|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 682 Week:

March 15 –March 21, 2021 Presentation:

March 26, 2021 Maruti

Suzuki Is The Healthiest Automotive Brand In India Toyota

Tops YouGov Thailand’s 2021 Automotive Rankings Honda

Tops YouGov Malaysia’s 2021 Automotive Rankings Toyota

Tops Yougov’s 2021 Automotive Rankings In Saudi Arabia Three-In-Four

Libyans Say The Economy Is In A Very Bad Or A Bad State Nine

In 10 Nigerians (85%) Say They Are Concerned About Kidnappings Six

In Ten Do Not Want To Cut Spending On Public Services To Pay Off Debt 43%

Londoners Think Sadiq Khan Has Handled COVID Well Less

Than Half Of Britons Expected To Tick ‘Christian’ In Uk Census 1

In 2 French People Think The Pandemic Has Exacerbated Ethnic Discrimination Youtube

Is The Most Popular Online Music Service Among Germans 71%

Of 14 To 24-Year-Olds State That They Have Good Social Contacts With Friends Finland's

Strongest Car Brands Above

50% Vaccination Propensity In Hungary Toyota

Tops YouGov Australia’s 2021 Automotive Rankings 73.7%

Of Australians Holding Private Health Insurance Are Satisfied Movement

Of People In Melbourne Cbd Is At 39% Of Normal One Year After The First Covid

Lockdown Global

Consumer Confidence Getting Closer To Pre-Pandemic Level 81%

Of Spanish Mothers And Fathers Feel Judged By Others After

Covid-19: Putting People Before Politics Is Key To Recovery The

Pandemic Stalls Growth In The Global Middle Class, Pushes Poverty Up Sharply INTRODUCTORY NOTE

682-43-23/Commentary:

The

Pandemic Stalls Growth In The Global Middle Class, Pushes Poverty Up Sharply

The COVID-19 pandemic is

having a deep effect on the global economy. In January 2020, as reports of

the novel coronavirus were emerging, the World Bank forecasted that the

global economy would expand by 2.5% that year. In January 2021, with the

pandemic still holding much of the world in its grip, the World Bank estimated that

the global economy contracted by 4.3% in 2020, a turnabout of 6.8 percentage

points.

The economic

downturn is likely to have diminished living standards around the world,

pushing millions out of the global middle class and swelling the ranks of the

poor. At the same time, the path to a recovery is clouded with uncertainties. A new Pew

Research Center analysis finds that the global middle class encompassed 54

million fewer people in 2020 than the number projected prior to the onset of

the pandemic. Meanwhile, the number of poor is estimated to have been 131

million higher because of the recession. The drop-off

in the global middle class was centered in South Asia and in East Asia and

the Pacific, and it stalled the expansion seen in the years preceding the

pandemic. South Asia, specifically India, along with Sub-Saharan Africa,

accounted for most of the increase in poverty, reversing years of progress on

this front. As defined

in this report (and in previous Pew Research Center

analyses), people who are middle income live on

$10.01-$20 a day, which translates to an annual income of about $14,600 to

$29,200 for a family of four. This is modest by the standards of advanced

economies. In fact, it straddles the official poverty line in

the United States – about $23,000 for a family of four in 2020 (expressed in

2011 prices). By global standards, the poor live on $2 or less a day, or no

more than $2,920 annually for a family of four. The number

of people in the global high-income tier (more than $50 daily) is estimated

to have decreased by 62 million in 2020, erasing about half of the gain since

2011, with most of the change emanating from advanced economies. Meanwhile,

the upper-middle income population ($20.01-$50 daily) fell by 36 million,

while the low-income population ($2.01-$10 daily) is estimated to have

increased by 21 million. Who is middle class (or middle income)? This report

uses the terms “middle income” and “middle class” interchangeably, a common

practice among economists who tend to define the middle class in terms of

income or consumption. But being middle class can connote more than income,

be it a college education, white-collar work, economic security, owning a

home, or having certain social and political values. Class could also simply

be a matter of self-identification. The interplay among these many factors is

examined in studies by Hout (2007) and Savage et al. (2013),

among others. The

population in each global region is divided into five groups: poor, low income,

middle income, upper-middle income and high income. The poor live on $2 or

less daily, low income on $2.01-$10, middle income on $10.01-$20,

upper-middle income on $20.01-$50 and high income on more than $50. All

dollar figures are expressed in 2011 prices and purchasing power parity dollars,

currency exchange rates adjusted for differences in the prices of goods and

services across countries. The

assignment to a group, or income tier, is based on a household’s daily per

capita income or consumption, a simple way of controlling for differences in

household size. In the source data, some countries only

report income data while others only report consumption data. The terms

“income” and “consumption” are used interchangeably for the sake of

convenience. A

middle-income, or middle-class, threshold of $10 follows the practice of

other researchers. A similar threshold has been used by the World Bank (2007, 2015),

researchers at the Organization for Economic Cooperation and Development (Kharas,

2010), the development community (Birdsall, Lustig and Meyer, 2013)

and others. There is evidence that the $10 threshold, which is about five

times higher than the World Bank’s global poverty line,

is associated with economic security and

“insulates” people from falling back into poverty. An earlier Pew Research Center report discusses

the choice of income thresholds in greater detail. The global

middle-class standard is modest by the standards of advanced economies. In

2020, the official poverty line for

a family of four in the U.S. stood at about $15.90 per person per day (in

2011 prices). Thus, many who are poor by the U.S. definition would meet the

global middle-income standard or, conversely, many who are in the global

middle class would be poor by U.S. standards.

These

estimates are based on the Center’s analysis of World Bank data on

the distribution of people by either income or consumption levels in seven

major global regions. The latest available estimates of income for each

region, such as for 2018 for Europe and Central Asia and 2015 for the Middle

East and North Africa, are extrapolated to 2020 using two sets of growth

estimates: the forecasts issued by the World Bank in January 2020, prior to

the pandemic, and the estimates issued in January 2021, with the pandemic’s

economic impact in plainer sight. The difference between these two measures

is taken to represent the impact of the COVID-19 downturn on the standard of

living of people globally. Prior to the

emergence of COVID-19, some 1.38 billion people were expected to be counted

in the global middle class in 2020. But the pandemic is estimated to have

driven this number down to 1.32 billion. The share of people in the middle

class globally is estimated to have been 17.1% in 2020, instead of

potentially 17.8%. The erosion in the middle class might have been deeper if

not for the fact that China – which is home to more than one-third of the

global middle class – evaded an economic contraction,

even though growth there was slower than anticipated. The number

of global poor is estimated to have risen to 803 million in 2020, much

greater than the 672 million initially expected. The global poverty rate,

which had been in steady decline this century,

is likely to have increased to 10.4%, nearly reverting to the rate in 2017,

instead of sinking to a new low of 8.7%, as previously expected. The steep

rise in global poverty is driven by the fact that many who were in the

low-income tier prior to the pandemic lived on the margin of poverty. In

2017, 877 million people lived on $2 to $3 a day, according to World Bank

estimates. Thus, large numbers were susceptible to falling back into poverty

prior to the pandemic, especially in South Asia and Sub-Saharan Africa. At the other

end of the economic spectrum, the global high-income population likely fell

to 531 million in 2020 from the 593 million originally expected.

Consequently, the expected share in the high-income tier is 6.8%, not 7.6%. A

vast majority of the global high-income population lives in advanced

economies, and this group of countries also experienced a sharp downturn in

2020. Ironically, this bolstered the global middle-income population as

people in advanced economies slipped down the ladder from higher income

tiers.

The reversal

in global living standards in 2020 comes on the heels of notable progress

earlier in the decade. From 2011 to 2019, the global middle-class population

increased from 899 million to 1.34 billion, or by 54 million people annually,

on average. The pandemic is estimated to have erased a year of growth,

leaving the global middle-class population nearly unchanged from 2019 to

2020. Global

poverty had abated at an average rate of 49 million annually from 2011 to 2019,

with the number of global poor falling from 1.10 billion to 691 million

during this period. The pandemic, by adding 131 million to the ranks of the

poor, has set the progress on poverty back by several years, and the poverty

rate is estimated to have increased from 9.0% in 2019 to 10.4% in 2020. From 2011 to

2019, the global high-income population had increased from 459 million to 576

million, growing by an average of 15 million annually. Thus, the setback of

62 million due to the pandemic in 2020 also reverses several years of growth

in the high-income population. The share of the global population in the

high-income tier is expected to have decreased from 7.5% in 2019 to 6.8% in

2020. The erosion of the middle class is centered in Asia, the rise in poverty

in Asia and Africa The effect

of the COVID-19 downturn on the middle class and other income tiers shows

distinct regional differences. Asia is expected to have accounted for most of

the shrinking of the global middle class in 2020, with the middle-class

population falling by 32 million in South Asia and by 19 million in East Asia

and the Pacific. Meanwhile, the middle class in advanced economies is

estimated to have increased by 16 million, in part due to the drop-off in the

high-income tier in those countries.

The

projected rise in global poverty in the pandemic is concentrated in South

Asia (an increase of 78 million) and Sub-Saharan Africa (40 million),

historically among the poorest regions in the world. The high-income

population in advanced economies is estimated to have shrunk by 47 million in

2020, accounting for most of the falloff globally. It should be noted that

the global cutoff for the high-income tier – more than $50 a day – is not

much higher than the median income across advanced economies, as an estimated

40% of the population in these countries is in the global high-income tier.

Thus, the contraction of the high-income tier in advanced economies is more a

reflection of the reduction in the standard of living of the typical person in

these countries than outcomes for the wealthy. The

contribution of a region to global changes overall and the shift in its own

income distribution depends mostly on two factors: the sizes of income tiers

in the region prior to the COVID-19 recession and the impact of the downturn

on economic growth in the region. Prior to the

pandemic, nearly half of the global middle-class population – 672 million of

1.38 billion – was estimated to live in East Asia and the Pacific, a region

that includes China. Latin America and the Caribbean accounted for 191

million, and Europe and Central Asia was home to 183 million. South Asia

accounted for 123 million more. In view of

these magnitudes, the estimated loss (relative to pre-pandemic expectations)

of 32 million people from the middle class in South Asia is notable for two

reasons. First, the region contributed the most to the shrinking of the

global middle class in 2020 despite having a middle-income population smaller

than several other regions. Second, the percentage decrease in South Asia’s

middle-income population from what was previously expected (26%) is much

greater than in any other region. Although East Asia and the Pacific shed 19

million from the middle-income tier, that represented only 3% of its middle

class.

Poverty is

most prevalent in Sub-Saharan Africa. Some 494 million people in Sub-Saharan

Africa, out of a total population of 1.14 billion, were expected to be living

in poverty ahead of the pandemic in 2020. South Asia, with a total population

of 1.86 billion, was expected to be home to 104 million poor. Nonetheless,

South Asia is estimated to have added nearly double the amount of people to

the ranks of the globally poor as Sub-Saharan Africa in the pandemic. The

percentage increase in poverty in South Asia (75%) dwarfs the increase in

Sub-Saharan Africa (8%). The number

of poor in other regions was smaller, estimated to range from 6 million in

Europe and Central Asia to 27 million in Latin America and the Caribbean

ahead of the pandemic in 2020. But, since that moment, the increase in

poverty in these regions is notable. The Middle East and North Africa and

East Asia and the Pacific are each estimated to have seen increases in

poverty of more than 20% due to the recession. The rise in poverty in both Europe

and Central Asia and Latin America and the Caribbean is not far behind, with

each experiencing a 17% increase in poverty. A large

majority of the global high-income population – 489 million of 593 million –

lived in advanced economies before the global recession took hold. The

estimated decrease of 47 million, or 10%, in this population in advanced

economies accounts for most of the shrinking of the global high-income tier. In

proportional terms, the drop off in the high-income tier is also notable in Latin

America and the Caribbean (15%), Europe and Central Asia (12%) and East Asia

and the Pacific (12%). The losses in the Middle East and North Africa, South

Asia and Sub-Saharan Africa are relatively small in magnitude (each less than

1 million people) but also represent double-digit shares of the high-income

populations in those regions.

The

relatively outsized role of South Asia in the contraction of the global

middle class and the expansion of poverty is the result of it seeing the

sharpest reduction in economic growth in the pandemic. In January 2020, the

World Bank forecasted that South Asia would experience a 4.3% increase in

gross domestic product (GDP) per capita in 2020. But, in January 2021, output

in South Asia was estimated to have decreased by

7.8% in 2020, a retreat of 12.1 percentage points from potential. The setback

to economic growth in other regions is smaller, ranging from 4.7 percentage

points in East Asia and the Pacific to 8.6 points in Latin America and the

Caribbean. East Asia and the Pacific is the only region in which growth is

estimated to have stayed positive in 2020, with GDP per capita inching up by

0.4% even after the onset of the pandemic. Otherwise, the latest estimates of

the change in output per capita in 2020 ranged from -3.2% in Europe and

Central Asia to -7.8% in Latin America and the Caribbean. (PEW) MARCH 18,

2021 SUMMARY

OF POLLS

ASIA (India) Maruti Suzuki Is The Healthiest Automotive Brand In India Maruti

Suzuki tops YouGov’s 2021 Auto Rankings in India with an

Index score of 28.6. Despite this year’s global pandemic and consequent

economic downturns, the Indian auto manufacturer enjoys the best brand health

among consumers in India. The rankings were based on the Index score

from YouGov BrandIndex, which is a measure of overall brand

health calculated by taking the average of Impression, Quality, Value,

Satisfaction, Recommend and Reputation. (YouGov

India) March

16, 2021 (Thailand) Toyota Tops YouGov Thailand’s 2021 Automotive Rankings Toyota

tops YouGov’s 2021 Automotive Rankings for Thailand with an Index score

of +42.8, making it the car brand with the best overall brand health

according to Thais. The rankings are compiled using YouGov BrandIndex Index

score, a measure of overall brand health calculated by taking the average of

Impression, Quality, Value, Satisfaction, Recommend and Reputation scores.

The rankings are measured from 1 February 2020 to 31 January

2021. (YouGov

Thailand) March

16, 2021 (Malaysia) Honda Tops YouGov Malaysia’s 2021 Automotive Rankings Honda

tops YouGov’s 2021 Automotive Rankings for Malaysia with an Index score of

+37.9, making it the car brand with the best overall brand health according

to Malaysians. The rankings are compiled using YouGov BrandIndex Index score,

a measure of overall brand health calculated by taking the average of

Impression, Quality, Value, Satisfaction, Recommend and Reputation scores.

The rankings are measured from 1 February 2020 to 31 January. (YouGov Malaysia) MENA (Saudi

Arabia) Toyota Tops Yougov’s 2021 Automotive Rankings In Saudi

Arabia YouGov’s

2021 Automotive Rankings reveal Toyota enjoys the best brand health among

Saudi residents and tops the list with an Index score of 36. Along with the

parent brand, its luxury segment subsidiary- Lexus also makes a presence in

the list in third (with a score of 22.6). (YouGov

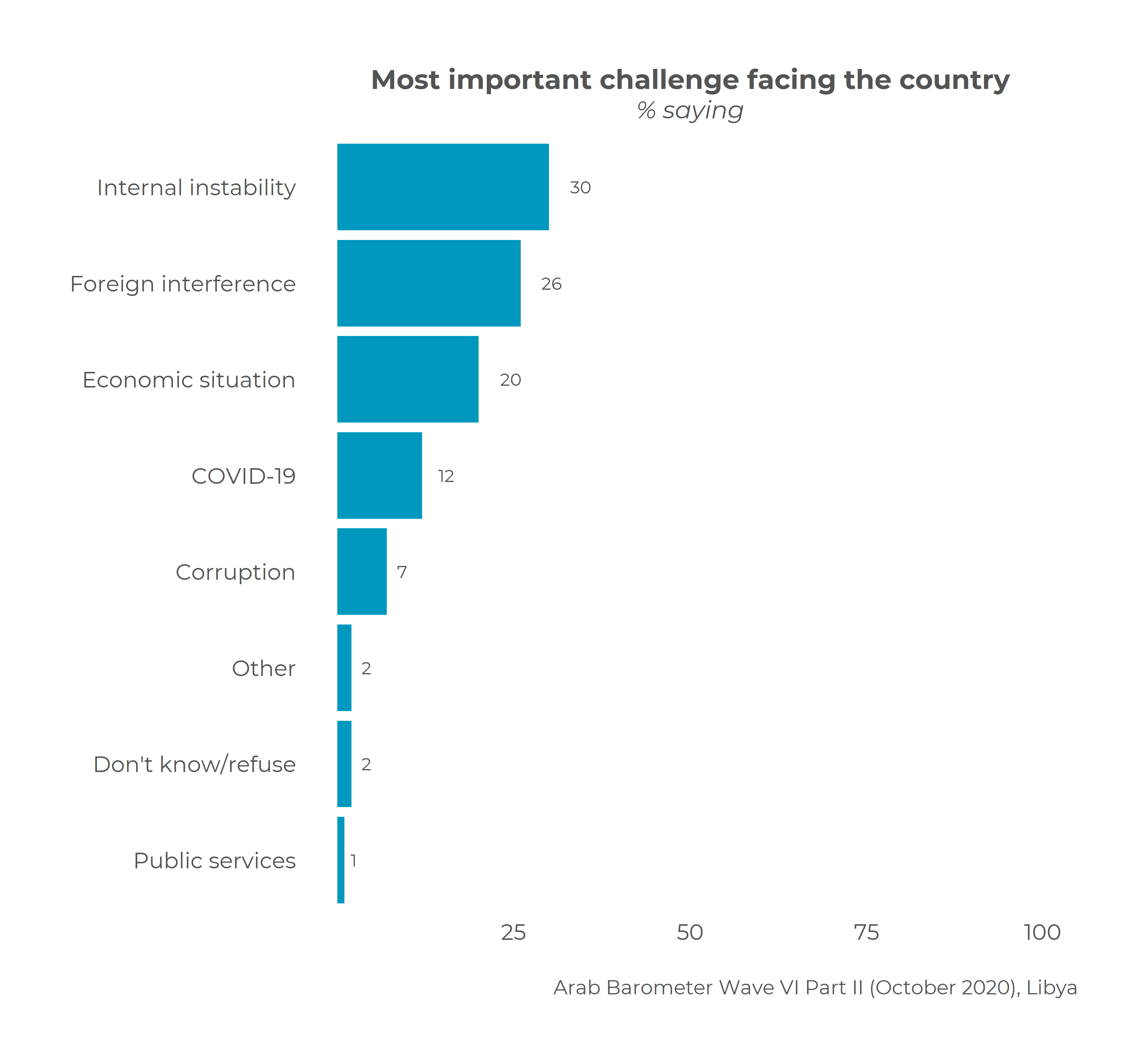

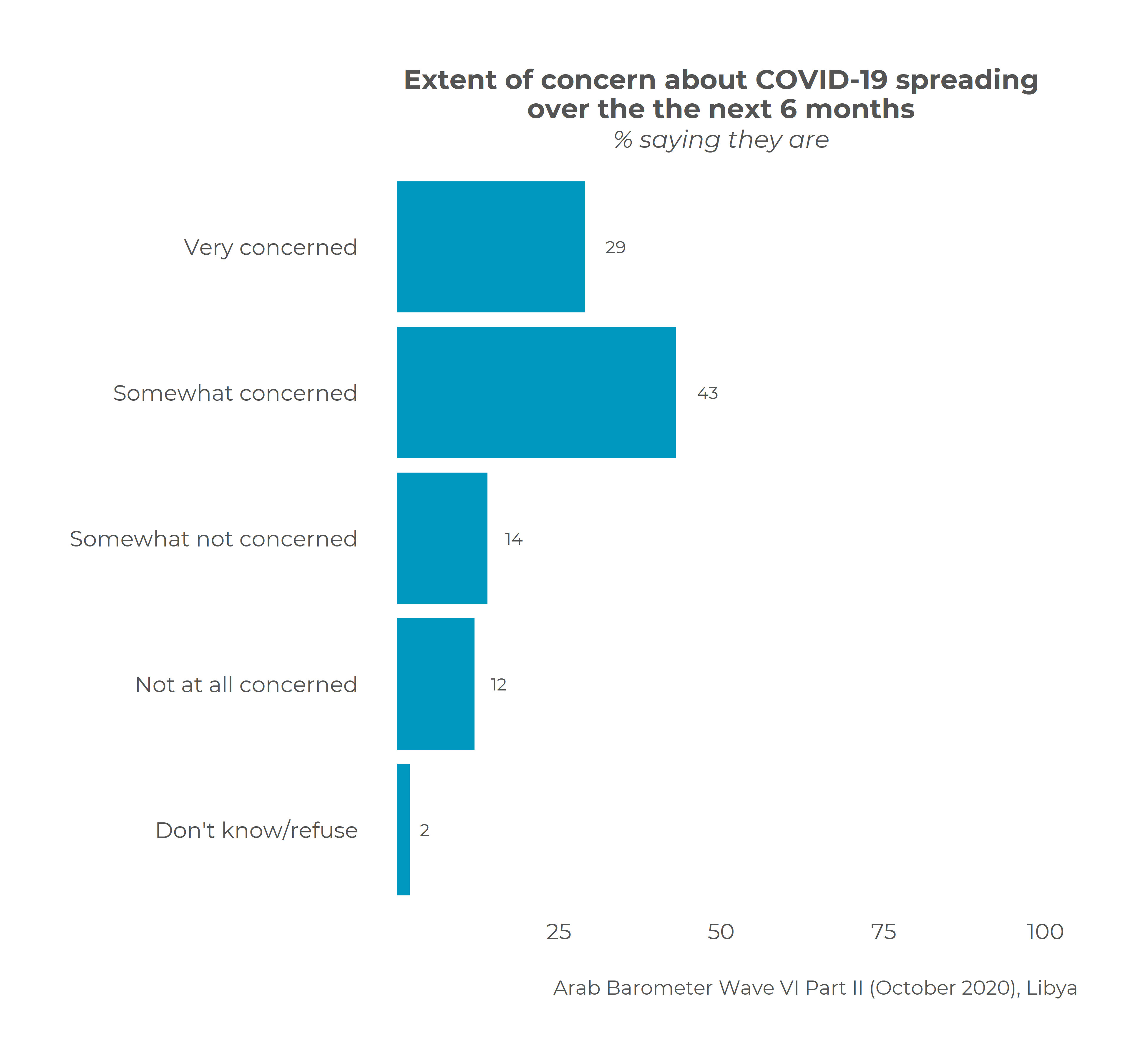

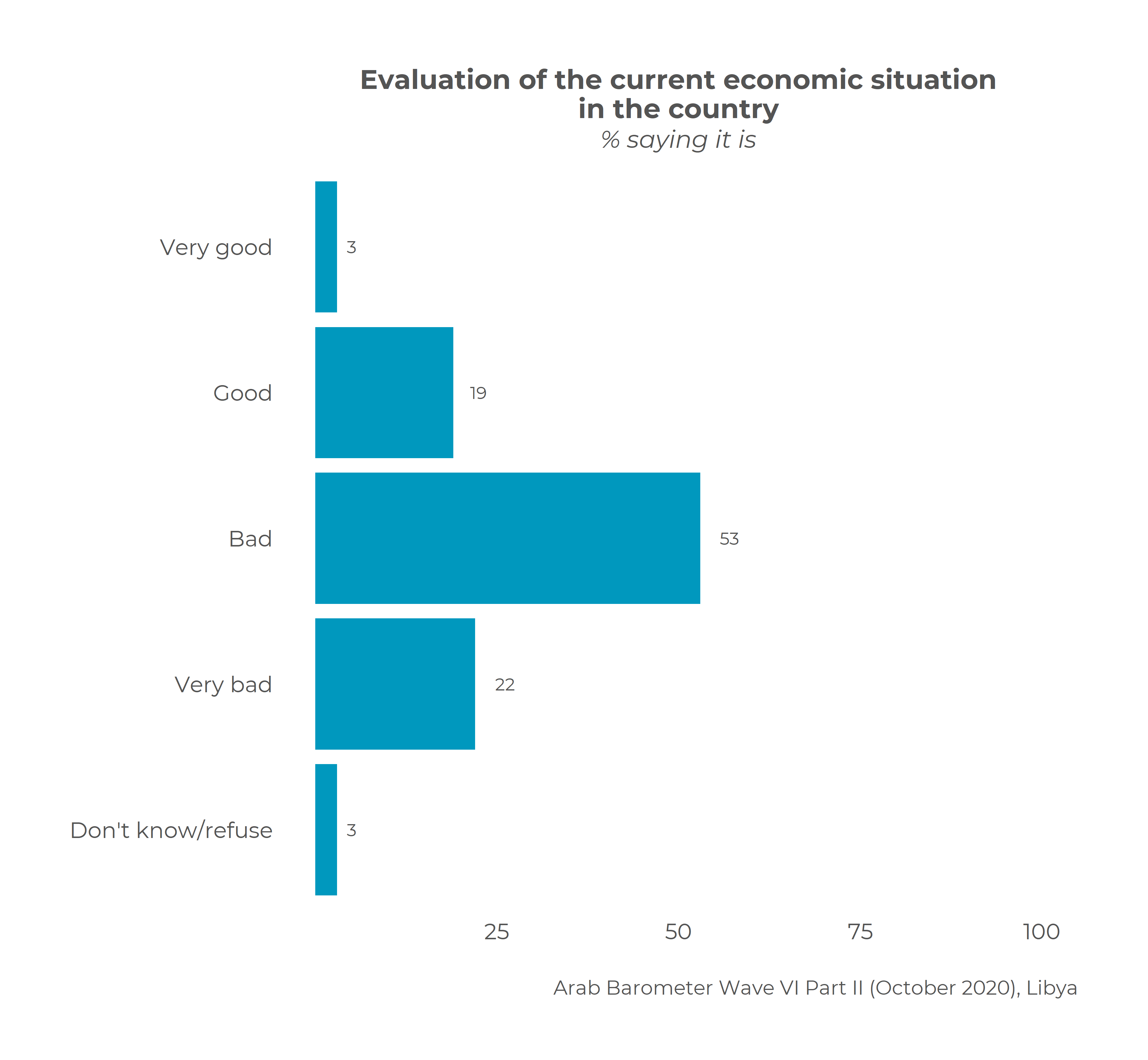

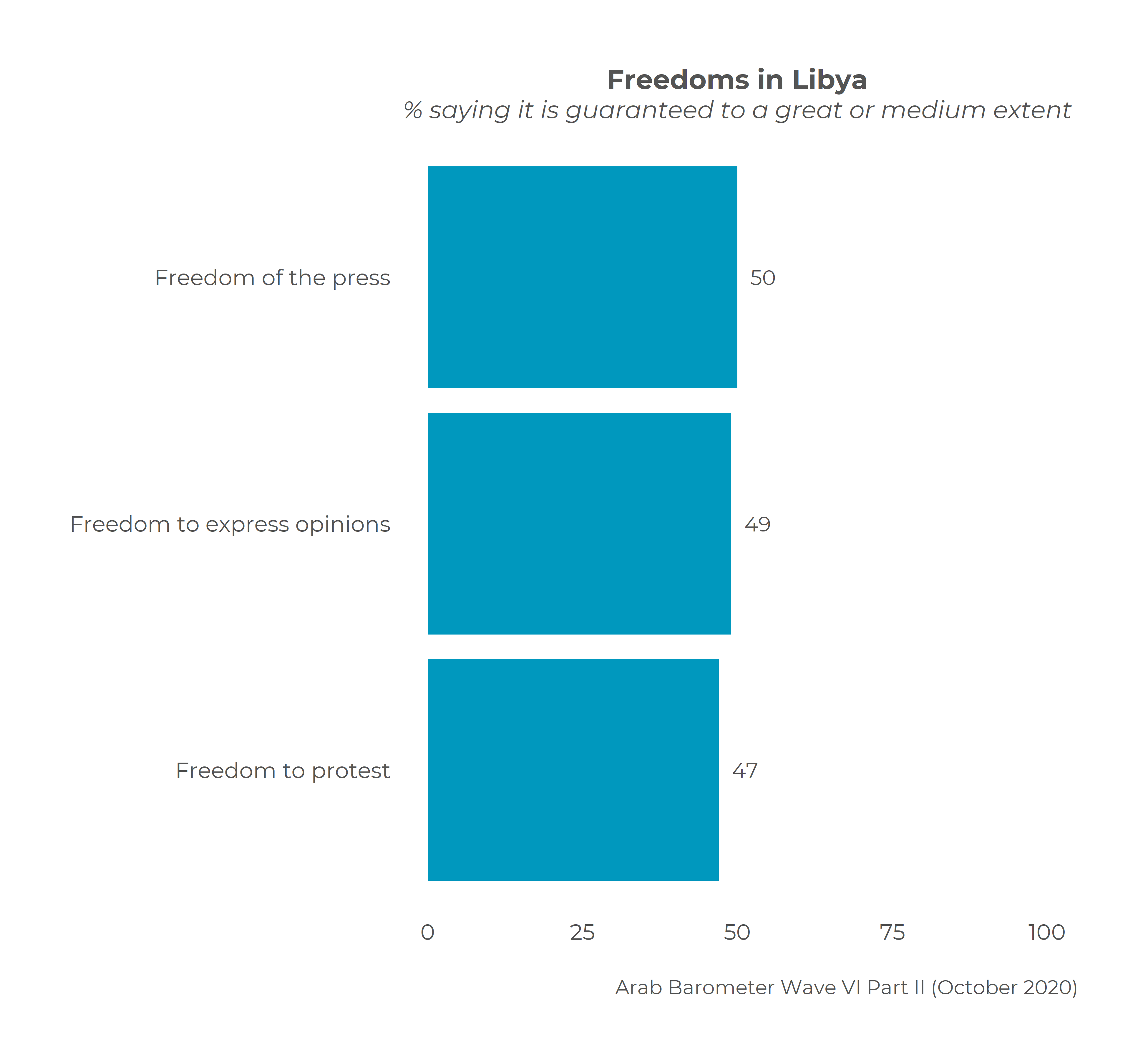

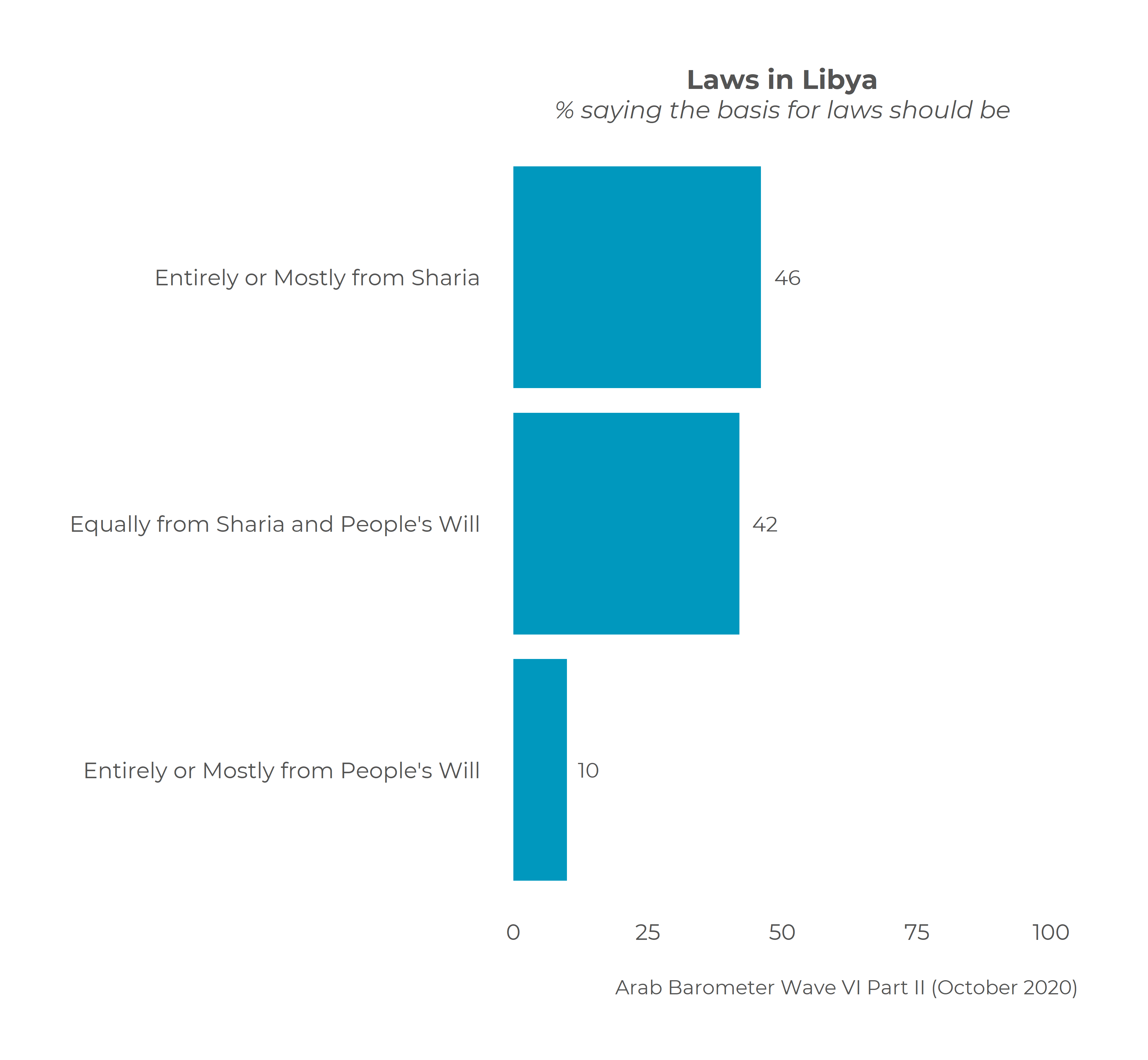

MENA) (Libya) Three-In-Four Libyans Say The Economy Is In A Very Bad Or A

Bad State When

asked about the most important challenge currently facing the country,

three-in-ten Libyans say it is the internal instability while 26% cite

foreign interference. The dire economic situation comes third with 20%, and

the COVID19 threat is seen by only 12% as the most important challenge facing

Libya. However, COVID19 remains a source of concern. The majority of Libyans

(72%) say they are very concerned or somewhat concerned about the spread of

the virus in the next 6 months. (Arabbarometer) March

16, 2021 AFRICA (Nigeria) Nine In 10 Nigerians (85%) Say They Are Concerned About

Kidnappings Almost

nine in 10 Nigerians (85%) say they are concerned about kidnappings and

attempted kidnappings in their state, including 55% who are “very concerned”

about this issue. Only 13% say they are either not that concerned or not

concerned at all. Apprehension about kidnappings is more widespread in the

three northern zones – North West (96%), North East (89%), and North Central

(87%) – than in the South. (Afrobarometer) March

18, 2021 WEST

EUROPE (UK) Six In Ten Do Not Want To Cut Spending On Public Services

To Pay Off Debt The new Ipsos MORI Political Monitor finds

that most Britons (54%) believe that the Government has spent about the right

amount on supporting ordinary people during the pandemic so far (29% say

they’ve spent too little). However, when it comes to future spending the

public are more split, with 45% thinking the Government will spend too little

on supporting ordinary people during the recovery from the pandemic and 40%

thinking they will spend the right amount. (Ipsos

MORI) 17

March 2021 43% Londoners Think Sadiq Khan Has Handled COVID Well Overall,

Londoners are split over Khan’s handling of the pandemic: 43% think he has

handled it well, while 39% think he has handled it badly. Labour voters (60%)

are the most likely to think Khan has handled the pandemic well, including

one in eight (12%) who think Khan has handled it “very well”. However, around

a quarter of Labour voters (26%) are not happy with Khan’s performance and

think he has handled the pandemic badly. (YouGov

UK) March

18, 2021 Less Than Half Of Britons Expected To Tick ‘Christian’ In

Uk Census The once-a-decade snapshot of the country

has included a voluntary question about religion since 2001. In 2011, returns

across England and Wales, Scotland, and Northern Ireland showed 59.3%

ticking Christianity, a fall from 71.6% a decade earlier. Day predicted the proportion of people ticking

Christianity “could drop below 50%”. Peter Brierley, an expert on religion

statistics, said he predicted 48% or 49% identifying as Christian, but David

Voas, head of the social sciences department at University College London,

said he would be surprised if the figure fell below 50%. (The

Guardian) March

20, 2021 (France) 1 In 2 French People Think The Pandemic Has

Exacerbated Ethnic Discrimination 7

out of 10 French people believe that the criteria of origin influence

the possibilities of access to housing. 69% of French people surveyed

also believe that they condition access to employment and 63% that they

determine access to education. Almost a quarter (24%) of French

people surveyed declared having had personal experience of situations in

which they considered their origin to have been an obstacle. More than

half (52%) of French people (n ° 2 after Spain) think that the

pandemic has exacerbated discrimination - employment, education, housing or

social services - linked to ethnic origins. (Ipsos

France) March

21, 2021 (Germany) Youtube Is The Most Popular Online Music Service Among

Germans Not

only video but also audio streaming was the focus, in the latter case

especially podcasts and music streaming. In this context, 35 percent of

Germans state that they currently use the YouTube platform, regardless of

whether they have free or paid access. This is what respondents aged 18

to 44 say most often (41-42 percent). The streaming portal Spotify only

ranks second among all German respondents with 21 percent, but it is more

important for the 18 to 29 year olds: Half (50 percent) of that age group

state that they currently use Spotify. (YouGov

Germany) March

19, 2021 71% Of 14 To 24-Year-Olds State That They Have Good Social

Contacts With Friends The

proportion of 14 to 24-year-olds who state that they have good social

contacts with friends has decreased by ten percentage points to 71 percent

during this period. In terms of contacts with family members, the

difference compared to the survey from December 2019 is eight percentage

points. Likewise, the proportion of those who can “be there for others”

to the desired extent falls in Generation Z by eight percentage points to 52 percent.

(Ipsos

Germany) 18

March 2021 (Finland) Finland's Strongest Car Brands When

Finns evaluate car brands on six indicators (quality, general image, value

for money, willingness to recommend, reputation and satisfaction), Toyota

ranks number one. Volvo grabs second place in the Finnish rankings and

Mercedes-Benz third place. In addition to Mercedes-Benz, several German

brands will rise to the TOP10 list. Volkswagen is fourth, Audi fifth and

BMW sixth. Japanese brands can also be found on the list in addition to

Toyota, with Honda ranked nineth and Nissan ranked tenth. (YouGov

Finland) March

16, 2021 (Hungary) Above 50% Vaccination Propensity In Hungary Rejection

is highest in the under-30 age group, at 56%, compared to only

32%. Among those over 50, the proportion is just the opposite. In

absolute terms, two-thirds of the population who have received at least one

vaccination is over 60, and two-thirds are also women. Half of those who

oppose the vaccine are under the age of 40 (although they make up 38% of the

adult population), yet vaccination can be measured at the same rate among

both sexes. (Ipsos

Hungary) March

16, 2021 NORTH AMERICA (USA) 69 Americans Say It Is Very Important For Federal Law

Enforcement Agencies To Find And Prosecute The People Who Broke Into The U.S.

Capitol On Jan 6 The

survey by Pew Research Center, conducted March 1-7, 2021, among 12,055 U.S.

adults who are members of the Center’s nationally representative American Trends Panel, finds a wide majority of Americans (69%) saying

it is “very important” for federal law enforcement agencies to find and

prosecute the people who broke into the U.S. Capitol on Jan. 6. Another 18%

say doing this is “somewhat important.” Just 12% say this is not too or not

at all important. (PEW) MARCH

18, 2021 AUSTRALIA Toyota Tops YouGov Australia’s 2021 Automotive Rankings Toyota

tops YouGov’s 2021 Automotive Rankings for Australia with an Index score of

+43.9, making it the car brand with the best overall brand health according

to Australians. The rankings are compiled using YouGov BrandIndex Index

score, a measure of overall brand health calculated by taking the average of

Impression, Quality, Value, Satisfaction, Recommend and Reputation scores.

The rankings are measured from 1 February 2020 to 31 January 2021. (YouGov

Australia) March

16, 2021 73.7% Of Australians Holding Private Health Insurance Are Satisfied Australia’s

largest fund by market share, Medibank Private, had a satisfaction rating of

69.8%, one of the lowest of the more than two dozen funds measured. BUPA,

which is a close second in terms of market share, had a slightly higher score

of 71.5%. Each of those funds has more than twice as many members as the next

largest fund, HCF, which had a customer satisfaction rating of 75%. (Roy

Morgan) March

17 2021 Movement Of People In Melbourne Cbd Is At 39% Of Normal One Year

After The First Covid Lockdown The Adelaide CBD has been the standout

performer over the last two months with movement levels in mid-March now at

83% of the pre-COVID-19 levels and above 70% since the start of February.

Movement levels in the Adelaide CBD have averaged more than 10% higher than

either Brisbane CBD, Perth CBD or Hobart CBD during the last two months. (Roy

Morgan) March

19 2021 MULTICOUNTRY STUDIES Global Consumer Confidence Getting Closer To Pre-Pandemic

Level Six of the 24 surveyed markets show

significant growth in their National Index when compared to February 2021:

Great Britain (+3.6), the United States (+2.2), Belgium (+1.8), Canada

(+1.7), Japan (+1.7), and Turkey (+1.6). Meanwhile, not a single market has experienced

a significant drop, defined as 1.5 index points or more. (Ipsos

Egypt) 17

March 2021 81% Of Spanish Mothers And Fathers Feel Judged By Others On

a global average, 82% parents interviewed in the countries where the study

was carried out, feel judged. A percentage very similar to that

of Spain, where 81% of parents feel questioned about their parenting

method . Positioning itself as the third country in Europe that

feels the most judged in this regard, only behind Poland (91%) and the United

Kingdom and Hungary (both with 83%). Germany, Holland and France, all of

them with the same percentage (77%), are the Europeans who feel less

questioned. (Ipsos

Spain) March

17, 2021 After Covid-19: Putting People Before Politics Is Key To

Recovery Mentioned

by a third of people (33%) and equally likely to be picked out by men and

women, the most important quality that people want from their political

leaders in order to be considered to do a good job in handling the recovery

from the pandemic is to put their country’s needs before politics. This is

followed by being honest with the public (29%), understanding the problems

facing ordinary people (28%), taking into account the impact on the economy

as well as on health (25%) and making the right decisions at the right time

(25%). (Ipsos

South Africa) 18

March 2021 The Pandemic Stalls Growth In The Global Middle Class,

Pushes Poverty Up Sharply Global

poverty had abated at an average rate of 49 million annually from 2011 to

2019, with the number of global poor falling from 1.10 billion to 691 million

during this period. The pandemic, by adding 131 million to the ranks of the

poor, has set the progress on poverty back by several years, and the poverty

rate is estimated to have increased from 9.0% in 2019 to 10.4% in 2020. (PEW) MARCH

18, 2021 ASIA

682-43-01/Poll Maruti

Suzuki Is The Healthiest Automotive Brand In India

Maruti Suzuki

tops YouGov’s 2021 Auto Rankings in India with an Index

score of 28.6. Despite this year’s global pandemic and consequent economic

downturns, the Indian auto manufacturer enjoys the best brand health among

consumers in India. The rankings were based on the Index

score from YouGov BrandIndex, which is a measure of overall

brand health calculated by taking the average of Impression, Quality, Value,

Satisfaction, Recommend and Reputation1.

The 2021 rankings show urban Indians’

strong affinity towards Japanese auto brands. After Maruti Suzuki, Honda

takes the second place with a score of 27.2. Honda particularly seems to have had a

great year despite the pandemic. The brand created awareness about the

pandemic through its successful ad campaign “Until we drive again

#Stayathome” created entirely from home. Apart from this, the Japanese car

manufacturer took several steps to ensure the safety, well-being and

convenience of its customers and dealers across the country amidst a national

lockdown. Along with the parent brand, Honda 2

wheelers also makes an entry into the list at nine (with a score of 19.8). Hyundai and Toyota take the sixth (21.7)

and tenth (17.2) place, respectively. German luxury auto brands BMW, Audi and

Mercedes Benz take fifth, seventh and eighth place in the rankings, with a

score of 22.2, 20.2 and 19.9, respectively. Despite stiff competition from foreign

brands, two Indian brands make an appearance in the list: Royal Enfield at

third (score of +23.3) and Tata Motors at fourth (score of +23.2)

Commenting on the research, Deepa

Bhatia, General Manager at YouGov India said: “YouGov’s 2021 Auto Rankings reveals the healthiest

auto brands in the market. The Indian rankings show a dominance of Japanese

car brands or their subsidiaries, with five leading brands making up the top

10 list. Affinity towards German luxury cars is also strong among urban

Indians. In an overall tough year for carmakers, it

is good to see Indian brands Tata Motors and Royal Enfield strengthening

their place amidst global players and enjoying good brand health among Indian

consumers. (YouGov India) March 16, 2021 Source: https://in.yougov.com/en-hi/news/2021/03/16/maruti-suzuki-healthiest-automotive-brand-india/ 682-43-02/Poll Toyota Tops

YouGov Thailand’s 2021 Automotive Rankings

Toyota tops YouGov’s 2021 Automotive

Rankings for Thailand with an Index score of +42.8, making it the car

brand with the best overall brand health according to Thais. The rankings are compiled using

YouGov BrandIndex Index score, a measure of overall brand health

calculated by taking the average of Impression, Quality, Value, Satisfaction,

Recommend and Reputation scores. The rankings are measured from 1 February

2020 to 31 January 2021.

Toyota tops the charts in every metric except

for one, particularly when it comes to Value (measuring the brand that

consumers think is the most value-for-money) with a score of +45.5, making it

9.8 points ahead Honda (Cars), the brand with the next highest score in this

metric (+35.7). The one metric however that Toyota does not score top in is

for Satisfaction (which measures how satisfied consumers are with that

brand), narrowly beat out by Honda (Motorcycles) (+30.4). Japanese brands dominate the top ten, with

Honda (Cars) in second (+36.8), Honda (Motorcycles) in third (+32.0), Isuzu

in fifth (+24.9), Mazda in seventh (+18.9), Yamaha in eighth (+18.5), Nissan

in ninth (+17.9) and Mitsubishi in tenth (+15.8). German automotive manufacturers make up the

rest of the top ten. BMW comes in fourth (+25.5) and Mercedes-Benz in sixth

(+20.1). They both fare well in the Reputation metric (which measures the

corporate reputation of a brand by asking which brands consumers would be

proud of working for). BMW comes in third (+35.0) and Mercedes-Benz in fourth

(+29.3). (YouGov Thailand) March 16, 2021 Source: https://th.yougov.com/en-th/news/2021/03/16/toyota-tops-yougov-thailands-2021-automotive-ranki/ 682-43-03/Poll Honda Tops

YouGov Malaysia’s 2021 Automotive Rankings

Honda tops YouGov’s 2021 Automotive

Rankings for Malaysia with an Index score of +37.9, making it the car brand

with the best overall brand health according to Malaysians. The rankings are compiled using YouGov

BrandIndex Index score, a measure of overall brand health calculated by

taking the average of Impression, Quality, Value, Satisfaction, Recommend and

Reputation scores. The rankings are measured from 1 February 2020 to 31 January

2021. While Honda tops the list overall, there

are three metrics where it falls behind other brands. It is beaten out by

local car manufacturer Perodua (+44.0) by a big margin when it comes to Value

(measuring the brand consumer see as most value-for-money), and Toyota

(+35.5) by a small margin – Honda comes in third (+35.2). Perodua (+29.6)

also beats out Honda (+21.5) when it comes to Satisfaction (which measures

how satisfied consumers are with that brand). By scoring top marks in Value

and Satisfaction, and high scores in other metrics, Perodua comes in third

place overall (+33.6). Honda is also beaten out by Mercedes-Benz

when it comes to Reputation (which measures the corporate reputation of a

brand by asking which brands consumers would be proud of working for). The

German automotive brand holds a Reputation score of +39.3, followed by BMW

(+38.8) and then Honda (+38.1). The brand Malaysians would be least proud to

work for is Proton (+14.9). Japanese brands dominate the top ten.

Toyota comes in second (+36.1), Nissan in eighth (+14.4) and Mazda in tenth

(+12.9). German brands also fare well with Mercedes-Benz in fourth (+23.4),

BMW in fifth (+23.3). Malaysia’s national car brand Proton places

sixth (+18.4), and the list is rounded off with British brand Range Rover in

ninth (+13.2). (YouGov Malaysia) Source: https://my.yougov.com/en-my/news/2021/03/16/honda-tops-yougov-malaysias-2021-automotive-rankin/ MENA

682-43-04/Poll Toyota Tops

Yougov’s 2021 Automotive Rankings In Saudi Arabia

YouGov’s 2021 Automotive Rankings reveal

Toyota enjoys the best brand health among Saudi residents and tops the list

with an Index score of 36. Along with the parent brand, its luxury segment

subsidiary- Lexus also makes a presence in the list in third (with a score of

22.6). YouGov 2021 BrandIndex Automotive Ranking

is determined using Index score – which assesses overall brand health. The score

takes into account consumers’ perception of a brand’s overall quality, value,

impression, reputation, satisfaction and whether consumers would recommend

the brand to others.

The 2021 rankings show Saudi residents’

affinity towards Japanese auto brands as they occupy four spots in the

rankings. Along with Toyota and Lexus, Honda and Nissan are also present in

the list, at sixth (17.6) and eight place (13.8), respectively. German luxury car brands are not far behind

and are equally well represented, with Mercedes Benz and BMW landing at

second (with a score of 29.7) and fourth (22.5), respectively, and Audi at

ninth place (13.7). The launch of the BMW X series and Audi’s new E-commerce

platform last year (enabling customers to buy Audi cars online during the

pandemic) may have helped the luxury carmakers strengthen their position in

the market and secure a place in the 2021 rankings. Hyundai is ranked fifth (19.6), while

American car brands Ford and GMC, took the seventh (16.2) and tenth spot

(13.6), completing the list of KSA’s top ten auto brands in 2021. Commenting on the rankings, Scott

Booth of YouGov said, “Like many

other industries automakers also suffered the impact of the Coronavirus

lockdowns. However, things seem to have gradually improved as vaccination

efforts expand across the world. Our data shows that Saudi residents have a

strong affinity towards Japanese automakers with four of the leading brands

making the top 10 list this year. Not far behind are German luxury cars that

enjoy strong brand health among the population. The rankings show that

despite the impact of the pandemic on consumer purchasing patterns, the

strength of bellwether auto brands remains and they maintain strong brand

health in the country." (YouGov MENA) Source: https://mena.yougov.com/en/news/2021/03/16/toyota-tops-yougovs-2021-automotive-rankings-saudi/ 682-43-05/Poll Three-In-Four

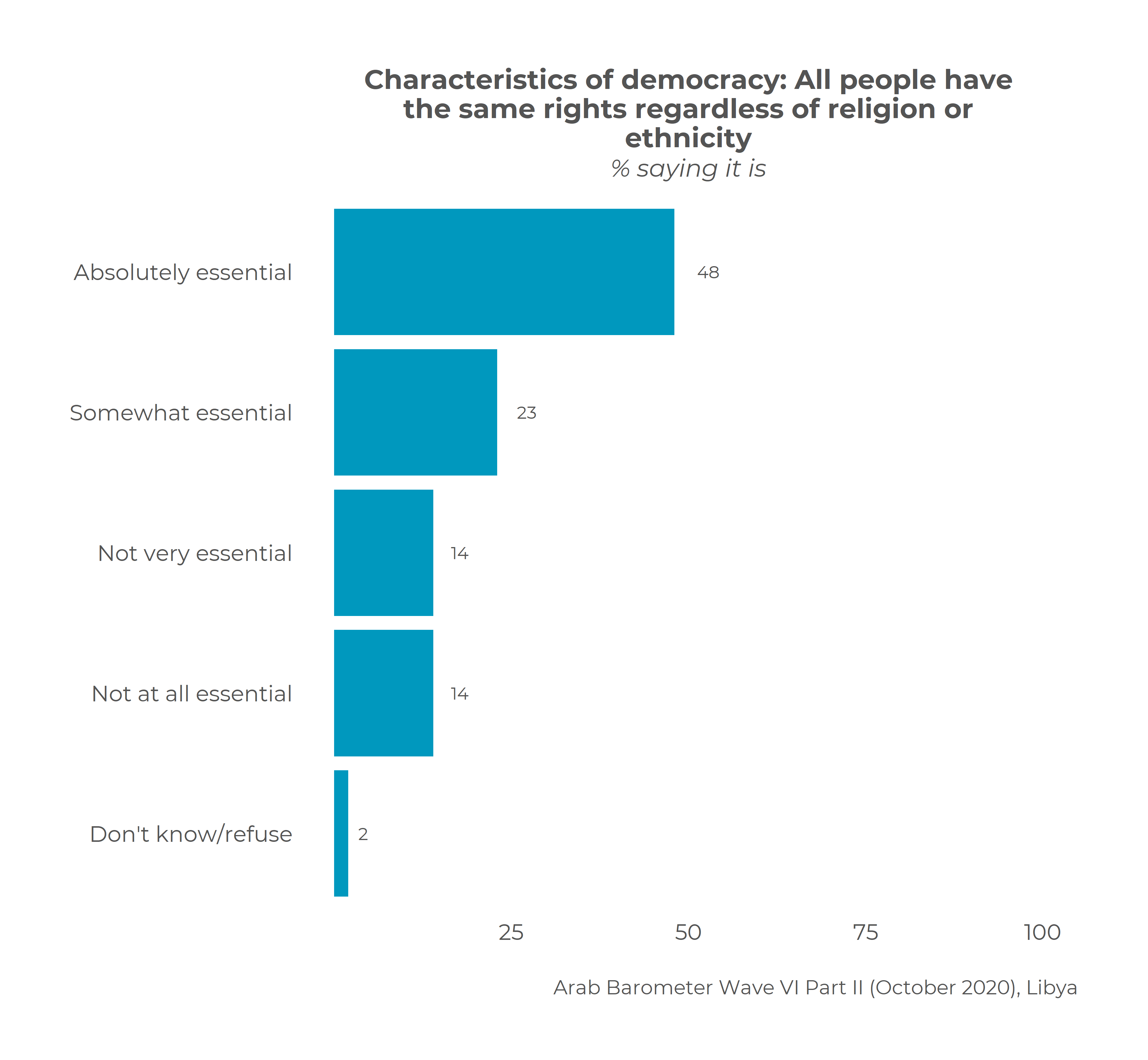

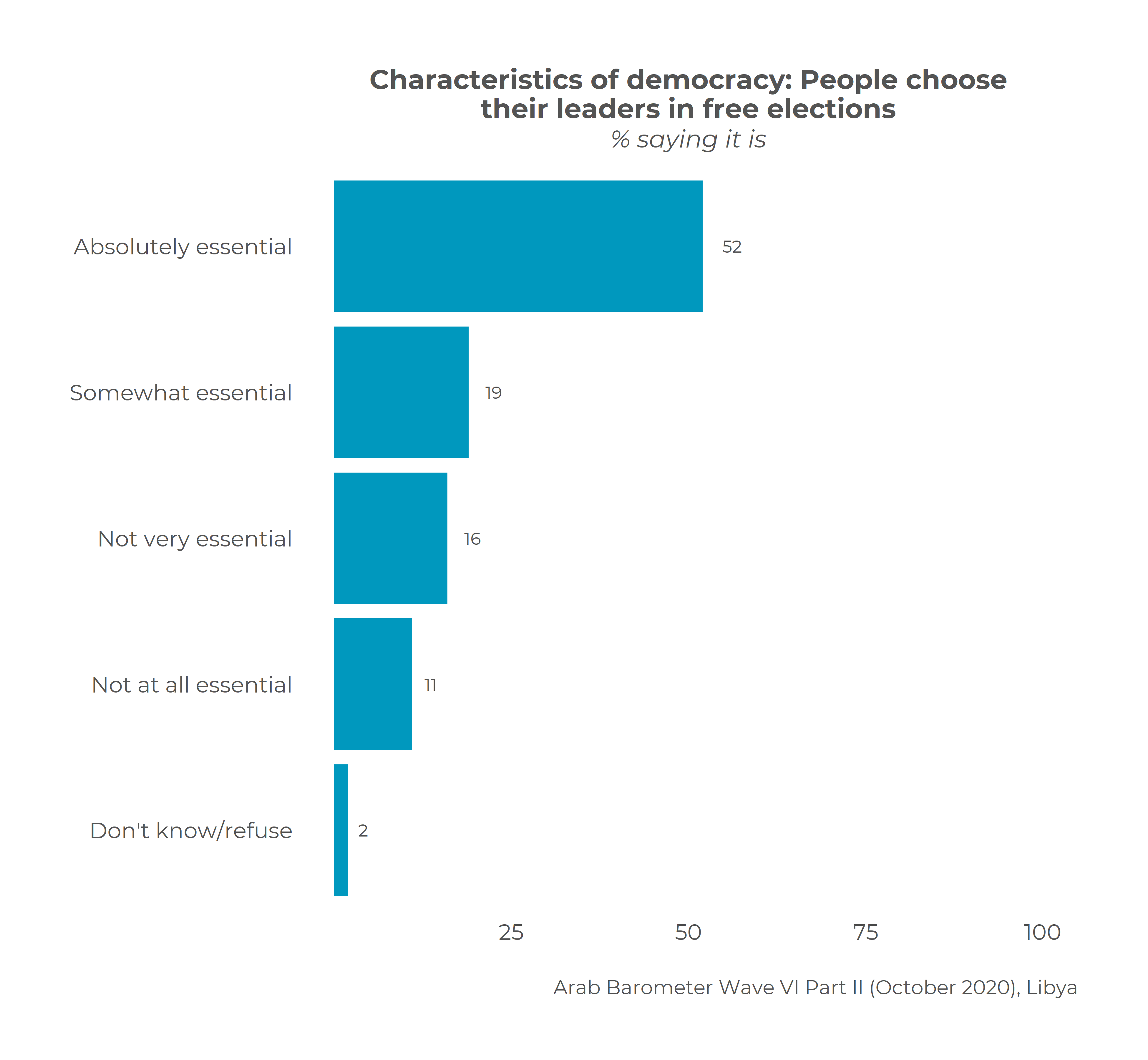

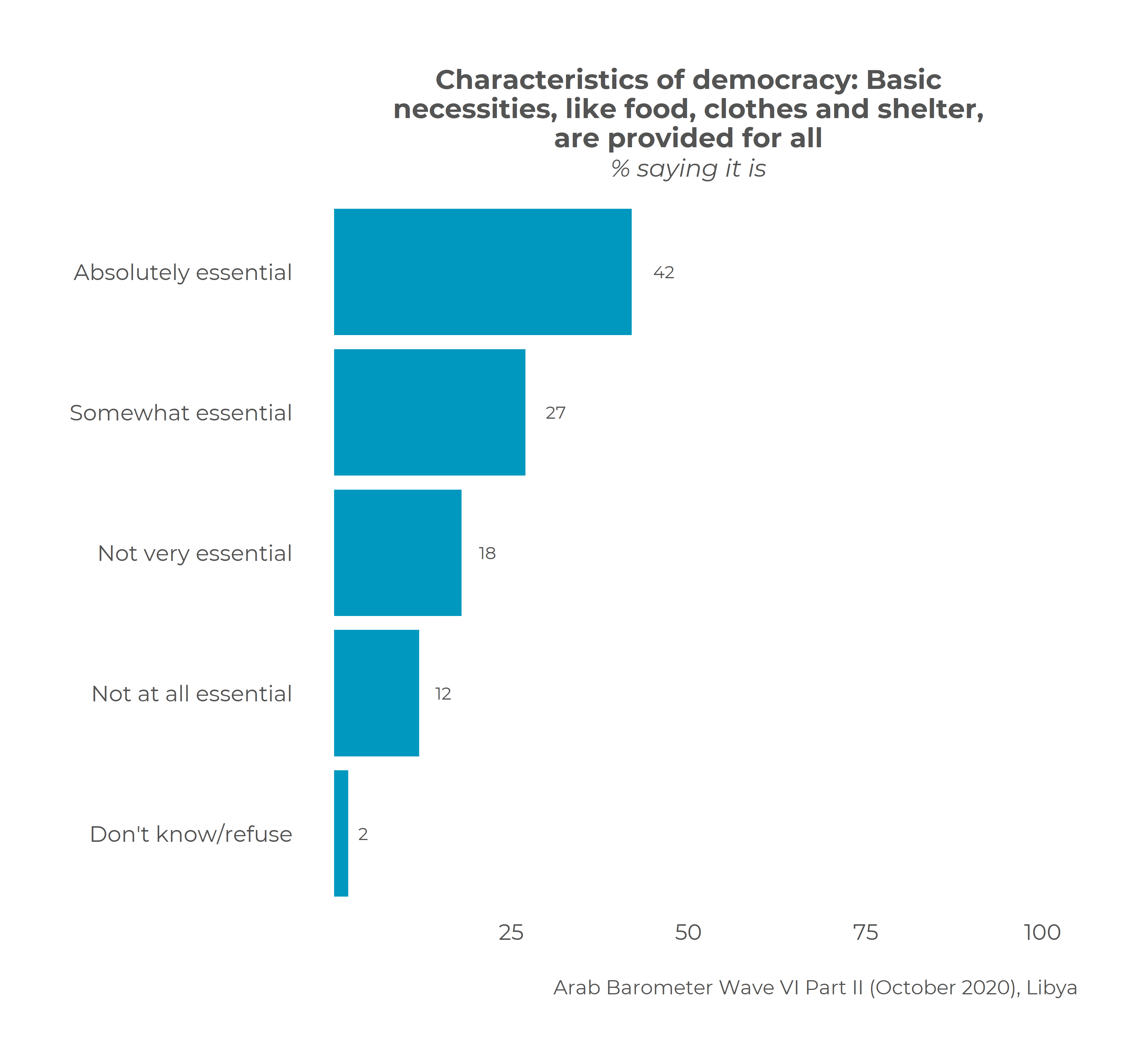

Libyans Say The Economy Is In A Very Bad Or A Bad State

The following are among the key findings

from a nationally-representative public opinion survey conducted in Libya by

Arab Barometer in October 2020. The survey conducted 1008 phone interviews

with randomly-selected Libyan citizens aged 18 or older. This unique survey

captures the sentiments of Libyan citizens during the unprecedented times of

the COVID-19 pandemic. The survey has a margin of error of ± 3 percent. Key facts and figures EVALUATION OF CURRENT SITUATION

VIEWS ON DEMOCRACY

VIEWS ON FOREIGN POWERS

(Arabbarometer) March 16, 2021 Source: https://www.arabbarometer.org/2021/03/fact-sheet-libyas-pulse-during-the-covid-19-pandemic/ AFRICA

682-43-06/Poll Nine In 10

Nigerians (85%) Say They Are Concerned About Kidnappings

Abuja, Nigeria – March 2, 2021: Most

Nigerians are concerned about kidnappings and attempted kidnappings in their

state, the most recent Afrobarometer study shows. The apprehension is

widespread among all socio-demographic groups and highest in northern

Nigeria. The study also shows that crime/security is

among the three most important problems that Nigerians want their government

to address. Kidnappings by extremists and criminal

gangs have plagued Nigeria in recent years, especially in the North. Hundreds

of schoolgirls in Zamfara State were kidnapped last Friday, and later

released, and about 26 people, including a chief imam, were kidnapped in

Niger State on Saturday – the same day that 42 students kidnapped in the same

state were ransomed. Key findings

Afrobarometer surveys Afrobarometer is a pan-African, nonpartisan

survey research network that provides reliable data on African experiences

and evaluations of democracy, governance, and quality of life. Seven rounds

of surveys were completed in up to 38 countries between 1999 and 2018. Round

8 surveys in 2019/2021 are planned in at least 35 countries. Afrobarometer

conducts face-to-face interviews in the language of the respondent’s choice

with nationally representative samples. The Afrobarometer team in Nigeria, led by

NOIPolls, interviewed 1,599 adult citizens of Nigeria in January-February

2020. A sample of this size yields country-level results with a margin of

error of +/-2.5 percentage points at a 95% confidence level. Previous surveys

were conducted in Nigeria in 1999, 2002, 2005, 2007, 2008, 2012, 2014, and

2017. Charts Figure 1: Concerns about kidnapping |

Nigeria | 2020

Respondents were asked: How concerned

are you about the problem of kidnappings and attempted kidnappings in your

state? Figure 2: Concerns about kidnapping | by

zone | Nigeria | 2020

Respondents were

asked: How

concerned are you about the problem of kidnappings and attempted kidnappings

in your state? (% who say “somewhat concerned” or “very concerned”) Figure 3: Top 10 most important problems |

Nigeria | 2020

(Afrobarometer) March 18, 2021 Source: https://noi-polls.com/kidnap-poll-afrobarometer-round-8-2020-survey-findings-in-nigeria/ WEST

EUROPE

682-43-07/Poll Six In Ten Do Not Want To Cut Spending On Public Services To Pay Off

Debt

The new Ipsos MORI Political Monitor finds that most Britons (54%)

believe that the Government has spent about the right amount on supporting

ordinary people during the pandemic so far (29% say they’ve spent too

little). However, when it comes to future spending the public are more split,

with 45% thinking the Government will spend too little on supporting ordinary

people during the recovery from the pandemic and 40% thinking they will spend

the right amount. This is largely spilt along party lines with two in three

Conservative supporters (66%) saying the Government will spend the right

amount (20% say too little) while 68% of Labour supporters believe it will

spend too little (24% say the right amount). When asked if there is a “real need to cut spending on public

services in order to pay off the very high national debt”, 26% agree but 61%

disagree – similar to the balance of opinion when last asked in August 2018

(when 19% agreed and 58% disagreed). However, this is very different to the

years after the financial crash in 2010, when most Britons believed there was

a need to cut spending to pay off the debt (for example, by 59% to 32% in

October 2010). Conservatives are more split on the matter, although are still

more likely to oppose spending cuts with 38% agreeing and 48% disagreeing,

while Labour supporters are more aligned with 12% agreeing and 75%

disagreeing. When it comes to the recent Budget half (52%) believe it is good

for the country (25% say bad) – similar to levels seen after the March 2020

budget (54% good vs 22% bad). The last Budget previous to this that achieved

similar ratings was in June 2010. Fewer however say that the Budget is good

for them personally (39% good vs 26% bad), slightly lower than in 2020 (45%

said good and 24% bad).

Other key findings from the budget include:

However, nearly four in five (78%) members of the public believe that

the pay rise of 1% for most NHS staff in England is too little. One in five

(20%) believe it is the right amount, and only 7% think it is too much. Even

Conservative supporters are at odds with the policy where 66% say that it is

too little (32% say it’s the right amount), as do 91% of Labour supporters. Overall, though, Rishi Sunak remains popular amongst the public.

Three in five (59%) are satisfied with the way he is doing his job at Chancellor

(up 3 points from February) while 27% are dissatisfied. When asked whether

Rishi Sunak or Boris Johnson would make the most capable Prime Minister the

public are split – 42% say Sunak and 41% say Johnson. Conservatives however

are more likely to favour the PM (70% vs. 24% for Sunak) while Labour

supporters are more likely to favour Sunak (57% vs. 24% for Johnson). The

public are also split when it comes to asking if either Rishi Sunak or Keir

Starmer would make the most capable Prime Minister (39% say Sunak and 37% say

Starmer).

Gideon Skinner, Head of Political Research

at Ipsos MORI, said: It looks like the politics of public

spending post-Covid will be quite different to the reaction to the financial

crash. Although then there was agreement that cuts were needed, now Britons

don’t want to see further austerity. Broadly, the reaction to the recent

Budget and the Chancellor’s satisfaction levels suggest that the public

believes that Rishi Sunak is getting the balance right, although there is

some concern that the recovery won’t see enough support for ordinary people –

especially among those in their twenties and early thirties. (Ipsos MORI) 17 March 2021 Source: https://www.ipsos.com/ipsos-mori/en-uk/six-ten-do-not-want-cut-spending-public-services-pay-debt 682-43-08/Poll 43% Londoners Think Sadiq Khan Has Handled COVID Well

With the mayoral election fast approaching, how do Londoners think incumbent

candidate Sadiq Khan has handled the pandemic ahead of visiting the polls? Overall, Londoners are split over Khan’s handling of the pandemic:

43% think he has handled it well, while 39% think he has handled it badly.

Labour voters (60%) are the most likely to think Khan has handled the

pandemic well, including one in eight (12%) who think Khan has handled it

“very well”. However, around a quarter of Labour voters (26%) are not happy

with Khan’s performance and think he has handled the pandemic badly. While a similar number of Liberal Democrats (52%) think Khan is

handling the pandemic well, Conservatives are more likely to think that Khan

has handled the pandemic badly (68%) - including 41% of Tory voters who think

Khan has handled the issue of COVID-19 “very badly”. Khan’s rating among Londoners puts him slightly behind that of

the UK government among Britons,

YouGov’s latest research shows that 50% of all Britons think the government

is handling the pandemic well, versus 45% of the population who think they

are handling it badly. However, in the devolved nations, people are much more positive of

their own government’s handling. Some six in ten (60%) of Welsh people think

the Welsh government are

handling the crisis well while 33% think they are handling it badly. Scots

held similar feelings in January, when 60% said the Scottish government was

handling the pandemic well, compared to 36% who thought it was handling the

crisis badly. (YouGov UK) March 18, 2021 682-43-09/Poll Less Than Half Of Britons Expected To Tick ‘Christian’ In Uk Census

The “post-Christian era” in the UK will be cemented by data emerging

from Sunday’s census which

is expected to show further generational disengagement from organised

religion, according to a leading academic. The once-a-decade snapshot of the country has included a voluntary

question about religion since 2001. In 2011, returns across England and

Wales, Scotland, and Northern Ireland showed 59.3% ticking Christianity, a fall from 71.6% a

decade earlier. Abby Day, professor of race, faith and culture at Goldsmiths,

University of London, expects this year’s census to show a further erosion in

Christian identity, mainly because postwar generations regard the church as

irrelevant and immoral. Day predicted the proportion of people ticking Christianity “could

drop below 50%”. Peter Brierley, an expert on religion statistics, said he predicted

48% or 49% identifying as Christian, but David Voas, head of the social

sciences department at University College London, said he would be surprised

if the figure fell below 50%. According to Day, further decline was largely due to baby boomers –

people born between 1946 and 1964 – raising their children outside the

institutions of religion. “Religion tends to be transmitted within families. But many baby

boomers, who were largely brought up by people who went to church,

dramatically broke with that,” she told the

Observer. “Baby boomers have since raised a generation of millennials who don’t

go to church. And people who weren’t brought up as practising Christians

generally don’t become religious later in life. You don’t get many teenagers

walking into churches when they haven’t been before.” Based on recent interviews with about 50 baby boomers who were brought

up in Christian families, Day said many had rejected church in favour of

values considered to be more relevant, inclusive and humane. “Post-Christians are motivated by ethics concerning gender and sexual

equality, social justice, climate change and compassion. The churches failed

to deliver on those moral issues and so lost moral authority. “Today’s younger generations have a different sense of soul, meaning

and morality, and it’s one that rejects the church’s record of abuse, racism,

homophobia and sexism,” she said. Church

of England data shows that average Sunday

attendance in 2019 was 600,000 adults, or fewer than 1% of the population. A

third of those attending church were aged 70 or over. Figures from the 2018 British Social Attitudes (BSA)

survey showed that 52% of the UK public said they did

not belong to any religion, 38% identified as Christian, and 9% identified

with other faiths.

But in the last census,

only 25% of the population said they had no religion. According to Voas, the

difference in wording between the census question in England and Wales and

the BSA question is “critical”. “The BSA question is, ‘Do you regard yourself as belonging to a religious

group?’ That notion of belonging pushes people to think, ‘Do I really belong,

am I a member of a church?’… as opposed to identification with a heritage,”

he told a Religion Media Centre event last

week. “The census question, ‘What is your religion?’, implies everyone

should have one… You end up with very different results.” A survey from YouGov on behalf of

Humanists UK, published this month, asked people the same

question as the census, but then asked those who identified as Christian the

reasons for their answer. Almost six in 10 (59%) said it was because they had been christened,

and 49% because they were brought up to think of themselves as Christian.

More than a quarter (26%) said it was “because this is a Christian country”.

Over half (51%) said they never attended a place of worship or did so less

than once a year. Only a third (34%) said they ticked Christian because they “believe

in the teachings of Christianity”. Andrew Copson, chief executive of Humanists UK, said: “Most people in

the UK say they are non-religious, a distinct minority have religious

beliefs, and very few attend places of worship.” Nevertheless, a majority of

people ticked a religion box in the last census because of their background

or upbringing. ‘A distinct minority have religious beliefs,’ says Andrew Copson of

Humanists UK. Photograph: coldsnowstorm/Getty Images/iStockphoto Humanists UK is urging people to tick the “no religion” box if they

don’t believe in or practice a religion. Day said there was a “dark side” to “cultural Christianity”. “The

populist right has pushed the idea that we are a Christian country to

reinforce its anti-immigration stance by fuelling rhetoric about Britain

losing its identity.” The proportion of the population identifying with non-Christian

faiths was likely to increase “quite substantially” in the 2021 census as a

result of immigration and higher birth rates in some minority communities,

said Brierley. The Office of National Statistics estimates it will take a year to

process data from the census. Northern Ireland was also holding a census on Sunday, but Scotland

has postponed its census until 2022 because of the Covid pandemic. (The Guardian) March 20, 2021 682-43-10/Poll 1 In 2 French People Think The Pandemic Has Exacerbated Ethnic

Discrimination

KEY FIGURES AND LESSONS FROM THE STUDY:

Access to housing, the sinews of war Has the crisis exacerbated discrimination based on ethnic

origins? The new Ipsos Global

Advisor study reveals that 65% of French respondents believe

that the criteria of origin really influence the possibilities of access to fundamentals , such as

housing, employment or education. Globally, the share rises to 60% of

those interviewed. On the issue of access to housing, 70% of respondents in France - 10 points more than the overall

average - think that the criteria of race, ethnicity or national origin play a role . Almost a quarter of French people (23%) say they have experienced it

themselves (compared to 35% globally). Note that on this point, France

appearing in the bottom four countries in the ranking, far behind India,

which comes first with 65%. Employment and education also impacted by

discrimination On the employment front ,

69% of French people believe that ethnic criteria can condition their access

(4 points more than the world average) and 24% of French people say they have

already had to suffer this discrimination in their professional

life. Note that more than half of French people (56%) said they had

never felt discriminated against at work because of their ethnic origins. Regarding education ,

63% of French people surveyed believe that race, ethnicity or country of

origin determine access to education, while 22% of French people say they

have had personal experience. Finally, if the health crisis has exacerbated certain social inequalities , making access

to social assistance essential or even vital in France, 6 out of 10 French people (57%)

consider that they have never felt

discrimination linked to their ethnic origins when they have wanted

to use it - a rate well above the

world average (33%). “The study reveals that more than 2/3 of

French people believe a priori that the criteria of origin really influence

the possibilities of access to the fundamentals: housing, employment, education…

It also shows that nearly a quarter of the respondents states that they have

experienced themselves situations in which they consider their origin to have

been an obstacle. What can be reassuring, despite this widely shared

feeling that origin is decisive in people's lives, is that France is one of

the three countries with Japan and Belgium where the gap between perception

and experience of the interviewees is the largest. » Emphasizes Yves Bardon, director of the Ipsos Flair

Program. The Coronavirus has widened the gaps On the face of discrimination ,

the pandemic has not improved things: 46% of

respondents worldwide believe that events in the world during the past year

have increased the are differences in

opportunities and to

access to housing, to education, to employment and / or social services in their

country. Conversely, 43% think

that the events had no impact on the differences and 12% who even believe that they

reduced them. In detail, 52% of

French people (2nd country after Spain at 63%) see in the events of 2020

f actors of aggravation of

discrimination , 40% do not find that they have had an impact

on them and 9% consider that these inequalities have lost ground . (Ipsos France) March 21, 2021 682-43-11/Poll Youtube Is The Most Popular Online Music Service Among Germans

Which online music services are currently

most popular around the world? As people spent more time at home in the past year, influenced by the

corona pandemic, streaming services for information and entertainment

purposes were booming. But not only video but also audio streaming was

the focus, in the latter case especially podcasts and music

streaming. In this context, 35 percent of Germans state that they

currently use the YouTube platform, regardless of whether they have free or

paid access. This is what respondents aged 18 to 44 say most often

(41-42 percent). The streaming portal Spotify only ranks second among

all German respondents with 21 percent, but it is more important for the 18

to 29 year olds: Half (50 percent) of that age group state that they

currently use Spotify. The International Media Consumption

Report 2021 looks, among other things, at the

frequency of media consumption and the services used by people worldwide and

how listening habits have changed. YOUTUBE ALSO LEADS IN THE US, SPOTIFY IN

THE UK A look at the data reveals that YouTube is also a world leader as a

music streaming platform, even if the portal is mainly known as a video

streaming platform. For example, in the United States, more than two in

five Americans (44 percent) say they use YouTube to listen to music, most

commonly between the ages of 18 and 34. Spotify is used by 27 percent of

Americans in the United States. In the UK, on the other

hand, Spotify is the most widely used music streaming platform of all Brits,

and especially those under the age of 55. This can be seen in Britons

aged 18-34, who listen to Spotify more than twice as often as any other music

streaming service, even YouTube. (YouGov Germany) March 19, 2021 Source: https://yougov.de/news/2021/03/19/youtube-ist-unter-deutschen-beliebtester-online-mu/ 682-43-12/Poll 71% Of 14 To 24-Year-Olds State That They Have Good Social Contacts

With Friends

It can be seen, for example, that younger people seem to suffer

particularly from contact restrictions. The proportion of 14 to

24-year-olds who state that they have good social contacts with friends has

decreased by ten percentage points to 71 percent during this period. In

terms of contacts with family members, the difference compared to the survey

from December 2019 is eight percentage points. Likewise, the proportion

of those who can “be there for others” to the desired extent falls in

Generation Z by eight percentage points to 52 percent. Generation Z feels increasing constraints Declining feeling of happiness and

increasing fear of the future A similar picture emerges when it comes to optimism about future

expectations. Despite being less secure in terms of economic factors

such as income or jobs, in the past younger people were far less afraid of

the future than the average population. However, Corona has fueled these

fears, so that the fear of the future in December 2020 among Generation Z is

roughly at the level of the other age groups. According to Hans-Peter Drews, NAWI-D project manager at Ipsos, this

uncertainty is influenced by many factors. “Can school or vocational

training or studies even be finished as planned? Are there any jobs to

finance a degree? Can an apprenticeship / study course be enriched with

valuable internships or stays abroad? Are companies currently even

taking on their trainees or are they hiring new employees? Since

expectations are important for future real developments, politicians should

attach particular importance to this target group in their measures and their

communication. " The young adults are definitely insecure. In December 2020, only

32 percent feel completely free of financial worries, compared to 41 percent

in December 2019. Futurologist Professor Horst Opaschowski

therefore warns of irreparable long-term effects:

(Ipsos Germany) 18 March 2021 682-43-13/Poll Finland's Strongest Car Brands

Each year, YouGov compiles a list of the

strongest car brands using six different imagers. When Finns evaluate car brands on six indicators (quality, general

image, value for money, willingness to recommend, reputation and

satisfaction), Toyota ranks number one.

Toyota is successful in many markets and ranks number one in the

rankings, in addition to Finland, including Australia, the United States,

Canada and Norway. Volvo grabs second place in the Finnish rankings and Mercedes-Benz

third place. In addition to Mercedes-Benz, several German brands will

rise to the TOP10 list. Volkswagen is fourth, Audi fifth and BMW sixth. Japanese brands can also be found on the list in addition to Toyota,

with Honda ranked nineth and Nissan ranked tenth. Who drives a Toyota?

People living in northern or eastern Finland are over-represented in

Toyota's owners in relation to the entire population. The gross

household income of Toyota owners is also higher than average and more of

them are married than average. Their interest in cars is higher than average and one in four of them

(26%) visits car websites at least weekly. About global listing YouGov has used a score index to compile the listing. The score

index consists of the average of 6 different image components: Quality,

General Image, Value for Money, Recommendation, Reputation and Customer

Satisfaction, which together give an overview of the overall condition of the

brand. In Finland, BrandIndex compares more than 350 different brands, 31 of

which are car brands. Every day, YouGov BrandIndex interviews hundreds

of people representing the entire population and asks them about their

attitudes towards different brands. (YouGov Finland) March 16, 2021 Source: https://yougov.fi/news/2021/03/16/automotive-rankings-2021-Finland/ 682-43-14/Poll Above 50% Vaccination Propensity In Hungary

According to the results of the research series, the proportion of

insecure people decreased in all age groups, but while there was a

significant shift towards vaccination among those over 40 years of age, the

relative proportion of those opposing vaccination among adults up to 39 years

of age increased. So despite the steep decline in the average age of

those who died as a result of the virus during the third wave,

anti-vaccination sentiment has intensified among those under 40 in the past

month. FIGURE: Would you vaccinate yourself with

the coronavirus vaccine currently available in Hungary? (on the basis of

the adult population, N = 1,000 people)

In absolute terms, two-thirds of the population who have received at

least one vaccination is over 60, and two-thirds are also women. Half of

those who oppose the vaccine are under the age of 40 (although they make up

38% of the adult population), yet vaccination can be measured at the same

rate among both sexes. FIGURE: Proportion of those registered on

the official website (based on the vaccinated population, N = 505 people)

In the order of vaccinations set up by the population, health workers

are clearly in first place, with one in two compatriots (47%) believing that

in a fair system, others can only receive the vaccine after vaccinating those

who work on the front line among patients. In contrast to the United Kingdom ,

which starts mass vaccination against Covid-19 early and is at the

forefront of vaccination , in Hungary it is not teachers, kindergarten

teachers and other employees of educational institutions who are in the

second place, but those over 60 (14%). FIGURE: In your opinion, which social group

should be vaccinated with the coronavirus vaccine in the first

place? (on the basis of the adult population, N = 1,000 people)

According to the

results of the research series in early March, young adults are susceptible

not only to those working in health care, but also to those working in

education and other public institutions, as well as to older age groups in

terms of vaccination order. - the leader of the now one-year research series, Annamária Földes,

summed up his experiences with the vaccination sequence expected by the

population. Primary vaccination among the 60-69 age group is initiated by the

youngest in the highest proportion (over 19%) and is equally susceptible to

those under 30 working in educational institutions, public institution staff

and social care workers. At the same time, people over the age of 60

would bring grocery store staff to the line much higher than average. FIGURE: In your opinion, which social group

should be vaccinated with the coronavirus vaccine in the first

place? (on the basis of the adult population, N = 1,000 people)

Examining the figures for the 12th month of personal protection

practice against Covid-19, another trend reversal can be observed. The

easing of discipline that characterized last month seems to be slowing down

and reversing as a result of the third coronavirus wave. Although Hungarian society has seemed to be

tired in recent months due to increasingly restrictive measures, the

resurgent numbers of cases have once again made the population already

preparing to open up uncertain. Ipsos has been monitoring the behavior

of the population in an epidemic situation in a way that is unique to the

market for 12 months now. FIGURE: Which of the following activities is

true for you? (on the basis of adult population, N = 1,000 persons /

month)

Wearing a mask Face-to-face protection was not mandatory in Hungary in the first

months of the pandemic. Nevertheless, the data

of April last year showed

a wear rate of 47%, which, after a gradual increase, reached about twice the

level of 90-95% in October. Regardless of the individual demographic

factors, such as age, place of residence, education, all segments of the

population are regularly wearing masks in Hungary. Hand washing Increased hand cleaning and disinfection, similar to the initial

phase of a pandemic, is still a more common defense practice for women, but

four out of five men make this small effort more often than

before. Unlike mask wearing, this phenomenon - thanks to information

campaigns - is immediately integrated into the daily routine and is expected

to remain with us in the long run, even after the epidemic. Personal contact, handshake Similar to the changed hand washing habits, there was an immediate

big change in the proportion of personal contacts when the pandemic broke out

a year ago. Looking back at the last 12 months, it can be stated that

not only in the first period, but also permanently, the older age group,

especially those over 60, closed in and reduced the number of contacts and

meetings related to their environment and family and friends. This

reaction of the population reached another local peak in January, but now it

is half as common to avoid contact as a year earlier. Closely related to the avoidance of meetings was the omission of

handshakes and alternative ways of greeting, even at the very beginning of

the epidemic period. The greatest indiscipline (similar to the frequency

of hand washing) was measured by Ipsos in mid-summer, July. Mainly due

to the middle and older age group, this form of protection currently

characterizes an average of two-thirds of the population. Public transport Avoiding the use of public transport has also proved unsustainable in

the long run. After the uncertainty and horror experienced in the first

months, the masses returned to this form of transport, partly voluntarily and

partly out of compulsion to work. Falling 22 percentage points in one

year, an average of 2 out of 5 residents can now afford to avoid public

transport. Higher rates can be measured among the elderly, as well as

among those with higher education and better earnings. The former is due

to lower mobility needs (pensioners), the latter due to a higher proportion

of car use (active workers but those traveling by car). Travel, events The number of domestic trips as well as event visits fell

again at the beginning of the year (also as a result of government measures

and central communications) following a temporary respite

in August-September . From January to

February , discipline eased significantly ,

a trend that seems to slow down and reverse with the onset of the third wave

of illness. The situation of foreign tourism has not improved

significantly for 12 months, based on which it can be stated that the market

is permanently, permanently reorganized following the pandemic. (Ipsos Hungary) March 16, 2021 Source: https://www.ipsos.com/hu-hu/50-felett-az-oltasi-hajlandosag-magyarorszagon NORTH

AMERICA

682-43-15/Poll 69 Americans Say It Is Very Important For Federal Law Enforcement

Agencies To Find And Prosecute The People Who Broke Into The U.S. Capitol On

Jan 6

As the FBI and other federal law enforcement agencies continue to pursue charges against

participants in the Jan. 6 riot at the U.S. Capitol, the American public

generally expresses strong support for continuing these efforts. Yet there

are sizable partisan differences in attitudes about the riot at the Capitol,

with Democrats far more likely than Republicans to view prosecution of the

rioters as very important and to say that penalties for the rioters are

likely to be less severe than they should be. The survey by Pew Research Center, conducted March 1-7, 2021, among

12,055 U.S. adults who are members of the Center’s nationally

representative American Trends Panel,

finds a wide majority of Americans (69%) saying it is “very important” for

federal law enforcement agencies to find and prosecute the people who broke

into the U.S. Capitol on Jan. 6. Another 18% say doing this is “somewhat

important.” Just 12% say this is not too or not at all important. Nearly half of Americans (47%) say the criminal penalties that the

rioters will receive are likely to be less severe than they should be given

what happened, while 22% say the penalties will be more severe than they

should be. Only about three-in-ten (29%) expect the punishments will be about

right. The public generally expresses confidence in federal law enforcement

agencies to find and prosecute those who broke into the Capitol on Jan. 6.

Still, of those who say it is important for these agencies to complete this

task, only 20% have a “great deal” of confidence that law enforcement will

bring the rioters to justice, while another 48% have a “fair amount” of

confidence. Republicans and Democrats differ sharply over how important it is for

law enforcement to prosecute those involved in the Jan. 6 riots and whether

criminal penalties will be less severe than deserved. Partisans are less

divided over whether federal law enforcement agencies are up to the task of

finding and prosecuting participants who scattered across the country after

the events that day.

While large majorities in both parties (95% of Democrats and 79% of

Republicans, including those who lean to each party) say it is at least

somewhat important that federal law enforcement agencies find and prosecute

those responsible for the Jan. 6 riot, Democrats are more intense in their

views: Fully 86% of Democrats and independents who lean toward the Democratic

Party say finding and prosecuting rioters is very important, compared with half of Republicans and

Republican leaners. Similarly, nearly two-thirds of Democrats (65%) say it is likely that

the criminal penalties the rioters receive will be less severe than they

should be. Republicans are divided: 37% say they are likely to be more severe

than they should be, while 26% expect them to be less severe. Additionally, Democrats express slightly higher confidence in federal

law enforcement to find and prosecute those responsible for what happened at

the U.S. Capitol in January. Among Democrats who said it was at least

somewhat important to find and prosecute those responsible for the Capitol

riots, about seven-in-ten Democrats (71%) say they have a great deal (23%) or

fair amount (48%) of confidence in federal law enforcement to do so, compared

with 66% of Republicans (18% a great deal and 49% a fair amount).

While a plurality of Americans (44%) say the Jan. 6 riot at the U.S.

Capitol and its impacts have been getting about the right amount of attention

overall, there also are significant differences in these views among

Republicans and Democrats. Many Republicans say the Jan. 6 riots and their aftermath have been

getting too much attention

(54% say this), which is not a widely shared view among Democrats (8% say too

much). By contrast, 40% of Democrats say the riot has been getting too little attention; just 11% of

Republicans say the same. About half of Democrats (52%) and a third of

Republicans say the riots have gotten about the right amount of attention.

The survey finds that the public expresses more concern about

right-wing and left-wing extremism stirring possible violence in the country

than either Islamic or Christian extremism. About half of U.S. adults say

right-wing extremism (52%) and left-wing extremism (51%) are major problems

in the country. Fewer than four-in-ten say violent extremism in the name of

Islam (37%) or in the name of Christianity (34%) is a major problem. Republicans and Democrats are widely divided over which political

wing represents the greater threat. About three-quarters of Democrats and

Democratic-leaning independents (73%) say right-wing extremism is a major

problem, while a similar share of Republicans and Republican leaners (76%)

say the same about left-wing extremism. Only about three-in-ten Democrats

(31%) say left-wing extremism is a major problem, and 29% of Republicans say

this about right-wing extremism. In addition, Republicans (49%) are more likely than Democrats (28%)

to say extremism in the name of Islam is a major problem. The reverse is the

case for extremism in the name of Christianity: 48% of Democrats say it is a

major problem, versus 16% of Republicans. Reactions to aftermath of the Jan. 6

Capitol riot Amid continued investigations and congressional hearings into the

riots that occurred at the U.S. Capitol on Jan. 6, nearly three-in-ten adults

(27%) say there has been too little attention paid to the riots and their

impacts. A similar share (28%) says there has been too much attention paid to

the events at the Capitol, while a 44% plurality says the riots have received

about the right amount of attention.

There are differences in these views by race, partisanship and

ideology. Among White adults, 44% say about the right amount of attention has

been given to the aftermath of the Capitol riots. Roughly a third (34%) say

too much focus has been given to the riots, while a smaller share (21%) says

too little attention has been paid. In contrast, Black adults are significantly more likely to say there

has been too little attention paid to the riots and its aftermath: 49% of

Black adults say there’s been too little, while just 8% say there has

been too much focus

on the riot. This racial divide in attitudes is also evident among Democrats and

Democratic-leaning adults. While a majority of White Democrats say there has

been the right amount of attention paid to the aftermath of the riots (58%),

a smaller share of Black Democrats says the same (43%). In fact, more Black

Democrats say there has been too little attention

given to the riots (50% of Black Democrats vs. 37% of White Democrats). A majority of Republicans and Republican leaners say there has

been too much attention

paid to the riot and its impacts (54%). Republicans, unlike Democrats, are divided

along ideological lines: 61% of conservative Republicans say the riot and its

aftermath have received too much attention, compared with 43% of moderate and

liberal Republicans. Pluralities of Democrats across the ideological spectrum say there

has been about the right amount of focus on the Capitol riots and its

impacts.

While there is broad consensus across demographic groups that it is

at least somewhat important for federal law enforcement to find and prosecute

those who broke into the U.S. Capitol on Jan. 6, there is some variation in

the degree to which these groups say it is a priority. And while majorities

say they have confidence in federal law enforcement agencies to locate and

prosecute those involved, relatively small shares express a great deal of confidence that

they can do this. Overall, about eight-in-ten or more adults across demographic groups

say it is at least somewhat important

for federal law enforcement agencies to seek out those responsible for the

Capitol breach (87% overall). There are racial, ethnic and partisan differences in these views.

Black adults are particularly likely to say it is very important for federal law

enforcement to penalize those involved (87%); smaller shares of White (66%),