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

RACE |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Whites |

81 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Blacks |

78 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Asians |

77 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Hispanics |

77 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

INCOME |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Less

than $36,000 |

77 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

$36,000

to <$60,000 |

79 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

$60,000

to <$90,000 |

79 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

$90,000+ |

82 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

AGE |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

18

to 24 |

83 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

25

to 34 |

75 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

35

to 49 |

75 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

50

to 65 |

77 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

65+ |

89 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GALLUP DAILY, MARCH 8-MAY 7,

2017 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Implications

In addition to contributing to the lowest uninsured rate since Gallup began tracking Americans' health insurance coverage in 2008, the Affordable Care Act today is more popular than at any point since it went into effect. Republicans and Democrats alike have warmed to the healthcare law in recent months, with 55% of U.S. adults approving of it in April 2017 after only 42% did so last November.

Yet uncertainty about the future of the healthcare system continues. In May, House Republicans passed a bill repealing many of the key features of the ACA. Against the backdrop of a Congressional Budget Office score that estimates 23 million Americans could lose coverage under the House bill, Senate Republicans say they will scrap the House version of the bill and start anew.

Meanwhile, in May, healthcare surged to tie dissatisfaction with government at the top of Americans' list of the biggest problems facing the country. And, despite a declining uninsured rate in recent years, Americans' out-of-pocket expenses on healthcare continue to rise. As leaders debate the merits of the ACA and competing Republican alternatives, both parties must pursue concurrent goals of minimizing healthcare costs and the number of uninsured while also maximizing the quality of the coverage received.

These data are available in Gallup Analytics.

SURVEY METHODS

Results for this Gallup poll are based on telephone interviews conducted March 8-May 7, 2017, on the Gallup U.S. Daily survey, with a random sample of 24,156 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia. For results based on the total sample of national adults, the margin of sampling error is ±1 percentage point at the 95% confidence level.

Each sample of national adults includes a minimum quota of 70% cellphone respondents and 30% landline respondents, with additional minimum quotas by time zone within region. Landline and cellular telephone numbers are selected using random-digit-dial methods.

488-43-13/POLL

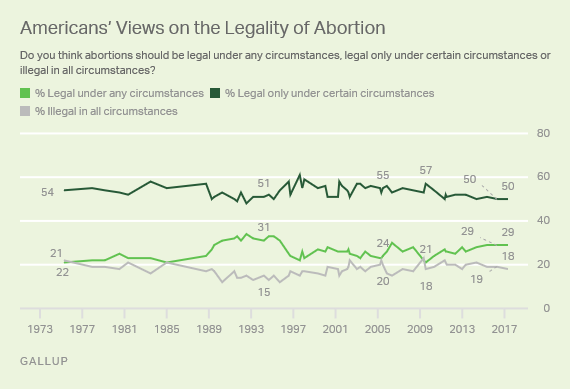

US Abortion Attitudes Stable; No Consensus on Legality

WASHINGTON, D.C. --

Stability remains the name of the game in U.S. abortion attitudes. Half of

Americans say abortion should be "legal only under certain

circumstances," identical to a year ago, while 29% still say it should be

legal in all circumstances. The smallest proportion -- 18% this year vs. 19% in

2016 -- say it should be illegal in all circumstances. (Gallup USA)

JUNE 9, 2017

The dispersion of abortion views today, with the largest segment of Americans favoring the middle position, is broadly similar to what Gallup has found in four decades of measurement.

Also, as is the case today, more Americans typically have thought abortion should be completely legal than completely illegal. The proportions have varied from a 20-percentage-point advantage for the always-legal position in 1994 to a virtual tie at several points. This year's 11-point edge for the always-legal position is similar to its average nine-point lead across the full trend.

Gallup also asks those who say abortion should be legal in certain circumstances whether those should be most circumstances or only a few, and, by nearly a 3-to-1 ratio, they choose only a few, 36% vs. 13%. Thus, the slight majority of Americans (54%) favor curtailing abortion rights -- saying abortion should be illegal or legal in only a few circumstances. Slightly fewer, 42%, want access to abortion to be unrestricted or legal in most circumstances.

The 2017 results are based on Gallup's annual Values and Beliefs survey, conducted May 3-7.

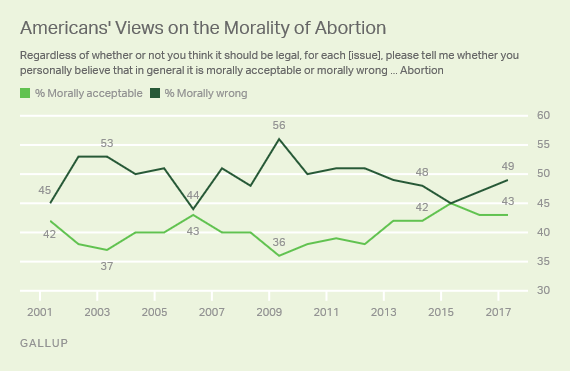

Americans Closely Divided on Morality of Abortion, Abortion Labels

Americans' views on two other aspects of abortion -- whether it's moral and whether they consider themselves "pro-choice" or "pro-life" -- have also been steady over the past year.

Slightly more U.S. adults today believe the procedure is morally wrong (49%) than morally acceptable (43%). This has also been the case in most readings since Gallup started tracking this annually in 2001.

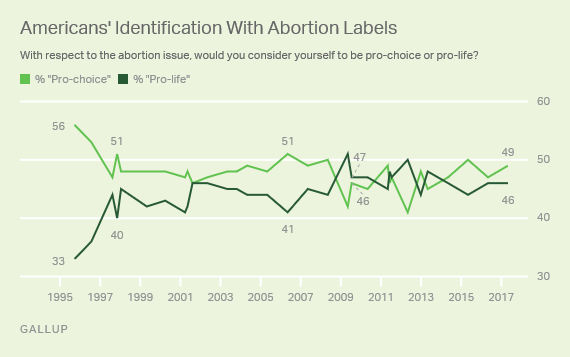

In terms of the two abortion labels, 49% of U.S. adults consider themselves pro-choice on the abortion issue, while 46% consider themselves pro-life.

Again, this represents almost no change compared with a year ago and is consistent with the close division seen over the past decade. By contrast, in the earliest years Gallup asked this, in 1995 and 1996, there was greater attachment to the pro-choice label, with 56% and 53%, respectively, identifying as such. Americans continued to prefer the pro-choice label over the pro-life label by a slight margin in most years through 2009, but the two have since been about tied.

Women Tilt Slightly More "Pro-Choice"

Women and men hold roughly similar positions on abortion, with the largest segments of both groups believing abortion should be legal in only certain circumstances and slightly more calling abortion morally wrong than morally acceptable.

At the same time, slightly more women than men take the always-legal position on abortion as well as call themselves pro-choice. These gender patterns are consistent with what Gallup has found in most of the past several years.

Summary

of 2017 Abortion Views by Gender

|

Men |

Women |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

% |

% |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

LEGALITY

OF ABORTION |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Legal

in all circumstances |

24 |

33 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Legal

in only certain circumstances |

55 |

46 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Illegal

in all circumstances |

18 |

18 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

MORALITY

OF ABORTION |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Morally

acceptable |

43 |

43 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Morally

wrong |

48 |

49 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

ABORTION

POSITION |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

"Pro-choice" |

45 |

52 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

"Pro-life" |

48 |

43 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GALLUP, MAY 3-7, 2017 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Record Percentage of Democrats Identify as "Pro-Choice"