BUSINESS

& POLITICS IN THE WORLD

GLOBAL

OPINION REPORT NO. 666

Week: November 23 – November

29, 2020

Presentation: December 04, 2020

Nearly

two-thirds of urban Indians favour the government’s decision to regulate

digital content

Singaporeans divided on decision to re-open

nightclubs

Nearly two-thirds of urban Indians favour the

government’s decision to regulate digital content

Improving immunity was a key reason to

participate in the Dubai Fitness Challenge this year

Most Basotho say government bungled teacher

strike, is failing on education and youth

23 percent of German corporate decision-makers

feel unprepared for Brexit

Faced with the controversy, what popularity for

the CNews channel?

Fruits preferred by Italians and sustainability

of production

Two thirds of Britons support cutting the

foreign aid budget

Two in five Britons plan to shop during Black

Friday and Cyber Monday

Hopes of vaccine boost public’s opinion of the

pharmaceutical industry

Eight in ten say it is currently difficult to

find a job in Britain

Leisure-wear, pyjamas and even showering less,

has COVID accelerated a decline in formality?

Americans' Holiday Spending Intentions

Strengthen in November

Biden's Favorability Rises to 55%, Trump's Dips

to 42%

Prior to COVID-19, child poverty rates had

reached record lows in U.S.

In the pandemic, the share of unpartnered moms

at work fell more sharply than among other parents

Movement

in Melbourne CBD at only 27% of normal after lockdown ends, well behind Sydney

CBD (42%)

COVID-19 Magnifies Pre-Existing Gender

Inequalities in MENA

NATO seen in a positive light by many across 10

member states

INTRODUCTORY NOTE

This weekly report consists of twenty two surveys.

The report includes four multi-country studies national surveys from different

states across the globe.

666-43-20/Commentary:

Nearly two-thirds of urban

Indians favour the government’s decision to regulate digital content

Millennials are

most likely to support as well as say their consumption of digital content is

likely to increase due to this move

YouGov’s latest survey

reveals nearly two-thirds (64%) of urban Indians support (either strongly or

somewhat) the government’s decision of bringing digital content including

films, web series as well as online news under the ambit of the Ministry of

Information and Broadcasting.

Only a small number (13%)

said they oppose this move, while 22% are unsure of their decision.

The findings are similar to

the ones revealed by YouGov’s survey last year where a majority had given their

consent for the censorship of digital content.

Is it interesting to note

that millennials emerged as the greatest advocates of digital censorship; with

one in seven (69%) saying they support the government’s decision to regulate

online content.

The majority of urban

Indians favour this decision because they feel online content includes a lot of

inappropriate content for children (56%). Many find depictions of violence and

bloodshed (48%) and nudity & strong language (44%) in certain kinds of

content concerning.

Thinking about the impact of

this decision on OTT/ Video-streaming platforms, two in five respondents (40%)

feel regulation of digital content will make it more suitable for children as

well as members of other age groups. A third (33%) are positive about the

content quality improving, and almost as many (31%) feel the viewership of

digital channels will increase due to this.

Many expect gloomy outcomes

such as restriction of access to the global/niche content (31%), increase in

the piracy of movies or series (23%), decrease in the viewership, and

deterioration of the quality of content (20% each).

People’s positive

expectations from digital media regulation extend to online news platforms as

well. One-third of urban Indians said regulation of digital news would lead to

better clarity of facts around current events and happening (33%). Another third

thinks the spread of fake news could now be controlled (33%), and just as many

feel that the quality of news on digital platforms will improve (32%).

Some believe once digital

news comes under the purview of the government, it may lose its essence as the

freedom of speech will get restricted (27%), while others are of the opinion

that it might affect the quality of news (21%).

When asked about the impact

on their personal consumption of digital media, a third (33%) said their

consumption of content on OTT platforms is likely to increase because of the

filtration of content. One in five (20%) feel it will decrease and for a

quarter (24%) it is likely to remain unchanged.

Similarly, two in five (39%)

respondents said their personal consumption of digital news is likely to surge

due to the regulation. One in three (31%) feel it will remain unchanged, and

only a small number (16%) hinted towards a decline in their online news

consumption.

Amongst all the age groups,

millennials were most likely to say their personal consumption of both digital

content and digital news will increase once content goes through regulation- at

40% and 45%, respectively.

(YouGov)

November 25, 2020

Source: https://in.yougov.com/en-hi/news/2020/11/25/nearly-two-thirds-urban-indians-favour-governments/

666-43-21/Country Profile: India

SUMMARY

OF POLLS

ASIA

(Singapore)

Singaporeans divided on decision to re-open nightclubs

Recently, a limited number of bars, pubs, nightclubs, discotheques and karaoke lounges re-opened with COVID-19 safety measures in place under a pilot programme. Latest YouGov data looks at what Singaporeans think of nightclubs re-opening and of nightlife as a whole. After eight months of remaining shut, the Ministry of Trade and Industry (MTI) and the Ministry of Home Affairs (MHA) announced that certain nightlife venues would be able to re-open. While three in ten (29%) of Singaporeans agree with this decision, the other three in ten (29%) disagree. The remaining two in ten (18%) are undecided. (YouGov)

December 01, 2020

(India)

Nearly two-thirds of urban Indians favour the

government’s decision to regulate digital content

YouGov’s latest survey reveals nearly

two-thirds (64%) of urban Indians support (either strongly or somewhat) the

government’s decision of bringing digital content including films, web series

as well as online news under the ambit of the Ministry of Information and

Broadcasting. Only a small number (13%) said they oppose this move, while 22%

are unsure of their decision. (YouGov)

November 25, 2020

MENA

(UAE)

Improving immunity was a key reason to participate in the Dubai Fitness

Challenge this year

The fourth edition of the Dubai Fitness

Challenge (DFC) commenced on October 30 with the introduction of global safety

practices and a mix of physical and virtual workouts. YouGov’s latest survey

reveals the pandemic has given people many more reasons to participate and a

large proportion of UAE residents (45%) took up the challenge this year in

order to improve their immunity. (YouGov)

November 25, 2020

AFRICA

(South Africa)

Most Basotho say government bungled teacher strike, is failing on

education and youth

Most Basotho say the government is doing

a poor job on education and youth, including mishandling its protracted dispute

with public school teachers, the latest Afrobarometer

survey shows. Citizens overwhelmingly support the teachers, who were on

intermittent strike for much of 2019 and continue to demand better salaries and

working conditions. (Afrobarometer)

December 03, 2020

EUROPE

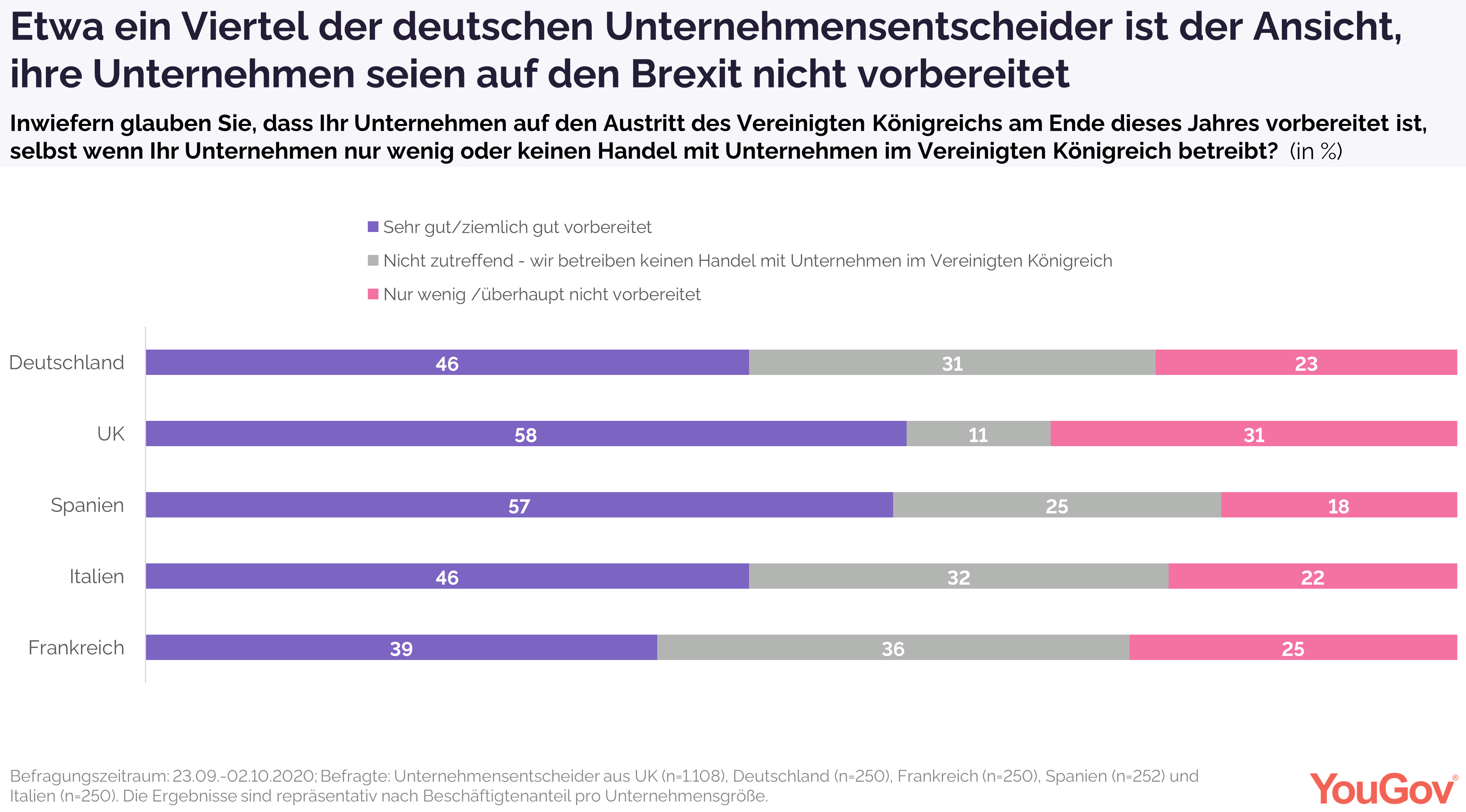

(Germany)

23 percent of German corporate decision-makers feel unprepared for

Brexit

The Brexit transition phase will end on

December 31, 2020. From 2021, the United Kingdom will no longer be part of the

EU internal market and the customs union as a “third country”. 22 percent of

European corporate decision-makers state that their company is little or not at

all prepared for the changes associated with Brexit. The UK has the highest

number (31 percent). In Germany, 23 percent of corporate decision-makers state

that they are little or not at all prepared for the final Brexit

implementation. (YouGov)

December 01, 2020

(France)

Faced with the controversy, what popularity for the CNews

channel?

CNews has come under heavy criticism in recent

months. However, audience figures suggest that the format of the news channel

is increasingly popular with the public. In September 2020, Vincent Bolloré's media thus reached an audience share of 1.5%

according to Médiamétrie, practically doubling its

score compared to the previous year. (YouGov)

November 30, 2020

(Italy)

Fruits preferred by Italians and sustainability of production

We asked the Italians what their favorite

fruits were this season and what they thought about the issue of sustainability

in agricultural production. Mandarin, grapes, apple, chestnut and orange are

the favorite fruits of the Italians in this period. Persimmon, in seventh

position by preference, shows a high share of "loyal": among those

who ate it in the last month, almost one in three people selected it as their

favorite fruit in this period. (YouGov)

November 27, 2020

(UK)

Two thirds of Britons support cutting the foreign aid budget

In 2015, then-Prime Minister David

Cameron enshrined in law the UK’s commitment to spending 0.7% of GDP on foreign

aid. The figure had been adopted as a target in principle as early as 1974,

although it wasn’t until 2013 that it was met for the first time. In light of the damage caused to the public finances by the

coronavirus crisis, Chancellor Rishi Sunak announced today that foreign aid

spending will be reduced to 0.5% of GDP – a reduction of £5bn. (YouGov)

November 25, 2020

(UK)

Two in five Britons plan to shop during Black Friday and Cyber Monday

There is unlikely to be any footage of

eager shoppers fighting over discounted TVs on Black Friday this year. But the

national lockdown isn’t putting people off. Two in five people (40%) plan to

bag a discount during the sales period – which is in line with last year when

39% of Britons participated. The four in ten Black Friday shoppers are mostly

composed of people who say they will only shop online (32%). Just 1% expect to

exclusively shop in-store and one in fourteen (7%) say they will do both.

(YouGov)

November 25, 2020

(UK)

Hopes of vaccine boost public’s opinion of the pharmaceutical industry

Britons are feeling increasingly positive

about pharmaceutical and biotech companies, with 47% of the public now saying

they have a favourable view of the industry, YouGov

tracker data shows. The latest figures were recorded on 12 Nov – three days

after Pfizer and BioTech announced that their

COVID-19 vaccine was 90% effective. The news appears to have prompted a

six-point jump in positive opinion, up from 41% in mid-October. (YouGov)

November 26, 2020

(UK)

Eight in ten say it is currently difficult to find a job in Britain

YouGov’s tracking data shows a massive

80% of the public think it is currently difficult for those in the market to

find a job in Britain, including 42% who think it is “very difficult”. Just 9%

say it is currently easy for those looking to find a job. Unsurprisingly this

is a massive shift from before the first UK lockdown. In February, 44% thought

finding a job was difficult while 39% thought it was easy. (YouGov)

November 26, 2020

(UK)

Leisure-wear, pyjamas and even showering less, has COVID accelerated a

decline in formality?

In new research by Ipsos MORI, two-thirds (67%) of Britons say they are

dressing more casually since the COVID-19 pandemic started. Two-thirds say this

means they can exercise their personal choices more while 63% say they are

happy that they can dress more casually. Six in ten (59%) feel confident

about knowing how to dress in a more casual way, the same proportion say

working from home makes it easier to do so. Just over half of Britons say you

rarely see people at work in business suits these days (54%). (Ipsos MORI)

November 27, 2020

NORTH AMERICA

Americans' Holiday Spending Intentions Strengthen

in November

Gallup's latest update of Americans' 2020 holiday spending plans

finds consumers estimating they will spend an average $852 on Christmas gifts,

nearly identical to the $846 they projected at the same time last year. Annual trend since 1999 in which Americans estimate each November

of the amount they will spend on Christmas gifts,

ranging from a high of $866 in 2007 to a low of $616 in 2008. The November 2020

figure is $852. (Gallup USA)

November 25, 2020

Biden's Favorability Rises to 55%, Trump's Dips to

42%

President-elect Joe Biden's favorability rating has risen six

percentage points to 55% since the election compared with his final preelection reading. At the same time, President Donald

Trump's favorability has edged down three points to 42%. Biden's current rating

is the highest it has been since February 2019, two months before he declared

his candidacy for president, when it was 56%. Trump's latest favorability falls

short of the highest of his presidency, 49% in April, during the initial stages

of the coronavirus pandemic. (Gallup USA)

November 30, 2020

Prior to COVID-19, child poverty rates had reached

record lows in U.S.

In 2019, the year with the most recently available data, 14% of

children under age 18, or 10.5 million children, were living in poverty, down

from 22%, or 16.3 million, in 2010. All major racial and ethnic groups saw

declines since 2010, but the greatest decreases were in the shares of Black and

Hispanic children living in poverty. About two-in-ten Hispanic children (21%)

were living in poverty in 2019, down from 35% in 2010. In 2019, 26% of Black

children were impoverished, dropping from 39% in 2010. Even so, Black and

Hispanic children were still about three times as likely as Asian (7%) and

White (8%) children to be living in poverty. (PEW)

November 29, 2020

In the pandemic, the share of unpartnered moms at

work fell more sharply than among other parents

Balancing work and family obligations is a challenge for many

parents, but remote learning and the closure of many child

care centers have put added stress on them in the COVID-19 pandemic,

especially on parents without the support of a partner at home. While previous research on the labor market shows that the pandemic

has similarly affected mothers and fathers overall from September 2019 to

September 2020, a new Pew Research Center analysis finds that the share of

unpartnered mothers who are employed and at work has fallen more precipitously

than among other parents. (PEW)

November 24, 2020

AUSTRALIA

Movement in Melbourne CBD at only 27% of normal

after lockdown ends, well behind Sydney CBD (42%)

Movement in the Melbourne CBD during mid-November was at an average

of only 27% of the pre-COVID-19 levels earlier in the year during January and

February – although this has almost doubled since being at only 14% during the

final week of lockdown in late October. Comparing movement levels during 2020

shows that movement levels in the Melbourne CBD have been lower than all other Capital

City CBDs every week since late March when the first national lockdown began

and hit a low of only 11% of normal in the final week of August. (Roy Morgan)

November 27, 2020

MULTICOUNTRY STUDIES

COVID-19 Magnifies Pre-Existing Gender

Inequalities in MENA

COVID 19 is being perceived as a disruptor, an accelerator and an

agent for innovation and advancement in various fields across the world. Yet,

its impact has been a decelerator for women’s rights and gender equality

globally. The UN Deputy Secretary-General

Amina Mohammed warned that without immediate action, “the pandemic could set

back women’s rights by decades”. And, the latest Arab Barometer public opinion

survey of citizens across five countries in the Arab world confirm that Arab

women have suffered more on economic and social dimensions. (Arab Barometer)

December 01, 2020

NATO seen in a positive light by many across 10

member states

The North Atlantic Treaty Organization (NATO) is seen more

favorably than not across 10 member states and Sweden. A median of 60% across

these 10 countries have a favorable view of the political and military

alliance, compared with a median of 30% who have an unfavorable opinion. This

is in keeping with previous Pew Research Center surveys, which found that NATO

was seen in a favorable light across most member countries. (PEW)

November 30, 2020

ASIA

666-43-01/Poll

Singaporeans divided on decision to re-open nightclubs

Four in five believe that keeping citizens safe during

pandemic more important that nightlife activities

Recently, a limited number of bars, pubs, nightclubs, discotheques and

karaoke lounges re-opened with COVID-19 safety measures in place under a pilot

programme. Latest YouGov data looks at what Singaporeans think of nightclubs

re-opening and of nightlife as a whole.

After eight months of remaining shut, the Ministry of Trade and Industry

(MTI) and the Ministry of Home Affairs (MHA) announced that

certain nightlife venues would be able to re-open. While three in ten (29%) of

Singaporeans agree with this decision, the other three in ten (29%) disagree.

The remaining two in ten (18%) are undecided. Younger Singaporeans (aged 18 to

34) are the most likely to agree with the decision to re-open, while older

Singaporeans (aged 55 and above) are the least likely (35% vs. 20%).

While Singaporeans might be split on whether nightlife venues should

re-open, data shows that most have never visited a nightclub before – with

seven in ten (72%) saying they’ve never set foot in a nightclub. Women are more

likely to have never visited a nightclub than men (80% vs. 65%) are. Out of the

remaining 28% who have visited a nightclub, only a small percentage are

frequent club-goers. Prior to the pandemic, one in twenty (5%) went clubbing at

least once a month, one in twenty (6%) at least once every six months and one

in six (16%) less than once every six months.

As a whole, two-thirds (67%) of Singaporeans are unbothered about

nightlife venues remaining shut. One in six (17%) actively dislike spending

time at these venues, and find that nightlife activities remaining shut have

benefited them. The remaining one in six (16%) miss going out at night and

enjoy spending time at these venues.

Amongst club-goers, the main reason to go clubbing is to spend time with

friends (64%). To enjoy the music and for a celebration and party (37%) come in

joint second, followed by to drink alcohol (36%), to dance (19%) and to chat up

people (14%). A small percentage (7%) say they go clubbing because there are no

other places to go at night.

The re-opening of these venues sees some very stringent measures in

place. For example, all customers must wear masks at all times even when on the

dancefloor or while singing. No alcohol can be sold, served or consumed after

10:30pm and all customers must be tested negative for COVID-19 24 hours prior

to entering the establishment. With these measures in mind, three in five (63%)

of Singaporeans are uninterested in returning to nightlife venues. A quarter

(25%) have no opinion, and slightly over one in ten (13%) are keen. However,

amongst younger Singaporeans (aged 18 to 34), this number doubles, with one in

five (19%) interested in returning to nightlife venues, even with stringent

measures in place.

Singaporeans are not only divided on whether nightlife venues should

re-open, they also appear divided on their attitudes towards nightlife venues

as a whole. Half (48%) agree that going to bars, clubs and karaoke lounges help

people relieve stress, and almost half (45%) agree that the nightlife industry

is an important part of Singapore's economy. However, a similar number (44%)

also believe that nightlife establishments do more harm than good. The majority

(79%) agrees that keeping citizens safe in a pandemic is more important than

allowing for nightlife activities.

(YouGov)

December 01, 2020

Source:

https://sg.yougov.com/en-sg/news/2020/12/01/singaporeans-divided-decision-re-open-nightclubs/

666-43-02/Poll

Nearly two-thirds of urban Indians favour the government’s

decision to regulate digital content

Millennials are most likely to support as well as say their

consumption of digital content is likely to increase due to this move

YouGov’s latest survey reveals nearly two-thirds (64%) of urban Indians

support (either strongly or somewhat) the government’s decision of bringing

digital content including films, web series as well as online news under the

ambit of the Ministry of Information and Broadcasting.

Only a small number (13%) said they oppose this move, while 22% are

unsure of their decision.

The findings are similar to the ones revealed by YouGov’s survey last

year where a majority had given their consent for the censorship of digital

content.

Is it interesting to note that millennials emerged as the greatest

advocates of digital censorship; with one in seven (69%) saying they support

the government’s decision to regulate online content.

The majority of urban Indians favour this decision because they feel

online content includes a lot of inappropriate content for children (56%). Many

find depictions of violence and bloodshed (48%) and nudity & strong

language (44%) in certain kinds of content concerning.

Thinking about the impact of this decision on OTT/ Video-streaming

platforms, two in five respondents (40%) feel regulation of digital content

will make it more suitable for children as well as members of other age groups.

A third (33%) are positive about the content quality improving, and almost as

many (31%) feel the viewership of digital channels will increase due to this.

Many expect gloomy outcomes such as restriction of access to the

global/niche content (31%), increase in the piracy of movies or series (23%),

decrease in the viewership, and deterioration of the quality of content (20%

each).

People’s positive expectations from digital media regulation extend to

online news platforms as well. One-third of urban Indians said regulation of

digital news would lead to better clarity of facts around current events and

happening (33%). Another third thinks the spread of fake news could now be

controlled (33%), and just as many feel that the quality of news on digital

platforms will improve (32%).

Some believe once digital news comes under the purview of the government,

it may lose its essence as the freedom of speech will get restricted (27%),

while others are of the opinion that it might affect the quality of news (21%).

When asked about the impact on their personal consumption of digital

media, a third (33%) said their consumption of content on OTT platforms is

likely to increase because of the filtration of content. One in five (20%) feel

it will decrease and for a quarter (24%) it is likely to remain unchanged.

Similarly, two in five (39%) respondents said their personal consumption

of digital news is likely to surge due to the regulation. One in three (31%)

feel it will remain unchanged, and only a small number (16%) hinted towards a

decline in their online news consumption.

Amongst all the age groups, millennials were most likely to say their

personal consumption of both digital content and digital news will increase

once content goes through regulation- at 40% and 45%, respectively.

(YouGov)

November 25, 2020

Source:

https://in.yougov.com/en-hi/news/2020/11/25/nearly-two-thirds-urban-indians-favour-governments/

MENA

666-43-03/Poll

Improving immunity was a key reason to participate in the

Dubai Fitness Challenge this year

Among residents who did not participate, fear of catching the

Covid infection was the top reason

The fourth edition of the Dubai Fitness Challenge (DFC) commenced on

October 30 with the introduction of global safety practices and a mix of

physical and virtual workouts.

YouGov’s latest survey reveals the pandemic has given people many more

reasons to participate and a large proportion of UAE residents (45%) took up

the challenge this year in order to improve their immunity.

In addition to this, nearly one in three (28%) participated to try the

newly the introduced stay-home workout sessions, and just as many enrolled

themselves to take a break from staying at home due to Covid (27%).

Even though many residents participated due to reasons related to Covid,

the majority took part in the challenge to keep themselves motivated to stay

fit (64%). Motivation for good health was the key reason for participation last

year as well (with 54% saying this).

A third (32%) participate every year and joined this time to keep the

tradition alive. Other reasons for participation included getting out of

comfort zone (40%), to have fun (38%) and for the free health check-ups and

classes (34%).

The pandemic has pushed many people to focus on fitness and transform

their lifestyles. Despite the fear of the virus, two-thirds (67%) of those

aware of the Dubai Fitness Challenge participated this year, compared to 75%

last year. A third (33%) did not participate this time, up from 25% last year.

Among those who did not participate, fear of catching the infection was

the main reason (as said by 34%). Another 17% did not take part out of concern

for social distancing practiced at the venues.

As a tradition, the Dubai Fitness Challenge encourages people to complete

30 minutes of activity a day for 30 days. Of the residents who participated

this year, seven in ten (72%) claimed to log at least 30 minutes of activity a

day. One in twelve (8%) pushed themselves further and clocked in more than 60

minutes.

Furthermore, all enthusiasts had specific fitness goals that they wanted

to achieve through this initiative. Improving overall fitness (61%) was the top

ambition, followed by weight loss and increasing stamina (51% each).

The data shows residents seem happy with the results of the challenge and

it had a positive impact on their health and wellness. For all the listed

goals, a large majority think the fitness challenge helped them achieve their

goals to a great extent.

Enthusiasm for fitness is likely to continue as nearly nine in ten (88%)

participants intend to take part in the challenge next year as well.

(YouGov)

November 25, 2020

Source:

https://mena.yougov.com/en/news/2020/11/26/improving-immunity-was-key-reason-participate-duba/

AFRICA

666-43-04/Poll

Most Basotho say government bungled teacher strike, is

failing on education and youth

Most Basotho say the government is doing a poor job on education and

youth, including mishandling its protracted dispute with public school

teachers, the latest Afrobarometer survey shows.

Citizens overwhelmingly support the teachers, who were on intermittent

strike for much of 2019 and continue to demand better salaries and working

conditions.

The survey also shows that a majority of Basotho expect more effective

government action to address the needs of youth and would willingly pay more

taxes if that would mean funding for initiatives to help young people,

especially through job creation.

These findings suggest that Basotho want a less intransigent government

response that will end the long-running dispute with teachers and address

critical education and youth development needs of the population.

(Afrobarometer)

December 03, 2020

EUROPE

666-43-05/Poll

23 percent of German

corporate decision-makers feel unprepared for Brexit

A YouGov poll of

European business decision-makers in the UK, Germany, France, Italy and Spain

on Brexit

The majority of British business decision-makers (58

percent) say that their companies are sufficiently prepared for Brexit. In

Spain it is 57 percent, and 46 percent each in Germany and Italy. In

France, 39 percent of corporate decision-makers say this.

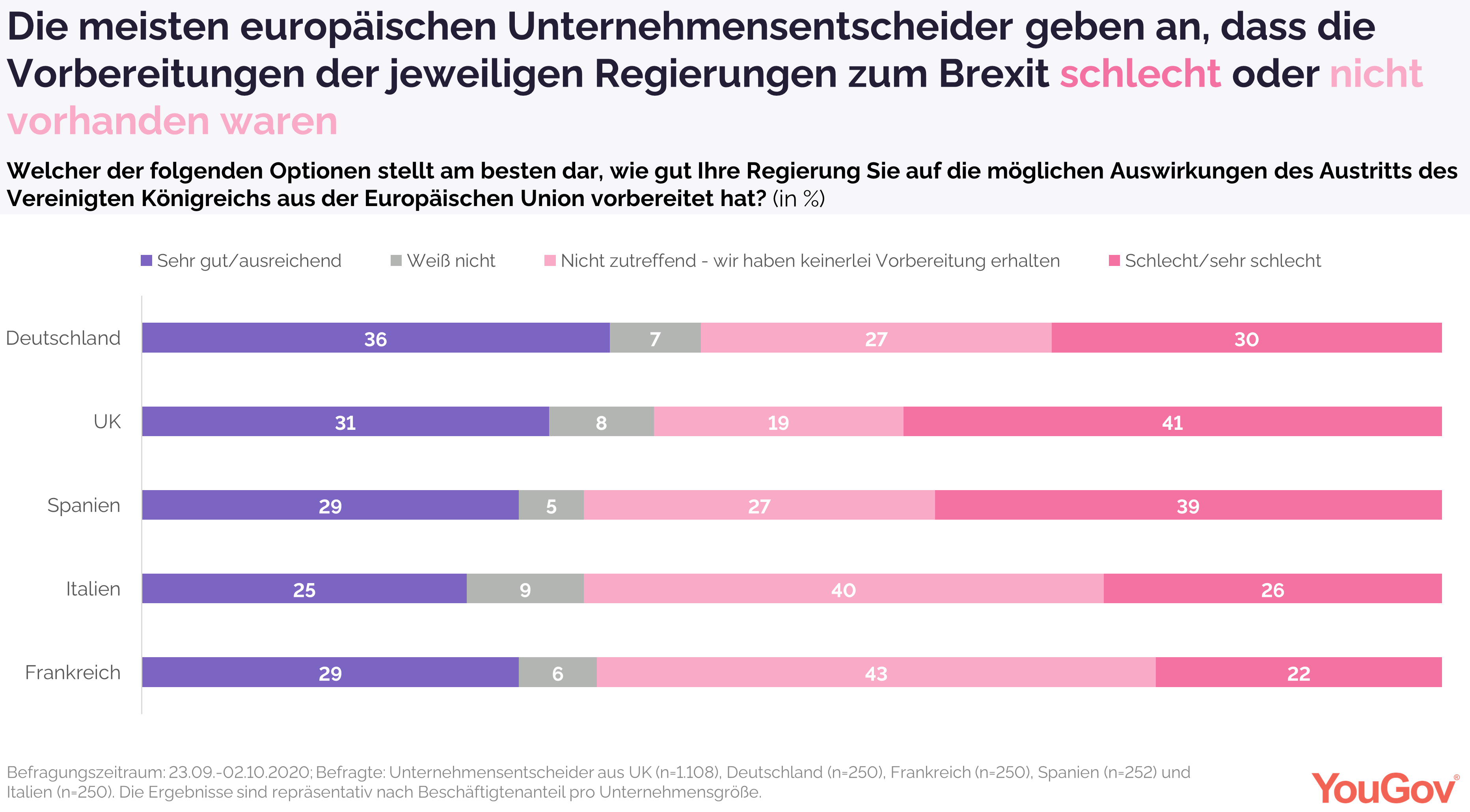

MORE CRITICISM

THAN PRAISE FOR BREXIT PREPARATIONS BY THE RESPECTIVE GOVERNMENTS

German decision-makers say the most (36 percent) that

their government prepared companies well or adequately for the possible effects

of the United Kingdom's exit from the European Union. Among the British, a

third (32 percent) say this, among the French and Spaniards 29 percent of

company decision-makers each make this statement, in Italy a quarter (25

percent).

UK respondents are most likely to say (41 percent)

that their companies have been poorly prepared by their government for the

potential impact of the exit. Just as many Spaniards make this

statement. In Germany, that's 30 percent. Among French corporate

decision-makers, as many as 43 percent say that they have not received any

preparations. Only 19 percent say this in Great Britain.

December 01, 2020

Source: https://yougov.de/news/2020/12/03/23-prozent-der-deutschen-unternehmensentscheider-f/

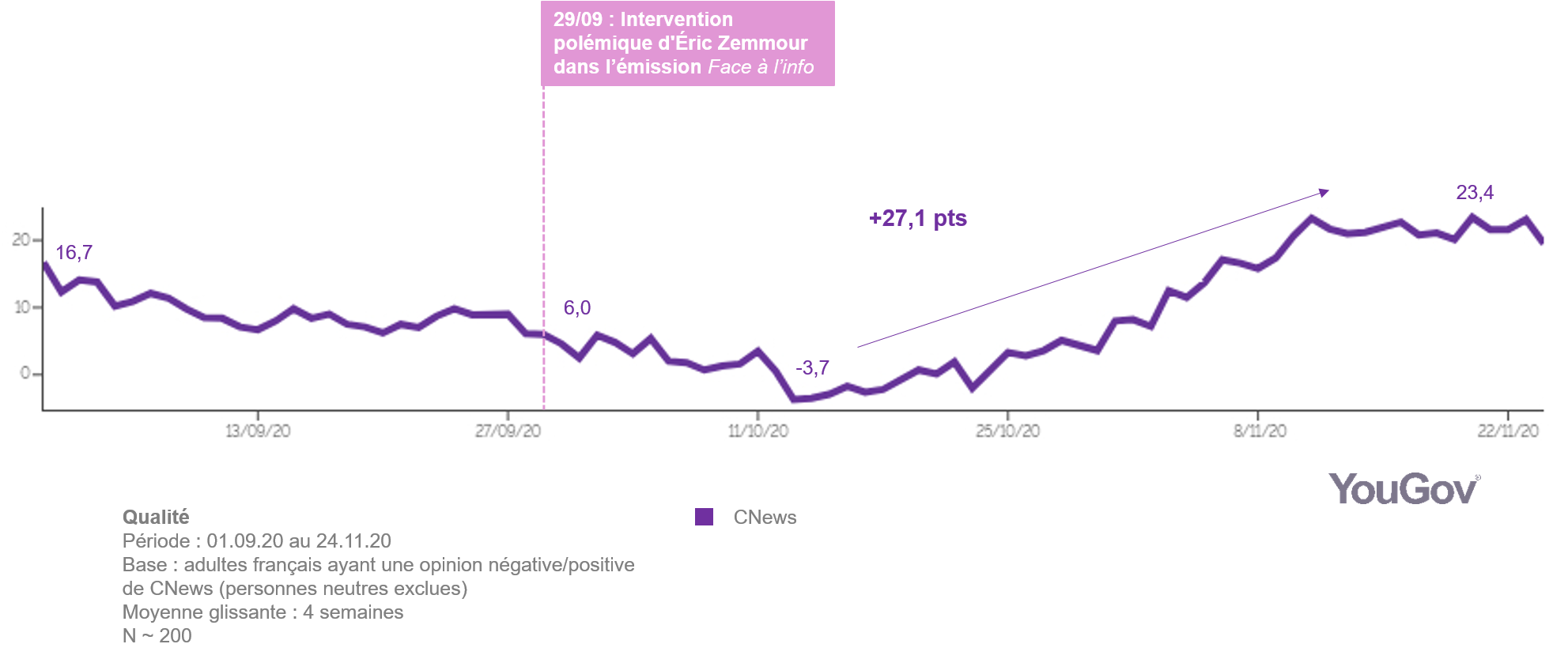

666-43-06/Poll

Faced with the controversy,

what popularity for the CNews channel?

Some shows perform particularly well, like "Face à l'Info",

which saw its audience explode. In October 2020, the program attracted an

average of 587,000 viewers, against 149,000 a year earlier.

Can we highlight certain correlations between recent

controversies and the evolution of brand indicators? Response with YouGov

BrandIndex.

A channel that

makes people talk about it

On September 29, Eric Zemmour's intervention in the

show Face à l'Info created

controversy on social networks. There is an increase in Word of Mouth from

the end of September. The indicator thus rose by 3.5 points in a few

weeks.

An increase in

perceived Quality

While CNews' Quality score had been falling since

early September, it started to rise again from October 13 and peaked at 23.4 in

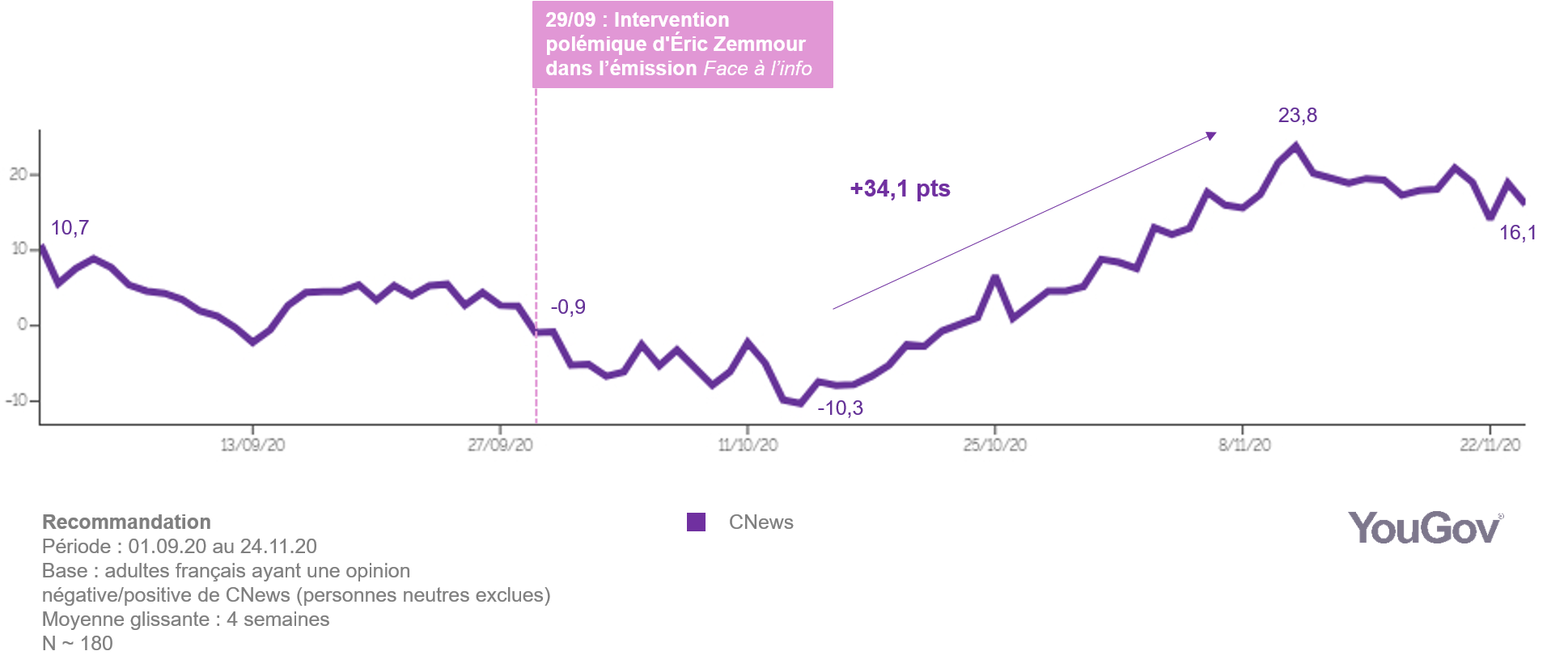

mid-November, a rapid increase of 27.1 points.

Recommended

media

Likewise, the Recommendation indicator fell and turned

negative on September 29, before starting to rise sharply a few days

later. The score thus increased by 34.1 points between mid-October and

mid-November.

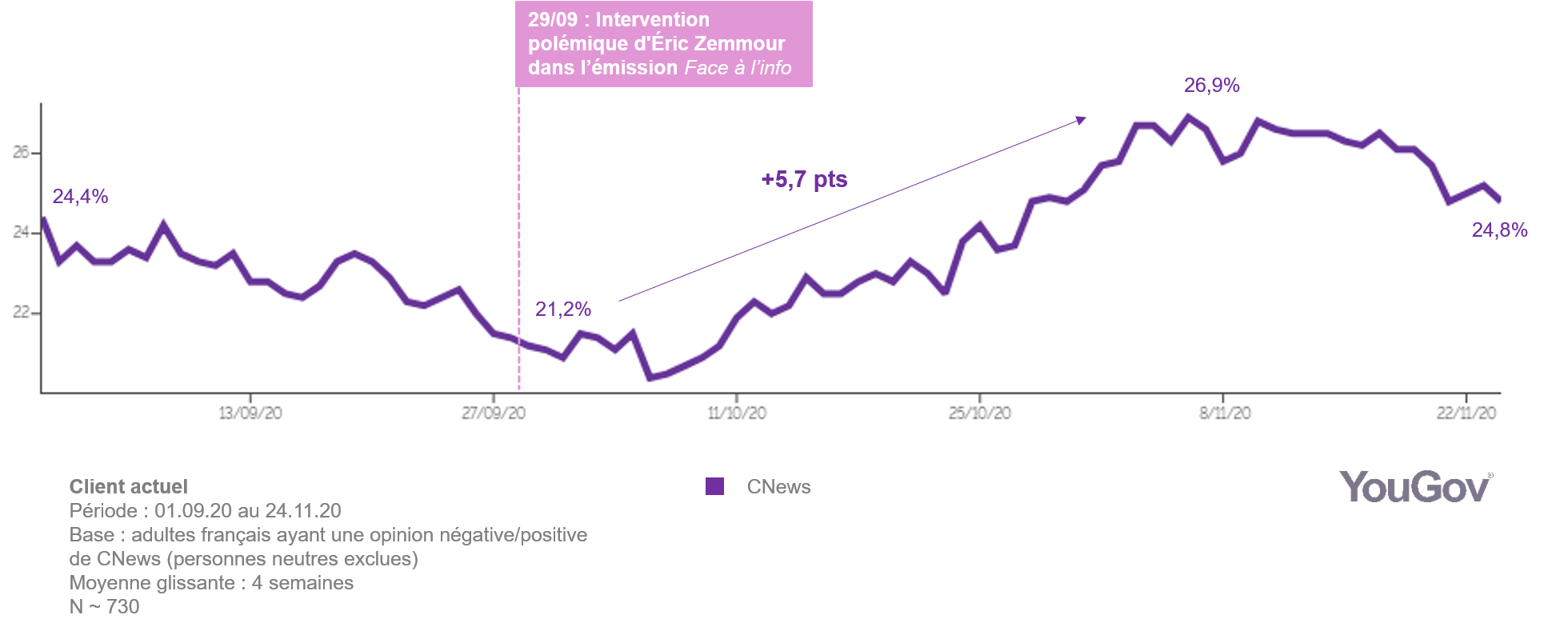

A growing

audience

Another major finding: the number of people watching

the channel increased by 5.7 points between the end of September and the

beginning of November.

Who are the

French who watch CNews?

.png)

November 30, 2020

Source: https://fr.yougov.com/news/2020/11/30/face-la-polemique-quelle-popularite-pour-cnews/

666-43-07/Poll

Fruits preferred by Italians

and sustainability of production

Mandarin, grapes, apple, chestnut and orange are the favorite fruits of

the Italians in this period . Persimmon,

in seventh position by preference, shows a high share of "loyal":

among those who ate it in the last month, almost one in three people selected

it as their favorite fruit in this period

67% of Italians said they had asked themselves at

least once if fruit and vegetables are grown in an eco-sustainable way and in

compliance with workers' rights, but there is still 22% who admit that they

never asked. Residual is the share of those who explicitly declare that

they are not interested in the issue.

The issue of eco-sustainability is more present in the

minds of consumers than that of workers' rights, but those who eat a lot of

fruit show more sensitivity to the latter in particular.

Avocado and

Banana are

the fruits considered less sustainable

in the eyes of Italian consumers . Only 13% of those who

ate Avocado in the last month think that this fruit is grown (often or always)

with respect for the environment and workers when it comes to non-European

crops (19% for local crops).

The avocado is therefore considered the unsustainable

fruit par excellence, followed by the banana, so the gap between the perceived

sustainability of our own and extra-EU is smaller. In third place of the

most critical crops outside the EU, we find grapes, on which, however, Italians

feel reassured to a greater extent within national borders.

In conclusion, considering the attention that fruit

enthusiasts place on ethical issues of production, focusing more on the

sustainability of exotic fruits "of the moment", such as avocado,

could please consumers and represent an opportunity for retailers.

November 27, 2020

Source: https://it.yougov.com/news/2020/11/27/frutti-preferiti-dagli-italiani-e-sostenibilita-de/

666-43-08/Poll

Two thirds of Britons

support cutting the foreign aid budget

In light of the damage caused to the public finances by the coronavirus

crisis, Chancellor Rishi Sunak announced today that foreign aid spending will

be reduced to 0.5% of GDP – a reduction of £5bn.

Such a move is controversial in political circles.

Baroness Sugg, a Foreign Office minister whose brief included overseas

development, resigned in protest at the news, describing it as “fundamentally wrong”. David

Cameron and fellow former Prime Minister Tony Blair have both described the

move as a “strategic mistake”, while former international development secretary

Andrew Mitchell has said the cuts will cause "100,000 preventable deaths,

mainly among children".

One group among whom the cut is not controversial,

however, is the British public. New YouGov research conducted in the run-up to

the announcement shows that two thirds (66%) say that reducing the amount spent

on overseas aid is the right decision. Only 18% think it is the wrong call.

The move is near-universally popular among

Conservative voters, 92% of whom are in support. Support is lower among Labour

and Lib Dem voters, but the move is still more popular than not: Labour voters

back it by 44% to 37% and Lib Dem voters do so by 49% to 35%.

Foreign aid spending levels have long been

consistently unpopular with the British public, topping our tracker on what sector people think the government

spends too much on by a wide margin.

November 25, 2020

666-43-09/Poll

Two in five Britons plan to

shop during Black Friday and Cyber Monday

Black Friday

shoppers overwhelmingly plan to shop online as only essential shops remain open

across Britain

There is unlikely to be any

footage of eager shoppers fighting over discounted TVs on Black Friday this

year. But the national lockdown isn’t putting people off. Two in five people

(40%) plan to bag a discount during the sales period – which is in line with

last year when 39% of

Britons participated.

The four in ten Black Friday shoppers are mostly composed of people who

say they will only shop online (32%). Just 1% expect to exclusively shop

in-store and one in fourteen (7%) say they will do both.

Slightly more than four in ten Britons (44%) say they

won’t do any Black Friday bargain hunting this year, while another one in six

Britons (16%) are undecided.

Younger people are the keenest Black Friday and Cyber

Monday shoppers, with nearly three in five 18- to 24-year-olds (58%) planning

to take part. This includes 11% who will go to a physical store either in

addition to shopping online (7%) or will shop in-store exclusively (4%).

Half of Britons aged 25 to 49 (51%) also expect to buy

discounted items, including one in ten (10%) who will shop online and in-store

(9%) or in-store only (1%).

Older people are less likely to go bargain-hunting,

although even among those aged 65 and over a fifth (21%) plan to take advantage

of Black Friday and Cyber Monday deals.

Social grade also appears to be an indicator of how

likely Britons are to partake in the sales period. People in grade ABC1, which

predominantly includes those in professional occupations, are keener at 45%,

while C2DEs, who often do manual work, are less likely to join in at 36%.

November 25, 2020

666-43-10/Poll

Hopes of vaccine boost

public’s opinion of the pharmaceutical industry

Approaching half

of Britons now have a favourable view of the industry

The latest figures were recorded on 12 Nov – three days after Pfizer and

BioTech announced that their COVID-19 vaccine was 90% effective. The news

appears to have prompted a six-point jump in positive opinion, up from 41% in

mid-October.

The same movement is reflected in the proportion of

people with an unfavourable view of pharmaceuticals dropping from a fifth (19%)

to about one in seven (14%). About three in ten people (31%) have neither

favourable nor unfavourable feelings.

Older people generally have more favourable views of

pharmaceutical companies than the wider population. Among this group three

in five (58%) now see them positively, eight points higher than last

month.

While the vaccine new has provided a boost in public

perceptions, the start of the pandemic prompted the largest leap in positive

opinion, from 32% in February to 51% in April. This remains the highest level

of positivity the industry has received, having receded slowly over the course

of the crisis. But with the roll-out of coronavirus vaccines imminent, the

pharmaceutical industry’s reputation may have further to rise.

November 26, 2020

666-43-11/Poll

Eight in ten say it is

currently difficult to find a job in Britain

Only 9% think it

is currently easy to do so, the lowest number since the coronavirus crisis

began

YouGov’s

tracking data shows a

massive 80% of the public think it is currently difficult for those in the

market to find a job in Britain, including 42% who think it is “very

difficult”. Just 9% say it is currently easy for those looking to find a job.

Unsurprisingly this is a massive shift from before the first UK lockdown. In

February, 44% thought finding a job was difficult while 39% thought it was

easy.

The number thinking the job market is currently

difficult has been on an upward trend over the course of the year, initially

jumping to 57% in April and then to 71% in June. Figures rose only slightly

thereafter, to 78% in July and have remained at about that level ever since.

Similar figures are seen across all age groups –

suggesting a wider understanding of the difficulties those in the job market

are currently facing. Conservatives, however, are slightly more optimistic

about the situation than Labour voters. Amongst Tory voters 14% think it is

currently easy to find a job, compared to 77% who say it is difficult. Just 5%

of Labour voters say it is currently easy, while 89% say it is hard to find

work.

The public are split on what kind of government would

do better getting Britons back to work: 27% of the public believe a Labour

government led by Keir Starmer would be better at providing more jobs, compared

to 25% who believe the same about a Conservative government led by Boris

Johnson.

November 26, 2020

666-43-12/Poll

Leisure-wear, pyjamas and

even showering less, has COVID accelerated a decline in formality?

Six in ten (59%) feel confident about knowing how to dress in a more

casual way, the same proportion say working from home makes it easier to do so.

Just over half of Britons say you rarely see people at work in business suits

these days (54%).

Half of Britons say they are more likely to

have worn clothes such as gym wear, joggers or leggings for everyday wear since

the start of the pandemic with 61% of knowledge workers saying they wear

business wear much less often these days. Just over a third (35%) have spent

more time than usual wearing pyjamas or night clothes during the day. Over 6 in

10 of those who identify as female say they are less likely to wear high heel

shoes now (62%).

Half of Britons say they are more likely to

have worn clothes such as gym wear, joggers or leggings for everyday wear since

the start of the pandemic with 61% of knowledge workers saying they wear

business wear much less often these days. Just over a third (35%) have spent

more time than usual wearing pyjamas or night clothes during the day. Over 6 in

10 of those who identify as female say they are less likely to wear high heel

shoes now (62%).

A quarter are less likely to shower each morning

compared to before the pandemic, luckily for our noses, only 14% are less

likely to use deodorant. A third say they are less likely to style their

hair.

Almost half of those who identify as male have

gone unshaven for more days than before the pandemic started, a third have

grown a beard (32%). Among women, half (52%) are wearing less make-up than

usual. Two in 10 (18%) say the only times they wear make-up are for video calls

with friends.

Almost half of those who identify as male have

gone unshaven for more days than before the pandemic started, a third have

grown a beard (32%). Among women, half (52%) are wearing less make-up than

usual. Two in 10 (18%) say the only times they wear make-up are for video calls

with friends.

Billie Ing, Head

of UK Trends at Ipsos MORI, says:

There has been a trend towards less formality for many years, but this

has been accelerated by the pandemic and people subsequently working from home.

Heels are being ditched, sportswear is on the up and people are embracing

casual work wear. For some, however, it is a tale of two halves – with a

quarter of people dressing smartly on the top, whilst keeping it casual on the

bottom!

November 27, 2020

NORTH AMERICA

666-43-13/Poll

Americans' Holiday Spending

Intentions Strengthen in November

Gallup's latest update of Americans' 2020 holiday

spending plans finds consumers estimating they will spend an average $852 on

Christmas gifts, nearly identical to the $846 they projected at the same time

last year.

Line graph. Annual trend since 1999 in which Americans

estimate each November of the amount they will spend on Christmas gifts,

ranging from a high of $866 in 2007 to a low of $616 in 2008. The November 2020

figure is $852.

The latest gift-buying estimate, based on a Gallup

telephone poll of U.S. adults conducted Nov. 5-19, is higher than the $805

Americans' expected to spend in October and points to stronger holiday sales

than were implied by that preliminary figure.

Holiday sales typically increase year-over-year, with

an average 3.3% annual increase since 2000, according to figures from the

National Retail Federation. Sales increased by more than 5% in strong years

(such as in 2004 and 2005) and by 2% or less in weak years, including negative

sales growth in 2008 and 2009.

Gallup analysis of the historical relationship between

Americans' Christmas spending intentions each November and actual holiday

retail sales suggests that this year's holiday retail sales are likely to rise

by an amount similar to the historical average (in the 3.3% range). By

contrast, the October estimate of $805 in spending on

gifts was indicative of below-average sales (rising by closer to 2%). Gallup has

historically found a stronger correlation between November spending estimates

and actual retail sales, in part due to changes in the economic or political

climate that have occurred between those months in some years.

Range of

Spending Is Also Similar to 2019

The latest spending estimate reflects 32% of Americans

planning to spend $1,000 or more on Christmas gifts, 21% spending between $500

and $999, 29% spending between $100 and $499, and 2% spending less than $100.

These percentages are nearly identical to what Gallup

found in November 2019, further indicating that the economic disruption caused

by the COVID-19 pandemic has not altered Americans' normal holiday spending

patterns.

Americans' Christmas Spending Estimate

Roughly how much money do you think you personally

will spend on Christmas gifts this year?

|

Nov 1-14, 2019 |

Nov 5-19, 2020 |

|

|

% |

% |

|

|

$1,000 or more |

34 |

35 |

|

$500-999 |

21 |

19 |

|

$250-499 |

16 |

13 |

|

$100-249 |

14 |

18 |

|

Under $100 |

2 |

3 |

|

None/Don't celebrate |

8 |

9 |

|

Not sure |

4 |

4 |

|

Average, including zero |

$846 |

$852 |

|

Average, excluding zero |

$927 |

$940 |

|

GALLUP |

||

Although spending intentions vary by household income, the figures at

each income level are also essentially unchanged from 2019. Currently, those living in households

earning $100,000 or more per year plan to spend an average of $1,291 on

Christmas gifts. This drops to $888 among those earning between $40,000 and

$99,999, and to $516 among those earning less than $40,000.

Estimated Christmas spending is also higher among

households with children younger than 18 living at home ($1,103) than in

households without children ($749).

Americans Are

Modestly Cautious in Describing Their Spending Plans

Separately, the poll asks Americans to say whether the

amount they plan to spend on Christmas gifts is more, the same as, or less than

what they spent the year prior.

As is almost always the case, the largest segment of

Americans, 57%, say they will spend about the same on gifts while a larger

proportion say they will spend less (28%) rather than more (15%).

Line graph. Annual trend since 1999 in Americans'

report each November of whether the amount they plan to spend on Christmas

gifts is more, about the same, or less than what they spent the year prior. In

all years except 2008, the majority have said they will spend the same amount.

The percentage saying they will spend less has varied from a high of 46% in

2008 to a low of 18% in 2000. The November 2020 figure is 28%.

Each November since 2002, the public has tilted toward

saying they will spend less money rather than more, with the gap between those

figures ranging from six points in 2016, 2017 and 2018 to 39 points in 2008.

Holiday sales tended to be below average in years when the advantage for less

spending was high, while spending was relatively strong in low-gap years.

This year's 13-point difference matches the mean

historical gap in spending expectations, providing further evidence that

holiday retail sales will be about average in 2020.

Bottom Line

Americans' latest estimate of their spending on gifts

this holiday season offers retailers some hope of normalcy at the end of a year

that has been anything but normal. Of course, how and where Americans spend may

differ from prior years amidst an accelerating surge in COVID-19 cases

nationwide, with some types of retailers benefiting more than others.

There is also no guarantee that consumers' spending

intentions will be sustained over the next month when holiday shopping

typically kicks into high gear. How much Christmas shoppers follow through on

their November spending mood could depend on the extent to which the present

surge in COVID-19 cases compels renewed lockdowns that crimp household income and

in-person retail shopping. Smaller family gatherings and fewer holiday parties

could also mean less impetus to expand gift-giving beyond one's immediate

household.

On the other hand, recent research by Franklin Templeton and

Gallup suggests

that should Congress pass a second stimulus bill before Christmas that includes

direct checks to families -- a long-shot at this late date -- retailers could

potentially see a slight boost in spending beyond what is predicted today.

(Gallup USA)

November 25, 2020

Source: https://news.gallup.com/poll/326654/americans-holiday-spending-intentions-strengthen-november.aspx

666-43-14/Poll

Biden's Favorability Rises

to 55%, Trump's Dips to 42%

President-elect Joe Biden's favorability rating has

risen six percentage points to 55% since the election compared with his final

preelection reading. At the same time, President Donald Trump's favorability

has edged down three points to 42%.

Biden's current rating is the highest it has been since February 2019, two months before he declared his candidacy

for president, when it was 56%. Trump's latest favorability falls short of the

highest of his presidency, 49% in April, during the initial stages of the

coronavirus pandemic.

Line graph. Favorable ratings of Donald Trump and Joe

Biden since January 2019. The latest readings, from November 2020, are 55% for

Biden and 42% for Trump.

These findings are from a postelection survey

conducted Nov. 5-19, a period during which Trump's legal team was challenging

the results in a number of states. The increase in Biden's favorability between

Gallup's final preelection and first postelection readings is driven by

independents and Republicans, whose positive ratings of Biden grew from 48% to

55% and 6% to 12%, respectively. Democrats' nearly unanimous positive ratings

remained constant.

Trump's slightly lower postelection favorable rating

is owed more to Republicans than independents or Democrats. Republicans' rating

of the president fell six points to 89%, while it was essentially unchanged

among independents and static among Democrats.

Partisans' Favorable Ratings of Donald Trump and Joe

Biden

% of Americans with a favorable opinion

|

Oct 16-27 |

Nov 5-19 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

% |

% |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Joe Biden |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Republicans |

6 |

12 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Independents |

48 |

55 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Democrats |

95 |

96 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Donald Trump |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Republicans |

95 |

89 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Independents |

38 |

36 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Democrats |

3 |

3 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GALLUP, 2020 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Historical Comparisons of Candidate Favorability Pre- and Postelection

Since 2000, the winning presidential candidate's

favorability ratings have increased slightly after the election. In 2000, when

George W. Bush was not declared the winner until several weeks after Election

Day, neither he nor Al Gore enjoyed an initial postelection bump. Yet, after

the Supreme Court's Dec. 12 decision in Bush v. Gore determined Bush had won

reelection, his favorability rose four points.

Additionally, since 2000, the winner's postelection

favorability reached the majority level in every election except 2016, when

Trump was the most personally unpopular presidential

candidate in Gallup polling history. Biden's six-point increase in favorability this year is in line with

those for other presidents and presidents-elect.

The pattern for losing presidential candidates is

mixed. Some, including John McCain in 2008 and Mitt Romney in 2012, had

significantly higher favorable ratings after the election. (McCain's showed the

greatest increase: 14 points.) Hillary Clinton's favorability was unchanged

after the 2016 election, and there is no reading for John Kerry until July

2005, by which time his favorability had fallen 10 points. Trump's three-point

postelection decline is unique over the past six presidential election cycles.

Pre- and Postelection Favorable Readings of

Presidential Candidates, 2000-2020

% of Americans with a favorable opinion

|

Final preelection reading |

Postelection reading (Nov/Dec) |

Change |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

% |

% |

pct. pts. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

2020 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Joe Biden |

49 |

55 |

+6 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Donald Trump |

45 |

42 |

-3 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

2016 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Donald Trump |

34 |

42 |

+8 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Hillary Clinton |

43 |

43 |

0 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

2012 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Barack Obama |

55 |

58 |

+3 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Mitt Romney |

46 |

50 |

+4 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

2008 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Barack Obama |

62 |

68 |

+6 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

John McCain |

50 |

64 |

+14 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

2004 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

George W. Bush |

51 |

60 |

+9 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

John Kerry |

52 |

NA |

NA |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

2000* |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

George W. Bush |

55 |

59 |

+4 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Al Gore |

56 |

57 |

+1 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

* Data for 2000 are among registered voters |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GALLUP |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Favorable Ratings of Parties Are Similar

Although Americans' views of the Republican and

Democratic Parties are not appreciably different from readings over the past

several months, the slight edge that the Democratic Party enjoyed

over the Republican Party in September has narrowed. The 45% of U.S. adults who view the Democratic Party

favorably is not significantly different from the 43% who have the same view of

the Republican Party.

The highest recent reading for the Republican Party

was 51% in January amid Trump's impeachment trial. The

Democratic Party has not reached that level since November 2012, after Barack

Obama won a second term.

Line graph. Favorable ratings of the Democratic and

Republican Parties since 2012. The latest readings, from November 2020, are 45%

for the Democratic Party and 43% for the Republican Party.

While roughly nine in 10 Democrats and Republicans

alike hold favorable opinions of their own parties, independents view the

Democratic Party more positively than the Republican Party, 41% vs. 33%.

Partisans' Favorability Ratings of the Democratic and

Republican Parties

% of Americans with a favorable opinion

|

Democratic Party |

Republican Party |

|

|

% |

% |

|

|

Republicans |

5 |

90 |

|

Independents |

41 |

33 |

|

Democrats |

92 |

9 |

|

GALLUP, NOV. 5-19, 2020 |

||

(Gallup USA)

November 30, 2020

Source: https://news.gallup.com/poll/326885/biden-favorability-rises-trump-dips.aspx

666-43-15/Poll

Prior to COVID-19, child

poverty rates had reached record lows in U.S.

Before the coronavirus outbreak sent the U.S. economy into a recession, the share of American children living in poverty was on a downward

trajectory, reaching record lows across racial and ethnic groups, according to

a new Pew Research Center analysis of U.S. Census Bureau data.

In 2019, the year with the most recently available

data, 14% of children under age 18, or 10.5 million children, were living in

poverty, down from 22%, or 16.3 million, in 2010. All major racial and ethnic

groups saw declines since 2010, but the greatest decreases were in the shares

of Black and Hispanic children living in poverty. About two-in-ten Hispanic

children (21%) were living in poverty in 2019, down from 35% in 2010. In 2019,

26% of Black children were impoverished, dropping from 39% in 2010. Even so,

Black and Hispanic children were still about three times as likely as Asian

(7%) and White (8%) children to be living in poverty.

The number of impoverished children also declined across racial and ethnic groups. In particular, the numbers of poor Black and White children reached new lows in 2019 (each around 3 million). While there are about as many White children as Black children living in poverty, it’s worth noting that there are more than three times as many White children as Black children in the U.S.

The greatest decline was in the number of Hispanic

children living in poverty. In 2019, 3.9 million Hispanic children were living

in poverty, down from 6.1 million impoverished Hispanic children nearly a

decade earlier. But there are still more Hispanic children in poverty than any

other racial or ethnic group, which has been the case since at least 2007. This is probably because Hispanics are the largest and the youngest racial or ethnic minority population in the U.S. and because the

Hispanic child poverty rate is relatively high (21%).

Overall, children are overrepresented among America’s

impoverished population. Some 22% of the U.S. population are children, but

those younger than 18 represent 31% of all Americans living in poverty.

Black and Hispanic children are particularly

overrepresented. Black children represent a quarter of the Black population but

35% of all Black people living in poverty. And Hispanic children are 31% of the

total Hispanic population but represent 41% of all impoverished Hispanics. In

comparison, children represent about equal shares of total Asian and White

populations and of impoverished Asians and Whites.

(PEW)

November 29, 2020

666-43-16/Poll

In the pandemic, the share

of unpartnered moms at work fell more sharply than among other parents

Balancing work and family obligations is a challenge for many parents, but remote learning and the closure of many child care

centers have put added stress on them in the COVID-19 pandemic, especially on parents without the support of

a partner at home.

While previous research on the labor market shows that

the pandemic has similarly affected mothers and fathers overall from September 2019 to September 2020, a

new Pew Research Center analysis finds that the share of unpartnered mothers

who are employed and at work has fallen more precipitously than among other

parents.

In September 2020, six months since the onset of the

COVID-19 outbreak, 67.4% of unpartnered mothers with children younger than 18

at home were working – employed and on the job – compared with 76.1% in

September 2019. This 9 percentage point drop is the largest among all groups of

parents, partnered or not. Unpartnered fathers experienced a less severe

decrease (4 points), about the same as the drop seen by partnered mothers and

fathers (about 5 points each).

How we did this

Terminology

Black and Hispanic unpartnered mothers each experienced

about a 10-point decline in the share employed and at work from September 2019

to September 2020. This was nearly double the decrease in the share of White

unpartnered mothers who are working (about 6 points). The decreases in the

shares of Black and Hispanic unpartnered mothers at work are also nearly double

what their partnered counterparts experienced in this yearlong period.

The decline in the share of unpartnered mothers

employed and at work is particularly pronounced among those whose youngest

child is 5 years old or younger. In September 2020, 58.5% of unpartnered moms

in this group were employed, down from 69.7% a year earlier. Unpartnered

mothers whose youngest child is 6 to 17 years old also saw a drop, but not as

steep – from 79.6% in September 2019 to 71.9% in September 2020. In this same

time frame, there was about a 4-point drop among partnered moms whose youngest

child is 5 years old or younger (from 60.5% to 56.9%) and a roughly 6-point

drop for those whose youngest child is 6 to 17 years old (from 72.7% to 67.0%).

Regardless of relationship status, mothers are generally more likely to be

employed and at work if they have older children.

Unpartnered mothers with young children at home also

saw more of a decrease in labor force participation — that is, the percentage

of the population 16 or older actively working or looking for work — from

September 2019 to September 2020 than did other mothers. The labor force

participation rates declined about 7 percentage points for unpartnered mothers

whose youngest child is 5 years old or younger, compared with a 3-point drop

for those whose youngest child is 6 to 17 years old. The labor force

participation rate for partnered mothers edged down by 1 point for those whose

youngest child is 5 years old or younger and dropped about 3 points for those

whose youngest child is 6 to 17 years old.

The disproportionate impact of pandemic-related job

loss on unpartnered mothers reflects, at least in part, the demographic

characteristics of this group. Black women made up 31.4% of unpartnered mothers

in September 2020, compared with only 12.2% of all mothers older than 16. When

it comes to education, 26.9% of unpartnered mothers had at least a bachelor’s

degree, compared with 43.3% of all mothers 16 and older. As previous research shows, the pandemic recession has hit

certain groups, such as Black and Hispanic women and those with less education,

particularly hard.

Overall, women are more likely to be unpartnered

parents than men. In September 2020, 19.7% of mothers living with children

younger than 18 at home had no partner present, a much higher share than among

fathers (4.7%). Unpartnered mothers are more likely than unpartnered fathers to

live with young children. Some 33.6% of unpartnered mothers live with children

younger than 6, compared with 25.9% of unpartnered fathers.

(PEW)

November 24, 2020

AUSTRALIA

666-43-17/Poll

Movement in Melbourne CBD at only 27% of normal after lockdown ends, well behind Sydney CBD (42%)

A special

analysis of movement data in Australia’s Capital City CBDs during 2020 shows

movement levels remain well below those seen earlier in the year in all six

State capitals.

Movement in the Melbourne CBD during mid-November was

at an average of only 27% of the pre-COVID-19 levels earlier in the year during

January and February – although this has almost doubled since being at only 14%

during the final week of lockdown in late October.

Comparing movement levels during 2020 shows that

movement levels in the Melbourne CBD have been lower than all other Capital

City CBDs every week since late March when the first national lockdown began

and hit a low of only 11% of normal in the final week of August.

Movement levels in the Sydney CBD have tended to track

lower than smaller cities since the ‘second wave’ began in early July and have

not been above 50% of normal since hitting 51% in mid-August. At the time there

were significant fears in Sydney that the city would soon follow the path

trodden by Melbourne in the preceding weeks and also enter a second lockdown.

The Adelaide CBD and Perth CBD have been the standouts

for most of 2020 with movement levels consistently between 70-80% of the

pre-COVID-19 levels including a high of 86% of normal in the Adelaide CBD in

early August.

However, Adelaide’s good run came to an abrupt end

last week with the three-day shutdown causing the city’s weekly movement

average to tumble to only 38% of normal in the week to November 23 and drop

from first place (at 75%) before the shut-down to now be above only Melbourne.

Australian

Capital City CBDs average 7-day movement levels March – November 2020:

% Movement is compared to the 7-day average in Jan-Feb 2020

Source: Roy Morgan collaboration with

UberMedia who provide anonymous aggregated insights using mobile location data. Note: Movement data for the Capital

City CBDs excludes the residents of the respective CBDs.

Source: Roy Morgan collaboration with

UberMedia who provide anonymous aggregated insights using mobile location data. Note: Movement data for the Capital

City CBDs excludes the residents of the respective CBDs.

Roy Morgan has partnered with leading technology

innovator UberMedia to aggregate data from tens of thousands of mobile devices

to assess the movements of Australians as we deal with the restrictions imposed

in response to the COVID-19 pandemic.

The interactive dashboard available on the website

tracks the movement data for those visiting the Capital City CBDs during 2020,

excluding the CBD residents of each city. Movement data from several key

locations around Australia is also available to view by using the interactive

dashboard.

Michele Levine,

CEO of Roy Morgan, says closely analysing the movement data in Australian

cities during 2020 shows the large impact measures taken to combat COVID-19

have had around with Melbourne an outlier as the hardest hit:

“Melburnians

finally emerged from a near four-month lockdown in the last week of October but

analysing movement data during the month of November shows there’s still a long

way for the southern capital to go to catch up to interstate rivals when it

comes to returning people to the Central Business District.

“In the week

to November 23 the average movement data in the Melbourne CBD was at only 27%

of the average level during January-February 2020 pre COVID-19 and the

associated lockdowns. This is nearly double the movement in the final week of

lockdown to October 27 (14%) but still well below all other Capital City CBDs.

“The

long-running trends show movement in the Melbourne CBD plunged further and

harder than any other CBD in late March and has tracked lower than other cities

ever since.

“Sydney CBD

has consistently been the second lowest and particularly since early July when

the ‘second wave’ of COVID-19 threatened to lockdown the ‘Harbour City’.

However, extensive contact tracing and testing eventually suppressed the

outbreak although the average movement in the Sydney CBD has not been above 50%

since mid-August more than three months ago.

“The big mover

(in the wrong direction) over the past week has been the Adelaide CBD for which

average movement data has plunged to only 38% of normal after the city

experienced a short-lived 3 days of lockdown last week. For the three days of

lockdown (November 19-21) average movement in the Adelaide CBD was at only 16%

of the pre COVID-19 level.

“The

underlying take-out from comparing the movement data of the Capital City CBDs

of all six States is that so-called ‘COVID-Normal’ is still significantly

different to pre COVID-19 with movement levels well below pre-pandemic

averages.

“The key

reasons movement levels remain significantly lower are the millions of city

office workers that are still working from home around the country and the

closure of domestic and international borders. The closed borders prevent

interstate or overseas tourists from visiting the Capital Cities and also mean

many international students that tend to congregate near the CBDs have been

blocked from re-entering Australia over the past few months.

“As long as

international borders remain closed there will clearly be only a trickle of

international tourists, and students, allowed into Australia from countries

such as New Zealand. Because of this it is vital that to revitalise and

reinvigorate the CBDs of Australia’s great cities that office workers are

encouraged to return to the office as soon as it is safe to do so.”

(Roy Morgan)

November 27, 2020

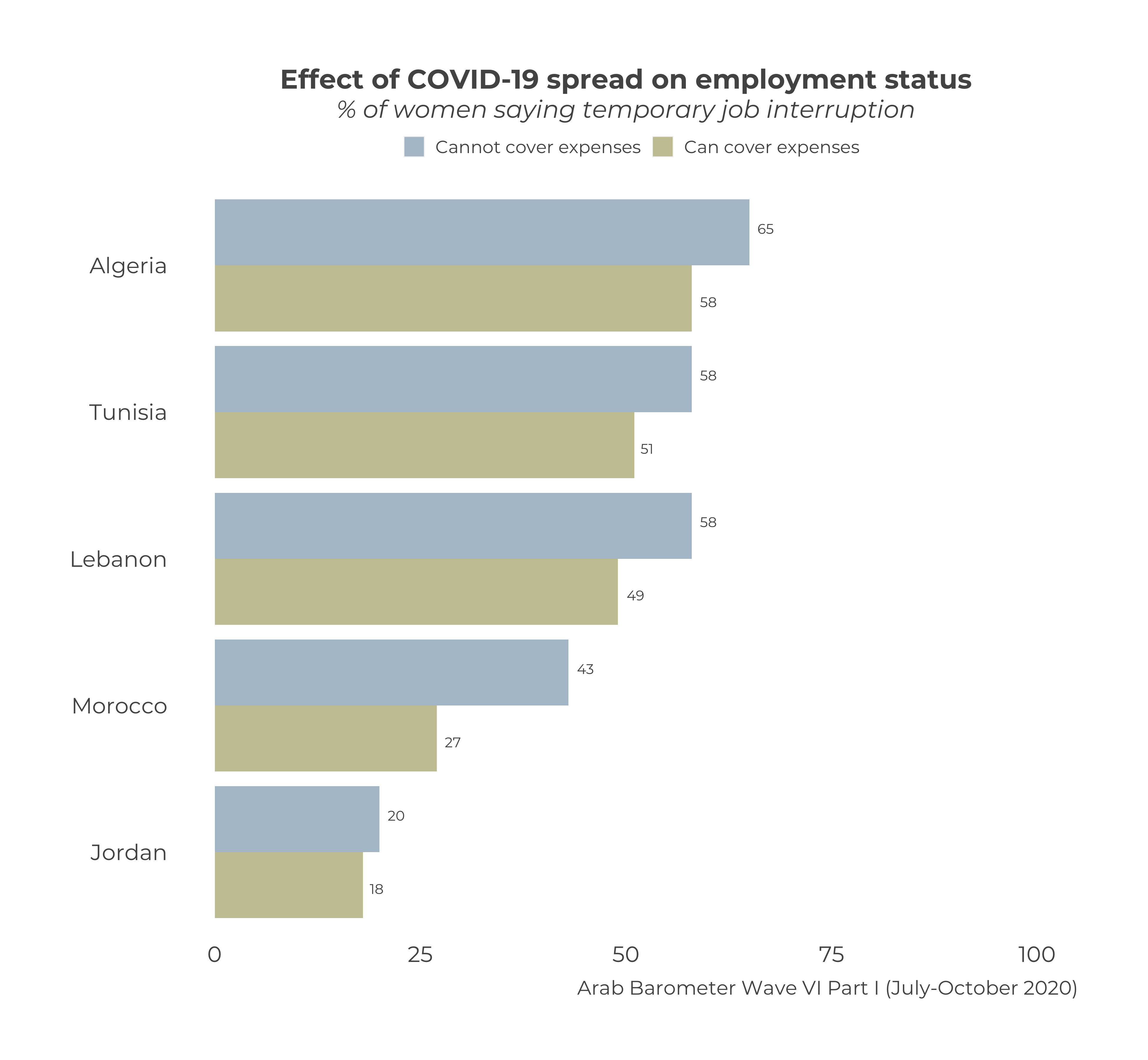

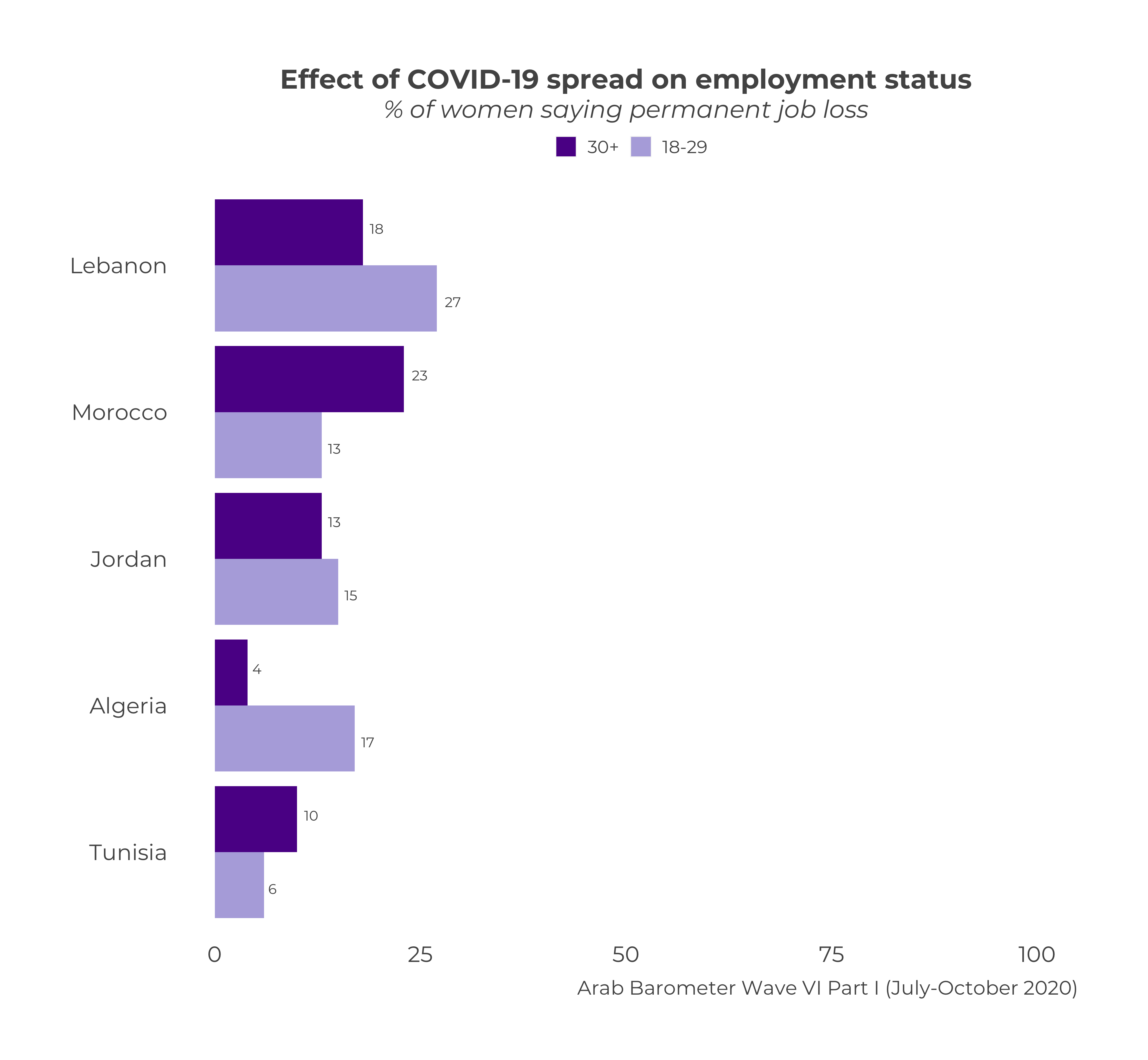

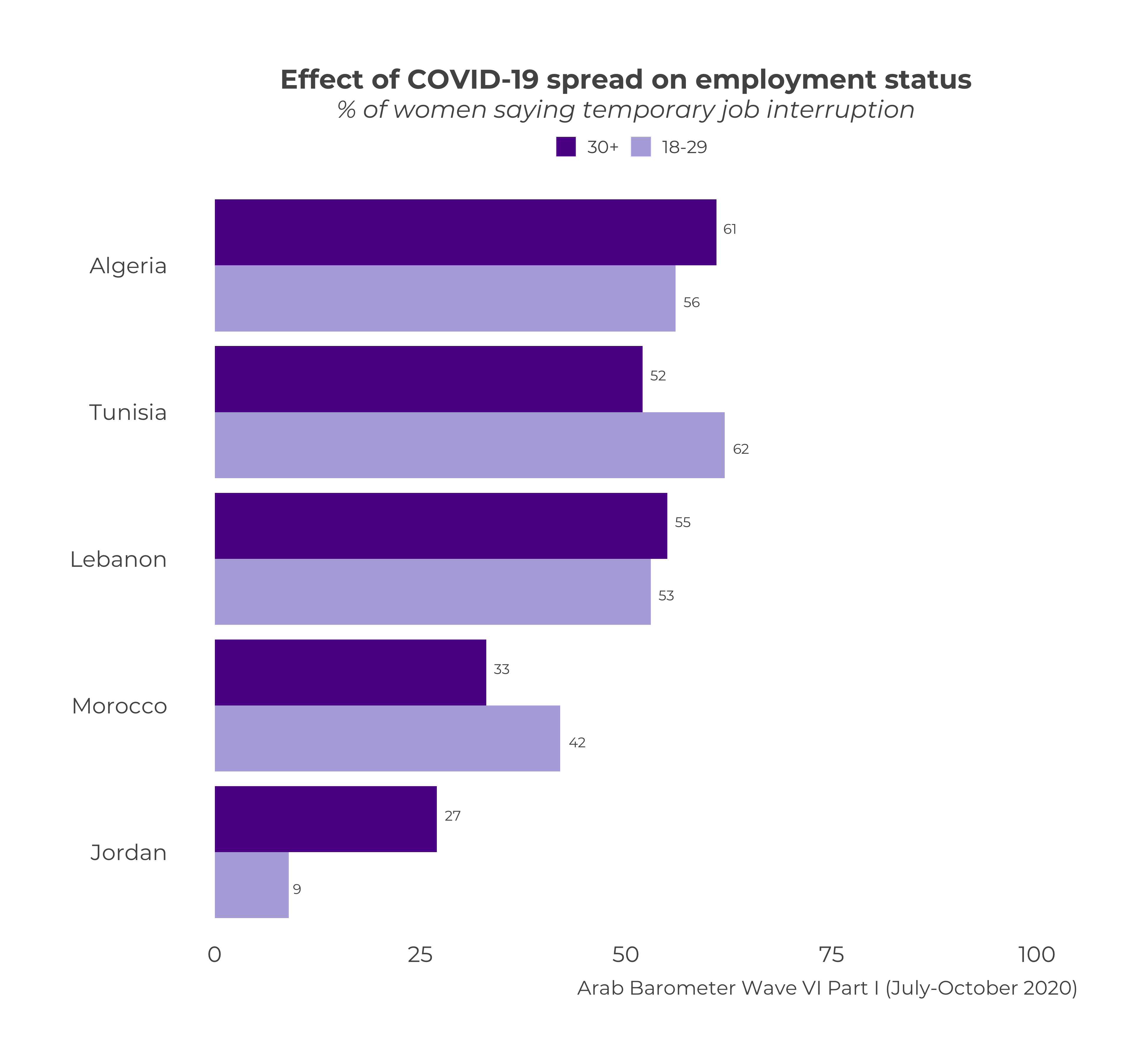

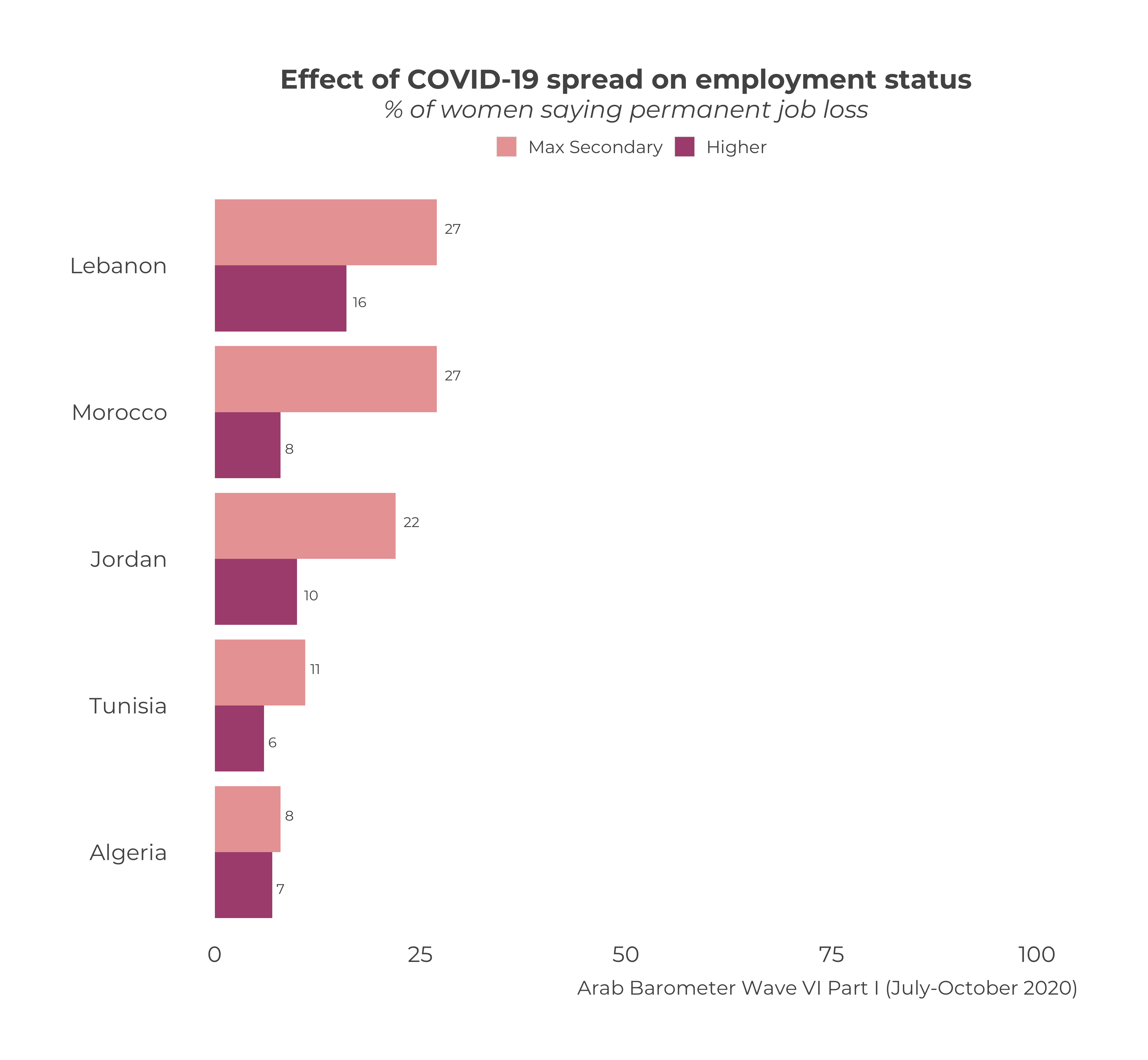

MULTICOUNTRY STUDIES

666-43-18/Poll

COVID-19 Magnifies

Pre-Existing Gender Inequalities in MENA

COVID 19 is being perceived as a disruptor, an

accelerator and an agent for innovation and advancement in

various fields across the world. Yet, its impact has been a decelerator for women’s rights and gender

equality globally. The UN Deputy Secretary-General Amina

Mohammed warned that without immediate action, “the pandemic could set

back women’s rights by decades”.

And, the latest Arab Barometer public opinion survey of citizens across

five countries in the Arab world confirm that Arab women have suffered

more on economic and social dimensions. As such, responses and recovery

plans should prioritize the support and protection of women in MENA.

Otherwise, COVID’s impact could “unravel the limited progress that we have seen

in terms of gender equality, women’s participation in the workforce and

positive attitudes towards some women’s rights and their roles in society in

the Arab world.”

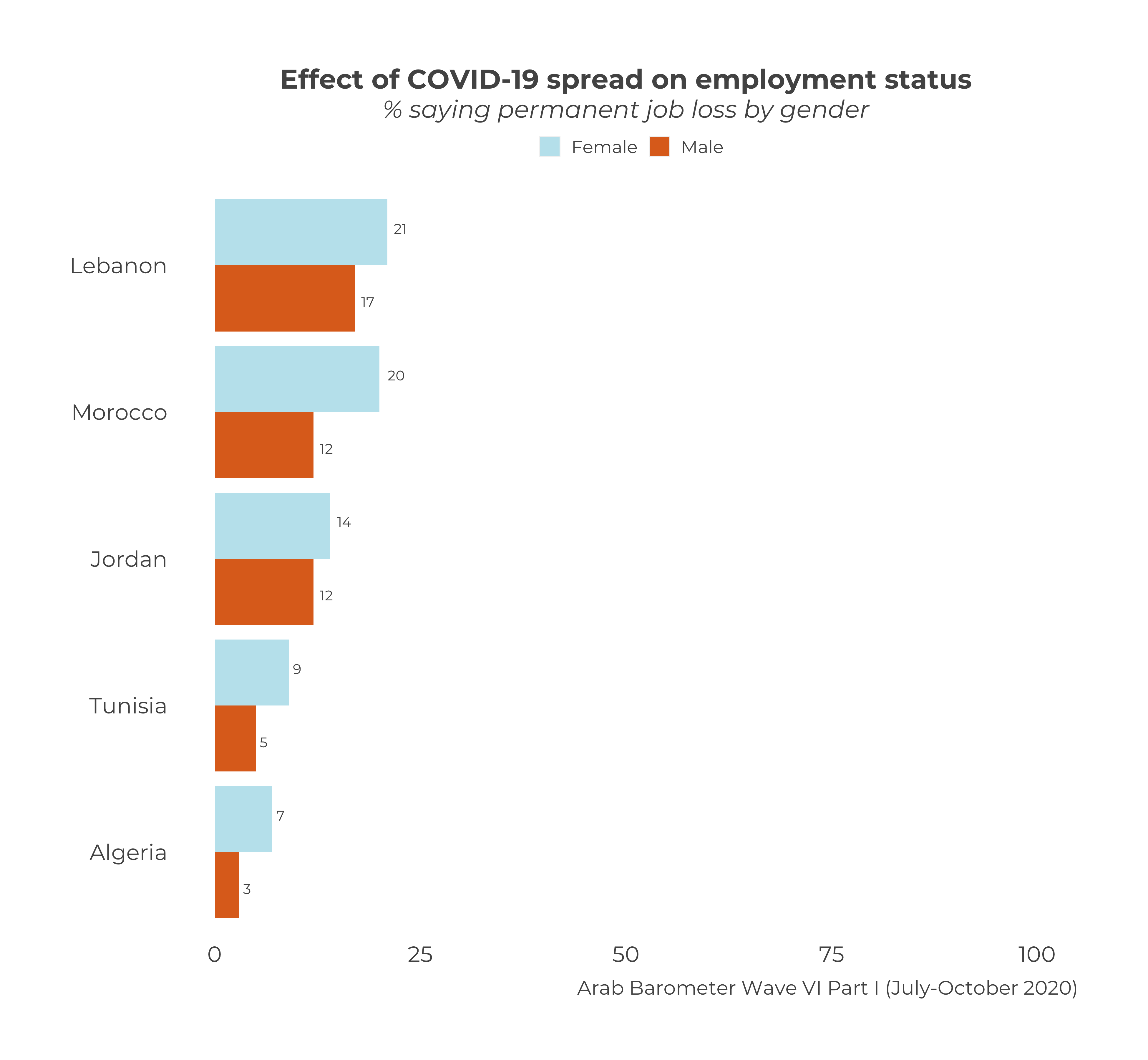

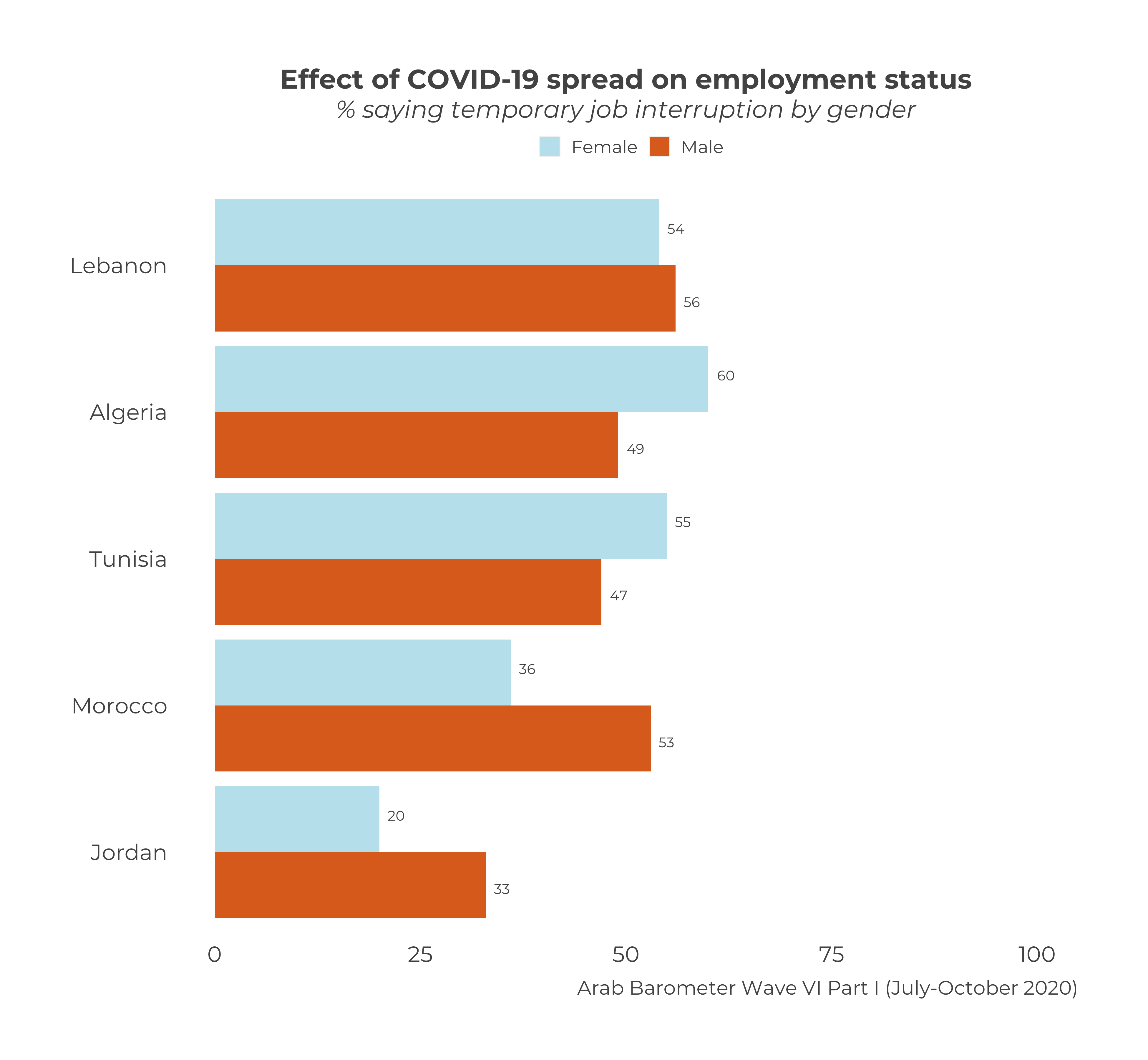

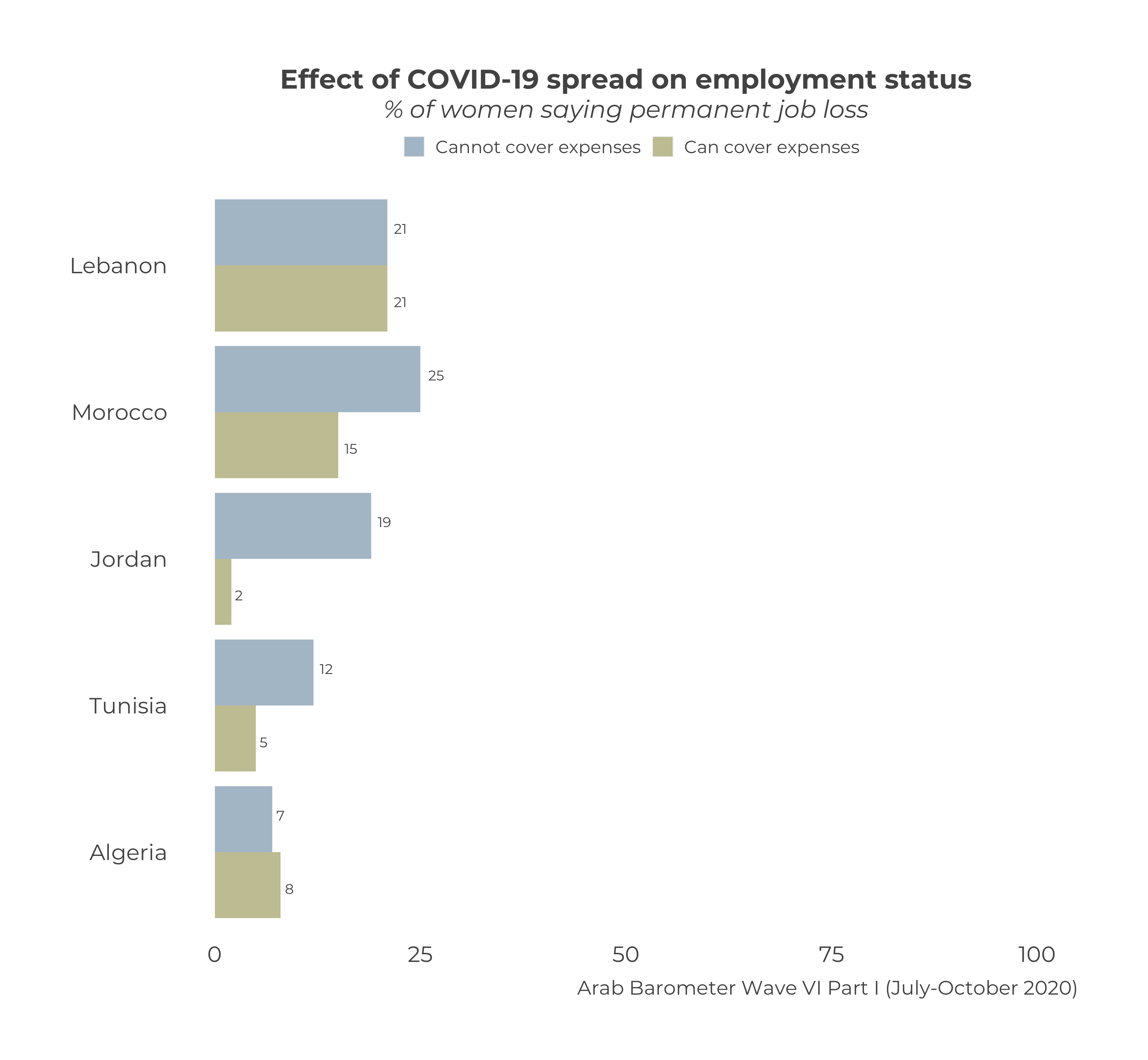

COVID-19’s

Economic Toll on Women in MENA

Prior to the COVID-19 pandemic, women’s labor force

participation was disproportionately less (21%) than that of men in the Arab world

(70%). Then, the

pandemic’s economic impact further threatened Arab women’s livelihood and

income security. Although Arab Barometer’s survey results show that,

overall, relatively few citizens in the countries surveyed have lost a job

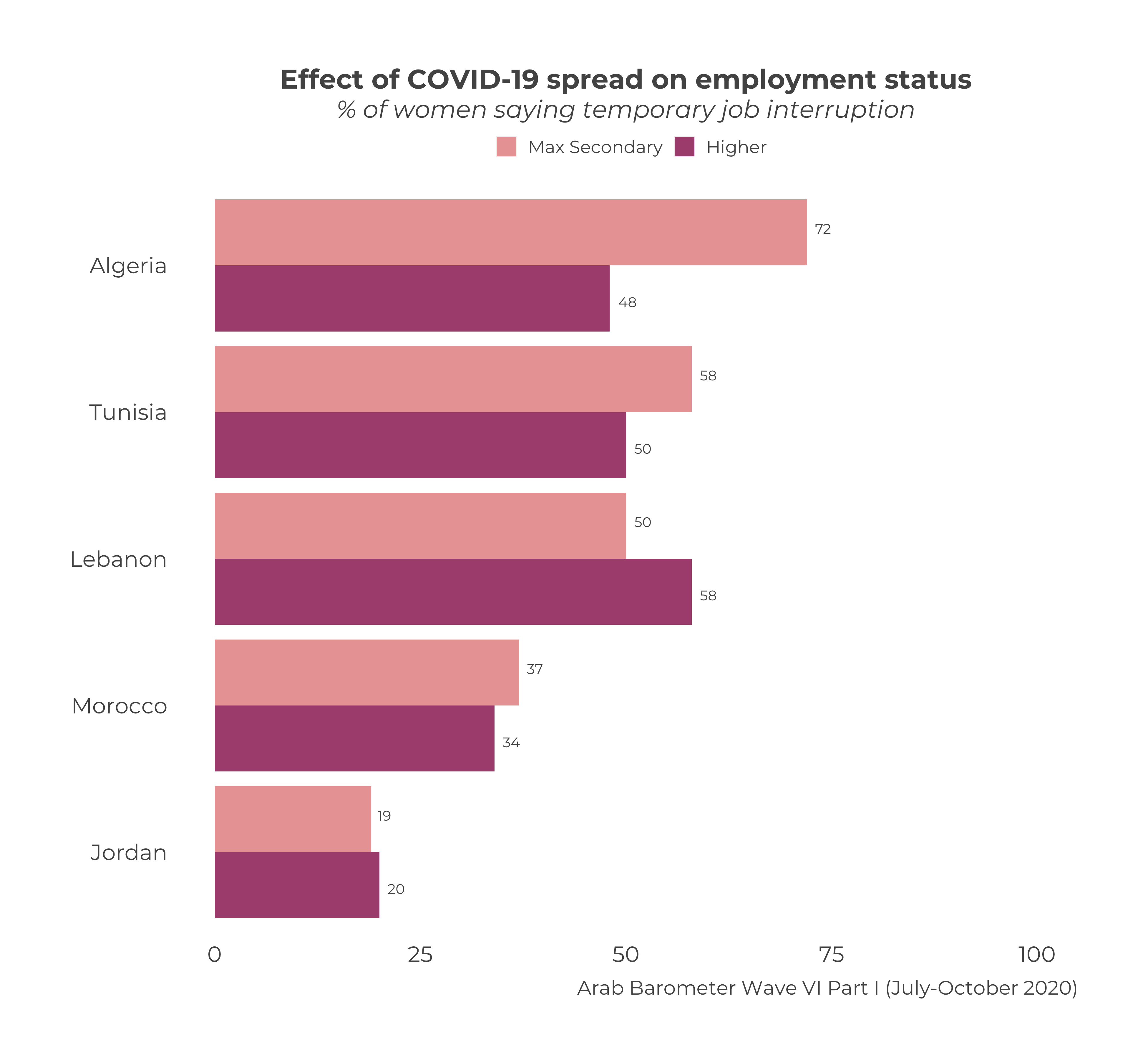

due to COVID-19, many more have suffered a temporary interruption. Yet, in both

cases, women bear a disproportional share of the job cuts: in Morocco the

difference between women and men who permanently lost their jobs is eight

percentage points while in Algeria and Tunisia it is four points. Similarly,

women are more likely to have temporarily lost their jobs in Algeria (11-point

difference compared to men) as well as Tunisia (8-point difference).

A closer look at the numbers reveal even deeper

disparities. The COVID-19 economic downturn might have hit Arab women

harder than men, but it is felt even harder by poorer women. Disparities based

on age and level of education are also noticeable among women’s permanent and

temporary disruption of work, although the magnitude varies across countries

surveyed.

The Pandemic’s

Impact on Arab Women’s Social Lives

COVID’s toll on Arab women isn’t only economic; the

pandemic has dramatically affected the social lives of Arab women as well. The

COVID-related health scare, the imposed lockdown, school closures, and the

increased demands of the family and home, which are predominantly women’s

responsibilities in MENA, have taken a heavy toll on Arab women. In four

of the five countries surveyed, roughly a third of citizens say their biggest

concern about COVID is the death of a family member, and citizens not following

recommendations, according to Arab Barometer wave 6. Lebanon is the only

exception where two-thirds worry about the death of a family member compared

with only 5 percent who say citizens not following recommendations. However,

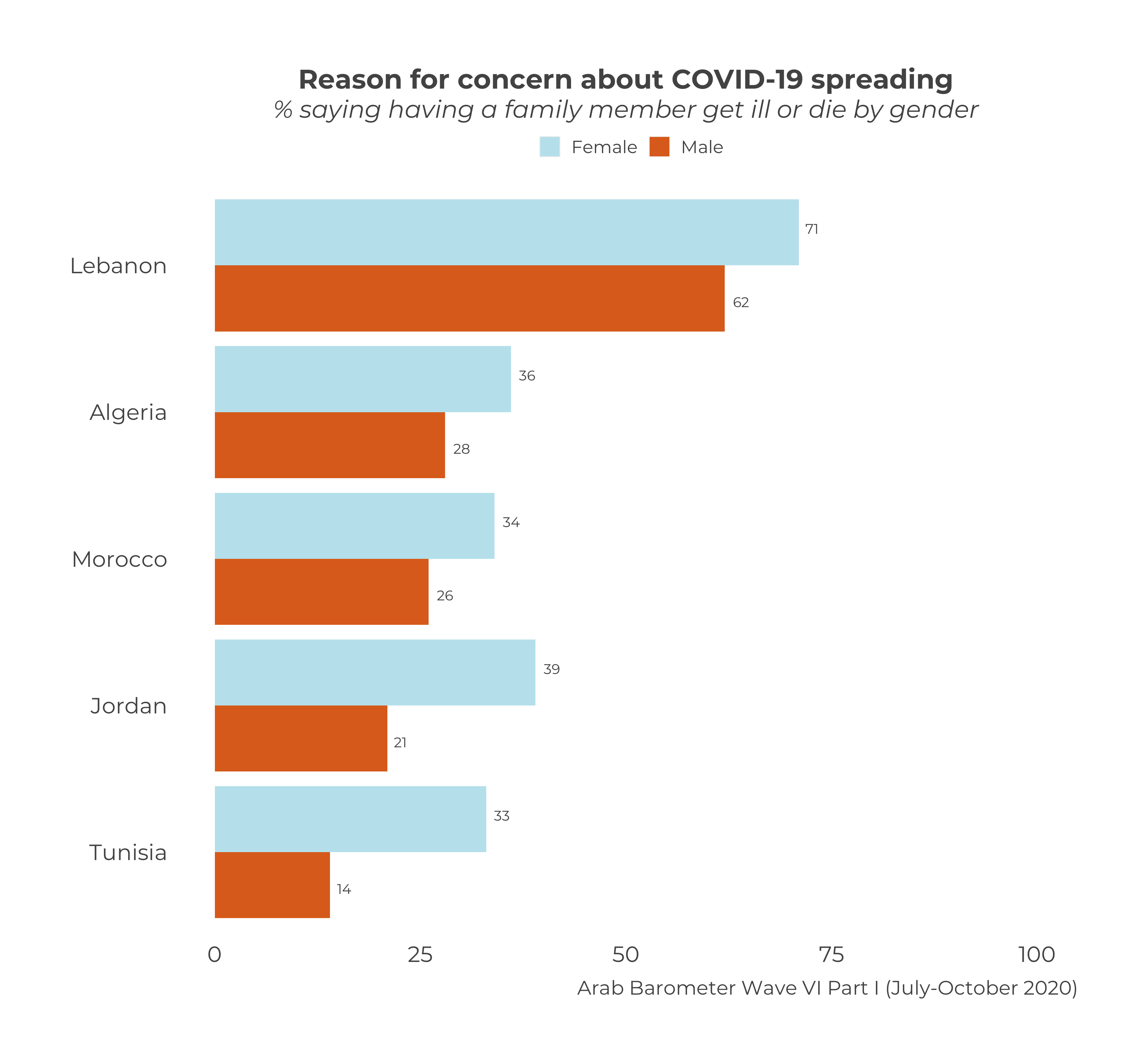

women are experiencing a higher level of health anxiety and stress about family

member’s health compared to men. In all five countries surveyed, more women

than men say they are worried about illness or death of a family member, with

the greatest percentage difference in Tunisia (19 points) and Jordan (18

points), while the difference in Lebanon is 9 points and in Algeria and Morocco

it is 8 points, respectively.

The Pandemic’s

outsized effect on Arab Women’s Safety

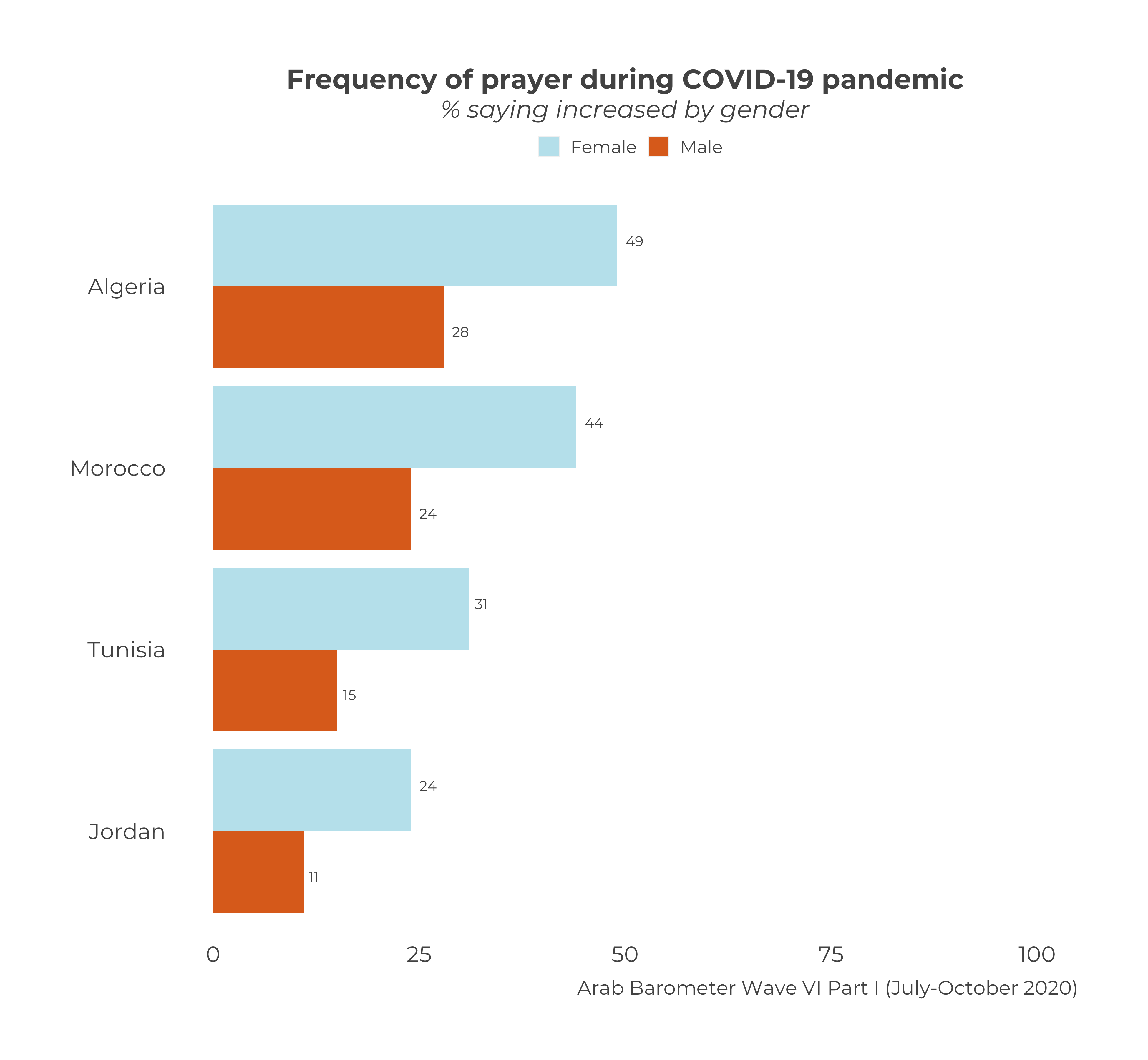

Moreover, the pandemic has had an outsized effect on

Arab women’s safety and general wellbeing. The recent UNESCWA report alerts of the dramatic

increase in levels of gender-based violence in the Arab world amid the Covid-19

crisis. For those

Arab women trapped in violent relationships, the crisis has forced many to stay

at home with their abuser making the likelihood of violent incidents more

frequent. Arab Barometer’s results further reinforce this reality. The results

reveal that citizens perceive that violence against women in their community

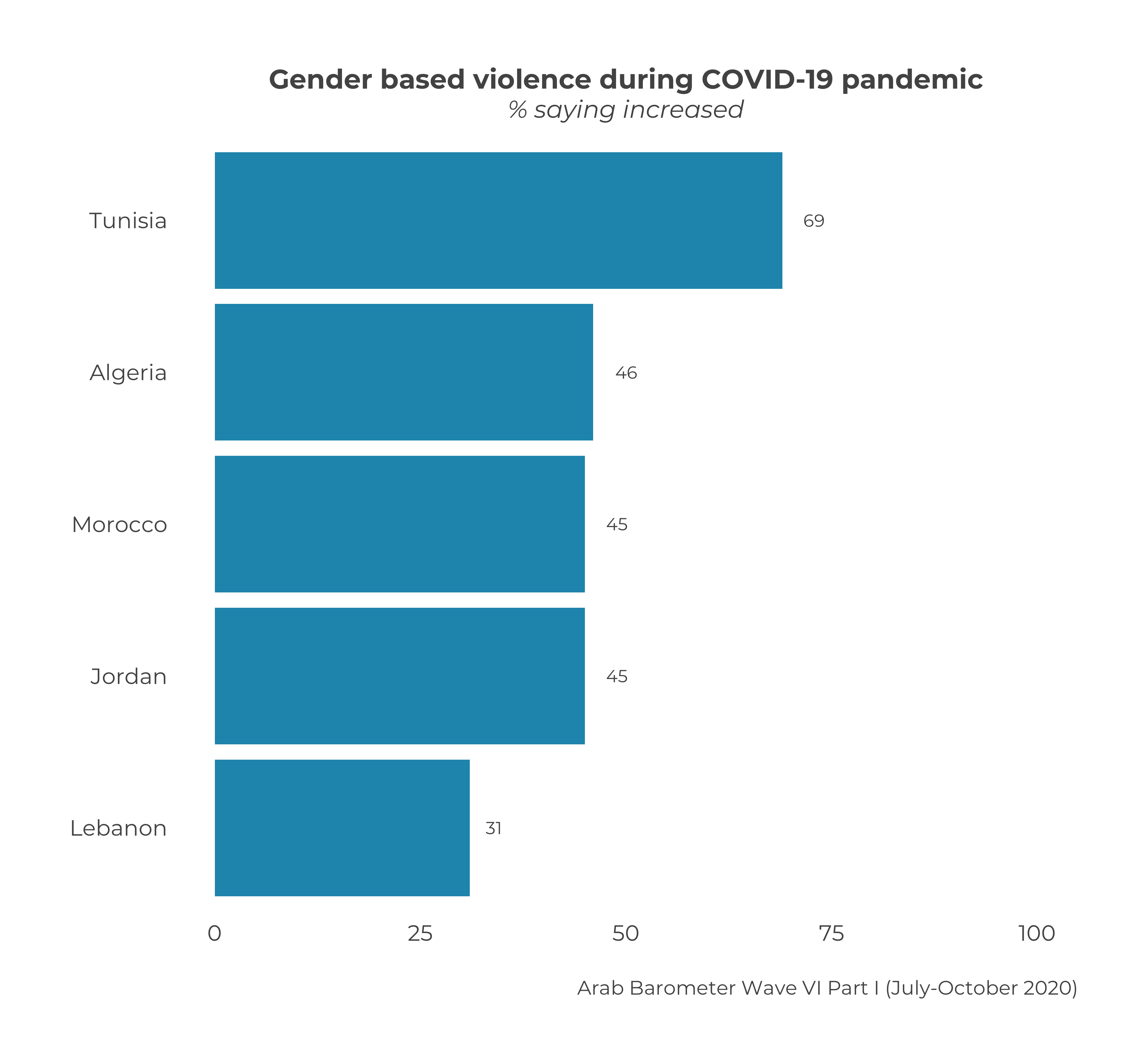

has increased since the outbreak of the coronavirus. The highest rate of

perceived increase in abuse of or violence against women is in Tunisia (63%),

followed by Algeria and Morocco (41%, respectively), while the perceived

increase of gender-based violence in Jordan is 27%, and in Lebanon is

20%.

In fact, as I mentioned in my previous blog on domestic violence during COVID-19 in

MENA, women at risk in

the Arab world who are seeking safety and security during the prolonged quarantine

are presented with false choices. This is primarily a result of the Arab

governments’ failure in prioritizing the support and protection of women in

their recovery-response plans. However, the situation is even more alarming for

women victims who have recently lost their jobs and are already living in or

dangerously close to poverty line, as they become even more dependent on their

abuser for financial security and shelter.

Arab Women

Seeking Refuge in Prayer

During this time of uncertainty, it appears that